American Airlines Group Inc.: Financial Analysis & Performance Report

VerifiedAdded on 2023/06/14

|20

|5988

|479

Report

AI Summary

This report offers a detailed financial analysis of American Airlines Group Inc., utilizing various financial analysis techniques such as ratio analysis, vertical analysis, and horizontal analysis. It begins with a business and industry overview, highlighting American Airlines' position within the aviation sector, its competitive landscape, and its strategic focus on market diversification. The analysis includes calculations and interpretations of key financial ratios including liquidity, financing, activity, and profitability ratios, derived from the company's historical financial data spanning several years. These ratios are used to assess the company's short-term solvency, long-term stability, operational efficiency, and overall profitability. The report also incorporates Porter’s Five Forces model to evaluate the competitive dynamics within the aviation industry. The findings provide stakeholders with insights into the financial health and performance of American Airlines Group Inc., aiding in investment decisions and strategic planning. Desklib is a valuable resource for students seeking similar financial analysis reports and solved assignments.

Running Head: Accounting for corporate structure

1

Project Report: Accounting for corporate structure

1

Project Report: Accounting for corporate structure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for corporate structure 2

Contents

Introduction.......................................................................................................................3

Business and industry analysis.........................................................................................3

Analysis of historical financial data.................................................................................4

Ratio analysis....................................................................................................................4

Horizontal analysis...........................................................................................................8

Vertical analysis................................................................................................................8

Analysis of financial performance....................................................................................9

Recommendation and conclusion.....................................................................................9

References.......................................................................................................................10

Appendix.........................................................................................................................12

Contents

Introduction.......................................................................................................................3

Business and industry analysis.........................................................................................3

Analysis of historical financial data.................................................................................4

Ratio analysis....................................................................................................................4

Horizontal analysis...........................................................................................................8

Vertical analysis................................................................................................................8

Analysis of financial performance....................................................................................9

Recommendation and conclusion.....................................................................................9

References.......................................................................................................................10

Appendix.........................................................................................................................12

Accounting for corporate structure 3

Introduction:

Financial statements of an organization explain about the financial strength, financial

position and financial performance of an organization. These statements are prepared by the

organization periodically to evaluate the performance of the company in context with the

accounting and finance. Financial statement includes statement of financial income, statement

of cash flows, and balance sheet and changes in equity statement. For evaluating and

analyzing the financial statement of an organization, financial analysis techniques are used.

Financial analysis techniques make it simple for the management of the comapny and the

stakeholders of the company to evaluate the financial statement and make a proper analysis

on the basis of it. Financial analysis techniques include ratio analysis, vertical analysis,

horizontal analysis etc. these methods evaluates the financial statements on the various basis

(Shapiro, 2005).

The report has been prepared to evaluate and analyze the financial performance and

position of AMERICAN AIRLINES GROUP INC. For evaluating and identifying the

position of the company, ratio analysis, vertical analysis and horizontal analysis techniques

have been used. The report makes it simple for the company and stakeholders of the

corporation to evaluate the financial performance of the company and make a conclusion

about the investment in the company.

Business and industry analysis:

AMERICAN AIRLINES GROUP INC is an American company which publicly

businesses in the airline holding company. Headquarter of the company is at Fort Worth,

Texas. The company is the outcome of a merger among AMR Corporation and US airways

group. The company is one of the biggest airline firms in the international market. The

company is operating its business under aviation industry. Currently, it is serving its services

at 350 destinations. Total revenue of the company is US $ 42.207 billion according to the

latest annual report. 1,18,500 employees are working in the company. the main competitive

company of AMERICAN AIRLINES GROUP INC is southwest airline group. Currently, the

company is diversifying its market and focusing on the new destinations to enhance the

market base of the company so that more market could be captured (Customer service, 2018).

The main mission and vision of the company is to serve the best quality services to its

clients as well as expand the market through focusing on the new destinations. The current

stock position of the comapny has been evaluated and it has been found that the current stock

price of the company is USD 50.90 which is quite higher than its book value (Yahoo finance,

2018). The stock position and the market position of the company are quite competitive and it

explains about the better changes in the organization. The future prediction about the stock

price of the company explains about the higher stock price from now (History, 2018).

Various other competitors are also available in the market for the company such as Delta

airlines, JetBlue airways, United continental holdings etc. the current financial trend of the

business explains about the few alterations and the company’s performance.

Aviation industry of America has also been evaluated and it has been recognized that

the industry is operating its business at a significant level. The performance of the company is

also better. The porter’s 5 forces model of aviation industry of America is as follows:

Competition among existing firms:

The competition among the already existing players is quite higher as many large and

small companies are offering the services at domestic as well as international level. Thus, the

threat of the company is quite higher.

Introduction:

Financial statements of an organization explain about the financial strength, financial

position and financial performance of an organization. These statements are prepared by the

organization periodically to evaluate the performance of the company in context with the

accounting and finance. Financial statement includes statement of financial income, statement

of cash flows, and balance sheet and changes in equity statement. For evaluating and

analyzing the financial statement of an organization, financial analysis techniques are used.

Financial analysis techniques make it simple for the management of the comapny and the

stakeholders of the company to evaluate the financial statement and make a proper analysis

on the basis of it. Financial analysis techniques include ratio analysis, vertical analysis,

horizontal analysis etc. these methods evaluates the financial statements on the various basis

(Shapiro, 2005).

The report has been prepared to evaluate and analyze the financial performance and

position of AMERICAN AIRLINES GROUP INC. For evaluating and identifying the

position of the company, ratio analysis, vertical analysis and horizontal analysis techniques

have been used. The report makes it simple for the company and stakeholders of the

corporation to evaluate the financial performance of the company and make a conclusion

about the investment in the company.

Business and industry analysis:

AMERICAN AIRLINES GROUP INC is an American company which publicly

businesses in the airline holding company. Headquarter of the company is at Fort Worth,

Texas. The company is the outcome of a merger among AMR Corporation and US airways

group. The company is one of the biggest airline firms in the international market. The

company is operating its business under aviation industry. Currently, it is serving its services

at 350 destinations. Total revenue of the company is US $ 42.207 billion according to the

latest annual report. 1,18,500 employees are working in the company. the main competitive

company of AMERICAN AIRLINES GROUP INC is southwest airline group. Currently, the

company is diversifying its market and focusing on the new destinations to enhance the

market base of the company so that more market could be captured (Customer service, 2018).

The main mission and vision of the company is to serve the best quality services to its

clients as well as expand the market through focusing on the new destinations. The current

stock position of the comapny has been evaluated and it has been found that the current stock

price of the company is USD 50.90 which is quite higher than its book value (Yahoo finance,

2018). The stock position and the market position of the company are quite competitive and it

explains about the better changes in the organization. The future prediction about the stock

price of the company explains about the higher stock price from now (History, 2018).

Various other competitors are also available in the market for the company such as Delta

airlines, JetBlue airways, United continental holdings etc. the current financial trend of the

business explains about the few alterations and the company’s performance.

Aviation industry of America has also been evaluated and it has been recognized that

the industry is operating its business at a significant level. The performance of the company is

also better. The porter’s 5 forces model of aviation industry of America is as follows:

Competition among existing firms:

The competition among the already existing players is quite higher as many large and

small companies are offering the services at domestic as well as international level. Thus, the

threat of the company is quite higher.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for corporate structure 4

Threat of new entrants:

Risk from new entrants is quite lower for aviation industry. As huge investments are

required to enter into the industry as well as various regulations is also there. Though, the

threat of the company is quite lower.

Threat of substitute products:

Risk from alternative products is moderate for aviation business. As there is various

transportation options are available for the customers. Though, for long travel people relies

on the aviation industry (Gitman and Zutter, 2012).

Bargaining power of suppliers:

There are a large number of suppliers which caters to the airline industry. The

suppliers of America hardly have any bargaining power. Overall, the bargaining power of

suppliers is quite low (Annual report, 2017).

Bargaining power of customers:

There is a great integer of customers which takes services from the airline industry.

The customers of America usually take the help of airlines to travel from one place to other.

Overall, the bargaining power of customers is quite low.

Analysis of historical financial data:

Financial analysis is a process which evaluates the financial reports of the company to

generate an idea about the position of the company at internal as well as external level.

Financial analysis techniques make it easier for the management of the comapny to appraise

the historical data and the stakeholders of the business to evaluate the financial statement and

make a proper analysis on the basis of it (Brigham and Ehrhardt, 2013). Financial analysis

techniques include ratio analysis, vertical analysis, horizontal analysis etc. these methods

evaluates the financial statements on the various basis. Following is the study of financial

analysis of AMERICAN AIRLINES GROUP INC:

Ratio analysis:

Ratio analysis is a quantitative evaluation technique which takes the concern of

financial statement and other financial activities of the company to analyze the operating and

financial level of the company. The ratio analysis evaluates the liquidity, efficiency, solvency

and profitability level. Following is the calculations and the analysis of AMERICAN

AIRLINES GROUP INC:

Year

(____2017____)

Year

(______2016__)

Year

(____2015____)

Current ratio 0.61 0.74 0.73

Acid test ratio 0.52 0.67 0.67

Cash ratio 0.02 0.02 0.03

Accruals ratio 0.06 0.04 0.16

Cash Flow Yield -0.05 0.03 0.00

Cash Flow to

Sales

-0.03 0.02 0.00

Cash Flow to

Assets

-0.02 0.02 0.00

Current Cash Debt

Coverage Ratio

0.32 0.47 0.46

Threat of new entrants:

Risk from new entrants is quite lower for aviation industry. As huge investments are

required to enter into the industry as well as various regulations is also there. Though, the

threat of the company is quite lower.

Threat of substitute products:

Risk from alternative products is moderate for aviation business. As there is various

transportation options are available for the customers. Though, for long travel people relies

on the aviation industry (Gitman and Zutter, 2012).

Bargaining power of suppliers:

There are a large number of suppliers which caters to the airline industry. The

suppliers of America hardly have any bargaining power. Overall, the bargaining power of

suppliers is quite low (Annual report, 2017).

Bargaining power of customers:

There is a great integer of customers which takes services from the airline industry.

The customers of America usually take the help of airlines to travel from one place to other.

Overall, the bargaining power of customers is quite low.

Analysis of historical financial data:

Financial analysis is a process which evaluates the financial reports of the company to

generate an idea about the position of the company at internal as well as external level.

Financial analysis techniques make it easier for the management of the comapny to appraise

the historical data and the stakeholders of the business to evaluate the financial statement and

make a proper analysis on the basis of it (Brigham and Ehrhardt, 2013). Financial analysis

techniques include ratio analysis, vertical analysis, horizontal analysis etc. these methods

evaluates the financial statements on the various basis. Following is the study of financial

analysis of AMERICAN AIRLINES GROUP INC:

Ratio analysis:

Ratio analysis is a quantitative evaluation technique which takes the concern of

financial statement and other financial activities of the company to analyze the operating and

financial level of the company. The ratio analysis evaluates the liquidity, efficiency, solvency

and profitability level. Following is the calculations and the analysis of AMERICAN

AIRLINES GROUP INC:

Year

(____2017____)

Year

(______2016__)

Year

(____2015____)

Current ratio 0.61 0.74 0.73

Acid test ratio 0.52 0.67 0.67

Cash ratio 0.02 0.02 0.03

Accruals ratio 0.06 0.04 0.16

Cash Flow Yield -0.05 0.03 0.00

Cash Flow to

Sales

-0.03 0.02 0.00

Cash Flow to

Assets

-0.02 0.02 0.00

Current Cash Debt

Coverage Ratio

0.32 0.47 0.46

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for corporate structure 5

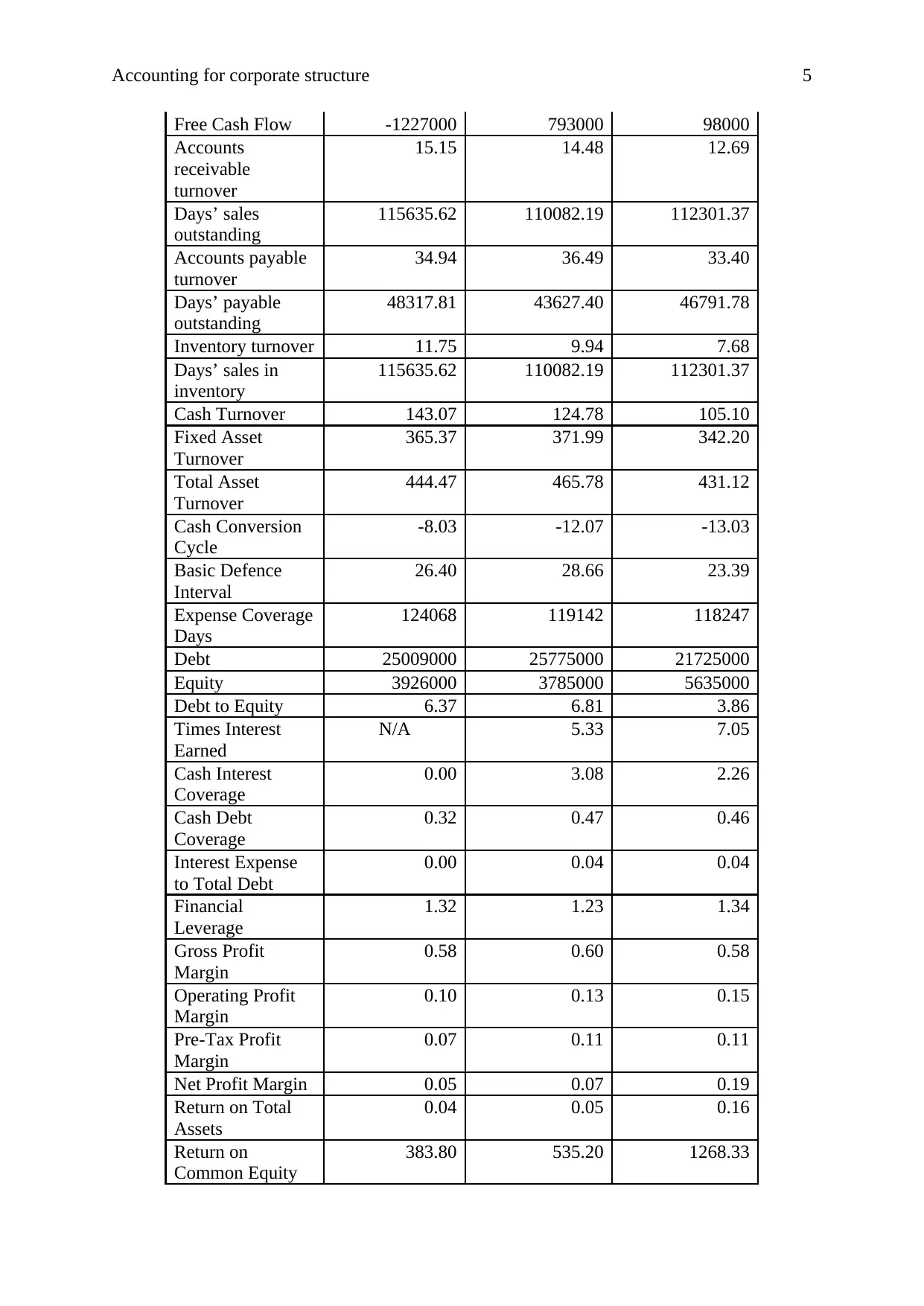

Free Cash Flow -1227000 793000 98000

Accounts

receivable

turnover

15.15 14.48 12.69

Days’ sales

outstanding

115635.62 110082.19 112301.37

Accounts payable

turnover

34.94 36.49 33.40

Days’ payable

outstanding

48317.81 43627.40 46791.78

Inventory turnover 11.75 9.94 7.68

Days’ sales in

inventory

115635.62 110082.19 112301.37

Cash Turnover 143.07 124.78 105.10

Fixed Asset

Turnover

365.37 371.99 342.20

Total Asset

Turnover

444.47 465.78 431.12

Cash Conversion

Cycle

-8.03 -12.07 -13.03

Basic Defence

Interval

26.40 28.66 23.39

Expense Coverage

Days

124068 119142 118247

Debt 25009000 25775000 21725000

Equity 3926000 3785000 5635000

Debt to Equity 6.37 6.81 3.86

Times Interest

Earned

N/A 5.33 7.05

Cash Interest

Coverage

0.00 3.08 2.26

Cash Debt

Coverage

0.32 0.47 0.46

Interest Expense

to Total Debt

0.00 0.04 0.04

Financial

Leverage

1.32 1.23 1.34

Gross Profit

Margin

0.58 0.60 0.58

Operating Profit

Margin

0.10 0.13 0.15

Pre-Tax Profit

Margin

0.07 0.11 0.11

Net Profit Margin 0.05 0.07 0.19

Return on Total

Assets

0.04 0.05 0.16

Return on

Common Equity

383.80 535.20 1268.33

Free Cash Flow -1227000 793000 98000

Accounts

receivable

turnover

15.15 14.48 12.69

Days’ sales

outstanding

115635.62 110082.19 112301.37

Accounts payable

turnover

34.94 36.49 33.40

Days’ payable

outstanding

48317.81 43627.40 46791.78

Inventory turnover 11.75 9.94 7.68

Days’ sales in

inventory

115635.62 110082.19 112301.37

Cash Turnover 143.07 124.78 105.10

Fixed Asset

Turnover

365.37 371.99 342.20

Total Asset

Turnover

444.47 465.78 431.12

Cash Conversion

Cycle

-8.03 -12.07 -13.03

Basic Defence

Interval

26.40 28.66 23.39

Expense Coverage

Days

124068 119142 118247

Debt 25009000 25775000 21725000

Equity 3926000 3785000 5635000

Debt to Equity 6.37 6.81 3.86

Times Interest

Earned

N/A 5.33 7.05

Cash Interest

Coverage

0.00 3.08 2.26

Cash Debt

Coverage

0.32 0.47 0.46

Interest Expense

to Total Debt

0.00 0.04 0.04

Financial

Leverage

1.32 1.23 1.34

Gross Profit

Margin

0.58 0.60 0.58

Operating Profit

Margin

0.10 0.13 0.15

Pre-Tax Profit

Margin

0.07 0.11 0.11

Net Profit Margin 0.05 0.07 0.19

Return on Total

Assets

0.04 0.05 0.16

Return on

Common Equity

383.80 535.20 1268.33

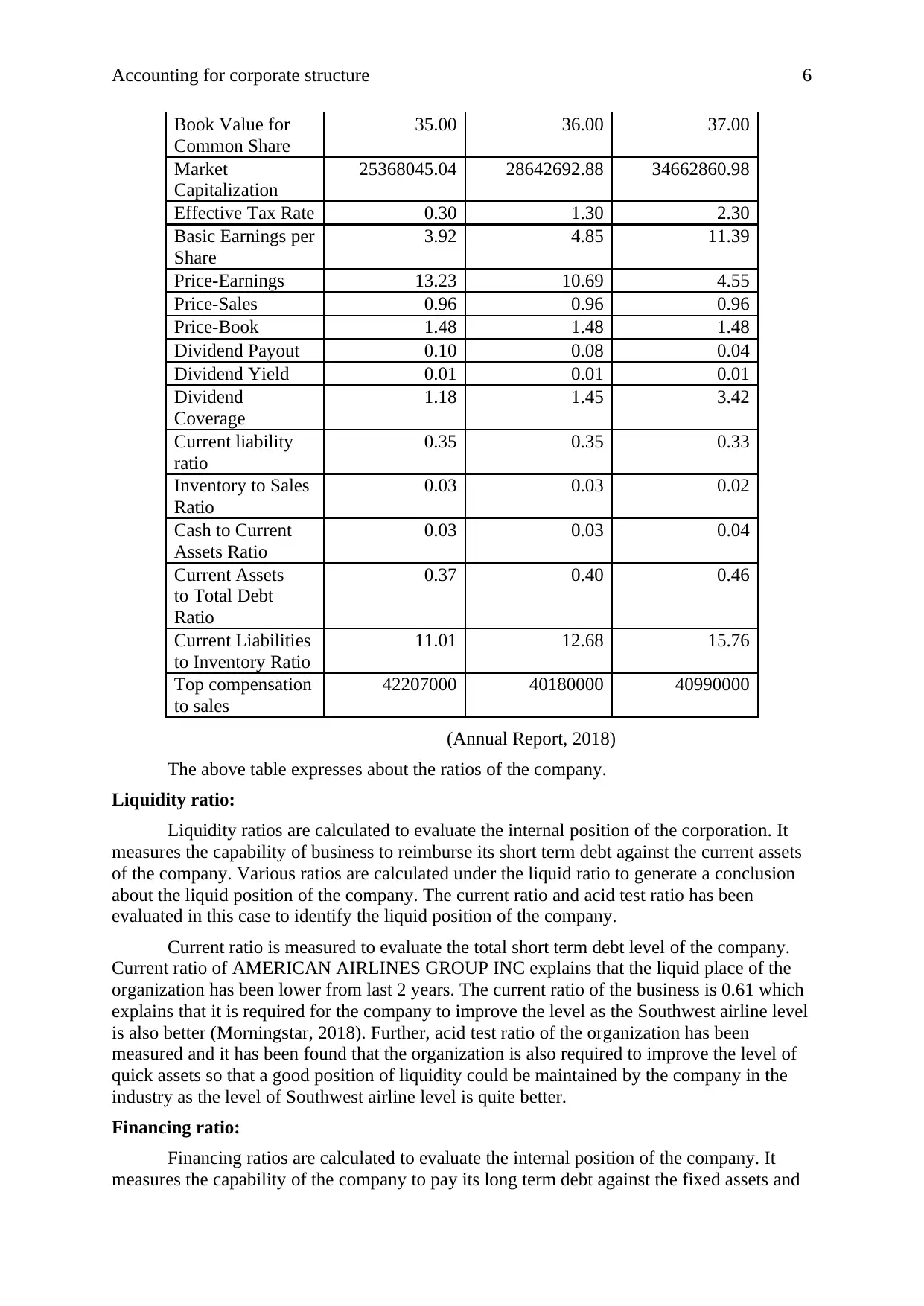

Accounting for corporate structure 6

Book Value for

Common Share

35.00 36.00 37.00

Market

Capitalization

25368045.04 28642692.88 34662860.98

Effective Tax Rate 0.30 1.30 2.30

Basic Earnings per

Share

3.92 4.85 11.39

Price-Earnings 13.23 10.69 4.55

Price-Sales 0.96 0.96 0.96

Price-Book 1.48 1.48 1.48

Dividend Payout 0.10 0.08 0.04

Dividend Yield 0.01 0.01 0.01

Dividend

Coverage

1.18 1.45 3.42

Current liability

ratio

0.35 0.35 0.33

Inventory to Sales

Ratio

0.03 0.03 0.02

Cash to Current

Assets Ratio

0.03 0.03 0.04

Current Assets

to Total Debt

Ratio

0.37 0.40 0.46

Current Liabilities

to Inventory Ratio

11.01 12.68 15.76

Top compensation

to sales

42207000 40180000 40990000

(Annual Report, 2018)

The above table expresses about the ratios of the company.

Liquidity ratio:

Liquidity ratios are calculated to evaluate the internal position of the corporation. It

measures the capability of business to reimburse its short term debt against the current assets

of the company. Various ratios are calculated under the liquid ratio to generate a conclusion

about the liquid position of the company. The current ratio and acid test ratio has been

evaluated in this case to identify the liquid position of the company.

Current ratio is measured to evaluate the total short term debt level of the company.

Current ratio of AMERICAN AIRLINES GROUP INC explains that the liquid place of the

organization has been lower from last 2 years. The current ratio of the business is 0.61 which

explains that it is required for the company to improve the level as the Southwest airline level

is also better (Morningstar, 2018). Further, acid test ratio of the organization has been

measured and it has been found that the organization is also required to improve the level of

quick assets so that a good position of liquidity could be maintained by the company in the

industry as the level of Southwest airline level is quite better.

Financing ratio:

Financing ratios are calculated to evaluate the internal position of the company. It

measures the capability of the company to pay its long term debt against the fixed assets and

Book Value for

Common Share

35.00 36.00 37.00

Market

Capitalization

25368045.04 28642692.88 34662860.98

Effective Tax Rate 0.30 1.30 2.30

Basic Earnings per

Share

3.92 4.85 11.39

Price-Earnings 13.23 10.69 4.55

Price-Sales 0.96 0.96 0.96

Price-Book 1.48 1.48 1.48

Dividend Payout 0.10 0.08 0.04

Dividend Yield 0.01 0.01 0.01

Dividend

Coverage

1.18 1.45 3.42

Current liability

ratio

0.35 0.35 0.33

Inventory to Sales

Ratio

0.03 0.03 0.02

Cash to Current

Assets Ratio

0.03 0.03 0.04

Current Assets

to Total Debt

Ratio

0.37 0.40 0.46

Current Liabilities

to Inventory Ratio

11.01 12.68 15.76

Top compensation

to sales

42207000 40180000 40990000

(Annual Report, 2018)

The above table expresses about the ratios of the company.

Liquidity ratio:

Liquidity ratios are calculated to evaluate the internal position of the corporation. It

measures the capability of business to reimburse its short term debt against the current assets

of the company. Various ratios are calculated under the liquid ratio to generate a conclusion

about the liquid position of the company. The current ratio and acid test ratio has been

evaluated in this case to identify the liquid position of the company.

Current ratio is measured to evaluate the total short term debt level of the company.

Current ratio of AMERICAN AIRLINES GROUP INC explains that the liquid place of the

organization has been lower from last 2 years. The current ratio of the business is 0.61 which

explains that it is required for the company to improve the level as the Southwest airline level

is also better (Morningstar, 2018). Further, acid test ratio of the organization has been

measured and it has been found that the organization is also required to improve the level of

quick assets so that a good position of liquidity could be maintained by the company in the

industry as the level of Southwest airline level is quite better.

Financing ratio:

Financing ratios are calculated to evaluate the internal position of the company. It

measures the capability of the company to pay its long term debt against the fixed assets and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for corporate structure 7

equity of the company. Various ratios are calculated under the financing ratio to generate a

conclusion about the financing and capital structure position. The debt to equity ratio and

times interest earned ratio has been evaluated in this case to identify the financing position of

the company (Brigham and Ehrhardt, 2013).

The ratio of Debt to equity is measured to estimate the total long term debt level of

the business against the whole equity of the concern. It explains about the capital structure

position of AMERICAN AIRLINES GROUP INC. The ratio explains that the long term debt

payment capability of the company is quite higher in the industry. The debt equity ratio of the

company is 6.37 which explain that it is required for the company to reduce the level of

equity to manage the risk and return as the Southwest airline level is also lower (Deegan,

2013). Further, times interest earned ratio of the business has been measured and it has also

been evaluated that interest amount of the business has been lowered from most recent years

and it briefs about the inferior cost of capital of the business.

Activity ratio:

Further, activity ratios are calculated to appraise the efficiency spot of the business. It

measures the capability of the troupe to manage its assets and the working capital for the

daily operations. Various ratios are calculated under the activity ratio to generate a conclusion

about the working capital position of the company. The receivable turnover ratio, payable

turnover ratio and inventory turnover ratio has been evaluated in this case to identify the

activity and efficiency position of the company.

Receivable turnover ratio is measured to evaluate the total time in which the debtors

pay the amount to the company. It explains about the efficiency position of AMERICAN

AIRLINES GROUP INC. The ratio explains that the debtors’ turnover ratio of the company

is 15.15 days. Further, the accounts payable days and inventory turnover days have been

calculated to identify the efficient position of the company (Romney et al, 2006). The

accounts payable turnover days of the company are 34.94 days and inventory turnover days

are 11.75 days which explains that the efficiency position of the company is quite

competitive and it has been better from last year. It has also been found that the level of the

company is also better then the Southwest airline level.

Profitability ratio:

Further, the profitability ratios of the company have also been evaluated to identify

the capability of the company to generate the profit (Grinblatt and Titman, 2016). Gross

profit % and return on shareholder’s equity has been evaluated to identify the profitability

position of American Airlines group. The gross profit margin of the company is 58% which

has been lower from last year. Though, the position of the company is quite better. Further,

ROCE has been evaluated and it has been found that the ROCE of the company is 383.8

which have also been lower from last year. Though, the position of the company is quite

competitive (Morningstar, 2018).

Stock ratios:

Lastly, the stock ratios of the company have been evaluated to identify the capability

of the company to manage the market position. Earnings per share, price earnings ratio and

dividend yield has been evaluated to identity the stock position of American Airlines group

(Kiran and Singh, 2014). The earnings per share of the company are 3.92 which have been

lower from last year. Further, price earnings ratio and dividend yield of the company has

been evaluated and it has been found that the position of the corporation has been improved

and it is quite competitive in the industry.

equity of the company. Various ratios are calculated under the financing ratio to generate a

conclusion about the financing and capital structure position. The debt to equity ratio and

times interest earned ratio has been evaluated in this case to identify the financing position of

the company (Brigham and Ehrhardt, 2013).

The ratio of Debt to equity is measured to estimate the total long term debt level of

the business against the whole equity of the concern. It explains about the capital structure

position of AMERICAN AIRLINES GROUP INC. The ratio explains that the long term debt

payment capability of the company is quite higher in the industry. The debt equity ratio of the

company is 6.37 which explain that it is required for the company to reduce the level of

equity to manage the risk and return as the Southwest airline level is also lower (Deegan,

2013). Further, times interest earned ratio of the business has been measured and it has also

been evaluated that interest amount of the business has been lowered from most recent years

and it briefs about the inferior cost of capital of the business.

Activity ratio:

Further, activity ratios are calculated to appraise the efficiency spot of the business. It

measures the capability of the troupe to manage its assets and the working capital for the

daily operations. Various ratios are calculated under the activity ratio to generate a conclusion

about the working capital position of the company. The receivable turnover ratio, payable

turnover ratio and inventory turnover ratio has been evaluated in this case to identify the

activity and efficiency position of the company.

Receivable turnover ratio is measured to evaluate the total time in which the debtors

pay the amount to the company. It explains about the efficiency position of AMERICAN

AIRLINES GROUP INC. The ratio explains that the debtors’ turnover ratio of the company

is 15.15 days. Further, the accounts payable days and inventory turnover days have been

calculated to identify the efficient position of the company (Romney et al, 2006). The

accounts payable turnover days of the company are 34.94 days and inventory turnover days

are 11.75 days which explains that the efficiency position of the company is quite

competitive and it has been better from last year. It has also been found that the level of the

company is also better then the Southwest airline level.

Profitability ratio:

Further, the profitability ratios of the company have also been evaluated to identify

the capability of the company to generate the profit (Grinblatt and Titman, 2016). Gross

profit % and return on shareholder’s equity has been evaluated to identify the profitability

position of American Airlines group. The gross profit margin of the company is 58% which

has been lower from last year. Though, the position of the company is quite better. Further,

ROCE has been evaluated and it has been found that the ROCE of the company is 383.8

which have also been lower from last year. Though, the position of the company is quite

competitive (Morningstar, 2018).

Stock ratios:

Lastly, the stock ratios of the company have been evaluated to identify the capability

of the company to manage the market position. Earnings per share, price earnings ratio and

dividend yield has been evaluated to identity the stock position of American Airlines group

(Kiran and Singh, 2014). The earnings per share of the company are 3.92 which have been

lower from last year. Further, price earnings ratio and dividend yield of the company has

been evaluated and it has been found that the position of the corporation has been improved

and it is quite competitive in the industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for corporate structure 8

The above ratio analysis calculations of the business brief that the superior spot and

performance of the company.

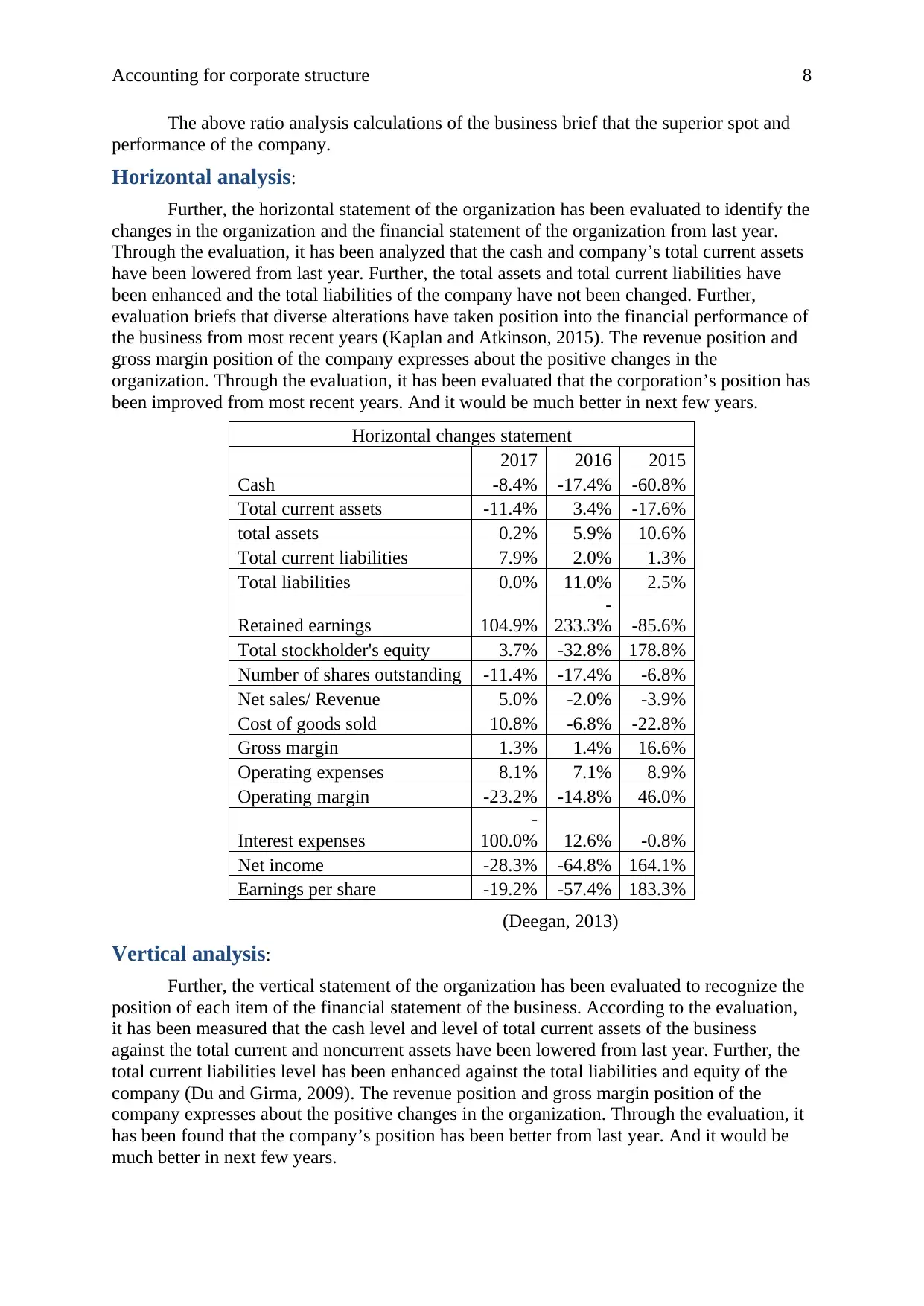

Horizontal analysis:

Further, the horizontal statement of the organization has been evaluated to identify the

changes in the organization and the financial statement of the organization from last year.

Through the evaluation, it has been analyzed that the cash and company’s total current assets

have been lowered from last year. Further, the total assets and total current liabilities have

been enhanced and the total liabilities of the company have not been changed. Further,

evaluation briefs that diverse alterations have taken position into the financial performance of

the business from most recent years (Kaplan and Atkinson, 2015). The revenue position and

gross margin position of the company expresses about the positive changes in the

organization. Through the evaluation, it has been evaluated that the corporation’s position has

been improved from most recent years. And it would be much better in next few years.

Horizontal changes statement

2017 2016 2015

Cash -8.4% -17.4% -60.8%

Total current assets -11.4% 3.4% -17.6%

total assets 0.2% 5.9% 10.6%

Total current liabilities 7.9% 2.0% 1.3%

Total liabilities 0.0% 11.0% 2.5%

Retained earnings 104.9%

-

233.3% -85.6%

Total stockholder's equity 3.7% -32.8% 178.8%

Number of shares outstanding -11.4% -17.4% -6.8%

Net sales/ Revenue 5.0% -2.0% -3.9%

Cost of goods sold 10.8% -6.8% -22.8%

Gross margin 1.3% 1.4% 16.6%

Operating expenses 8.1% 7.1% 8.9%

Operating margin -23.2% -14.8% 46.0%

Interest expenses

-

100.0% 12.6% -0.8%

Net income -28.3% -64.8% 164.1%

Earnings per share -19.2% -57.4% 183.3%

(Deegan, 2013)

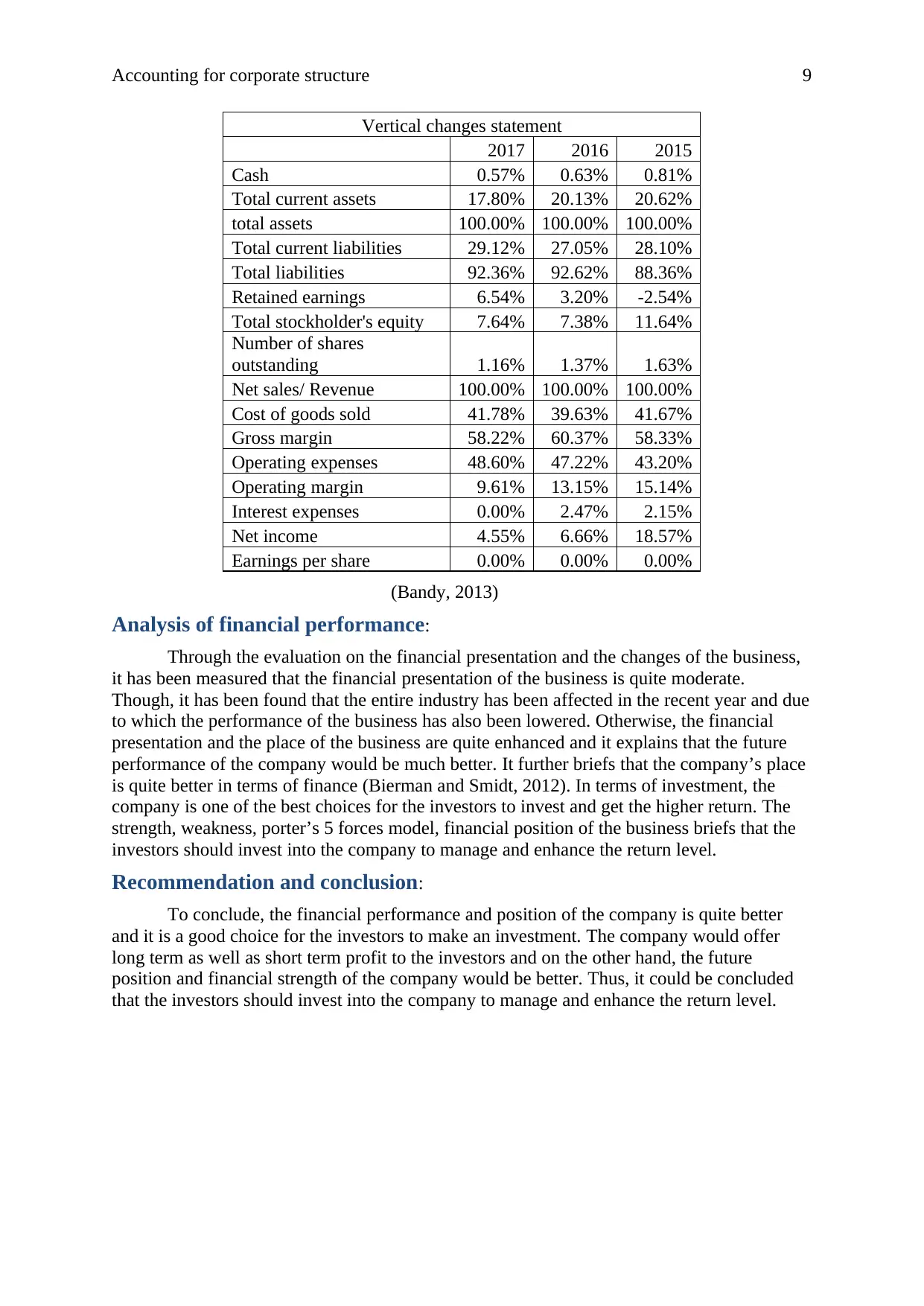

Vertical analysis:

Further, the vertical statement of the organization has been evaluated to recognize the

position of each item of the financial statement of the business. According to the evaluation,

it has been measured that the cash level and level of total current assets of the business

against the total current and noncurrent assets have been lowered from last year. Further, the

total current liabilities level has been enhanced against the total liabilities and equity of the

company (Du and Girma, 2009). The revenue position and gross margin position of the

company expresses about the positive changes in the organization. Through the evaluation, it

has been found that the company’s position has been better from last year. And it would be

much better in next few years.

The above ratio analysis calculations of the business brief that the superior spot and

performance of the company.

Horizontal analysis:

Further, the horizontal statement of the organization has been evaluated to identify the

changes in the organization and the financial statement of the organization from last year.

Through the evaluation, it has been analyzed that the cash and company’s total current assets

have been lowered from last year. Further, the total assets and total current liabilities have

been enhanced and the total liabilities of the company have not been changed. Further,

evaluation briefs that diverse alterations have taken position into the financial performance of

the business from most recent years (Kaplan and Atkinson, 2015). The revenue position and

gross margin position of the company expresses about the positive changes in the

organization. Through the evaluation, it has been evaluated that the corporation’s position has

been improved from most recent years. And it would be much better in next few years.

Horizontal changes statement

2017 2016 2015

Cash -8.4% -17.4% -60.8%

Total current assets -11.4% 3.4% -17.6%

total assets 0.2% 5.9% 10.6%

Total current liabilities 7.9% 2.0% 1.3%

Total liabilities 0.0% 11.0% 2.5%

Retained earnings 104.9%

-

233.3% -85.6%

Total stockholder's equity 3.7% -32.8% 178.8%

Number of shares outstanding -11.4% -17.4% -6.8%

Net sales/ Revenue 5.0% -2.0% -3.9%

Cost of goods sold 10.8% -6.8% -22.8%

Gross margin 1.3% 1.4% 16.6%

Operating expenses 8.1% 7.1% 8.9%

Operating margin -23.2% -14.8% 46.0%

Interest expenses

-

100.0% 12.6% -0.8%

Net income -28.3% -64.8% 164.1%

Earnings per share -19.2% -57.4% 183.3%

(Deegan, 2013)

Vertical analysis:

Further, the vertical statement of the organization has been evaluated to recognize the

position of each item of the financial statement of the business. According to the evaluation,

it has been measured that the cash level and level of total current assets of the business

against the total current and noncurrent assets have been lowered from last year. Further, the

total current liabilities level has been enhanced against the total liabilities and equity of the

company (Du and Girma, 2009). The revenue position and gross margin position of the

company expresses about the positive changes in the organization. Through the evaluation, it

has been found that the company’s position has been better from last year. And it would be

much better in next few years.

Accounting for corporate structure 9

Vertical changes statement

2017 2016 2015

Cash 0.57% 0.63% 0.81%

Total current assets 17.80% 20.13% 20.62%

total assets 100.00% 100.00% 100.00%

Total current liabilities 29.12% 27.05% 28.10%

Total liabilities 92.36% 92.62% 88.36%

Retained earnings 6.54% 3.20% -2.54%

Total stockholder's equity 7.64% 7.38% 11.64%

Number of shares

outstanding 1.16% 1.37% 1.63%

Net sales/ Revenue 100.00% 100.00% 100.00%

Cost of goods sold 41.78% 39.63% 41.67%

Gross margin 58.22% 60.37% 58.33%

Operating expenses 48.60% 47.22% 43.20%

Operating margin 9.61% 13.15% 15.14%

Interest expenses 0.00% 2.47% 2.15%

Net income 4.55% 6.66% 18.57%

Earnings per share 0.00% 0.00% 0.00%

(Bandy, 2013)

Analysis of financial performance:

Through the evaluation on the financial presentation and the changes of the business,

it has been measured that the financial presentation of the business is quite moderate.

Though, it has been found that the entire industry has been affected in the recent year and due

to which the performance of the business has also been lowered. Otherwise, the financial

presentation and the place of the business are quite enhanced and it explains that the future

performance of the company would be much better. It further briefs that the company’s place

is quite better in terms of finance (Bierman and Smidt, 2012). In terms of investment, the

company is one of the best choices for the investors to invest and get the higher return. The

strength, weakness, porter’s 5 forces model, financial position of the business briefs that the

investors should invest into the company to manage and enhance the return level.

Recommendation and conclusion:

To conclude, the financial performance and position of the company is quite better

and it is a good choice for the investors to make an investment. The company would offer

long term as well as short term profit to the investors and on the other hand, the future

position and financial strength of the company would be better. Thus, it could be concluded

that the investors should invest into the company to manage and enhance the return level.

Vertical changes statement

2017 2016 2015

Cash 0.57% 0.63% 0.81%

Total current assets 17.80% 20.13% 20.62%

total assets 100.00% 100.00% 100.00%

Total current liabilities 29.12% 27.05% 28.10%

Total liabilities 92.36% 92.62% 88.36%

Retained earnings 6.54% 3.20% -2.54%

Total stockholder's equity 7.64% 7.38% 11.64%

Number of shares

outstanding 1.16% 1.37% 1.63%

Net sales/ Revenue 100.00% 100.00% 100.00%

Cost of goods sold 41.78% 39.63% 41.67%

Gross margin 58.22% 60.37% 58.33%

Operating expenses 48.60% 47.22% 43.20%

Operating margin 9.61% 13.15% 15.14%

Interest expenses 0.00% 2.47% 2.15%

Net income 4.55% 6.66% 18.57%

Earnings per share 0.00% 0.00% 0.00%

(Bandy, 2013)

Analysis of financial performance:

Through the evaluation on the financial presentation and the changes of the business,

it has been measured that the financial presentation of the business is quite moderate.

Though, it has been found that the entire industry has been affected in the recent year and due

to which the performance of the business has also been lowered. Otherwise, the financial

presentation and the place of the business are quite enhanced and it explains that the future

performance of the company would be much better. It further briefs that the company’s place

is quite better in terms of finance (Bierman and Smidt, 2012). In terms of investment, the

company is one of the best choices for the investors to invest and get the higher return. The

strength, weakness, porter’s 5 forces model, financial position of the business briefs that the

investors should invest into the company to manage and enhance the return level.

Recommendation and conclusion:

To conclude, the financial performance and position of the company is quite better

and it is a good choice for the investors to make an investment. The company would offer

long term as well as short term profit to the investors and on the other hand, the future

position and financial strength of the company would be better. Thus, it could be concluded

that the investors should invest into the company to manage and enhance the return level.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for corporate structure 10

References:

Annual Report. 2017. AMERICAN AIRLINES GROUP. [Online]. Available at:

https://americanairlines.gcs-web.com/static-files/17cae9f4-55b0-4a05-a2dc-33fcc0a01985

[Accessed as on 28th Mar 2018].

Bandy, G. 2013. Financial management and accounting in the public sector. Oxon:

Routledge.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Customer services. 2018. AMERICAN AIRLINES GROUP. [Online]. Available at:

https://www.aa.com/i18n/customer-service/about-us/american-airlines-group.jsp [Accessed

as on 28th Mar 2018].

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Du, J. and Girma, S., 2009. Source of finance, growth and firm size: evidence from

China (No. 2009.03). Research paper/UNU-WIDER.

Fernandes, D., Lynch Jr, J.G. and Netemeyer, R.G., 2014. Financial literacy, financial

education, and downstream financial behaviors. Management Science, 60(8), pp.1861-1883.

Gitman, L.J. and Zutter, C.J., 2012. Principles of managerial finance. Prentice Hall.

Grinblatt, M. and Titman, S., 2016. Financial markets & corporate strategy. Prentice Hall.

History. 2018.. Southwest AIRLINES GROUP. [Online]. Available at:

https://www.southwest.com/ [Accessed as on 28th Mar 2018].

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kiran, R. S., & Singh, V. K. 2014. How to make the financial analysis an easy task – A

comparative analysis between the traditional and the modern approach? International Journal

of Engineering Research and Applications, 4(8), 61-66.

Morningstar. 2018. AMERICAN AIRLINES GROUP. [Online]. Available at:

http://financials.morningstar.com/income-statement/is.html?

t=AAL®ion=usa&culture=en-US [Accessed as on 28th Mar 2018].

Morningstar. 2018.. Southwest AIRLINES GROUP. [Online]. Available at:

http://financials.morningstar.com/income-statement/is.html?t=LUV®ion=USA [Accessed

as on 28th Mar 2018].

Romney, M.B., Steinbart, P.J., Zhang, R. and Xu, G., 2006. Accounting information systems.

Pearson Education.

Shapiro, A.C., 2005. Capital budgeting and investment analysis. Prentice Hall.

Yahoo finance. 2018.. AMERICAN AIRLINES GROUP. [Online]. Available at:

https://finance.yahoo.com/quote/AAL/ [Accessed as on 28th Mar 2018].

References:

Annual Report. 2017. AMERICAN AIRLINES GROUP. [Online]. Available at:

https://americanairlines.gcs-web.com/static-files/17cae9f4-55b0-4a05-a2dc-33fcc0a01985

[Accessed as on 28th Mar 2018].

Bandy, G. 2013. Financial management and accounting in the public sector. Oxon:

Routledge.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Customer services. 2018. AMERICAN AIRLINES GROUP. [Online]. Available at:

https://www.aa.com/i18n/customer-service/about-us/american-airlines-group.jsp [Accessed

as on 28th Mar 2018].

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Du, J. and Girma, S., 2009. Source of finance, growth and firm size: evidence from

China (No. 2009.03). Research paper/UNU-WIDER.

Fernandes, D., Lynch Jr, J.G. and Netemeyer, R.G., 2014. Financial literacy, financial

education, and downstream financial behaviors. Management Science, 60(8), pp.1861-1883.

Gitman, L.J. and Zutter, C.J., 2012. Principles of managerial finance. Prentice Hall.

Grinblatt, M. and Titman, S., 2016. Financial markets & corporate strategy. Prentice Hall.

History. 2018.. Southwest AIRLINES GROUP. [Online]. Available at:

https://www.southwest.com/ [Accessed as on 28th Mar 2018].

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kiran, R. S., & Singh, V. K. 2014. How to make the financial analysis an easy task – A

comparative analysis between the traditional and the modern approach? International Journal

of Engineering Research and Applications, 4(8), 61-66.

Morningstar. 2018. AMERICAN AIRLINES GROUP. [Online]. Available at:

http://financials.morningstar.com/income-statement/is.html?

t=AAL®ion=usa&culture=en-US [Accessed as on 28th Mar 2018].

Morningstar. 2018.. Southwest AIRLINES GROUP. [Online]. Available at:

http://financials.morningstar.com/income-statement/is.html?t=LUV®ion=USA [Accessed

as on 28th Mar 2018].

Romney, M.B., Steinbart, P.J., Zhang, R. and Xu, G., 2006. Accounting information systems.

Pearson Education.

Shapiro, A.C., 2005. Capital budgeting and investment analysis. Prentice Hall.

Yahoo finance. 2018.. AMERICAN AIRLINES GROUP. [Online]. Available at:

https://finance.yahoo.com/quote/AAL/ [Accessed as on 28th Mar 2018].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for corporate structure 11

Accounting for corporate structure 12

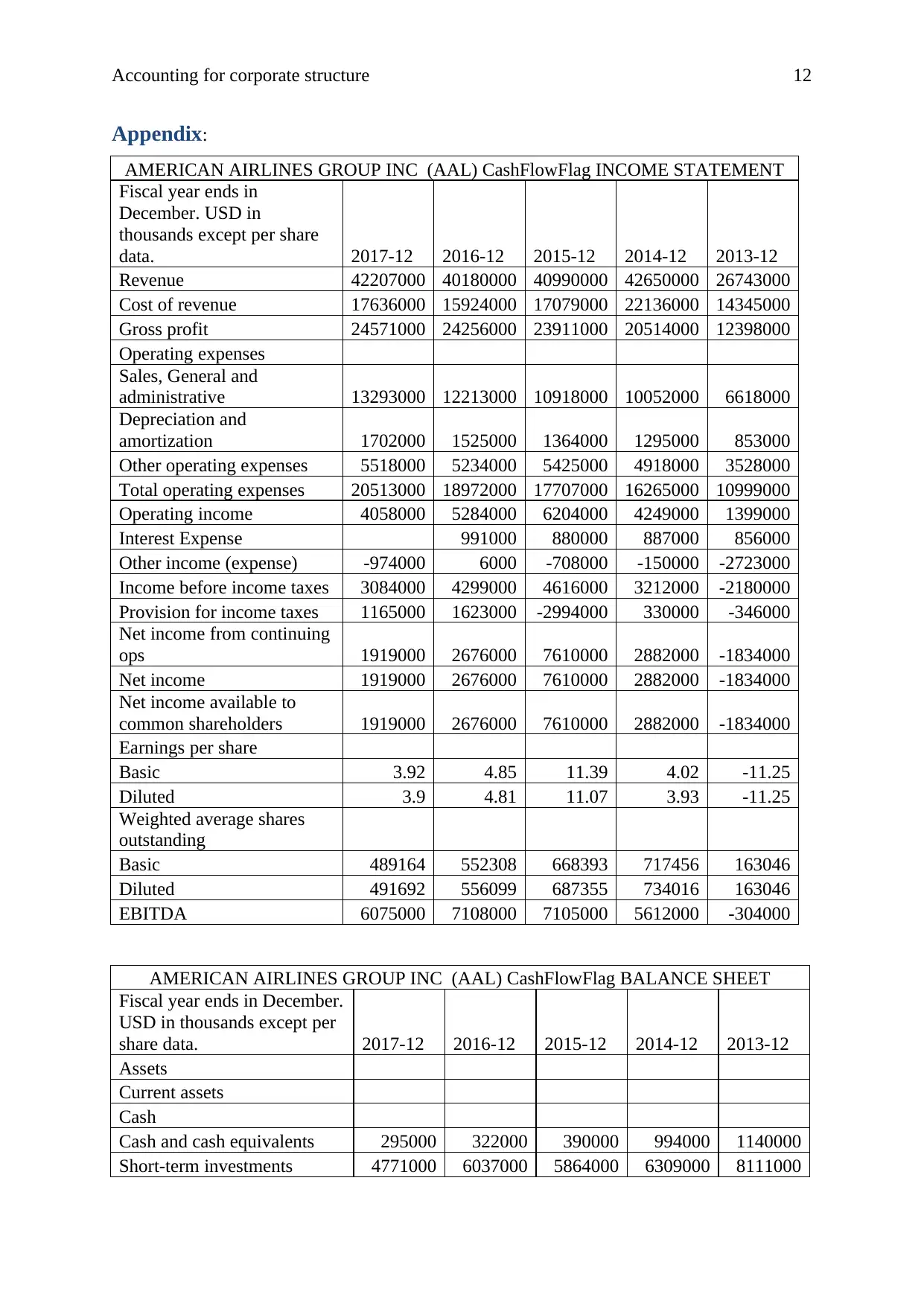

Appendix:

AMERICAN AIRLINES GROUP INC (AAL) CashFlowFlag INCOME STATEMENT

Fiscal year ends in

December. USD in

thousands except per share

data. 2017-12 2016-12 2015-12 2014-12 2013-12

Revenue 42207000 40180000 40990000 42650000 26743000

Cost of revenue 17636000 15924000 17079000 22136000 14345000

Gross profit 24571000 24256000 23911000 20514000 12398000

Operating expenses

Sales, General and

administrative 13293000 12213000 10918000 10052000 6618000

Depreciation and

amortization 1702000 1525000 1364000 1295000 853000

Other operating expenses 5518000 5234000 5425000 4918000 3528000

Total operating expenses 20513000 18972000 17707000 16265000 10999000

Operating income 4058000 5284000 6204000 4249000 1399000

Interest Expense 991000 880000 887000 856000

Other income (expense) -974000 6000 -708000 -150000 -2723000

Income before income taxes 3084000 4299000 4616000 3212000 -2180000

Provision for income taxes 1165000 1623000 -2994000 330000 -346000

Net income from continuing

ops 1919000 2676000 7610000 2882000 -1834000

Net income 1919000 2676000 7610000 2882000 -1834000

Net income available to

common shareholders 1919000 2676000 7610000 2882000 -1834000

Earnings per share

Basic 3.92 4.85 11.39 4.02 -11.25

Diluted 3.9 4.81 11.07 3.93 -11.25

Weighted average shares

outstanding

Basic 489164 552308 668393 717456 163046

Diluted 491692 556099 687355 734016 163046

EBITDA 6075000 7108000 7105000 5612000 -304000

AMERICAN AIRLINES GROUP INC (AAL) CashFlowFlag BALANCE SHEET

Fiscal year ends in December.

USD in thousands except per

share data. 2017-12 2016-12 2015-12 2014-12 2013-12

Assets

Current assets

Cash

Cash and cash equivalents 295000 322000 390000 994000 1140000

Short-term investments 4771000 6037000 5864000 6309000 8111000

Appendix:

AMERICAN AIRLINES GROUP INC (AAL) CashFlowFlag INCOME STATEMENT

Fiscal year ends in

December. USD in

thousands except per share

data. 2017-12 2016-12 2015-12 2014-12 2013-12

Revenue 42207000 40180000 40990000 42650000 26743000

Cost of revenue 17636000 15924000 17079000 22136000 14345000

Gross profit 24571000 24256000 23911000 20514000 12398000

Operating expenses

Sales, General and

administrative 13293000 12213000 10918000 10052000 6618000

Depreciation and

amortization 1702000 1525000 1364000 1295000 853000

Other operating expenses 5518000 5234000 5425000 4918000 3528000

Total operating expenses 20513000 18972000 17707000 16265000 10999000

Operating income 4058000 5284000 6204000 4249000 1399000

Interest Expense 991000 880000 887000 856000

Other income (expense) -974000 6000 -708000 -150000 -2723000

Income before income taxes 3084000 4299000 4616000 3212000 -2180000

Provision for income taxes 1165000 1623000 -2994000 330000 -346000

Net income from continuing

ops 1919000 2676000 7610000 2882000 -1834000

Net income 1919000 2676000 7610000 2882000 -1834000

Net income available to

common shareholders 1919000 2676000 7610000 2882000 -1834000

Earnings per share

Basic 3.92 4.85 11.39 4.02 -11.25

Diluted 3.9 4.81 11.07 3.93 -11.25

Weighted average shares

outstanding

Basic 489164 552308 668393 717456 163046

Diluted 491692 556099 687355 734016 163046

EBITDA 6075000 7108000 7105000 5612000 -304000

AMERICAN AIRLINES GROUP INC (AAL) CashFlowFlag BALANCE SHEET

Fiscal year ends in December.

USD in thousands except per

share data. 2017-12 2016-12 2015-12 2014-12 2013-12

Assets

Current assets

Cash

Cash and cash equivalents 295000 322000 390000 994000 1140000

Short-term investments 4771000 6037000 5864000 6309000 8111000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.