Comprehensive Financial Analysis of ANZ Bank's Performance

VerifiedAdded on 2023/04/23

|11

|1487

|408

Report

AI Summary

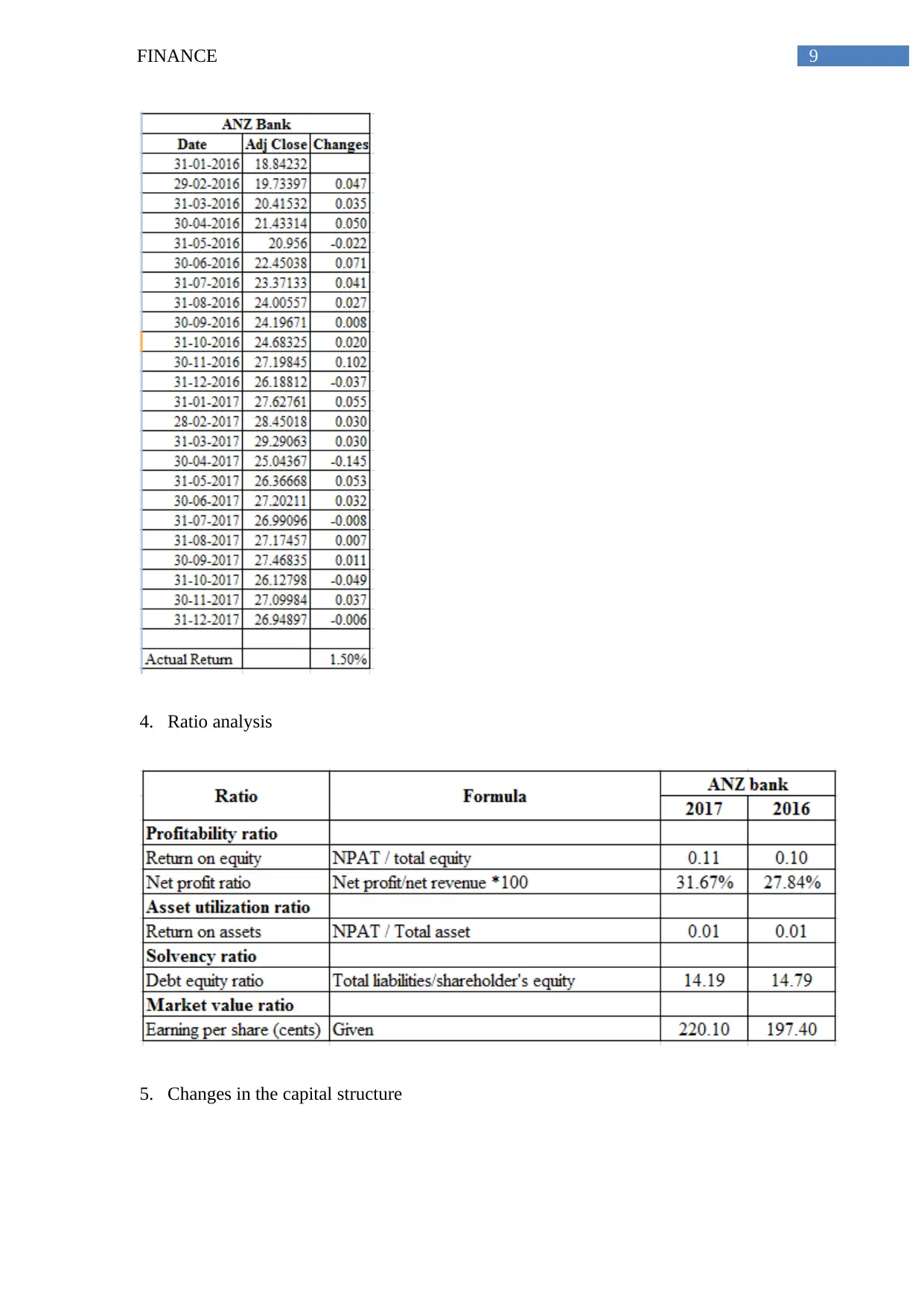

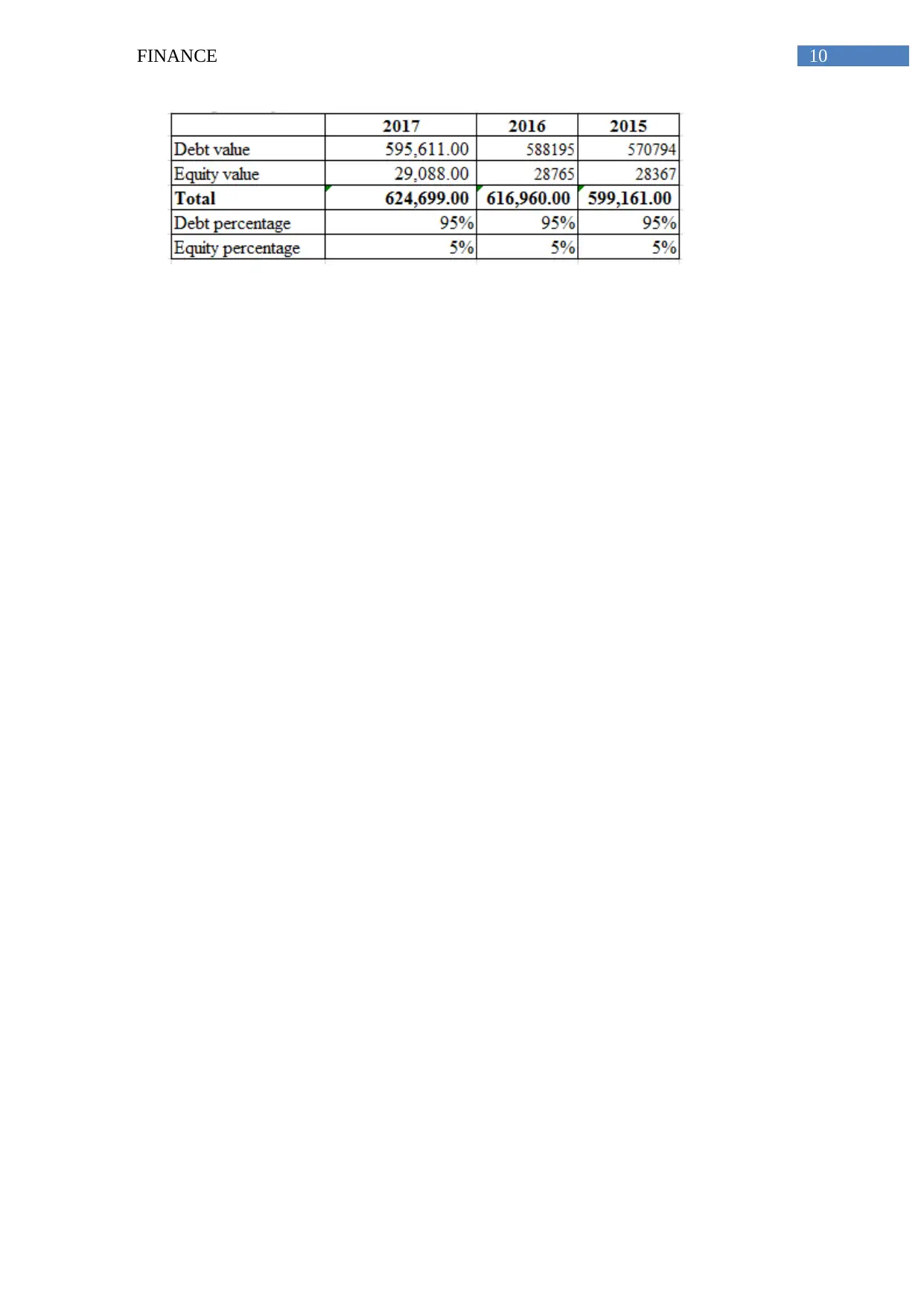

This report provides a comprehensive financial analysis of the Australia and New Zealand Banking Group (ANZ) Bank. It examines the bank's capital structure, revealing a significant reliance on debt financing. The report calculates the Weighted Average Cost of Capital (WACC) and assesses the stock's return relative to its associated risk using the Capital Asset Pricing Model (CAPM), indicating potential underperformance. A comparative analysis of ANZ's capital structure with National Australia Bank (NAB) is also included. Furthermore, the report delves into ratio analysis, evaluating profitability, solvency, asset utilization, and market value ratios to gauge ANZ's financial health. It also addresses the bank's accountability and integrity in light of past ethical issues, concluding that while profitability improved, there were shortcomings in efficiency, solvency, and operational risk management.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.