In-depth Financial Analysis, Budgeting, and Investment Report

VerifiedAdded on 2023/06/04

|17

|3868

|246

Report

AI Summary

This report provides a comprehensive financial analysis of Liverton Company, including the calculation and interpretation of financial ratios such as gross profit ratio, assets usage ratio, current ratio, acid test ratio, stock holding period, and debt to equity ratio. It critically evaluates financial statements and assesses the liquidity and profitability of the company. Additionally, the report prepares an opening statement of financial position and a cash budget for Sassy Clothing, analyzing additional expenditures and proposing strategies to improve cash flow. Furthermore, it analyzes the break-even point, calculates the margin of safety, and evaluates a new business strategy. Finally, the report covers investment appraisal techniques, including payback period, net present value, and average rate of return, discussing the best method of appraisal and providing a conclusion with key findings and recommendations.

To Finance

(Distinction Criteria)

(Distinction Criteria)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

Question 1 .......................................................................................................................................3

a) Calculation and interpretation of financial ratios....................................................................3

b) Critically evaluation of financial statement............................................................................5

Question 2........................................................................................................................................6

a) opening statement of financial position..................................................................................6

b) cash budget of Sassy clothing for 6 month ............................................................................7

c) Critical analyse of additional expenditures.............................................................................7

Question 3........................................................................................................................................8

a) Analysis of Break even point..................................................................................................8

b) 2019 and 2020 Margin of safety ( MOS ) ..............................................................................9

c) New strategy that has been developed by Jessica.................................................................10

Question 4......................................................................................................................................11

(a) calculation of pay back period, Net present value and average rate of return.....................11

b) Discuss the best method of appraisal technique...................................................................14

c) Investment appraisal techniques...........................................................................................14

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION ..........................................................................................................................3

Question 1 .......................................................................................................................................3

a) Calculation and interpretation of financial ratios....................................................................3

b) Critically evaluation of financial statement............................................................................5

Question 2........................................................................................................................................6

a) opening statement of financial position..................................................................................6

b) cash budget of Sassy clothing for 6 month ............................................................................7

c) Critical analyse of additional expenditures.............................................................................7

Question 3........................................................................................................................................8

a) Analysis of Break even point..................................................................................................8

b) 2019 and 2020 Margin of safety ( MOS ) ..............................................................................9

c) New strategy that has been developed by Jessica.................................................................10

Question 4......................................................................................................................................11

(a) calculation of pay back period, Net present value and average rate of return.....................11

b) Discuss the best method of appraisal technique...................................................................14

c) Investment appraisal techniques...........................................................................................14

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Finance means the manages of fund and considers different types of activities like

lending, saving and borrowing. It includes personal, public and corporate finance. It also

includes the raising on money for any kind of expenditure. Customers, enterprises and company

are not have enough money to pay the expenses, make payment of debtors. They also issue

equity share and debts to arrange the fund to conduct the daily operations. Financial ratios are

also very important component because it describes the financial position of the company and

determines the company have sufficient money to pay its debtors (Berrou and et.al, 2019). This

report includes, income statement and financial position of Liverton Company through which

analyse the liquidity position of the company. It also includes the preparation of opening

statement of financial position of Sassy clothing that sells their product by online and mail order.

Further this report includes the various investment appraisal techniques to select the project.

Question 1

a) Calculation and interpretation of financial ratios

There are various types of ratios that evaluates the liquidity position of the company such

as profitability, efficiency, turnover based and solvency ratios.

Gross profit ratio- It is the type of profitability ratio. The gross profit ratios tells the profit of

the company that is earned by selling of goods and services. It describes the relationship between

GP and sales revenue.

Formula= GP = ( revenue – cost of sales) * 100 / sales revenue\

=(3495 – 2182) *100 / 3495

=37.57 %

Interpretation- The GP ratio describes the true profit of the company. In year 2019 shows the

high GP margin it means the cost of products are low. But company should adopt special

technique that reduces the cost of the products and company can earn more GP in future.

Assets usage ratio- It is type of efficiency ratio. It describes the efficiency of the company with

that company utilises its total assets (Bharti, 2018).

Assets usage ratio = Total revenue / average fixed assets + average current assets

= 3495 / 3157.5

=1.10 times

Finance means the manages of fund and considers different types of activities like

lending, saving and borrowing. It includes personal, public and corporate finance. It also

includes the raising on money for any kind of expenditure. Customers, enterprises and company

are not have enough money to pay the expenses, make payment of debtors. They also issue

equity share and debts to arrange the fund to conduct the daily operations. Financial ratios are

also very important component because it describes the financial position of the company and

determines the company have sufficient money to pay its debtors (Berrou and et.al, 2019). This

report includes, income statement and financial position of Liverton Company through which

analyse the liquidity position of the company. It also includes the preparation of opening

statement of financial position of Sassy clothing that sells their product by online and mail order.

Further this report includes the various investment appraisal techniques to select the project.

Question 1

a) Calculation and interpretation of financial ratios

There are various types of ratios that evaluates the liquidity position of the company such

as profitability, efficiency, turnover based and solvency ratios.

Gross profit ratio- It is the type of profitability ratio. The gross profit ratios tells the profit of

the company that is earned by selling of goods and services. It describes the relationship between

GP and sales revenue.

Formula= GP = ( revenue – cost of sales) * 100 / sales revenue\

=(3495 – 2182) *100 / 3495

=37.57 %

Interpretation- The GP ratio describes the true profit of the company. In year 2019 shows the

high GP margin it means the cost of products are low. But company should adopt special

technique that reduces the cost of the products and company can earn more GP in future.

Assets usage ratio- It is type of efficiency ratio. It describes the efficiency of the company with

that company utilises its total assets (Bharti, 2018).

Assets usage ratio = Total revenue / average fixed assets + average current assets

= 3495 / 3157.5

=1.10 times

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation- In year 2019 the total assets turnover ratio shows 1.10times which are relatively

low. It means the company are not efficiency to used of assets in generation of sales. The ideal

ratio is 2.5 or more times. So that company must to improve their efficiency to earned more

revenue and proper utilisation of fixed assets and current assets (Boissay and et.al, 2021).

Current ratio – Liquidity ratio can be divided into the two types such as current ratio and acid

test ratio. Current ratio measures the relationship between current assets and current liabilities.

Current assets means those assets that are easily converted into the assets and current liabilities

means those assets that are payable within 12 months.

Year 2019

CR = current assets / current liabilities

= 1687 / 744

=2.27:1

Year 2018

CR = 418 / 502

0.83:1

Interpretation- It evaluates the capacity of the company to pay its short term liabilities. Ideal ratio

of the current assets is 2:1. But in the given question the current ratio of year 2019 is better than

as compare to year 2018. Because in 2019 the current ratio is also better than ideal ratio, it means

the liquidity of the company was better. But in 2018 company should increase the liquidity

position that they can pay its liabilities (Elie and et.al, 2021).

Acid test ratio – It shows the true liquidity position of the company. It evaluates the liquidity of

the short period. It evaluates the relationship among current assets after deduct stock divided by

current liabilities.

2019

= ( CA – stock) / current liabilities

= ( 1687 – 150) / 744

=2.06:1

2018

=(418 – 102) / 502

=316 / 502

=0.62:1

low. It means the company are not efficiency to used of assets in generation of sales. The ideal

ratio is 2.5 or more times. So that company must to improve their efficiency to earned more

revenue and proper utilisation of fixed assets and current assets (Boissay and et.al, 2021).

Current ratio – Liquidity ratio can be divided into the two types such as current ratio and acid

test ratio. Current ratio measures the relationship between current assets and current liabilities.

Current assets means those assets that are easily converted into the assets and current liabilities

means those assets that are payable within 12 months.

Year 2019

CR = current assets / current liabilities

= 1687 / 744

=2.27:1

Year 2018

CR = 418 / 502

0.83:1

Interpretation- It evaluates the capacity of the company to pay its short term liabilities. Ideal ratio

of the current assets is 2:1. But in the given question the current ratio of year 2019 is better than

as compare to year 2018. Because in 2019 the current ratio is also better than ideal ratio, it means

the liquidity of the company was better. But in 2018 company should increase the liquidity

position that they can pay its liabilities (Elie and et.al, 2021).

Acid test ratio – It shows the true liquidity position of the company. It evaluates the liquidity of

the short period. It evaluates the relationship among current assets after deduct stock divided by

current liabilities.

2019

= ( CA – stock) / current liabilities

= ( 1687 – 150) / 744

=2.06:1

2018

=(418 – 102) / 502

=316 / 502

=0.62:1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

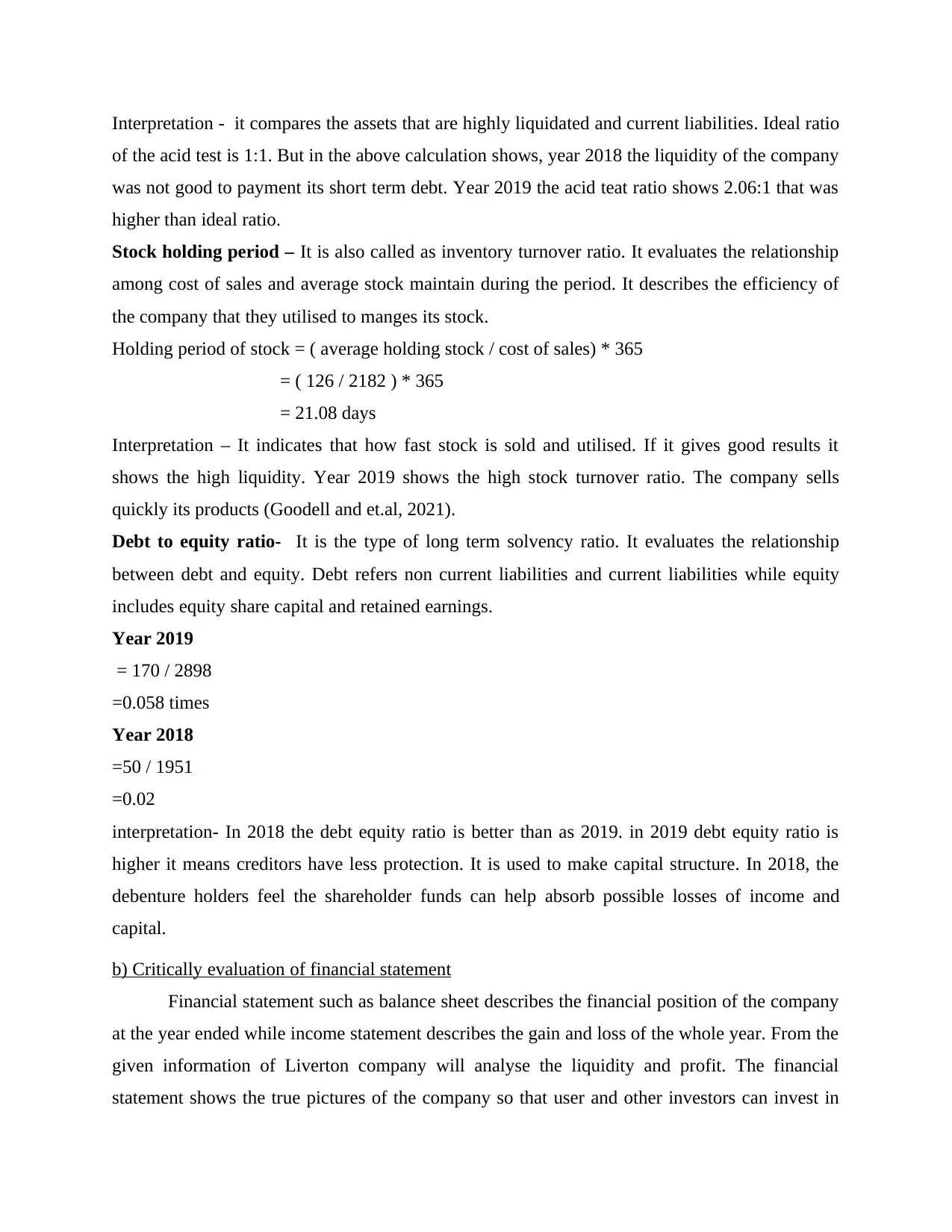

Interpretation - it compares the assets that are highly liquidated and current liabilities. Ideal ratio

of the acid test is 1:1. But in the above calculation shows, year 2018 the liquidity of the company

was not good to payment its short term debt. Year 2019 the acid teat ratio shows 2.06:1 that was

higher than ideal ratio.

Stock holding period – It is also called as inventory turnover ratio. It evaluates the relationship

among cost of sales and average stock maintain during the period. It describes the efficiency of

the company that they utilised to manges its stock.

Holding period of stock = ( average holding stock / cost of sales) * 365

= ( 126 / 2182 ) * 365

= 21.08 days

Interpretation – It indicates that how fast stock is sold and utilised. If it gives good results it

shows the high liquidity. Year 2019 shows the high stock turnover ratio. The company sells

quickly its products (Goodell and et.al, 2021).

Debt to equity ratio- It is the type of long term solvency ratio. It evaluates the relationship

between debt and equity. Debt refers non current liabilities and current liabilities while equity

includes equity share capital and retained earnings.

Year 2019

= 170 / 2898

=0.058 times

Year 2018

=50 / 1951

=0.02

interpretation- In 2018 the debt equity ratio is better than as 2019. in 2019 debt equity ratio is

higher it means creditors have less protection. It is used to make capital structure. In 2018, the

debenture holders feel the shareholder funds can help absorb possible losses of income and

capital.

b) Critically evaluation of financial statement

Financial statement such as balance sheet describes the financial position of the company

at the year ended while income statement describes the gain and loss of the whole year. From the

given information of Liverton company will analyse the liquidity and profit. The financial

statement shows the true pictures of the company so that user and other investors can invest in

of the acid test is 1:1. But in the above calculation shows, year 2018 the liquidity of the company

was not good to payment its short term debt. Year 2019 the acid teat ratio shows 2.06:1 that was

higher than ideal ratio.

Stock holding period – It is also called as inventory turnover ratio. It evaluates the relationship

among cost of sales and average stock maintain during the period. It describes the efficiency of

the company that they utilised to manges its stock.

Holding period of stock = ( average holding stock / cost of sales) * 365

= ( 126 / 2182 ) * 365

= 21.08 days

Interpretation – It indicates that how fast stock is sold and utilised. If it gives good results it

shows the high liquidity. Year 2019 shows the high stock turnover ratio. The company sells

quickly its products (Goodell and et.al, 2021).

Debt to equity ratio- It is the type of long term solvency ratio. It evaluates the relationship

between debt and equity. Debt refers non current liabilities and current liabilities while equity

includes equity share capital and retained earnings.

Year 2019

= 170 / 2898

=0.058 times

Year 2018

=50 / 1951

=0.02

interpretation- In 2018 the debt equity ratio is better than as 2019. in 2019 debt equity ratio is

higher it means creditors have less protection. It is used to make capital structure. In 2018, the

debenture holders feel the shareholder funds can help absorb possible losses of income and

capital.

b) Critically evaluation of financial statement

Financial statement such as balance sheet describes the financial position of the company

at the year ended while income statement describes the gain and loss of the whole year. From the

given information of Liverton company will analyse the liquidity and profit. The financial

statement shows the true pictures of the company so that user and other investors can invest in

the company. The income statement of Liverton company can be broken down into two

categories such as expenditures and incomes. The shareholders analyse the whole financial

statement because they invest in the company for long term. It provides the benefits of the

company in various types. It gives opportunities of the internal and external stakeholders to take

decision regarding investing. They also give information of borrowing institutions to tell about

the financial health of the company that is support to making borrowing decision. And as top

level management and other people of the company rely on financial to give a true depiction of

the effects of their decisions. It also helps solving the matter of corporate governance. It

increases the monetary role of the company by taking proper and suitable choice (Guild, 2020).

Question 2

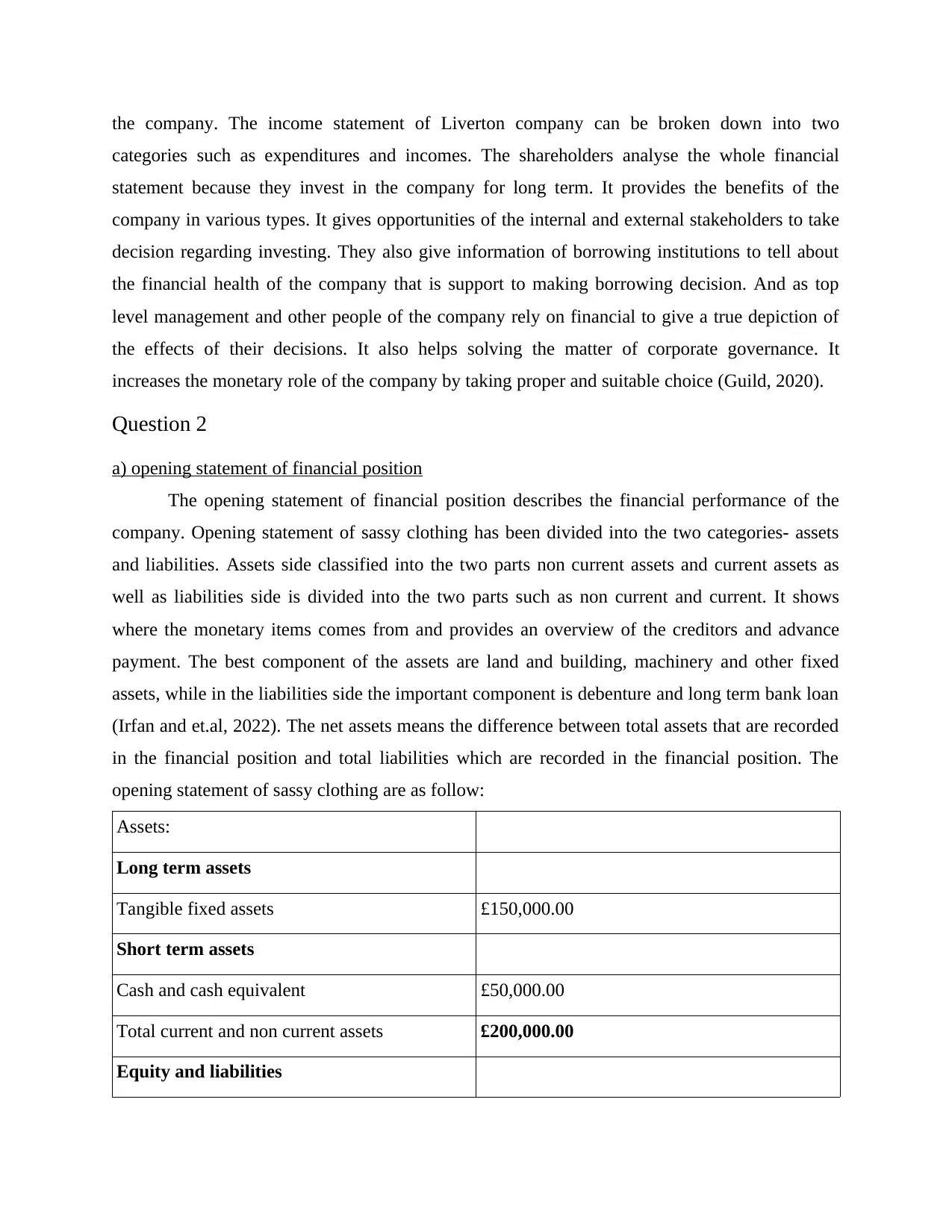

a) opening statement of financial position

The opening statement of financial position describes the financial performance of the

company. Opening statement of sassy clothing has been divided into the two categories- assets

and liabilities. Assets side classified into the two parts non current assets and current assets as

well as liabilities side is divided into the two parts such as non current and current. It shows

where the monetary items comes from and provides an overview of the creditors and advance

payment. The best component of the assets are land and building, machinery and other fixed

assets, while in the liabilities side the important component is debenture and long term bank loan

(Irfan and et.al, 2022). The net assets means the difference between total assets that are recorded

in the financial position and total liabilities which are recorded in the financial position. The

opening statement of sassy clothing are as follow:

Assets:

Long term assets

Tangible fixed assets £150,000.00

Short term assets

Cash and cash equivalent £50,000.00

Total current and non current assets £200,000.00

Equity and liabilities

categories such as expenditures and incomes. The shareholders analyse the whole financial

statement because they invest in the company for long term. It provides the benefits of the

company in various types. It gives opportunities of the internal and external stakeholders to take

decision regarding investing. They also give information of borrowing institutions to tell about

the financial health of the company that is support to making borrowing decision. And as top

level management and other people of the company rely on financial to give a true depiction of

the effects of their decisions. It also helps solving the matter of corporate governance. It

increases the monetary role of the company by taking proper and suitable choice (Guild, 2020).

Question 2

a) opening statement of financial position

The opening statement of financial position describes the financial performance of the

company. Opening statement of sassy clothing has been divided into the two categories- assets

and liabilities. Assets side classified into the two parts non current assets and current assets as

well as liabilities side is divided into the two parts such as non current and current. It shows

where the monetary items comes from and provides an overview of the creditors and advance

payment. The best component of the assets are land and building, machinery and other fixed

assets, while in the liabilities side the important component is debenture and long term bank loan

(Irfan and et.al, 2022). The net assets means the difference between total assets that are recorded

in the financial position and total liabilities which are recorded in the financial position. The

opening statement of sassy clothing are as follow:

Assets:

Long term assets

Tangible fixed assets £150,000.00

Short term assets

Cash and cash equivalent £50,000.00

Total current and non current assets £200,000.00

Equity and liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital £200,000.00

Total equity and liabilities £200,000.00

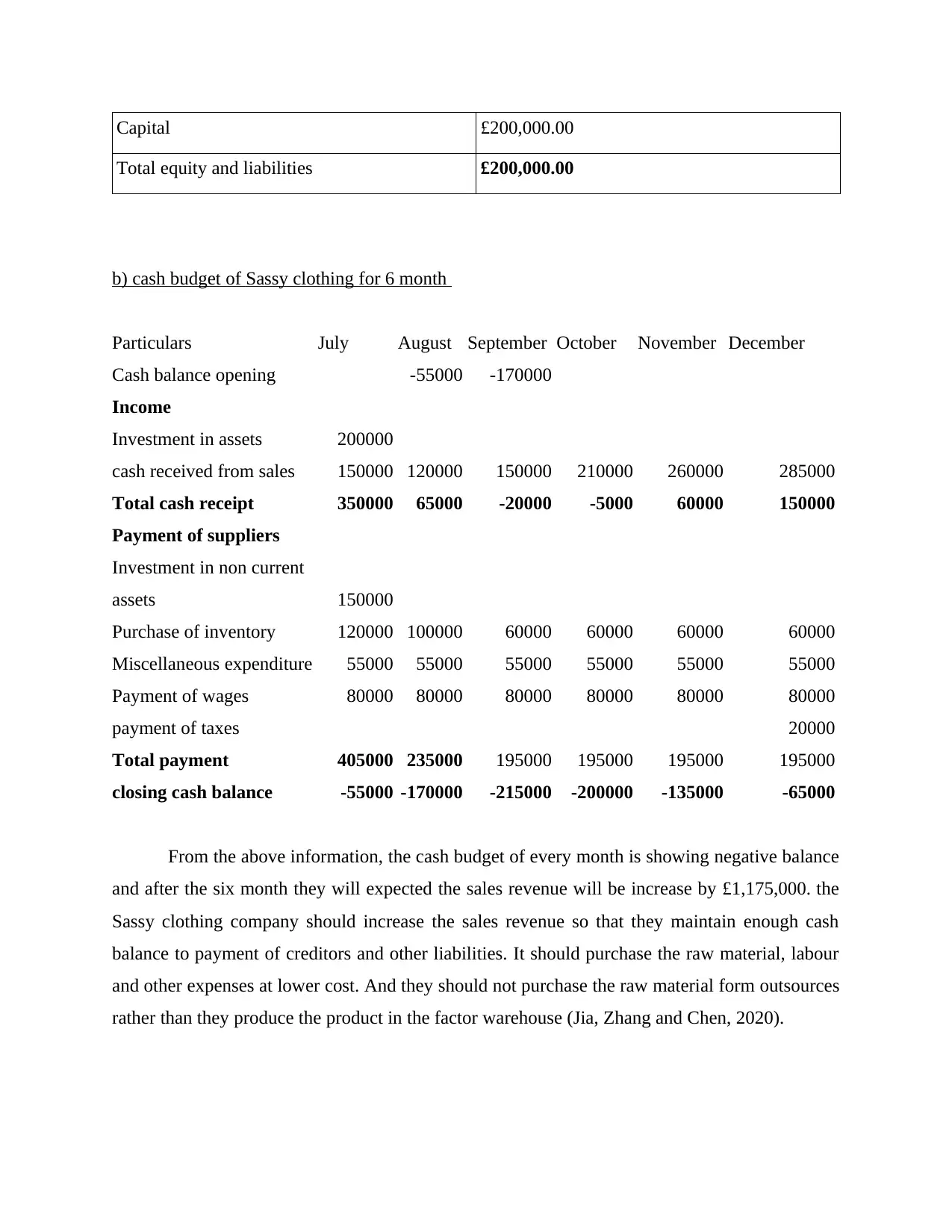

b) cash budget of Sassy clothing for 6 month

Particulars July August September October November December

Cash balance opening -55000 -170000

Income

Investment in assets 200000

cash received from sales 150000 120000 150000 210000 260000 285000

Total cash receipt 350000 65000 -20000 -5000 60000 150000

Payment of suppliers

Investment in non current

assets 150000

Purchase of inventory 120000 100000 60000 60000 60000 60000

Miscellaneous expenditure 55000 55000 55000 55000 55000 55000

Payment of wages 80000 80000 80000 80000 80000 80000

payment of taxes 20000

Total payment 405000 235000 195000 195000 195000 195000

closing cash balance -55000 -170000 -215000 -200000 -135000 -65000

From the above information, the cash budget of every month is showing negative balance

and after the six month they will expected the sales revenue will be increase by £1,175,000. the

Sassy clothing company should increase the sales revenue so that they maintain enough cash

balance to payment of creditors and other liabilities. It should purchase the raw material, labour

and other expenses at lower cost. And they should not purchase the raw material form outsources

rather than they produce the product in the factor warehouse (Jia, Zhang and Chen, 2020).

Total equity and liabilities £200,000.00

b) cash budget of Sassy clothing for 6 month

Particulars July August September October November December

Cash balance opening -55000 -170000

Income

Investment in assets 200000

cash received from sales 150000 120000 150000 210000 260000 285000

Total cash receipt 350000 65000 -20000 -5000 60000 150000

Payment of suppliers

Investment in non current

assets 150000

Purchase of inventory 120000 100000 60000 60000 60000 60000

Miscellaneous expenditure 55000 55000 55000 55000 55000 55000

Payment of wages 80000 80000 80000 80000 80000 80000

payment of taxes 20000

Total payment 405000 235000 195000 195000 195000 195000

closing cash balance -55000 -170000 -215000 -200000 -135000 -65000

From the above information, the cash budget of every month is showing negative balance

and after the six month they will expected the sales revenue will be increase by £1,175,000. the

Sassy clothing company should increase the sales revenue so that they maintain enough cash

balance to payment of creditors and other liabilities. It should purchase the raw material, labour

and other expenses at lower cost. And they should not purchase the raw material form outsources

rather than they produce the product in the factor warehouse (Jia, Zhang and Chen, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c) Critical analyse of additional expenditures

In the month f July and December, company need to make additional expenditures such

as ware house rent, electricity bill and running fees. The overdraft balance shows the company

have not sufficient bank balance to payment of liabilities but payment has also made by bank. It

keeps good financial position of the company. With the help of overdraft the owners is maintain

of do bills in their expenses on time (Khan and et.al, 2021).

Question 3

a) Analysis of Break even point

Break even point- The break even point is the point at which the total revenues and the

cost are equal. This actually means that there is no gain or no loss. It is the level at which the

total production cost is equal to the total revenues of the product. For every company, this is the

most important analysis in the quantitative terms. It is a management tool used internally. This

information is mostly shares with the external stakeholders like investors or regulators. The

potential investors always want to know that in how much period they will get return. As they

will plan their further return or investment in the same company. A break even point analysis

helps in determining the required number of units or the dollars. This is required for covering the

total costs. The total costs includes both fixed and variable costs. The variable costs are changed

according to the changes in the sales. While the fixed costs remains the same throughout the

sales. The variable costs includes the labour, raw materials and all those costs that are needed to

produce a single unit. The break even point is usually measured in the new businesses or start

ups. As after this level the company try to reduces its cost and focuses on earning the profits. In

investment terms, the market price of an asset is equal to its original cost. This point also proves

the potential of any company to face the disastrous scenarios (Parrado-Martínez and et.al, 2020).

The company is expected to be at break even scale within the months or in few years. If it takes

more time then it will be risky.

Calculate in units of BEP = fixed cost / contribution per unit

Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

In the month f July and December, company need to make additional expenditures such

as ware house rent, electricity bill and running fees. The overdraft balance shows the company

have not sufficient bank balance to payment of liabilities but payment has also made by bank. It

keeps good financial position of the company. With the help of overdraft the owners is maintain

of do bills in their expenses on time (Khan and et.al, 2021).

Question 3

a) Analysis of Break even point

Break even point- The break even point is the point at which the total revenues and the

cost are equal. This actually means that there is no gain or no loss. It is the level at which the

total production cost is equal to the total revenues of the product. For every company, this is the

most important analysis in the quantitative terms. It is a management tool used internally. This

information is mostly shares with the external stakeholders like investors or regulators. The

potential investors always want to know that in how much period they will get return. As they

will plan their further return or investment in the same company. A break even point analysis

helps in determining the required number of units or the dollars. This is required for covering the

total costs. The total costs includes both fixed and variable costs. The variable costs are changed

according to the changes in the sales. While the fixed costs remains the same throughout the

sales. The variable costs includes the labour, raw materials and all those costs that are needed to

produce a single unit. The break even point is usually measured in the new businesses or start

ups. As after this level the company try to reduces its cost and focuses on earning the profits. In

investment terms, the market price of an asset is equal to its original cost. This point also proves

the potential of any company to face the disastrous scenarios (Parrado-Martínez and et.al, 2020).

The company is expected to be at break even scale within the months or in few years. If it takes

more time then it will be risky.

Calculate in units of BEP = fixed cost / contribution per unit

Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

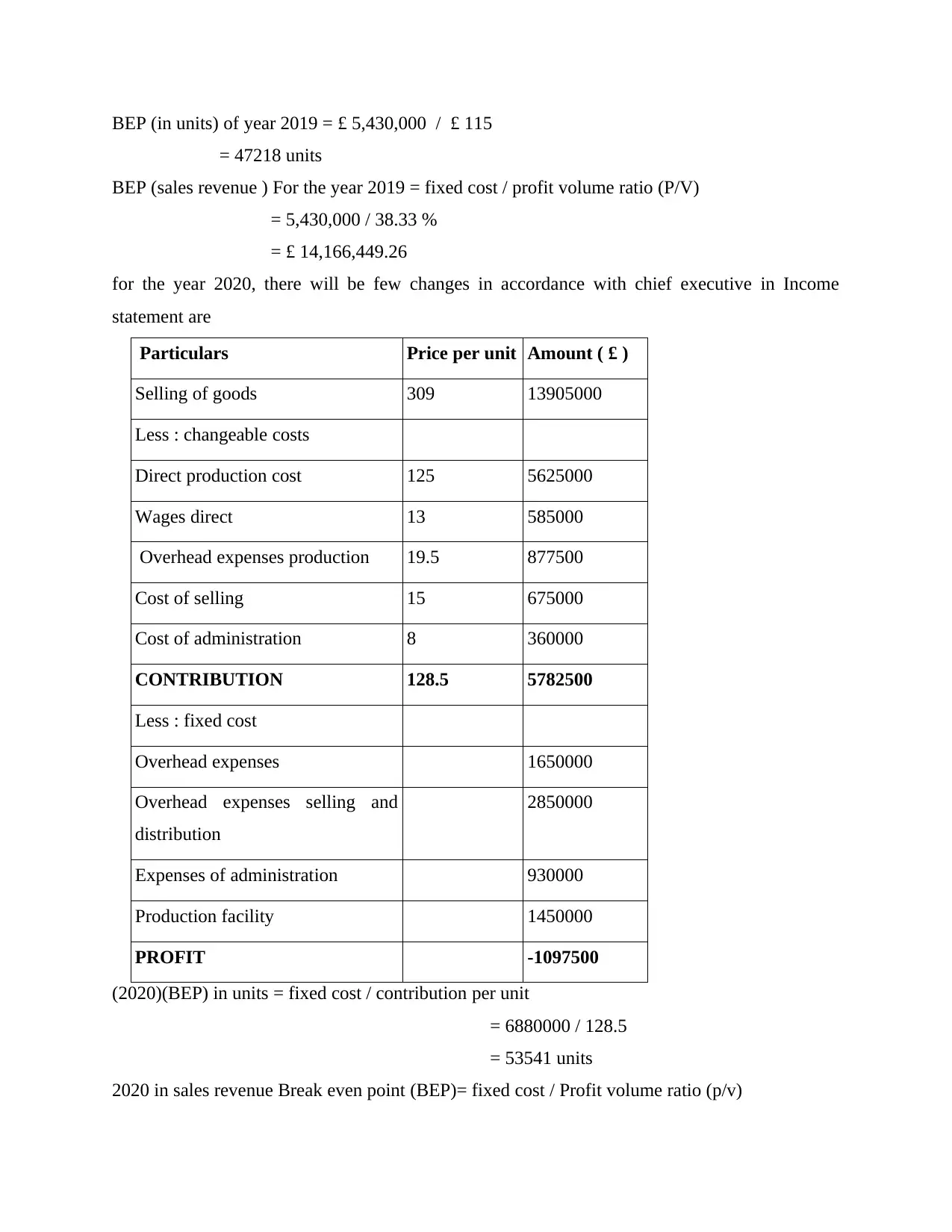

BEP (in units) of year 2019 = £ 5,430,000 / £ 115

= 47218 units

BEP (sales revenue ) For the year 2019 = fixed cost / profit volume ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

for the year 2020, there will be few changes in accordance with chief executive in Income

statement are

Particulars Price per unit Amount ( £ )

Selling of goods 309 13905000

Less : changeable costs

Direct production cost 125 5625000

Wages direct 13 585000

Overhead expenses production 19.5 877500

Cost of selling 15 675000

Cost of administration 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Overhead expenses 1650000

Overhead expenses selling and

distribution

2850000

Expenses of administration 930000

Production facility 1450000

PROFIT -1097500

(2020)(BEP) in units = fixed cost / contribution per unit

= 6880000 / 128.5

= 53541 units

2020 in sales revenue Break even point (BEP)= fixed cost / Profit volume ratio (p/v)

= 47218 units

BEP (sales revenue ) For the year 2019 = fixed cost / profit volume ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

for the year 2020, there will be few changes in accordance with chief executive in Income

statement are

Particulars Price per unit Amount ( £ )

Selling of goods 309 13905000

Less : changeable costs

Direct production cost 125 5625000

Wages direct 13 585000

Overhead expenses production 19.5 877500

Cost of selling 15 675000

Cost of administration 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Overhead expenses 1650000

Overhead expenses selling and

distribution

2850000

Expenses of administration 930000

Production facility 1450000

PROFIT -1097500

(2020)(BEP) in units = fixed cost / contribution per unit

= 6880000 / 128.5

= 53541 units

2020 in sales revenue Break even point (BEP)= fixed cost / Profit volume ratio (p/v)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 6880000 / 41.59 %

= £ 16542438.09

b) 2019 and 2020 Margin of safety ( MOS )

Margin of safety- The margin of safety is the point at which the amount of sales have

exceeded the break even point. This is the financial ratio that shows the profit which the

company is actually earning. It is calculated after the company pays all the variable and the fixed

costs. If any company reached the margin of safety before the break even point. This is actually

the point below which the company loses. Then it means that there is a risk of loss. This

identifies the particular level of the sales. That level should be identified and would be declined

or eliminated. This is measured as the difference between the actual sales and the break even

sales. This is a measure which is used in the company where the large portion of the sales are at

risk. And the company has only few customers (Ruan and et.al, 2019). It may leads to the

cancellation of the contracts. Accordingly the company may change its promotional and

marketing strategies. This also helps in the analyses and the expansion of the inventory. The

margin of safety is the financial ratio that helps in forming the judgement of the analyst. And

also in the prevention of the errors. The margin of safety is not beneficial for the business that

have inconsistent sales. For any business, the higher margin of safety is good. This level varies

from company to company (Wang and et.al, 2022).

For the year 2019 MOS in terms of units = profit / contribution per unit

= -255000 / 115

= - 2217 units

Units MOS for the year 2020 = -1097500 / 128.5

= -8541 units

For the year 2019 MOS in terms of sales revenue = profit / p/v ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of sales revenue for the year 2020 = profit / p/v ratio

= -1097500 / 41.59 %

= £-2638855.49

= £ 16542438.09

b) 2019 and 2020 Margin of safety ( MOS )

Margin of safety- The margin of safety is the point at which the amount of sales have

exceeded the break even point. This is the financial ratio that shows the profit which the

company is actually earning. It is calculated after the company pays all the variable and the fixed

costs. If any company reached the margin of safety before the break even point. This is actually

the point below which the company loses. Then it means that there is a risk of loss. This

identifies the particular level of the sales. That level should be identified and would be declined

or eliminated. This is measured as the difference between the actual sales and the break even

sales. This is a measure which is used in the company where the large portion of the sales are at

risk. And the company has only few customers (Ruan and et.al, 2019). It may leads to the

cancellation of the contracts. Accordingly the company may change its promotional and

marketing strategies. This also helps in the analyses and the expansion of the inventory. The

margin of safety is the financial ratio that helps in forming the judgement of the analyst. And

also in the prevention of the errors. The margin of safety is not beneficial for the business that

have inconsistent sales. For any business, the higher margin of safety is good. This level varies

from company to company (Wang and et.al, 2022).

For the year 2019 MOS in terms of units = profit / contribution per unit

= -255000 / 115

= - 2217 units

Units MOS for the year 2020 = -1097500 / 128.5

= -8541 units

For the year 2019 MOS in terms of sales revenue = profit / p/v ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of sales revenue for the year 2020 = profit / p/v ratio

= -1097500 / 41.59 %

= £-2638855.49

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

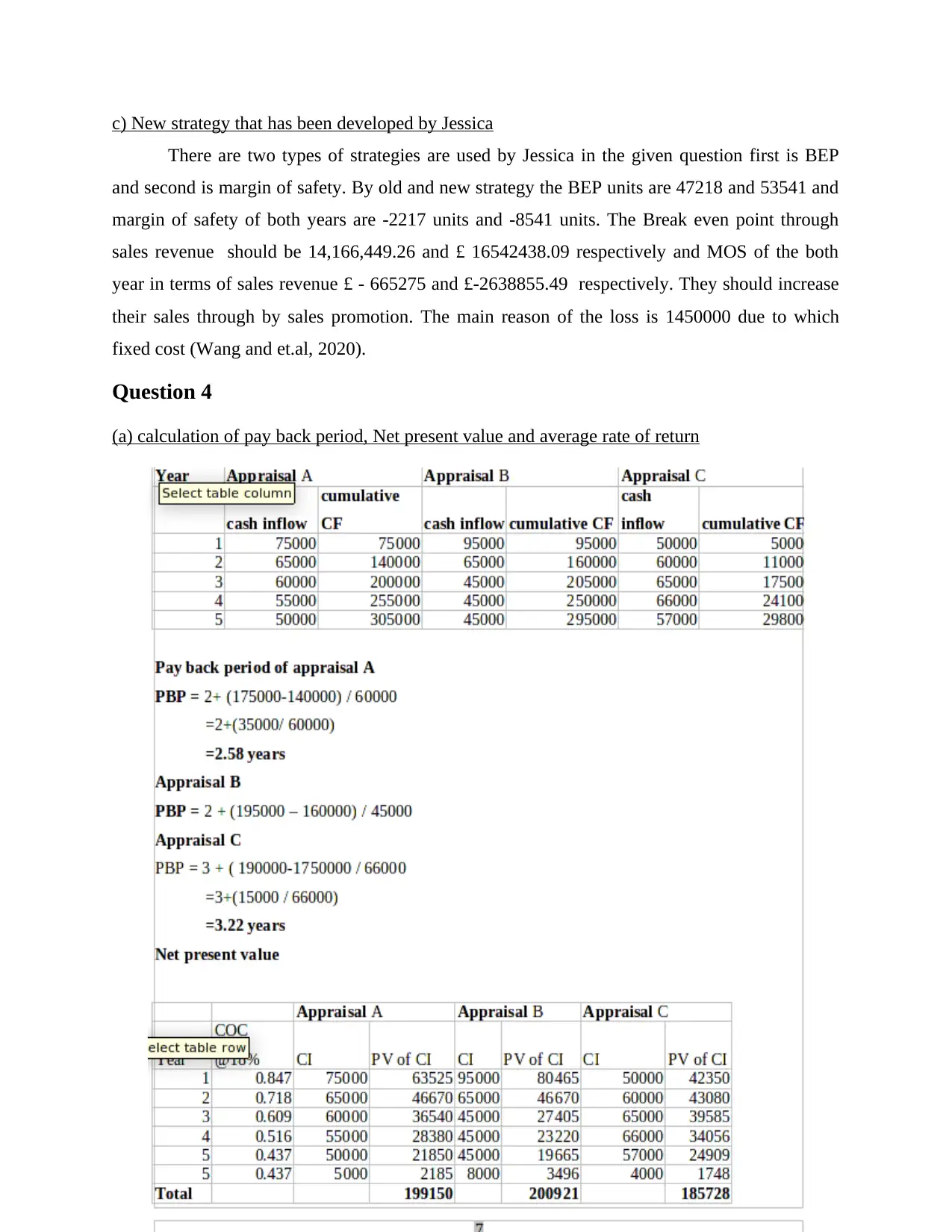

c) New strategy that has been developed by Jessica

There are two types of strategies are used by Jessica in the given question first is BEP

and second is margin of safety. By old and new strategy the BEP units are 47218 and 53541 and

margin of safety of both years are -2217 units and -8541 units. The Break even point through

sales revenue should be 14,166,449.26 and £ 16542438.09 respectively and MOS of the both

year in terms of sales revenue £ - 665275 and £-2638855.49 respectively. They should increase

their sales through by sales promotion. The main reason of the loss is 1450000 due to which

fixed cost (Wang and et.al, 2020).

Question 4

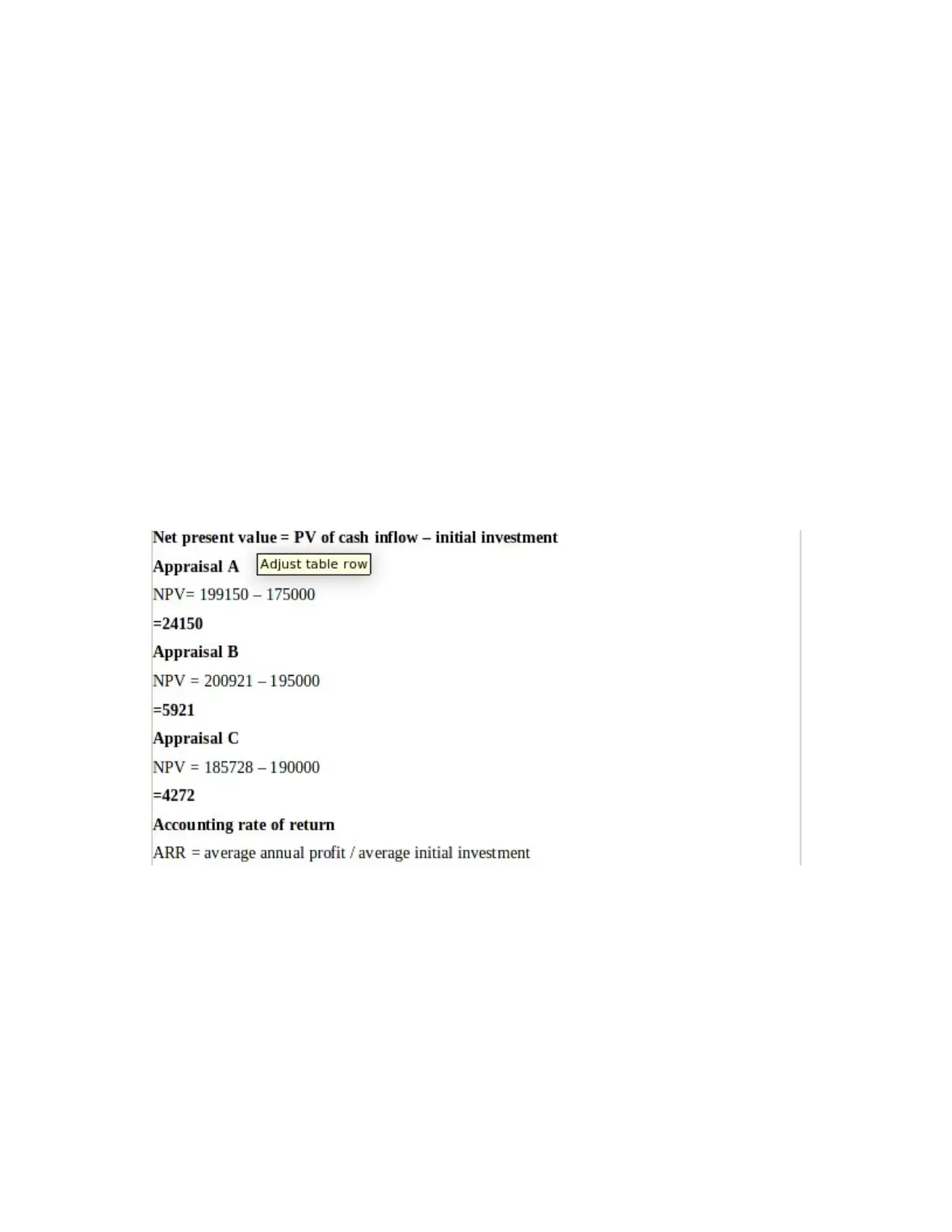

(a) calculation of pay back period, Net present value and average rate of return

There are two types of strategies are used by Jessica in the given question first is BEP

and second is margin of safety. By old and new strategy the BEP units are 47218 and 53541 and

margin of safety of both years are -2217 units and -8541 units. The Break even point through

sales revenue should be 14,166,449.26 and £ 16542438.09 respectively and MOS of the both

year in terms of sales revenue £ - 665275 and £-2638855.49 respectively. They should increase

their sales through by sales promotion. The main reason of the loss is 1450000 due to which

fixed cost (Wang and et.al, 2020).

Question 4

(a) calculation of pay back period, Net present value and average rate of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.