Advanced Finance Homework: Investment and Valuation Analysis

VerifiedAdded on 2023/06/07

|11

|2265

|169

Homework Assignment

AI Summary

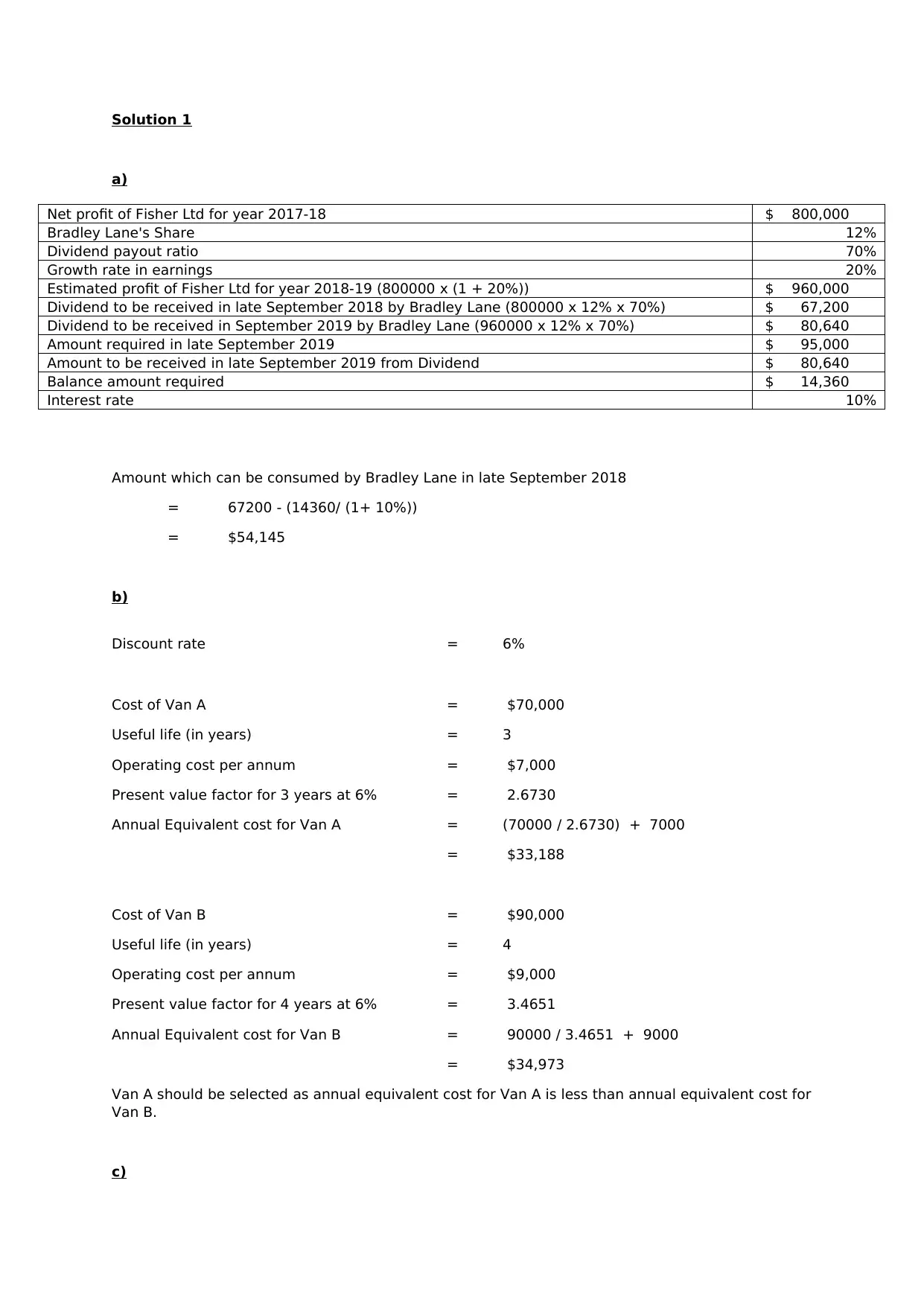

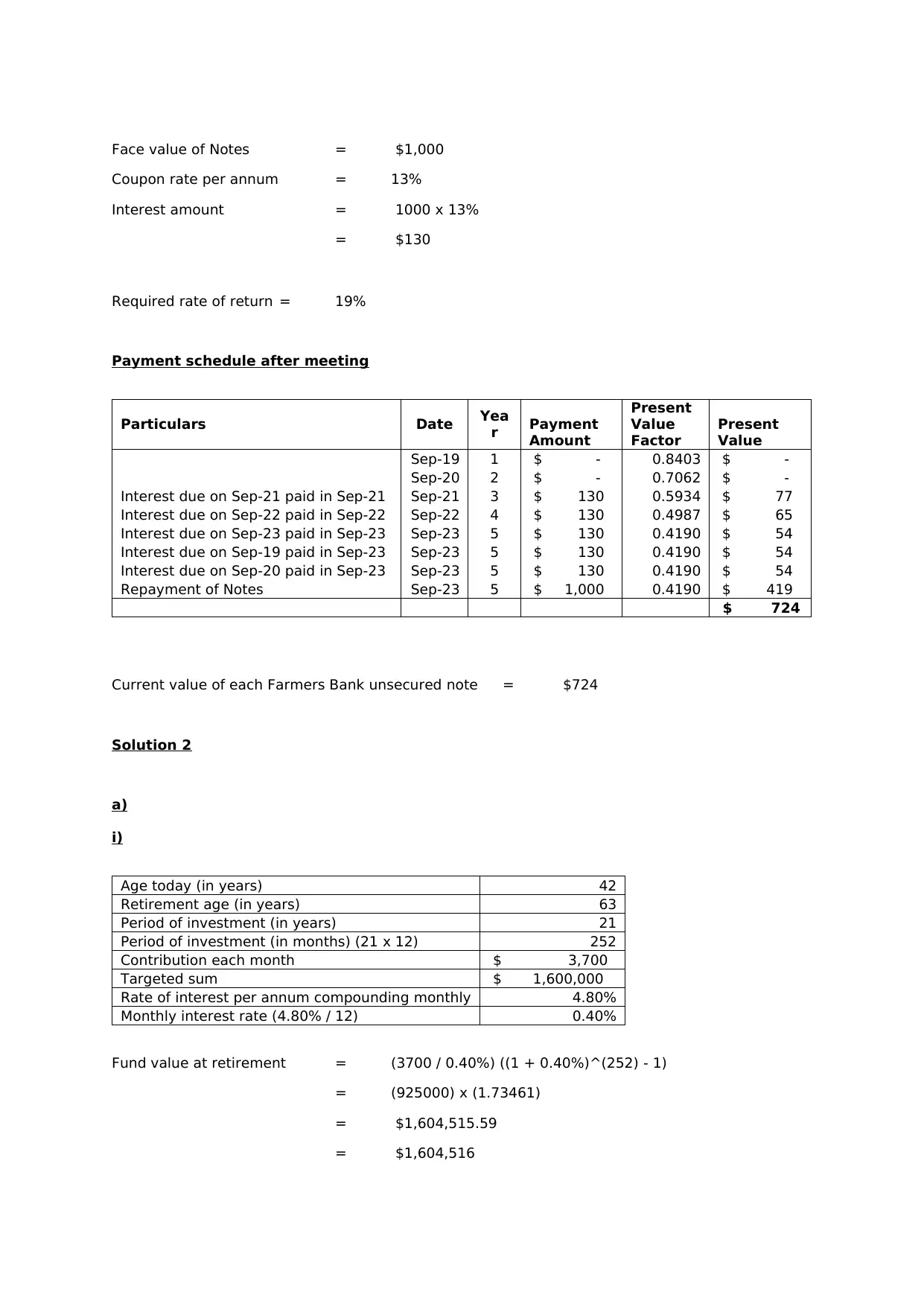

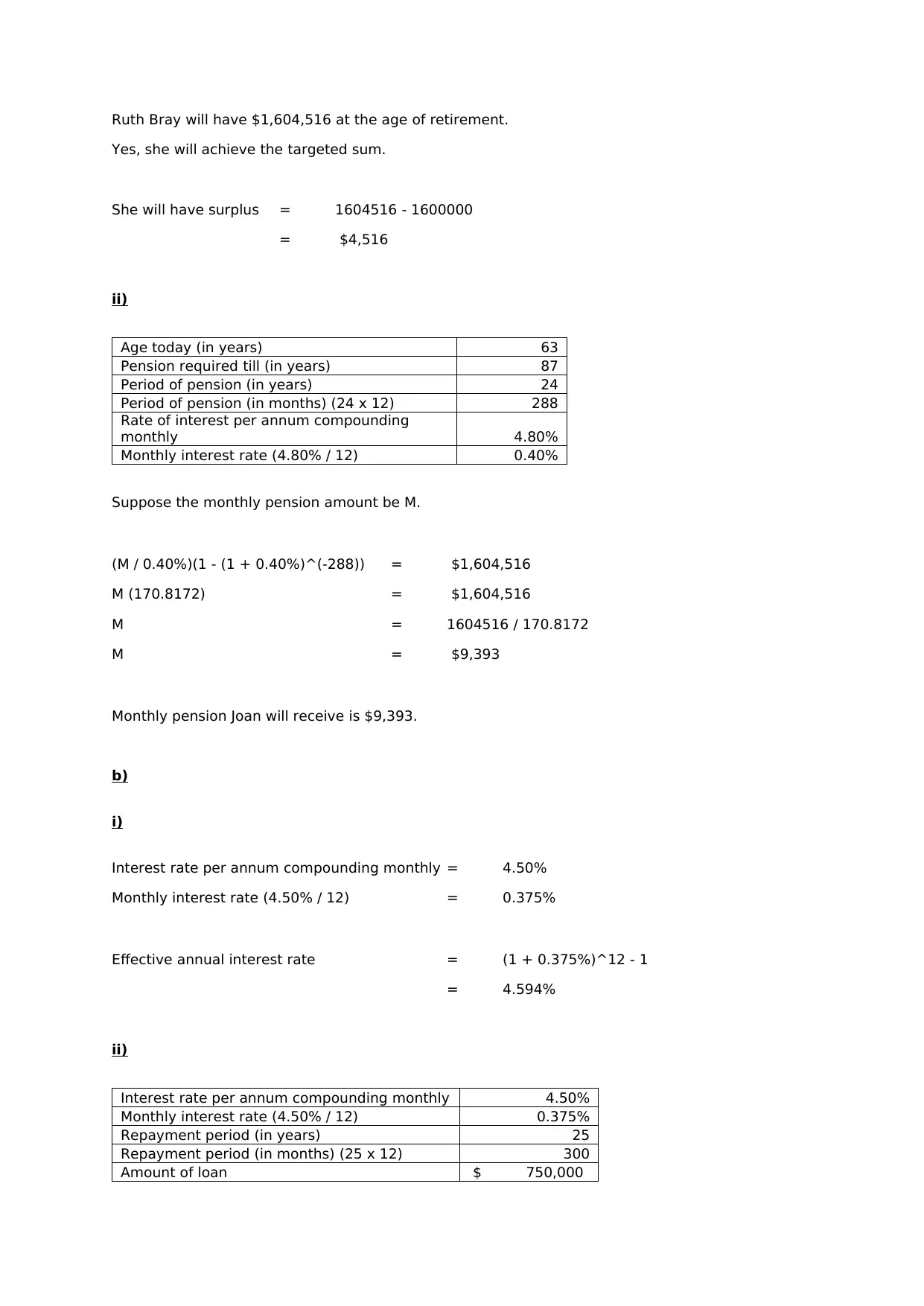

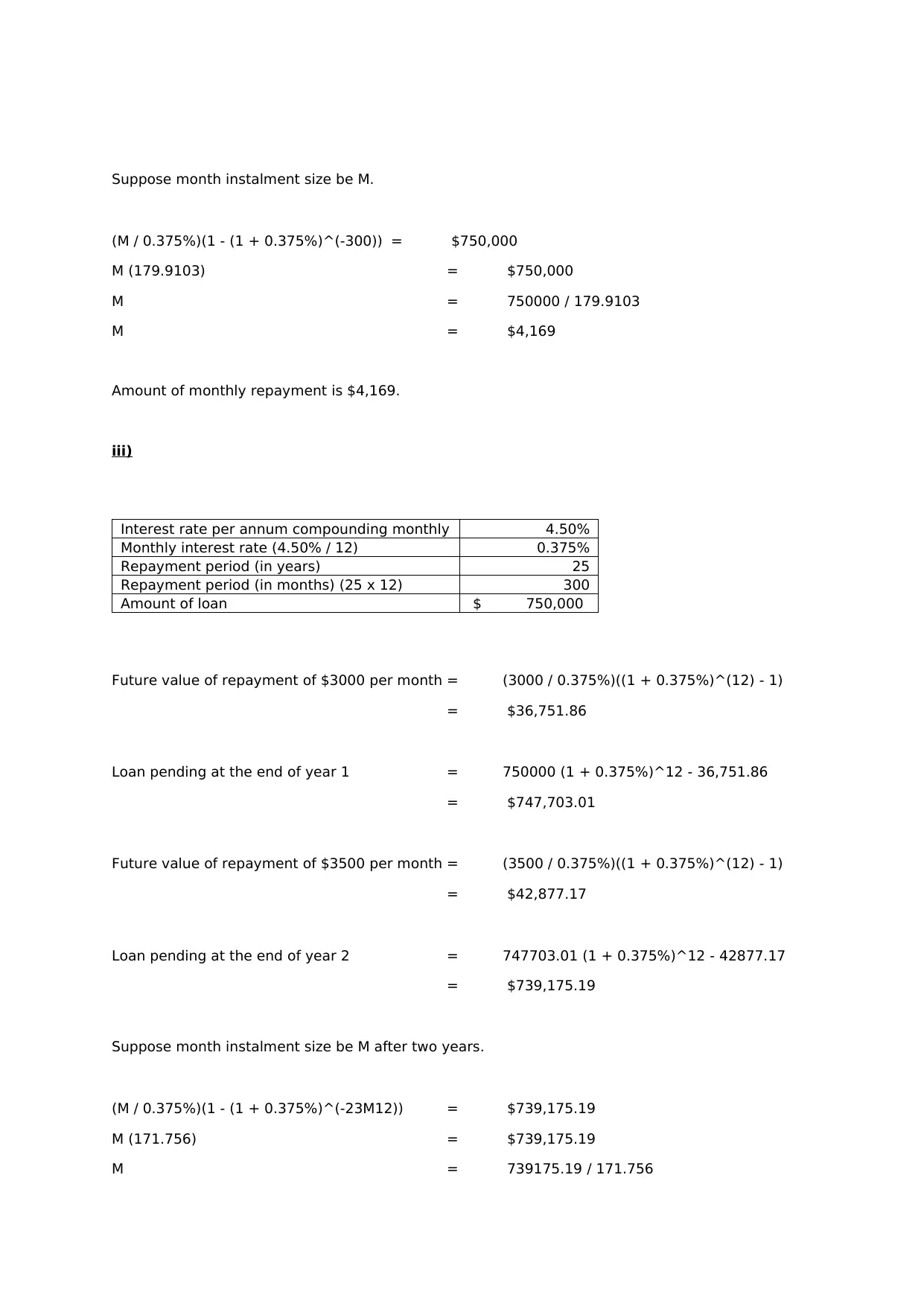

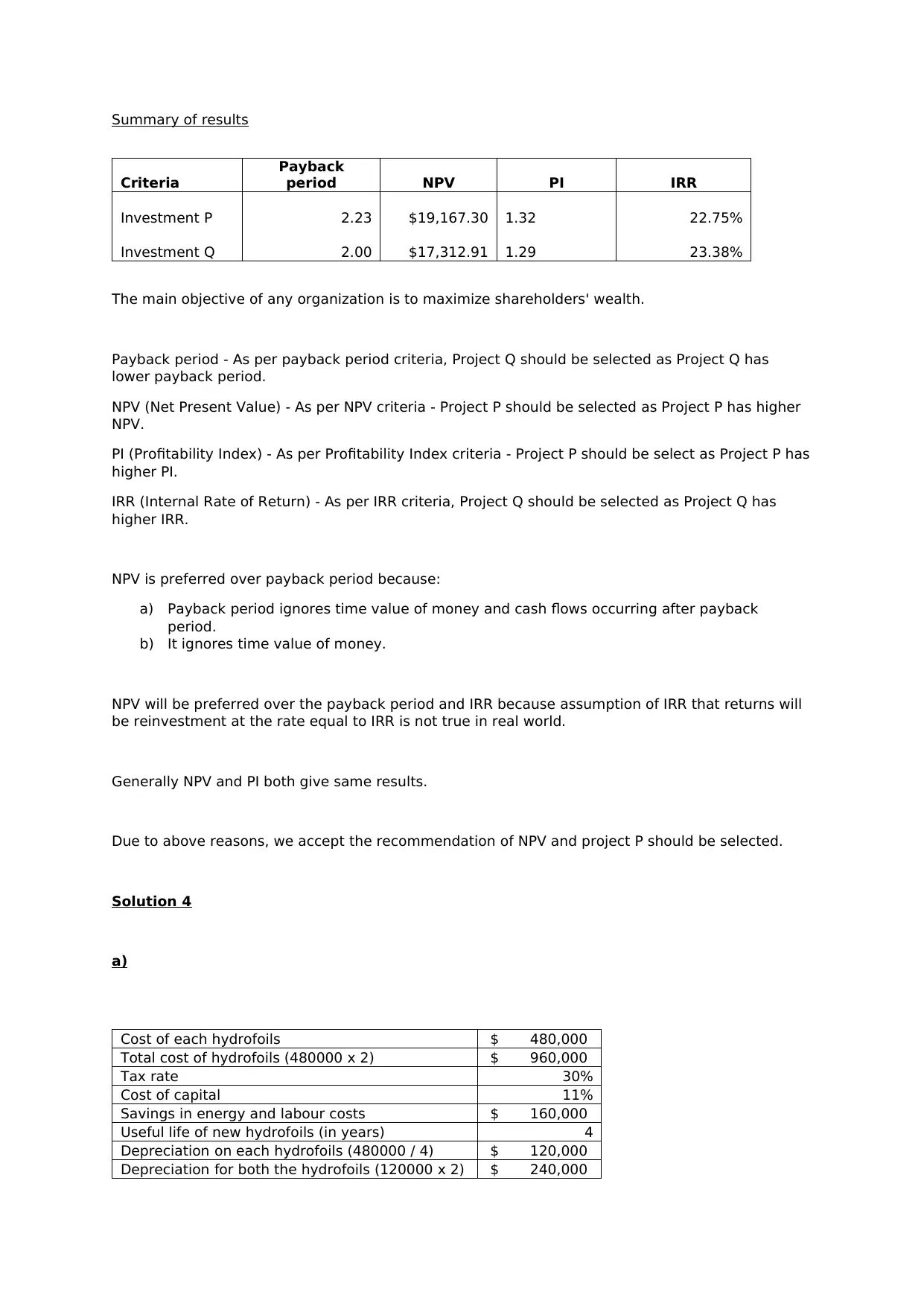

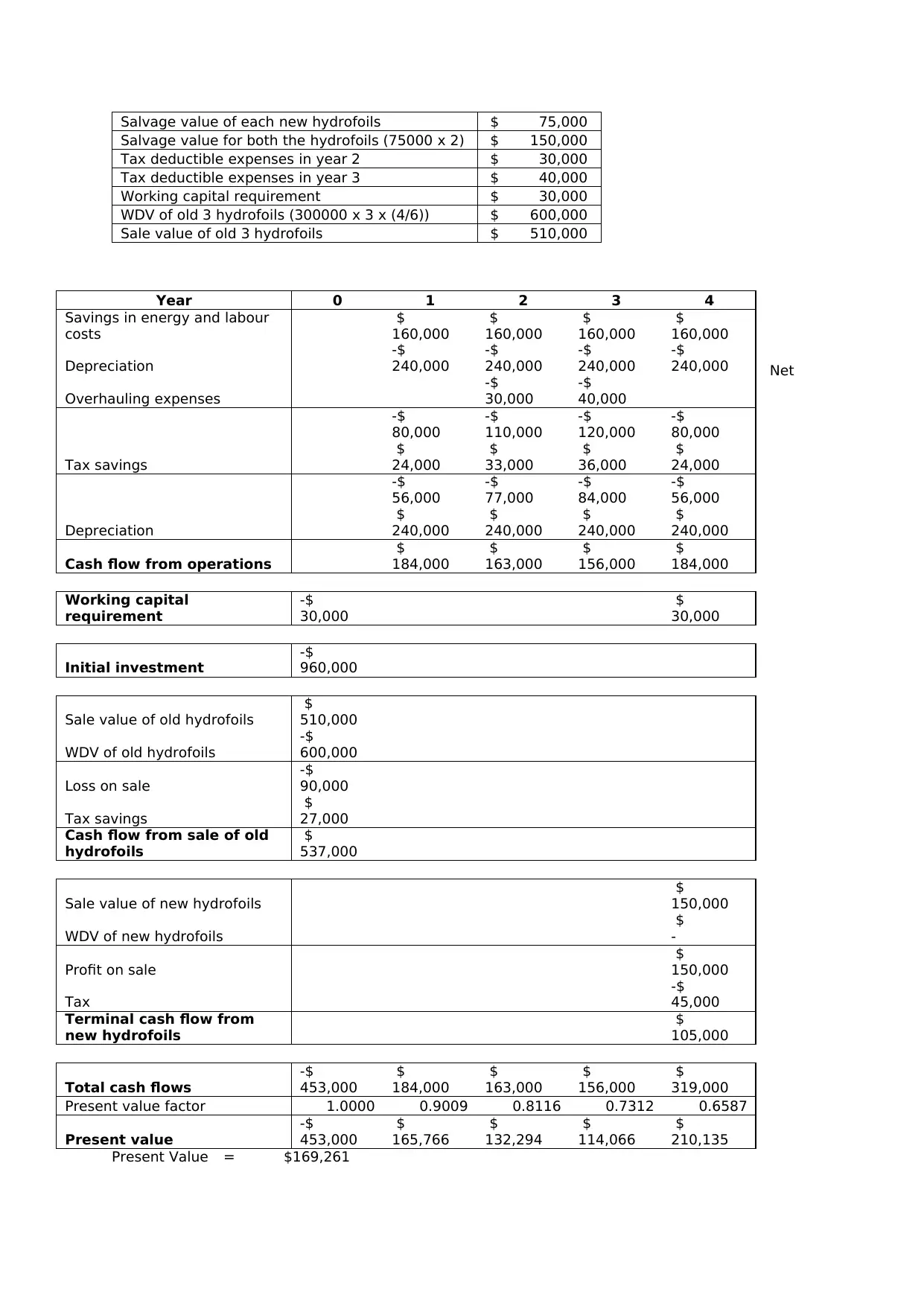

This document presents a comprehensive solution to a finance assignment, covering various financial concepts and calculations. The solution includes detailed calculations for net profit, dividend payouts, and growth rates. It analyzes investment decisions using annual equivalent costs, evaluates the present value of notes, and addresses retirement planning and loan repayment scenarios. The assignment also delves into capital budgeting techniques, such as payback period, net present value (NPV), profitability index (PI), and internal rate of return (IRR), to evaluate investment projects. Furthermore, the solution provides a detailed analysis of a hydrofoil investment, considering depreciation, tax implications, and cash flow analysis to determine the net present value and make informed investment recommendations. The document provides students with a valuable resource for understanding financial concepts and solving complex problems.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.