Financial Analysis Management Report: Astro Malaysia Holdings Berhad

VerifiedAdded on 2023/06/15

|23

|6174

|325

Report

AI Summary

This report provides a comprehensive financial analysis of Astro Malaysia Holdings Berhad, a Malaysian media and entertainment company. It begins by detailing the company's background, market presence, and the dynamics of the Malaysian mass media and entertainment industry, including regulatory restrictions and the shift from old to new media. The report then evaluates the company's financial performance over five years, focusing on profitability (gross and net profit margins), liquidity (times interest earned ratio), efficiency, capital structure, investor returns, and cash flows. Key drivers of change affecting Astro Malaysia Holdings are identified as consumer behavior, regulatory changes, technological advancements, and macroeconomic conditions. The analysis uses financial ratios and graphs to illustrate trends and provides insights into the company's strengths and areas for improvement. This report is useful for investors and those interested in the financial health and strategic challenges of media companies in Malaysia. Desklib provides access to similar solved assignments and past papers for students.

Running head: FINANCIAL ANALYSIS MANAGEMENT

Financial Analysis Management

Name of the Student

Name of the University

Author’s Note

Financial Analysis Management

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS MANAGEMENT

Table of Contents

Company and Market Details..........................................................................................................2

Industry Dynamics and Drivers of Change.....................................................................................3

Evaluation of Financial Performance..............................................................................................5

Profitability Analysis...................................................................................................................5

Liquidity Position Analysis.........................................................................................................7

Efficiency Analysis......................................................................................................................9

Capital Structure Analysis.........................................................................................................11

Investor Return Analysis...........................................................................................................13

Analysis of Cash Flows.................................................................................................................14

References......................................................................................................................................17

Appendix........................................................................................................................................20

Table of Contents

Company and Market Details..........................................................................................................2

Industry Dynamics and Drivers of Change.....................................................................................3

Evaluation of Financial Performance..............................................................................................5

Profitability Analysis...................................................................................................................5

Liquidity Position Analysis.........................................................................................................7

Efficiency Analysis......................................................................................................................9

Capital Structure Analysis.........................................................................................................11

Investor Return Analysis...........................................................................................................13

Analysis of Cash Flows.................................................................................................................14

References......................................................................................................................................17

Appendix........................................................................................................................................20

2FINANCIAL ANALYSIS MANAGEMENT

Company and Market Details

Astro Malaysia Holdings Berhad is a media and entertainment Company operates in the

regions of Malaysia. More specifically, it can be said that Astro Malaysia Holdings is a

Malaysian and ASEAN consumer and content company (corporate.astro.com.my 2018). In the

recent years, the company has taken strong commitment towards becoming a technology-driven

business organization in the TV, digital, e-commerce and radio space. The company was

established in the year of 1996 and it is headquartered at Technology Park Malaysia, Kuala

Lumpur, Malaysia. The main products of the company are pay television, broadcasting and

publishing. Astro Malaysia Holdings has a customer base of 5.8 million that is considered as the

71% of the total household of Malaysia. The company offers vast range of media and

entertainment spanning across different digital media, television, radio and home shopping to

almost 21 million individuals (corporate.astro.com.my 2018). The major value propositions of

Astro Malaysia Holdings includes the broadcast of 188 TV channels via DTH Satellite TV, OTT

and IPTV platforms; among all these, 60 includes in the brand of Astro and 72 are HD. Apart

from this, the company also offers various other services like HD, PVR, OD, IPTV and many

others. In this context, it needs to be mentioned that the main aim of the company is to originate

and create excellent content for consumption in the different regions of Malaysia. Astro Malaysia

Holdings has won different awards for their different products and services. The company has

won Gold Award in the category of media and entertainment of the Putra Brand Awards for the

last six years. Apart from this, the company has also won Brand of the Year award and Brand

Icon award in the year 2012 and 2013 respectively (corporate.astro.com.my 2018).

The mass media and entertainment industry of Malaysia is considered as a major industry

of the company as it contributes significantly towards the economic development of the country.

The government of Malaysia and the ruling political party control the mass media and

entertainment industry. Thus, all the mass media and entertainment companies of Malaysia need

to acquire business license from the government of the company and the licenses are required to

be renewed at regular period (factsanddetails.com 2018). In most of the cases, the mainstream

mass media is pro-government. Most importantly, the media and entertainment industry of

Malaysia is subject to various legal restrictions. In 1998, the implementation of Communications

Company and Market Details

Astro Malaysia Holdings Berhad is a media and entertainment Company operates in the

regions of Malaysia. More specifically, it can be said that Astro Malaysia Holdings is a

Malaysian and ASEAN consumer and content company (corporate.astro.com.my 2018). In the

recent years, the company has taken strong commitment towards becoming a technology-driven

business organization in the TV, digital, e-commerce and radio space. The company was

established in the year of 1996 and it is headquartered at Technology Park Malaysia, Kuala

Lumpur, Malaysia. The main products of the company are pay television, broadcasting and

publishing. Astro Malaysia Holdings has a customer base of 5.8 million that is considered as the

71% of the total household of Malaysia. The company offers vast range of media and

entertainment spanning across different digital media, television, radio and home shopping to

almost 21 million individuals (corporate.astro.com.my 2018). The major value propositions of

Astro Malaysia Holdings includes the broadcast of 188 TV channels via DTH Satellite TV, OTT

and IPTV platforms; among all these, 60 includes in the brand of Astro and 72 are HD. Apart

from this, the company also offers various other services like HD, PVR, OD, IPTV and many

others. In this context, it needs to be mentioned that the main aim of the company is to originate

and create excellent content for consumption in the different regions of Malaysia. Astro Malaysia

Holdings has won different awards for their different products and services. The company has

won Gold Award in the category of media and entertainment of the Putra Brand Awards for the

last six years. Apart from this, the company has also won Brand of the Year award and Brand

Icon award in the year 2012 and 2013 respectively (corporate.astro.com.my 2018).

The mass media and entertainment industry of Malaysia is considered as a major industry

of the company as it contributes significantly towards the economic development of the country.

The government of Malaysia and the ruling political party control the mass media and

entertainment industry. Thus, all the mass media and entertainment companies of Malaysia need

to acquire business license from the government of the company and the licenses are required to

be renewed at regular period (factsanddetails.com 2018). In most of the cases, the mainstream

mass media is pro-government. Most importantly, the media and entertainment industry of

Malaysia is subject to various legal restrictions. In 1998, the implementation of Communications

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS MANAGEMENT

and Multimedia Act liberalized acceptable broadcast content. In this context, it needs to be

mentioned that various acts like media and press acts, Internal Security Acts, Control and Import

Acts and others provide the authority to the government of Malaysia to put ban on imported and

domestic materials in the country. Thus, from the above discussion, it can be seen that the

Malaysian mass media industry is sensitive of various legal restrictions that hampers the business

of the mass media companies in the country to some extent (pressreference.com 2018).

Industry Dynamics and Drivers of Change

Industry dynamics refer to the certain means and processes through which changes come

in a particular industry over a period of time with the help of various processes and evolutions. It

needs to be mentioned that the mass media and entertainment industry of Malaysia is going

through some major changes due to the advancements of technology and various others reasons.

Thus, it can be observed that there has been a transformation in the mass media and

entertainment industry of Malaysia from old media to new media (Zavyalova et al. 2012). In the

recent years, it can be observed that the new advanced technology based mass media and

entertainment is challenging the old mass media and entertainment industry. After observing the

mass media and entertainment industry of Malaysia, it can clearly be seen that there has been

many changes in this industry and some major factors are responsible for this change. Thus,

these factors are known as Drivers of Change. In the mass media and entertainment industry of

Malaysia, the existence of some major drivers of change can be seen. It is required for the mass

media and entertainment companies in Malaysia to consider these drivers of changes. They are

discussed in the following discussion (Kotabe and Helsen 2014).

There are four major drivers of change having effects on the business operations of Astro

Malaysia Holdings; they are Consumer Behavior, Regulatory Changes, Technological Changes

and the Effects of different Macroeconomic Conditions. The following discussing shows how

these drivers of change affect the business operations of Astro Malaysia Holdings.

Consumer Behavior: The behavior of consumers towards the products and services of the

company is a major driver of change (Solomon, Russell-Bennett and Previte 2012). Consumer

behavior include various aspects like the willingness to make payment for a product or service,

their preferences related to various contents of media, level of interactivity with the company,

and Multimedia Act liberalized acceptable broadcast content. In this context, it needs to be

mentioned that various acts like media and press acts, Internal Security Acts, Control and Import

Acts and others provide the authority to the government of Malaysia to put ban on imported and

domestic materials in the country. Thus, from the above discussion, it can be seen that the

Malaysian mass media industry is sensitive of various legal restrictions that hampers the business

of the mass media companies in the country to some extent (pressreference.com 2018).

Industry Dynamics and Drivers of Change

Industry dynamics refer to the certain means and processes through which changes come

in a particular industry over a period of time with the help of various processes and evolutions. It

needs to be mentioned that the mass media and entertainment industry of Malaysia is going

through some major changes due to the advancements of technology and various others reasons.

Thus, it can be observed that there has been a transformation in the mass media and

entertainment industry of Malaysia from old media to new media (Zavyalova et al. 2012). In the

recent years, it can be observed that the new advanced technology based mass media and

entertainment is challenging the old mass media and entertainment industry. After observing the

mass media and entertainment industry of Malaysia, it can clearly be seen that there has been

many changes in this industry and some major factors are responsible for this change. Thus,

these factors are known as Drivers of Change. In the mass media and entertainment industry of

Malaysia, the existence of some major drivers of change can be seen. It is required for the mass

media and entertainment companies in Malaysia to consider these drivers of changes. They are

discussed in the following discussion (Kotabe and Helsen 2014).

There are four major drivers of change having effects on the business operations of Astro

Malaysia Holdings; they are Consumer Behavior, Regulatory Changes, Technological Changes

and the Effects of different Macroeconomic Conditions. The following discussing shows how

these drivers of change affect the business operations of Astro Malaysia Holdings.

Consumer Behavior: The behavior of consumers towards the products and services of the

company is a major driver of change (Solomon, Russell-Bennett and Previte 2012). Consumer

behavior include various aspects like the willingness to make payment for a product or service,

their preferences related to various contents of media, level of interactivity with the company,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS MANAGEMENT

privacy, genre and many others. It can be seen that all these aspects have large impact on the

business model of Astro Malaysia Holding along with their media services, prices, profit margin

and others. For example, the consumers of Malaysia have become fond of the e-media; and

based on this particular preference of the consumers, Astro Malaysia Holdings has had to change

their business model (Schütte and Ciarlante 2016).

Regulatory Changes: As per the earlier discussion, the mass media and entertainment industry

of Malaysia has to comply with various legislative regulations and all these aspects affect the

business operations of Astro Malaysia Holdings (Keane and Donald 2014). This particular driver

of change includes various aspects like privacy regulation, net neutrality, various antitrust

enforcements, copyright enforcement, censorship, regulations related to advertisement, universal

broadcasting regulations and many others. All these aspects have negative impact on the

profitability of the company as the company needs to comply with all these legislative

regulations. In addition, frequent changes can be seen in the legal regulations and it is difficult

for Astro Malaysia Holdings to change the compliance with these regulations on time-to-time

basis. Thus, it is considered as a major driver of change for Astro Malaysia Holdings (Pepinsky

2013).

Technological Changes: Technological change is considered as one of the major drivers of

change having impact on the business operations of Astro Malaysia Holdings. This driver of

change includes some major aspects like ultra HD television, flexible screens, semantic analysis,

advanced technology of power system, ultra broadband services and many others (Jomo 2013).

For this reason, it is required for the company to update themselves with the latest technology in

order to stay in the market. This process affects the profitability of Astro Malaysia Holdings as

the company has to incur large amount of costs while implementing these advance technological

aspects. At the same time, this also brings positive changes in the company as the company has

become able to increase their revenue (Hashim 2015).

Macroeconomics Conditions: This is also considered as a major driver of change. The major

factors of this driver are recession, balance of trade, price of commodity, supply, demand and

many others. These factors are considered as less predictable; but at the same time, they have

drastic impact on the business organizations of the company (Nor, Ibrahim and Rashid 2013).

privacy, genre and many others. It can be seen that all these aspects have large impact on the

business model of Astro Malaysia Holding along with their media services, prices, profit margin

and others. For example, the consumers of Malaysia have become fond of the e-media; and

based on this particular preference of the consumers, Astro Malaysia Holdings has had to change

their business model (Schütte and Ciarlante 2016).

Regulatory Changes: As per the earlier discussion, the mass media and entertainment industry

of Malaysia has to comply with various legislative regulations and all these aspects affect the

business operations of Astro Malaysia Holdings (Keane and Donald 2014). This particular driver

of change includes various aspects like privacy regulation, net neutrality, various antitrust

enforcements, copyright enforcement, censorship, regulations related to advertisement, universal

broadcasting regulations and many others. All these aspects have negative impact on the

profitability of the company as the company needs to comply with all these legislative

regulations. In addition, frequent changes can be seen in the legal regulations and it is difficult

for Astro Malaysia Holdings to change the compliance with these regulations on time-to-time

basis. Thus, it is considered as a major driver of change for Astro Malaysia Holdings (Pepinsky

2013).

Technological Changes: Technological change is considered as one of the major drivers of

change having impact on the business operations of Astro Malaysia Holdings. This driver of

change includes some major aspects like ultra HD television, flexible screens, semantic analysis,

advanced technology of power system, ultra broadband services and many others (Jomo 2013).

For this reason, it is required for the company to update themselves with the latest technology in

order to stay in the market. This process affects the profitability of Astro Malaysia Holdings as

the company has to incur large amount of costs while implementing these advance technological

aspects. At the same time, this also brings positive changes in the company as the company has

become able to increase their revenue (Hashim 2015).

Macroeconomics Conditions: This is also considered as a major driver of change. The major

factors of this driver are recession, balance of trade, price of commodity, supply, demand and

many others. These factors are considered as less predictable; but at the same time, they have

drastic impact on the business organizations of the company (Nor, Ibrahim and Rashid 2013).

5FINANCIAL ANALYSIS MANAGEMENT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS MANAGEMENT

Evaluation of Financial Performance

Evaluation of financial performance of the business organizations indicates towards the

overall financial condition of the businesses over the years. The evaluation of financial

performance is a useful tool for the investors as they can make investment decisions by

analyzing the trend of financial performance of the companies (Brigham and Houston 2012).

There is not any exception of this fact in case of Astro Malaysia Holdings. The following

discussion shows the evaluation of the financial performance of the company by analyzing the

profitability, liquidity, efficiency, debt position of the company along with the analysis of

investors return.

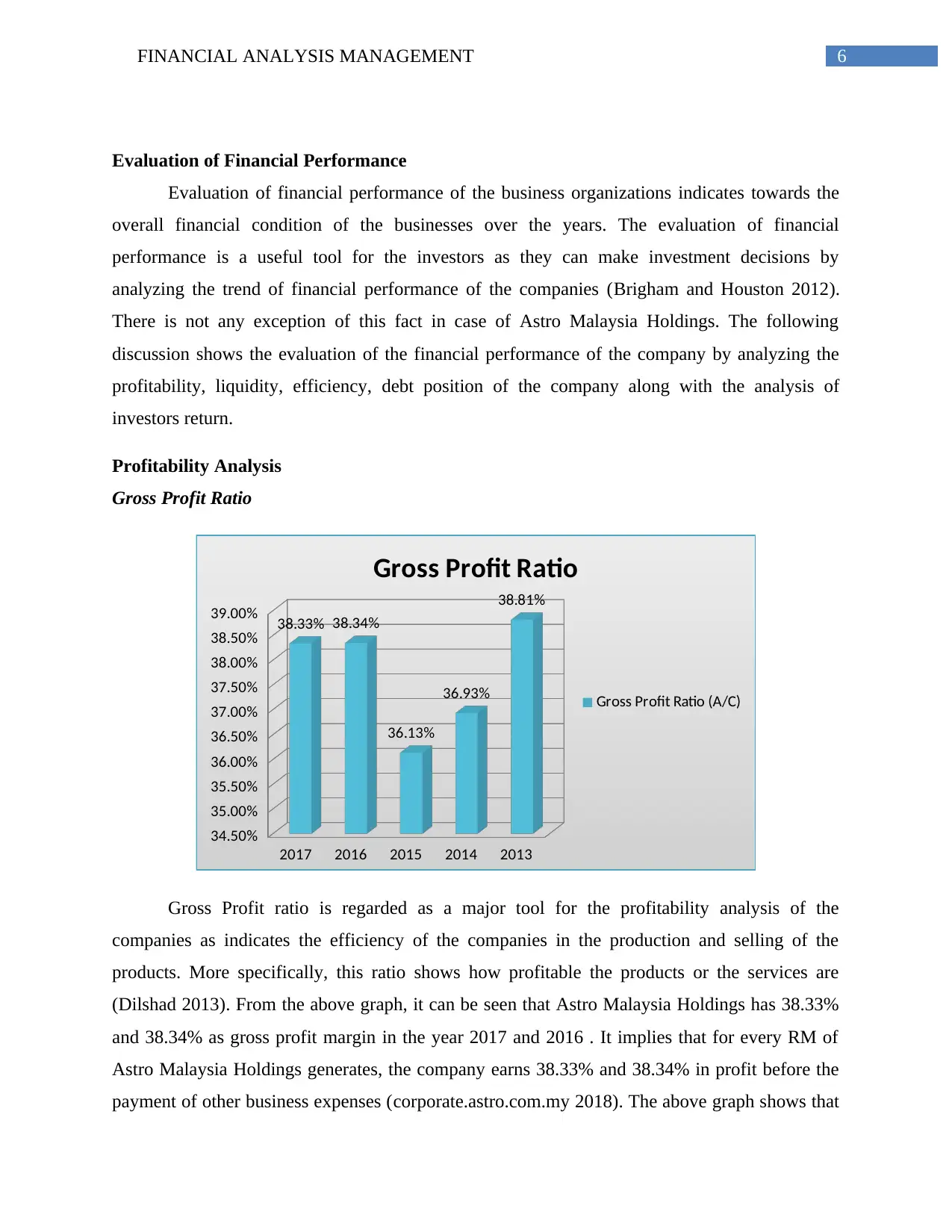

Profitability Analysis

Gross Profit Ratio

2017 2016 2015 2014 2013

34.50%

35.00%

35.50%

36.00%

36.50%

37.00%

37.50%

38.00%

38.50%

39.00% 38.33% 38.34%

36.13%

36.93%

38.81%

Gross Profit Ratio

Gross Profit Ratio (A/C)

Gross Profit ratio is regarded as a major tool for the profitability analysis of the

companies as indicates the efficiency of the companies in the production and selling of the

products. More specifically, this ratio shows how profitable the products or the services are

(Dilshad 2013). From the above graph, it can be seen that Astro Malaysia Holdings has 38.33%

and 38.34% as gross profit margin in the year 2017 and 2016 . It implies that for every RM of

Astro Malaysia Holdings generates, the company earns 38.33% and 38.34% in profit before the

payment of other business expenses (corporate.astro.com.my 2018). The above graph shows that

Evaluation of Financial Performance

Evaluation of financial performance of the business organizations indicates towards the

overall financial condition of the businesses over the years. The evaluation of financial

performance is a useful tool for the investors as they can make investment decisions by

analyzing the trend of financial performance of the companies (Brigham and Houston 2012).

There is not any exception of this fact in case of Astro Malaysia Holdings. The following

discussion shows the evaluation of the financial performance of the company by analyzing the

profitability, liquidity, efficiency, debt position of the company along with the analysis of

investors return.

Profitability Analysis

Gross Profit Ratio

2017 2016 2015 2014 2013

34.50%

35.00%

35.50%

36.00%

36.50%

37.00%

37.50%

38.00%

38.50%

39.00% 38.33% 38.34%

36.13%

36.93%

38.81%

Gross Profit Ratio

Gross Profit Ratio (A/C)

Gross Profit ratio is regarded as a major tool for the profitability analysis of the

companies as indicates the efficiency of the companies in the production and selling of the

products. More specifically, this ratio shows how profitable the products or the services are

(Dilshad 2013). From the above graph, it can be seen that Astro Malaysia Holdings has 38.33%

and 38.34% as gross profit margin in the year 2017 and 2016 . It implies that for every RM of

Astro Malaysia Holdings generates, the company earns 38.33% and 38.34% in profit before the

payment of other business expenses (corporate.astro.com.my 2018). The above graph shows that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS MANAGEMENT

there have been fluctuations in this gross profit margin over the five years as 2015 and 2014

witnessed decline in the gross profit. It needs to be mentioned that the main reason behind this

fluctuation in gross profit margin is the decline in sales of Astro Malaysia Holdings. It is evident

from the financial statements of the company that there has been decline in sales in 2015 and

2014 that affected the gross profit margin. Thus, for Astro Malaysia Holdings, some of the major

ways to improve their gross profit margin are th increase in sales, increase in the price, less

discounting and less competition in price.

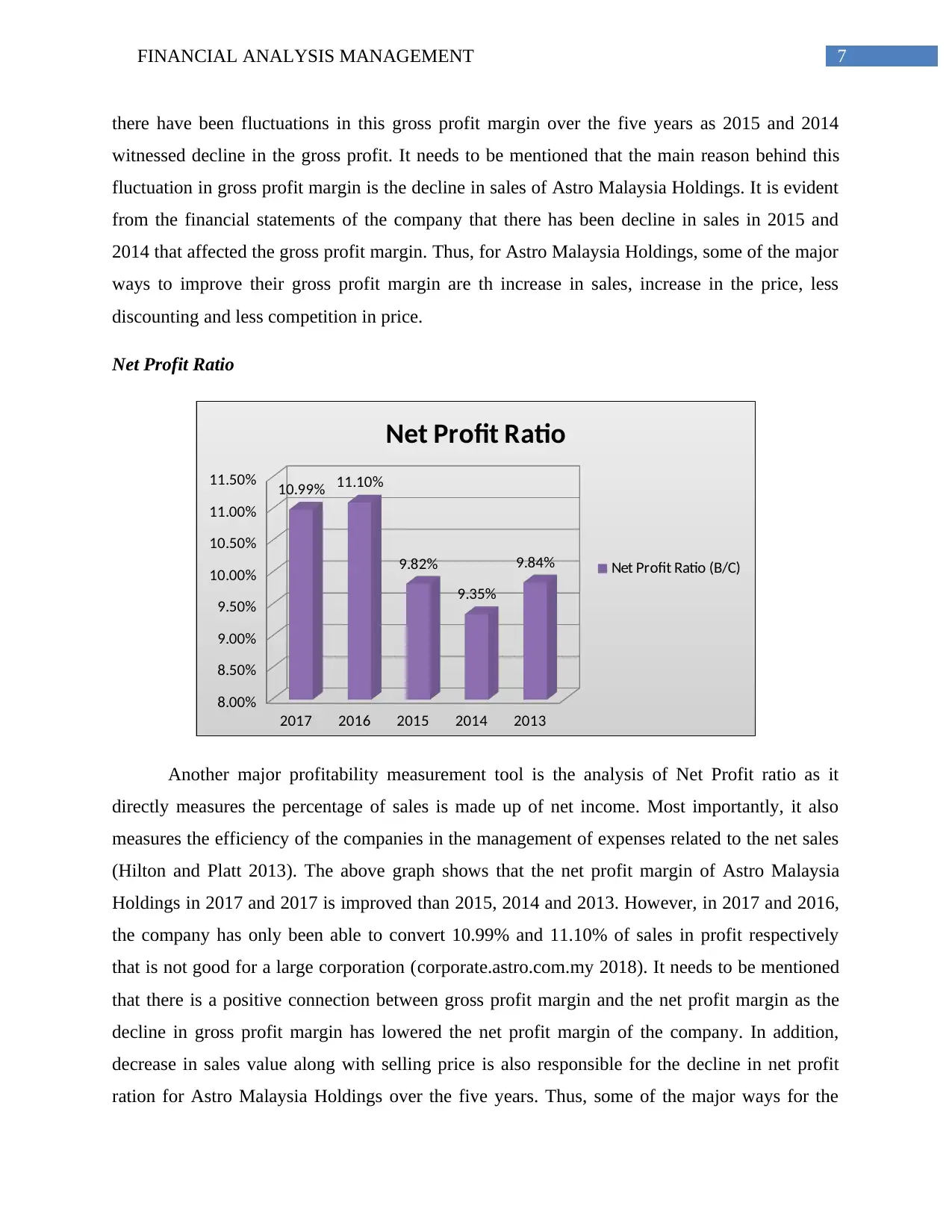

Net Profit Ratio

2017 2016 2015 2014 2013

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

11.00%

11.50% 10.99% 11.10%

9.82%

9.35%

9.84%

Net Profit Ratio

Net Profit Ratio (B/C)

Another major profitability measurement tool is the analysis of Net Profit ratio as it

directly measures the percentage of sales is made up of net income. Most importantly, it also

measures the efficiency of the companies in the management of expenses related to the net sales

(Hilton and Platt 2013). The above graph shows that the net profit margin of Astro Malaysia

Holdings in 2017 and 2017 is improved than 2015, 2014 and 2013. However, in 2017 and 2016,

the company has only been able to convert 10.99% and 11.10% of sales in profit respectively

that is not good for a large corporation (corporate.astro.com.my 2018). It needs to be mentioned

that there is a positive connection between gross profit margin and the net profit margin as the

decline in gross profit margin has lowered the net profit margin of the company. In addition,

decrease in sales value along with selling price is also responsible for the decline in net profit

ration for Astro Malaysia Holdings over the five years. Thus, some of the major ways for the

there have been fluctuations in this gross profit margin over the five years as 2015 and 2014

witnessed decline in the gross profit. It needs to be mentioned that the main reason behind this

fluctuation in gross profit margin is the decline in sales of Astro Malaysia Holdings. It is evident

from the financial statements of the company that there has been decline in sales in 2015 and

2014 that affected the gross profit margin. Thus, for Astro Malaysia Holdings, some of the major

ways to improve their gross profit margin are th increase in sales, increase in the price, less

discounting and less competition in price.

Net Profit Ratio

2017 2016 2015 2014 2013

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

11.00%

11.50% 10.99% 11.10%

9.82%

9.35%

9.84%

Net Profit Ratio

Net Profit Ratio (B/C)

Another major profitability measurement tool is the analysis of Net Profit ratio as it

directly measures the percentage of sales is made up of net income. Most importantly, it also

measures the efficiency of the companies in the management of expenses related to the net sales

(Hilton and Platt 2013). The above graph shows that the net profit margin of Astro Malaysia

Holdings in 2017 and 2017 is improved than 2015, 2014 and 2013. However, in 2017 and 2016,

the company has only been able to convert 10.99% and 11.10% of sales in profit respectively

that is not good for a large corporation (corporate.astro.com.my 2018). It needs to be mentioned

that there is a positive connection between gross profit margin and the net profit margin as the

decline in gross profit margin has lowered the net profit margin of the company. In addition,

decrease in sales value along with selling price is also responsible for the decline in net profit

ration for Astro Malaysia Holdings over the five years. Thus, some of the major ways for the

8FINANCIAL ANALYSIS MANAGEMENT

company to increase their net profit margin are the increase in sales and decrease in labor as well

as operation costs.

Liquidity Position Analysis

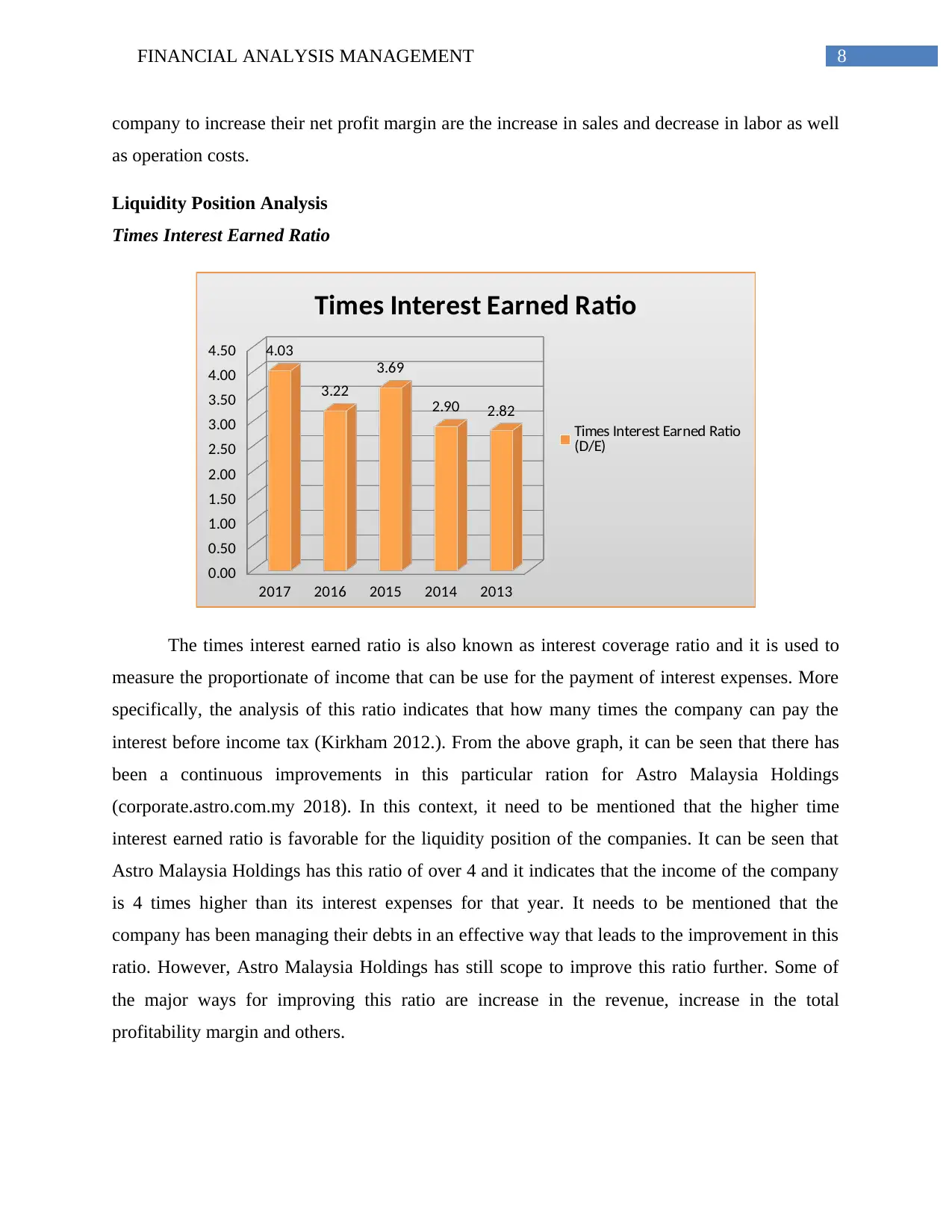

Times Interest Earned Ratio

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50 4.03

3.22

3.69

2.90 2.82

Times Interest Earned Ratio

Times Interest Earned Ratio

(D/E)

The times interest earned ratio is also known as interest coverage ratio and it is used to

measure the proportionate of income that can be use for the payment of interest expenses. More

specifically, the analysis of this ratio indicates that how many times the company can pay the

interest before income tax (Kirkham 2012.). From the above graph, it can be seen that there has

been a continuous improvements in this particular ration for Astro Malaysia Holdings

(corporate.astro.com.my 2018). In this context, it need to be mentioned that the higher time

interest earned ratio is favorable for the liquidity position of the companies. It can be seen that

Astro Malaysia Holdings has this ratio of over 4 and it indicates that the income of the company

is 4 times higher than its interest expenses for that year. It needs to be mentioned that the

company has been managing their debts in an effective way that leads to the improvement in this

ratio. However, Astro Malaysia Holdings has still scope to improve this ratio further. Some of

the major ways for improving this ratio are increase in the revenue, increase in the total

profitability margin and others.

company to increase their net profit margin are the increase in sales and decrease in labor as well

as operation costs.

Liquidity Position Analysis

Times Interest Earned Ratio

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50 4.03

3.22

3.69

2.90 2.82

Times Interest Earned Ratio

Times Interest Earned Ratio

(D/E)

The times interest earned ratio is also known as interest coverage ratio and it is used to

measure the proportionate of income that can be use for the payment of interest expenses. More

specifically, the analysis of this ratio indicates that how many times the company can pay the

interest before income tax (Kirkham 2012.). From the above graph, it can be seen that there has

been a continuous improvements in this particular ration for Astro Malaysia Holdings

(corporate.astro.com.my 2018). In this context, it need to be mentioned that the higher time

interest earned ratio is favorable for the liquidity position of the companies. It can be seen that

Astro Malaysia Holdings has this ratio of over 4 and it indicates that the income of the company

is 4 times higher than its interest expenses for that year. It needs to be mentioned that the

company has been managing their debts in an effective way that leads to the improvement in this

ratio. However, Astro Malaysia Holdings has still scope to improve this ratio further. Some of

the major ways for improving this ratio are increase in the revenue, increase in the total

profitability margin and others.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS MANAGEMENT

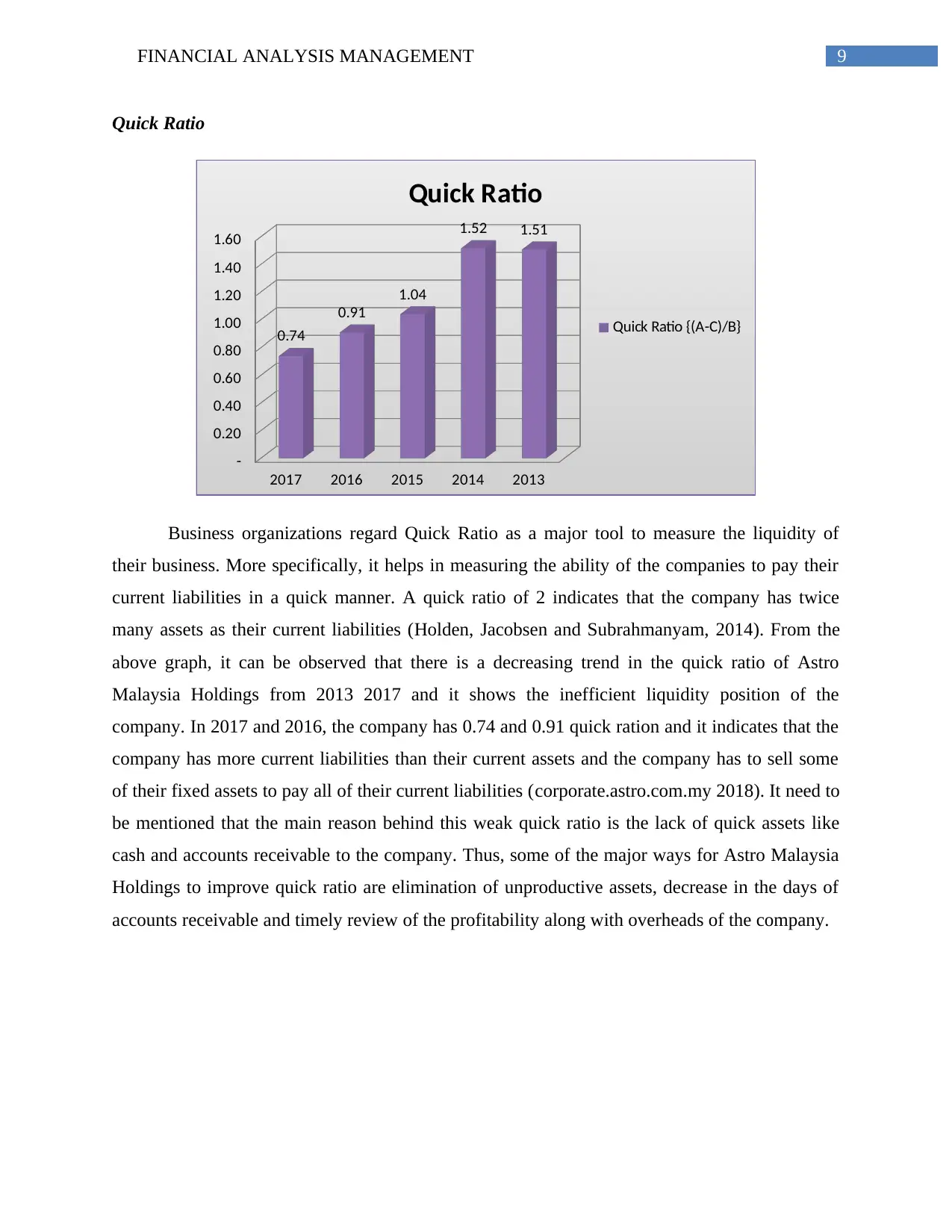

Quick Ratio

2017 2016 2015 2014 2013

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.74

0.91

1.04

1.52 1.51

Quick Ratio

Quick Ratio {(A-C)/B}

Business organizations regard Quick Ratio as a major tool to measure the liquidity of

their business. More specifically, it helps in measuring the ability of the companies to pay their

current liabilities in a quick manner. A quick ratio of 2 indicates that the company has twice

many assets as their current liabilities (Holden, Jacobsen and Subrahmanyam, 2014). From the

above graph, it can be observed that there is a decreasing trend in the quick ratio of Astro

Malaysia Holdings from 2013 2017 and it shows the inefficient liquidity position of the

company. In 2017 and 2016, the company has 0.74 and 0.91 quick ration and it indicates that the

company has more current liabilities than their current assets and the company has to sell some

of their fixed assets to pay all of their current liabilities (corporate.astro.com.my 2018). It need to

be mentioned that the main reason behind this weak quick ratio is the lack of quick assets like

cash and accounts receivable to the company. Thus, some of the major ways for Astro Malaysia

Holdings to improve quick ratio are elimination of unproductive assets, decrease in the days of

accounts receivable and timely review of the profitability along with overheads of the company.

Quick Ratio

2017 2016 2015 2014 2013

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.74

0.91

1.04

1.52 1.51

Quick Ratio

Quick Ratio {(A-C)/B}

Business organizations regard Quick Ratio as a major tool to measure the liquidity of

their business. More specifically, it helps in measuring the ability of the companies to pay their

current liabilities in a quick manner. A quick ratio of 2 indicates that the company has twice

many assets as their current liabilities (Holden, Jacobsen and Subrahmanyam, 2014). From the

above graph, it can be observed that there is a decreasing trend in the quick ratio of Astro

Malaysia Holdings from 2013 2017 and it shows the inefficient liquidity position of the

company. In 2017 and 2016, the company has 0.74 and 0.91 quick ration and it indicates that the

company has more current liabilities than their current assets and the company has to sell some

of their fixed assets to pay all of their current liabilities (corporate.astro.com.my 2018). It need to

be mentioned that the main reason behind this weak quick ratio is the lack of quick assets like

cash and accounts receivable to the company. Thus, some of the major ways for Astro Malaysia

Holdings to improve quick ratio are elimination of unproductive assets, decrease in the days of

accounts receivable and timely review of the profitability along with overheads of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS MANAGEMENT

Efficiency Analysis

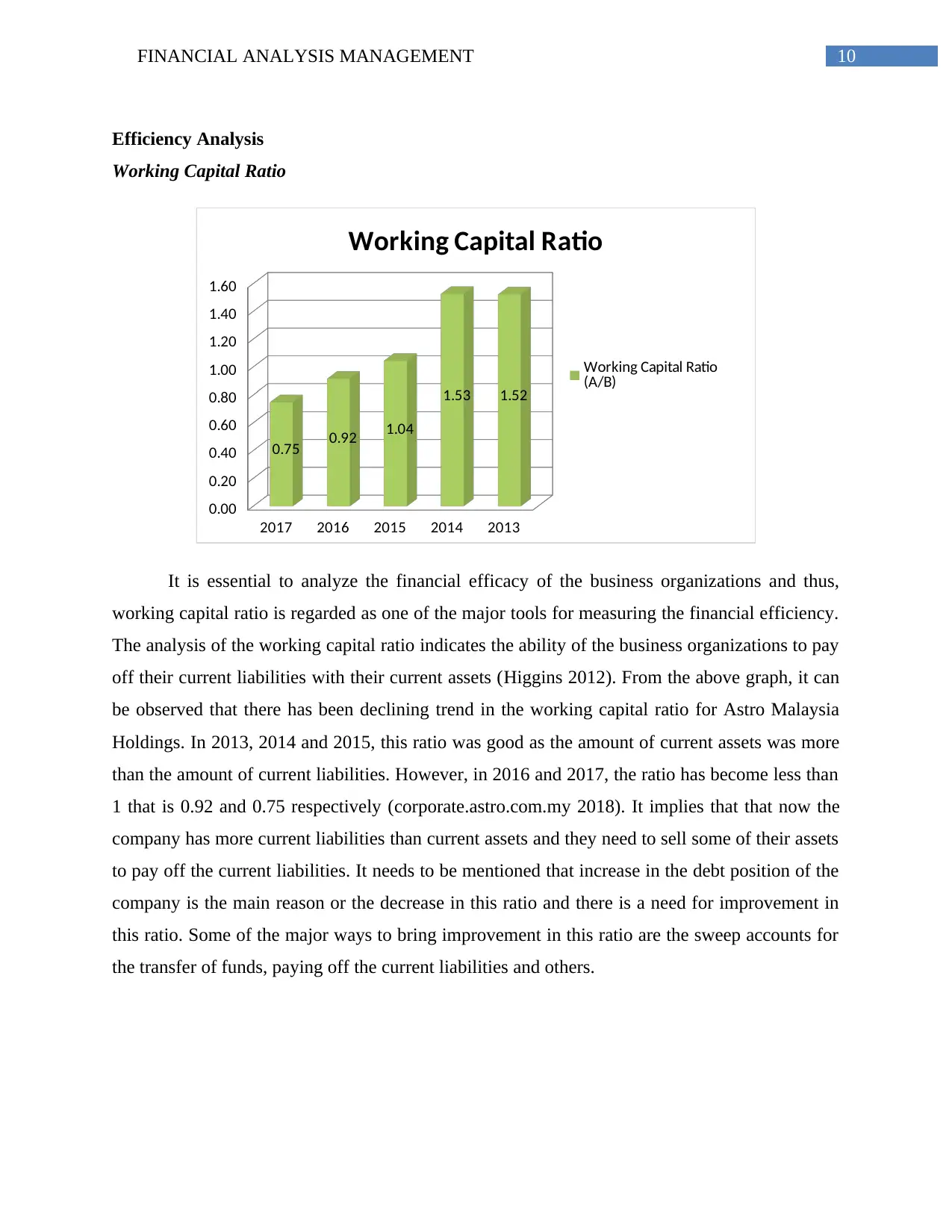

Working Capital Ratio

2017 2016 2015 2014 2013

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.75 0.92 1.04

1.53 1.52

Working Capital Ratio

Working Capital Ratio

(A/B)

It is essential to analyze the financial efficacy of the business organizations and thus,

working capital ratio is regarded as one of the major tools for measuring the financial efficiency.

The analysis of the working capital ratio indicates the ability of the business organizations to pay

off their current liabilities with their current assets (Higgins 2012). From the above graph, it can

be observed that there has been declining trend in the working capital ratio for Astro Malaysia

Holdings. In 2013, 2014 and 2015, this ratio was good as the amount of current assets was more

than the amount of current liabilities. However, in 2016 and 2017, the ratio has become less than

1 that is 0.92 and 0.75 respectively (corporate.astro.com.my 2018). It implies that that now the

company has more current liabilities than current assets and they need to sell some of their assets

to pay off the current liabilities. It needs to be mentioned that increase in the debt position of the

company is the main reason or the decrease in this ratio and there is a need for improvement in

this ratio. Some of the major ways to bring improvement in this ratio are the sweep accounts for

the transfer of funds, paying off the current liabilities and others.

Efficiency Analysis

Working Capital Ratio

2017 2016 2015 2014 2013

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.75 0.92 1.04

1.53 1.52

Working Capital Ratio

Working Capital Ratio

(A/B)

It is essential to analyze the financial efficacy of the business organizations and thus,

working capital ratio is regarded as one of the major tools for measuring the financial efficiency.

The analysis of the working capital ratio indicates the ability of the business organizations to pay

off their current liabilities with their current assets (Higgins 2012). From the above graph, it can

be observed that there has been declining trend in the working capital ratio for Astro Malaysia

Holdings. In 2013, 2014 and 2015, this ratio was good as the amount of current assets was more

than the amount of current liabilities. However, in 2016 and 2017, the ratio has become less than

1 that is 0.92 and 0.75 respectively (corporate.astro.com.my 2018). It implies that that now the

company has more current liabilities than current assets and they need to sell some of their assets

to pay off the current liabilities. It needs to be mentioned that increase in the debt position of the

company is the main reason or the decrease in this ratio and there is a need for improvement in

this ratio. Some of the major ways to bring improvement in this ratio are the sweep accounts for

the transfer of funds, paying off the current liabilities and others.

11FINANCIAL ANALYSIS MANAGEMENT

Inventory Turnover ratio

2017 2016 2015 2014 2013

0.00

50.00

100.00

150.00

200.00

250.00

169.10

201.19

218.92

146.82

220.93

Inventory Turnover Ratio

Inventory Turnover Ratio

(C/E)

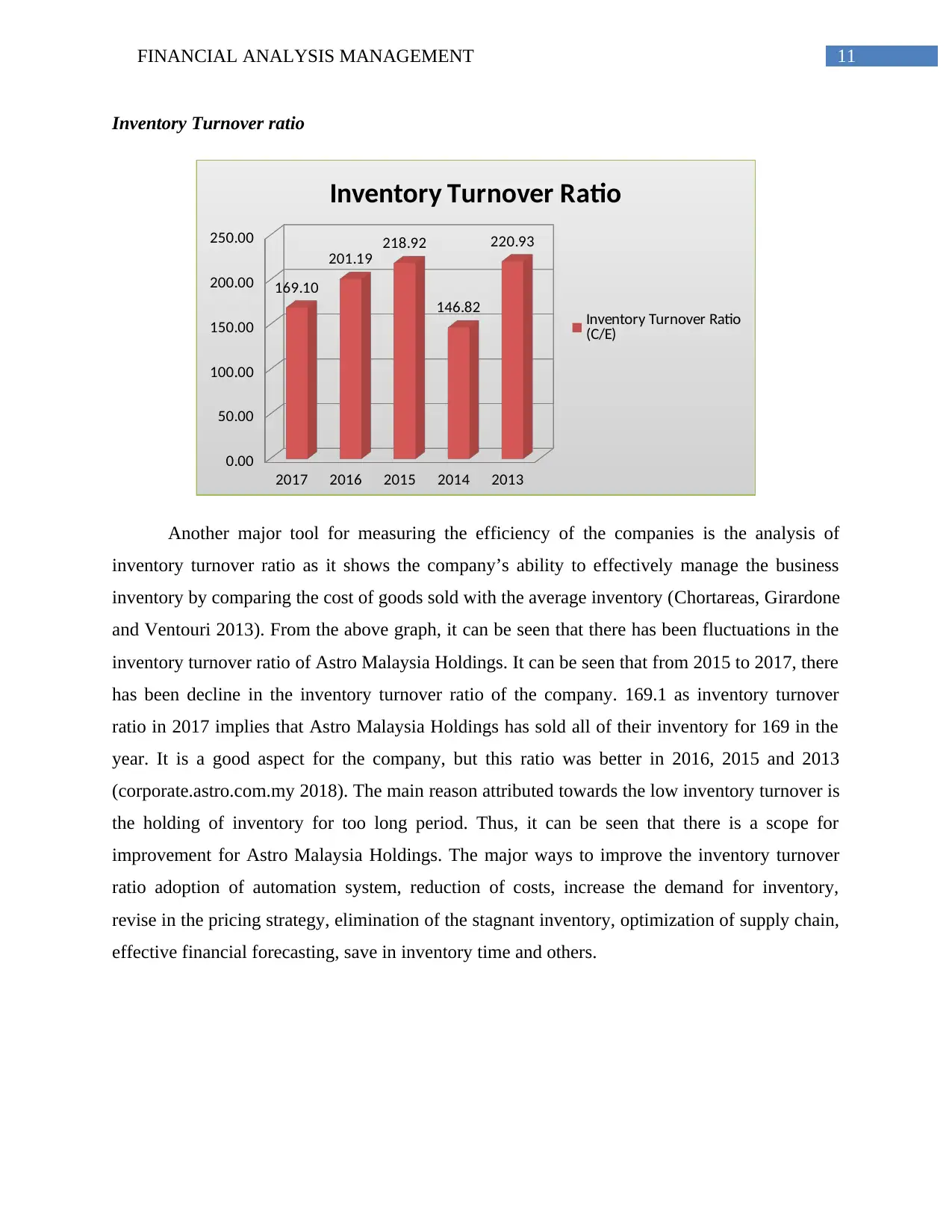

Another major tool for measuring the efficiency of the companies is the analysis of

inventory turnover ratio as it shows the company’s ability to effectively manage the business

inventory by comparing the cost of goods sold with the average inventory (Chortareas, Girardone

and Ventouri 2013). From the above graph, it can be seen that there has been fluctuations in the

inventory turnover ratio of Astro Malaysia Holdings. It can be seen that from 2015 to 2017, there

has been decline in the inventory turnover ratio of the company. 169.1 as inventory turnover

ratio in 2017 implies that Astro Malaysia Holdings has sold all of their inventory for 169 in the

year. It is a good aspect for the company, but this ratio was better in 2016, 2015 and 2013

(corporate.astro.com.my 2018). The main reason attributed towards the low inventory turnover is

the holding of inventory for too long period. Thus, it can be seen that there is a scope for

improvement for Astro Malaysia Holdings. The major ways to improve the inventory turnover

ratio adoption of automation system, reduction of costs, increase the demand for inventory,

revise in the pricing strategy, elimination of the stagnant inventory, optimization of supply chain,

effective financial forecasting, save in inventory time and others.

Inventory Turnover ratio

2017 2016 2015 2014 2013

0.00

50.00

100.00

150.00

200.00

250.00

169.10

201.19

218.92

146.82

220.93

Inventory Turnover Ratio

Inventory Turnover Ratio

(C/E)

Another major tool for measuring the efficiency of the companies is the analysis of

inventory turnover ratio as it shows the company’s ability to effectively manage the business

inventory by comparing the cost of goods sold with the average inventory (Chortareas, Girardone

and Ventouri 2013). From the above graph, it can be seen that there has been fluctuations in the

inventory turnover ratio of Astro Malaysia Holdings. It can be seen that from 2015 to 2017, there

has been decline in the inventory turnover ratio of the company. 169.1 as inventory turnover

ratio in 2017 implies that Astro Malaysia Holdings has sold all of their inventory for 169 in the

year. It is a good aspect for the company, but this ratio was better in 2016, 2015 and 2013

(corporate.astro.com.my 2018). The main reason attributed towards the low inventory turnover is

the holding of inventory for too long period. Thus, it can be seen that there is a scope for

improvement for Astro Malaysia Holdings. The major ways to improve the inventory turnover

ratio adoption of automation system, reduction of costs, increase the demand for inventory,

revise in the pricing strategy, elimination of the stagnant inventory, optimization of supply chain,

effective financial forecasting, save in inventory time and others.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.