Issues in Auditing: Financial Statement Analysis Report

VerifiedAdded on 2020/05/11

|16

|3256

|54

Report

AI Summary

This report delves into the critical aspects of auditing, commencing with the planning phase, which is essential for successful audit execution. It then explores analytical review procedures, comparing financial statement items to identify relationships and trends. The report emphasizes the importance of preliminary judgment of materiality, illustrating how auditors assess the significance of misstatements. It proceeds to analyze specific accounts, including consultancy fees, bank charges, interest income, sales, depreciation, cost of sales, and superannuation, providing rationale for selection, key assertions, and recommended audit procedures for each. The analysis includes percentage changes, materiality assessments, and detailed audit steps to ensure the accuracy and reliability of financial statements. References and an appendix are included to support the findings.

ISSUES IN AUDITING

Student Name:

Student ID:

10/9/2017

Student Name:

Student ID:

10/9/2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

PLANNING OF AUDIT...................................................................................................................................4

ANALYTICAL REVIEW...............................................................................................................................4

PRELIMINARY JUDGMENT OF MATERIALITY............................................................................................5

CONSULTANCY FEES....................................................................................................................................5

RATIONALE FOR SELECTION....................................................................................................................5

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

BANK CHARGES...........................................................................................................................................6

RATIONALE FOR SELECTION....................................................................................................................6

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

INTEREST INCOME.......................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................7

RECOMMENDED AUDIT PROCEDURE......................................................................................................7

SALES...........................................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

DEPRECIATION.............................................................................................................................................8

RATIONALE FOR SELECTION....................................................................................................................8

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

COST OF SALES............................................................................................................................................8

RATIONALE FOR SELECTION....................................................................................................................8

ASSERTION AND EXPLANATION...............................................................................................................9

RECOMMENDED AUDIT PROCEDURE......................................................................................................9

SUPERANNUATION......................................................................................................................................9

RATIONALE FOR SELECTION....................................................................................................................9

PLANNING OF AUDIT...................................................................................................................................4

ANALYTICAL REVIEW...............................................................................................................................4

PRELIMINARY JUDGMENT OF MATERIALITY............................................................................................5

CONSULTANCY FEES....................................................................................................................................5

RATIONALE FOR SELECTION....................................................................................................................5

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

BANK CHARGES...........................................................................................................................................6

RATIONALE FOR SELECTION....................................................................................................................6

ASSERTION AND EXPLANATION...............................................................................................................6

RECOMMENDED AUDIT PROCEDURE......................................................................................................6

INTEREST INCOME.......................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................7

RECOMMENDED AUDIT PROCEDURE......................................................................................................7

SALES...........................................................................................................................................................7

RATIONALE FOR SELECTION....................................................................................................................7

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

DEPRECIATION.............................................................................................................................................8

RATIONALE FOR SELECTION....................................................................................................................8

ASSERTION AND EXPLANATION...............................................................................................................8

RECOMMENDED AUDIT PROCEDURE......................................................................................................8

COST OF SALES............................................................................................................................................8

RATIONALE FOR SELECTION....................................................................................................................8

ASSERTION AND EXPLANATION...............................................................................................................9

RECOMMENDED AUDIT PROCEDURE......................................................................................................9

SUPERANNUATION......................................................................................................................................9

RATIONALE FOR SELECTION....................................................................................................................9

ASSERTION AND EXPLANATION...............................................................................................................9

RECOMMENDED AUDIT PROCEDURE......................................................................................................9

REFERENCES................................................................................................................................................9

APPENDIX..................................................................................................................................................11

RECOMMENDED AUDIT PROCEDURE......................................................................................................9

REFERENCES................................................................................................................................................9

APPENDIX..................................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PLANNING OF AUDIT

For the start of any activity whether it is related to accounting, production, marketing or any other

function, the planning plays the very important role in the successful execution of the function. Any

activity done without proper and adequate planning will always gives the vague and futile results. In the

given case, the auditing function is required to be discussed and accordingly planning is also required for

the successful completion of the audit. It is the first step towards the audit. It defines the manner in

which the auditor is required to execute the function of the audit. At first it writes down the nature and

size of the business of the company and after that it provides the layout of the whole process of the

audit including the items of the financial statements which are required to be checked in detail and how

the evidences has to be obtained from the company and how the same needs to be documented in the

audit file and so on. Secondly, the planning of audit also includes carrying out some preliminary tests

which will help the auditors to concentrate on those items more which are more prone to the existence

of the material misstatements therein (Leung, Coram, Copper and Richardson, 2015). These tests

include preliminary analytical review, judging about the materiality of the concept and substantive tests.

In order to conduct the study, the financials of Calamansi Enterprises have been made available.

ANALYTICAL REVIEW

The first test which is done at the time of planning of the audit is the preliminary analytical review.

Under the preliminary analytical review procedures, the auditor is required to compare the items stated

in the financial statements in two ways. One way is to link the items stated in the financial statements of

the company for the particular year with the other stated items of that year only and the other way is to

link the particular item stated in the financial statements of the company for the current year with the

previous year. The both ways helps in establishing the relationship and making the comparison between

two or three items. For instance in the current year two head of accounts can be linked like gross profit

margin and the sales and the requisite percentage can be find out (ACCA, 2016). And for the consecutive

two years the current ratio, change in working capital, change in the revenue earned in percentage

terms, change in the cash and cash equivalents in percentage term can be done. The second method of

analysis is commonly known as the trend analysis and it is one of the best methods of analysis

prescribed in the statistical measures. The trend analysis can give two types of results either positive or

negative and provides the degree up to which the head of the account is affected by other account

For the start of any activity whether it is related to accounting, production, marketing or any other

function, the planning plays the very important role in the successful execution of the function. Any

activity done without proper and adequate planning will always gives the vague and futile results. In the

given case, the auditing function is required to be discussed and accordingly planning is also required for

the successful completion of the audit. It is the first step towards the audit. It defines the manner in

which the auditor is required to execute the function of the audit. At first it writes down the nature and

size of the business of the company and after that it provides the layout of the whole process of the

audit including the items of the financial statements which are required to be checked in detail and how

the evidences has to be obtained from the company and how the same needs to be documented in the

audit file and so on. Secondly, the planning of audit also includes carrying out some preliminary tests

which will help the auditors to concentrate on those items more which are more prone to the existence

of the material misstatements therein (Leung, Coram, Copper and Richardson, 2015). These tests

include preliminary analytical review, judging about the materiality of the concept and substantive tests.

In order to conduct the study, the financials of Calamansi Enterprises have been made available.

ANALYTICAL REVIEW

The first test which is done at the time of planning of the audit is the preliminary analytical review.

Under the preliminary analytical review procedures, the auditor is required to compare the items stated

in the financial statements in two ways. One way is to link the items stated in the financial statements of

the company for the particular year with the other stated items of that year only and the other way is to

link the particular item stated in the financial statements of the company for the current year with the

previous year. The both ways helps in establishing the relationship and making the comparison between

two or three items. For instance in the current year two head of accounts can be linked like gross profit

margin and the sales and the requisite percentage can be find out (ACCA, 2016). And for the consecutive

two years the current ratio, change in working capital, change in the revenue earned in percentage

terms, change in the cash and cash equivalents in percentage term can be done. The second method of

analysis is commonly known as the trend analysis and it is one of the best methods of analysis

prescribed in the statistical measures. The trend analysis can give two types of results either positive or

negative and provides the degree up to which the head of the account is affected by other account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Glover, Prawitt and Drake, 2014). For instance positive trend in the administration expenses indicates

that the company’s management on the cost control methods has become ineffective and positive

increase in sales on one hand emphasizes on the company’s reputation and on other hand raise doubts

on the correctness and accuracy of the figure of the sales figure.

In the Calamansi Enterprises, seven accounts have been selected which requires the detailed checking.

These are consultancy fees, bank charges, interest income, sales, depreciation, cost of sales and

superannuation. (Abidin and Baabbad, 2015).

PRELIMINARY JUDGMENT OF MATERIALITY

Apart from the adoption of the preliminary analytical review procedures by the auditors, the

auditors are also required to check the how far the head of accounts so selected for the purpose of

the analysis can have the presence of the material misstatement in financial statements of the

company for the period ending as on the date of analysis. Materiality in itself exhibits the

importance of each and every effect that the particular item shall have in the financial statements.

For instance, the consultancy fees have been increased from $57000 in the year ending 30th of

June 2016 to $59250 in the year ending 30th of June 2017. The increase counts for 3.95% which

is regarded as the material enough to increase the retained earnings of the company which in turn

will increase the equity and also the share price of the company (Langevoort, 2015).

While judging the materiality of the particular item as stated in the financial statements of the

company, the auditor is required to set out the limit in either percentage terms or in monetary

terms depending upon the nature of the item which will be regarded as the material limit. The

effect of the same shall be analysed if either the item crosses the material limit or falls below the

material limit. For instance, of the auditor kept the material limit for consultancy fees as 3%,

then the 3.95% is the material enough to consider and for the analysis of the effect it gives over

the financial health and performance of the company (Ullah, 2014). As the company’s

management has not specified any materiality limit, the auditor will do the judgment in

accordance with the analytical procedures (Chen and Tsay, 2017 and Mao, 2014).

that the company’s management on the cost control methods has become ineffective and positive

increase in sales on one hand emphasizes on the company’s reputation and on other hand raise doubts

on the correctness and accuracy of the figure of the sales figure.

In the Calamansi Enterprises, seven accounts have been selected which requires the detailed checking.

These are consultancy fees, bank charges, interest income, sales, depreciation, cost of sales and

superannuation. (Abidin and Baabbad, 2015).

PRELIMINARY JUDGMENT OF MATERIALITY

Apart from the adoption of the preliminary analytical review procedures by the auditors, the

auditors are also required to check the how far the head of accounts so selected for the purpose of

the analysis can have the presence of the material misstatement in financial statements of the

company for the period ending as on the date of analysis. Materiality in itself exhibits the

importance of each and every effect that the particular item shall have in the financial statements.

For instance, the consultancy fees have been increased from $57000 in the year ending 30th of

June 2016 to $59250 in the year ending 30th of June 2017. The increase counts for 3.95% which

is regarded as the material enough to increase the retained earnings of the company which in turn

will increase the equity and also the share price of the company (Langevoort, 2015).

While judging the materiality of the particular item as stated in the financial statements of the

company, the auditor is required to set out the limit in either percentage terms or in monetary

terms depending upon the nature of the item which will be regarded as the material limit. The

effect of the same shall be analysed if either the item crosses the material limit or falls below the

material limit. For instance, of the auditor kept the material limit for consultancy fees as 3%,

then the 3.95% is the material enough to consider and for the analysis of the effect it gives over

the financial health and performance of the company (Ullah, 2014). As the company’s

management has not specified any materiality limit, the auditor will do the judgment in

accordance with the analytical procedures (Chen and Tsay, 2017 and Mao, 2014).

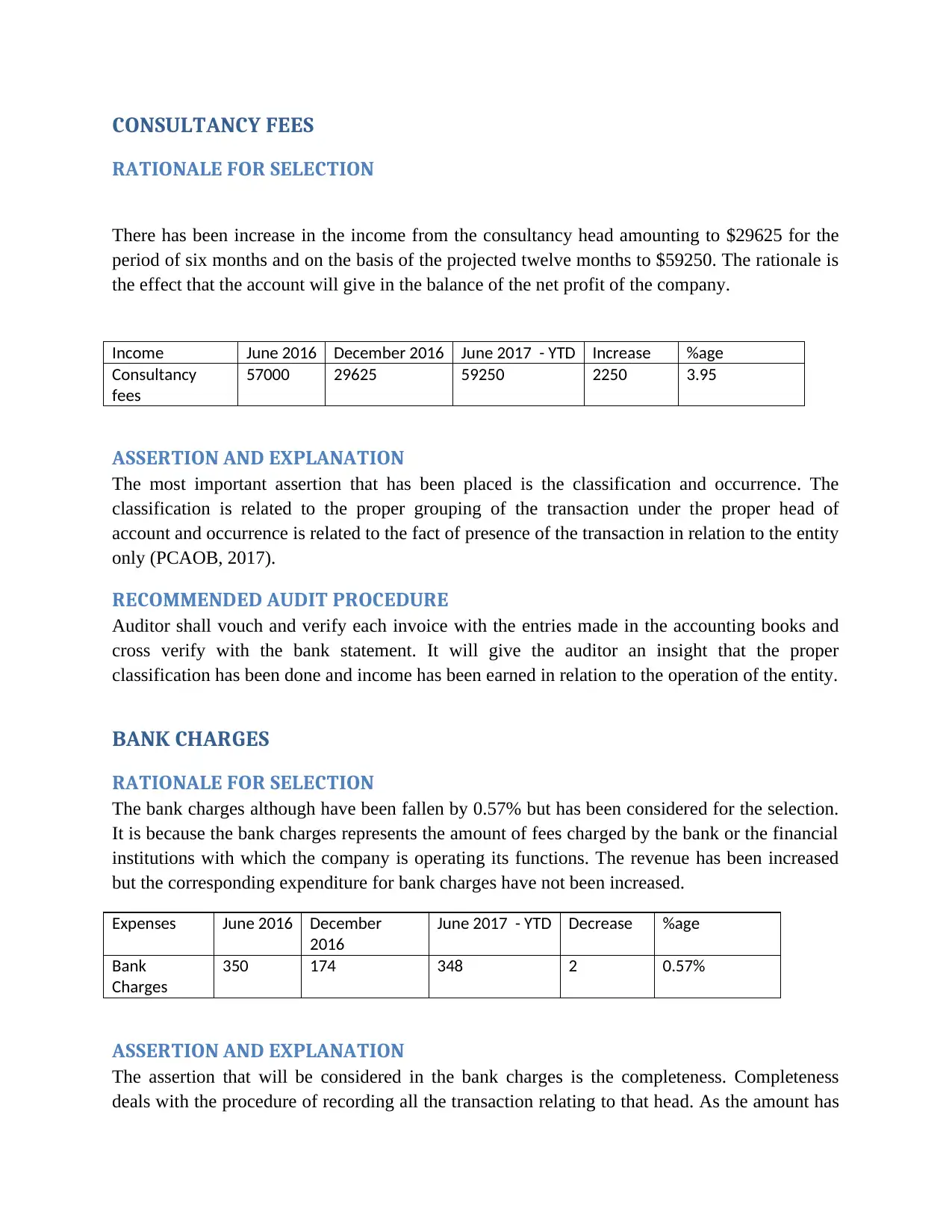

CONSULTANCY FEES

RATIONALE FOR SELECTION

There has been increase in the income from the consultancy head amounting to $29625 for the

period of six months and on the basis of the projected twelve months to $59250. The rationale is

the effect that the account will give in the balance of the net profit of the company.

Income June 2016 December 2016 June 2017 - YTD Increase %age

Consultancy

fees

57000 29625 59250 2250 3.95

ASSERTION AND EXPLANATION

The most important assertion that has been placed is the classification and occurrence. The

classification is related to the proper grouping of the transaction under the proper head of

account and occurrence is related to the fact of presence of the transaction in relation to the entity

only (PCAOB, 2017).

RECOMMENDED AUDIT PROCEDURE

Auditor shall vouch and verify each invoice with the entries made in the accounting books and

cross verify with the bank statement. It will give the auditor an insight that the proper

classification has been done and income has been earned in relation to the operation of the entity.

BANK CHARGES

RATIONALE FOR SELECTION

The bank charges although have been fallen by 0.57% but has been considered for the selection.

It is because the bank charges represents the amount of fees charged by the bank or the financial

institutions with which the company is operating its functions. The revenue has been increased

but the corresponding expenditure for bank charges have not been increased.

Expenses June 2016 December

2016

June 2017 - YTD Decrease %age

Bank

Charges

350 174 348 2 0.57%

ASSERTION AND EXPLANATION

The assertion that will be considered in the bank charges is the completeness. Completeness

deals with the procedure of recording all the transaction relating to that head. As the amount has

RATIONALE FOR SELECTION

There has been increase in the income from the consultancy head amounting to $29625 for the

period of six months and on the basis of the projected twelve months to $59250. The rationale is

the effect that the account will give in the balance of the net profit of the company.

Income June 2016 December 2016 June 2017 - YTD Increase %age

Consultancy

fees

57000 29625 59250 2250 3.95

ASSERTION AND EXPLANATION

The most important assertion that has been placed is the classification and occurrence. The

classification is related to the proper grouping of the transaction under the proper head of

account and occurrence is related to the fact of presence of the transaction in relation to the entity

only (PCAOB, 2017).

RECOMMENDED AUDIT PROCEDURE

Auditor shall vouch and verify each invoice with the entries made in the accounting books and

cross verify with the bank statement. It will give the auditor an insight that the proper

classification has been done and income has been earned in relation to the operation of the entity.

BANK CHARGES

RATIONALE FOR SELECTION

The bank charges although have been fallen by 0.57% but has been considered for the selection.

It is because the bank charges represents the amount of fees charged by the bank or the financial

institutions with which the company is operating its functions. The revenue has been increased

but the corresponding expenditure for bank charges have not been increased.

Expenses June 2016 December

2016

June 2017 - YTD Decrease %age

Bank

Charges

350 174 348 2 0.57%

ASSERTION AND EXPLANATION

The assertion that will be considered in the bank charges is the completeness. Completeness

deals with the procedure of recording all the transaction relating to that head. As the amount has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

been fallen, there might be the possibility that the expenditure has been booked under different

heads.

RECOMMENDED AUDIT PROCEDURE

The audit team is required to closely monitor and verify the bank statement of the company and

obtain the confirmation from the bank as to the amount of bank charges incurred during the

period.

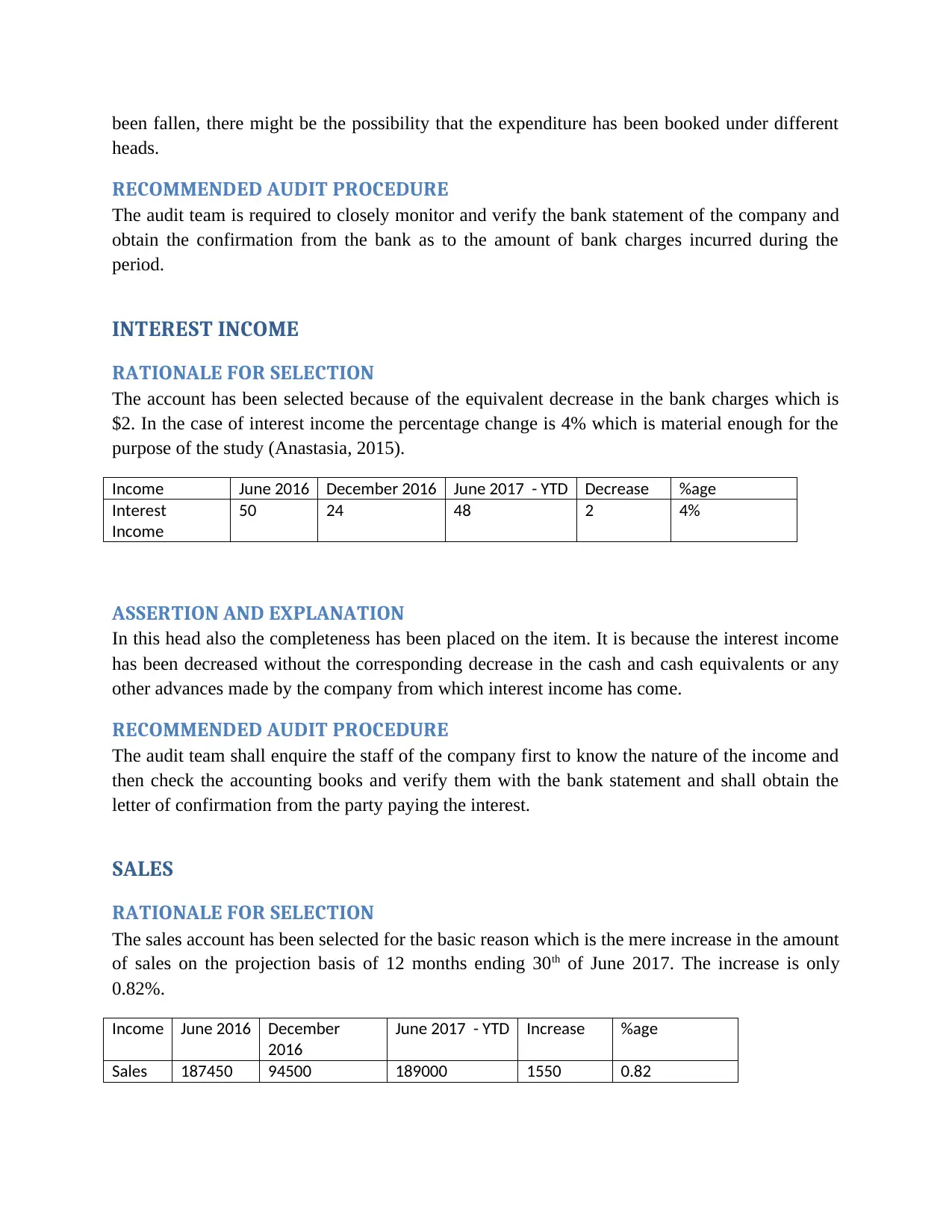

INTEREST INCOME

RATIONALE FOR SELECTION

The account has been selected because of the equivalent decrease in the bank charges which is

$2. In the case of interest income the percentage change is 4% which is material enough for the

purpose of the study (Anastasia, 2015).

Income June 2016 December 2016 June 2017 - YTD Decrease %age

Interest

Income

50 24 48 2 4%

ASSERTION AND EXPLANATION

In this head also the completeness has been placed on the item. It is because the interest income

has been decreased without the corresponding decrease in the cash and cash equivalents or any

other advances made by the company from which interest income has come.

RECOMMENDED AUDIT PROCEDURE

The audit team shall enquire the staff of the company first to know the nature of the income and

then check the accounting books and verify them with the bank statement and shall obtain the

letter of confirmation from the party paying the interest.

SALES

RATIONALE FOR SELECTION

The sales account has been selected for the basic reason which is the mere increase in the amount

of sales on the projection basis of 12 months ending 30th of June 2017. The increase is only

0.82%.

Income June 2016 December

2016

June 2017 - YTD Increase %age

Sales 187450 94500 189000 1550 0.82

heads.

RECOMMENDED AUDIT PROCEDURE

The audit team is required to closely monitor and verify the bank statement of the company and

obtain the confirmation from the bank as to the amount of bank charges incurred during the

period.

INTEREST INCOME

RATIONALE FOR SELECTION

The account has been selected because of the equivalent decrease in the bank charges which is

$2. In the case of interest income the percentage change is 4% which is material enough for the

purpose of the study (Anastasia, 2015).

Income June 2016 December 2016 June 2017 - YTD Decrease %age

Interest

Income

50 24 48 2 4%

ASSERTION AND EXPLANATION

In this head also the completeness has been placed on the item. It is because the interest income

has been decreased without the corresponding decrease in the cash and cash equivalents or any

other advances made by the company from which interest income has come.

RECOMMENDED AUDIT PROCEDURE

The audit team shall enquire the staff of the company first to know the nature of the income and

then check the accounting books and verify them with the bank statement and shall obtain the

letter of confirmation from the party paying the interest.

SALES

RATIONALE FOR SELECTION

The sales account has been selected for the basic reason which is the mere increase in the amount

of sales on the projection basis of 12 months ending 30th of June 2017. The increase is only

0.82%.

Income June 2016 December

2016

June 2017 - YTD Increase %age

Sales 187450 94500 189000 1550 0.82

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

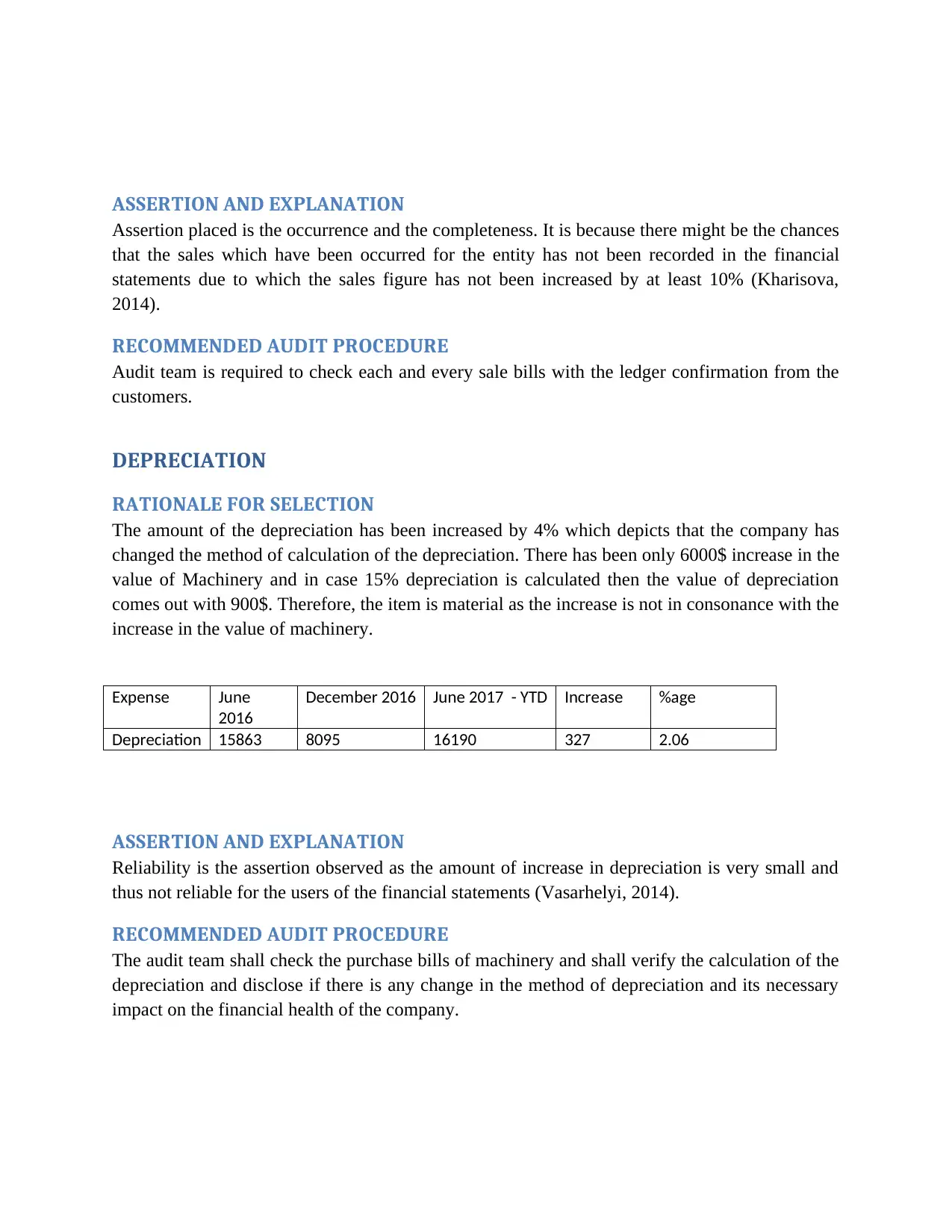

ASSERTION AND EXPLANATION

Assertion placed is the occurrence and the completeness. It is because there might be the chances

that the sales which have been occurred for the entity has not been recorded in the financial

statements due to which the sales figure has not been increased by at least 10% (Kharisova,

2014).

RECOMMENDED AUDIT PROCEDURE

Audit team is required to check each and every sale bills with the ledger confirmation from the

customers.

DEPRECIATION

RATIONALE FOR SELECTION

The amount of the depreciation has been increased by 4% which depicts that the company has

changed the method of calculation of the depreciation. There has been only 6000$ increase in the

value of Machinery and in case 15% depreciation is calculated then the value of depreciation

comes out with 900$. Therefore, the item is material as the increase is not in consonance with the

increase in the value of machinery.

Expense June

2016

December 2016 June 2017 - YTD Increase %age

Depreciation 15863 8095 16190 327 2.06

ASSERTION AND EXPLANATION

Reliability is the assertion observed as the amount of increase in depreciation is very small and

thus not reliable for the users of the financial statements (Vasarhelyi, 2014).

RECOMMENDED AUDIT PROCEDURE

The audit team shall check the purchase bills of machinery and shall verify the calculation of the

depreciation and disclose if there is any change in the method of depreciation and its necessary

impact on the financial health of the company.

Assertion placed is the occurrence and the completeness. It is because there might be the chances

that the sales which have been occurred for the entity has not been recorded in the financial

statements due to which the sales figure has not been increased by at least 10% (Kharisova,

2014).

RECOMMENDED AUDIT PROCEDURE

Audit team is required to check each and every sale bills with the ledger confirmation from the

customers.

DEPRECIATION

RATIONALE FOR SELECTION

The amount of the depreciation has been increased by 4% which depicts that the company has

changed the method of calculation of the depreciation. There has been only 6000$ increase in the

value of Machinery and in case 15% depreciation is calculated then the value of depreciation

comes out with 900$. Therefore, the item is material as the increase is not in consonance with the

increase in the value of machinery.

Expense June

2016

December 2016 June 2017 - YTD Increase %age

Depreciation 15863 8095 16190 327 2.06

ASSERTION AND EXPLANATION

Reliability is the assertion observed as the amount of increase in depreciation is very small and

thus not reliable for the users of the financial statements (Vasarhelyi, 2014).

RECOMMENDED AUDIT PROCEDURE

The audit team shall check the purchase bills of machinery and shall verify the calculation of the

depreciation and disclose if there is any change in the method of depreciation and its necessary

impact on the financial health of the company.

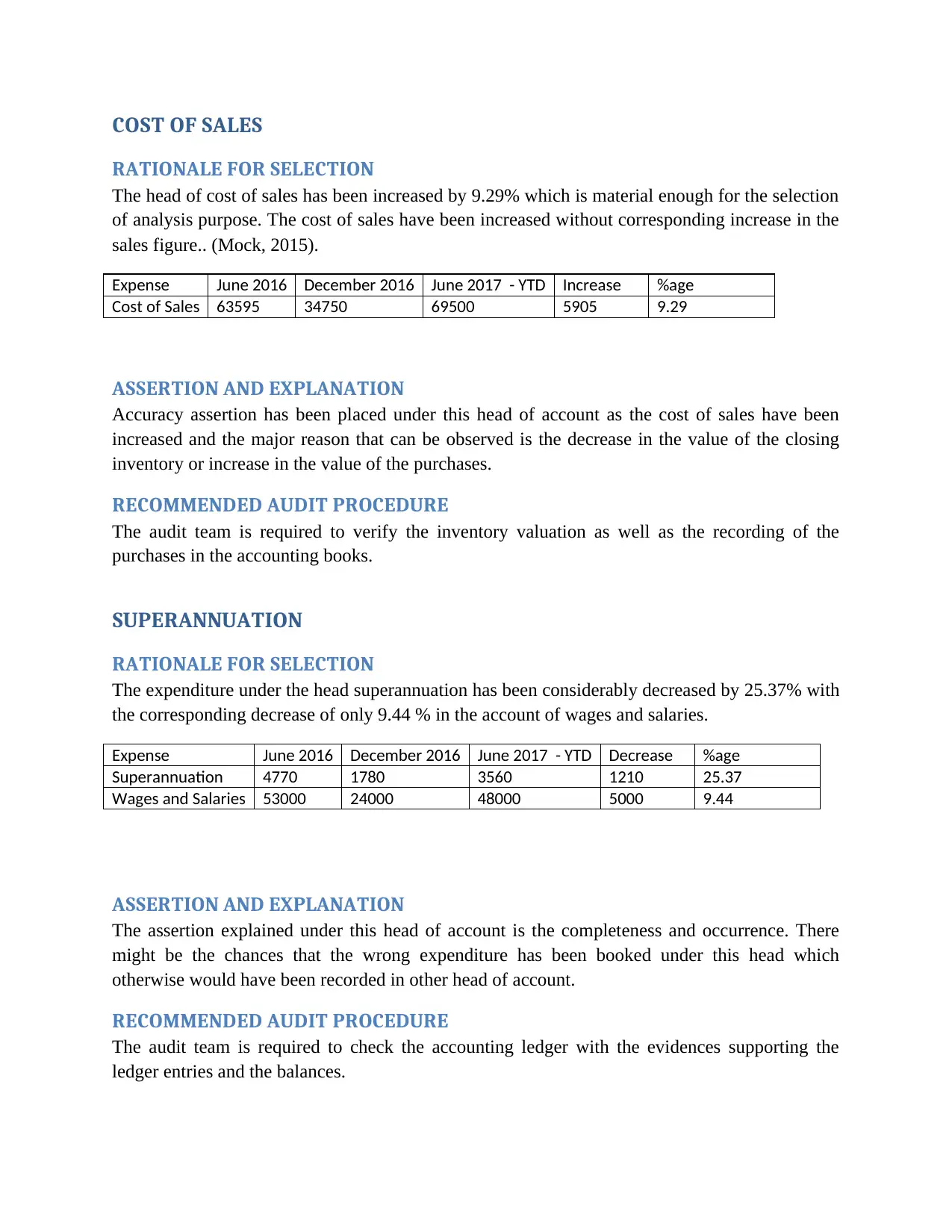

COST OF SALES

RATIONALE FOR SELECTION

The head of cost of sales has been increased by 9.29% which is material enough for the selection

of analysis purpose. The cost of sales have been increased without corresponding increase in the

sales figure.. (Mock, 2015).

Expense June 2016 December 2016 June 2017 - YTD Increase %age

Cost of Sales 63595 34750 69500 5905 9.29

ASSERTION AND EXPLANATION

Accuracy assertion has been placed under this head of account as the cost of sales have been

increased and the major reason that can be observed is the decrease in the value of the closing

inventory or increase in the value of the purchases.

RECOMMENDED AUDIT PROCEDURE

The audit team is required to verify the inventory valuation as well as the recording of the

purchases in the accounting books.

SUPERANNUATION

RATIONALE FOR SELECTION

The expenditure under the head superannuation has been considerably decreased by 25.37% with

the corresponding decrease of only 9.44 % in the account of wages and salaries.

Expense June 2016 December 2016 June 2017 - YTD Decrease %age

Superannuation 4770 1780 3560 1210 25.37

Wages and Salaries 53000 24000 48000 5000 9.44

ASSERTION AND EXPLANATION

The assertion explained under this head of account is the completeness and occurrence. There

might be the chances that the wrong expenditure has been booked under this head which

otherwise would have been recorded in other head of account.

RECOMMENDED AUDIT PROCEDURE

The audit team is required to check the accounting ledger with the evidences supporting the

ledger entries and the balances.

RATIONALE FOR SELECTION

The head of cost of sales has been increased by 9.29% which is material enough for the selection

of analysis purpose. The cost of sales have been increased without corresponding increase in the

sales figure.. (Mock, 2015).

Expense June 2016 December 2016 June 2017 - YTD Increase %age

Cost of Sales 63595 34750 69500 5905 9.29

ASSERTION AND EXPLANATION

Accuracy assertion has been placed under this head of account as the cost of sales have been

increased and the major reason that can be observed is the decrease in the value of the closing

inventory or increase in the value of the purchases.

RECOMMENDED AUDIT PROCEDURE

The audit team is required to verify the inventory valuation as well as the recording of the

purchases in the accounting books.

SUPERANNUATION

RATIONALE FOR SELECTION

The expenditure under the head superannuation has been considerably decreased by 25.37% with

the corresponding decrease of only 9.44 % in the account of wages and salaries.

Expense June 2016 December 2016 June 2017 - YTD Decrease %age

Superannuation 4770 1780 3560 1210 25.37

Wages and Salaries 53000 24000 48000 5000 9.44

ASSERTION AND EXPLANATION

The assertion explained under this head of account is the completeness and occurrence. There

might be the chances that the wrong expenditure has been booked under this head which

otherwise would have been recorded in other head of account.

RECOMMENDED AUDIT PROCEDURE

The audit team is required to check the accounting ledger with the evidences supporting the

ledger entries and the balances.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-study-

resources/p7/technical-articles/analytical-procedures.html accessed on 08-10-2017.

Abidin, S., & Baabbad, M. A. (2015), “The use of analytical procedures by yemeni

auditors”,Corporate Ownership & Control, 12(2), 17-25.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 08-10-2017

Chen, S., & Tsay, B. Y. (2017), “Refer to Materiality as a Legal Concept”. Journal of

Corporate Accounting & Finance, 28(2), 55-61.

Glover, S. M., Prawitt, D. F., & Drake, M. S. (2014), “Between a Rock and a Hard Place: A Path

Forward for Using Substantive Analytical Procedures in Auditing Large P&L

Accounts:Commentary and Analysis”. Auditing: A Journal of Practice & Theory, 34(3), 161-

179.

Kharisova, F. I., (2014), “Applying the category of Assertions (or preconditions)» in audit of

financial statement”. Mediterranean Journal of Social Sciences, 5(24), 180

Langevoort, D. C. (2015), “Judgment Day for Fraud-on-the-Market: Reflections on Amgen and

the Second Coming of Halliburton”. Ariz. L. Rev., 57, 37.

Leung P, Coram P, Copper B and Richardson P, (2015), “Modern Auditing and Assurance

Services”, Wiley John and Sons, Ed. 6, Pp 425-463, 582-684.

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-study-

resources/p7/technical-articles/analytical-procedures.html accessed on 08-10-2017.

Abidin, S., & Baabbad, M. A. (2015), “The use of analytical procedures by yemeni

auditors”,Corporate Ownership & Control, 12(2), 17-25.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 08-10-2017

Chen, S., & Tsay, B. Y. (2017), “Refer to Materiality as a Legal Concept”. Journal of

Corporate Accounting & Finance, 28(2), 55-61.

Glover, S. M., Prawitt, D. F., & Drake, M. S. (2014), “Between a Rock and a Hard Place: A Path

Forward for Using Substantive Analytical Procedures in Auditing Large P&L

Accounts:Commentary and Analysis”. Auditing: A Journal of Practice & Theory, 34(3), 161-

179.

Kharisova, F. I., (2014), “Applying the category of Assertions (or preconditions)» in audit of

financial statement”. Mediterranean Journal of Social Sciences, 5(24), 180

Langevoort, D. C. (2015), “Judgment Day for Fraud-on-the-Market: Reflections on Amgen and

the Second Coming of Halliburton”. Ariz. L. Rev., 57, 37.

Leung P, Coram P, Copper B and Richardson P, (2015), “Modern Auditing and Assurance

Services”, Wiley John and Sons, Ed. 6, Pp 425-463, 582-684.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mao, M., (2014), “Experimental Methods of Materiality Judgment on Auditor’s Experience

and Performance” In 3rd International Conference on Science and Social Research

(ICSSR 2014) Atlantis Press.

Mock, T. J, (2015). “Auditors' Risk Assessments: The Effects of Elicitation Approach and

Assertion Framing” Behavioral Research in Accounting, 28(2), 75-84.

PCAOB, (2017), “Analytical Procedures” available at

https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx accessed on 08-10-2017

Ullah A, (2014), “Planning and Audit of Financial Statements” available on

http://leaccountant.com/2014/12/08/asa-300-summary-planning-an-audit-of-financial -

statements/ accessed on 08-10-2017

Vasarhelyi, M. A., (2014), “Embracing the Automated Audit: How the Audit Data Standards and

Audit Tools Can Enhance Auditor Judgment and Assurance” Journal of

accountancy, 217(4), 34.

APPENDIX

Calamansi Enterprises

Ratio Analysis

Jul 1, 2016 - Dec 31, 2016

Jul 1, 2015 - June 30,

2016

Current Assets 390,840 365,000

Current Liability 0 0

Working Capital 390,840 365,000

Cost of Sales 34,750 63,595

Sales 94,500 187,450

Costs % of Sales 36.77% 33.93%

and Performance” In 3rd International Conference on Science and Social Research

(ICSSR 2014) Atlantis Press.

Mock, T. J, (2015). “Auditors' Risk Assessments: The Effects of Elicitation Approach and

Assertion Framing” Behavioral Research in Accounting, 28(2), 75-84.

PCAOB, (2017), “Analytical Procedures” available at

https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx accessed on 08-10-2017

Ullah A, (2014), “Planning and Audit of Financial Statements” available on

http://leaccountant.com/2014/12/08/asa-300-summary-planning-an-audit-of-financial -

statements/ accessed on 08-10-2017

Vasarhelyi, M. A., (2014), “Embracing the Automated Audit: How the Audit Data Standards and

Audit Tools Can Enhance Auditor Judgment and Assurance” Journal of

accountancy, 217(4), 34.

APPENDIX

Calamansi Enterprises

Ratio Analysis

Jul 1, 2016 - Dec 31, 2016

Jul 1, 2015 - June 30,

2016

Current Assets 390,840 365,000

Current Liability 0 0

Working Capital 390,840 365,000

Cost of Sales 34,750 63,595

Sales 94,500 187,450

Costs % of Sales 36.77% 33.93%

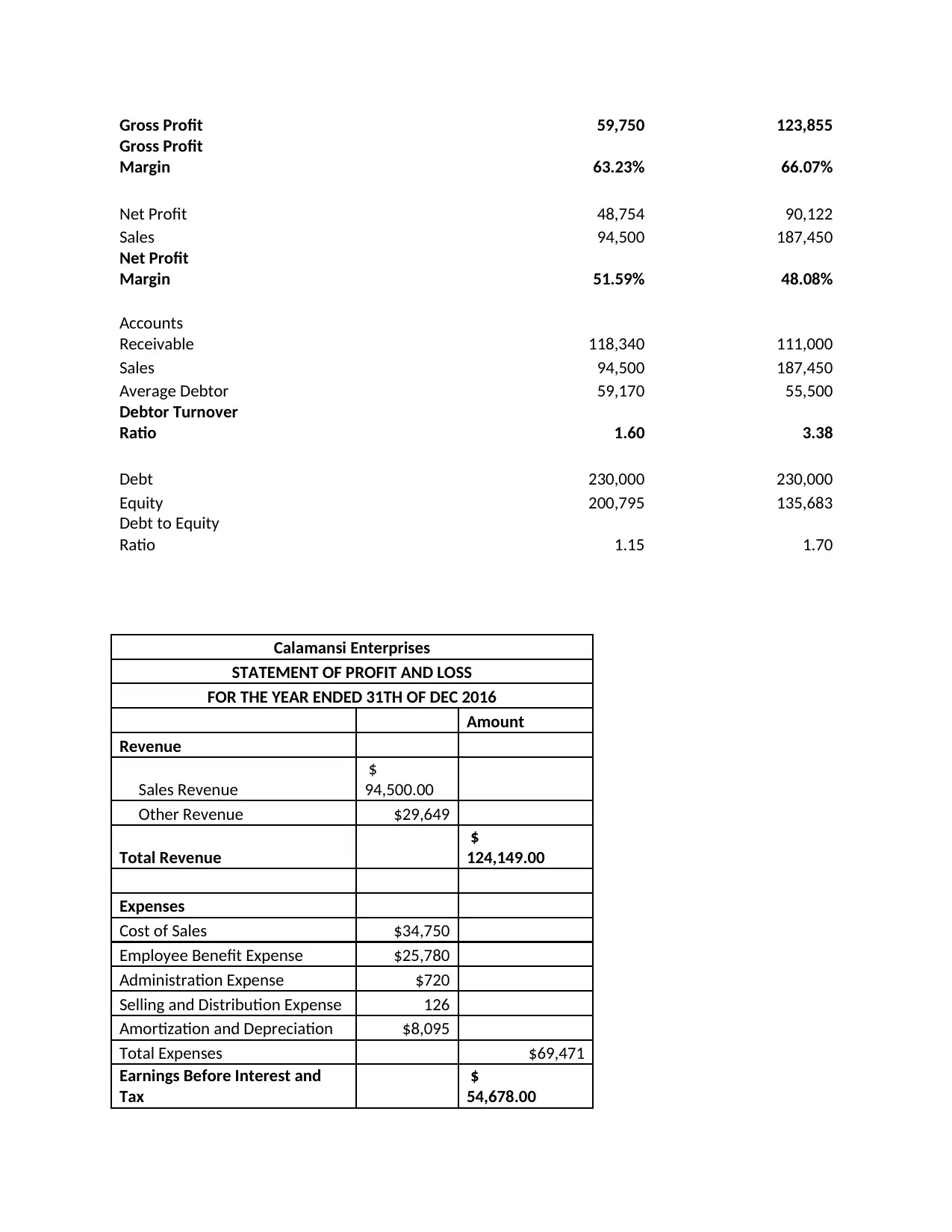

Gross Profit 59,750 123,855

Gross Profit

Margin 63.23% 66.07%

Net Profit 48,754 90,122

Sales 94,500 187,450

Net Profit

Margin 51.59% 48.08%

Accounts

Receivable 118,340 111,000

Sales 94,500 187,450

Average Debtor 59,170 55,500

Debtor Turnover

Ratio 1.60 3.38

Debt 230,000 230,000

Equity 200,795 135,683

Debt to Equity

Ratio 1.15 1.70

Calamansi Enterprises

STATEMENT OF PROFIT AND LOSS

FOR THE YEAR ENDED 31TH OF DEC 2016

Amount

Revenue

Sales Revenue

$

94,500.00

Other Revenue $29,649

Total Revenue

$

124,149.00

Expenses

Cost of Sales $34,750

Employee Benefit Expense $25,780

Administration Expense $720

Selling and Distribution Expense 126

Amortization and Depreciation $8,095

Total Expenses $69,471

Earnings Before Interest and

Tax

$

54,678.00

Gross Profit

Margin 63.23% 66.07%

Net Profit 48,754 90,122

Sales 94,500 187,450

Net Profit

Margin 51.59% 48.08%

Accounts

Receivable 118,340 111,000

Sales 94,500 187,450

Average Debtor 59,170 55,500

Debtor Turnover

Ratio 1.60 3.38

Debt 230,000 230,000

Equity 200,795 135,683

Debt to Equity

Ratio 1.15 1.70

Calamansi Enterprises

STATEMENT OF PROFIT AND LOSS

FOR THE YEAR ENDED 31TH OF DEC 2016

Amount

Revenue

Sales Revenue

$

94,500.00

Other Revenue $29,649

Total Revenue

$

124,149.00

Expenses

Cost of Sales $34,750

Employee Benefit Expense $25,780

Administration Expense $720

Selling and Distribution Expense 126

Amortization and Depreciation $8,095

Total Expenses $69,471

Earnings Before Interest and

Tax

$

54,678.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.