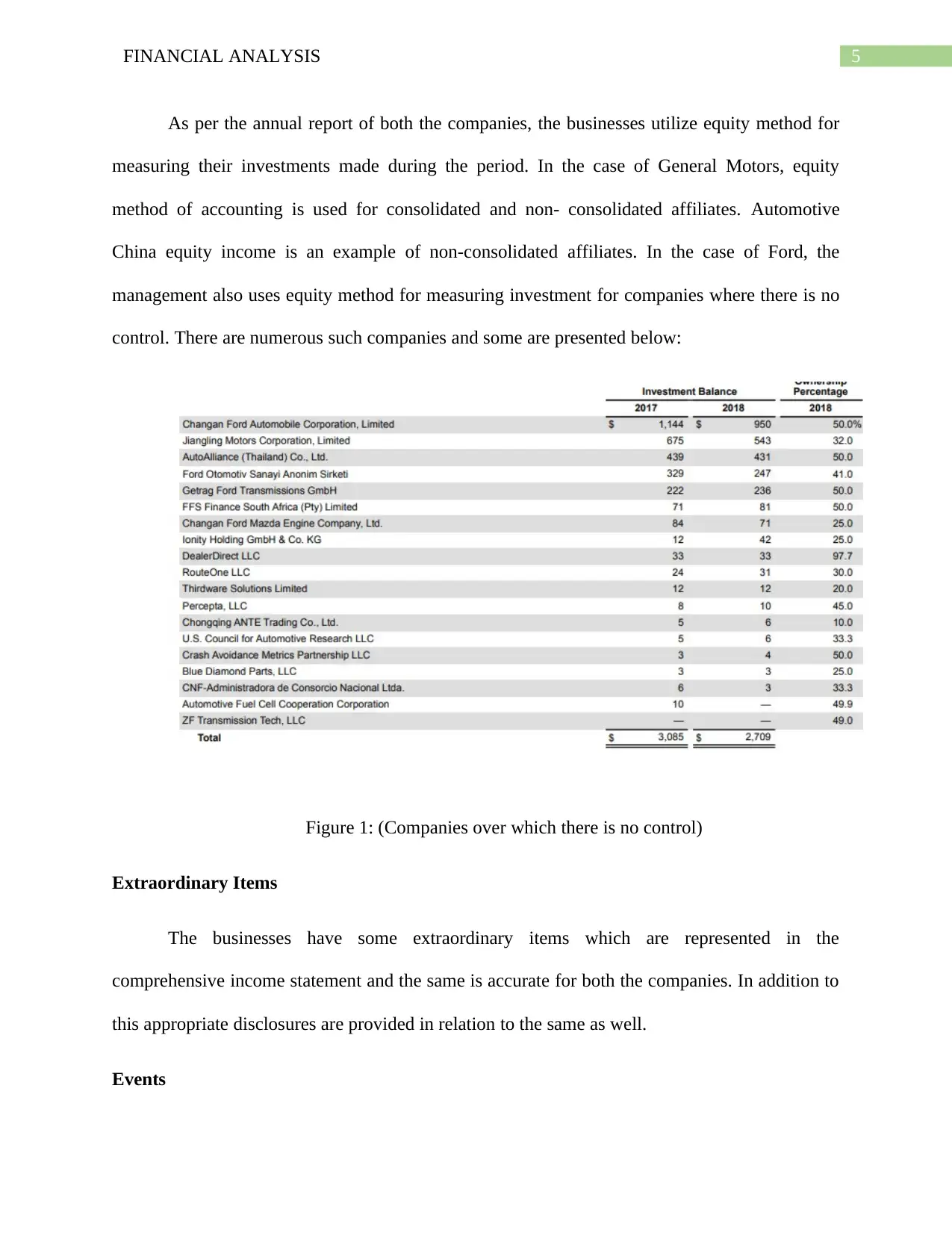

Financial Analysis Report: Comparing Ford and General Motors

VerifiedAdded on 2022/08/12

|8

|1637

|29

Report

AI Summary

This report presents a detailed financial analysis comparing Ford Motor Company and General Motors, two major players in the automotive industry. The analysis, conducted as part of an ACC 685 assignment, utilizes financial statements from the companies' 10-K filings to evaluate their performance across various metrics. The report begins with an introduction to the companies and the scope of the analysis. It then delves into ratio analysis, covering liquidity, capital structure, return on investment, operating performance, asset utilization, and market measures. The report also examines the accounting methods used by both companies, including those for leases, inventory, depreciation, and intangibles. It further discusses disclosures related to contingencies, accounting changes, financial instruments, long-term debt, incentive programs, pension benefits, and income taxes. The report concludes with an investment decision based on the 2018 financial performance, recommending an investment strategy based on the analysis conducted. The report uses common size financial statements and computes ratios such as current ratio, acid-test ratio, debt-to-equity, return on assets, and price-to-earnings ratio, among others. The analysis also incorporates information from recent quarterly filings (10-Q) to provide a comprehensive overview of the companies' financial health. The report covers the key financial ratios, accounting methods, and provides insights into the companies' financial health and investment potential.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.