ACCY801: Financial Performance Analysis and Comparison of AX1 and NCK

VerifiedAdded on 2022/09/15

|15

|3788

|17

Report

AI Summary

This report presents a comparative financial analysis of two companies, AX1 and NCK, focusing on their performance in key areas. The analysis begins with an executive summary outlining the objectives and evaluation of each company's position. It includes a table of contents and an introduction setting the stage for the comparative study. The report delves into the companies' objectives and long-term plans, followed by a detailed examination of financial ratios, including liquidity, capital structure, asset management efficiency, operating profitability, and returns on shareholders' investment. The report highlights the strengths and weaknesses of each company, offering recommendations for improvement, particularly for AX1, in areas such as liquidity and asset utilization. The analysis is based on the 2019 financial data and includes calculations of various financial ratios, providing insights into the companies' financial health and strategic decisions. The report concludes with recommendations for improvement and references to support the analysis, along with an appendix for additional data.

1

Accounting & Financial Management

Accounting & Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

The company evaluation is made in the report for NCK and AX1 and in that, all of the

important elements have been covered. There is the identification of the objectives and then

the position and performance are evaluated in an effective manner. the calculation of the

ratios is made and by that, it has been determined that the company needs improvement the

performance and position both are maintained in a better manner by the NCK and it is

considered as the competitor. There are various areas in which the improvement will be made

and for that, the investment will be made in assets. This will be improving the liquidity

position of the business and also the utilization of them shall be made appropriately by the

management. This efficiency will lead to a positive impact on the turnover of the company.

There will be a reduction in the expenses which will be made and that will help in improving

the profits which will add to the further benefits. The shareholder returns will be increasing

and that will also be affecting the further funding which will be required in the company. All

of these actions will be incorporated by the management so that required improvements are

made and success is attained.

Executive summary

The company evaluation is made in the report for NCK and AX1 and in that, all of the

important elements have been covered. There is the identification of the objectives and then

the position and performance are evaluated in an effective manner. the calculation of the

ratios is made and by that, it has been determined that the company needs improvement the

performance and position both are maintained in a better manner by the NCK and it is

considered as the competitor. There are various areas in which the improvement will be made

and for that, the investment will be made in assets. This will be improving the liquidity

position of the business and also the utilization of them shall be made appropriately by the

management. This efficiency will lead to a positive impact on the turnover of the company.

There will be a reduction in the expenses which will be made and that will help in improving

the profits which will add to the further benefits. The shareholder returns will be increasing

and that will also be affecting the further funding which will be required in the company. All

of these actions will be incorporated by the management so that required improvements are

made and success is attained.

3

Table of Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Objectives and long term plans..................................................................................................4

Financial ratios...........................................................................................................................6

Liquidity, Capital structure and asset management efficiency..................................................6

Operating profitability................................................................................................................8

Returns on shareholders’ investment.......................................................................................10

Capital expenditures.................................................................................................................11

Conclusion and recommendations...........................................................................................11

References................................................................................................................................13

Appendix..................................................................................................................................15

Table of Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Objectives and long term plans..................................................................................................4

Financial ratios...........................................................................................................................6

Liquidity, Capital structure and asset management efficiency..................................................6

Operating profitability................................................................................................................8

Returns on shareholders’ investment.......................................................................................10

Capital expenditures.................................................................................................................11

Conclusion and recommendations...........................................................................................11

References................................................................................................................................13

Appendix..................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

The analysis is required to be performed in the business by which all the areas and their

performance can be evaluated. In this report, there will be consideration of the AXI and NCK

which are the companies to be used for the evaluation purpose. The various aspects in

relation to them will be undertaken and that will help in making the proper comparison

among them. The issues which are involved will be identified so that the analysis can be used

to provide the management with the recommendation in this respect. The use of ratio analysis

will be made that will be covering various calculations. They will help in ascertaining the

financial position and performance of the business which is necessary to take further

decisions and make the situation better. There will be involvement of the return which is

made by the shareholders on the investment so that the same can be evaluated and the coming

period can be considered on that basis. The main capital expenditures which are made in the

business together with the source which is used to finance them will be identified in the

report.

Objectives and long term plans

The companies which are involved have been framed with a certain objective that will be

required to be achieved and for that various actions are taken. They are the main aim for

which the various policies and procedures are followed. In the NCK there are various short

and medium-term objectives that are set in order to attain something which is beneficial in

the long-run. There are various resources that are involved and it is important that they are

allocated in an adequate manner. For this, the objectives are set and the complete process is

carried in the best possible manner (NCK, 2019). There are several interests and other risks

which are involved with the company and it is highly required that they are eliminated. For

Introduction

The analysis is required to be performed in the business by which all the areas and their

performance can be evaluated. In this report, there will be consideration of the AXI and NCK

which are the companies to be used for the evaluation purpose. The various aspects in

relation to them will be undertaken and that will help in making the proper comparison

among them. The issues which are involved will be identified so that the analysis can be used

to provide the management with the recommendation in this respect. The use of ratio analysis

will be made that will be covering various calculations. They will help in ascertaining the

financial position and performance of the business which is necessary to take further

decisions and make the situation better. There will be involvement of the return which is

made by the shareholders on the investment so that the same can be evaluated and the coming

period can be considered on that basis. The main capital expenditures which are made in the

business together with the source which is used to finance them will be identified in the

report.

Objectives and long term plans

The companies which are involved have been framed with a certain objective that will be

required to be achieved and for that various actions are taken. They are the main aim for

which the various policies and procedures are followed. In the NCK there are various short

and medium-term objectives that are set in order to attain something which is beneficial in

the long-run. There are various resources that are involved and it is important that they are

allocated in an adequate manner. For this, the objectives are set and the complete process is

carried in the best possible manner (NCK, 2019). There are several interests and other risks

which are involved with the company and it is highly required that they are eliminated. For

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

this, the company makes various risk management objectives and they help in controlling the

risk which has a negative impact on the business.

In the NCK there are various long-term goals that are set and by that the long-term gains will

be attained by the business. There is a plan which has been formulated under which four new

stores will be opened. This plan will be making the network strong and by that, the company

will be available in all areas to provide the customers with the required services and products

which will be beneficial for them.

The AX1 is also operating and is having the objectives which are required to be fulfilled by

it. The main among all is the growth plan objective and under that, the consideration is given

to the investments which are innovation-driven and are in the store formats, digital

capabilities, new business development and store environment. With the help of them, it will

be ensured that the customers are given the high-class experience and there will be growth in

the value of shareholders (AX1. (2019). There is the focus made on the overall improvement

of all the areas by which combined improvement will be made. The interest of all the parties

will be combined so that they will be working in one direction for the attainment of the same

goal and objective.

There is a growth plan which is prepared by the group and in that various aspects have been

covered. There will be the opening of 40 new stores looking to attractive deals and the

strength which is available in the market. There are estimations by which the positive cash

flow is considered by these plans. There will also be the opening of corporate stores by which

the sales and the profit margin will be affected in a positive direction.

this, the company makes various risk management objectives and they help in controlling the

risk which has a negative impact on the business.

In the NCK there are various long-term goals that are set and by that the long-term gains will

be attained by the business. There is a plan which has been formulated under which four new

stores will be opened. This plan will be making the network strong and by that, the company

will be available in all areas to provide the customers with the required services and products

which will be beneficial for them.

The AX1 is also operating and is having the objectives which are required to be fulfilled by

it. The main among all is the growth plan objective and under that, the consideration is given

to the investments which are innovation-driven and are in the store formats, digital

capabilities, new business development and store environment. With the help of them, it will

be ensured that the customers are given the high-class experience and there will be growth in

the value of shareholders (AX1. (2019). There is the focus made on the overall improvement

of all the areas by which combined improvement will be made. The interest of all the parties

will be combined so that they will be working in one direction for the attainment of the same

goal and objective.

There is a growth plan which is prepared by the group and in that various aspects have been

covered. There will be the opening of 40 new stores looking to attractive deals and the

strength which is available in the market. There are estimations by which the positive cash

flow is considered by these plans. There will also be the opening of corporate stores by which

the sales and the profit margin will be affected in a positive direction.

6

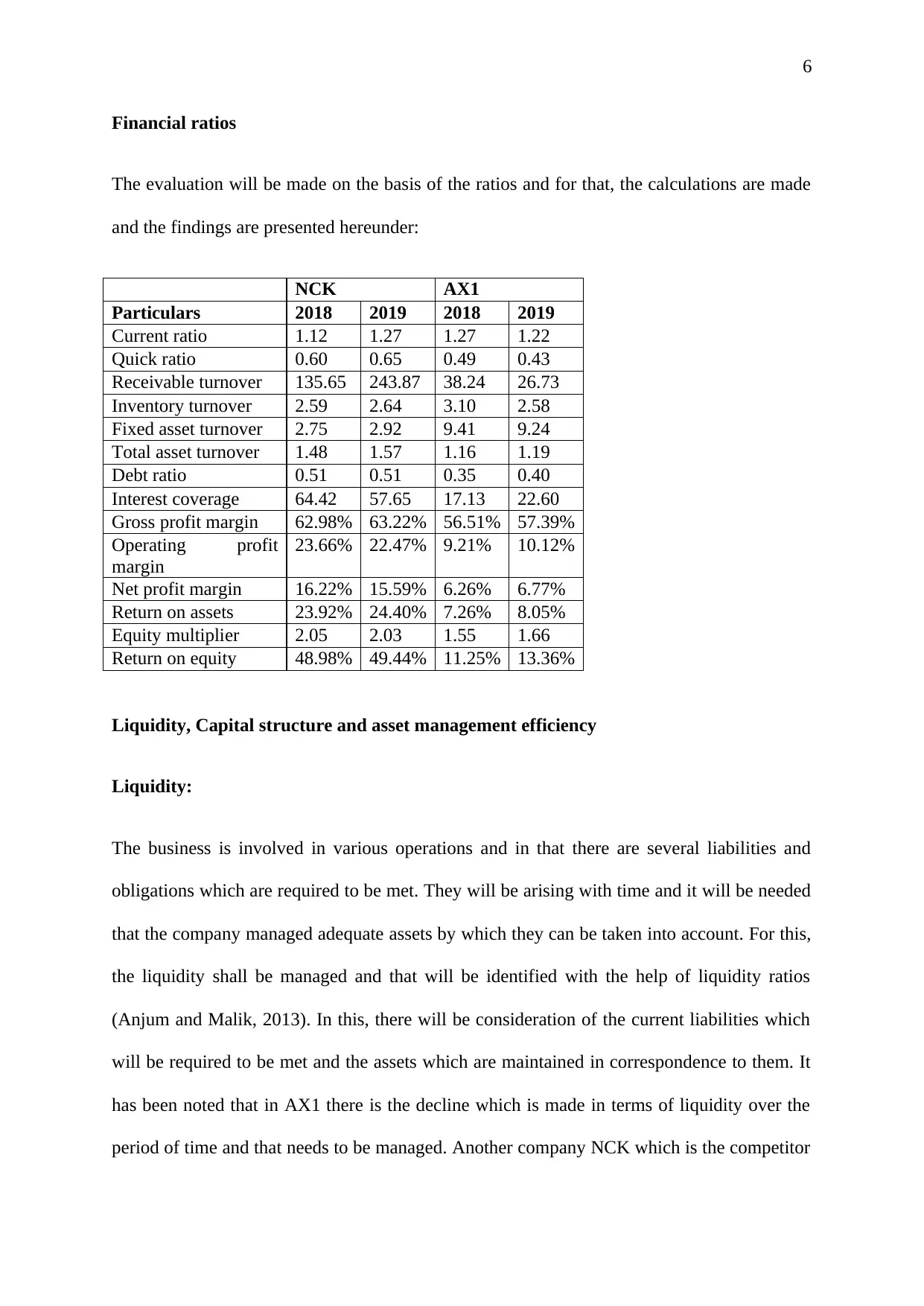

Financial ratios

The evaluation will be made on the basis of the ratios and for that, the calculations are made

and the findings are presented hereunder:

NCK AX1

Particulars 2018 2019 2018 2019

Current ratio 1.12 1.27 1.27 1.22

Quick ratio 0.60 0.65 0.49 0.43

Receivable turnover 135.65 243.87 38.24 26.73

Inventory turnover 2.59 2.64 3.10 2.58

Fixed asset turnover 2.75 2.92 9.41 9.24

Total asset turnover 1.48 1.57 1.16 1.19

Debt ratio 0.51 0.51 0.35 0.40

Interest coverage 64.42 57.65 17.13 22.60

Gross profit margin 62.98% 63.22% 56.51% 57.39%

Operating profit

margin

23.66% 22.47% 9.21% 10.12%

Net profit margin 16.22% 15.59% 6.26% 6.77%

Return on assets 23.92% 24.40% 7.26% 8.05%

Equity multiplier 2.05 2.03 1.55 1.66

Return on equity 48.98% 49.44% 11.25% 13.36%

Liquidity, Capital structure and asset management efficiency

Liquidity:

The business is involved in various operations and in that there are several liabilities and

obligations which are required to be met. They will be arising with time and it will be needed

that the company managed adequate assets by which they can be taken into account. For this,

the liquidity shall be managed and that will be identified with the help of liquidity ratios

(Anjum and Malik, 2013). In this, there will be consideration of the current liabilities which

will be required to be met and the assets which are maintained in correspondence to them. It

has been noted that in AX1 there is the decline which is made in terms of liquidity over the

period of time and that needs to be managed. Another company NCK which is the competitor

Financial ratios

The evaluation will be made on the basis of the ratios and for that, the calculations are made

and the findings are presented hereunder:

NCK AX1

Particulars 2018 2019 2018 2019

Current ratio 1.12 1.27 1.27 1.22

Quick ratio 0.60 0.65 0.49 0.43

Receivable turnover 135.65 243.87 38.24 26.73

Inventory turnover 2.59 2.64 3.10 2.58

Fixed asset turnover 2.75 2.92 9.41 9.24

Total asset turnover 1.48 1.57 1.16 1.19

Debt ratio 0.51 0.51 0.35 0.40

Interest coverage 64.42 57.65 17.13 22.60

Gross profit margin 62.98% 63.22% 56.51% 57.39%

Operating profit

margin

23.66% 22.47% 9.21% 10.12%

Net profit margin 16.22% 15.59% 6.26% 6.77%

Return on assets 23.92% 24.40% 7.26% 8.05%

Equity multiplier 2.05 2.03 1.55 1.66

Return on equity 48.98% 49.44% 11.25% 13.36%

Liquidity, Capital structure and asset management efficiency

Liquidity:

The business is involved in various operations and in that there are several liabilities and

obligations which are required to be met. They will be arising with time and it will be needed

that the company managed adequate assets by which they can be taken into account. For this,

the liquidity shall be managed and that will be identified with the help of liquidity ratios

(Anjum and Malik, 2013). In this, there will be consideration of the current liabilities which

will be required to be met and the assets which are maintained in correspondence to them. It

has been noted that in AX1 there is the decline which is made in terms of liquidity over the

period of time and that needs to be managed. Another company NCK which is the competitor

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

of AX1 in the market is, on the other hand, maintaining a positive liquidity position. There is

an increase in the ratios which are taking place and that shows the company is moving in the

proper direction. The current ratio and quick ratio which are maintained by AX1 are 1.22 and

0.43 in 2019 but for NCK there is a ratio of 1.27 and 0.65 respectively. It can be said that

while making the comparison the position of NCK is better and AX1 is required to make the

improvement.

There will be increment that will be made in assets and also the liabilities will be reduced by

taking the required actions. The overall performance will be made better when the set

standards in this respect will be attained.

Capital structure:

The maintenance of the capital structure is an important decision for any business and it is

required that there shall be consideration of all the important points while making this

decision. The other activities which are performed are also affected by the same and so the

correct structure becomes all the more important. In that, there is the consideration of the

proportion in which the various assets and liabilities are maintained (Delen, Kuzey and Uyar,

2013). The ratios are calculated for the same also and in that debt ratio and interest ratio have

been calculated. The position of the AX1 is not satisfactory as in that the amount of the

liabilities is increasing which will be creating the burden on the company. The debt position

in the case of NCK is higher than AX1 but that is maintained at a constant level and there is

no change in the same.

The interest coverage position of the company is improving and there is an increase which is

made and reached to 22.60 which is at 57.65 in 2019. The overall position of a competitor is

better but the yearly performance showed some improvement in the case of AX1 due to the

increase in the profits which are made and decline in the interest expense. This will be

of AX1 in the market is, on the other hand, maintaining a positive liquidity position. There is

an increase in the ratios which are taking place and that shows the company is moving in the

proper direction. The current ratio and quick ratio which are maintained by AX1 are 1.22 and

0.43 in 2019 but for NCK there is a ratio of 1.27 and 0.65 respectively. It can be said that

while making the comparison the position of NCK is better and AX1 is required to make the

improvement.

There will be increment that will be made in assets and also the liabilities will be reduced by

taking the required actions. The overall performance will be made better when the set

standards in this respect will be attained.

Capital structure:

The maintenance of the capital structure is an important decision for any business and it is

required that there shall be consideration of all the important points while making this

decision. The other activities which are performed are also affected by the same and so the

correct structure becomes all the more important. In that, there is the consideration of the

proportion in which the various assets and liabilities are maintained (Delen, Kuzey and Uyar,

2013). The ratios are calculated for the same also and in that debt ratio and interest ratio have

been calculated. The position of the AX1 is not satisfactory as in that the amount of the

liabilities is increasing which will be creating the burden on the company. The debt position

in the case of NCK is higher than AX1 but that is maintained at a constant level and there is

no change in the same.

The interest coverage position of the company is improving and there is an increase which is

made and reached to 22.60 which is at 57.65 in 2019. The overall position of a competitor is

better but the yearly performance showed some improvement in the case of AX1 due to the

increase in the profits which are made and decline in the interest expense. This will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

required to be further improved and for that, the debt balance will be managed in such a

manner that the cost which is involved in that respect reduces. This will also be affecting the

profitability in a positive manner and that will be the additional gain that will be made by the

company.

Asset management efficiency:

The management is responsible in relation to making the efficient use of the assets which are

available. They shall be utilized in such a manner that the revenue which is generated from

them is increased and the benefit of the same is received to the business which is positive in

the long-run. In this, there will be consideration of various assets that involve the inventory,

receivables, total assets and fixed assets (Halim et al., 2012). They help in generating the

revenue and the efficiency with which they have been utilized to generate the sales is

identified with the help of these ratios. The calculations have been made and it is identified

that the efficiency of the assets has declined in the current period and there is less

contribution which is made by them in the case of AX1. On the other hand, the reverse

situation is involved with NCK in which the ratios are increasing and that shows the

efficiency of management in using the available resources. It is required that all the assets

which are available with the AX1 will have to be used in such a manner that they contribute

to making the additional sales. This will be making the position positive and the company

will be able to deal with the competition that is available in the market.

Operating profitability

The evaluation of the profitability is made which is maintained in the company and which is

the main aim of the business. There are various operations that are performed in the business

and it is required that they are maintained in such a manner that profits arise with them. This

will be made possible when the expenses which are incurred in relation to the operations are

required to be further improved and for that, the debt balance will be managed in such a

manner that the cost which is involved in that respect reduces. This will also be affecting the

profitability in a positive manner and that will be the additional gain that will be made by the

company.

Asset management efficiency:

The management is responsible in relation to making the efficient use of the assets which are

available. They shall be utilized in such a manner that the revenue which is generated from

them is increased and the benefit of the same is received to the business which is positive in

the long-run. In this, there will be consideration of various assets that involve the inventory,

receivables, total assets and fixed assets (Halim et al., 2012). They help in generating the

revenue and the efficiency with which they have been utilized to generate the sales is

identified with the help of these ratios. The calculations have been made and it is identified

that the efficiency of the assets has declined in the current period and there is less

contribution which is made by them in the case of AX1. On the other hand, the reverse

situation is involved with NCK in which the ratios are increasing and that shows the

efficiency of management in using the available resources. It is required that all the assets

which are available with the AX1 will have to be used in such a manner that they contribute

to making the additional sales. This will be making the position positive and the company

will be able to deal with the competition that is available in the market.

Operating profitability

The evaluation of the profitability is made which is maintained in the company and which is

the main aim of the business. There are various operations that are performed in the business

and it is required that they are maintained in such a manner that profits arise with them. This

will be made possible when the expenses which are incurred in relation to the operations are

9

controlled appropriately (Kirkham, 2012). It has been noted that the profitability of the

company AX1 is improving in the current year as there is an increase in the ratios which are

determined but the same is lower than the profitability which is managed by NCK.

There is a high difference which is involved in the profits which are maintained by the

company and its competitor. There is a rise in the sales which is made and with that, the costs

which are associated with that are also increasing (Fai, Siew and Hoe, 2016). It has been

noted that there is an increase in the gross profit margin which was earlier maintained at

56.51% is not identified to be at 57.39%. There is the rise but the competitor is still

making the higher profits and for that adequate steps will be undertaken.

The Operating profit margins which are maintained are almost half of the margin that is

maintained by the competitor company. This shows that there is a high need for improvement

and then only the target can be attained and the benefit of the competition will be taken. This

will be made possible with the help of identifying the expenses which are incurred and the

proper analysis of them will be performed (Mousa, 2015). This is required as then only the

expenses which are high and are not relevant will be determined. Once this is done there will

be a proper process that will be set and according to that the reduction in the cost will be

made.

This will be making the profitability grow and businesses will be able to grow in the long-

run. The AX1 Company is growing and this will continue if it continues to carry the actions

by more care. The overall analysis involves the consideration of operations and in that the

costs which are involved will have to be accounted for. The interest expense which is

incurred by AX1 is very high in comparison to NCK. This shows that the company is

maintaining a high level of debts and on that, there are various interest expenses that are paid.

They lead to a decline in the profits and the complete profitability of the company is affected

controlled appropriately (Kirkham, 2012). It has been noted that the profitability of the

company AX1 is improving in the current year as there is an increase in the ratios which are

determined but the same is lower than the profitability which is managed by NCK.

There is a high difference which is involved in the profits which are maintained by the

company and its competitor. There is a rise in the sales which is made and with that, the costs

which are associated with that are also increasing (Fai, Siew and Hoe, 2016). It has been

noted that there is an increase in the gross profit margin which was earlier maintained at

56.51% is not identified to be at 57.39%. There is the rise but the competitor is still

making the higher profits and for that adequate steps will be undertaken.

The Operating profit margins which are maintained are almost half of the margin that is

maintained by the competitor company. This shows that there is a high need for improvement

and then only the target can be attained and the benefit of the competition will be taken. This

will be made possible with the help of identifying the expenses which are incurred and the

proper analysis of them will be performed (Mousa, 2015). This is required as then only the

expenses which are high and are not relevant will be determined. Once this is done there will

be a proper process that will be set and according to that the reduction in the cost will be

made.

This will be making the profitability grow and businesses will be able to grow in the long-

run. The AX1 Company is growing and this will continue if it continues to carry the actions

by more care. The overall analysis involves the consideration of operations and in that the

costs which are involved will have to be accounted for. The interest expense which is

incurred by AX1 is very high in comparison to NCK. This shows that the company is

maintaining a high level of debts and on that, there are various interest expenses that are paid.

They lead to a decline in the profits and the complete profitability of the company is affected

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

in an adverse manner. There are less interest costs which are involved with NCK and that

increases the earnings which are made by it. It will be required that loans are reduced and

some other source of funding is obtained. This will help in avoiding the excessive interest

cost and the profitability will be improving and beat the competition.

Returns on shareholders’ investment

Shareholders are considered to be very important in any business as they are the main source

of funds for the company. The company issues shares to raise the funds and in that

shareholders are the ones who make the investment. They provide the funds to the company

with the motive to earn the appropriate returns on their amount (Nirajini and Priya, 2013).

Due to this, the company is required to consider this and maintain adequate profits. The

payment of the return to shareholders will be made when the profits will be available and so

this shall be taken into account. For the proper analysis of this, there is the calculation of

return on equity which is made (Kara, 2012). Under this, the rate at which the return is

available to the shareholders is calculated and that helps them in taking the required decision.

The return on equity for AX1 is increasing from 11.25% to 13.36% in 2019 which is good for

the investors but if they compare the position with the competitor then they will not be

willing to make an investment. This is because of the high return which is provided by NCK

on its investments. There is a rate of 48.98% which is further increasing to 49.44% in the

current year. This is far higher than the rate provided by AX1 and so the investors will be

attracted to the competitor. In order to deal with this, the company will be required to focus

on the profits which are made and then the return on equity will be increased. This is

necessary to retain the investors from moving to other companies and to obtain the funds in

the required manner.

in an adverse manner. There are less interest costs which are involved with NCK and that

increases the earnings which are made by it. It will be required that loans are reduced and

some other source of funding is obtained. This will help in avoiding the excessive interest

cost and the profitability will be improving and beat the competition.

Returns on shareholders’ investment

Shareholders are considered to be very important in any business as they are the main source

of funds for the company. The company issues shares to raise the funds and in that

shareholders are the ones who make the investment. They provide the funds to the company

with the motive to earn the appropriate returns on their amount (Nirajini and Priya, 2013).

Due to this, the company is required to consider this and maintain adequate profits. The

payment of the return to shareholders will be made when the profits will be available and so

this shall be taken into account. For the proper analysis of this, there is the calculation of

return on equity which is made (Kara, 2012). Under this, the rate at which the return is

available to the shareholders is calculated and that helps them in taking the required decision.

The return on equity for AX1 is increasing from 11.25% to 13.36% in 2019 which is good for

the investors but if they compare the position with the competitor then they will not be

willing to make an investment. This is because of the high return which is provided by NCK

on its investments. There is a rate of 48.98% which is further increasing to 49.44% in the

current year. This is far higher than the rate provided by AX1 and so the investors will be

attracted to the competitor. In order to deal with this, the company will be required to focus

on the profits which are made and then the return on equity will be increased. This is

necessary to retain the investors from moving to other companies and to obtain the funds in

the required manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Capital expenditures

The capital projects are undertaken by the companies so that they can develop themselves and

they are such projects in which investment is once but the return is gained for the lifetime.

There are several such investments that are made in various forms and for that funds are

collected from different sources (Liang et al., 2016). The NCK has made the capital

expenditure in relation to the new showroom which has been opened. The amount which will

be contributed to the same amounts to $1118000. There is a solar panel that is installed and

by that, the energy efficiency will be upgraded which is a positive decision for the company.

The consideration in this respect is obtained with the debt funding. This expenditure will be

bringing benefits to the company and so will be in the interest of the company for a longer

duration.

The capital expenditure is also involved with the AX1 and that has been made in respect of

the non-current assets. There is an addition which is made for that the amount is incurred.

The amount which is involved in this is $12970000. The commitment in this respect has been

made but the liability in relation to the same has not been recognized yet. This is the amount

involved but the payments are not involved in this respect to date. The amount which is

considered in the accounts amounts to $61000 for the year. This has been obtained from the

borrowings which are made and in that, a particular rate of interest is paid by the company on

a timely basis.

Conclusion and recommendations

The report has been prepared and in that the analysis for the companies is made. The

consideration of the several information has been made and firstly the objective which is

there with the company has been identified and with that, the plan that is involved to attain

the same has also been determined. There is the consideration of the various aspects and in

Capital expenditures

The capital projects are undertaken by the companies so that they can develop themselves and

they are such projects in which investment is once but the return is gained for the lifetime.

There are several such investments that are made in various forms and for that funds are

collected from different sources (Liang et al., 2016). The NCK has made the capital

expenditure in relation to the new showroom which has been opened. The amount which will

be contributed to the same amounts to $1118000. There is a solar panel that is installed and

by that, the energy efficiency will be upgraded which is a positive decision for the company.

The consideration in this respect is obtained with the debt funding. This expenditure will be

bringing benefits to the company and so will be in the interest of the company for a longer

duration.

The capital expenditure is also involved with the AX1 and that has been made in respect of

the non-current assets. There is an addition which is made for that the amount is incurred.

The amount which is involved in this is $12970000. The commitment in this respect has been

made but the liability in relation to the same has not been recognized yet. This is the amount

involved but the payments are not involved in this respect to date. The amount which is

considered in the accounts amounts to $61000 for the year. This has been obtained from the

borrowings which are made and in that, a particular rate of interest is paid by the company on

a timely basis.

Conclusion and recommendations

The report has been prepared and in that the analysis for the companies is made. The

consideration of the several information has been made and firstly the objective which is

there with the company has been identified and with that, the plan that is involved to attain

the same has also been determined. There is the consideration of the various aspects and in

12

that comparison among AX1 and NCK has been made. The ratios have been calculated and

with that proper evaluation is made. The NCK is considered as the competitor of the other

company and then the explanation is provided accordingly. There is the evaluation of

liquidity, management efficiency in assets and capital structure has been considered. In that,

it has been determined that the company needs to make the improvement so that it can

compete in the market and attain a higher position. There are various shortcomings that are

involved and the manner in which they can be resolved has also been taken into

consideration. The profitability is taken into use and in that also the rates are calculated and it

is identified that AX1 is maintaining the profitability at a very low level and there is the need

to make the changes. The expenses which are incurred involve the interest which is at a

higher amount and in order to improve the profits the same will be required to be eliminated.

The returns to the shareholders are provided at a lower rate than that of the competitor and

this will prove to be disadvantageous as the investors will not invest further in the company.

This will be improved when higher returns will be provided to them and that requires the

increase in profits. Capital expenditures are considered and they will be for the benefit of the

company. Overall the improvement will be made in the AX1 so that it can achieve the

objectives and attain success in a competitive market.

that comparison among AX1 and NCK has been made. The ratios have been calculated and

with that proper evaluation is made. The NCK is considered as the competitor of the other

company and then the explanation is provided accordingly. There is the evaluation of

liquidity, management efficiency in assets and capital structure has been considered. In that,

it has been determined that the company needs to make the improvement so that it can

compete in the market and attain a higher position. There are various shortcomings that are

involved and the manner in which they can be resolved has also been taken into

consideration. The profitability is taken into use and in that also the rates are calculated and it

is identified that AX1 is maintaining the profitability at a very low level and there is the need

to make the changes. The expenses which are incurred involve the interest which is at a

higher amount and in order to improve the profits the same will be required to be eliminated.

The returns to the shareholders are provided at a lower rate than that of the competitor and

this will prove to be disadvantageous as the investors will not invest further in the company.

This will be improved when higher returns will be provided to them and that requires the

increase in profits. Capital expenditures are considered and they will be for the benefit of the

company. Overall the improvement will be made in the AX1 so that it can achieve the

objectives and attain success in a competitive market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.