Comparative Financial Analysis of Axiata Group Berhad and Digi.Com

VerifiedAdded on 2022/09/09

|27

|5822

|22

Report

AI Summary

This report presents a detailed financial analysis of Axiata Group Berhad and Digi.Com Berhad, two prominent telecommunication companies in Malaysia. The analysis begins with an introduction to the companies, followed by a comparison of their financial performance using ratio analysis across profitability, liquidity, efficiency, capital structure, and investor ratios. The report employs graphs and charts to visually represent the data, highlighting key trends and differences between the two companies over a five-year period. Strategic and operational issues are identified for each company, drawing conclusions based on the financial data. The analysis reveals that Digi generally outperforms Axiata in terms of profitability and efficiency, while Axiata demonstrates a stronger capital structure. The report also discusses the implications of these findings for investors and stakeholders. This report is a comprehensive comparative study of the financial health and strategic challenges faced by Axiata and Digi, providing valuable insights into the telecommunications industry in Malaysia.

Running head: FINANCIAL ANALYSIS AND MANAGEMENT

Financial Analysis and Management

Name of the Student

Name of the University

Author’s Note

Financial Analysis and Management

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS AND MANAGEMENT

Table of Contents

Part 1..........................................................................................................................................2

Introduction............................................................................................................................2

Introduction on the Companies..............................................................................................2

Comparison and Analysis of the Financial Performance.......................................................3

Identification of Strategic and Operational Issues...............................................................13

Conclusion............................................................................................................................16

Part 2........................................................................................................................................17

Introduction..........................................................................................................................17

Five Difference Sources of External Finance......................................................................17

Weighted Average Cost of Capital......................................................................................19

Conclusion............................................................................................................................20

References................................................................................................................................22

Table of Contents

Part 1..........................................................................................................................................2

Introduction............................................................................................................................2

Introduction on the Companies..............................................................................................2

Comparison and Analysis of the Financial Performance.......................................................3

Identification of Strategic and Operational Issues...............................................................13

Conclusion............................................................................................................................16

Part 2........................................................................................................................................17

Introduction..........................................................................................................................17

Five Difference Sources of External Finance......................................................................17

Weighted Average Cost of Capital......................................................................................19

Conclusion............................................................................................................................20

References................................................................................................................................22

2FINANCIAL ANALYSIS AND MANAGEMENT

Part 1

Introduction

Determination of the overall financial health of a company demands assessing and

evaluating both financial performance and position of the same company with the use of

different financial analysis techniques. This helps the investors, creditors and other

stakeholders to know the trend of financial performance of the companies. In this regard,

analysis of ratios is considered as a major technique for assessing and comparing the financial

performance of more than one companies (Fatihudin 2018). In addition, the use of graphs and

charts largely helps in the analysis. This report intends at analysing as well as evaluating the

financial performance and financial position of two companies operating in the

telecommunication industry of Malaysia. These two companies are Axiata Group Berhad

(Axiata) and Digi.Com Berhad (Digi) that is the competitor company; and both of these

companies are listed in Bursa Malaysia. This report also discusses about the strategic and

operational issues in these two companies.

Introduction on the Companies

Axiata is considered a major telecommunication companies in Asia. The

transformation of this companies can be seen from a holding business entity with a portfolio

of pure-play mobile assets into a Triple Core Strategy-driven business organization with a

focus on Digital Telco, Digital Businesses and communication infrastructure. The main

products of the company include mobile network operation, network infrustrurure and digital

internet (axiata.com 2019). Digi is a major Malaysian company involves in providing mobile

connectivity and internet services on its advanced G+ network. Digi is famous for providing

its customers with relevant, personalized and engaging digital products and services with the

aim to enhance their digital lifestyle. The key product line of the business include mobile

Part 1

Introduction

Determination of the overall financial health of a company demands assessing and

evaluating both financial performance and position of the same company with the use of

different financial analysis techniques. This helps the investors, creditors and other

stakeholders to know the trend of financial performance of the companies. In this regard,

analysis of ratios is considered as a major technique for assessing and comparing the financial

performance of more than one companies (Fatihudin 2018). In addition, the use of graphs and

charts largely helps in the analysis. This report intends at analysing as well as evaluating the

financial performance and financial position of two companies operating in the

telecommunication industry of Malaysia. These two companies are Axiata Group Berhad

(Axiata) and Digi.Com Berhad (Digi) that is the competitor company; and both of these

companies are listed in Bursa Malaysia. This report also discusses about the strategic and

operational issues in these two companies.

Introduction on the Companies

Axiata is considered a major telecommunication companies in Asia. The

transformation of this companies can be seen from a holding business entity with a portfolio

of pure-play mobile assets into a Triple Core Strategy-driven business organization with a

focus on Digital Telco, Digital Businesses and communication infrastructure. The main

products of the company include mobile network operation, network infrustrurure and digital

internet (axiata.com 2019). Digi is a major Malaysian company involves in providing mobile

connectivity and internet services on its advanced G+ network. Digi is famous for providing

its customers with relevant, personalized and engaging digital products and services with the

aim to enhance their digital lifestyle. The key product line of the business include mobile

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS AND MANAGEMENT

services, telecommunication services and cable television (ocs.digi.com.my 2019). Both

Axiata and Digi operate in the telecommunication industry of Malaysia. In case of the market

share, Digi has the maximum share in the Malaysian telecommunication industry where

Axiata has less market share as compared to Digi (statista.com 2019). As per the chairman’s

statement of Axiata, the company had to face many business risks due to the presence of

volatile macroeconomic condition, market as well as technological disruption, shift in

demand and key regulatory uncertainties across the region (axiata.listedcompany.com 2019).

On the other hand, Digi has been able in providing a solid financial performance that

provided the shareholders with healthy returns. This has provided the company with major

confidence (digi.listedcompany.com 2019). In the presence of this reasons, Digi can be

considered as a major competitor of Axiata in case it want to become the market leader.

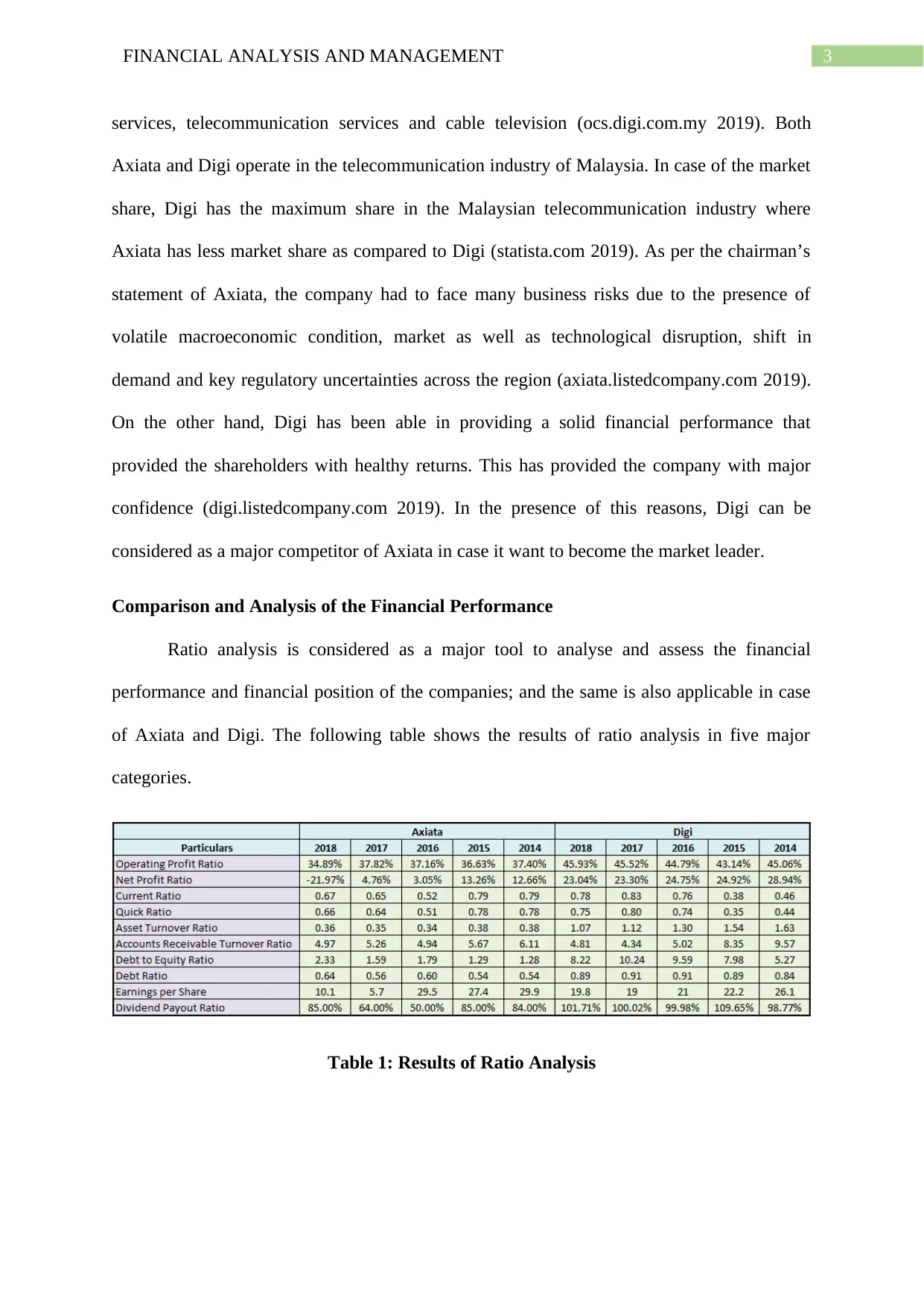

Comparison and Analysis of the Financial Performance

Ratio analysis is considered as a major tool to analyse and assess the financial

performance and financial position of the companies; and the same is also applicable in case

of Axiata and Digi. The following table shows the results of ratio analysis in five major

categories.

Table 1: Results of Ratio Analysis

services, telecommunication services and cable television (ocs.digi.com.my 2019). Both

Axiata and Digi operate in the telecommunication industry of Malaysia. In case of the market

share, Digi has the maximum share in the Malaysian telecommunication industry where

Axiata has less market share as compared to Digi (statista.com 2019). As per the chairman’s

statement of Axiata, the company had to face many business risks due to the presence of

volatile macroeconomic condition, market as well as technological disruption, shift in

demand and key regulatory uncertainties across the region (axiata.listedcompany.com 2019).

On the other hand, Digi has been able in providing a solid financial performance that

provided the shareholders with healthy returns. This has provided the company with major

confidence (digi.listedcompany.com 2019). In the presence of this reasons, Digi can be

considered as a major competitor of Axiata in case it want to become the market leader.

Comparison and Analysis of the Financial Performance

Ratio analysis is considered as a major tool to analyse and assess the financial

performance and financial position of the companies; and the same is also applicable in case

of Axiata and Digi. The following table shows the results of ratio analysis in five major

categories.

Table 1: Results of Ratio Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS AND MANAGEMENT

It can be seen from the above table that both the companies have performed

differently under the ratios. The following discussion shows the use of graphs with the aim to

compare the financial performance and position of these two selected companies.

Profitability Ratios

Axiata Digi

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

34.89%

45.93%

37.82%

45.52%

37.16%

44.79%

36.63%

43.14%

37.40%

45.06%

Operating Profit Ratio

2018 2017 2016 2015 2014

Figure 1: Operating Profit Ratio

(Source: As created by Author)

Operating profit ratio can be considered as the return that a company achieves from

standard operations. This assesses how much profit a company makes after the payment of

variable costs like raw material, wages and others (Innocent, Mary and Matthew 2013).

Operating profit ration of Axiata is less for the last five years as compared to the same ratio

of Digi for the same period. Moreover, this ratio of Axiata has decreased in the current year

where this has increased in Digi. This leads the implication that there have been certain

operational flaws in Axiata along with inefficient management of organizational resources.

Since both the companies have same operational characteristics, this is a key negative aspect

of the profitability performance of Axiata.

It can be seen from the above table that both the companies have performed

differently under the ratios. The following discussion shows the use of graphs with the aim to

compare the financial performance and position of these two selected companies.

Profitability Ratios

Axiata Digi

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

34.89%

45.93%

37.82%

45.52%

37.16%

44.79%

36.63%

43.14%

37.40%

45.06%

Operating Profit Ratio

2018 2017 2016 2015 2014

Figure 1: Operating Profit Ratio

(Source: As created by Author)

Operating profit ratio can be considered as the return that a company achieves from

standard operations. This assesses how much profit a company makes after the payment of

variable costs like raw material, wages and others (Innocent, Mary and Matthew 2013).

Operating profit ration of Axiata is less for the last five years as compared to the same ratio

of Digi for the same period. Moreover, this ratio of Axiata has decreased in the current year

where this has increased in Digi. This leads the implication that there have been certain

operational flaws in Axiata along with inefficient management of organizational resources.

Since both the companies have same operational characteristics, this is a key negative aspect

of the profitability performance of Axiata.

5FINANCIAL ANALYSIS AND MANAGEMENT

Axiata Digi

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

-21.97%

23.04%

4.76%

23.30%

3.05%

24.75%

13.26%

24.92%

12.66%

28.94%

Net Profit Ratio

2018 2017 2016 2015 2014

Figure 2: Net Profit Ratio

(Source: As created by Author)

The use of net profit ratio is seen for determining the overall efficiency of the

operationa of a company since this is an indicator of how well a firm’s trading activities are

performing. Axiata has registered net loss in the present year where Digi has registered

healthy net profit in the same period. In addition, Digi has better net profit ratio over the last

five years as compared to Axiata. It implies that Digi has performed better in term of

profitability than Axiata (Lartey, Antwi and Boadi 2013). Net loss indicates that Axiata may

have unnecessary direct and indirect cost that has contributed to net loss. This needs to be

considered as a major negative aspect of the financial performance of Axiata as compared to

Digi.

Axiata Digi

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

-21.97%

23.04%

4.76%

23.30%

3.05%

24.75%

13.26%

24.92%

12.66%

28.94%

Net Profit Ratio

2018 2017 2016 2015 2014

Figure 2: Net Profit Ratio

(Source: As created by Author)

The use of net profit ratio is seen for determining the overall efficiency of the

operationa of a company since this is an indicator of how well a firm’s trading activities are

performing. Axiata has registered net loss in the present year where Digi has registered

healthy net profit in the same period. In addition, Digi has better net profit ratio over the last

five years as compared to Axiata. It implies that Digi has performed better in term of

profitability than Axiata (Lartey, Antwi and Boadi 2013). Net loss indicates that Axiata may

have unnecessary direct and indirect cost that has contributed to net loss. This needs to be

considered as a major negative aspect of the financial performance of Axiata as compared to

Digi.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS AND MANAGEMENT

Liquidity Ratios

Axiata Digi

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.67

0.78

0.65

0.83

0.52

0.760.79

0.38

0.79

0.46

Current Ratio

2018 2017 2016 2015 2014

Figure 3: Current Ratio

(Source: As created by Author)

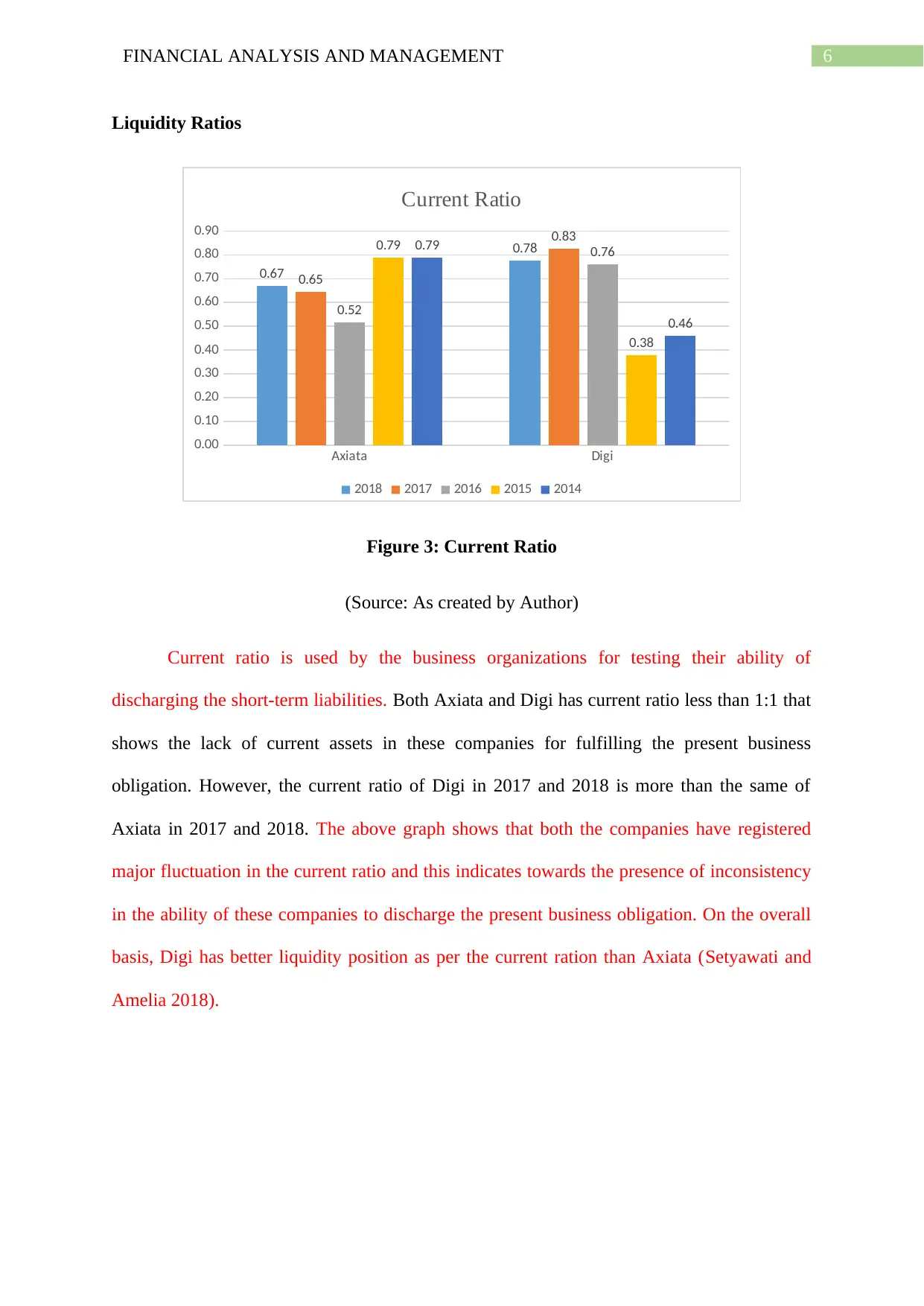

Current ratio is used by the business organizations for testing their ability of

discharging the short-term liabilities. Both Axiata and Digi has current ratio less than 1:1 that

shows the lack of current assets in these companies for fulfilling the present business

obligation. However, the current ratio of Digi in 2017 and 2018 is more than the same of

Axiata in 2017 and 2018. The above graph shows that both the companies have registered

major fluctuation in the current ratio and this indicates towards the presence of inconsistency

in the ability of these companies to discharge the present business obligation. On the overall

basis, Digi has better liquidity position as per the current ration than Axiata (Setyawati and

Amelia 2018).

Liquidity Ratios

Axiata Digi

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.67

0.78

0.65

0.83

0.52

0.760.79

0.38

0.79

0.46

Current Ratio

2018 2017 2016 2015 2014

Figure 3: Current Ratio

(Source: As created by Author)

Current ratio is used by the business organizations for testing their ability of

discharging the short-term liabilities. Both Axiata and Digi has current ratio less than 1:1 that

shows the lack of current assets in these companies for fulfilling the present business

obligation. However, the current ratio of Digi in 2017 and 2018 is more than the same of

Axiata in 2017 and 2018. The above graph shows that both the companies have registered

major fluctuation in the current ratio and this indicates towards the presence of inconsistency

in the ability of these companies to discharge the present business obligation. On the overall

basis, Digi has better liquidity position as per the current ration than Axiata (Setyawati and

Amelia 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS AND MANAGEMENT

Axiata Digi

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.66

0.75

0.64

0.80

0.51

0.74

0.78

0.35

0.78

0.44

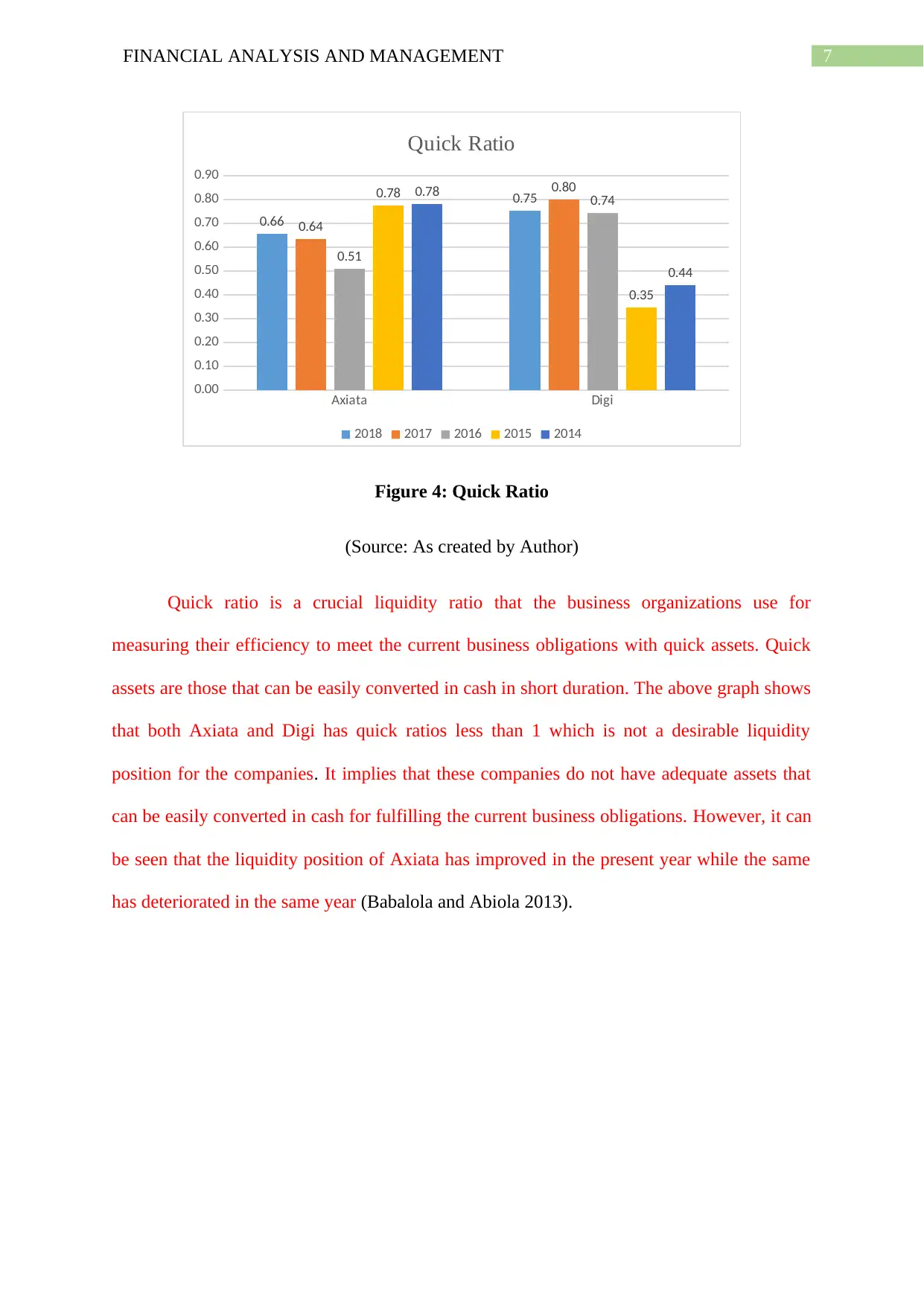

Quick Ratio

2018 2017 2016 2015 2014

Figure 4: Quick Ratio

(Source: As created by Author)

Quick ratio is a crucial liquidity ratio that the business organizations use for

measuring their efficiency to meet the current business obligations with quick assets. Quick

assets are those that can be easily converted in cash in short duration. The above graph shows

that both Axiata and Digi has quick ratios less than 1 which is not a desirable liquidity

position for the companies. It implies that these companies do not have adequate assets that

can be easily converted in cash for fulfilling the current business obligations. However, it can

be seen that the liquidity position of Axiata has improved in the present year while the same

has deteriorated in the same year (Babalola and Abiola 2013).

Axiata Digi

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.66

0.75

0.64

0.80

0.51

0.74

0.78

0.35

0.78

0.44

Quick Ratio

2018 2017 2016 2015 2014

Figure 4: Quick Ratio

(Source: As created by Author)

Quick ratio is a crucial liquidity ratio that the business organizations use for

measuring their efficiency to meet the current business obligations with quick assets. Quick

assets are those that can be easily converted in cash in short duration. The above graph shows

that both Axiata and Digi has quick ratios less than 1 which is not a desirable liquidity

position for the companies. It implies that these companies do not have adequate assets that

can be easily converted in cash for fulfilling the current business obligations. However, it can

be seen that the liquidity position of Axiata has improved in the present year while the same

has deteriorated in the same year (Babalola and Abiola 2013).

8FINANCIAL ANALYSIS AND MANAGEMENT

Efficiency Ratios

Axiata Digi

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

0.36

1.07

0.35

1.12

0.34

1.30

0.38

1.54

0.38

1.63

Asset Turnover Ratio

2018 2017 2016 2015 2014

Figure 5: Asset Turnover Ratio

(Source: As created by Author)

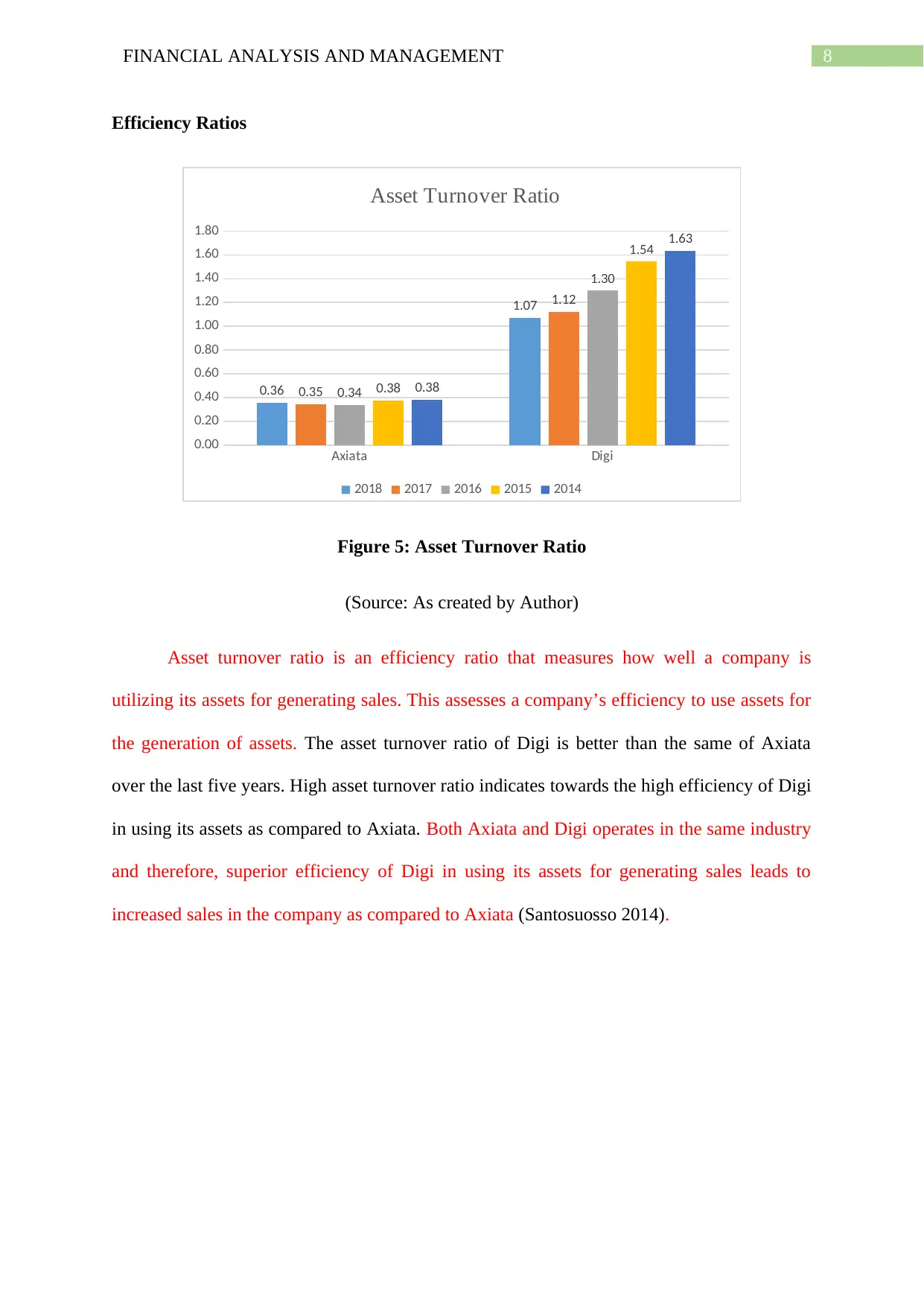

Asset turnover ratio is an efficiency ratio that measures how well a company is

utilizing its assets for generating sales. This assesses a company’s efficiency to use assets for

the generation of assets. The asset turnover ratio of Digi is better than the same of Axiata

over the last five years. High asset turnover ratio indicates towards the high efficiency of Digi

in using its assets as compared to Axiata. Both Axiata and Digi operates in the same industry

and therefore, superior efficiency of Digi in using its assets for generating sales leads to

increased sales in the company as compared to Axiata (Santosuosso 2014).

Efficiency Ratios

Axiata Digi

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

0.36

1.07

0.35

1.12

0.34

1.30

0.38

1.54

0.38

1.63

Asset Turnover Ratio

2018 2017 2016 2015 2014

Figure 5: Asset Turnover Ratio

(Source: As created by Author)

Asset turnover ratio is an efficiency ratio that measures how well a company is

utilizing its assets for generating sales. This assesses a company’s efficiency to use assets for

the generation of assets. The asset turnover ratio of Digi is better than the same of Axiata

over the last five years. High asset turnover ratio indicates towards the high efficiency of Digi

in using its assets as compared to Axiata. Both Axiata and Digi operates in the same industry

and therefore, superior efficiency of Digi in using its assets for generating sales leads to

increased sales in the company as compared to Axiata (Santosuosso 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS AND MANAGEMENT

Axiata Digi

0.00

2.00

4.00

6.00

8.00

10.00

12.00

4.97 4.81

5.26

4.34

4.94 5.02

5.67

8.35

6.11

9.57

Accounts Receivable Turnover Ratio

2018 2017 2016 2015 2014

Figure 6: Accounts Receivable Turnover Ratio

(Source: As created by Author)

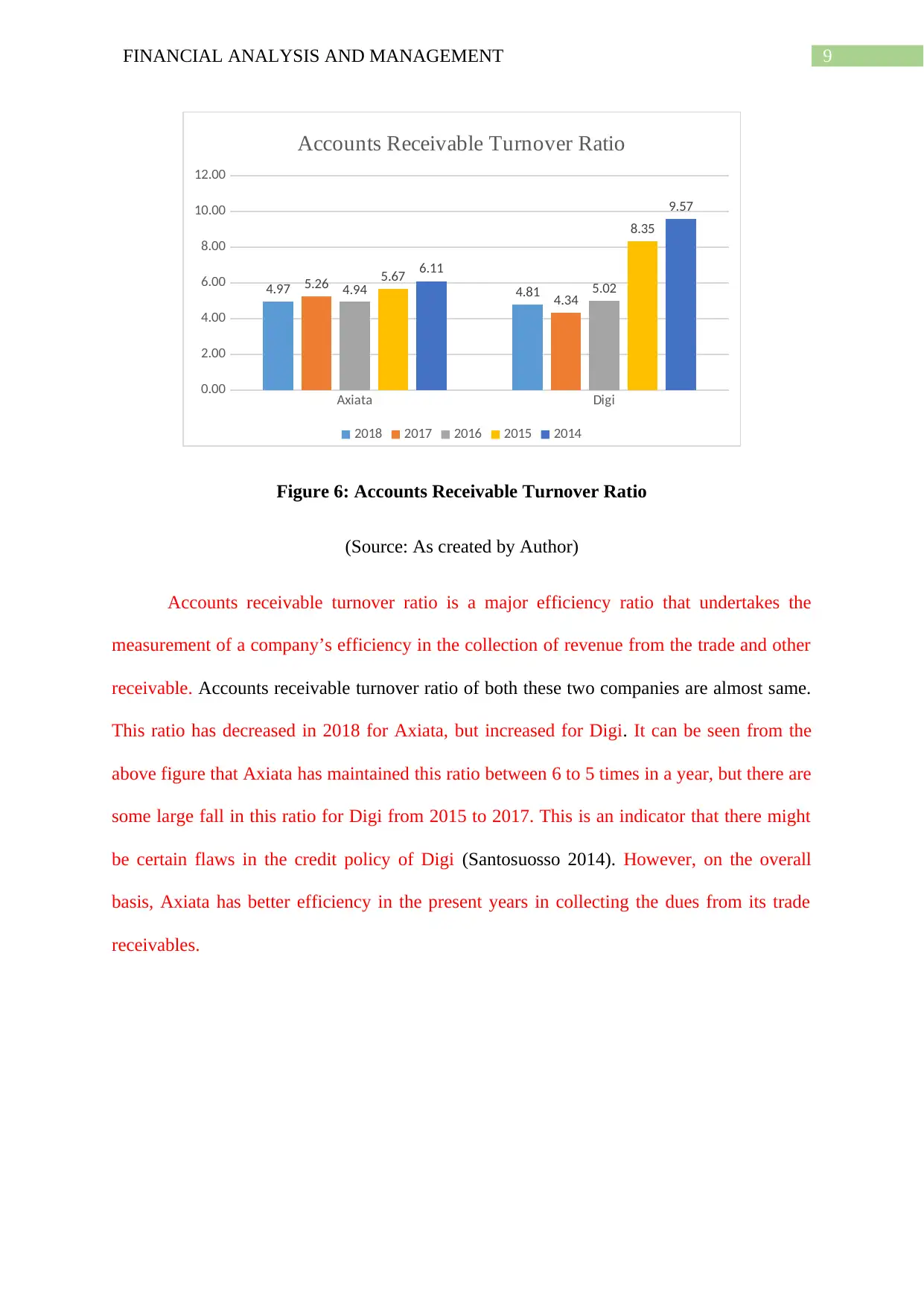

Accounts receivable turnover ratio is a major efficiency ratio that undertakes the

measurement of a company’s efficiency in the collection of revenue from the trade and other

receivable. Accounts receivable turnover ratio of both these two companies are almost same.

This ratio has decreased in 2018 for Axiata, but increased for Digi. It can be seen from the

above figure that Axiata has maintained this ratio between 6 to 5 times in a year, but there are

some large fall in this ratio for Digi from 2015 to 2017. This is an indicator that there might

be certain flaws in the credit policy of Digi (Santosuosso 2014). However, on the overall

basis, Axiata has better efficiency in the present years in collecting the dues from its trade

receivables.

Axiata Digi

0.00

2.00

4.00

6.00

8.00

10.00

12.00

4.97 4.81

5.26

4.34

4.94 5.02

5.67

8.35

6.11

9.57

Accounts Receivable Turnover Ratio

2018 2017 2016 2015 2014

Figure 6: Accounts Receivable Turnover Ratio

(Source: As created by Author)

Accounts receivable turnover ratio is a major efficiency ratio that undertakes the

measurement of a company’s efficiency in the collection of revenue from the trade and other

receivable. Accounts receivable turnover ratio of both these two companies are almost same.

This ratio has decreased in 2018 for Axiata, but increased for Digi. It can be seen from the

above figure that Axiata has maintained this ratio between 6 to 5 times in a year, but there are

some large fall in this ratio for Digi from 2015 to 2017. This is an indicator that there might

be certain flaws in the credit policy of Digi (Santosuosso 2014). However, on the overall

basis, Axiata has better efficiency in the present years in collecting the dues from its trade

receivables.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS AND MANAGEMENT

Capital Structure Ratios

Axiata Digi

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2.33

8.22

1.59

10.24

1.79

9.59

1.29

7.98

1.28

5.27

Debt to Equity Ratio

2018 2017 2016 2015 2014

Figure 7: Debt-to-Equity Ratio

(Source: As created by Author)

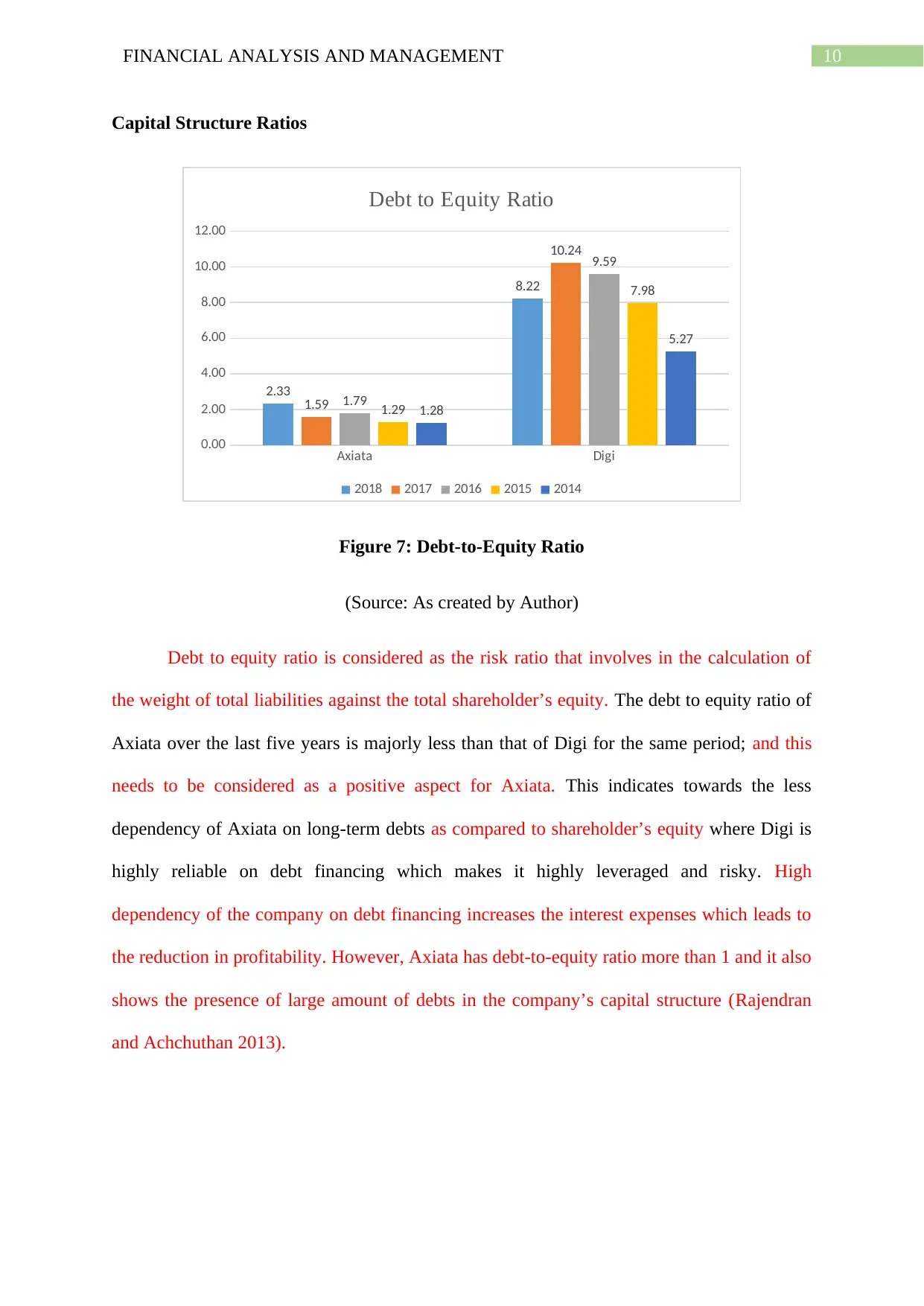

Debt to equity ratio is considered as the risk ratio that involves in the calculation of

the weight of total liabilities against the total shareholder’s equity. The debt to equity ratio of

Axiata over the last five years is majorly less than that of Digi for the same period; and this

needs to be considered as a positive aspect for Axiata. This indicates towards the less

dependency of Axiata on long-term debts as compared to shareholder’s equity where Digi is

highly reliable on debt financing which makes it highly leveraged and risky. High

dependency of the company on debt financing increases the interest expenses which leads to

the reduction in profitability. However, Axiata has debt-to-equity ratio more than 1 and it also

shows the presence of large amount of debts in the company’s capital structure (Rajendran

and Achchuthan 2013).

Capital Structure Ratios

Axiata Digi

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2.33

8.22

1.59

10.24

1.79

9.59

1.29

7.98

1.28

5.27

Debt to Equity Ratio

2018 2017 2016 2015 2014

Figure 7: Debt-to-Equity Ratio

(Source: As created by Author)

Debt to equity ratio is considered as the risk ratio that involves in the calculation of

the weight of total liabilities against the total shareholder’s equity. The debt to equity ratio of

Axiata over the last five years is majorly less than that of Digi for the same period; and this

needs to be considered as a positive aspect for Axiata. This indicates towards the less

dependency of Axiata on long-term debts as compared to shareholder’s equity where Digi is

highly reliable on debt financing which makes it highly leveraged and risky. High

dependency of the company on debt financing increases the interest expenses which leads to

the reduction in profitability. However, Axiata has debt-to-equity ratio more than 1 and it also

shows the presence of large amount of debts in the company’s capital structure (Rajendran

and Achchuthan 2013).

11FINANCIAL ANALYSIS AND MANAGEMENT

Axiata Digi

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.64

0.89

0.56

0.91

0.60

0.91

0.54

0.89

0.54

0.84

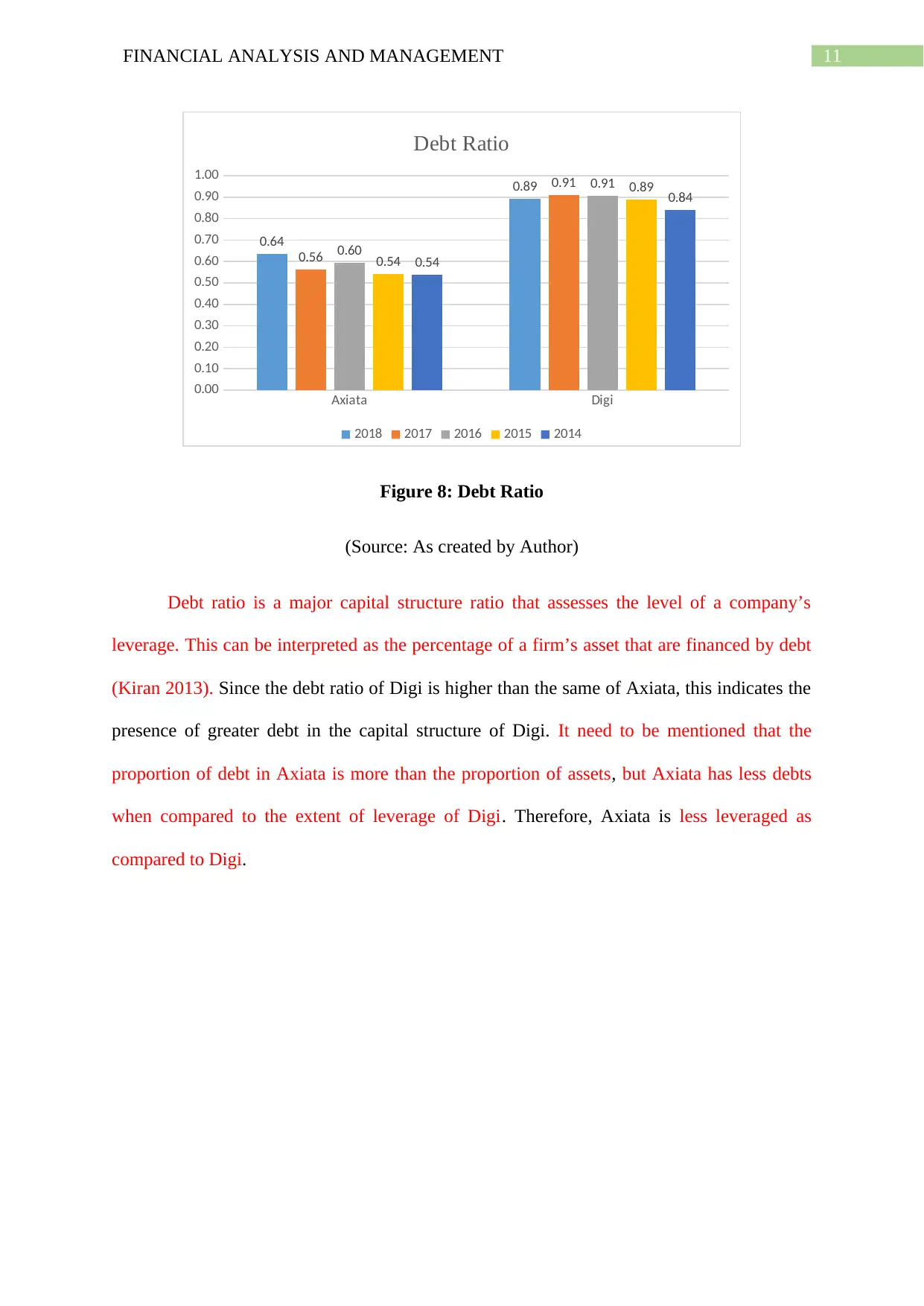

Debt Ratio

2018 2017 2016 2015 2014

Figure 8: Debt Ratio

(Source: As created by Author)

Debt ratio is a major capital structure ratio that assesses the level of a company’s

leverage. This can be interpreted as the percentage of a firm’s asset that are financed by debt

(Kiran 2013). Since the debt ratio of Digi is higher than the same of Axiata, this indicates the

presence of greater debt in the capital structure of Digi. It need to be mentioned that the

proportion of debt in Axiata is more than the proportion of assets, but Axiata has less debts

when compared to the extent of leverage of Digi. Therefore, Axiata is less leveraged as

compared to Digi.

Axiata Digi

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.64

0.89

0.56

0.91

0.60

0.91

0.54

0.89

0.54

0.84

Debt Ratio

2018 2017 2016 2015 2014

Figure 8: Debt Ratio

(Source: As created by Author)

Debt ratio is a major capital structure ratio that assesses the level of a company’s

leverage. This can be interpreted as the percentage of a firm’s asset that are financed by debt

(Kiran 2013). Since the debt ratio of Digi is higher than the same of Axiata, this indicates the

presence of greater debt in the capital structure of Digi. It need to be mentioned that the

proportion of debt in Axiata is more than the proportion of assets, but Axiata has less debts

when compared to the extent of leverage of Digi. Therefore, Axiata is less leveraged as

compared to Digi.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.