Detailed Investment Project Evaluation Report for AYR Co. (Finance)

VerifiedAdded on 2023/04/23

|15

|4246

|205

Report

AI Summary

This report, prepared for the Board of Directors of AYR Co., evaluates two potential investment projects: Project Aspire and Project Wolf. The analysis employs capital budgeting techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period, to determine the most viable option. The report also considers non-financial factors and discusses appropriate funding sources, analyzing the cost of capital and its impact on AYR Co.'s Weighted Average Cost of Capital (WACC). The findings suggest selecting Project Aspire based on its superior NPV and IRR compared to Project Wolf, while also acknowledging the limitations of each capital budgeting technique. Furthermore, the report delves into the aspects of debt and equity financing, detailing the costs associated with each and their implications on the company's financial structure. The report concludes with a recommendation for Project Aspire, supported by a thorough comparative analysis of the investment appraisal techniques used.

Prepared By

Student Name:

Date:

Executive Summary

This report is primarily drafted to cater the need of the Board

of Directors of the AYR Co. which is in the process of

making selection between two proposed investment options

named as Project Aspire and Project Wolf .In order to serve

this purpose both of the projects have been evaluated using

the various Capital budgeting techniques .Apart from

resorting to the capital budgeting techniques, an attempt has

been made to consider other factors while making our

suggestion to choose the specific project. As the investment

in the selected project demands the fund, hence making the

appropriate selection of fund and the consequent cost of such

fund and finally the impact on the WACC (cost of capital) of

the AYR co too have been analyzed in this report.

1

A Brief

Analysi

s of the

Evaluat

ion of

Investm

ent

options

Alongwi

th the

Sources

of

Funds

Student Name:

Date:

Executive Summary

This report is primarily drafted to cater the need of the Board

of Directors of the AYR Co. which is in the process of

making selection between two proposed investment options

named as Project Aspire and Project Wolf .In order to serve

this purpose both of the projects have been evaluated using

the various Capital budgeting techniques .Apart from

resorting to the capital budgeting techniques, an attempt has

been made to consider other factors while making our

suggestion to choose the specific project. As the investment

in the selected project demands the fund, hence making the

appropriate selection of fund and the consequent cost of such

fund and finally the impact on the WACC (cost of capital) of

the AYR co too have been analyzed in this report.

1

A Brief

Analysi

s of the

Evaluat

ion of

Investm

ent

options

Alongwi

th the

Sources

of

Funds

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction...........................................................................................................................................4

Answer to Question No.1 [See Appendix 1]..........................................................................................5

Net Present Value..............................................................................................................................5

Internal rate of Return.......................................................................................................................5

Payback period..................................................................................................................................5

Discussion and Analysis of the investment project................................................................................7

Discussion on two factors of financing: AYR co.....................................................................................9

Conclusion...........................................................................................................................................12

Appendix -1.........................................................................................................................................12

References...........................................................................................................................................15

2

Introduction...........................................................................................................................................4

Answer to Question No.1 [See Appendix 1]..........................................................................................5

Net Present Value..............................................................................................................................5

Internal rate of Return.......................................................................................................................5

Payback period..................................................................................................................................5

Discussion and Analysis of the investment project................................................................................7

Discussion on two factors of financing: AYR co.....................................................................................9

Conclusion...........................................................................................................................................12

Appendix -1.........................................................................................................................................12

References...........................................................................................................................................15

2

Introduction

The Board of AYR Co. is considering the option for the selection of the most suitable project

by making the evaluation of these investment proposals using three widely used capital

budgeting techniques like those of net present value, payback period and internal rate of

return. It further emphasizes on the fact that not only the financial but the non-financial

factors also play the major role in making such evaluation (Belton, 2017). The two project

options are the Project Aspire and the project Wolf with their distinct characteristics for

which our report also suggests the sources of the fund to be opted for making the investment

in the selected project. While making decision on the sources of funds the major

considerations kept in mind are the cost of the capital along with its overall impact on the

WACC of the selected Company. Our report covers both the practical as well as the

theoretical conceptual analysis of the Investment evaluation criteria. Further as it is often seen

that the financial factors play major role in making such investment decision, but non-

financial factors too have their own role to play in this regard, hence the detailed discussion

on the same has been made too (Bromwich & Scapens, 2016).

3

The Board of AYR Co. is considering the option for the selection of the most suitable project

by making the evaluation of these investment proposals using three widely used capital

budgeting techniques like those of net present value, payback period and internal rate of

return. It further emphasizes on the fact that not only the financial but the non-financial

factors also play the major role in making such evaluation (Belton, 2017). The two project

options are the Project Aspire and the project Wolf with their distinct characteristics for

which our report also suggests the sources of the fund to be opted for making the investment

in the selected project. While making decision on the sources of funds the major

considerations kept in mind are the cost of the capital along with its overall impact on the

WACC of the selected Company. Our report covers both the practical as well as the

theoretical conceptual analysis of the Investment evaluation criteria. Further as it is often seen

that the financial factors play major role in making such investment decision, but non-

financial factors too have their own role to play in this regard, hence the detailed discussion

on the same has been made too (Bromwich & Scapens, 2016).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer to Question No.1 [See Appendix 1]

In the following section an attempt has been made to have a brief inside about the concepts of

the Net Present value, internal rate of return and the payback period. Capital budgeting are

the long term precious decisions as they demand high volume of investment. Hence if the

decision taken is wrong then t might prove to be too costly for the company in terms of its

loss of time and money both (Alexander, 2016).

Net Present Value

In this technique the all the cash inflows generated by the project during its tenure are

discounted using a suitable discounting factor and then all the cash outflows are deducted

from the inflow streams. The same rate of discount is being applied uniformly throughout the

calculation. If this difference is either positive or zero then it is recommended for the

selection of the project otherwise the project is not considered worthy enough to be

undertaken (Choy, 2018). The present value of the future cash inflows are calculated using

appropriate discounting rate. Net present value method is easy to use provided the

discounting rate is chosen appropriately. Again it depends the correct estimation of the future

cash inflows too. But such estimation is not so easy too.

4

In the following section an attempt has been made to have a brief inside about the concepts of

the Net Present value, internal rate of return and the payback period. Capital budgeting are

the long term precious decisions as they demand high volume of investment. Hence if the

decision taken is wrong then t might prove to be too costly for the company in terms of its

loss of time and money both (Alexander, 2016).

Net Present Value

In this technique the all the cash inflows generated by the project during its tenure are

discounted using a suitable discounting factor and then all the cash outflows are deducted

from the inflow streams. The same rate of discount is being applied uniformly throughout the

calculation. If this difference is either positive or zero then it is recommended for the

selection of the project otherwise the project is not considered worthy enough to be

undertaken (Choy, 2018). The present value of the future cash inflows are calculated using

appropriate discounting rate. Net present value method is easy to use provided the

discounting rate is chosen appropriately. Again it depends the correct estimation of the future

cash inflows too. But such estimation is not so easy too.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Internal rate of Return

It is the technique in which none of the external factors are taken into consideration while

determining the rate of return from the given project scenario and it is said to be the rate

which makes the cumulative inflows as well as outflows equal at a given rate of return. In the

nutshell, net present value of any given project in this case should be zero (Dumay & Baard,

2017). It is completely impossible that there won’t be any external factors present in the

determination of the discounting rate.

Payback period

It is one of the most simple but quite an unrealistic approach for the calculation of the time

period during by which the capital invested initially and over the project period will be

realized. The reason is that it does not recognize the time value of money along with the fact

that the inflows from the project generated beyond this payback period are never considered

under this method (Werner, 2017). It focuses on only the time aspect of the cash flows and

not the time value of money and hence it is not being considered realistic approach to come

to any conclusion.

i. NPV of the Project Aspire

=Present value of cash inflow - Present value of cash outflow

=$818000/(1.1)^1+$698000/(1.1)^2+$677997/(1.1)^3+$667309/(1.1)^4+$653507/(1.1)^5+

$140000/(1.1)^5+$375000/(1.1)^5-$140000-$2250000

=$3011487-$2390000

=$621487

ii. NPV of the Project Wolf

= Present value of cash inflow- Present value of cash outflow

=$83300/(1.1)^1+$648700/(1.1)^2+$647511/(1.1)^3+$646524/(1.1)^4+$645461/(1.1)^5-

$2250000-$75000/(1.1)^1-75000/(1.1)^2-75000/(1.1)^3-75000/(1.1)^4-75000/(1.1)^5

=$2622238-$2534309

=$87929

iii. internal rate of return of Project - Aspire

Internal rate of return of the project is that rate at which present value of cash

inflow is equal to present value of cash outflow

Froom the above,

10%=$621487, Rate 1 = 10%, NPV1

X% =$2390000

Taking discount rate 20%, Rate 2

NPV 2=$-39616

5

It is the technique in which none of the external factors are taken into consideration while

determining the rate of return from the given project scenario and it is said to be the rate

which makes the cumulative inflows as well as outflows equal at a given rate of return. In the

nutshell, net present value of any given project in this case should be zero (Dumay & Baard,

2017). It is completely impossible that there won’t be any external factors present in the

determination of the discounting rate.

Payback period

It is one of the most simple but quite an unrealistic approach for the calculation of the time

period during by which the capital invested initially and over the project period will be

realized. The reason is that it does not recognize the time value of money along with the fact

that the inflows from the project generated beyond this payback period are never considered

under this method (Werner, 2017). It focuses on only the time aspect of the cash flows and

not the time value of money and hence it is not being considered realistic approach to come

to any conclusion.

i. NPV of the Project Aspire

=Present value of cash inflow - Present value of cash outflow

=$818000/(1.1)^1+$698000/(1.1)^2+$677997/(1.1)^3+$667309/(1.1)^4+$653507/(1.1)^5+

$140000/(1.1)^5+$375000/(1.1)^5-$140000-$2250000

=$3011487-$2390000

=$621487

ii. NPV of the Project Wolf

= Present value of cash inflow- Present value of cash outflow

=$83300/(1.1)^1+$648700/(1.1)^2+$647511/(1.1)^3+$646524/(1.1)^4+$645461/(1.1)^5-

$2250000-$75000/(1.1)^1-75000/(1.1)^2-75000/(1.1)^3-75000/(1.1)^4-75000/(1.1)^5

=$2622238-$2534309

=$87929

iii. internal rate of return of Project - Aspire

Internal rate of return of the project is that rate at which present value of cash

inflow is equal to present value of cash outflow

Froom the above,

10%=$621487, Rate 1 = 10%, NPV1

X% =$2390000

Taking discount rate 20%, Rate 2

NPV 2=$-39616

5

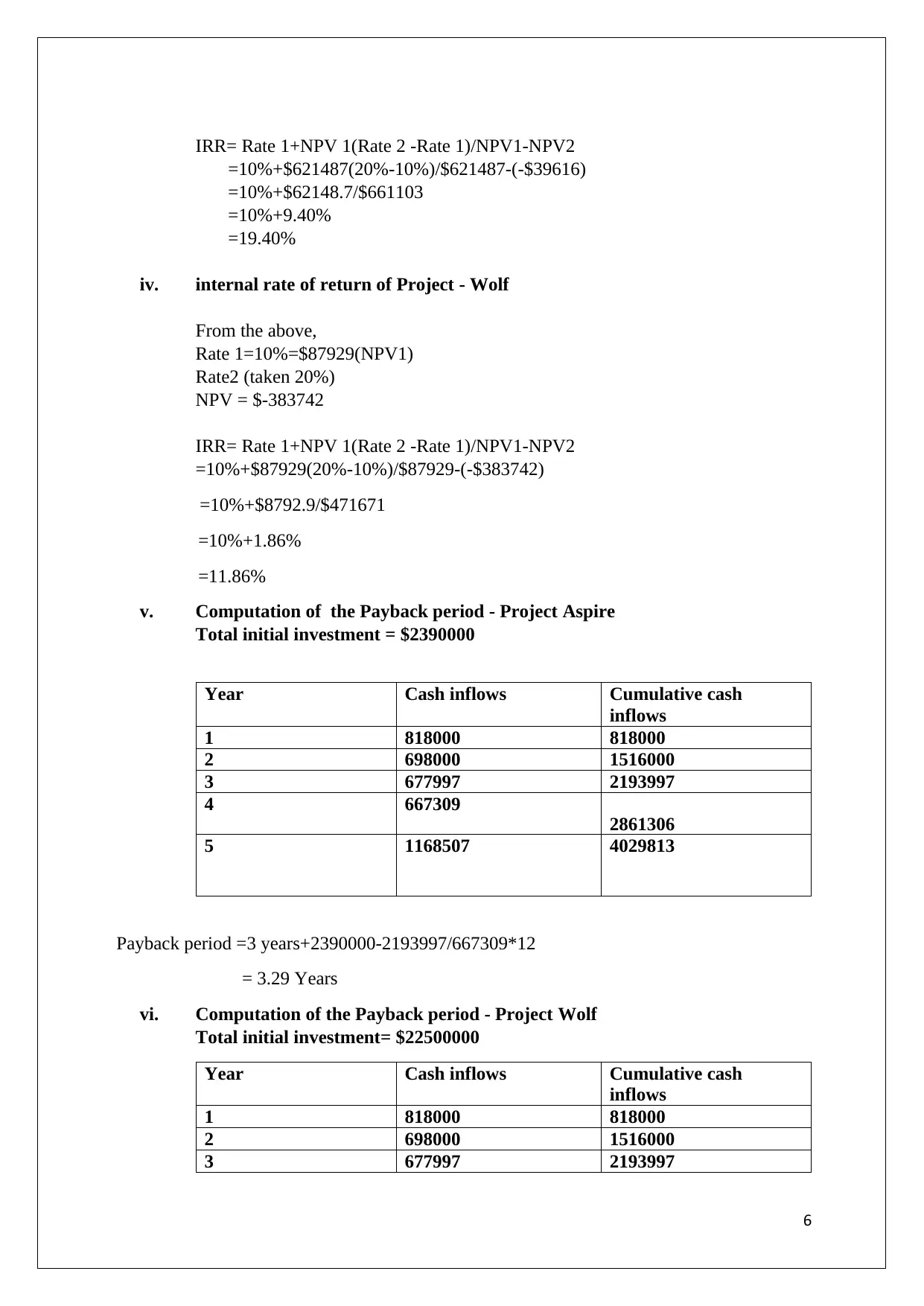

IRR= Rate 1+NPV 1(Rate 2 -Rate 1)/NPV1-NPV2

=10%+$621487(20%-10%)/$621487-(-$39616)

=10%+$62148.7/$661103

=10%+9.40%

=19.40%

iv. internal rate of return of Project - Wolf

From the above,

Rate 1=10%=$87929(NPV1)

Rate2 (taken 20%)

NPV = $-383742

IRR= Rate 1+NPV 1(Rate 2 -Rate 1)/NPV1-NPV2

=10%+$87929(20%-10%)/$87929-(-$383742)

=10%+$8792.9/$471671

=10%+1.86%

=11.86%

v. Computation of the Payback period - Project Aspire

Total initial investment = $2390000

Year Cash inflows Cumulative cash

inflows

1 818000 818000

2 698000 1516000

3 677997 2193997

4 667309

2861306

5 1168507 4029813

Payback period =3 years+2390000-2193997/667309*12

= 3.29 Years

vi. Computation of the Payback period - Project Wolf

Total initial investment= $22500000

Year Cash inflows Cumulative cash

inflows

1 818000 818000

2 698000 1516000

3 677997 2193997

6

=10%+$621487(20%-10%)/$621487-(-$39616)

=10%+$62148.7/$661103

=10%+9.40%

=19.40%

iv. internal rate of return of Project - Wolf

From the above,

Rate 1=10%=$87929(NPV1)

Rate2 (taken 20%)

NPV = $-383742

IRR= Rate 1+NPV 1(Rate 2 -Rate 1)/NPV1-NPV2

=10%+$87929(20%-10%)/$87929-(-$383742)

=10%+$8792.9/$471671

=10%+1.86%

=11.86%

v. Computation of the Payback period - Project Aspire

Total initial investment = $2390000

Year Cash inflows Cumulative cash

inflows

1 818000 818000

2 698000 1516000

3 677997 2193997

4 667309

2861306

5 1168507 4029813

Payback period =3 years+2390000-2193997/667309*12

= 3.29 Years

vi. Computation of the Payback period - Project Wolf

Total initial investment= $22500000

Year Cash inflows Cumulative cash

inflows

1 818000 818000

2 698000 1516000

3 677997 2193997

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

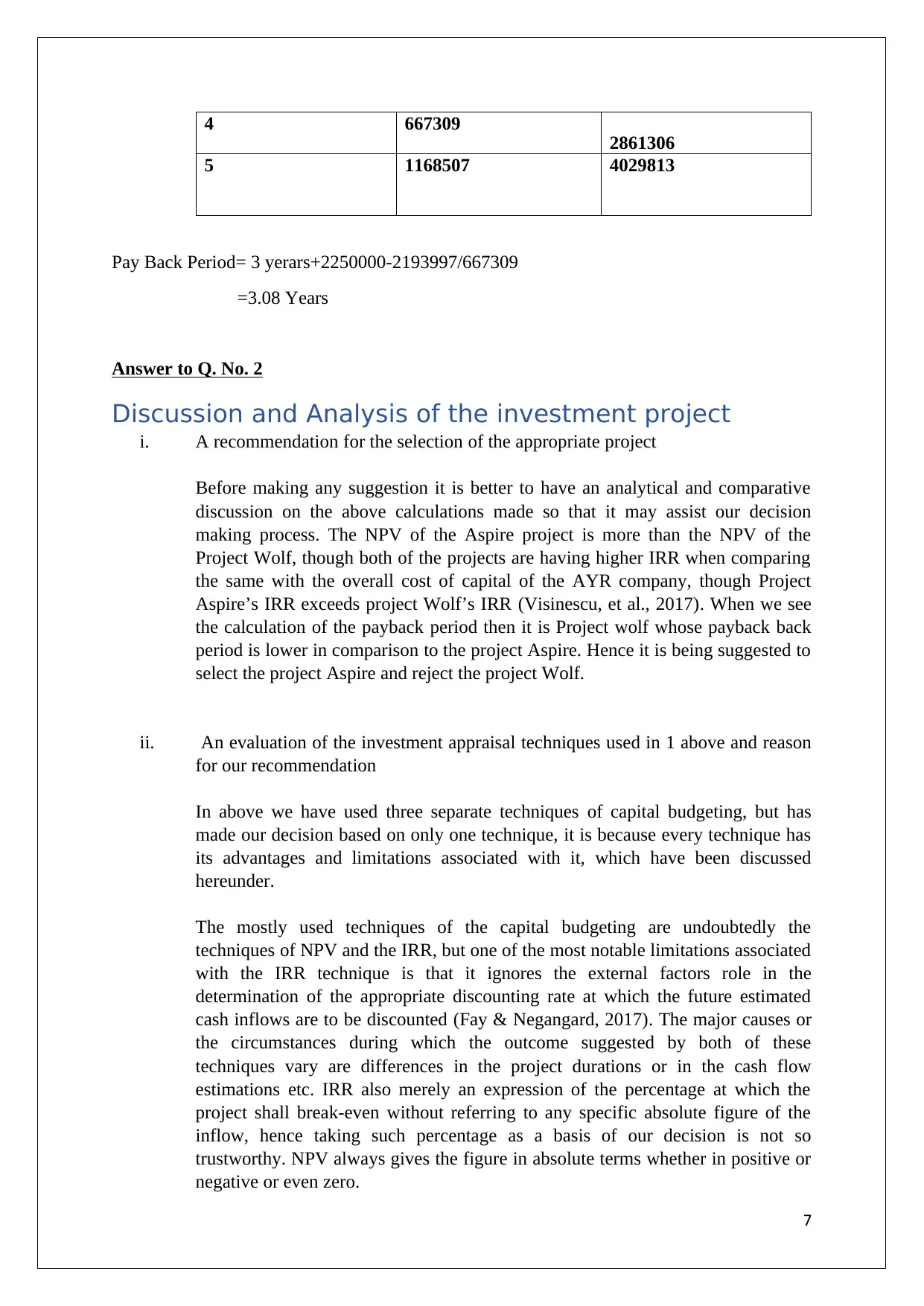

4 667309

2861306

5 1168507 4029813

Pay Back Period= 3 yerars+2250000-2193997/667309

=3.08 Years

Answer to Q. No. 2

Discussion and Analysis of the investment project

i. A recommendation for the selection of the appropriate project

Before making any suggestion it is better to have an analytical and comparative

discussion on the above calculations made so that it may assist our decision

making process. The NPV of the Aspire project is more than the NPV of the

Project Wolf, though both of the projects are having higher IRR when comparing

the same with the overall cost of capital of the AYR company, though Project

Aspire’s IRR exceeds project Wolf’s IRR (Visinescu, et al., 2017). When we see

the calculation of the payback period then it is Project wolf whose payback back

period is lower in comparison to the project Aspire. Hence it is being suggested to

select the project Aspire and reject the project Wolf.

ii. An evaluation of the investment appraisal techniques used in 1 above and reason

for our recommendation

In above we have used three separate techniques of capital budgeting, but has

made our decision based on only one technique, it is because every technique has

its advantages and limitations associated with it, which have been discussed

hereunder.

The mostly used techniques of the capital budgeting are undoubtedly the

techniques of NPV and the IRR, but one of the most notable limitations associated

with the IRR technique is that it ignores the external factors role in the

determination of the appropriate discounting rate at which the future estimated

cash inflows are to be discounted (Fay & Negangard, 2017). The major causes or

the circumstances during which the outcome suggested by both of these

techniques vary are differences in the project durations or in the cash flow

estimations etc. IRR also merely an expression of the percentage at which the

project shall break-even without referring to any specific absolute figure of the

inflow, hence taking such percentage as a basis of our decision is not so

trustworthy. NPV always gives the figure in absolute terms whether in positive or

negative or even zero.

7

2861306

5 1168507 4029813

Pay Back Period= 3 yerars+2250000-2193997/667309

=3.08 Years

Answer to Q. No. 2

Discussion and Analysis of the investment project

i. A recommendation for the selection of the appropriate project

Before making any suggestion it is better to have an analytical and comparative

discussion on the above calculations made so that it may assist our decision

making process. The NPV of the Aspire project is more than the NPV of the

Project Wolf, though both of the projects are having higher IRR when comparing

the same with the overall cost of capital of the AYR company, though Project

Aspire’s IRR exceeds project Wolf’s IRR (Visinescu, et al., 2017). When we see

the calculation of the payback period then it is Project wolf whose payback back

period is lower in comparison to the project Aspire. Hence it is being suggested to

select the project Aspire and reject the project Wolf.

ii. An evaluation of the investment appraisal techniques used in 1 above and reason

for our recommendation

In above we have used three separate techniques of capital budgeting, but has

made our decision based on only one technique, it is because every technique has

its advantages and limitations associated with it, which have been discussed

hereunder.

The mostly used techniques of the capital budgeting are undoubtedly the

techniques of NPV and the IRR, but one of the most notable limitations associated

with the IRR technique is that it ignores the external factors role in the

determination of the appropriate discounting rate at which the future estimated

cash inflows are to be discounted (Fay & Negangard, 2017). The major causes or

the circumstances during which the outcome suggested by both of these

techniques vary are differences in the project durations or in the cash flow

estimations etc. IRR also merely an expression of the percentage at which the

project shall break-even without referring to any specific absolute figure of the

inflow, hence taking such percentage as a basis of our decision is not so

trustworthy. NPV always gives the figure in absolute terms whether in positive or

negative or even zero.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payback period is quite illogical in the sense that it ignores the concept of the time

value of money. Furthermore, though the cash flows generated post the initial

payback period are significant enough, but payback period fails to recognize the

same (Vieira, et al., 2017). Hence, decision on the basis of the outcome of this

technique is again not recommended.

From the above comparative analysis, it is easily concluded that the Net present

value technique outclasses all the other capital budgeting techniques and our

recommendation is based on the outcome of this technique only.

iii. A brief in sight on other factors and information to be considered before making

a final decision are given hereunder:

The below mentioned factors are also to be kept in mind while making the final

decision:

a. The nature of Consumer demand

b. Uncertainty factor

c. Elements of Innovations and inventions

d. Income level

e. Element of Corporation Tax (Goldmann, 2016)

f. The savings level

g. The capital stock

h. The economic activity level etc.

Answer to Question no.3

Discussion on two factors of financing: AYR co

i. A discussion on the debt and equity aspect

The total capital employed by the business can be categorized as debt and

equity. Here the term debt refers to the long term debt.

Long term debt providers are those who expect a fixed percentage of return on

the debt provide to the company, but are not the owners of the company

(Jefferson, 2017). Though in the event of liquidation they have preference

over the equity holders to claim their demand on the assets of the company.

The company can claim the interest tax shield on the interest paid to the long

term debt providers

Equity shareholders are the owners of the company enjoying the voting rights

and are responsible for making the major decision for the business. They are

8

value of money. Furthermore, though the cash flows generated post the initial

payback period are significant enough, but payback period fails to recognize the

same (Vieira, et al., 2017). Hence, decision on the basis of the outcome of this

technique is again not recommended.

From the above comparative analysis, it is easily concluded that the Net present

value technique outclasses all the other capital budgeting techniques and our

recommendation is based on the outcome of this technique only.

iii. A brief in sight on other factors and information to be considered before making

a final decision are given hereunder:

The below mentioned factors are also to be kept in mind while making the final

decision:

a. The nature of Consumer demand

b. Uncertainty factor

c. Elements of Innovations and inventions

d. Income level

e. Element of Corporation Tax (Goldmann, 2016)

f. The savings level

g. The capital stock

h. The economic activity level etc.

Answer to Question no.3

Discussion on two factors of financing: AYR co

i. A discussion on the debt and equity aspect

The total capital employed by the business can be categorized as debt and

equity. Here the term debt refers to the long term debt.

Long term debt providers are those who expect a fixed percentage of return on

the debt provide to the company, but are not the owners of the company

(Jefferson, 2017). Though in the event of liquidation they have preference

over the equity holders to claim their demand on the assets of the company.

The company can claim the interest tax shield on the interest paid to the long

term debt providers

Equity shareholders are the owners of the company enjoying the voting rights

and are responsible for making the major decision for the business. They are

8

entitled to the share of the profit or loss earned by the company, hence can be

said that they are the highest risk takers. They get the dividend in terms of the

share of profit, but the same is not deductible expenses in terms of tax

provision.

Hence though the debts may seem to be cheaper source of fund than equity,

but there is always the risk associated with the company for being bankrupt if

the debt equity ratio exceeds the optimum level (Heminway, 2017).

ii. An explanation on each of the cost of sources of finance

Cost of debt

When we talk about the cost of the debt .we indirectly means it is the post tax

cost of debt as the interest paid on such debt is considered as an allowable

expenses. This is the reason why the real cost of debt comes down while

calculating the after tax cost of debt (Linden & Freeman, 2017). The formula

of for computing the cost of debt has been shown below

KD= I (1-tc)

Where,

KD= after tax cost of debt

I =Rate of Interest

Tc= Tax rate

Cost of equity

Cost of equity is generally being calculated using the capital asset pricing

model (CAPM) or the dividend capitalization model depending on the

circumstances of the case. It is the rate of return which the shareholders of the

company expect in return for the funds invested by them in form of equity and

the risk they bear by making such investment in the company (Sithole, et al.,

2017).

The formula for the same has been described below:

CAPM makes use of historical information to calculate the cost of equity that

is the reason why it is not mostly used for this calculation

E=Rf+Beta*(Rm-Rf)

Where E = Expected return from the Asset

RF= Risk-free Rate of return

Beta= Systematic Risk of the asset

Rm= Return from the market

9

said that they are the highest risk takers. They get the dividend in terms of the

share of profit, but the same is not deductible expenses in terms of tax

provision.

Hence though the debts may seem to be cheaper source of fund than equity,

but there is always the risk associated with the company for being bankrupt if

the debt equity ratio exceeds the optimum level (Heminway, 2017).

ii. An explanation on each of the cost of sources of finance

Cost of debt

When we talk about the cost of the debt .we indirectly means it is the post tax

cost of debt as the interest paid on such debt is considered as an allowable

expenses. This is the reason why the real cost of debt comes down while

calculating the after tax cost of debt (Linden & Freeman, 2017). The formula

of for computing the cost of debt has been shown below

KD= I (1-tc)

Where,

KD= after tax cost of debt

I =Rate of Interest

Tc= Tax rate

Cost of equity

Cost of equity is generally being calculated using the capital asset pricing

model (CAPM) or the dividend capitalization model depending on the

circumstances of the case. It is the rate of return which the shareholders of the

company expect in return for the funds invested by them in form of equity and

the risk they bear by making such investment in the company (Sithole, et al.,

2017).

The formula for the same has been described below:

CAPM makes use of historical information to calculate the cost of equity that

is the reason why it is not mostly used for this calculation

E=Rf+Beta*(Rm-Rf)

Where E = Expected return from the Asset

RF= Risk-free Rate of return

Beta= Systematic Risk of the asset

Rm= Return from the market

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk Free rate of return is the rate of return which is expected to be earned in

the risk free securities like those government securities.

If the value of the beta is one then it means that the asset is as volatile as the

market, if it is less than one then the degree of the volatility seems to be low in

the context of the market condition and if it is greater than one then the asset is

said to be highly volatile in nature (Meroño-Cerdán, et al., 2017).

Dividend capitalization model

One of the major limitation associated with this formula is that it is to be

applied only if the company is paying dividend and at the same time it does

not consider the level of risk as it is being considered in case of the application

of the CAPM .

The formula to be used

E= (D1/P0)/G

Where

E= Cost of equity

D1= Dividend in next year

P0= Current market price of the share

G= growth rate of dividend

Growth rate of dividend

The rate of the growth of the dividend can be calculated using the following

formula

G= (dt/dt-1)-1

Where,

DT= payment of dividend in T period

Dt-1= payment of dividend one year prior to t period

iv. How the selection of the source of finance may affect AYR co.’s weighted

average cost of capital has been shown below (Marques, 2018).

If the total fund required is inform of debt. Then the new capital structure of AYR

co shall be

10

the risk free securities like those government securities.

If the value of the beta is one then it means that the asset is as volatile as the

market, if it is less than one then the degree of the volatility seems to be low in

the context of the market condition and if it is greater than one then the asset is

said to be highly volatile in nature (Meroño-Cerdán, et al., 2017).

Dividend capitalization model

One of the major limitation associated with this formula is that it is to be

applied only if the company is paying dividend and at the same time it does

not consider the level of risk as it is being considered in case of the application

of the CAPM .

The formula to be used

E= (D1/P0)/G

Where

E= Cost of equity

D1= Dividend in next year

P0= Current market price of the share

G= growth rate of dividend

Growth rate of dividend

The rate of the growth of the dividend can be calculated using the following

formula

G= (dt/dt-1)-1

Where,

DT= payment of dividend in T period

Dt-1= payment of dividend one year prior to t period

iv. How the selection of the source of finance may affect AYR co.’s weighted

average cost of capital has been shown below (Marques, 2018).

If the total fund required is inform of debt. Then the new capital structure of AYR

co shall be

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Equity = $20 million

Debt= $18+$2.25= $20.25 million

Let the after tax cost of debt be 5% and cost of equity be 7%

Hence the WACC would be

=5*$20.25/$40.25+7*$20/$40.25

=5.99%

If the entire fund is invested by means of equity. Then the new capital structure of

AYR co shall be

Equity= $20million+$2.25milloion= $22.25million

Debt= $18 million

Let the after tax cost of debt be 5% and cost of equity be 7%

Hence the WACC would be

=5*$18/$40.25+7*$22.5/$40.25

=6.14%

As the WACC of AYR co is lower when making the investment by procuring the

funds through debt, hence the form of financing to be chosen in the case is debt

v. An Assessment of the impact on the current and potential shareholders and lenders

This is described through the following points

a. Sourcing the fund through the means of debt shall cause the AYR company to

be overburdened with the debt, hence the amount of risk of default in making

repayment of debt and the interest thereon shall be high (Kewell & Linsley,

2017).

b. The company may loose the trust and reputation in the market as the funds of

the owners become lower than the debt fund holders.

c. If in near future the AYR wants to procure further funds then it might be

difficult to raise the fund though the means of debt unless it makes the

sufficient arrangement to repay its existing debt.

d. The share price of the AYR Company may decline to a great extent in future

just because of its overburdened debt.

e. If the interest obligations become too high then it may be quite difficult to

generate sufficient amount of profit so that to think about to make payment of

dividend to its shareholders (Timothy, 2004).

11

Debt= $18+$2.25= $20.25 million

Let the after tax cost of debt be 5% and cost of equity be 7%

Hence the WACC would be

=5*$20.25/$40.25+7*$20/$40.25

=5.99%

If the entire fund is invested by means of equity. Then the new capital structure of

AYR co shall be

Equity= $20million+$2.25milloion= $22.25million

Debt= $18 million

Let the after tax cost of debt be 5% and cost of equity be 7%

Hence the WACC would be

=5*$18/$40.25+7*$22.5/$40.25

=6.14%

As the WACC of AYR co is lower when making the investment by procuring the

funds through debt, hence the form of financing to be chosen in the case is debt

v. An Assessment of the impact on the current and potential shareholders and lenders

This is described through the following points

a. Sourcing the fund through the means of debt shall cause the AYR company to

be overburdened with the debt, hence the amount of risk of default in making

repayment of debt and the interest thereon shall be high (Kewell & Linsley,

2017).

b. The company may loose the trust and reputation in the market as the funds of

the owners become lower than the debt fund holders.

c. If in near future the AYR wants to procure further funds then it might be

difficult to raise the fund though the means of debt unless it makes the

sufficient arrangement to repay its existing debt.

d. The share price of the AYR Company may decline to a great extent in future

just because of its overburdened debt.

e. If the interest obligations become too high then it may be quite difficult to

generate sufficient amount of profit so that to think about to make payment of

dividend to its shareholders (Timothy, 2004).

11

f. There shall be more pressure on the shareholders of the company in terms of

generating sufficient amount of revenue.

Conclusion

On the basis of the above critical discussion and analysis it can be concluded that the while

making the choice of the capital budgeting techniques it is to be kept in mind the specific

merits and demerits associated with each of the techniques. Further the technique of the Net

present value is always preferred than any other techniques as suggested.

Again none of the investment decisions can be made final only on the basis of financial

evaluations rather the non- financial factors are also as important as the financial one. Hence

they too demand equal merit.

The determination of the appropriate sources of funds is a critical judgement to be made and

it is the best strategy to have the optimum balance of the equity and the debt in the capital

structure of the company. As neither the total equity nor total debt funded company can best

utilize its resources? Debt is cheaper but may prove to be costly if not paid. Again debts

funds are not very easy to procure as it depends on the credibility of the company too.

Finally cost of equity is a major factor to be considered as at times if dividend is not paid by

the company in such a case if the capital asset pricing model is used then it may make

difference or even can lead to wrong decisions too.

Appendix -1

Working Note No. 1

a. Statement showing the after tax cash inflow from the Project Aspire of AYR Co.

(Figures in $)

Particulars First year Second

year

Third Year Fourth

Year

Fifth Year

Cash Inflows 650000 698750 698750 698750 698750

Less : Variable

Expenses

27000 28823 30768 32845 35062

Net cash inflow

before capital

allowance and

depreciation

and Taxes

623000 669927 667982 665905 663688

Less:

Taxes@20%

Nil 124600 133985 133596 133181

Net cash inflow

after taxes

623000 545327 533997 532309 530507

Add: 75000 75000 75000 75000 75000

12

generating sufficient amount of revenue.

Conclusion

On the basis of the above critical discussion and analysis it can be concluded that the while

making the choice of the capital budgeting techniques it is to be kept in mind the specific

merits and demerits associated with each of the techniques. Further the technique of the Net

present value is always preferred than any other techniques as suggested.

Again none of the investment decisions can be made final only on the basis of financial

evaluations rather the non- financial factors are also as important as the financial one. Hence

they too demand equal merit.

The determination of the appropriate sources of funds is a critical judgement to be made and

it is the best strategy to have the optimum balance of the equity and the debt in the capital

structure of the company. As neither the total equity nor total debt funded company can best

utilize its resources? Debt is cheaper but may prove to be costly if not paid. Again debts

funds are not very easy to procure as it depends on the credibility of the company too.

Finally cost of equity is a major factor to be considered as at times if dividend is not paid by

the company in such a case if the capital asset pricing model is used then it may make

difference or even can lead to wrong decisions too.

Appendix -1

Working Note No. 1

a. Statement showing the after tax cash inflow from the Project Aspire of AYR Co.

(Figures in $)

Particulars First year Second

year

Third Year Fourth

Year

Fifth Year

Cash Inflows 650000 698750 698750 698750 698750

Less : Variable

Expenses

27000 28823 30768 32845 35062

Net cash inflow

before capital

allowance and

depreciation

and Taxes

623000 669927 667982 665905 663688

Less:

Taxes@20%

Nil 124600 133985 133596 133181

Net cash inflow

after taxes

623000 545327 533997 532309 530507

Add: 75000 75000 75000 75000 75000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.