Comprehensive Financial Statement Analysis of B Ltd. (2021-2022)

VerifiedAdded on 2023/06/04

|6

|1298

|233

Report

AI Summary

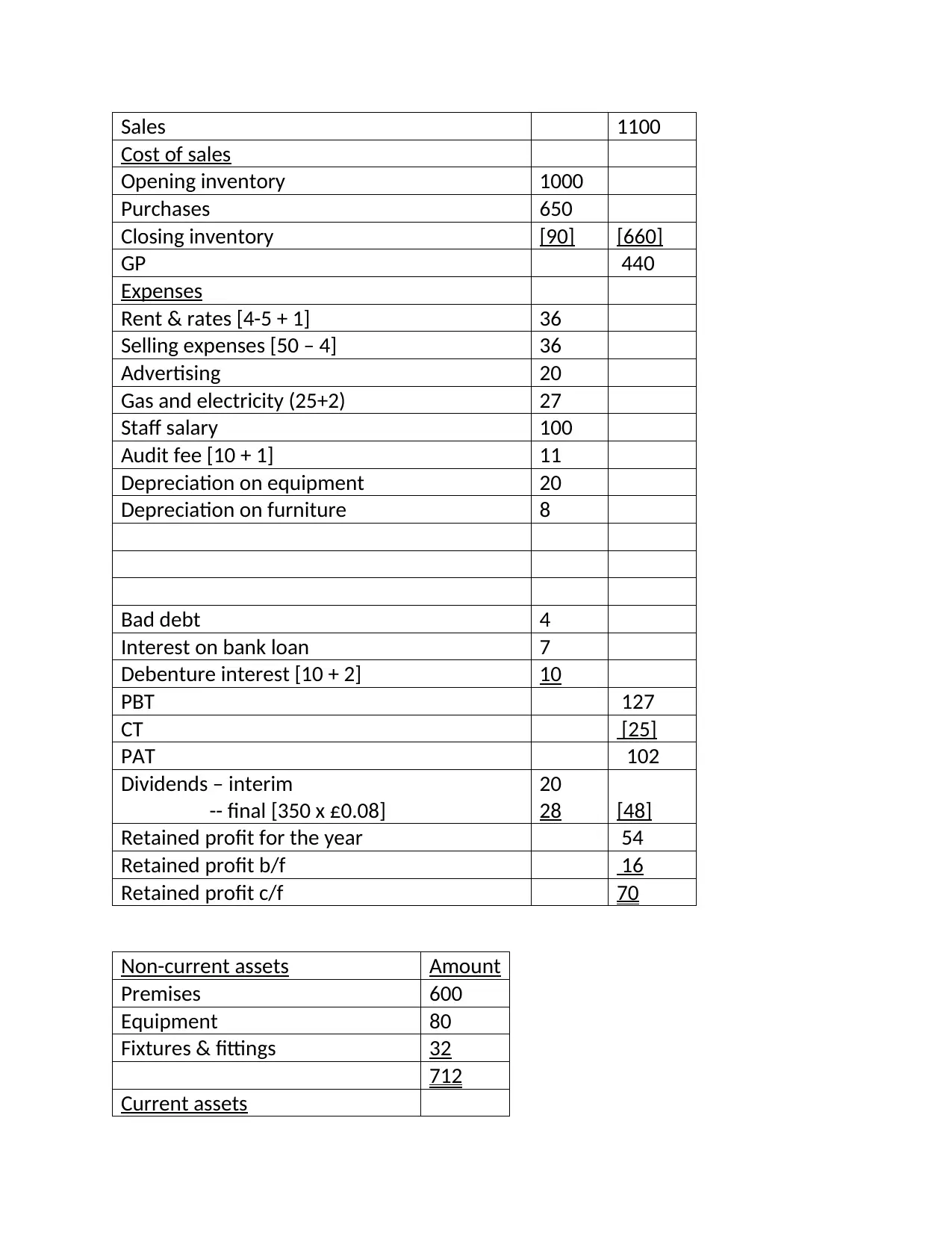

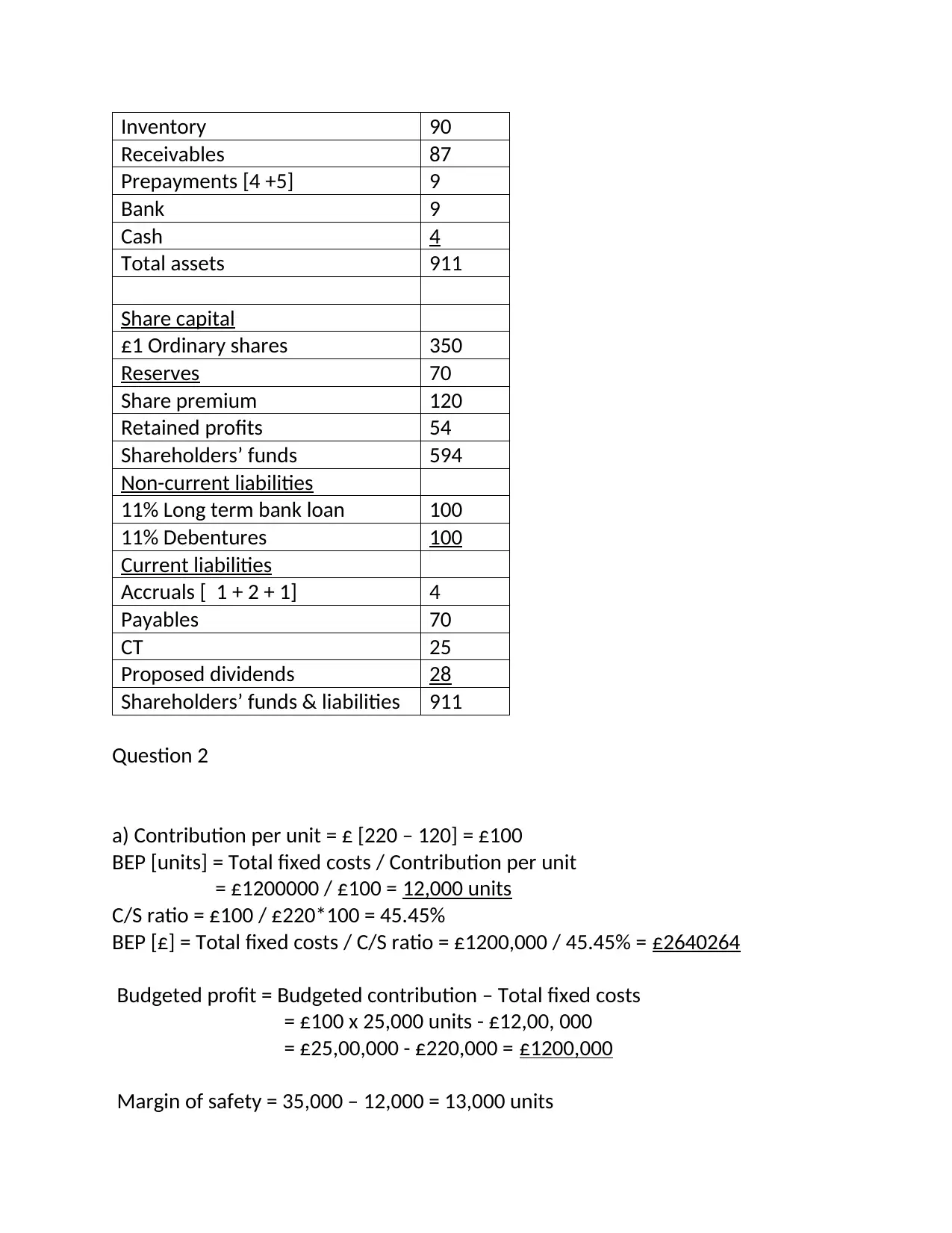

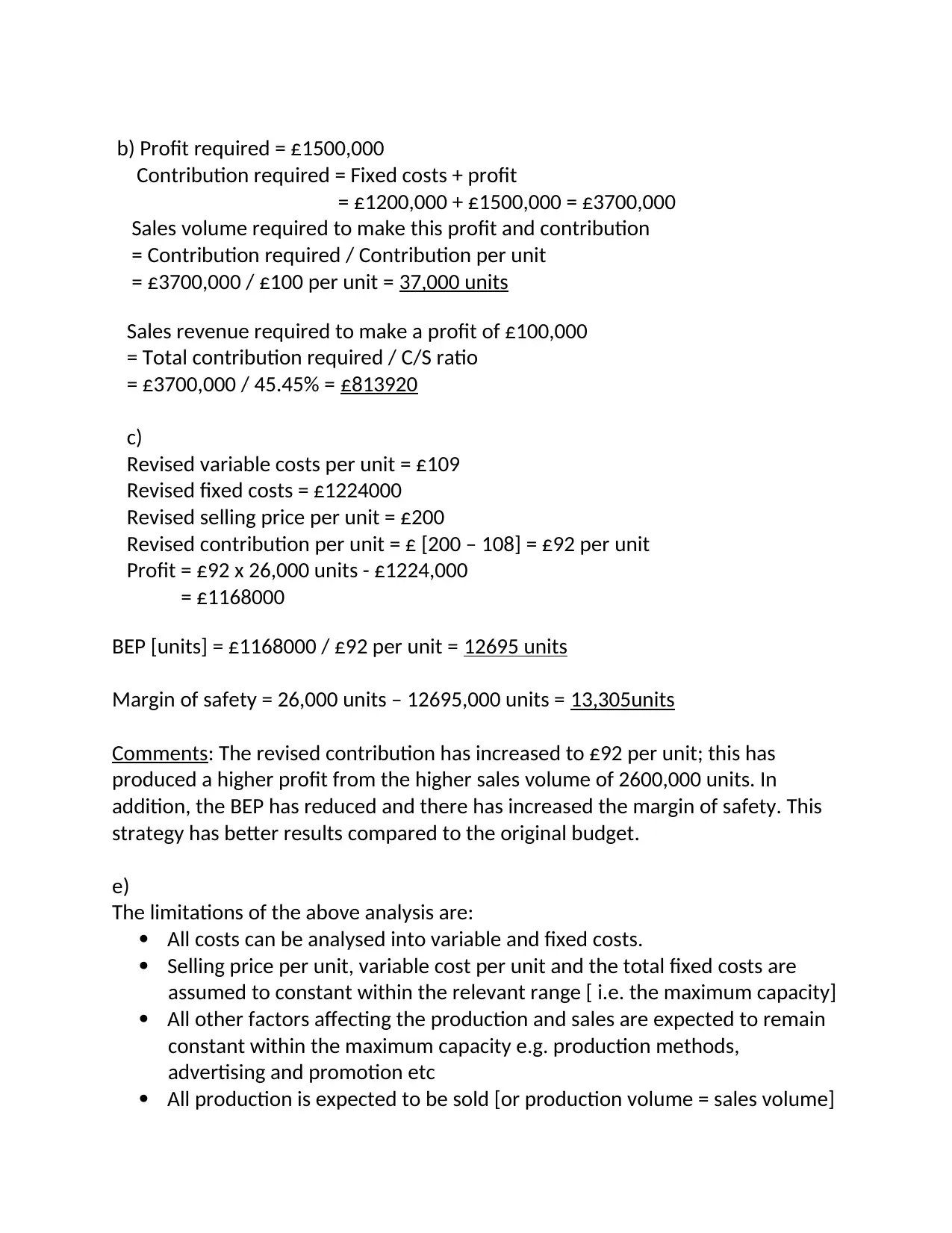

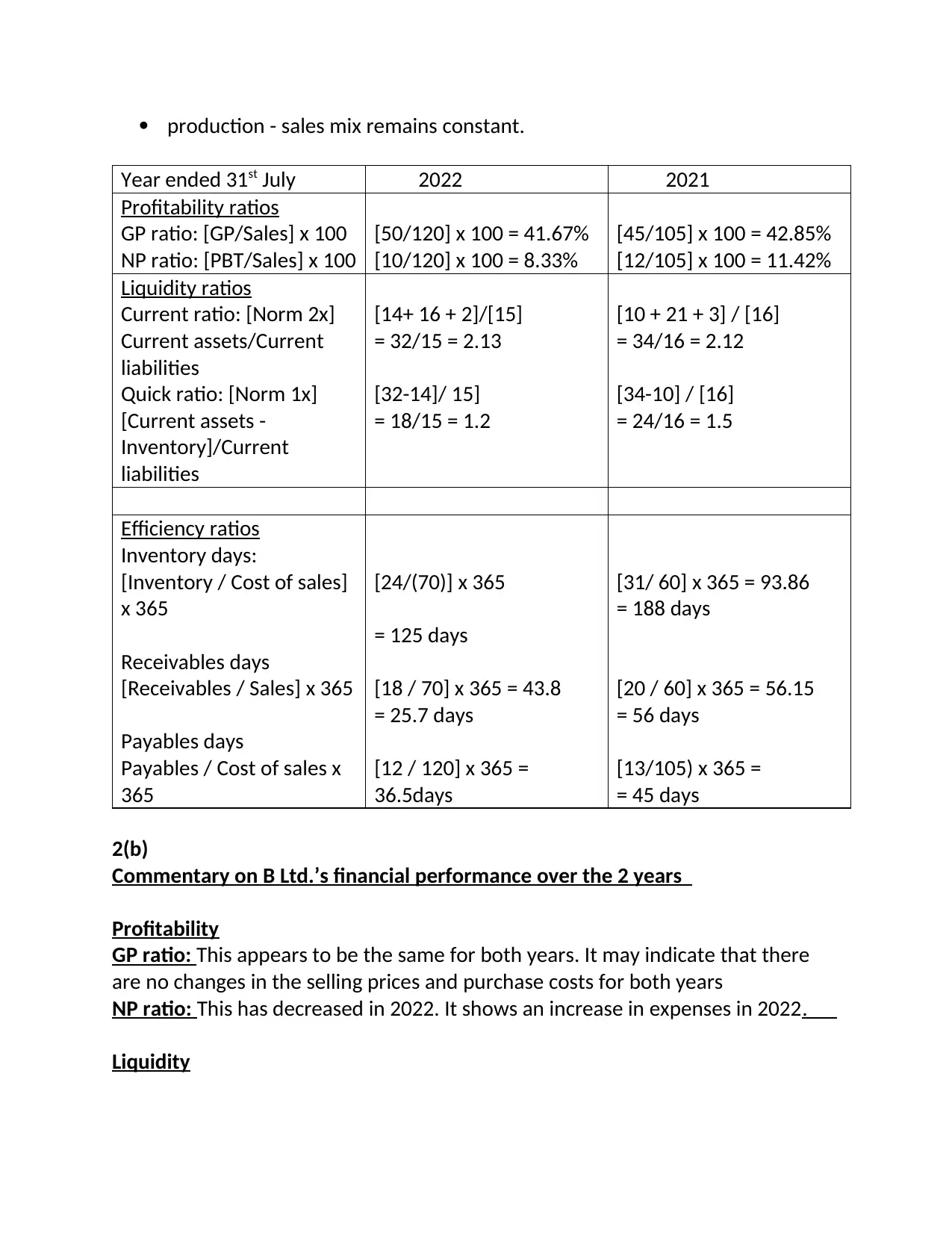

This report provides a comprehensive analysis of B Ltd.'s financial performance, encompassing the years 2021 and 2022. It begins with the construction of the financial statements, including the income statement, balance sheet, and calculation of key financial ratios. The report delves into profitability, liquidity, and efficiency ratios, providing insights into the company's financial health and performance trends. A break-even analysis is conducted to determine the sales volume needed to cover costs and achieve profitability. The analysis includes commentary on the company's financial performance over the two years, and also the limitations of the analysis. The report concludes with recommendations for B Ltd. to improve its financial performance, covering areas such as expense management, liquidity, inventory management, and payables management. Finally, the report provides a list of references for further reading.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.