Financial Management: GSK Plc and Roche Holding AG Analysis

VerifiedAdded on 2023/04/25

|27

|6251

|74

Report

AI Summary

This comprehensive report delves into various aspects of financial management, commencing with a comparative profitability analysis of GSK Plc and Roche Holding AG for the years 2016 and 2017, utilizing key ratios such as return on capital employed, operating profit margin, and earnings per share. The analysis reveals Roche Holding AG's stronger financial position. The report then explores zero-based budgeting (ZBB), outlining its advantages (accuracy, efficiency, and cooperation) and disadvantages (time-consuming nature), along with circumstances favoring its implementation. Further, it examines the benefits and limitations of the balanced scorecard and discusses process failures. Finally, the report addresses financial considerations essential for making sound investment decisions. The report also touches upon the potential of Artificial Intelligence (AI) in banking, specifically focusing on the retail credit center and disbursal units, considering the risks and opportunities of AI implementation in Emirates NBD, aligning with the UAE government's vision for digital transformation. The report includes the student's analysis of the given assignment brief.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Part 1:...............................................................................................................................................3

Introduction:................................................................................................................................3

Organisational profiles of GSK Plc and Roche Holding AG:.....................................................3

Profitability analysis of GSK Plc and Roche Holding AG for the years 2016 and 2017:...........4

Conclusion:..................................................................................................................................9

Part 2:.............................................................................................................................................10

Introduction:..............................................................................................................................10

Advantages and disadvantages of Zero Based Budgeting:........................................................10

Circumstances under which Zero Based Budgeting would be used:.........................................12

Conclusion:................................................................................................................................13

Part 3:.............................................................................................................................................13

Introduction:..............................................................................................................................13

Benefits and limitations of balanced scorecard:........................................................................14

Process failure:...........................................................................................................................17

Conclusion:................................................................................................................................18

Part 4:.............................................................................................................................................18

Introduction:..............................................................................................................................18

Financial issues to be considered before undertaking investment decision:.............................19

Table of Contents

Part 1:...............................................................................................................................................3

Introduction:................................................................................................................................3

Organisational profiles of GSK Plc and Roche Holding AG:.....................................................3

Profitability analysis of GSK Plc and Roche Holding AG for the years 2016 and 2017:...........4

Conclusion:..................................................................................................................................9

Part 2:.............................................................................................................................................10

Introduction:..............................................................................................................................10

Advantages and disadvantages of Zero Based Budgeting:........................................................10

Circumstances under which Zero Based Budgeting would be used:.........................................12

Conclusion:................................................................................................................................13

Part 3:.............................................................................................................................................13

Introduction:..............................................................................................................................13

Benefits and limitations of balanced scorecard:........................................................................14

Process failure:...........................................................................................................................17

Conclusion:................................................................................................................................18

Part 4:.............................................................................................................................................18

Introduction:..............................................................................................................................18

Financial issues to be considered before undertaking investment decision:.............................19

2FINANCIAL MANAGEMENT

Conclusion:................................................................................................................................21

References and Bibliographies:.....................................................................................................22

Conclusion:................................................................................................................................21

References and Bibliographies:.....................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

Part 1:

Introduction:

The current section would provide a brief comparison of the profitability positions of

GSK Plc and Roche Holding AG for the years 2016 and 2017. For determination of the

profitability position of these two healthcare organisations, three useful ratios have been used.

These ratios mainly constitute of return on capital employed, operating profit margin and

earnings per share. The comparison of these ratios would help in understanding the financial

performance of the two chosen organisations in the years 2016 and 2017.

Organisational profiles of GSK Plc and Roche Holding AG:

GSK Plc is a UK-based pharmaceutical firm dealing with inventing, developing,

producing and marketing vaccines along with other health products in the global marketplace. It

is listed on FTSE 100 having market capitalisation of almost £81 million in 2016, which is the

fourth biggest in the stated index (Gsk.com 2019). The main products that it sells in the global

arena comprise of Flovent, Avodart, Advair and other medicines. The organisation has the

objective of becoming the most trusted and innovative healthcare in the global marketplace. In

2010, GSK Plc made the acquisitions of Laboratorious Phoenix for $253 million and it has

employees of nearly 95,400 in 2018.

Roche Holding AG is involved in pharmaceuticals and diagnostics business in

Switzerland, Germany and other European nations (Roche.com 2019). It is a Swiss global

healthcare organisation operating under two divisions, which include diagnostics and

pharmaceuticals. In addition, the organisation is focusing on maintaining competitive advantage

Part 1:

Introduction:

The current section would provide a brief comparison of the profitability positions of

GSK Plc and Roche Holding AG for the years 2016 and 2017. For determination of the

profitability position of these two healthcare organisations, three useful ratios have been used.

These ratios mainly constitute of return on capital employed, operating profit margin and

earnings per share. The comparison of these ratios would help in understanding the financial

performance of the two chosen organisations in the years 2016 and 2017.

Organisational profiles of GSK Plc and Roche Holding AG:

GSK Plc is a UK-based pharmaceutical firm dealing with inventing, developing,

producing and marketing vaccines along with other health products in the global marketplace. It

is listed on FTSE 100 having market capitalisation of almost £81 million in 2016, which is the

fourth biggest in the stated index (Gsk.com 2019). The main products that it sells in the global

arena comprise of Flovent, Avodart, Advair and other medicines. The organisation has the

objective of becoming the most trusted and innovative healthcare in the global marketplace. In

2010, GSK Plc made the acquisitions of Laboratorious Phoenix for $253 million and it has

employees of nearly 95,400 in 2018.

Roche Holding AG is involved in pharmaceuticals and diagnostics business in

Switzerland, Germany and other European nations (Roche.com 2019). It is a Swiss global

healthcare organisation operating under two divisions, which include diagnostics and

pharmaceuticals. In addition, the organisation is focusing on maintaining competitive advantage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

through simplification of its business processes by retaining the best talent. At present, it has

employee base of 65,000.

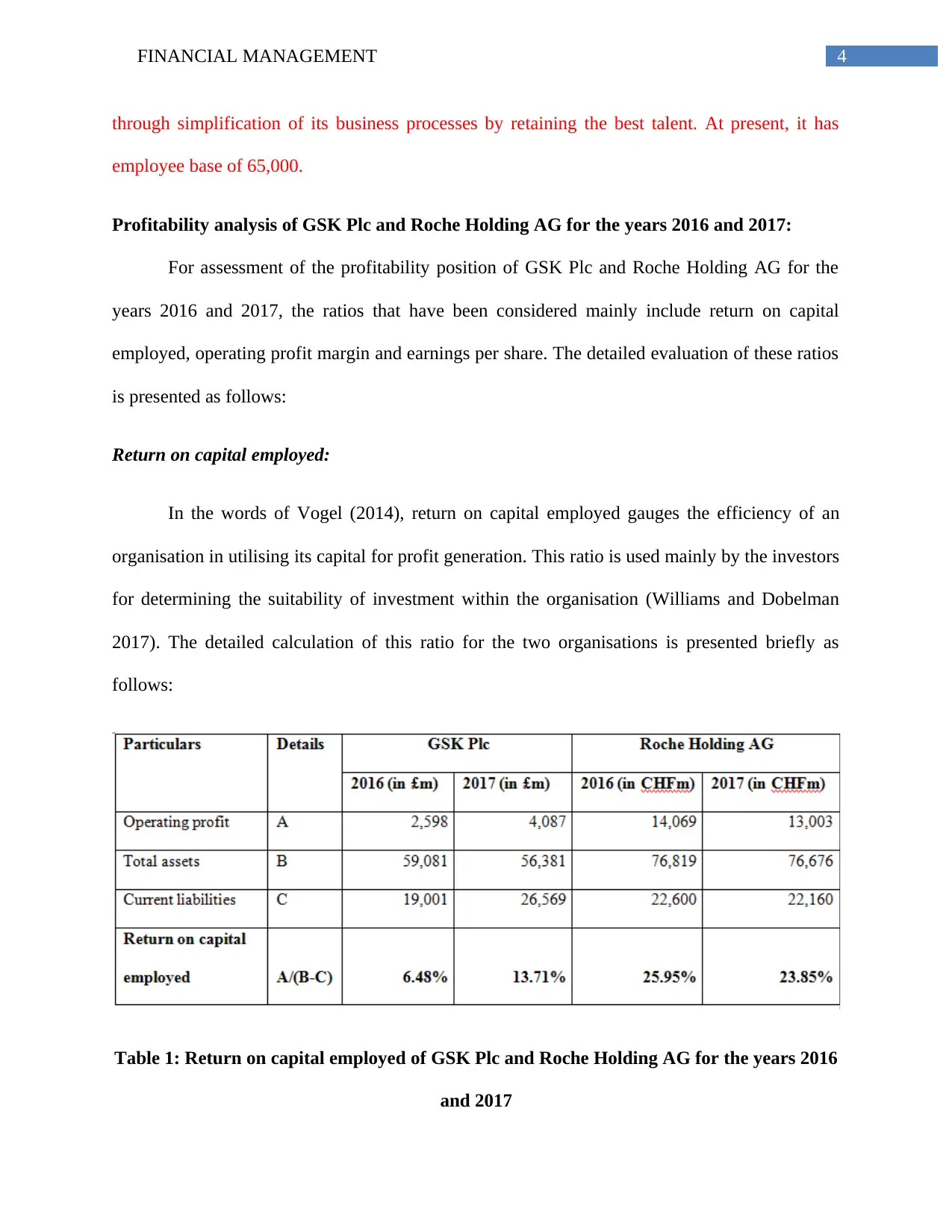

Profitability analysis of GSK Plc and Roche Holding AG for the years 2016 and 2017:

For assessment of the profitability position of GSK Plc and Roche Holding AG for the

years 2016 and 2017, the ratios that have been considered mainly include return on capital

employed, operating profit margin and earnings per share. The detailed evaluation of these ratios

is presented as follows:

Return on capital employed:

In the words of Vogel (2014), return on capital employed gauges the efficiency of an

organisation in utilising its capital for profit generation. This ratio is used mainly by the investors

for determining the suitability of investment within the organisation (Williams and Dobelman

2017). The detailed calculation of this ratio for the two organisations is presented briefly as

follows:

Table 1: Return on capital employed of GSK Plc and Roche Holding AG for the years 2016

and 2017

through simplification of its business processes by retaining the best talent. At present, it has

employee base of 65,000.

Profitability analysis of GSK Plc and Roche Holding AG for the years 2016 and 2017:

For assessment of the profitability position of GSK Plc and Roche Holding AG for the

years 2016 and 2017, the ratios that have been considered mainly include return on capital

employed, operating profit margin and earnings per share. The detailed evaluation of these ratios

is presented as follows:

Return on capital employed:

In the words of Vogel (2014), return on capital employed gauges the efficiency of an

organisation in utilising its capital for profit generation. This ratio is used mainly by the investors

for determining the suitability of investment within the organisation (Williams and Dobelman

2017). The detailed calculation of this ratio for the two organisations is presented briefly as

follows:

Table 1: Return on capital employed of GSK Plc and Roche Holding AG for the years 2016

and 2017

5FINANCIAL MANAGEMENT

(Source: Gsk.com 2019: Roche.com 2019)

2016 2017 2016 2017

GSK Plc Roche Holding AG

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

6.48%

13.71%

25.95% 23.85%

Return on capital employed

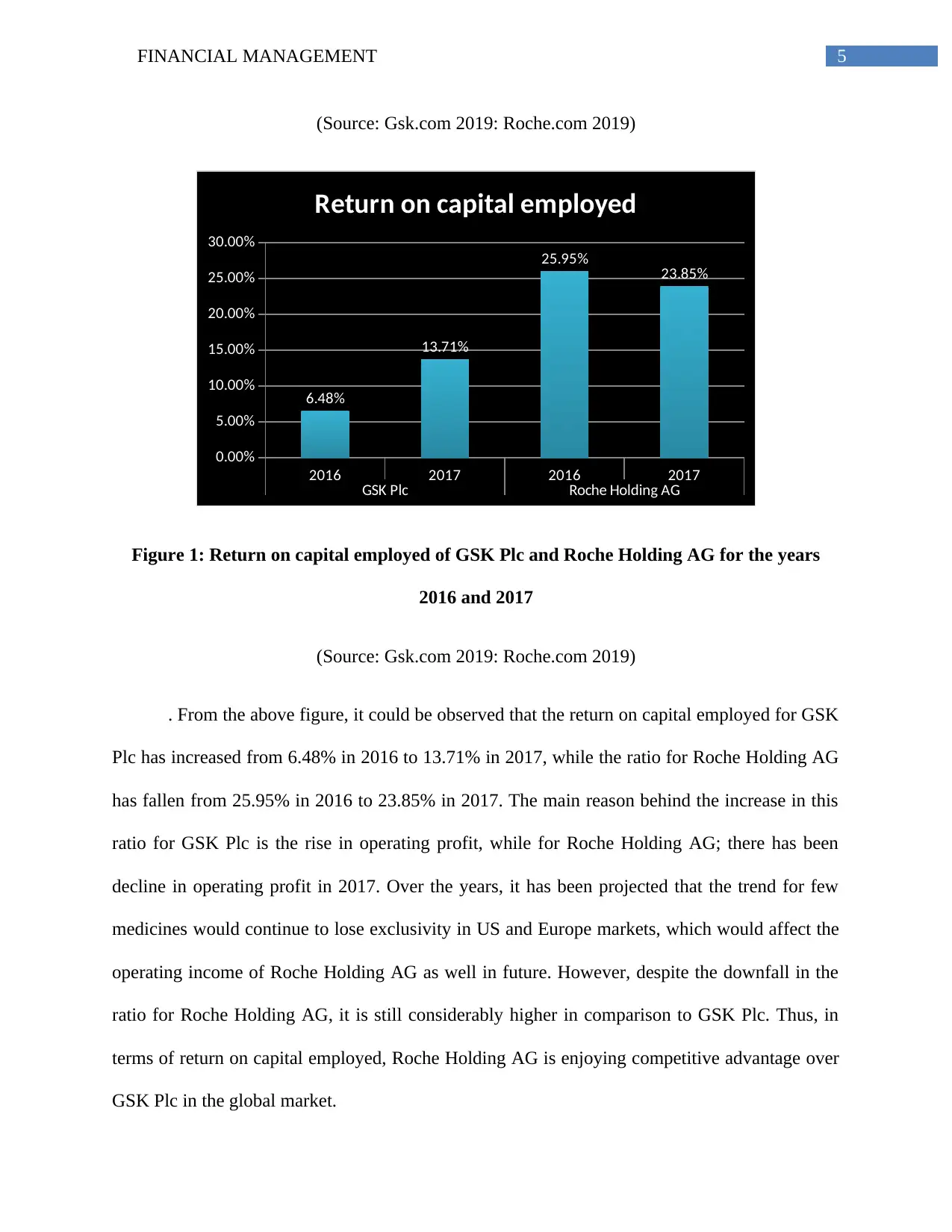

Figure 1: Return on capital employed of GSK Plc and Roche Holding AG for the years

2016 and 2017

(Source: Gsk.com 2019: Roche.com 2019)

. From the above figure, it could be observed that the return on capital employed for GSK

Plc has increased from 6.48% in 2016 to 13.71% in 2017, while the ratio for Roche Holding AG

has fallen from 25.95% in 2016 to 23.85% in 2017. The main reason behind the increase in this

ratio for GSK Plc is the rise in operating profit, while for Roche Holding AG; there has been

decline in operating profit in 2017. Over the years, it has been projected that the trend for few

medicines would continue to lose exclusivity in US and Europe markets, which would affect the

operating income of Roche Holding AG as well in future. However, despite the downfall in the

ratio for Roche Holding AG, it is still considerably higher in comparison to GSK Plc. Thus, in

terms of return on capital employed, Roche Holding AG is enjoying competitive advantage over

GSK Plc in the global market.

(Source: Gsk.com 2019: Roche.com 2019)

2016 2017 2016 2017

GSK Plc Roche Holding AG

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

6.48%

13.71%

25.95% 23.85%

Return on capital employed

Figure 1: Return on capital employed of GSK Plc and Roche Holding AG for the years

2016 and 2017

(Source: Gsk.com 2019: Roche.com 2019)

. From the above figure, it could be observed that the return on capital employed for GSK

Plc has increased from 6.48% in 2016 to 13.71% in 2017, while the ratio for Roche Holding AG

has fallen from 25.95% in 2016 to 23.85% in 2017. The main reason behind the increase in this

ratio for GSK Plc is the rise in operating profit, while for Roche Holding AG; there has been

decline in operating profit in 2017. Over the years, it has been projected that the trend for few

medicines would continue to lose exclusivity in US and Europe markets, which would affect the

operating income of Roche Holding AG as well in future. However, despite the downfall in the

ratio for Roche Holding AG, it is still considerably higher in comparison to GSK Plc. Thus, in

terms of return on capital employed, Roche Holding AG is enjoying competitive advantage over

GSK Plc in the global market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

Operating profit margin:

As pointed out by Robinson et al. (2015), operating profit margin denotes the percentage

of profit an organisation makes after it has incurred variable production costs like raw materials

and wages. The detailed calculation of this ratio for the two organisations is presented briefly as

follows:

Table 2: Operating profit margin of GSK Plc and Roche Holding AG for the years 2016

and 2017

(Source: Gsk.com 2019: Roche.com 2019)

Operating profit margin:

As pointed out by Robinson et al. (2015), operating profit margin denotes the percentage

of profit an organisation makes after it has incurred variable production costs like raw materials

and wages. The detailed calculation of this ratio for the two organisations is presented briefly as

follows:

Table 2: Operating profit margin of GSK Plc and Roche Holding AG for the years 2016

and 2017

(Source: Gsk.com 2019: Roche.com 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

2016 2017 2016 2017

GSK Plc Roche Holding AG

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

9.32%

13.54%

27.82%

24.40%

Operating profit margin

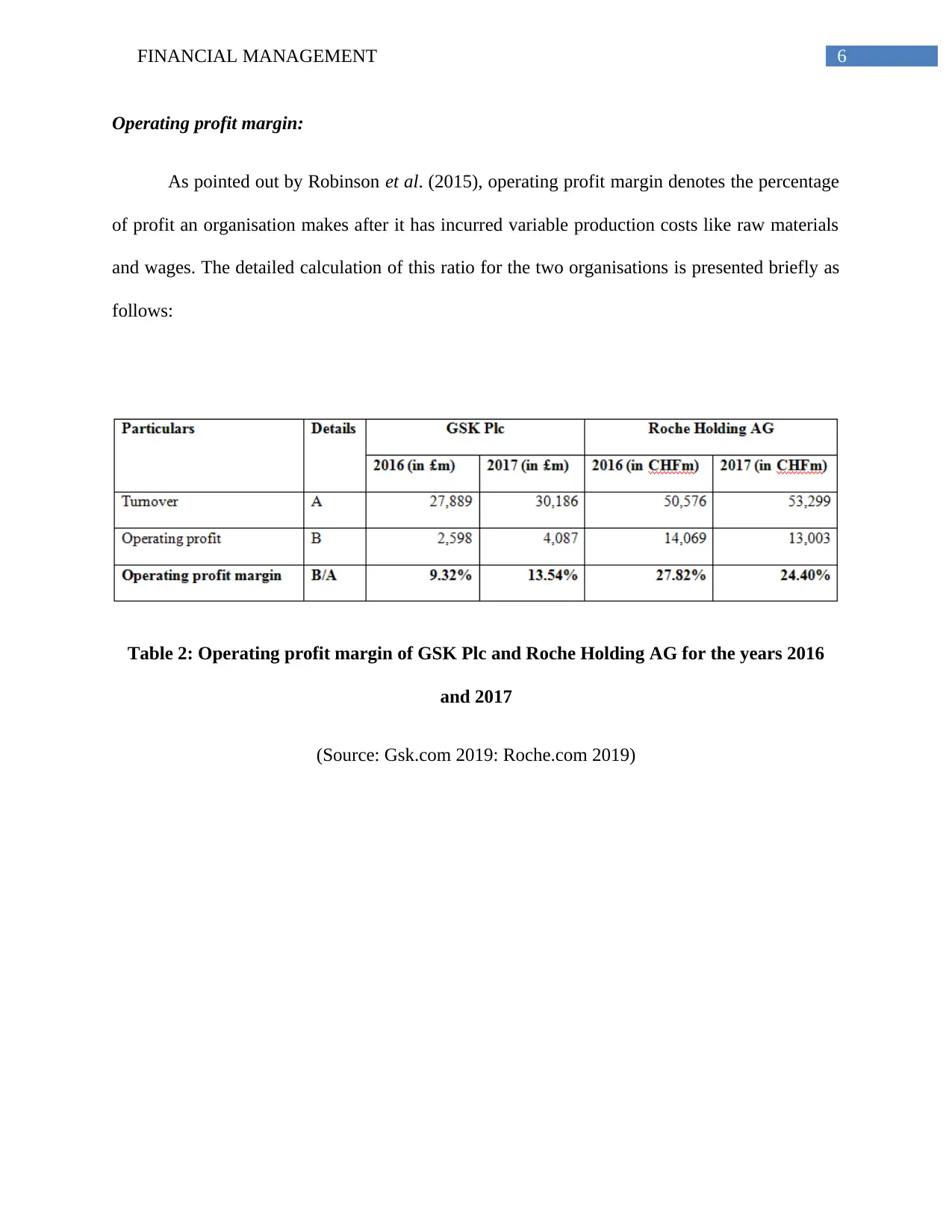

Figure 2: Operating profit margin of GSK Plc and Roche Holding AG for the years 2016

and 2017

(Source: Gsk.com 2019: Roche.com 2019)

According to the above figure, it could be seen that the operating profit margin of GSK

Plc has risen from 9.32% in 2016 to 13.54% in 2017, while the same for Roche Holding AG has

declined from 27.82% in 2016 to 24.40% in 2017. The main reason that the ratio for Roche

Holding AG has declined over the year is due to the fact that it has adopted aggressive pricing

strategy, coupled with rise in cost of direct materials and labour costs in the global healthcare

industry. On the other hand, the ratio for GSK Plc has risen over the years is due to the change in

management strategy leading to decline in overall operating expenses of the organisation over

the year. Although both the organisations have experienced a sharp increase in revenue in 2017,

GSK Plc has managed to keep its operating expenses under control, which is not the case in case

of Roche Holding AG. However, despite such increase, GSK Plc is not able to match with the

operating margin generated by Roche Holding AG in 2017. Hence, in terms of this ratio, the

2016 2017 2016 2017

GSK Plc Roche Holding AG

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

9.32%

13.54%

27.82%

24.40%

Operating profit margin

Figure 2: Operating profit margin of GSK Plc and Roche Holding AG for the years 2016

and 2017

(Source: Gsk.com 2019: Roche.com 2019)

According to the above figure, it could be seen that the operating profit margin of GSK

Plc has risen from 9.32% in 2016 to 13.54% in 2017, while the same for Roche Holding AG has

declined from 27.82% in 2016 to 24.40% in 2017. The main reason that the ratio for Roche

Holding AG has declined over the year is due to the fact that it has adopted aggressive pricing

strategy, coupled with rise in cost of direct materials and labour costs in the global healthcare

industry. On the other hand, the ratio for GSK Plc has risen over the years is due to the change in

management strategy leading to decline in overall operating expenses of the organisation over

the year. Although both the organisations have experienced a sharp increase in revenue in 2017,

GSK Plc has managed to keep its operating expenses under control, which is not the case in case

of Roche Holding AG. However, despite such increase, GSK Plc is not able to match with the

operating margin generated by Roche Holding AG in 2017. Hence, in terms of this ratio, the

8FINANCIAL MANAGEMENT

competitive position of Roche Holding AG is better in comparison to GSK Plc in the global

healthcare industry.

Earnings per share:

Earnings per share, termed as net income per share, is a profitability or market prospect

ratio, which gauges the amount of net profit earned per share of stock outstanding (Wahlen,

Baginski and Bradshaw 2014). Hence, a larger organisation would need to divide its earnings

among increased shares of stock in contrast to a smaller organisation (Islam 2014). The detailed

calculation of this ratio for the two organisations is presented briefly as follows:

Table 3: Earnings per share of GSK Plc and Roche Holding AG for the years 2016 and

2017

(Source: Gsk.com 2019: Roche.com 2019)

competitive position of Roche Holding AG is better in comparison to GSK Plc in the global

healthcare industry.

Earnings per share:

Earnings per share, termed as net income per share, is a profitability or market prospect

ratio, which gauges the amount of net profit earned per share of stock outstanding (Wahlen,

Baginski and Bradshaw 2014). Hence, a larger organisation would need to divide its earnings

among increased shares of stock in contrast to a smaller organisation (Islam 2014). The detailed

calculation of this ratio for the two organisations is presented briefly as follows:

Table 3: Earnings per share of GSK Plc and Roche Holding AG for the years 2016 and

2017

(Source: Gsk.com 2019: Roche.com 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

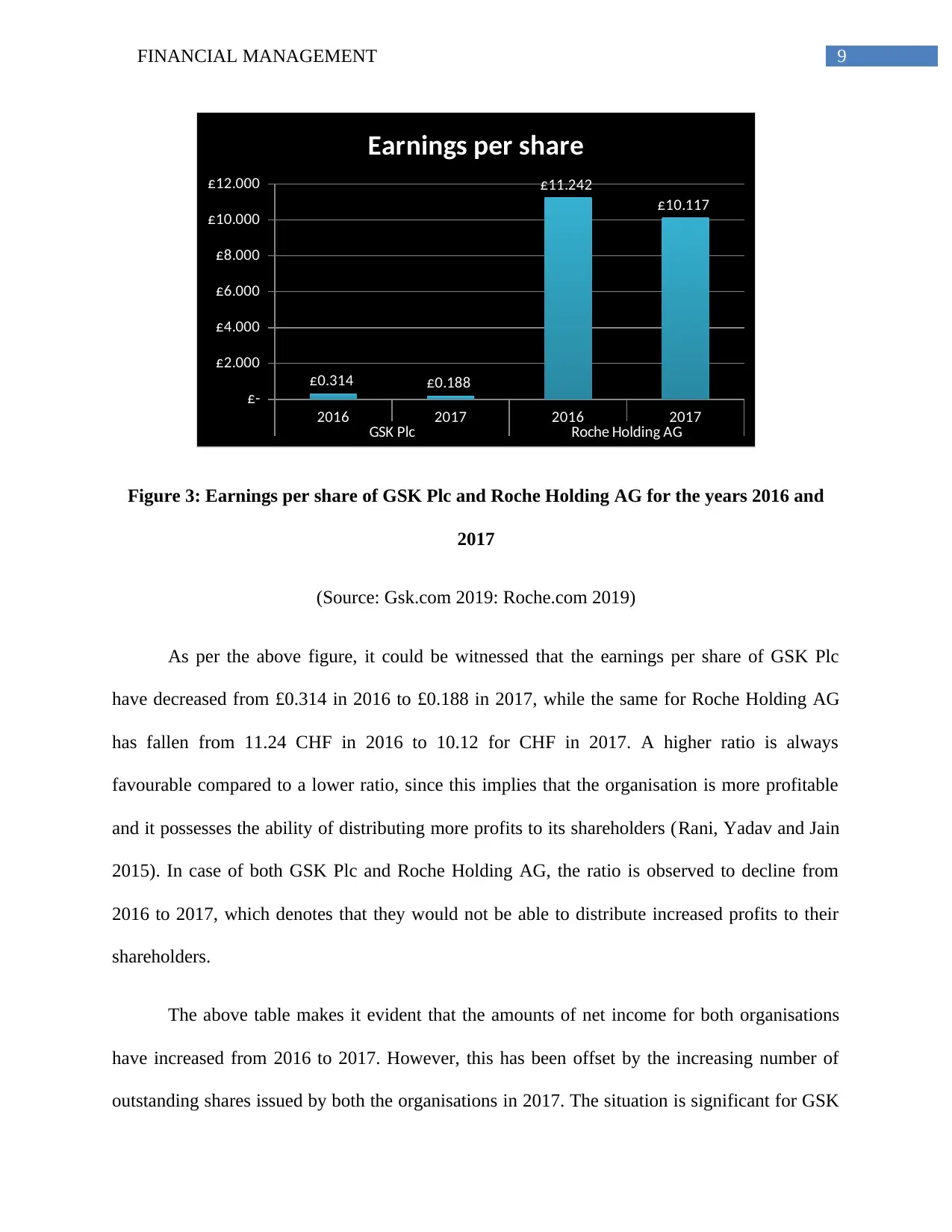

2016 2017 2016 2017

GSK Plc Roche Holding AG

£-

£2.000

£4.000

£6.000

£8.000

£10.000

£12.000

£0.314 £0.188

£11.242

£10.117

Earnings per share

Figure 3: Earnings per share of GSK Plc and Roche Holding AG for the years 2016 and

2017

(Source: Gsk.com 2019: Roche.com 2019)

As per the above figure, it could be witnessed that the earnings per share of GSK Plc

have decreased from £0.314 in 2016 to £0.188 in 2017, while the same for Roche Holding AG

has fallen from 11.24 CHF in 2016 to 10.12 for CHF in 2017. A higher ratio is always

favourable compared to a lower ratio, since this implies that the organisation is more profitable

and it possesses the ability of distributing more profits to its shareholders (Rani, Yadav and Jain

2015). In case of both GSK Plc and Roche Holding AG, the ratio is observed to decline from

2016 to 2017, which denotes that they would not be able to distribute increased profits to their

shareholders.

The above table makes it evident that the amounts of net income for both organisations

have increased from 2016 to 2017. However, this has been offset by the increasing number of

outstanding shares issued by both the organisations in 2017. The situation is significant for GSK

2016 2017 2016 2017

GSK Plc Roche Holding AG

£-

£2.000

£4.000

£6.000

£8.000

£10.000

£12.000

£0.314 £0.188

£11.242

£10.117

Earnings per share

Figure 3: Earnings per share of GSK Plc and Roche Holding AG for the years 2016 and

2017

(Source: Gsk.com 2019: Roche.com 2019)

As per the above figure, it could be witnessed that the earnings per share of GSK Plc

have decreased from £0.314 in 2016 to £0.188 in 2017, while the same for Roche Holding AG

has fallen from 11.24 CHF in 2016 to 10.12 for CHF in 2017. A higher ratio is always

favourable compared to a lower ratio, since this implies that the organisation is more profitable

and it possesses the ability of distributing more profits to its shareholders (Rani, Yadav and Jain

2015). In case of both GSK Plc and Roche Holding AG, the ratio is observed to decline from

2016 to 2017, which denotes that they would not be able to distribute increased profits to their

shareholders.

The above table makes it evident that the amounts of net income for both organisations

have increased from 2016 to 2017. However, this has been offset by the increasing number of

outstanding shares issued by both the organisations in 2017. The situation is significant for GSK

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

Plc, as the number of shares issued has increased from 3,382 in 2016 to 11,537 in 2017, while

the same has increased from 785 in 2016 to 962 in 2017 for Roche Holding AG. Due to this, the

earnings per share of the two organisations have declined in 2017. However, it is noteworthy to

mention that the ratio still seems to be better for Roche Holding AG compared to GSK Plc and

hence, investing in the shares of the former would be a profitable option for the investors (Faello

2015).

Conclusion:

From the above discussion, it is apparent that for conducting the profitability analysis of

GSK Plc and Roche Holding AG, return on capital employed, operating profit margin and

earnings per share have been taken into consideration. In terms of all the ratios, it has been found

that the position of Roche Holding AG is found to be more favourable compared to GSK Plc

because of increased revenue and controlled operating expenses over the year. Over the years, it

has been projected that the trend for few medicines would continue to lose exclusivity in US and

Europe markets, which would affect the operating income of Roche Holding AG as well in

future. Moreover, Roche Holding AG has not issued too much additional equity shares in the

market owing to which earnings per share have not declined significantly, as in the case of GSK

Plc. Hence, it could be inferred that Roche Holding AG is enjoying competitive edge over GSK

Plc in the global healthcare market in terms of profitability.

Part 2:

Introduction:

The current study discusses the concept of zero based budgeting (ZBB). The ZBB is a

process of budgeting where all the expenditures need to be rationalised for every new financial

period. The method of ZBB begins from "zero base" and each activity within a company is

Plc, as the number of shares issued has increased from 3,382 in 2016 to 11,537 in 2017, while

the same has increased from 785 in 2016 to 962 in 2017 for Roche Holding AG. Due to this, the

earnings per share of the two organisations have declined in 2017. However, it is noteworthy to

mention that the ratio still seems to be better for Roche Holding AG compared to GSK Plc and

hence, investing in the shares of the former would be a profitable option for the investors (Faello

2015).

Conclusion:

From the above discussion, it is apparent that for conducting the profitability analysis of

GSK Plc and Roche Holding AG, return on capital employed, operating profit margin and

earnings per share have been taken into consideration. In terms of all the ratios, it has been found

that the position of Roche Holding AG is found to be more favourable compared to GSK Plc

because of increased revenue and controlled operating expenses over the year. Over the years, it

has been projected that the trend for few medicines would continue to lose exclusivity in US and

Europe markets, which would affect the operating income of Roche Holding AG as well in

future. Moreover, Roche Holding AG has not issued too much additional equity shares in the

market owing to which earnings per share have not declined significantly, as in the case of GSK

Plc. Hence, it could be inferred that Roche Holding AG is enjoying competitive edge over GSK

Plc in the global healthcare market in terms of profitability.

Part 2:

Introduction:

The current study discusses the concept of zero based budgeting (ZBB). The ZBB is a

process of budgeting where all the expenditures need to be rationalised for every new financial

period. The method of ZBB begins from "zero base" and each activity within a company is

11FINANCIAL MANAGEMENT

examined for its requirements and expenditures. Then the Budget is prepared for the upcoming

period, disregarding the fact that the current budget could be either higher or lower than the

earlier period (Miller 2018). The first part of this study introduces the features of ZBB, followed

by the advantages and disadvantages of ZBB and finally we take a look on the best way to

implement ZBB based on different aspects, which are related to it.

Advantages and disadvantages of Zero Based Budgeting:

The advantages are discussed below -

Accuracy -

As opposed to the traditional budgeting process, in which just some random variations

are being made to the budget of the earlier years, ZBB makes each sector to overview each and

every commodity cash flow and calculate the operational expenses (Lin and 2017). This would

help in reducing the expenditures as it would clearly give an overview of these expenses against

the anticipated performance.

Efficiency -

ZBB assists in allotment of resources (sector wise), as it does not pay any attention to the

past figures. However, it pays a close attention to the real figures.

Reduction of unnecessary functionalities -

This process allows to recognise those events, which would allow the activities to take

place in a (cost effective) manner that would lead to the reduction of (unproductive) and

unnecessary functionalities.

Budget inflation -

examined for its requirements and expenditures. Then the Budget is prepared for the upcoming

period, disregarding the fact that the current budget could be either higher or lower than the

earlier period (Miller 2018). The first part of this study introduces the features of ZBB, followed

by the advantages and disadvantages of ZBB and finally we take a look on the best way to

implement ZBB based on different aspects, which are related to it.

Advantages and disadvantages of Zero Based Budgeting:

The advantages are discussed below -

Accuracy -

As opposed to the traditional budgeting process, in which just some random variations

are being made to the budget of the earlier years, ZBB makes each sector to overview each and

every commodity cash flow and calculate the operational expenses (Lin and 2017). This would

help in reducing the expenditures as it would clearly give an overview of these expenses against

the anticipated performance.

Efficiency -

ZBB assists in allotment of resources (sector wise), as it does not pay any attention to the

past figures. However, it pays a close attention to the real figures.

Reduction of unnecessary functionalities -

This process allows to recognise those events, which would allow the activities to take

place in a (cost effective) manner that would lead to the reduction of (unproductive) and

unnecessary functionalities.

Budget inflation -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.