Financial Performance Report: BENDIGO & ADELAIDE BANK vs. QUEENSLAND

VerifiedAdded on 2021/06/14

|24

|6983

|19

Report

AI Summary

This report provides a detailed financial analysis of BENDIGO AND ADELAIDE BANK LTD and BANK OF QUEENSLAND LTD, focusing on their financial performance and position. It utilizes ratio analysis to evaluate short-term solvency, long-term solvency, asset utilization, profitability, and market value. The analysis reveals that BANK OF QUEENSLAND LTD generally exhibits better financial performance and lower risk compared to BENDIGO AND ADELAIDE BANK LTD, making it a potentially better investment option. The report includes calculations and comparisons of key financial ratios such as current ratio, acid-test ratio, gearing ratio, and interest coverage ratio, drawing conclusions based on the data from 2016 and 2017.

Running Head: Business Finance

1

Project Report: Business Finance

1

Project Report: Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance

2

Executive summary

Financial analysis is a process to evaluate the financial performance and the position of

an organization. It is essential for the internal management of the company as well as the

external parties of the company to evaluate the performance of the company. The report has

been prepared to evaluate the financial performance of BENDIGO AND ADELAIDE BANK

LTD and BANK OF QUEENSLAND LTD. BANK OF QUEENSLAND LTD and

BENDIGO AND ADELAIDE BANK LTD are operating their business in Australian market

in the same industry. The financial analysis study on both the company explains that the

performance of the bank, BANK OF QUEENSLAND LTD is better than the other bank and

thus the investment into the company would be a better option.

2

Executive summary

Financial analysis is a process to evaluate the financial performance and the position of

an organization. It is essential for the internal management of the company as well as the

external parties of the company to evaluate the performance of the company. The report has

been prepared to evaluate the financial performance of BENDIGO AND ADELAIDE BANK

LTD and BANK OF QUEENSLAND LTD. BANK OF QUEENSLAND LTD and

BENDIGO AND ADELAIDE BANK LTD are operating their business in Australian market

in the same industry. The financial analysis study on both the company explains that the

performance of the bank, BANK OF QUEENSLAND LTD is better than the other bank and

thus the investment into the company would be a better option.

Business Finance

3

Contents

Introduction.......................................................................................................................5

Company overview...........................................................................................................5

BENDIGO AND ADELAIDE BANK LTD................................................................5

BANK OF QUEENSLAND LTD................................................................................5

Financial analysis (ratio analysis).....................................................................................6

Short term solvency position........................................................................................6

Long term solvency position........................................................................................7

Asset utilization............................................................................................................9

Profitability ratios.......................................................................................................11

Market value ratios.....................................................................................................13

Recommendation............................................................................................................14

Conclusion......................................................................................................................15

References.......................................................................................................................16

Annual report. 2017........................................................................................................16

Annual report. 2018........................................................................................................16

Bloomberg. 2018............................................................................................................16

Bloomberg. 2018............................................................................................................16

Home. 2018.....................................................................................................................17

Home. 2018.....................................................................................................................17

Morningstar. 2018...........................................................................................................17

Morningstar. 2018...........................................................................................................17

Yahoo finance. 2018.......................................................................................................17

Appendix.........................................................................................................................18

3

Contents

Introduction.......................................................................................................................5

Company overview...........................................................................................................5

BENDIGO AND ADELAIDE BANK LTD................................................................5

BANK OF QUEENSLAND LTD................................................................................5

Financial analysis (ratio analysis).....................................................................................6

Short term solvency position........................................................................................6

Long term solvency position........................................................................................7

Asset utilization............................................................................................................9

Profitability ratios.......................................................................................................11

Market value ratios.....................................................................................................13

Recommendation............................................................................................................14

Conclusion......................................................................................................................15

References.......................................................................................................................16

Annual report. 2017........................................................................................................16

Annual report. 2018........................................................................................................16

Bloomberg. 2018............................................................................................................16

Bloomberg. 2018............................................................................................................16

Home. 2018.....................................................................................................................17

Home. 2018.....................................................................................................................17

Morningstar. 2018...........................................................................................................17

Morningstar. 2018...........................................................................................................17

Yahoo finance. 2018.......................................................................................................17

Appendix.........................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance

4

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance

5

Introduction:

Business finance is a branch of finance which is used to evaluate the fund of the

company. Business finance evaluates the financial statement and the transaction of an

organization to evaluate the performance of the company and make a conclusion about the

process of the company. Business finance follows process of financial analysis to evaluate the

financial performance and the position of an organization (Bierman, 2010). Financial

performance evaluation makes it easy for the stakeholders of the company to analyze that

whether the company is performing well in the market or not. It is essential for the internal

management of the company as well as the external parties of the company to evaluate the

performance of the company (Baker and Nofsinger, 2010). This offers a good base to the

parties to make better decisions. The report has been prepared to evaluate the financial

performance of BENDIGO AND ADELAIDE BANK LTD and BANK OF QUEENSLAND

LTD.

Company overview:

BENDIGO AND ADELAIDE BANK LTD:

It is an Australian financial institution which is operating its business in retail sector

of Australia. The company is a result f merger of Bendigo bank and Adelaide bank. The

merger has taken place in 2007. Headquarter of the bank is in Bendigo, Australia. The main

products of the bank are banking services, financial services and other services which are

related to banking (Home, 2018). The bank is currently serving its services through 400

outlets in Australia. The merger has helped the company to grow the market as well as the

market base of the company has also been enhanced (Bloomberg, 2018).

BANK OF QUEENSLAND LTD:

The bank of Queensland is an Australian financial institution which is operating its

business in retail sector of Australia. The company is one of the oldest financial institutions in

the market of Queensland (Home, 2018). The company has been established in 1874 and

currently, it has a network of 252 branched which includes the 166 owner managed branches

and 78 corporate branches. Headquarter of the bank is in Queensland, Australia. The main

products of the bank are consumer banking, finance and insurance, commercial banking,

credit cards etc. The bank has surveyed and it has been found that 88% customers of the

5

Introduction:

Business finance is a branch of finance which is used to evaluate the fund of the

company. Business finance evaluates the financial statement and the transaction of an

organization to evaluate the performance of the company and make a conclusion about the

process of the company. Business finance follows process of financial analysis to evaluate the

financial performance and the position of an organization (Bierman, 2010). Financial

performance evaluation makes it easy for the stakeholders of the company to analyze that

whether the company is performing well in the market or not. It is essential for the internal

management of the company as well as the external parties of the company to evaluate the

performance of the company (Baker and Nofsinger, 2010). This offers a good base to the

parties to make better decisions. The report has been prepared to evaluate the financial

performance of BENDIGO AND ADELAIDE BANK LTD and BANK OF QUEENSLAND

LTD.

Company overview:

BENDIGO AND ADELAIDE BANK LTD:

It is an Australian financial institution which is operating its business in retail sector

of Australia. The company is a result f merger of Bendigo bank and Adelaide bank. The

merger has taken place in 2007. Headquarter of the bank is in Bendigo, Australia. The main

products of the bank are banking services, financial services and other services which are

related to banking (Home, 2018). The bank is currently serving its services through 400

outlets in Australia. The merger has helped the company to grow the market as well as the

market base of the company has also been enhanced (Bloomberg, 2018).

BANK OF QUEENSLAND LTD:

The bank of Queensland is an Australian financial institution which is operating its

business in retail sector of Australia. The company is one of the oldest financial institutions in

the market of Queensland (Home, 2018). The company has been established in 1874 and

currently, it has a network of 252 branched which includes the 166 owner managed branches

and 78 corporate branches. Headquarter of the bank is in Queensland, Australia. The main

products of the bank are consumer banking, finance and insurance, commercial banking,

credit cards etc. The bank has surveyed and it has been found that 88% customers of the

Business Finance

6

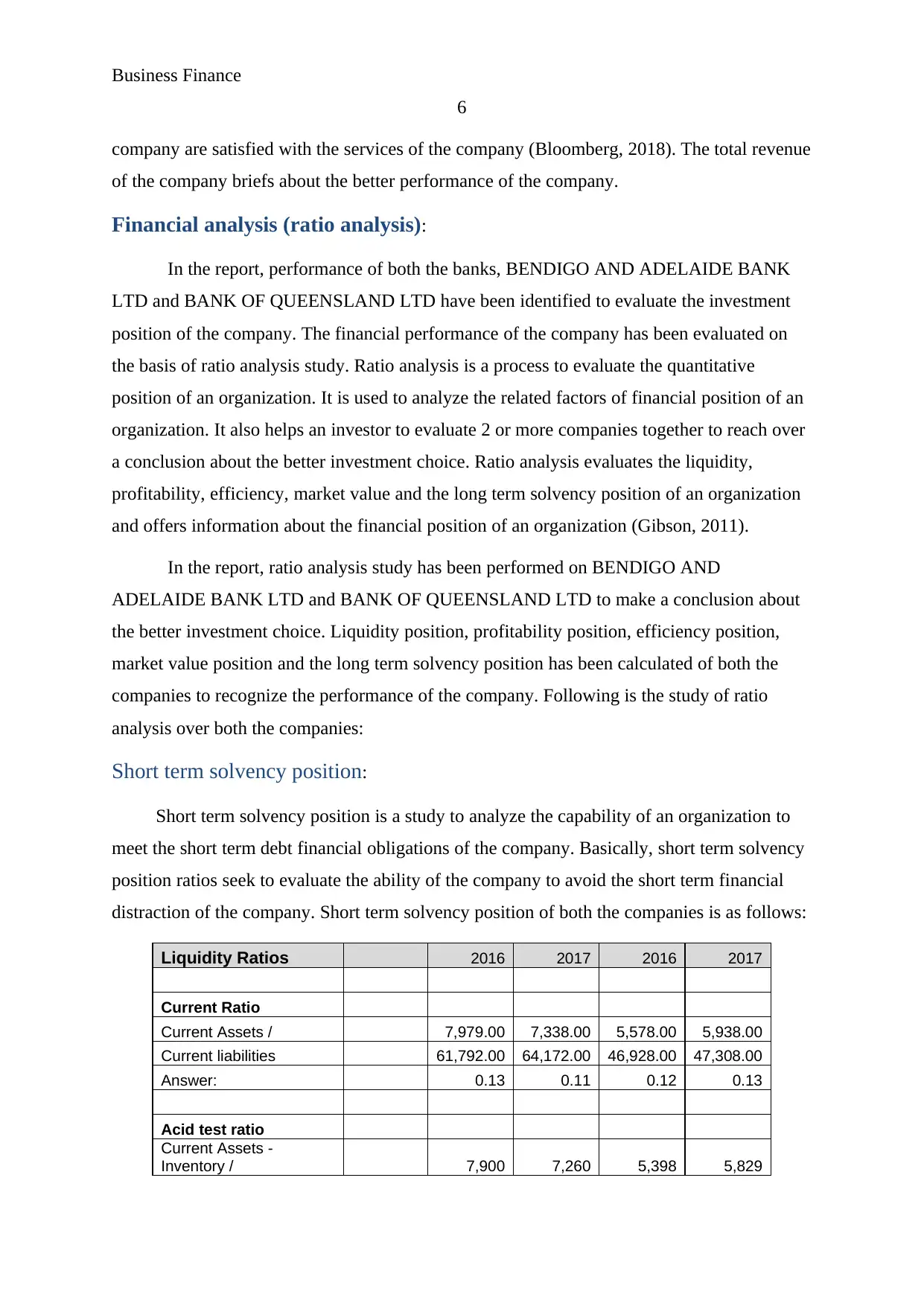

company are satisfied with the services of the company (Bloomberg, 2018). The total revenue

of the company briefs about the better performance of the company.

Financial analysis (ratio analysis):

In the report, performance of both the banks, BENDIGO AND ADELAIDE BANK

LTD and BANK OF QUEENSLAND LTD have been identified to evaluate the investment

position of the company. The financial performance of the company has been evaluated on

the basis of ratio analysis study. Ratio analysis is a process to evaluate the quantitative

position of an organization. It is used to analyze the related factors of financial position of an

organization. It also helps an investor to evaluate 2 or more companies together to reach over

a conclusion about the better investment choice. Ratio analysis evaluates the liquidity,

profitability, efficiency, market value and the long term solvency position of an organization

and offers information about the financial position of an organization (Gibson, 2011).

In the report, ratio analysis study has been performed on BENDIGO AND

ADELAIDE BANK LTD and BANK OF QUEENSLAND LTD to make a conclusion about

the better investment choice. Liquidity position, profitability position, efficiency position,

market value position and the long term solvency position has been calculated of both the

companies to recognize the performance of the company. Following is the study of ratio

analysis over both the companies:

Short term solvency position:

Short term solvency position is a study to analyze the capability of an organization to

meet the short term debt financial obligations of the company. Basically, short term solvency

position ratios seek to evaluate the ability of the company to avoid the short term financial

distraction of the company. Short term solvency position of both the companies is as follows:

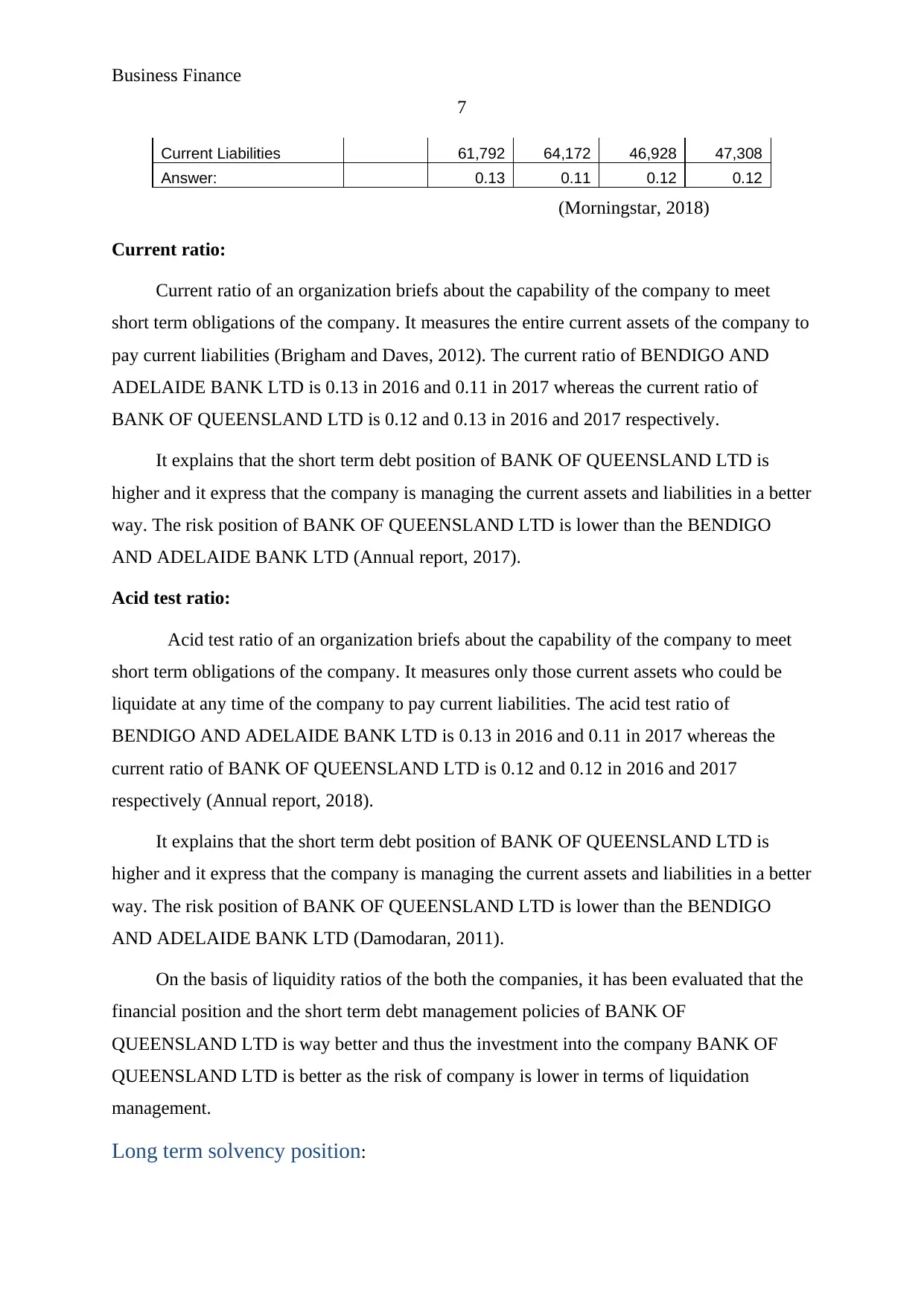

Liquidity Ratios 2016 2017 2016 2017

Current Ratio

Current Assets / 7,979.00 7,338.00 5,578.00 5,938.00

Current liabilities 61,792.00 64,172.00 46,928.00 47,308.00

Answer: 0.13 0.11 0.12 0.13

Acid test ratio

Current Assets -

Inventory / 7,900 7,260 5,398 5,829

6

company are satisfied with the services of the company (Bloomberg, 2018). The total revenue

of the company briefs about the better performance of the company.

Financial analysis (ratio analysis):

In the report, performance of both the banks, BENDIGO AND ADELAIDE BANK

LTD and BANK OF QUEENSLAND LTD have been identified to evaluate the investment

position of the company. The financial performance of the company has been evaluated on

the basis of ratio analysis study. Ratio analysis is a process to evaluate the quantitative

position of an organization. It is used to analyze the related factors of financial position of an

organization. It also helps an investor to evaluate 2 or more companies together to reach over

a conclusion about the better investment choice. Ratio analysis evaluates the liquidity,

profitability, efficiency, market value and the long term solvency position of an organization

and offers information about the financial position of an organization (Gibson, 2011).

In the report, ratio analysis study has been performed on BENDIGO AND

ADELAIDE BANK LTD and BANK OF QUEENSLAND LTD to make a conclusion about

the better investment choice. Liquidity position, profitability position, efficiency position,

market value position and the long term solvency position has been calculated of both the

companies to recognize the performance of the company. Following is the study of ratio

analysis over both the companies:

Short term solvency position:

Short term solvency position is a study to analyze the capability of an organization to

meet the short term debt financial obligations of the company. Basically, short term solvency

position ratios seek to evaluate the ability of the company to avoid the short term financial

distraction of the company. Short term solvency position of both the companies is as follows:

Liquidity Ratios 2016 2017 2016 2017

Current Ratio

Current Assets / 7,979.00 7,338.00 5,578.00 5,938.00

Current liabilities 61,792.00 64,172.00 46,928.00 47,308.00

Answer: 0.13 0.11 0.12 0.13

Acid test ratio

Current Assets -

Inventory / 7,900 7,260 5,398 5,829

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance

7

Current Liabilities 61,792 64,172 46,928 47,308

Answer: 0.13 0.11 0.12 0.12

(Morningstar, 2018)

Current ratio:

Current ratio of an organization briefs about the capability of the company to meet

short term obligations of the company. It measures the entire current assets of the company to

pay current liabilities (Brigham and Daves, 2012). The current ratio of BENDIGO AND

ADELAIDE BANK LTD is 0.13 in 2016 and 0.11 in 2017 whereas the current ratio of

BANK OF QUEENSLAND LTD is 0.12 and 0.13 in 2016 and 2017 respectively.

It explains that the short term debt position of BANK OF QUEENSLAND LTD is

higher and it express that the company is managing the current assets and liabilities in a better

way. The risk position of BANK OF QUEENSLAND LTD is lower than the BENDIGO

AND ADELAIDE BANK LTD (Annual report, 2017).

Acid test ratio:

Acid test ratio of an organization briefs about the capability of the company to meet

short term obligations of the company. It measures only those current assets who could be

liquidate at any time of the company to pay current liabilities. The acid test ratio of

BENDIGO AND ADELAIDE BANK LTD is 0.13 in 2016 and 0.11 in 2017 whereas the

current ratio of BANK OF QUEENSLAND LTD is 0.12 and 0.12 in 2016 and 2017

respectively (Annual report, 2018).

It explains that the short term debt position of BANK OF QUEENSLAND LTD is

higher and it express that the company is managing the current assets and liabilities in a better

way. The risk position of BANK OF QUEENSLAND LTD is lower than the BENDIGO

AND ADELAIDE BANK LTD (Damodaran, 2011).

On the basis of liquidity ratios of the both the companies, it has been evaluated that the

financial position and the short term debt management policies of BANK OF

QUEENSLAND LTD is way better and thus the investment into the company BANK OF

QUEENSLAND LTD is better as the risk of company is lower in terms of liquidation

management.

Long term solvency position:

7

Current Liabilities 61,792 64,172 46,928 47,308

Answer: 0.13 0.11 0.12 0.12

(Morningstar, 2018)

Current ratio:

Current ratio of an organization briefs about the capability of the company to meet

short term obligations of the company. It measures the entire current assets of the company to

pay current liabilities (Brigham and Daves, 2012). The current ratio of BENDIGO AND

ADELAIDE BANK LTD is 0.13 in 2016 and 0.11 in 2017 whereas the current ratio of

BANK OF QUEENSLAND LTD is 0.12 and 0.13 in 2016 and 2017 respectively.

It explains that the short term debt position of BANK OF QUEENSLAND LTD is

higher and it express that the company is managing the current assets and liabilities in a better

way. The risk position of BANK OF QUEENSLAND LTD is lower than the BENDIGO

AND ADELAIDE BANK LTD (Annual report, 2017).

Acid test ratio:

Acid test ratio of an organization briefs about the capability of the company to meet

short term obligations of the company. It measures only those current assets who could be

liquidate at any time of the company to pay current liabilities. The acid test ratio of

BENDIGO AND ADELAIDE BANK LTD is 0.13 in 2016 and 0.11 in 2017 whereas the

current ratio of BANK OF QUEENSLAND LTD is 0.12 and 0.12 in 2016 and 2017

respectively (Annual report, 2018).

It explains that the short term debt position of BANK OF QUEENSLAND LTD is

higher and it express that the company is managing the current assets and liabilities in a better

way. The risk position of BANK OF QUEENSLAND LTD is lower than the BENDIGO

AND ADELAIDE BANK LTD (Damodaran, 2011).

On the basis of liquidity ratios of the both the companies, it has been evaluated that the

financial position and the short term debt management policies of BANK OF

QUEENSLAND LTD is way better and thus the investment into the company BANK OF

QUEENSLAND LTD is better as the risk of company is lower in terms of liquidation

management.

Long term solvency position:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance

8

Long term solvency position is a study to analyze the capability of an organization to

meet the Long term debt financial obligations of the company. It evaluates the debt and the

total equity of the company and measure the cash flow of the company on the basis of the

debt and equity of the company (Brown, 2012). Basically, Long term solvency position ratios

seek to evaluate the ability of the company to avoid the Long term financial distraction of the

company. Long term solvency position of both the companies is as follows:

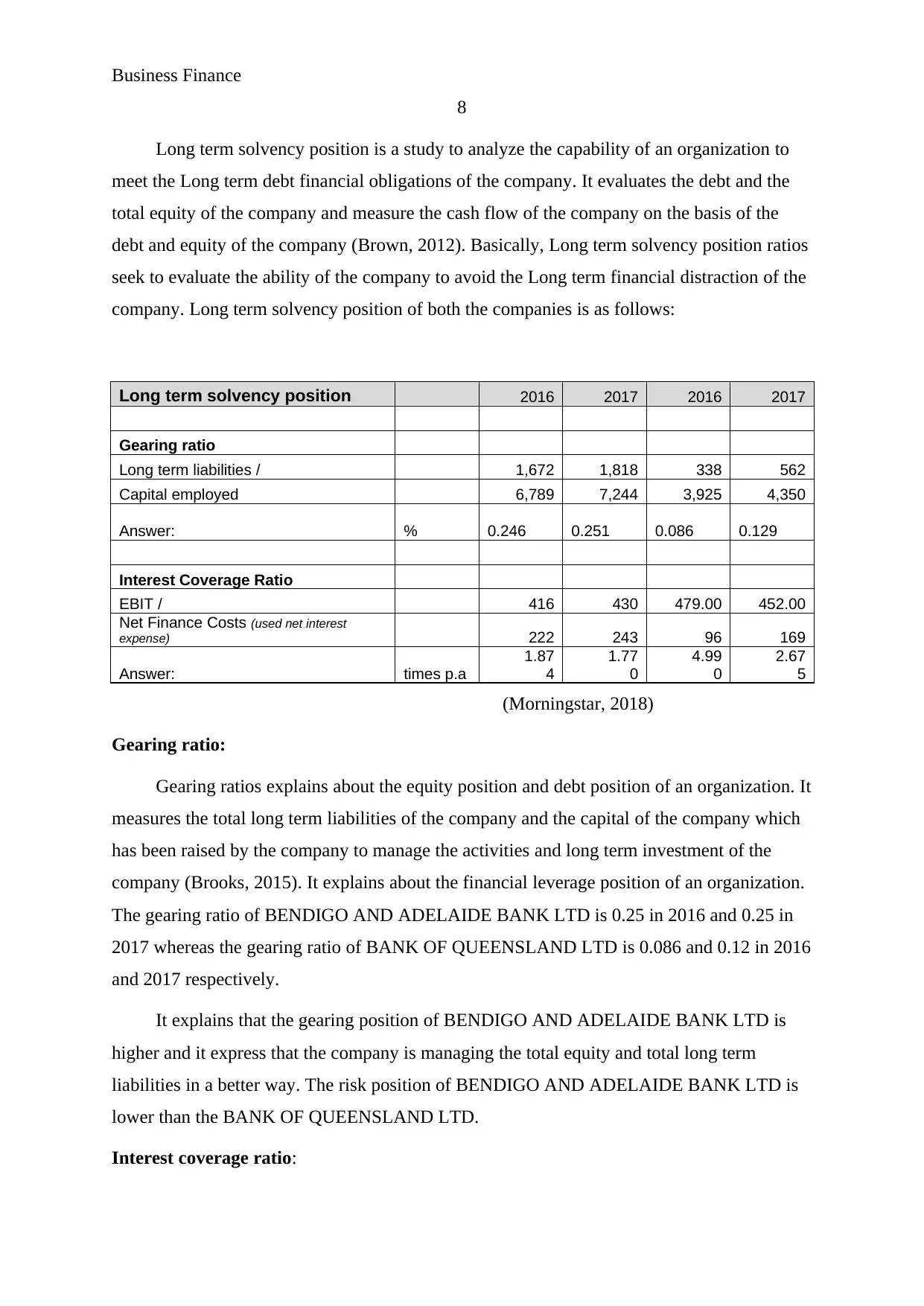

Long term solvency position 2016 2017 2016 2017

Gearing ratio

Long term liabilities / 1,672 1,818 338 562

Capital employed 6,789 7,244 3,925 4,350

Answer: % 0.246 0.251 0.086 0.129

Interest Coverage Ratio

EBIT / 416 430 479.00 452.00

Net Finance Costs (used net interest

expense) 222 243 96 169

Answer: times p.a

1.87

4

1.77

0

4.99

0

2.67

5

(Morningstar, 2018)

Gearing ratio:

Gearing ratios explains about the equity position and debt position of an organization. It

measures the total long term liabilities of the company and the capital of the company which

has been raised by the company to manage the activities and long term investment of the

company (Brooks, 2015). It explains about the financial leverage position of an organization.

The gearing ratio of BENDIGO AND ADELAIDE BANK LTD is 0.25 in 2016 and 0.25 in

2017 whereas the gearing ratio of BANK OF QUEENSLAND LTD is 0.086 and 0.12 in 2016

and 2017 respectively.

It explains that the gearing position of BENDIGO AND ADELAIDE BANK LTD is

higher and it express that the company is managing the total equity and total long term

liabilities in a better way. The risk position of BENDIGO AND ADELAIDE BANK LTD is

lower than the BANK OF QUEENSLAND LTD.

Interest coverage ratio:

8

Long term solvency position is a study to analyze the capability of an organization to

meet the Long term debt financial obligations of the company. It evaluates the debt and the

total equity of the company and measure the cash flow of the company on the basis of the

debt and equity of the company (Brown, 2012). Basically, Long term solvency position ratios

seek to evaluate the ability of the company to avoid the Long term financial distraction of the

company. Long term solvency position of both the companies is as follows:

Long term solvency position 2016 2017 2016 2017

Gearing ratio

Long term liabilities / 1,672 1,818 338 562

Capital employed 6,789 7,244 3,925 4,350

Answer: % 0.246 0.251 0.086 0.129

Interest Coverage Ratio

EBIT / 416 430 479.00 452.00

Net Finance Costs (used net interest

expense) 222 243 96 169

Answer: times p.a

1.87

4

1.77

0

4.99

0

2.67

5

(Morningstar, 2018)

Gearing ratio:

Gearing ratios explains about the equity position and debt position of an organization. It

measures the total long term liabilities of the company and the capital of the company which

has been raised by the company to manage the activities and long term investment of the

company (Brooks, 2015). It explains about the financial leverage position of an organization.

The gearing ratio of BENDIGO AND ADELAIDE BANK LTD is 0.25 in 2016 and 0.25 in

2017 whereas the gearing ratio of BANK OF QUEENSLAND LTD is 0.086 and 0.12 in 2016

and 2017 respectively.

It explains that the gearing position of BENDIGO AND ADELAIDE BANK LTD is

higher and it express that the company is managing the total equity and total long term

liabilities in a better way. The risk position of BENDIGO AND ADELAIDE BANK LTD is

lower than the BANK OF QUEENSLAND LTD.

Interest coverage ratio:

Business Finance

9

Interest coverage ratio is used to determine the interest expenses and the debt of an

organization. It explains about the interest expenses and EBIT of an organization. It measures

the total interest amount which would be paid by the company from the operating profits. It

explains about the financial leverage position of an organization. The interest coverage ratio

of BENDIGO AND ADELAIDE BANK LTD is 1.87 in 2016 and 1.77 in 2017 whereas the

gearing ratio of BANK OF QUEENSLAND LTD is 4.9 and 2.67 in 2016 and 2017

respectively (Yahoo finance, 2018).

It explains that the gearing position of BANK OF QUEENSLAND LTD is quite higher

and it express that the company has managed the long term solvency position in a better way.

The company is enough capable to pay all the interest expenses to the debt holders of the

company.

On the basis of long term solvency ratios of the both the companies, it has been

evaluated that the financial position and the long term debt management policies of BANK

OF QUEENSLAND LTD is way better and thus the investment into the company BANK OF

QUEENSLAND LTD is better as the risk of company is lower in terms of paying the

expenses to the related parties.

Asset utilization:

Asset utilization is a study to analyze the sales, revenue etc of an organization on the

basis of its inventory, receivables etc. these ratios often use an indicator of the efficiency

which is used by the company to develop the assets to generate the revenue. Basically, asset

utilization position ratios seek to evaluate the ability of the company to manage the assets and

revenue in a proper form so that the position of the company could be enhanced. Asset

utilization position of both the companies is as follows:

Asset Efficiency Ratios 2016 2017 2016 2017

Trade payable payment period ratio

Accounts payable/ 803 861 506 915

Cost of sales 1,423 1,454 1,075 1,048

Answer: (note the above needs to be x

365) 205.97 216.1382 171.80 318.68

Inventory Turnover (days)

Average Inventory / 79 78 180 109

Cost of Sales # 1,423 1,454 1,075 1,048

9

Interest coverage ratio is used to determine the interest expenses and the debt of an

organization. It explains about the interest expenses and EBIT of an organization. It measures

the total interest amount which would be paid by the company from the operating profits. It

explains about the financial leverage position of an organization. The interest coverage ratio

of BENDIGO AND ADELAIDE BANK LTD is 1.87 in 2016 and 1.77 in 2017 whereas the

gearing ratio of BANK OF QUEENSLAND LTD is 4.9 and 2.67 in 2016 and 2017

respectively (Yahoo finance, 2018).

It explains that the gearing position of BANK OF QUEENSLAND LTD is quite higher

and it express that the company has managed the long term solvency position in a better way.

The company is enough capable to pay all the interest expenses to the debt holders of the

company.

On the basis of long term solvency ratios of the both the companies, it has been

evaluated that the financial position and the long term debt management policies of BANK

OF QUEENSLAND LTD is way better and thus the investment into the company BANK OF

QUEENSLAND LTD is better as the risk of company is lower in terms of paying the

expenses to the related parties.

Asset utilization:

Asset utilization is a study to analyze the sales, revenue etc of an organization on the

basis of its inventory, receivables etc. these ratios often use an indicator of the efficiency

which is used by the company to develop the assets to generate the revenue. Basically, asset

utilization position ratios seek to evaluate the ability of the company to manage the assets and

revenue in a proper form so that the position of the company could be enhanced. Asset

utilization position of both the companies is as follows:

Asset Efficiency Ratios 2016 2017 2016 2017

Trade payable payment period ratio

Accounts payable/ 803 861 506 915

Cost of sales 1,423 1,454 1,075 1,048

Answer: (note the above needs to be x

365) 205.97 216.1382 171.80 318.68

Inventory Turnover (days)

Average Inventory / 79 78 180 109

Cost of Sales # 1,423 1,454 1,075 1,048

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance

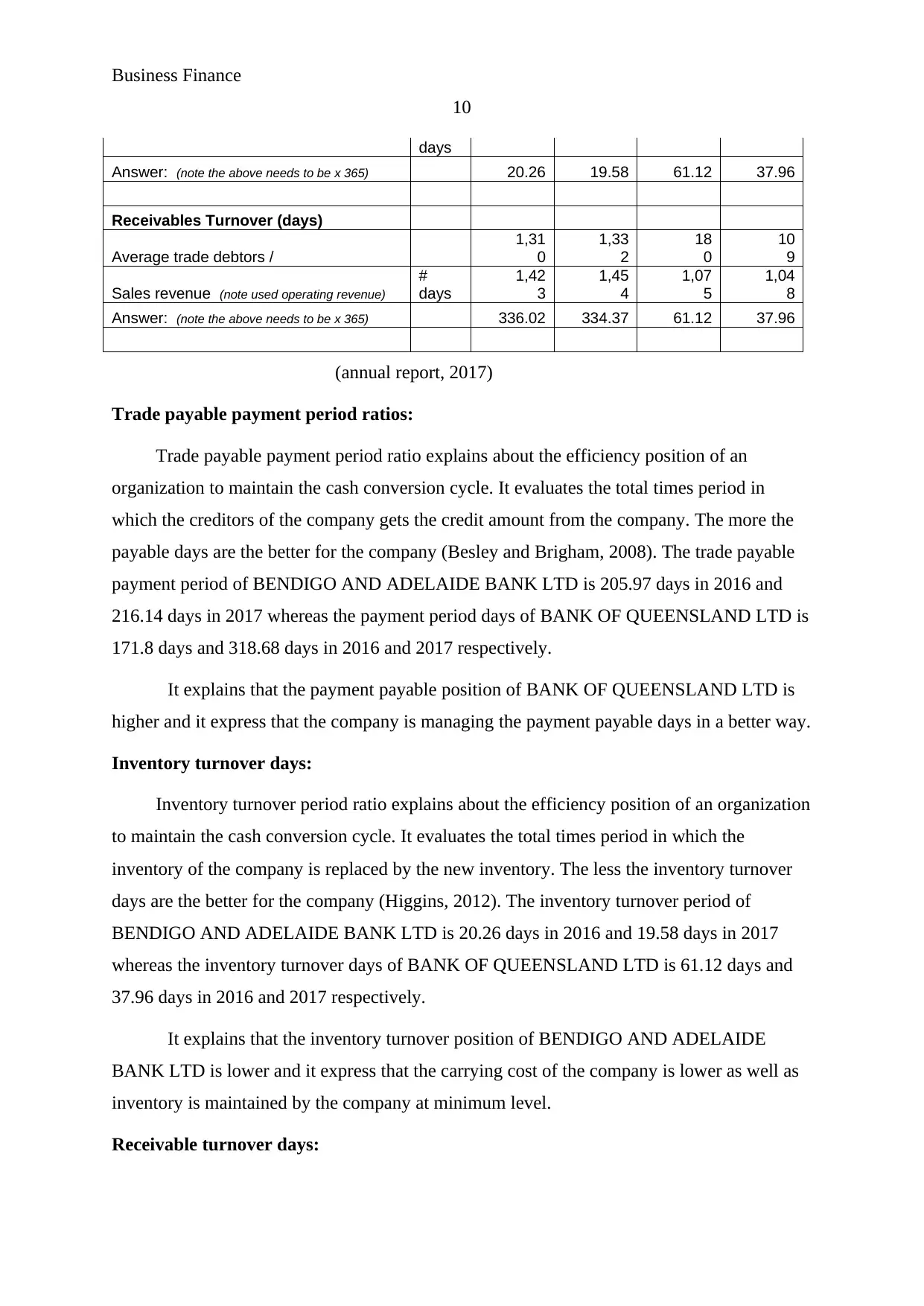

10

days

Answer: (note the above needs to be x 365) 20.26 19.58 61.12 37.96

Receivables Turnover (days)

Average trade debtors /

1,31

0

1,33

2

18

0

10

9

Sales revenue (note used operating revenue)

#

days

1,42

3

1,45

4

1,07

5

1,04

8

Answer: (note the above needs to be x 365) 336.02 334.37 61.12 37.96

(annual report, 2017)

Trade payable payment period ratios:

Trade payable payment period ratio explains about the efficiency position of an

organization to maintain the cash conversion cycle. It evaluates the total times period in

which the creditors of the company gets the credit amount from the company. The more the

payable days are the better for the company (Besley and Brigham, 2008). The trade payable

payment period of BENDIGO AND ADELAIDE BANK LTD is 205.97 days in 2016 and

216.14 days in 2017 whereas the payment period days of BANK OF QUEENSLAND LTD is

171.8 days and 318.68 days in 2016 and 2017 respectively.

It explains that the payment payable position of BANK OF QUEENSLAND LTD is

higher and it express that the company is managing the payment payable days in a better way.

Inventory turnover days:

Inventory turnover period ratio explains about the efficiency position of an organization

to maintain the cash conversion cycle. It evaluates the total times period in which the

inventory of the company is replaced by the new inventory. The less the inventory turnover

days are the better for the company (Higgins, 2012). The inventory turnover period of

BENDIGO AND ADELAIDE BANK LTD is 20.26 days in 2016 and 19.58 days in 2017

whereas the inventory turnover days of BANK OF QUEENSLAND LTD is 61.12 days and

37.96 days in 2016 and 2017 respectively.

It explains that the inventory turnover position of BENDIGO AND ADELAIDE

BANK LTD is lower and it express that the carrying cost of the company is lower as well as

inventory is maintained by the company at minimum level.

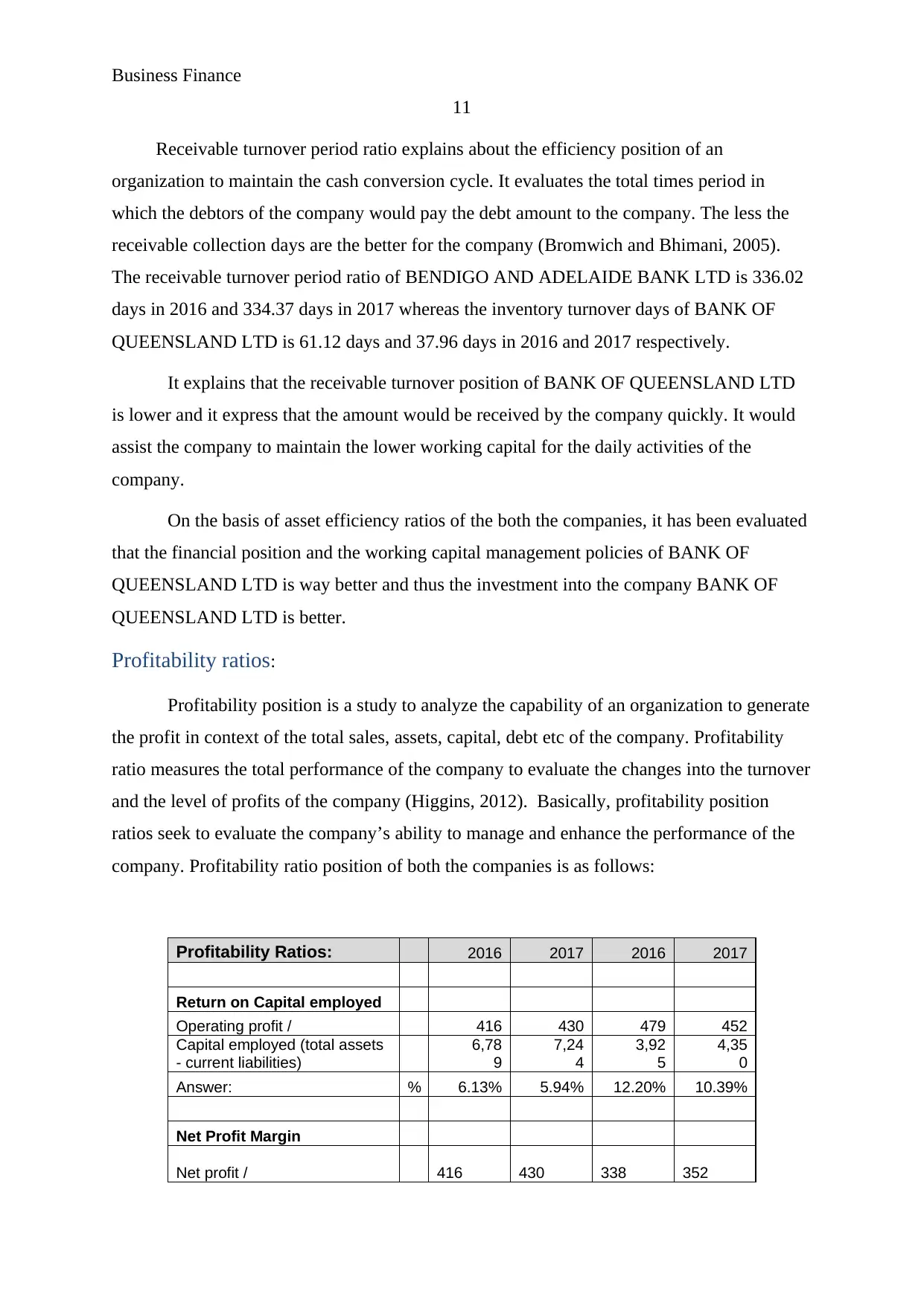

Receivable turnover days:

10

days

Answer: (note the above needs to be x 365) 20.26 19.58 61.12 37.96

Receivables Turnover (days)

Average trade debtors /

1,31

0

1,33

2

18

0

10

9

Sales revenue (note used operating revenue)

#

days

1,42

3

1,45

4

1,07

5

1,04

8

Answer: (note the above needs to be x 365) 336.02 334.37 61.12 37.96

(annual report, 2017)

Trade payable payment period ratios:

Trade payable payment period ratio explains about the efficiency position of an

organization to maintain the cash conversion cycle. It evaluates the total times period in

which the creditors of the company gets the credit amount from the company. The more the

payable days are the better for the company (Besley and Brigham, 2008). The trade payable

payment period of BENDIGO AND ADELAIDE BANK LTD is 205.97 days in 2016 and

216.14 days in 2017 whereas the payment period days of BANK OF QUEENSLAND LTD is

171.8 days and 318.68 days in 2016 and 2017 respectively.

It explains that the payment payable position of BANK OF QUEENSLAND LTD is

higher and it express that the company is managing the payment payable days in a better way.

Inventory turnover days:

Inventory turnover period ratio explains about the efficiency position of an organization

to maintain the cash conversion cycle. It evaluates the total times period in which the

inventory of the company is replaced by the new inventory. The less the inventory turnover

days are the better for the company (Higgins, 2012). The inventory turnover period of

BENDIGO AND ADELAIDE BANK LTD is 20.26 days in 2016 and 19.58 days in 2017

whereas the inventory turnover days of BANK OF QUEENSLAND LTD is 61.12 days and

37.96 days in 2016 and 2017 respectively.

It explains that the inventory turnover position of BENDIGO AND ADELAIDE

BANK LTD is lower and it express that the carrying cost of the company is lower as well as

inventory is maintained by the company at minimum level.

Receivable turnover days:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance

11

Receivable turnover period ratio explains about the efficiency position of an

organization to maintain the cash conversion cycle. It evaluates the total times period in

which the debtors of the company would pay the debt amount to the company. The less the

receivable collection days are the better for the company (Bromwich and Bhimani, 2005).

The receivable turnover period ratio of BENDIGO AND ADELAIDE BANK LTD is 336.02

days in 2016 and 334.37 days in 2017 whereas the inventory turnover days of BANK OF

QUEENSLAND LTD is 61.12 days and 37.96 days in 2016 and 2017 respectively.

It explains that the receivable turnover position of BANK OF QUEENSLAND LTD

is lower and it express that the amount would be received by the company quickly. It would

assist the company to maintain the lower working capital for the daily activities of the

company.

On the basis of asset efficiency ratios of the both the companies, it has been evaluated

that the financial position and the working capital management policies of BANK OF

QUEENSLAND LTD is way better and thus the investment into the company BANK OF

QUEENSLAND LTD is better.

Profitability ratios:

Profitability position is a study to analyze the capability of an organization to generate

the profit in context of the total sales, assets, capital, debt etc of the company. Profitability

ratio measures the total performance of the company to evaluate the changes into the turnover

and the level of profits of the company (Higgins, 2012). Basically, profitability position

ratios seek to evaluate the company’s ability to manage and enhance the performance of the

company. Profitability ratio position of both the companies is as follows:

Profitability Ratios: 2016 2017 2016 2017

Return on Capital employed

Operating profit / 416 430 479 452

Capital employed (total assets

- current liabilities)

6,78

9

7,24

4

3,92

5

4,35

0

Answer: % 6.13% 5.94% 12.20% 10.39%

Net Profit Margin

Net profit / 416 430 338 352

11

Receivable turnover period ratio explains about the efficiency position of an

organization to maintain the cash conversion cycle. It evaluates the total times period in

which the debtors of the company would pay the debt amount to the company. The less the

receivable collection days are the better for the company (Bromwich and Bhimani, 2005).

The receivable turnover period ratio of BENDIGO AND ADELAIDE BANK LTD is 336.02

days in 2016 and 334.37 days in 2017 whereas the inventory turnover days of BANK OF

QUEENSLAND LTD is 61.12 days and 37.96 days in 2016 and 2017 respectively.

It explains that the receivable turnover position of BANK OF QUEENSLAND LTD

is lower and it express that the amount would be received by the company quickly. It would

assist the company to maintain the lower working capital for the daily activities of the

company.

On the basis of asset efficiency ratios of the both the companies, it has been evaluated

that the financial position and the working capital management policies of BANK OF

QUEENSLAND LTD is way better and thus the investment into the company BANK OF

QUEENSLAND LTD is better.

Profitability ratios:

Profitability position is a study to analyze the capability of an organization to generate

the profit in context of the total sales, assets, capital, debt etc of the company. Profitability

ratio measures the total performance of the company to evaluate the changes into the turnover

and the level of profits of the company (Higgins, 2012). Basically, profitability position

ratios seek to evaluate the company’s ability to manage and enhance the performance of the

company. Profitability ratio position of both the companies is as follows:

Profitability Ratios: 2016 2017 2016 2017

Return on Capital employed

Operating profit / 416 430 479 452

Capital employed (total assets

- current liabilities)

6,78

9

7,24

4

3,92

5

4,35

0

Answer: % 6.13% 5.94% 12.20% 10.39%

Net Profit Margin

Net profit / 416 430 338 352

Business Finance

12

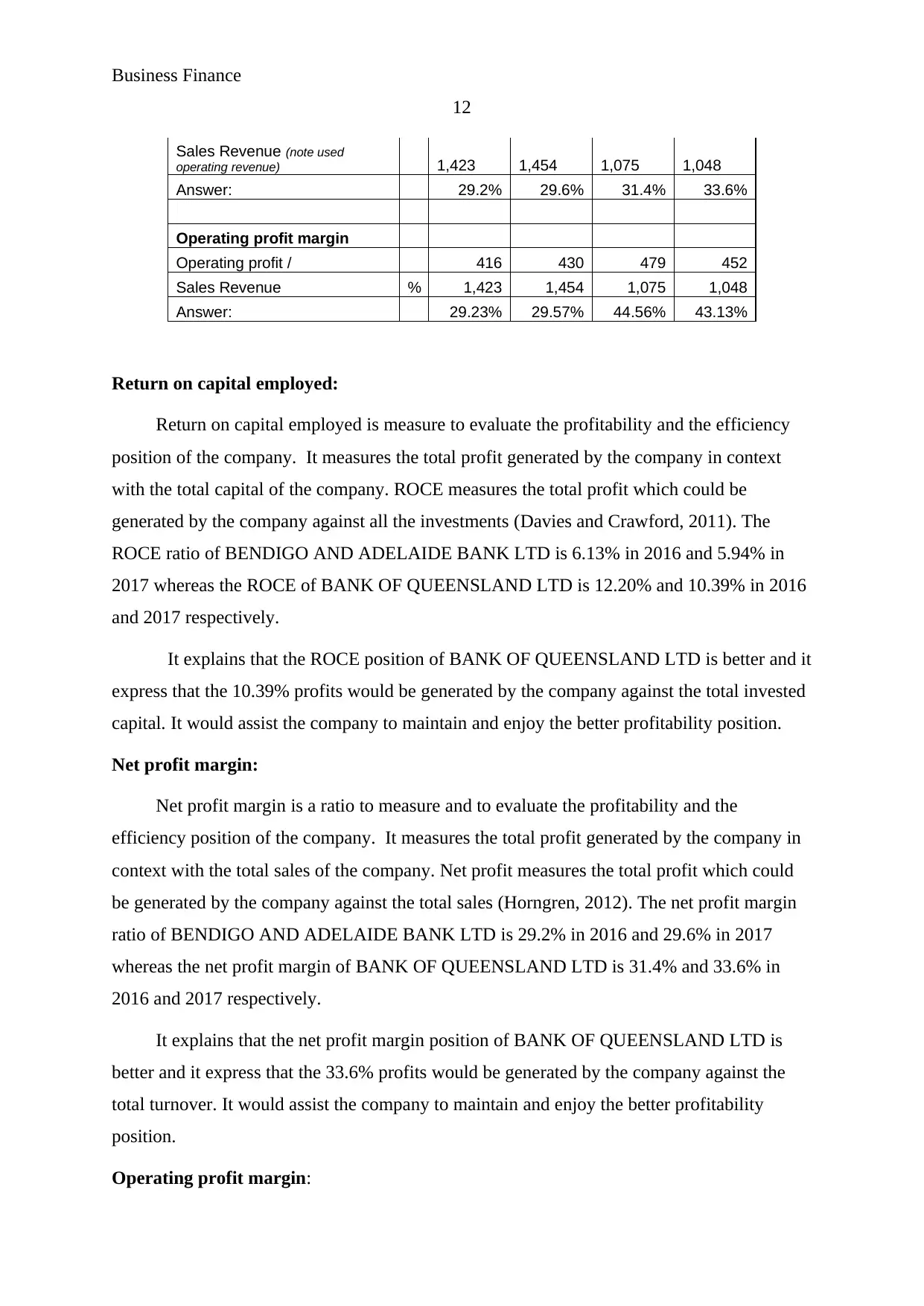

Sales Revenue (note used

operating revenue) 1,423 1,454 1,075 1,048

Answer: 29.2% 29.6% 31.4% 33.6%

Operating profit margin

Operating profit / 416 430 479 452

Sales Revenue % 1,423 1,454 1,075 1,048

Answer: 29.23% 29.57% 44.56% 43.13%

Return on capital employed:

Return on capital employed is measure to evaluate the profitability and the efficiency

position of the company. It measures the total profit generated by the company in context

with the total capital of the company. ROCE measures the total profit which could be

generated by the company against all the investments (Davies and Crawford, 2011). The

ROCE ratio of BENDIGO AND ADELAIDE BANK LTD is 6.13% in 2016 and 5.94% in

2017 whereas the ROCE of BANK OF QUEENSLAND LTD is 12.20% and 10.39% in 2016

and 2017 respectively.

It explains that the ROCE position of BANK OF QUEENSLAND LTD is better and it

express that the 10.39% profits would be generated by the company against the total invested

capital. It would assist the company to maintain and enjoy the better profitability position.

Net profit margin:

Net profit margin is a ratio to measure and to evaluate the profitability and the

efficiency position of the company. It measures the total profit generated by the company in

context with the total sales of the company. Net profit measures the total profit which could

be generated by the company against the total sales (Horngren, 2012). The net profit margin

ratio of BENDIGO AND ADELAIDE BANK LTD is 29.2% in 2016 and 29.6% in 2017

whereas the net profit margin of BANK OF QUEENSLAND LTD is 31.4% and 33.6% in

2016 and 2017 respectively.

It explains that the net profit margin position of BANK OF QUEENSLAND LTD is

better and it express that the 33.6% profits would be generated by the company against the

total turnover. It would assist the company to maintain and enjoy the better profitability

position.

Operating profit margin:

12

Sales Revenue (note used

operating revenue) 1,423 1,454 1,075 1,048

Answer: 29.2% 29.6% 31.4% 33.6%

Operating profit margin

Operating profit / 416 430 479 452

Sales Revenue % 1,423 1,454 1,075 1,048

Answer: 29.23% 29.57% 44.56% 43.13%

Return on capital employed:

Return on capital employed is measure to evaluate the profitability and the efficiency

position of the company. It measures the total profit generated by the company in context

with the total capital of the company. ROCE measures the total profit which could be

generated by the company against all the investments (Davies and Crawford, 2011). The

ROCE ratio of BENDIGO AND ADELAIDE BANK LTD is 6.13% in 2016 and 5.94% in

2017 whereas the ROCE of BANK OF QUEENSLAND LTD is 12.20% and 10.39% in 2016

and 2017 respectively.

It explains that the ROCE position of BANK OF QUEENSLAND LTD is better and it

express that the 10.39% profits would be generated by the company against the total invested

capital. It would assist the company to maintain and enjoy the better profitability position.

Net profit margin:

Net profit margin is a ratio to measure and to evaluate the profitability and the

efficiency position of the company. It measures the total profit generated by the company in

context with the total sales of the company. Net profit measures the total profit which could

be generated by the company against the total sales (Horngren, 2012). The net profit margin

ratio of BENDIGO AND ADELAIDE BANK LTD is 29.2% in 2016 and 29.6% in 2017

whereas the net profit margin of BANK OF QUEENSLAND LTD is 31.4% and 33.6% in

2016 and 2017 respectively.

It explains that the net profit margin position of BANK OF QUEENSLAND LTD is

better and it express that the 33.6% profits would be generated by the company against the

total turnover. It would assist the company to maintain and enjoy the better profitability

position.

Operating profit margin:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.