Financial Analysis Project: Blackmores Company Report

VerifiedAdded on 2023/01/11

|10

|2446

|34

Project

AI Summary

This project provides a comprehensive financial analysis of Blackmores, an Australian listed company. It begins with an examination of Blackmores' corporate governance structure, policies, and their alignment with stakeholder interests. The project then delves into the company's cash conversion cycle, comparing its performance in 2018 and 2019, identifying key drivers of change. Furthermore, it calculates and discusses Blackmores' net working capital, exploring its asset management strategy, and outlining the pros and cons. The project also identifies and categorizes major financial risks, including liquidity, credit, and interest rate risks. An analysis of Blackmores' share price is presented, considering dividend growth and market risk. The project concludes with the determination of the issue price of bonds, followed by a capital budgeting analysis of a new manufacturing facility. This includes calculating free cash flows (FCFs), net present value (NPV) at different discount rates, and the discounted payback period, culminating in a justification for the investment decision. The project utilizes financial data and calculations to support its conclusions, offering insights into Blackmores' financial performance and investment potential.

Project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

COMPANY PESPECTIVE.............................................................................................................1

a. analysis of the way in which Blackmore’s governance is organised.......................................1

b. calculation and discussion of the way in which cash conversion cycle of Blackmore is

changed during year 2018 and 2019............................................................................................1

c. What is the net working capital of Blackmore, which asset management strategy is used by

the company and props and cons of this strategy........................................................................3

d. Identification of three major risks in the annual report and these are systematic or not.........4

e. Analysis of the share price of Blackmore................................................................................4

f. Determination of the issue price of the bonds..........................................................................5

CAPITAL BUDGETING................................................................................................................6

a. Calculation of FCFs of the project...........................................................................................6

b. Calculation of NPV of the new manufacturing facility of the entity.......................................6

c. Discounted pay-back period for the project.............................................................................7

d. Justification regarding selecting the project or not..................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

COMPANY PESPECTIVE.............................................................................................................1

a. analysis of the way in which Blackmore’s governance is organised.......................................1

b. calculation and discussion of the way in which cash conversion cycle of Blackmore is

changed during year 2018 and 2019............................................................................................1

c. What is the net working capital of Blackmore, which asset management strategy is used by

the company and props and cons of this strategy........................................................................3

d. Identification of three major risks in the annual report and these are systematic or not.........4

e. Analysis of the share price of Blackmore................................................................................4

f. Determination of the issue price of the bonds..........................................................................5

CAPITAL BUDGETING................................................................................................................6

a. Calculation of FCFs of the project...........................................................................................6

b. Calculation of NPV of the new manufacturing facility of the entity.......................................6

c. Discounted pay-back period for the project.............................................................................7

d. Justification regarding selecting the project or not..................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Project can be defined as the task which is allocated by a senior authority to their juniors.

Present report is based upon Blackmore which is one of the listed companies of Australia. This

assignment covers various topics such as analysis of governance, determination of share price,

analysis of bond issue price etc. Apart from this, NPV and discounted pay back along with future

cash flow are calculated for the organisation.

COMPANY PESPECTIVE

a. analysis of the way in which Blackmore’s governance is organised

From the annual report of Blackmores, it has been determined that the entity is highly

focused with management of the business and dedicated towards the highest standard of

corporate behaviour and accountability throughout all the level of enterprise. The corporate

governance of the company is developed with the help of framework of ASX Corporate

Governance council’s corporate governance principles and recommendations. There are various

policies which are focused by the enterprise (Blackmores Group Governance & Board of

Directors, 2019). These are Anti Bribery and Corruption policy, Blackmores Constitution, Board

Charter, Code of Conduct etc. By analysing the annual report, it has been determined that the

company is following specific strategy so that it can align manager and stakeholder interest

within the entity. For this purpose, the organisation is paying attention towards different types of

policies such as nominations committee charter, share trading policy, supplier code of product,

sustainability position etc. For example, if the company will follow the strategies which are

focused with managers and shareholders then it will help to align both of them at the enterprise.

As the organisation is following different types of policies so it can help to make sure that

managers and shareholders are aligned with the business properly.

b. calculation and discussion of the way in which cash conversion cycle of Blackmore is changed

during year 2018 and 2019

Cash conversion cycle:

Cash conversion cycle

Particulars 2018 2019

Days of sales outstanding 91.48 86.08

Add: Days of inventory outstanding 162.95 187.18

Less: Days of payable outstanding 248.3 197.3

1

Project can be defined as the task which is allocated by a senior authority to their juniors.

Present report is based upon Blackmore which is one of the listed companies of Australia. This

assignment covers various topics such as analysis of governance, determination of share price,

analysis of bond issue price etc. Apart from this, NPV and discounted pay back along with future

cash flow are calculated for the organisation.

COMPANY PESPECTIVE

a. analysis of the way in which Blackmore’s governance is organised

From the annual report of Blackmores, it has been determined that the entity is highly

focused with management of the business and dedicated towards the highest standard of

corporate behaviour and accountability throughout all the level of enterprise. The corporate

governance of the company is developed with the help of framework of ASX Corporate

Governance council’s corporate governance principles and recommendations. There are various

policies which are focused by the enterprise (Blackmores Group Governance & Board of

Directors, 2019). These are Anti Bribery and Corruption policy, Blackmores Constitution, Board

Charter, Code of Conduct etc. By analysing the annual report, it has been determined that the

company is following specific strategy so that it can align manager and stakeholder interest

within the entity. For this purpose, the organisation is paying attention towards different types of

policies such as nominations committee charter, share trading policy, supplier code of product,

sustainability position etc. For example, if the company will follow the strategies which are

focused with managers and shareholders then it will help to align both of them at the enterprise.

As the organisation is following different types of policies so it can help to make sure that

managers and shareholders are aligned with the business properly.

b. calculation and discussion of the way in which cash conversion cycle of Blackmore is changed

during year 2018 and 2019

Cash conversion cycle:

Cash conversion cycle

Particulars 2018 2019

Days of sales outstanding 91.48 86.08

Add: Days of inventory outstanding 162.95 187.18

Less: Days of payable outstanding 248.3 197.3

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

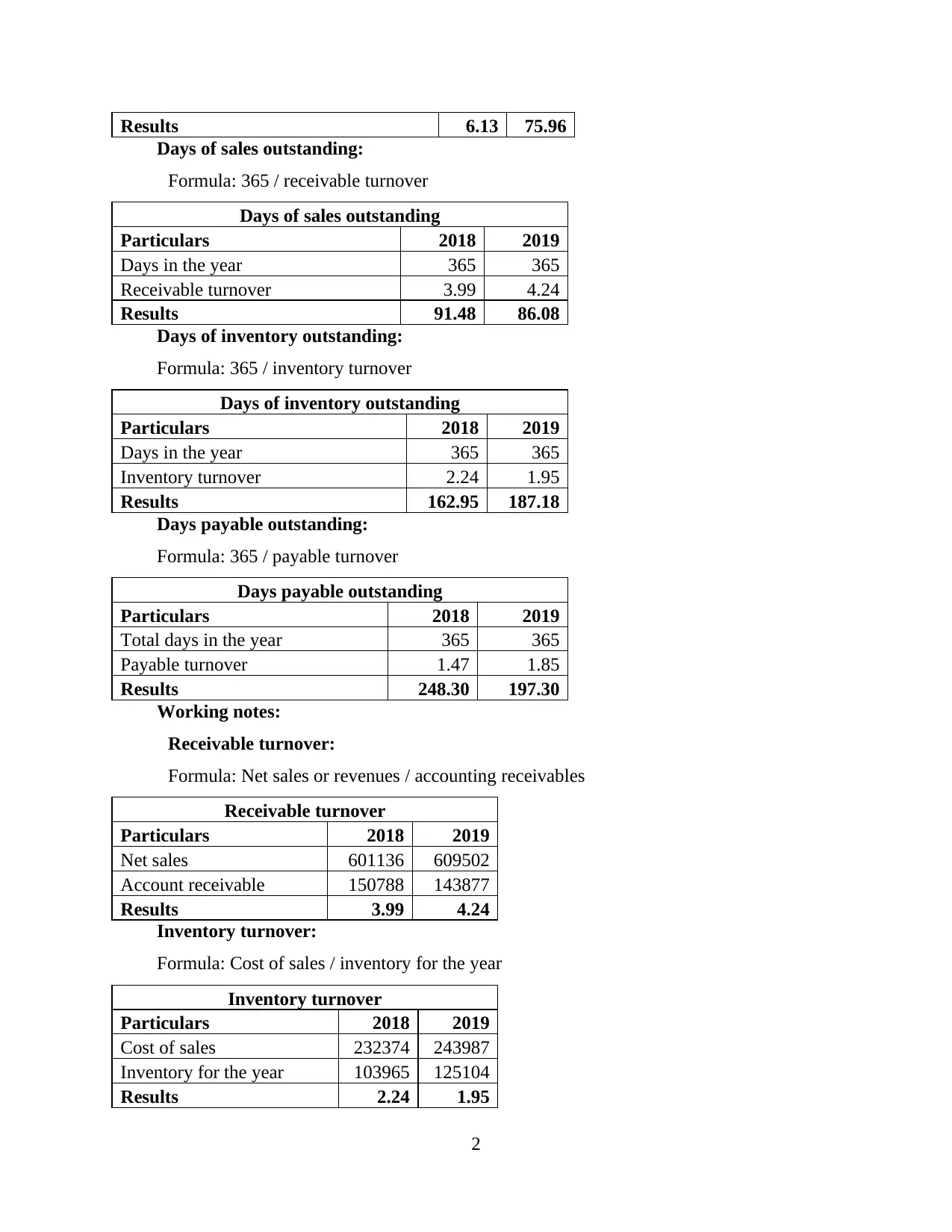

Results 6.13 75.96

Days of sales outstanding:

Formula: 365 / receivable turnover

Days of sales outstanding

Particulars 2018 2019

Days in the year 365 365

Receivable turnover 3.99 4.24

Results 91.48 86.08

Days of inventory outstanding:

Formula: 365 / inventory turnover

Days of inventory outstanding

Particulars 2018 2019

Days in the year 365 365

Inventory turnover 2.24 1.95

Results 162.95 187.18

Days payable outstanding:

Formula: 365 / payable turnover

Days payable outstanding

Particulars 2018 2019

Total days in the year 365 365

Payable turnover 1.47 1.85

Results 248.30 197.30

Working notes:

Receivable turnover:

Formula: Net sales or revenues / accounting receivables

Receivable turnover

Particulars 2018 2019

Net sales 601136 609502

Account receivable 150788 143877

Results 3.99 4.24

Inventory turnover:

Formula: Cost of sales / inventory for the year

Inventory turnover

Particulars 2018 2019

Cost of sales 232374 243987

Inventory for the year 103965 125104

Results 2.24 1.95

2

Days of sales outstanding:

Formula: 365 / receivable turnover

Days of sales outstanding

Particulars 2018 2019

Days in the year 365 365

Receivable turnover 3.99 4.24

Results 91.48 86.08

Days of inventory outstanding:

Formula: 365 / inventory turnover

Days of inventory outstanding

Particulars 2018 2019

Days in the year 365 365

Inventory turnover 2.24 1.95

Results 162.95 187.18

Days payable outstanding:

Formula: 365 / payable turnover

Days payable outstanding

Particulars 2018 2019

Total days in the year 365 365

Payable turnover 1.47 1.85

Results 248.30 197.30

Working notes:

Receivable turnover:

Formula: Net sales or revenues / accounting receivables

Receivable turnover

Particulars 2018 2019

Net sales 601136 609502

Account receivable 150788 143877

Results 3.99 4.24

Inventory turnover:

Formula: Cost of sales / inventory for the year

Inventory turnover

Particulars 2018 2019

Cost of sales 232374 243987

Inventory for the year 103965 125104

Results 2.24 1.95

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

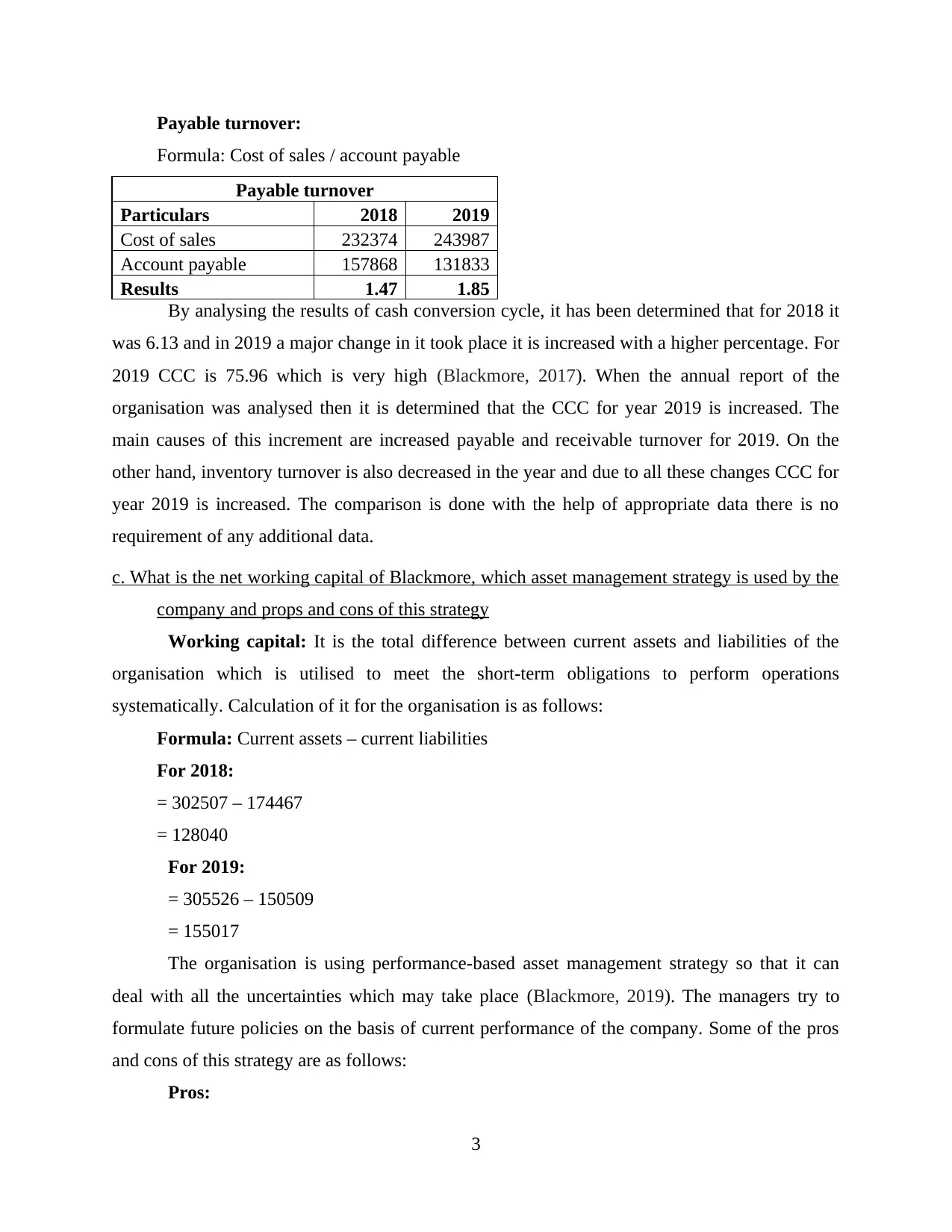

Payable turnover:

Formula: Cost of sales / account payable

Payable turnover

Particulars 2018 2019

Cost of sales 232374 243987

Account payable 157868 131833

Results 1.47 1.85

By analysing the results of cash conversion cycle, it has been determined that for 2018 it

was 6.13 and in 2019 a major change in it took place it is increased with a higher percentage. For

2019 CCC is 75.96 which is very high (Blackmore, 2017). When the annual report of the

organisation was analysed then it is determined that the CCC for year 2019 is increased. The

main causes of this increment are increased payable and receivable turnover for 2019. On the

other hand, inventory turnover is also decreased in the year and due to all these changes CCC for

year 2019 is increased. The comparison is done with the help of appropriate data there is no

requirement of any additional data.

c. What is the net working capital of Blackmore, which asset management strategy is used by the

company and props and cons of this strategy

Working capital: It is the total difference between current assets and liabilities of the

organisation which is utilised to meet the short-term obligations to perform operations

systematically. Calculation of it for the organisation is as follows:

Formula: Current assets – current liabilities

For 2018:

= 302507 – 174467

= 128040

For 2019:

= 305526 – 150509

= 155017

The organisation is using performance-based asset management strategy so that it can

deal with all the uncertainties which may take place (Blackmore, 2019). The managers try to

formulate future policies on the basis of current performance of the company. Some of the pros

and cons of this strategy are as follows:

Pros:

3

Formula: Cost of sales / account payable

Payable turnover

Particulars 2018 2019

Cost of sales 232374 243987

Account payable 157868 131833

Results 1.47 1.85

By analysing the results of cash conversion cycle, it has been determined that for 2018 it

was 6.13 and in 2019 a major change in it took place it is increased with a higher percentage. For

2019 CCC is 75.96 which is very high (Blackmore, 2017). When the annual report of the

organisation was analysed then it is determined that the CCC for year 2019 is increased. The

main causes of this increment are increased payable and receivable turnover for 2019. On the

other hand, inventory turnover is also decreased in the year and due to all these changes CCC for

year 2019 is increased. The comparison is done with the help of appropriate data there is no

requirement of any additional data.

c. What is the net working capital of Blackmore, which asset management strategy is used by the

company and props and cons of this strategy

Working capital: It is the total difference between current assets and liabilities of the

organisation which is utilised to meet the short-term obligations to perform operations

systematically. Calculation of it for the organisation is as follows:

Formula: Current assets – current liabilities

For 2018:

= 302507 – 174467

= 128040

For 2019:

= 305526 – 150509

= 155017

The organisation is using performance-based asset management strategy so that it can

deal with all the uncertainties which may take place (Blackmore, 2019). The managers try to

formulate future policies on the basis of current performance of the company. Some of the pros

and cons of this strategy are as follows:

Pros:

3

With the help of it, actual performance of business could be determined so that assets

could be managed properly.

It provides actual insight to the managers for formulate of future strategies.

Cons:

The process of it is time consuming which may affect the process of policy formulation.

The cost of using it is very high as experienced individual is required to analyse its

results.

d. Identification of three major risks in the annual report and these are systematic or not

By analysing the annual report of Blackmores, it has been identified that there are various

types of risks that may affect the functionality of business. The major risks that are affecting the

company are as follows:

Liquidity risk: This risk takes place when the company is not able to keep the minimum

funds that are required to meet short term obligations. This risk is systematic as it directly leaves

impact upon performance of business (Annual report of Blackmore, 2019).

Credit risk: This type of risk is related to the recovery of all the outstanding amount

which is required to be recovered from debtors. This type of risk is unsystematic because it is not

possible to estimate as any debtor may fail to make payment on due date.

Interest rate risk: When an entity invests funds in outsider sources then it is the main

risk which may take place. It is also an unsystematic risk as it could not be forecasted that

interest rate will incline or decline in future (Sun, 2019).

e. Analysis of the share price of Blackmore

As the current price of the share is 88.16 and the dividend rate of it will be increased in

future so it will be good option for investment. The main reason for it is that for the next two

years the dividend will be increased by 30 and 25% respectively. Afterwards, for next three year

it will be growing by 6% forever. It shows that if investment in it will be made then it can benefit

the shareholders to get higher and higher dividend as the rate of it is increasing continuously. On

the other hand, the market risk premium for the shares is also very high so it will be a good

option to buy the shares (Ducastel and Anseeuw, 2018).

4

could be managed properly.

It provides actual insight to the managers for formulate of future strategies.

Cons:

The process of it is time consuming which may affect the process of policy formulation.

The cost of using it is very high as experienced individual is required to analyse its

results.

d. Identification of three major risks in the annual report and these are systematic or not

By analysing the annual report of Blackmores, it has been identified that there are various

types of risks that may affect the functionality of business. The major risks that are affecting the

company are as follows:

Liquidity risk: This risk takes place when the company is not able to keep the minimum

funds that are required to meet short term obligations. This risk is systematic as it directly leaves

impact upon performance of business (Annual report of Blackmore, 2019).

Credit risk: This type of risk is related to the recovery of all the outstanding amount

which is required to be recovered from debtors. This type of risk is unsystematic because it is not

possible to estimate as any debtor may fail to make payment on due date.

Interest rate risk: When an entity invests funds in outsider sources then it is the main

risk which may take place. It is also an unsystematic risk as it could not be forecasted that

interest rate will incline or decline in future (Sun, 2019).

e. Analysis of the share price of Blackmore

As the current price of the share is 88.16 and the dividend rate of it will be increased in

future so it will be good option for investment. The main reason for it is that for the next two

years the dividend will be increased by 30 and 25% respectively. Afterwards, for next three year

it will be growing by 6% forever. It shows that if investment in it will be made then it can benefit

the shareholders to get higher and higher dividend as the rate of it is increasing continuously. On

the other hand, the market risk premium for the shares is also very high so it will be a good

option to buy the shares (Ducastel and Anseeuw, 2018).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

f. Determination of the issue price of the bonds

As the company is planning to launch new bonds in the market so it will be very important

for it to analyse the issue price (QUANSAH, SARPONG and ASUMDA, 2018). Which is

calculated as follows:

Provided information:

Coupon rate = 1.5%

Rate of return = 2.5%

Face value = 1

Interest rate: 2.5 – 1.5 = 1%

Determining the interest for the bonds = 1 * 1%

= 0.01 per bond

As the bonds are semi annual coupon bond for 10 years so its value will be calculated for

1% for 20 years as the duration of it will be doubled because of its nature. According to

Present Value table for this period the PV factor will be 0.8195. The present value annuity

factor for the same is 18.045 (Kenfack, Nguiffo and Nkuintchua, 2016).

Afterwards the interest will be required to be multiplied with it so the calculation of it is

as follows:

= 0.01 * 18.045

= 0.18045

Now the current value of bond is required to be analysed which is as follows:

= 1 * 0.8195

= 0.8195

The issue price of bond will be as follows:

= 0.18045 + 0.8195

= 0.99995

According to above calculations the issue price is 0.99995

CAPITAL BUDGETING

a. Calculation of FCFs of the project

Years Sales

Capital

expenses

Operating

cost

Net

income Dep.

Profit

before Tax

Profit

after

tax Dep.

Future

cash

flow

5

As the company is planning to launch new bonds in the market so it will be very important

for it to analyse the issue price (QUANSAH, SARPONG and ASUMDA, 2018). Which is

calculated as follows:

Provided information:

Coupon rate = 1.5%

Rate of return = 2.5%

Face value = 1

Interest rate: 2.5 – 1.5 = 1%

Determining the interest for the bonds = 1 * 1%

= 0.01 per bond

As the bonds are semi annual coupon bond for 10 years so its value will be calculated for

1% for 20 years as the duration of it will be doubled because of its nature. According to

Present Value table for this period the PV factor will be 0.8195. The present value annuity

factor for the same is 18.045 (Kenfack, Nguiffo and Nkuintchua, 2016).

Afterwards the interest will be required to be multiplied with it so the calculation of it is

as follows:

= 0.01 * 18.045

= 0.18045

Now the current value of bond is required to be analysed which is as follows:

= 1 * 0.8195

= 0.8195

The issue price of bond will be as follows:

= 0.18045 + 0.8195

= 0.99995

According to above calculations the issue price is 0.99995

CAPITAL BUDGETING

a. Calculation of FCFs of the project

Years Sales

Capital

expenses

Operating

cost

Net

income Dep.

Profit

before Tax

Profit

after

tax Dep.

Future

cash

flow

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

2 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

3 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

4 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

5 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

6 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

7 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

8 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

9 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

10 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

Total 1057

b. Calculation of NPV of the new manufacturing facility of the entity

Years

Future

cash flow

Present

value

factor

@10%

Discounted

cash

inflow

Present

value

factor

@15%

Discounted

cash

inflow

1 82.55 0.909 75.04 0.87 71.82

2 82.55 0.826 68.19 0.756 62.41

3 82.55 0.751 62.00 0.658 54.32

4 82.55 0.683 56.38 0.571 47.14

5 82.55 0.621 51.26 0.497 41.03

6 128.8 0.565 72.77 0.432 55.64

7 128.8 0.513 66.07 0.376 48.43

8 128.8 0.467 60.15 0.327 42.12

9 128.8 0.424 54.61 0.284 36.58

10 128.8 0.389 50.10 0.247 31.81

Scrap

value 10 0.389 3.89 0.247 2.47

Total 620.46 493.76

Net present value = Discounted cash inflow – initial investment

NPV @ 10% = 620.46 – 500

= 120.46

NPV @ 15% = 493.76 – 500

= - 6.24

c. Discounted pay-back period for the project

Discounted pay back period =

6

2 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

3 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

4 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

5 150 1 52.5 96.5 50 46.5 13.95 32.55 50 82.55

6 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

7 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

8 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

9 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

10 250 0 87.5 162.5 50 112.5 33.75 78.75 50 128.8

Total 1057

b. Calculation of NPV of the new manufacturing facility of the entity

Years

Future

cash flow

Present

value

factor

@10%

Discounted

cash

inflow

Present

value

factor

@15%

Discounted

cash

inflow

1 82.55 0.909 75.04 0.87 71.82

2 82.55 0.826 68.19 0.756 62.41

3 82.55 0.751 62.00 0.658 54.32

4 82.55 0.683 56.38 0.571 47.14

5 82.55 0.621 51.26 0.497 41.03

6 128.8 0.565 72.77 0.432 55.64

7 128.8 0.513 66.07 0.376 48.43

8 128.8 0.467 60.15 0.327 42.12

9 128.8 0.424 54.61 0.284 36.58

10 128.8 0.389 50.10 0.247 31.81

Scrap

value 10 0.389 3.89 0.247 2.47

Total 620.46 493.76

Net present value = Discounted cash inflow – initial investment

NPV @ 10% = 620.46 – 500

= 120.46

NPV @ 15% = 493.76 – 500

= - 6.24

c. Discounted pay-back period for the project

Discounted pay back period =

6

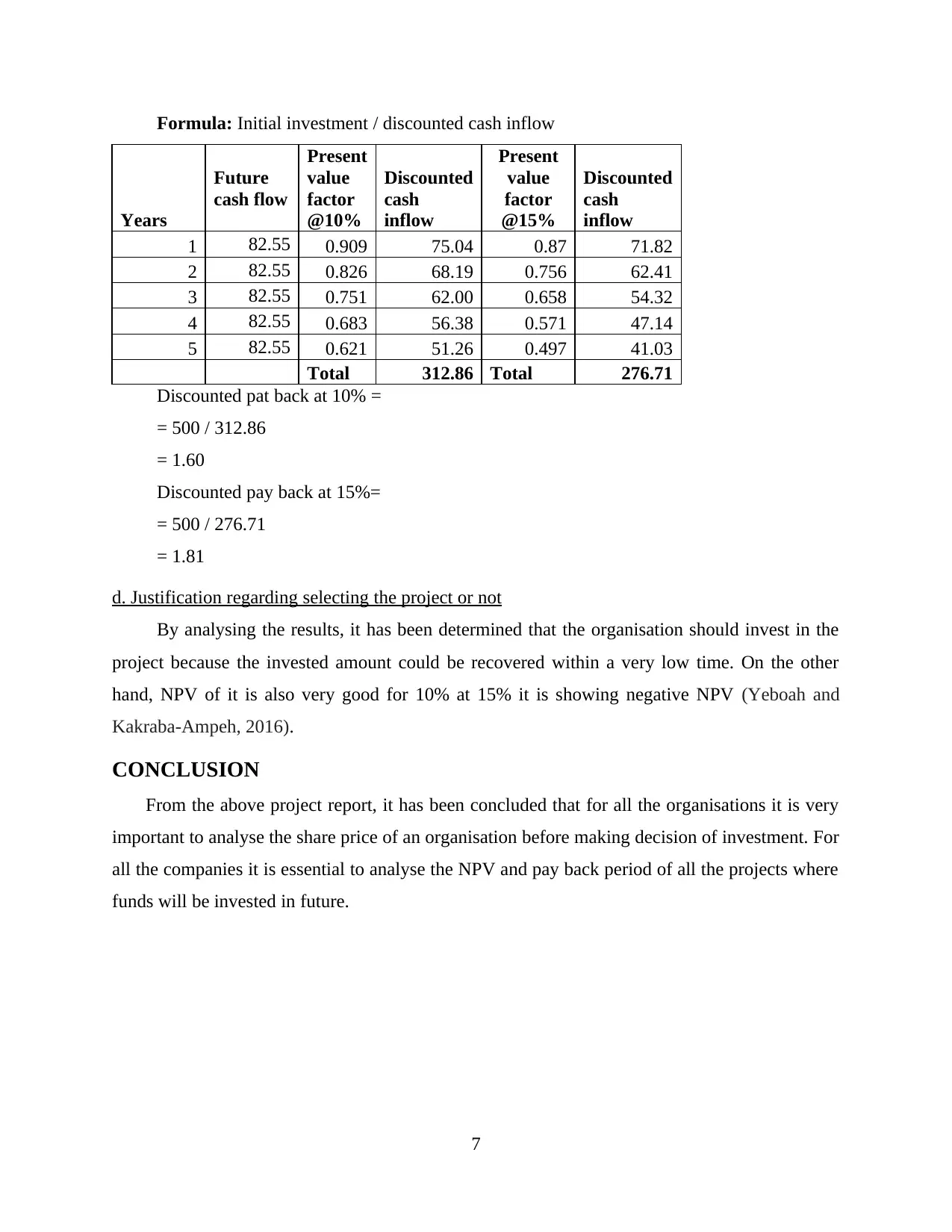

Formula: Initial investment / discounted cash inflow

Years

Future

cash flow

Present

value

factor

@10%

Discounted

cash

inflow

Present

value

factor

@15%

Discounted

cash

inflow

1 82.55 0.909 75.04 0.87 71.82

2 82.55 0.826 68.19 0.756 62.41

3 82.55 0.751 62.00 0.658 54.32

4 82.55 0.683 56.38 0.571 47.14

5 82.55 0.621 51.26 0.497 41.03

Total 312.86 Total 276.71

Discounted pat back at 10% =

= 500 / 312.86

= 1.60

Discounted pay back at 15%=

= 500 / 276.71

= 1.81

d. Justification regarding selecting the project or not

By analysing the results, it has been determined that the organisation should invest in the

project because the invested amount could be recovered within a very low time. On the other

hand, NPV of it is also very good for 10% at 15% it is showing negative NPV (Yeboah and

Kakraba-Ampeh, 2016).

CONCLUSION

From the above project report, it has been concluded that for all the organisations it is very

important to analyse the share price of an organisation before making decision of investment. For

all the companies it is essential to analyse the NPV and pay back period of all the projects where

funds will be invested in future.

7

Years

Future

cash flow

Present

value

factor

@10%

Discounted

cash

inflow

Present

value

factor

@15%

Discounted

cash

inflow

1 82.55 0.909 75.04 0.87 71.82

2 82.55 0.826 68.19 0.756 62.41

3 82.55 0.751 62.00 0.658 54.32

4 82.55 0.683 56.38 0.571 47.14

5 82.55 0.621 51.26 0.497 41.03

Total 312.86 Total 276.71

Discounted pat back at 10% =

= 500 / 312.86

= 1.60

Discounted pay back at 15%=

= 500 / 276.71

= 1.81

d. Justification regarding selecting the project or not

By analysing the results, it has been determined that the organisation should invest in the

project because the invested amount could be recovered within a very low time. On the other

hand, NPV of it is also very good for 10% at 15% it is showing negative NPV (Yeboah and

Kakraba-Ampeh, 2016).

CONCLUSION

From the above project report, it has been concluded that for all the organisations it is very

important to analyse the share price of an organisation before making decision of investment. For

all the companies it is essential to analyse the NPV and pay back period of all the projects where

funds will be invested in future.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Blackmore, L., 2017. El H elicoide and L a T orre de D avid as P hantom P avilions: R ethinking

S pectacles of P rogress in V enezuela. Bulletin of Latin American Research, 36(2),

pp.206-222.

Blackmore, R., 2019. The effects of commercial privileges in late medieval Bordeaux, 1348–

1449. French History.

Ducastel, A. and Anseeuw, W., 2018. 13 Large-scale land investments and financialisation of

agriculture. Ecology, Capitalism and the New Agricultural Economy: The Second Great

Transformation.

Kenfack, P. E., Nguiffo, S. and Nkuintchua, T., 2016. Land investments, accountability and the

law: Lessons from Cameroon. International Institute for Environment and

Development..

QUANSAH, J. D. G., SARPONG, M. and ASUMDA, D., 2018. Natural Resources Law II. 5th

May, 2018.

Sun, S. H., 2019. 01 Sydney Investor Forum 2019.

Yeboah, E. and Kakraba-Ampeh, M., 2016. Land investments, accountability and the law:

Lessons from Ghana. International Institute for Environmental and Development.

Online

Annual report of Blackmore. 2019. [Online]. Available through:

< https://www.blackmores.com.au/about-us/investor-centre/annual-and-half-year-

reports>

Blackmores Group Governance & Board of Directors. 2019. [Online]. Available through:

< https://www.blackmores.com.au/about-us/investor-centre/corporate-governance>

8

Books and Journals:

Blackmore, L., 2017. El H elicoide and L a T orre de D avid as P hantom P avilions: R ethinking

S pectacles of P rogress in V enezuela. Bulletin of Latin American Research, 36(2),

pp.206-222.

Blackmore, R., 2019. The effects of commercial privileges in late medieval Bordeaux, 1348–

1449. French History.

Ducastel, A. and Anseeuw, W., 2018. 13 Large-scale land investments and financialisation of

agriculture. Ecology, Capitalism and the New Agricultural Economy: The Second Great

Transformation.

Kenfack, P. E., Nguiffo, S. and Nkuintchua, T., 2016. Land investments, accountability and the

law: Lessons from Cameroon. International Institute for Environment and

Development..

QUANSAH, J. D. G., SARPONG, M. and ASUMDA, D., 2018. Natural Resources Law II. 5th

May, 2018.

Sun, S. H., 2019. 01 Sydney Investor Forum 2019.

Yeboah, E. and Kakraba-Ampeh, M., 2016. Land investments, accountability and the law:

Lessons from Ghana. International Institute for Environmental and Development.

Online

Annual report of Blackmore. 2019. [Online]. Available through:

< https://www.blackmores.com.au/about-us/investor-centre/annual-and-half-year-

reports>

Blackmores Group Governance & Board of Directors. 2019. [Online]. Available through:

< https://www.blackmores.com.au/about-us/investor-centre/corporate-governance>

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.