Financial Ratio Analysis of BMW Group: A Comprehensive Report

VerifiedAdded on 2023/01/18

|14

|3647

|100

Report

AI Summary

This report presents a financial analysis of the BMW Group, examining its performance through various financial ratios. It begins with an executive summary and an introduction to accounting and financial analysis, highlighting their importance in managing finances and developing business strategies. The main body of the report delves into the calculation and analysis of several key ratios, including liquidity ratios (quick and current ratios), profitability ratios (gross profit and operating profit ratios), efficiency ratios (average receivable turnover and average payable turnover ratios), and gearing ratios (debt and debt-to-equity ratios). Each ratio is calculated using financial data from BMW's annual reports for 2017 and 2018, with interpretations of the results and their implications for the company's financial health and operational efficiency. The analysis identifies trends, such as changes in profitability and debt levels, and offers insights into BMW's ability to manage its assets, liabilities, and overall financial risk. The report concludes with a summary of the findings and references used. This report is a student contribution to Desklib, a platform offering AI-based study tools.

Accounting and

finance analysis of

a listed company

finance analysis of

a listed company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report summarised that use of financial ratio in order to identify the liquidity,

profitability, efficacy or market value of the company. With the help of accounting or financial

analysis business able to collect or summarised the accounting information and further used for

the analysis which helps in developing future strategies in respect of the company.

This report summarised that use of financial ratio in order to identify the liquidity,

profitability, efficacy or market value of the company. With the help of accounting or financial

analysis business able to collect or summarised the accounting information and further used for

the analysis which helps in developing future strategies in respect of the company.

Table of Contents

EXECUTIVE SUMMARY ............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

EXECUTIVE SUMMARY ............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

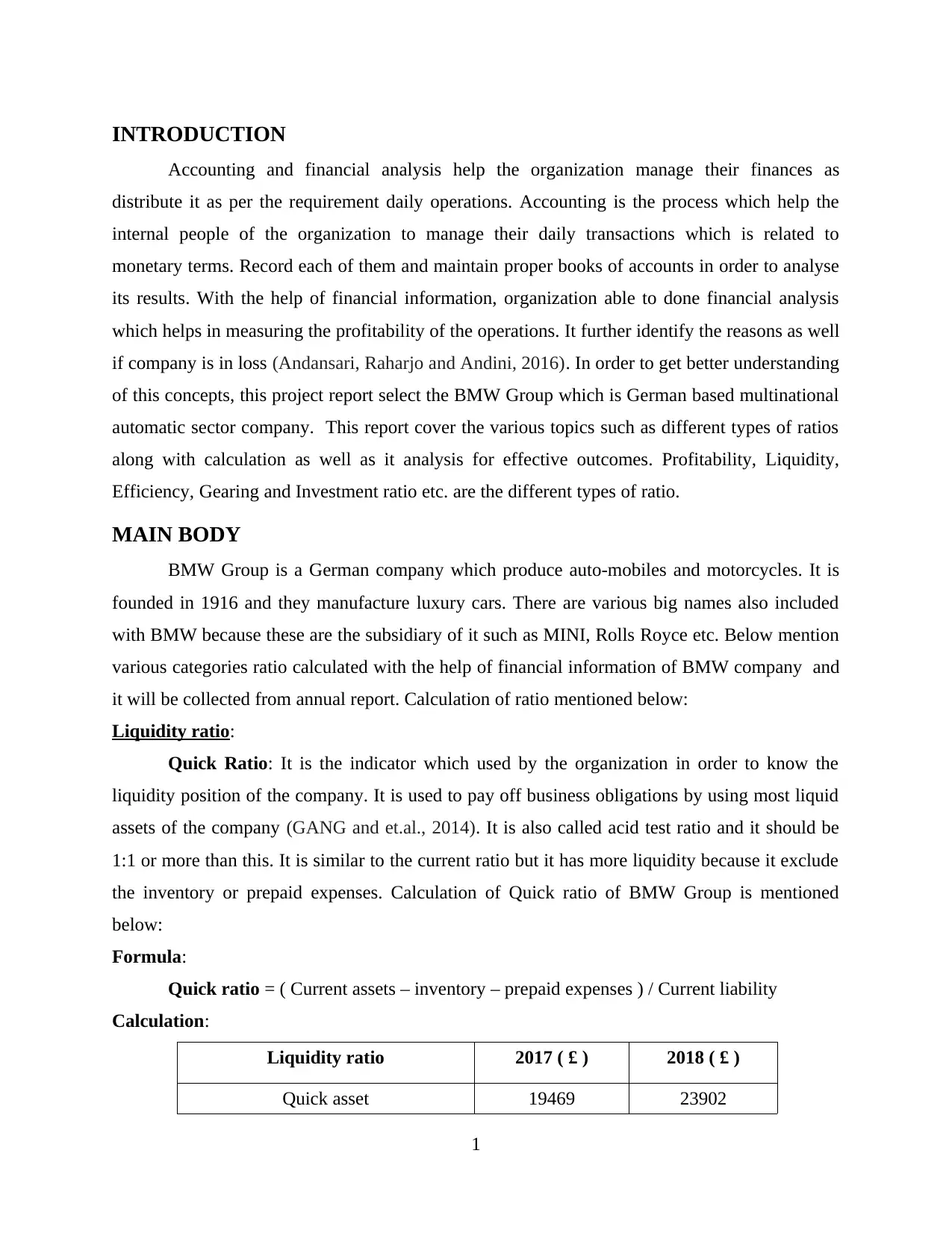

INTRODUCTION

Accounting and financial analysis help the organization manage their finances as

distribute it as per the requirement daily operations. Accounting is the process which help the

internal people of the organization to manage their daily transactions which is related to

monetary terms. Record each of them and maintain proper books of accounts in order to analyse

its results. With the help of financial information, organization able to done financial analysis

which helps in measuring the profitability of the operations. It further identify the reasons as well

if company is in loss (Andansari, Raharjo and Andini, 2016). In order to get better understanding

of this concepts, this project report select the BMW Group which is German based multinational

automatic sector company. This report cover the various topics such as different types of ratios

along with calculation as well as it analysis for effective outcomes. Profitability, Liquidity,

Efficiency, Gearing and Investment ratio etc. are the different types of ratio.

MAIN BODY

BMW Group is a German company which produce auto-mobiles and motorcycles. It is

founded in 1916 and they manufacture luxury cars. There are various big names also included

with BMW because these are the subsidiary of it such as MINI, Rolls Royce etc. Below mention

various categories ratio calculated with the help of financial information of BMW company and

it will be collected from annual report. Calculation of ratio mentioned below:

Liquidity ratio:

Quick Ratio: It is the indicator which used by the organization in order to know the

liquidity position of the company. It is used to pay off business obligations by using most liquid

assets of the company (GANG and et.al., 2014). It is also called acid test ratio and it should be

1:1 or more than this. It is similar to the current ratio but it has more liquidity because it exclude

the inventory or prepaid expenses. Calculation of Quick ratio of BMW Group is mentioned

below:

Formula:

Quick ratio = ( Current assets – inventory – prepaid expenses ) / Current liability

Calculation:

Liquidity ratio 2017 ( £ ) 2018 ( £ )

Quick asset 19469 23902

1

Accounting and financial analysis help the organization manage their finances as

distribute it as per the requirement daily operations. Accounting is the process which help the

internal people of the organization to manage their daily transactions which is related to

monetary terms. Record each of them and maintain proper books of accounts in order to analyse

its results. With the help of financial information, organization able to done financial analysis

which helps in measuring the profitability of the operations. It further identify the reasons as well

if company is in loss (Andansari, Raharjo and Andini, 2016). In order to get better understanding

of this concepts, this project report select the BMW Group which is German based multinational

automatic sector company. This report cover the various topics such as different types of ratios

along with calculation as well as it analysis for effective outcomes. Profitability, Liquidity,

Efficiency, Gearing and Investment ratio etc. are the different types of ratio.

MAIN BODY

BMW Group is a German company which produce auto-mobiles and motorcycles. It is

founded in 1916 and they manufacture luxury cars. There are various big names also included

with BMW because these are the subsidiary of it such as MINI, Rolls Royce etc. Below mention

various categories ratio calculated with the help of financial information of BMW company and

it will be collected from annual report. Calculation of ratio mentioned below:

Liquidity ratio:

Quick Ratio: It is the indicator which used by the organization in order to know the

liquidity position of the company. It is used to pay off business obligations by using most liquid

assets of the company (GANG and et.al., 2014). It is also called acid test ratio and it should be

1:1 or more than this. It is similar to the current ratio but it has more liquidity because it exclude

the inventory or prepaid expenses. Calculation of Quick ratio of BMW Group is mentioned

below:

Formula:

Quick ratio = ( Current assets – inventory – prepaid expenses ) / Current liability

Calculation:

Liquidity ratio 2017 ( £ ) 2018 ( £ )

Quick asset 19469 23902

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

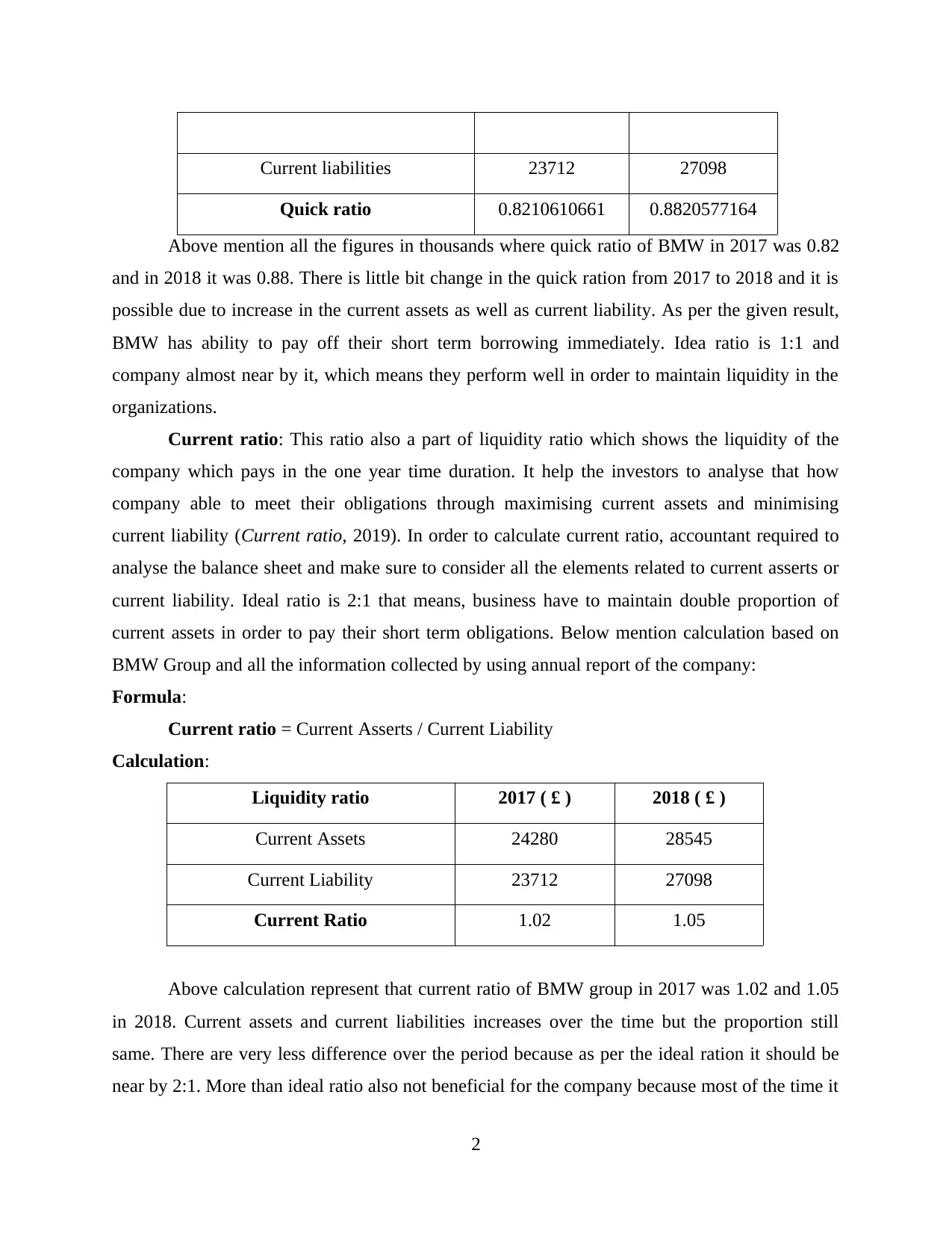

Current liabilities 23712 27098

Quick ratio 0.8210610661 0.8820577164

Above mention all the figures in thousands where quick ratio of BMW in 2017 was 0.82

and in 2018 it was 0.88. There is little bit change in the quick ration from 2017 to 2018 and it is

possible due to increase in the current assets as well as current liability. As per the given result,

BMW has ability to pay off their short term borrowing immediately. Idea ratio is 1:1 and

company almost near by it, which means they perform well in order to maintain liquidity in the

organizations.

Current ratio: This ratio also a part of liquidity ratio which shows the liquidity of the

company which pays in the one year time duration. It help the investors to analyse that how

company able to meet their obligations through maximising current assets and minimising

current liability (Current ratio, 2019). In order to calculate current ratio, accountant required to

analyse the balance sheet and make sure to consider all the elements related to current asserts or

current liability. Ideal ratio is 2:1 that means, business have to maintain double proportion of

current assets in order to pay their short term obligations. Below mention calculation based on

BMW Group and all the information collected by using annual report of the company:

Formula:

Current ratio = Current Asserts / Current Liability

Calculation:

Liquidity ratio 2017 ( £ ) 2018 ( £ )

Current Assets 24280 28545

Current Liability 23712 27098

Current Ratio 1.02 1.05

Above calculation represent that current ratio of BMW group in 2017 was 1.02 and 1.05

in 2018. Current assets and current liabilities increases over the time but the proportion still

same. There are very less difference over the period because as per the ideal ration it should be

near by 2:1. More than ideal ratio also not beneficial for the company because most of the time it

2

Quick ratio 0.8210610661 0.8820577164

Above mention all the figures in thousands where quick ratio of BMW in 2017 was 0.82

and in 2018 it was 0.88. There is little bit change in the quick ration from 2017 to 2018 and it is

possible due to increase in the current assets as well as current liability. As per the given result,

BMW has ability to pay off their short term borrowing immediately. Idea ratio is 1:1 and

company almost near by it, which means they perform well in order to maintain liquidity in the

organizations.

Current ratio: This ratio also a part of liquidity ratio which shows the liquidity of the

company which pays in the one year time duration. It help the investors to analyse that how

company able to meet their obligations through maximising current assets and minimising

current liability (Current ratio, 2019). In order to calculate current ratio, accountant required to

analyse the balance sheet and make sure to consider all the elements related to current asserts or

current liability. Ideal ratio is 2:1 that means, business have to maintain double proportion of

current assets in order to pay their short term obligations. Below mention calculation based on

BMW Group and all the information collected by using annual report of the company:

Formula:

Current ratio = Current Asserts / Current Liability

Calculation:

Liquidity ratio 2017 ( £ ) 2018 ( £ )

Current Assets 24280 28545

Current Liability 23712 27098

Current Ratio 1.02 1.05

Above calculation represent that current ratio of BMW group in 2017 was 1.02 and 1.05

in 2018. Current assets and current liabilities increases over the time but the proportion still

same. There are very less difference over the period because as per the ideal ration it should be

near by 2:1. More than ideal ratio also not beneficial for the company because most of the time it

2

happen that business stored huge amount of inventory which is not easy to converting into cash.

BMW should focus on increasing their current assets in comparison to current liability.

Profitability ratio:

Gross profit ratio: It is the profitability ratio which indicate that how much gross profit

business earn from the sales of their goods. It shows the relationship between net sales and gross

profit, it is most popular tool which used to evaluate the operational performance. It is calculated

by dividing gross profit by net sales (Ichsani and Suhardi, 2015). Higher the ratio indicate that

business make reasonable profit through selling enough products. Below mention calculation

based on BMW Group which help the management to analyse their financial ability and what

improvement they required to improve their figures.

Formula:

Gross profit ratio = ( Gross profit / Net Sales ) * 100

Calculation:

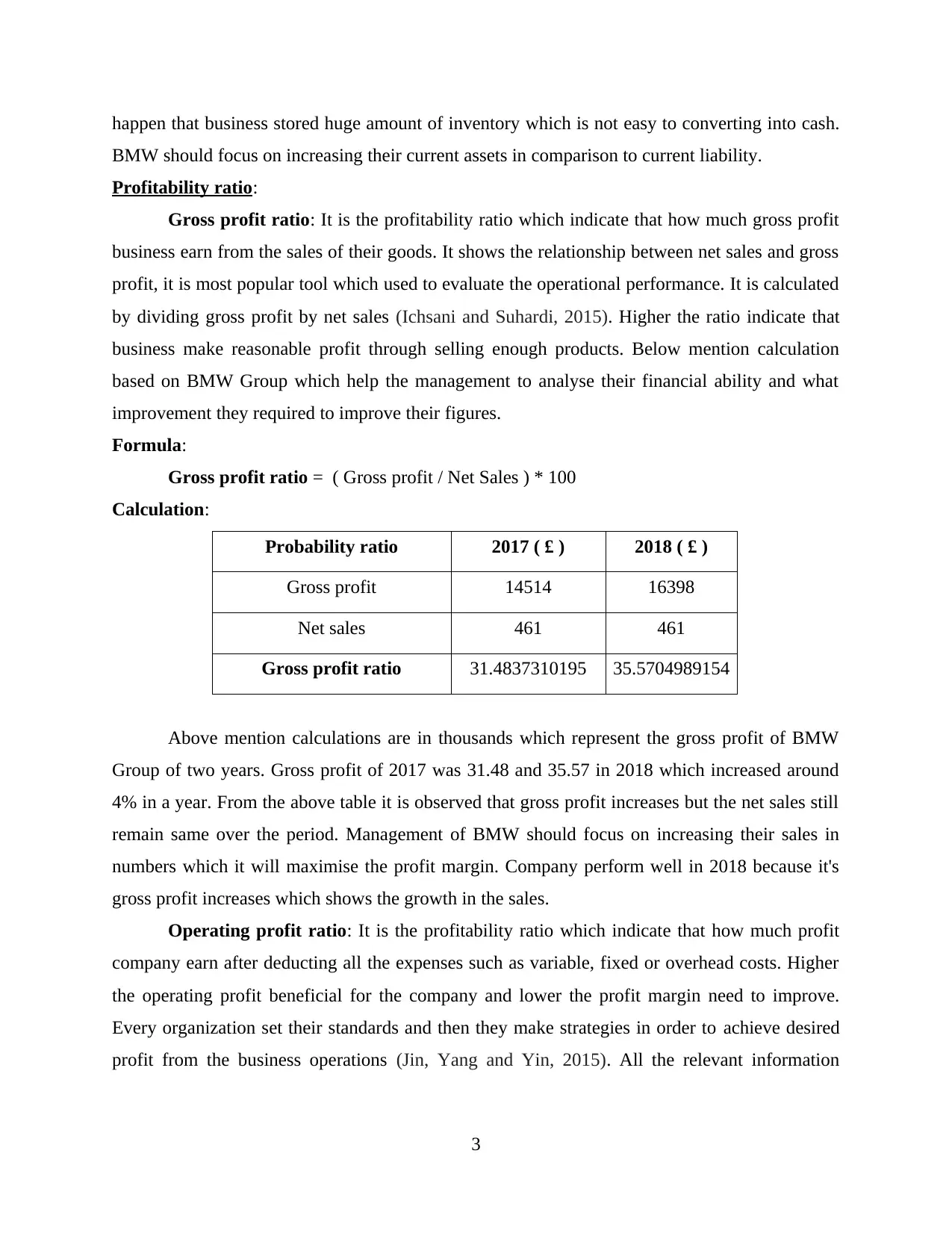

Probability ratio 2017 ( £ ) 2018 ( £ )

Gross profit 14514 16398

Net sales 461 461

Gross profit ratio 31.4837310195 35.5704989154

Above mention calculations are in thousands which represent the gross profit of BMW

Group of two years. Gross profit of 2017 was 31.48 and 35.57 in 2018 which increased around

4% in a year. From the above table it is observed that gross profit increases but the net sales still

remain same over the period. Management of BMW should focus on increasing their sales in

numbers which it will maximise the profit margin. Company perform well in 2018 because it's

gross profit increases which shows the growth in the sales.

Operating profit ratio: It is the profitability ratio which indicate that how much profit

company earn after deducting all the expenses such as variable, fixed or overhead costs. Higher

the operating profit beneficial for the company and lower the profit margin need to improve.

Every organization set their standards and then they make strategies in order to achieve desired

profit from the business operations (Jin, Yang and Yin, 2015). All the relevant information

3

BMW should focus on increasing their current assets in comparison to current liability.

Profitability ratio:

Gross profit ratio: It is the profitability ratio which indicate that how much gross profit

business earn from the sales of their goods. It shows the relationship between net sales and gross

profit, it is most popular tool which used to evaluate the operational performance. It is calculated

by dividing gross profit by net sales (Ichsani and Suhardi, 2015). Higher the ratio indicate that

business make reasonable profit through selling enough products. Below mention calculation

based on BMW Group which help the management to analyse their financial ability and what

improvement they required to improve their figures.

Formula:

Gross profit ratio = ( Gross profit / Net Sales ) * 100

Calculation:

Probability ratio 2017 ( £ ) 2018 ( £ )

Gross profit 14514 16398

Net sales 461 461

Gross profit ratio 31.4837310195 35.5704989154

Above mention calculations are in thousands which represent the gross profit of BMW

Group of two years. Gross profit of 2017 was 31.48 and 35.57 in 2018 which increased around

4% in a year. From the above table it is observed that gross profit increases but the net sales still

remain same over the period. Management of BMW should focus on increasing their sales in

numbers which it will maximise the profit margin. Company perform well in 2018 because it's

gross profit increases which shows the growth in the sales.

Operating profit ratio: It is the profitability ratio which indicate that how much profit

company earn after deducting all the expenses such as variable, fixed or overhead costs. Higher

the operating profit beneficial for the company and lower the profit margin need to improve.

Every organization set their standards and then they make strategies in order to achieve desired

profit from the business operations (Jin, Yang and Yin, 2015). All the relevant information

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

available in the income statement of the organization. In context on BMW, by using financial

information operating profit will be calculated.

Formula:

Operating profit ratio = (Operating profit / Net sales) * 100

Calculation:

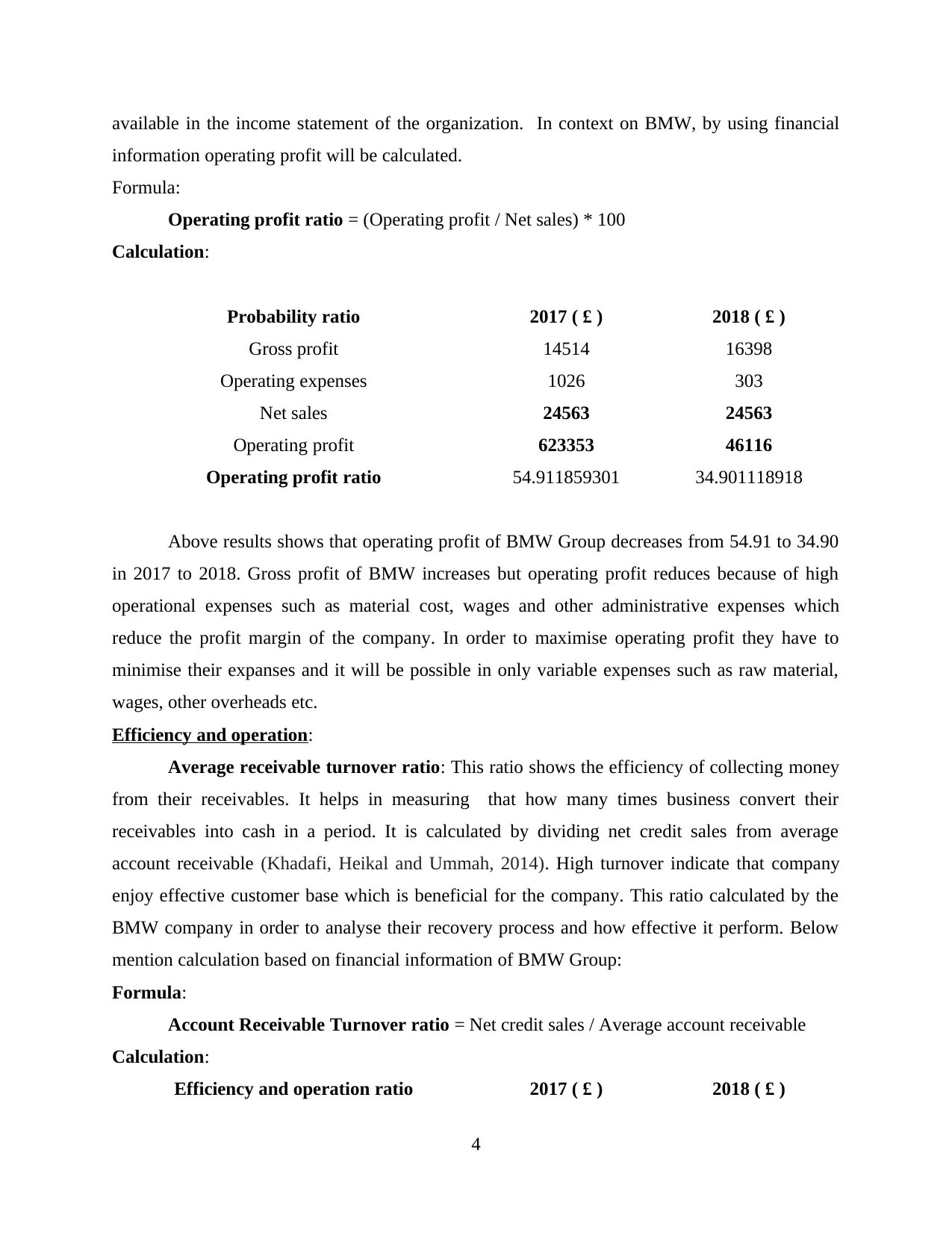

Probability ratio 2017 ( £ ) 2018 ( £ )

Gross profit 14514 16398

Operating expenses 1026 303

Net sales 24563 24563

Operating profit 623353 46116

Operating profit ratio 54.911859301 34.901118918

Above results shows that operating profit of BMW Group decreases from 54.91 to 34.90

in 2017 to 2018. Gross profit of BMW increases but operating profit reduces because of high

operational expenses such as material cost, wages and other administrative expenses which

reduce the profit margin of the company. In order to maximise operating profit they have to

minimise their expanses and it will be possible in only variable expenses such as raw material,

wages, other overheads etc.

Efficiency and operation:

Average receivable turnover ratio: This ratio shows the efficiency of collecting money

from their receivables. It helps in measuring that how many times business convert their

receivables into cash in a period. It is calculated by dividing net credit sales from average

account receivable (Khadafi, Heikal and Ummah, 2014). High turnover indicate that company

enjoy effective customer base which is beneficial for the company. This ratio calculated by the

BMW company in order to analyse their recovery process and how effective it perform. Below

mention calculation based on financial information of BMW Group:

Formula:

Account Receivable Turnover ratio = Net credit sales / Average account receivable

Calculation:

Efficiency and operation ratio 2017 ( £ ) 2018 ( £ )

4

information operating profit will be calculated.

Formula:

Operating profit ratio = (Operating profit / Net sales) * 100

Calculation:

Probability ratio 2017 ( £ ) 2018 ( £ )

Gross profit 14514 16398

Operating expenses 1026 303

Net sales 24563 24563

Operating profit 623353 46116

Operating profit ratio 54.911859301 34.901118918

Above results shows that operating profit of BMW Group decreases from 54.91 to 34.90

in 2017 to 2018. Gross profit of BMW increases but operating profit reduces because of high

operational expenses such as material cost, wages and other administrative expenses which

reduce the profit margin of the company. In order to maximise operating profit they have to

minimise their expanses and it will be possible in only variable expenses such as raw material,

wages, other overheads etc.

Efficiency and operation:

Average receivable turnover ratio: This ratio shows the efficiency of collecting money

from their receivables. It helps in measuring that how many times business convert their

receivables into cash in a period. It is calculated by dividing net credit sales from average

account receivable (Khadafi, Heikal and Ummah, 2014). High turnover indicate that company

enjoy effective customer base which is beneficial for the company. This ratio calculated by the

BMW company in order to analyse their recovery process and how effective it perform. Below

mention calculation based on financial information of BMW Group:

Formula:

Account Receivable Turnover ratio = Net credit sales / Average account receivable

Calculation:

Efficiency and operation ratio 2017 ( £ ) 2018 ( £ )

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

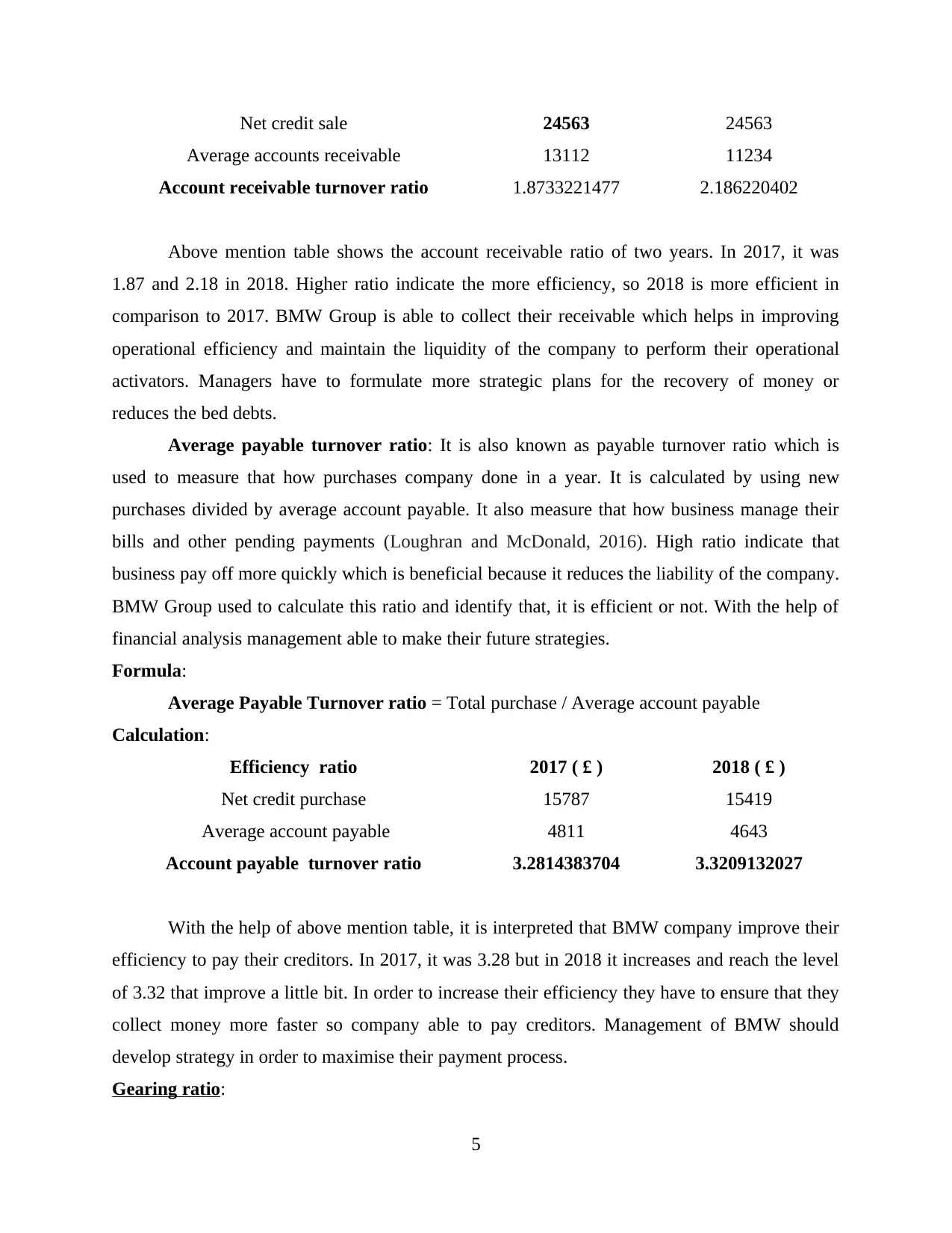

Net credit sale 24563 24563

Average accounts receivable 13112 11234

Account receivable turnover ratio 1.8733221477 2.186220402

Above mention table shows the account receivable ratio of two years. In 2017, it was

1.87 and 2.18 in 2018. Higher ratio indicate the more efficiency, so 2018 is more efficient in

comparison to 2017. BMW Group is able to collect their receivable which helps in improving

operational efficiency and maintain the liquidity of the company to perform their operational

activators. Managers have to formulate more strategic plans for the recovery of money or

reduces the bed debts.

Average payable turnover ratio: It is also known as payable turnover ratio which is

used to measure that how purchases company done in a year. It is calculated by using new

purchases divided by average account payable. It also measure that how business manage their

bills and other pending payments (Loughran and McDonald, 2016). High ratio indicate that

business pay off more quickly which is beneficial because it reduces the liability of the company.

BMW Group used to calculate this ratio and identify that, it is efficient or not. With the help of

financial analysis management able to make their future strategies.

Formula:

Average Payable Turnover ratio = Total purchase / Average account payable

Calculation:

Efficiency ratio 2017 ( £ ) 2018 ( £ )

Net credit purchase 15787 15419

Average account payable 4811 4643

Account payable turnover ratio 3.2814383704 3.3209132027

With the help of above mention table, it is interpreted that BMW company improve their

efficiency to pay their creditors. In 2017, it was 3.28 but in 2018 it increases and reach the level

of 3.32 that improve a little bit. In order to increase their efficiency they have to ensure that they

collect money more faster so company able to pay creditors. Management of BMW should

develop strategy in order to maximise their payment process.

Gearing ratio:

5

Average accounts receivable 13112 11234

Account receivable turnover ratio 1.8733221477 2.186220402

Above mention table shows the account receivable ratio of two years. In 2017, it was

1.87 and 2.18 in 2018. Higher ratio indicate the more efficiency, so 2018 is more efficient in

comparison to 2017. BMW Group is able to collect their receivable which helps in improving

operational efficiency and maintain the liquidity of the company to perform their operational

activators. Managers have to formulate more strategic plans for the recovery of money or

reduces the bed debts.

Average payable turnover ratio: It is also known as payable turnover ratio which is

used to measure that how purchases company done in a year. It is calculated by using new

purchases divided by average account payable. It also measure that how business manage their

bills and other pending payments (Loughran and McDonald, 2016). High ratio indicate that

business pay off more quickly which is beneficial because it reduces the liability of the company.

BMW Group used to calculate this ratio and identify that, it is efficient or not. With the help of

financial analysis management able to make their future strategies.

Formula:

Average Payable Turnover ratio = Total purchase / Average account payable

Calculation:

Efficiency ratio 2017 ( £ ) 2018 ( £ )

Net credit purchase 15787 15419

Average account payable 4811 4643

Account payable turnover ratio 3.2814383704 3.3209132027

With the help of above mention table, it is interpreted that BMW company improve their

efficiency to pay their creditors. In 2017, it was 3.28 but in 2018 it increases and reach the level

of 3.32 that improve a little bit. In order to increase their efficiency they have to ensure that they

collect money more faster so company able to pay creditors. Management of BMW should

develop strategy in order to maximise their payment process.

Gearing ratio:

5

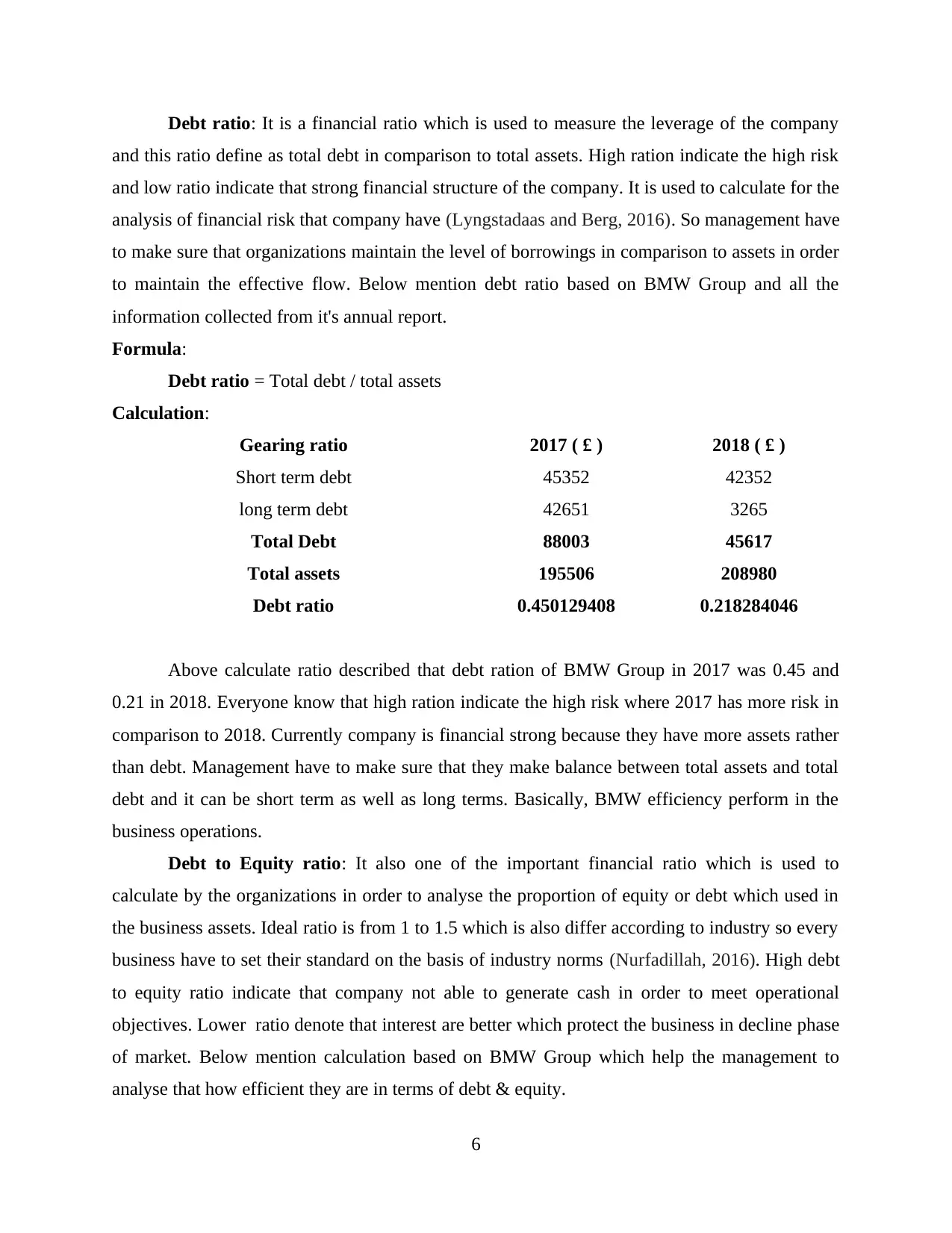

Debt ratio: It is a financial ratio which is used to measure the leverage of the company

and this ratio define as total debt in comparison to total assets. High ration indicate the high risk

and low ratio indicate that strong financial structure of the company. It is used to calculate for the

analysis of financial risk that company have (Lyngstadaas and Berg, 2016). So management have

to make sure that organizations maintain the level of borrowings in comparison to assets in order

to maintain the effective flow. Below mention debt ratio based on BMW Group and all the

information collected from it's annual report.

Formula:

Debt ratio = Total debt / total assets

Calculation:

Gearing ratio 2017 ( £ ) 2018 ( £ )

Short term debt 45352 42352

long term debt 42651 3265

Total Debt 88003 45617

Total assets 195506 208980

Debt ratio 0.450129408 0.218284046

Above calculate ratio described that debt ration of BMW Group in 2017 was 0.45 and

0.21 in 2018. Everyone know that high ration indicate the high risk where 2017 has more risk in

comparison to 2018. Currently company is financial strong because they have more assets rather

than debt. Management have to make sure that they make balance between total assets and total

debt and it can be short term as well as long terms. Basically, BMW efficiency perform in the

business operations.

Debt to Equity ratio: It also one of the important financial ratio which is used to

calculate by the organizations in order to analyse the proportion of equity or debt which used in

the business assets. Ideal ratio is from 1 to 1.5 which is also differ according to industry so every

business have to set their standard on the basis of industry norms (Nurfadillah, 2016). High debt

to equity ratio indicate that company not able to generate cash in order to meet operational

objectives. Lower ratio denote that interest are better which protect the business in decline phase

of market. Below mention calculation based on BMW Group which help the management to

analyse that how efficient they are in terms of debt & equity.

6

and this ratio define as total debt in comparison to total assets. High ration indicate the high risk

and low ratio indicate that strong financial structure of the company. It is used to calculate for the

analysis of financial risk that company have (Lyngstadaas and Berg, 2016). So management have

to make sure that organizations maintain the level of borrowings in comparison to assets in order

to maintain the effective flow. Below mention debt ratio based on BMW Group and all the

information collected from it's annual report.

Formula:

Debt ratio = Total debt / total assets

Calculation:

Gearing ratio 2017 ( £ ) 2018 ( £ )

Short term debt 45352 42352

long term debt 42651 3265

Total Debt 88003 45617

Total assets 195506 208980

Debt ratio 0.450129408 0.218284046

Above calculate ratio described that debt ration of BMW Group in 2017 was 0.45 and

0.21 in 2018. Everyone know that high ration indicate the high risk where 2017 has more risk in

comparison to 2018. Currently company is financial strong because they have more assets rather

than debt. Management have to make sure that they make balance between total assets and total

debt and it can be short term as well as long terms. Basically, BMW efficiency perform in the

business operations.

Debt to Equity ratio: It also one of the important financial ratio which is used to

calculate by the organizations in order to analyse the proportion of equity or debt which used in

the business assets. Ideal ratio is from 1 to 1.5 which is also differ according to industry so every

business have to set their standard on the basis of industry norms (Nurfadillah, 2016). High debt

to equity ratio indicate that company not able to generate cash in order to meet operational

objectives. Lower ratio denote that interest are better which protect the business in decline phase

of market. Below mention calculation based on BMW Group which help the management to

analyse that how efficient they are in terms of debt & equity.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

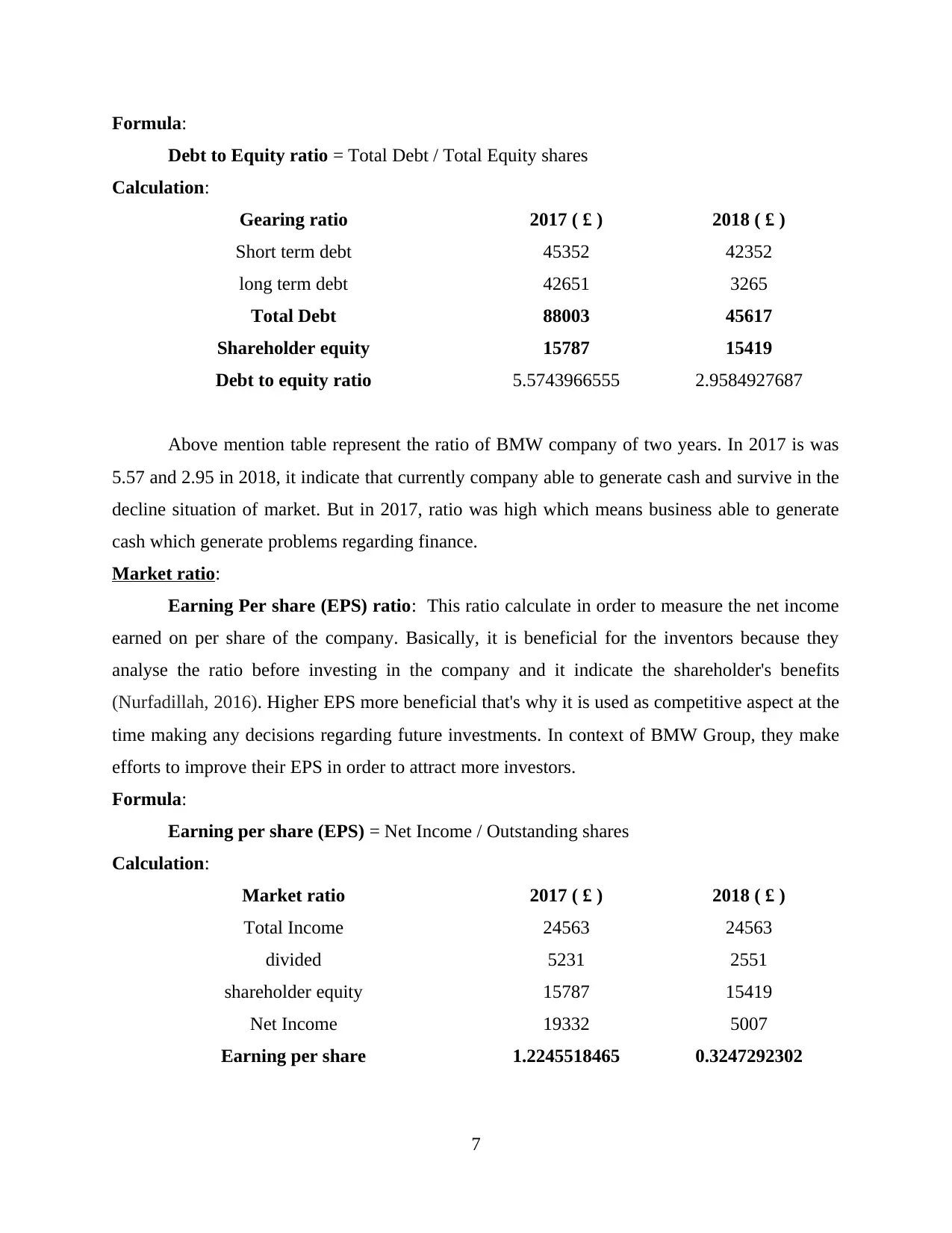

Formula:

Debt to Equity ratio = Total Debt / Total Equity shares

Calculation:

Gearing ratio 2017 ( £ ) 2018 ( £ )

Short term debt 45352 42352

long term debt 42651 3265

Total Debt 88003 45617

Shareholder equity 15787 15419

Debt to equity ratio 5.5743966555 2.9584927687

Above mention table represent the ratio of BMW company of two years. In 2017 is was

5.57 and 2.95 in 2018, it indicate that currently company able to generate cash and survive in the

decline situation of market. But in 2017, ratio was high which means business able to generate

cash which generate problems regarding finance.

Market ratio:

Earning Per share (EPS) ratio: This ratio calculate in order to measure the net income

earned on per share of the company. Basically, it is beneficial for the inventors because they

analyse the ratio before investing in the company and it indicate the shareholder's benefits

(Nurfadillah, 2016). Higher EPS more beneficial that's why it is used as competitive aspect at the

time making any decisions regarding future investments. In context of BMW Group, they make

efforts to improve their EPS in order to attract more investors.

Formula:

Earning per share (EPS) = Net Income / Outstanding shares

Calculation:

Market ratio 2017 ( £ ) 2018 ( £ )

Total Income 24563 24563

divided 5231 2551

shareholder equity 15787 15419

Net Income 19332 5007

Earning per share 1.2245518465 0.3247292302

7

Debt to Equity ratio = Total Debt / Total Equity shares

Calculation:

Gearing ratio 2017 ( £ ) 2018 ( £ )

Short term debt 45352 42352

long term debt 42651 3265

Total Debt 88003 45617

Shareholder equity 15787 15419

Debt to equity ratio 5.5743966555 2.9584927687

Above mention table represent the ratio of BMW company of two years. In 2017 is was

5.57 and 2.95 in 2018, it indicate that currently company able to generate cash and survive in the

decline situation of market. But in 2017, ratio was high which means business able to generate

cash which generate problems regarding finance.

Market ratio:

Earning Per share (EPS) ratio: This ratio calculate in order to measure the net income

earned on per share of the company. Basically, it is beneficial for the inventors because they

analyse the ratio before investing in the company and it indicate the shareholder's benefits

(Nurfadillah, 2016). Higher EPS more beneficial that's why it is used as competitive aspect at the

time making any decisions regarding future investments. In context of BMW Group, they make

efforts to improve their EPS in order to attract more investors.

Formula:

Earning per share (EPS) = Net Income / Outstanding shares

Calculation:

Market ratio 2017 ( £ ) 2018 ( £ )

Total Income 24563 24563

divided 5231 2551

shareholder equity 15787 15419

Net Income 19332 5007

Earning per share 1.2245518465 0.3247292302

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

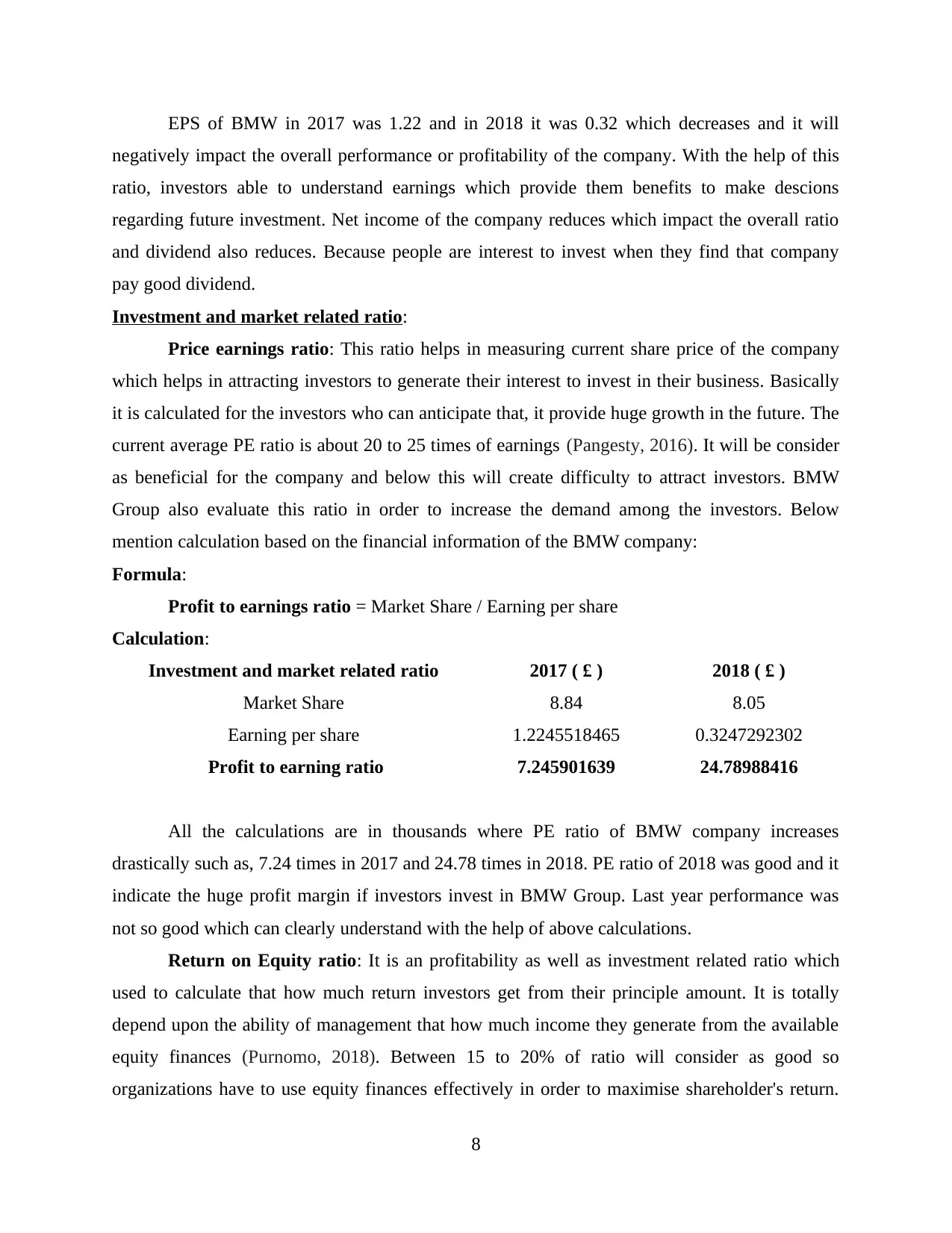

EPS of BMW in 2017 was 1.22 and in 2018 it was 0.32 which decreases and it will

negatively impact the overall performance or profitability of the company. With the help of this

ratio, investors able to understand earnings which provide them benefits to make descions

regarding future investment. Net income of the company reduces which impact the overall ratio

and dividend also reduces. Because people are interest to invest when they find that company

pay good dividend.

Investment and market related ratio:

Price earnings ratio: This ratio helps in measuring current share price of the company

which helps in attracting investors to generate their interest to invest in their business. Basically

it is calculated for the investors who can anticipate that, it provide huge growth in the future. The

current average PE ratio is about 20 to 25 times of earnings (Pangesty, 2016). It will be consider

as beneficial for the company and below this will create difficulty to attract investors. BMW

Group also evaluate this ratio in order to increase the demand among the investors. Below

mention calculation based on the financial information of the BMW company:

Formula:

Profit to earnings ratio = Market Share / Earning per share

Calculation:

Investment and market related ratio 2017 ( £ ) 2018 ( £ )

Market Share 8.84 8.05

Earning per share 1.2245518465 0.3247292302

Profit to earning ratio 7.245901639 24.78988416

All the calculations are in thousands where PE ratio of BMW company increases

drastically such as, 7.24 times in 2017 and 24.78 times in 2018. PE ratio of 2018 was good and it

indicate the huge profit margin if investors invest in BMW Group. Last year performance was

not so good which can clearly understand with the help of above calculations.

Return on Equity ratio: It is an profitability as well as investment related ratio which

used to calculate that how much return investors get from their principle amount. It is totally

depend upon the ability of management that how much income they generate from the available

equity finances (Purnomo, 2018). Between 15 to 20% of ratio will consider as good so

organizations have to use equity finances effectively in order to maximise shareholder's return.

8

negatively impact the overall performance or profitability of the company. With the help of this

ratio, investors able to understand earnings which provide them benefits to make descions

regarding future investment. Net income of the company reduces which impact the overall ratio

and dividend also reduces. Because people are interest to invest when they find that company

pay good dividend.

Investment and market related ratio:

Price earnings ratio: This ratio helps in measuring current share price of the company

which helps in attracting investors to generate their interest to invest in their business. Basically

it is calculated for the investors who can anticipate that, it provide huge growth in the future. The

current average PE ratio is about 20 to 25 times of earnings (Pangesty, 2016). It will be consider

as beneficial for the company and below this will create difficulty to attract investors. BMW

Group also evaluate this ratio in order to increase the demand among the investors. Below

mention calculation based on the financial information of the BMW company:

Formula:

Profit to earnings ratio = Market Share / Earning per share

Calculation:

Investment and market related ratio 2017 ( £ ) 2018 ( £ )

Market Share 8.84 8.05

Earning per share 1.2245518465 0.3247292302

Profit to earning ratio 7.245901639 24.78988416

All the calculations are in thousands where PE ratio of BMW company increases

drastically such as, 7.24 times in 2017 and 24.78 times in 2018. PE ratio of 2018 was good and it

indicate the huge profit margin if investors invest in BMW Group. Last year performance was

not so good which can clearly understand with the help of above calculations.

Return on Equity ratio: It is an profitability as well as investment related ratio which

used to calculate that how much return investors get from their principle amount. It is totally

depend upon the ability of management that how much income they generate from the available

equity finances (Purnomo, 2018). Between 15 to 20% of ratio will consider as good so

organizations have to use equity finances effectively in order to maximise shareholder's return.

8

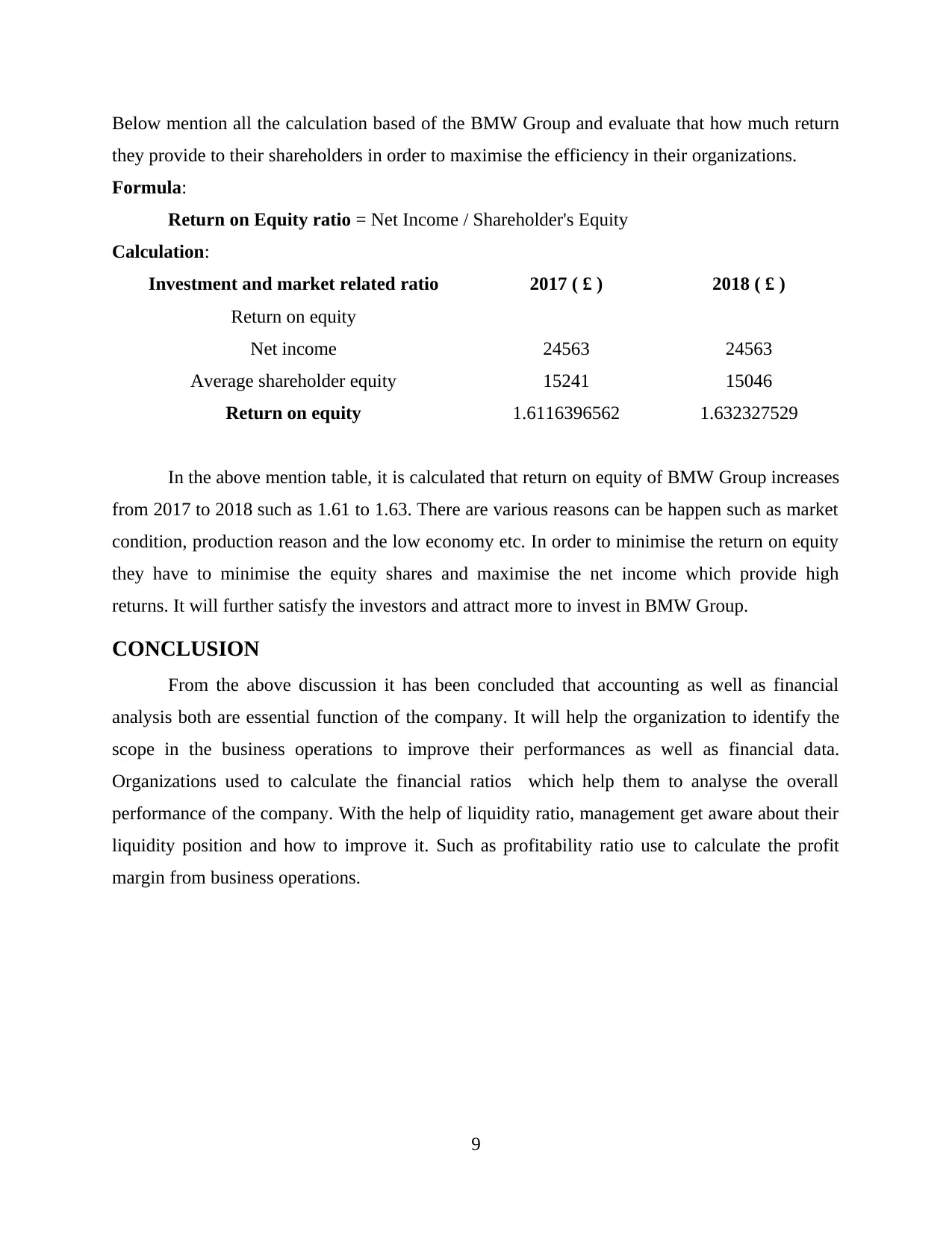

Below mention all the calculation based of the BMW Group and evaluate that how much return

they provide to their shareholders in order to maximise the efficiency in their organizations.

Formula:

Return on Equity ratio = Net Income / Shareholder's Equity

Calculation:

Investment and market related ratio 2017 ( £ ) 2018 ( £ )

Return on equity

Net income 24563 24563

Average shareholder equity 15241 15046

Return on equity 1.6116396562 1.632327529

In the above mention table, it is calculated that return on equity of BMW Group increases

from 2017 to 2018 such as 1.61 to 1.63. There are various reasons can be happen such as market

condition, production reason and the low economy etc. In order to minimise the return on equity

they have to minimise the equity shares and maximise the net income which provide high

returns. It will further satisfy the investors and attract more to invest in BMW Group.

CONCLUSION

From the above discussion it has been concluded that accounting as well as financial

analysis both are essential function of the company. It will help the organization to identify the

scope in the business operations to improve their performances as well as financial data.

Organizations used to calculate the financial ratios which help them to analyse the overall

performance of the company. With the help of liquidity ratio, management get aware about their

liquidity position and how to improve it. Such as profitability ratio use to calculate the profit

margin from business operations.

9

they provide to their shareholders in order to maximise the efficiency in their organizations.

Formula:

Return on Equity ratio = Net Income / Shareholder's Equity

Calculation:

Investment and market related ratio 2017 ( £ ) 2018 ( £ )

Return on equity

Net income 24563 24563

Average shareholder equity 15241 15046

Return on equity 1.6116396562 1.632327529

In the above mention table, it is calculated that return on equity of BMW Group increases

from 2017 to 2018 such as 1.61 to 1.63. There are various reasons can be happen such as market

condition, production reason and the low economy etc. In order to minimise the return on equity

they have to minimise the equity shares and maximise the net income which provide high

returns. It will further satisfy the investors and attract more to invest in BMW Group.

CONCLUSION

From the above discussion it has been concluded that accounting as well as financial

analysis both are essential function of the company. It will help the organization to identify the

scope in the business operations to improve their performances as well as financial data.

Organizations used to calculate the financial ratios which help them to analyse the overall

performance of the company. With the help of liquidity ratio, management get aware about their

liquidity position and how to improve it. Such as profitability ratio use to calculate the profit

margin from business operations.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.