Financial Analysis Report: Bombardier's Taxation, Compliance, and Risk

VerifiedAdded on 2023/04/07

|23

|827

|256

Report

AI Summary

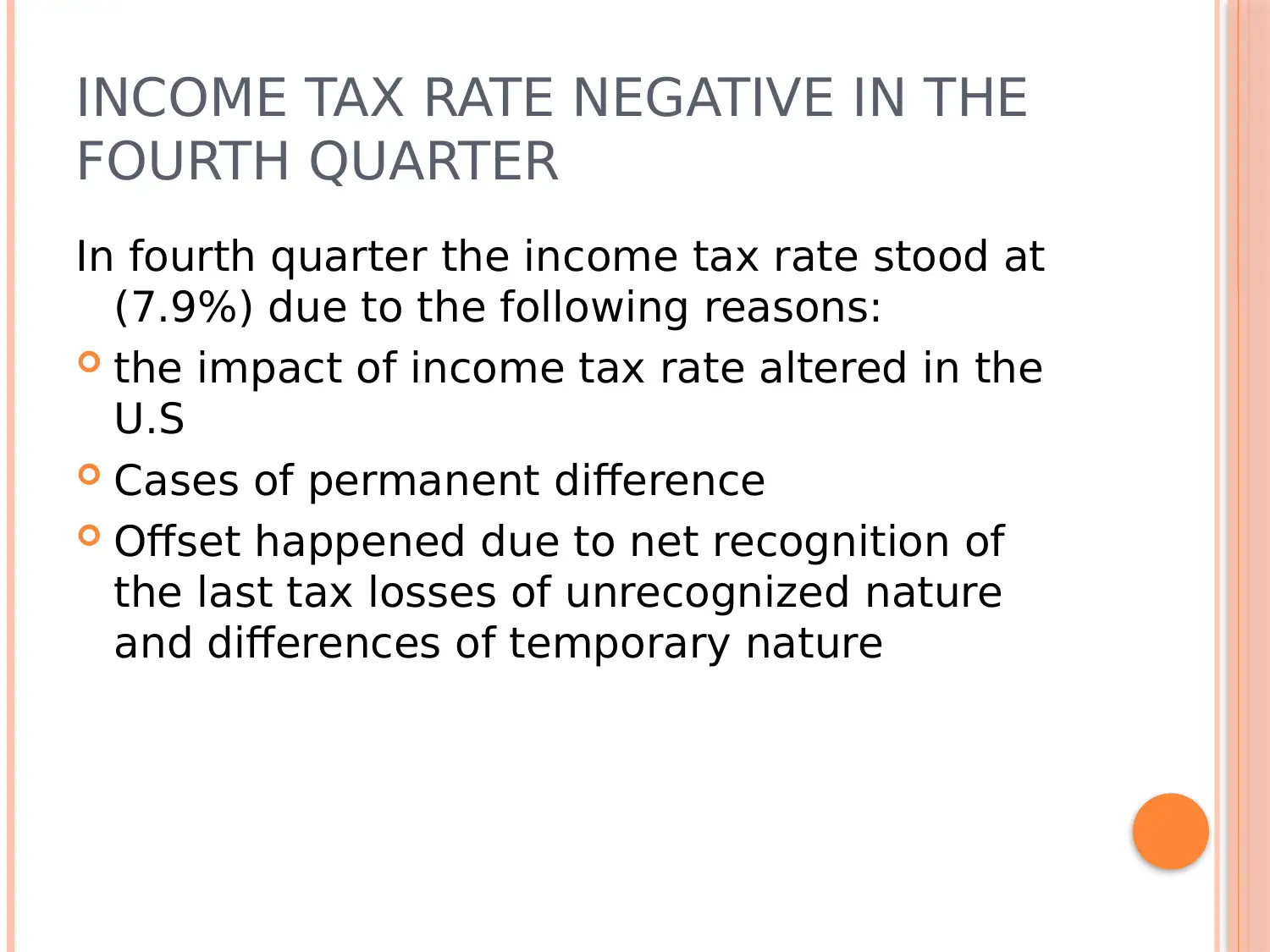

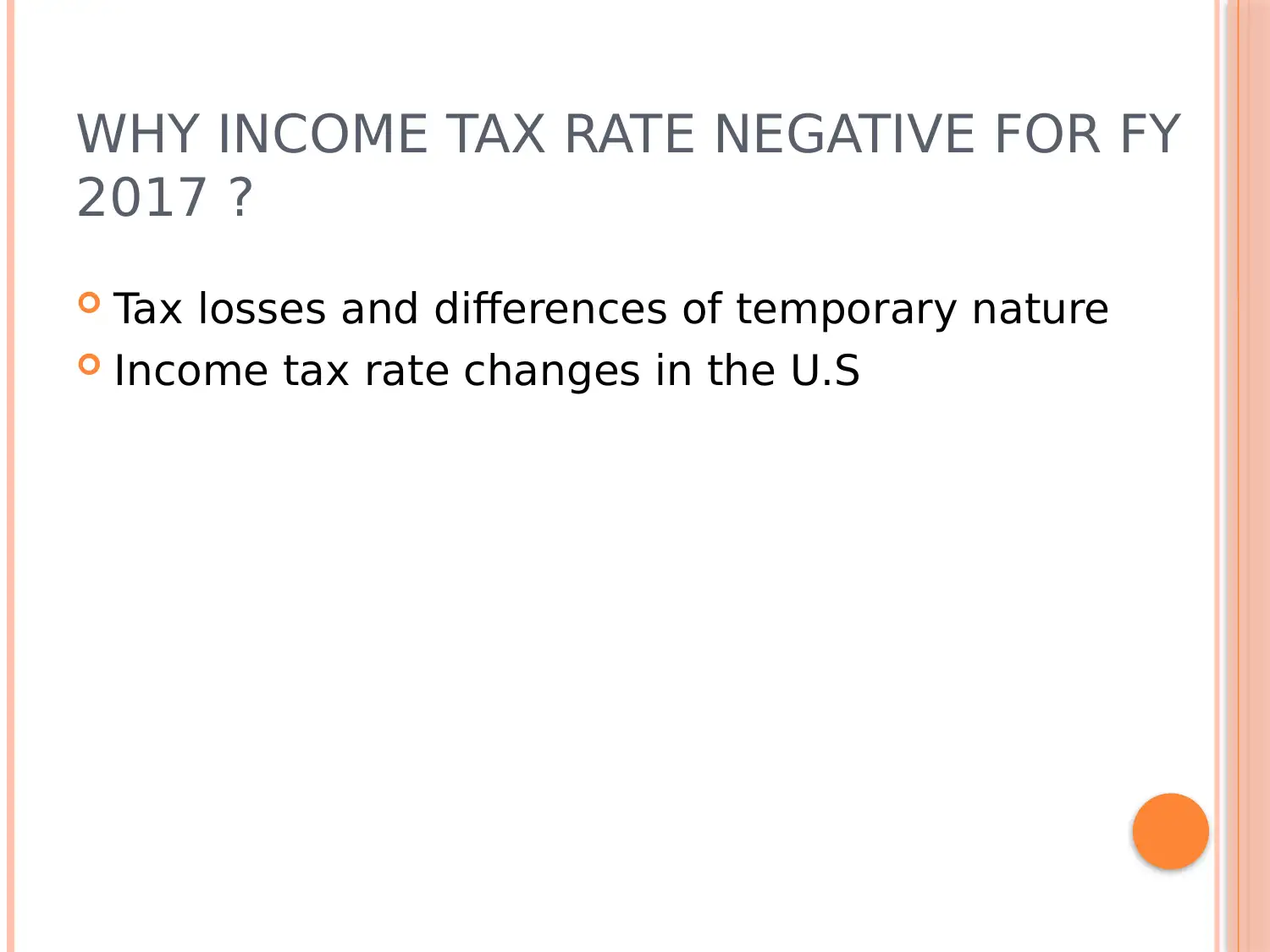

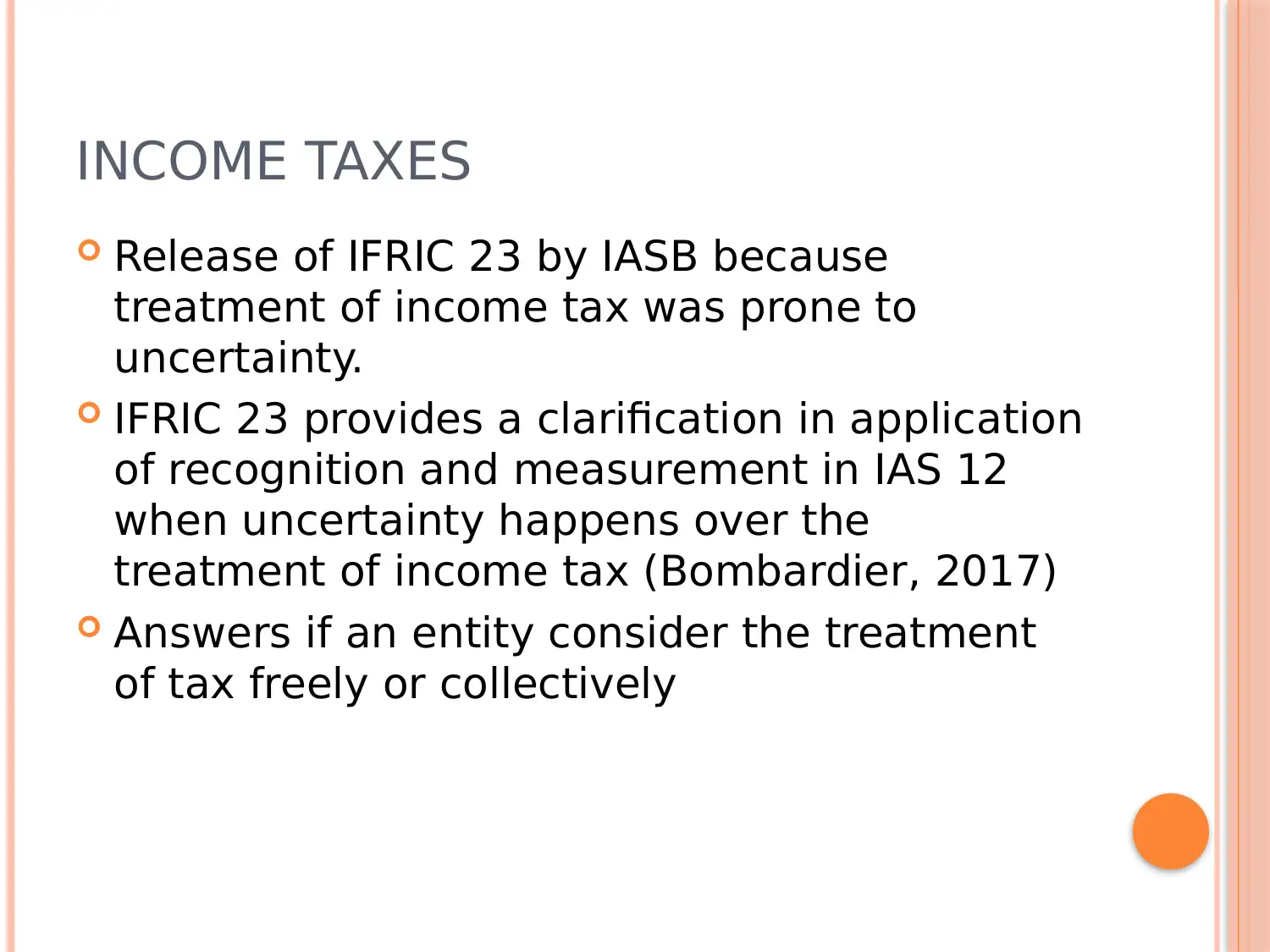

This financial analysis report examines Bombardier's financial performance, particularly focusing on taxation, compliance, and related strategies. The report delves into the company's tax payments, including payroll, profit, and property taxes, highlighting the significant tax contributions made over a five-year period. It explores the use of the liability method for income tax accounting, the recognition of deferred income tax assets and liabilities, and the methods used for measuring these items. The analysis also covers taxation rates, the impact of tax changes in the U.S., and the implications of IFRIC 23. Furthermore, it examines the company's tax contribution, compliance with tax regulations, tax risk management, and its dealings with tax authorities, including the role of an internal tax team. The report also addresses tax avoidance strategies, the use of tax havens, and the government's stance on these practices, concluding with a call for a fair tax system in Canada. The report uses Bombardier's 2017 annual report as a reference.

1 out of 23

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.