Strategic Financial Analysis and Comparison of Booker and Tate & Lyle

VerifiedAdded on 2023/05/28

|69

|13055

|110

Report

AI Summary

This report conducts a strategic financial analysis of Booker and Tate & Lyle using methods such as trend analysis, ratio analysis, and DuPont analysis. The analysis reveals that Booker's financial performance is generally better than Tate & Lyle's. However, the report recommends that both companies adopt contemporary methods like EVA, CAPM, and the efficient market hypothesis to enhance their financial evaluations and overcome the limitations of traditional methods. The report includes a detailed comparison of profitability, liquidity, and efficiency ratios, along with an assessment of the merits and demerits of each analytical method used. It also discusses the application of contemporary financial analysis models for improved strategic decision-making.

1

Strategic financial analysis

Strategic financial analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

The present report is developed for providing an insight into different methods of

strategic financial analysis adopted by business companies for financial evaluation. This has

been carried out by conducting strategic financial analysis of the two companies that are Booker

and Tata&Lyle. The financial analysis is carried out with the use of trend analysis, ratio and du-

Pont analysis that Booker financial performance is better than that if its competitor Tate&Lyle.

However, it is recommended to the financial managers of both the companies to adopt the use of

contemporary methods such as EVA, CAPM and efficient market hypothesis for conducting

financial analysis to overcome the drawbacks presents in the traditional methods.

Executive Summary

The present report is developed for providing an insight into different methods of

strategic financial analysis adopted by business companies for financial evaluation. This has

been carried out by conducting strategic financial analysis of the two companies that are Booker

and Tata&Lyle. The financial analysis is carried out with the use of trend analysis, ratio and du-

Pont analysis that Booker financial performance is better than that if its competitor Tate&Lyle.

However, it is recommended to the financial managers of both the companies to adopt the use of

contemporary methods such as EVA, CAPM and efficient market hypothesis for conducting

financial analysis to overcome the drawbacks presents in the traditional methods.

3

Contents

Executive Summary.........................................................................................................................2

1.0: Introduction..............................................................................................................................4

2.0: Brief Introduction of Two Companies......................................................................................4

3.0: Financial Analysis Method.......................................................................................................5

3.1: Ratio Analysis...........................................................................................................................6

3.1.1: Profitability Ratio Analysis...................................................................................................6

3.1.2: Liquidity Analysis.................................................................................................................8

3.1.3: Efficiency Ratios.................................................................................................................10

3.1.4: Investors Analysis................................................................................................................12

3.2: Common Size Analysis..........................................................................................................14

3.2.1: Vertical – SOPL, SOFP and SOCF.....................................................................................14

3.2.2: Horizontal – SOPL, SOFP and SOCF.................................................................................17

3.3: Du-Pont Analysis of Booker for last five years......................................................................20

4.0: Merits and Demerits of each of analytical methods used to analyse the performance of

company.........................................................................................................................................22

4.1 Ratio Analysis..........................................................................................................................22

4.2 Trend Analysis (Horizontal &Vertical Analysis)....................................................................23

4.3: Du-Pont Analysis....................................................................................................................24

5. Contemporary Methods.............................................................................................................24

5.1 Capital Asset Pricing Model....................................................................................................24

5.2 Economic Value Added (EVA)...............................................................................................24

5.3 Efficient Market Hypothesis....................................................................................................25

6.0: Conclusion and Recommendation..........................................................................................25

7.0: References..............................................................................................................................26

8.0: Appendixes.............................................................................................................................28

Contents

Executive Summary.........................................................................................................................2

1.0: Introduction..............................................................................................................................4

2.0: Brief Introduction of Two Companies......................................................................................4

3.0: Financial Analysis Method.......................................................................................................5

3.1: Ratio Analysis...........................................................................................................................6

3.1.1: Profitability Ratio Analysis...................................................................................................6

3.1.2: Liquidity Analysis.................................................................................................................8

3.1.3: Efficiency Ratios.................................................................................................................10

3.1.4: Investors Analysis................................................................................................................12

3.2: Common Size Analysis..........................................................................................................14

3.2.1: Vertical – SOPL, SOFP and SOCF.....................................................................................14

3.2.2: Horizontal – SOPL, SOFP and SOCF.................................................................................17

3.3: Du-Pont Analysis of Booker for last five years......................................................................20

4.0: Merits and Demerits of each of analytical methods used to analyse the performance of

company.........................................................................................................................................22

4.1 Ratio Analysis..........................................................................................................................22

4.2 Trend Analysis (Horizontal &Vertical Analysis)....................................................................23

4.3: Du-Pont Analysis....................................................................................................................24

5. Contemporary Methods.............................................................................................................24

5.1 Capital Asset Pricing Model....................................................................................................24

5.2 Economic Value Added (EVA)...............................................................................................24

5.3 Efficient Market Hypothesis....................................................................................................25

6.0: Conclusion and Recommendation..........................................................................................25

7.0: References..............................................................................................................................26

8.0: Appendixes.............................................................................................................................28

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

1.0: Introduction

The process of Strategic Financial Analysis (SFA) can be described as the task of

preparing the financial plan for development of business goals and objectives to be achieved.

The financial plan is developed for determining the ways that a business can adopt for achieving

its strategic goals and objectives. It can be regarded as a value-creating framework that helps

senior executives to examine the business strategy, evaluate its performance and thereby valuing

the business. The financial analysis is regarded to be very important for businesses to undertaken

an overview of the financial position of a company that can assist in its future financial planning

process. The financial management decisions help a company to make important investment

decisions regarding its future growth and development. The financial analysis enables a company

to develop adequate financial strategy that results in maximization of shareholder value. The

financial strategy developed though conducting financial evaluation helps a company to gain an

insight into the financial resources possessed for achieving its strategic goals and objectives

(Ehrhardt and Brigham, 2016).

The main objective of the report is to conduct a critical assessment of the principal

method used for analyzing the financial position of a company as an outsider. The method of

financial analysis includes calculation of financial ratios, vertical and horizontal and DuPont

analysis. Also, it intends to present the major drawbacks that re present within the financial

analysis methods and proposed more effective methods that can be sued for overcoming these

drawbacks. The overall financial analysis is carried out by presenting working examples from the

selected listed companies that are Booker Group PLC & Tate &Lyre PLC.

2.0: Brief Introduction of Two Companies

Booker Group PLC is recognized as the largest food wholesale operator within the UK

that is involved in providing both branded and private label goods to about 40,000 customers. It

operates convenience stores, grocers, pubs and restaurants and as such the group comprises of

Booker Wholesale, Booker Direct, Classic Drinks, Family Shopper and many other business

units. The major product of the company includes grocery, fresh food, beers, wines, tobacco and

1.0: Introduction

The process of Strategic Financial Analysis (SFA) can be described as the task of

preparing the financial plan for development of business goals and objectives to be achieved.

The financial plan is developed for determining the ways that a business can adopt for achieving

its strategic goals and objectives. It can be regarded as a value-creating framework that helps

senior executives to examine the business strategy, evaluate its performance and thereby valuing

the business. The financial analysis is regarded to be very important for businesses to undertaken

an overview of the financial position of a company that can assist in its future financial planning

process. The financial management decisions help a company to make important investment

decisions regarding its future growth and development. The financial analysis enables a company

to develop adequate financial strategy that results in maximization of shareholder value. The

financial strategy developed though conducting financial evaluation helps a company to gain an

insight into the financial resources possessed for achieving its strategic goals and objectives

(Ehrhardt and Brigham, 2016).

The main objective of the report is to conduct a critical assessment of the principal

method used for analyzing the financial position of a company as an outsider. The method of

financial analysis includes calculation of financial ratios, vertical and horizontal and DuPont

analysis. Also, it intends to present the major drawbacks that re present within the financial

analysis methods and proposed more effective methods that can be sued for overcoming these

drawbacks. The overall financial analysis is carried out by presenting working examples from the

selected listed companies that are Booker Group PLC & Tate &Lyre PLC.

2.0: Brief Introduction of Two Companies

Booker Group PLC is recognized as the largest food wholesale operator within the UK

that is involved in providing both branded and private label goods to about 40,000 customers. It

operates convenience stores, grocers, pubs and restaurants and as such the group comprises of

Booker Wholesale, Booker Direct, Classic Drinks, Family Shopper and many other business

units. The major product of the company includes grocery, fresh food, beers, wines, tobacco and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

alcoholic products. The non-food product items of the company include stationery, furniture,

office equipment and clothing (Booker, 2017).

On the other hand, Tate & Lyle PLC is recognized as a global supplier of food and

beverage ingredients to industrial markets. The company is headquartered within the UK and has

attained a leadership position within the food and beverage industry at a global level with the use

of its innovative technology to transform the raw materials and developing large-scale

manufacturing plants. The high manufacturing capabilities of the company has enabled it to

produce high quality ingredients for the customers. The company aspired to attain a global

position in providing special food ingredients and solutions.

3.0: Financial Analysis Method

Ratio Analysis

The method of ratio analysis has proved to be very effective for gaining an analysis of the

financial position of a company. It is regarded to be a quantitative method of analysis that can be

effectively sued for evaluating different financial aspects of a company such as determination of

its efficiency, liquidity, profitability, solvency and others. The different financial ratios are

calculated with the use of financial information disclosed by a company in its financial

statements.

Vertical Analysis

Vertical analysis can be regarded as a method of comparing the financial statement in

which each line item can be expressed as a percentage of base figures such as income statements

can be expressed as a percentage of gross sales (Gibson, 2008).

Horizontal Analysis

It is also known as trend analysis that involves expressing the financial items in the

financial statements as a percentage of the amount in the baseline year and taking the baseline

amount to be 100%.

DuPont

alcoholic products. The non-food product items of the company include stationery, furniture,

office equipment and clothing (Booker, 2017).

On the other hand, Tate & Lyle PLC is recognized as a global supplier of food and

beverage ingredients to industrial markets. The company is headquartered within the UK and has

attained a leadership position within the food and beverage industry at a global level with the use

of its innovative technology to transform the raw materials and developing large-scale

manufacturing plants. The high manufacturing capabilities of the company has enabled it to

produce high quality ingredients for the customers. The company aspired to attain a global

position in providing special food ingredients and solutions.

3.0: Financial Analysis Method

Ratio Analysis

The method of ratio analysis has proved to be very effective for gaining an analysis of the

financial position of a company. It is regarded to be a quantitative method of analysis that can be

effectively sued for evaluating different financial aspects of a company such as determination of

its efficiency, liquidity, profitability, solvency and others. The different financial ratios are

calculated with the use of financial information disclosed by a company in its financial

statements.

Vertical Analysis

Vertical analysis can be regarded as a method of comparing the financial statement in

which each line item can be expressed as a percentage of base figures such as income statements

can be expressed as a percentage of gross sales (Gibson, 2008).

Horizontal Analysis

It is also known as trend analysis that involves expressing the financial items in the

financial statements as a percentage of the amount in the baseline year and taking the baseline

amount to be 100%.

DuPont

6

The method of financial analysis involves analyzing decomposing the different metrics of

return on equity for assessing the financial performance of a company (Monks and Lajoux,

2010).

3.1: Ratio Analysis

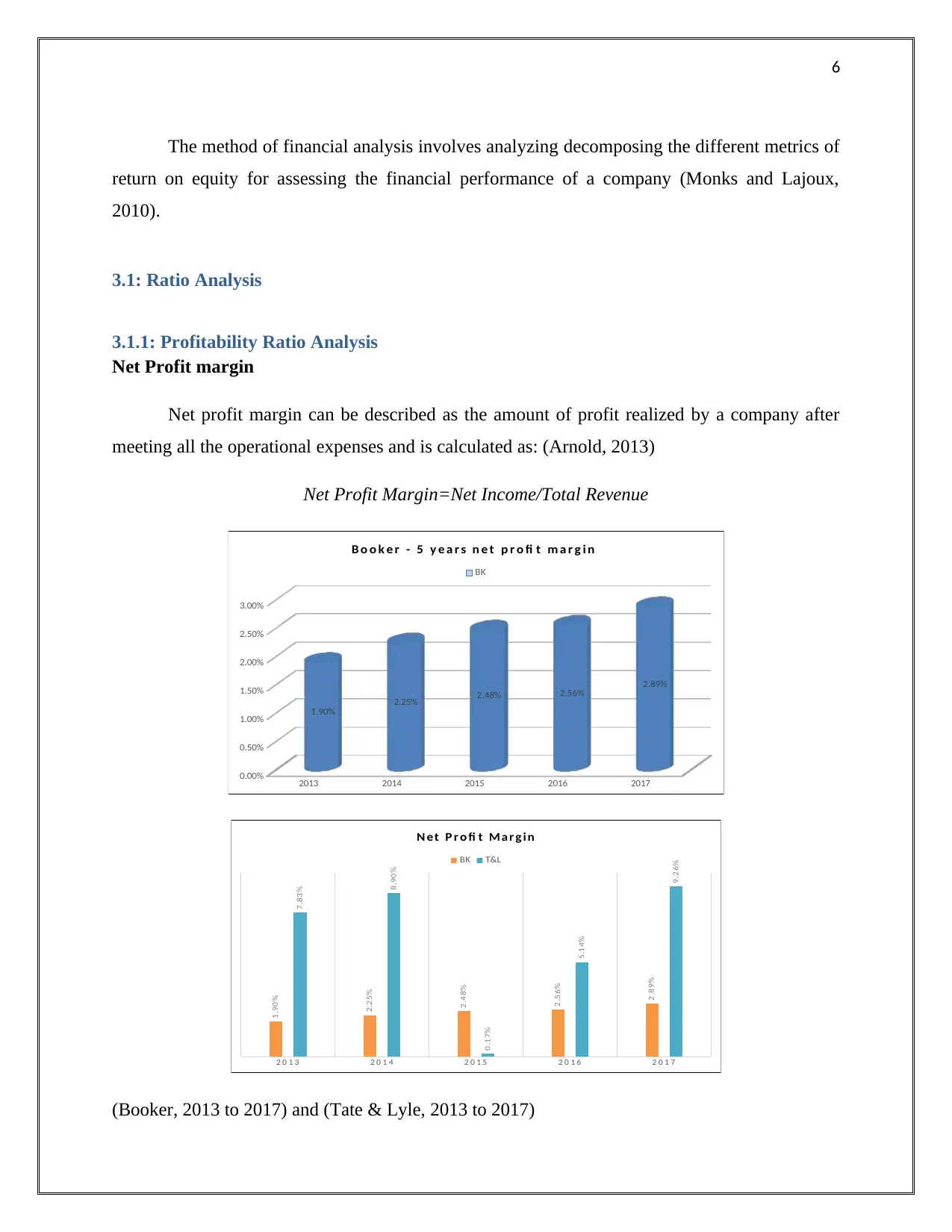

3.1.1: Profitability Ratio Analysis

Net Profit margin

Net profit margin can be described as the amount of profit realized by a company after

meeting all the operational expenses and is calculated as: (Arnold, 2013)

Net Profit Margin=Net Income/Total Revenue

2013 2014 2015 2016 2017

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

1.90%

2.25% 2.48% 2.56% 2.89%

B o o k e r - 5 y e a r s n e t p r o fi t m a r g i n

BK

2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7

1.90%

2.25%

2.48%

2.56%

2.89%

7.83%

8.90%

0.17%

5.14%

9.26%

N et P r o fi t Ma r g in

BK T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The method of financial analysis involves analyzing decomposing the different metrics of

return on equity for assessing the financial performance of a company (Monks and Lajoux,

2010).

3.1: Ratio Analysis

3.1.1: Profitability Ratio Analysis

Net Profit margin

Net profit margin can be described as the amount of profit realized by a company after

meeting all the operational expenses and is calculated as: (Arnold, 2013)

Net Profit Margin=Net Income/Total Revenue

2013 2014 2015 2016 2017

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

1.90%

2.25% 2.48% 2.56% 2.89%

B o o k e r - 5 y e a r s n e t p r o fi t m a r g i n

BK

2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7

1.90%

2.25%

2.48%

2.56%

2.89%

7.83%

8.90%

0.17%

5.14%

9.26%

N et P r o fi t Ma r g in

BK T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

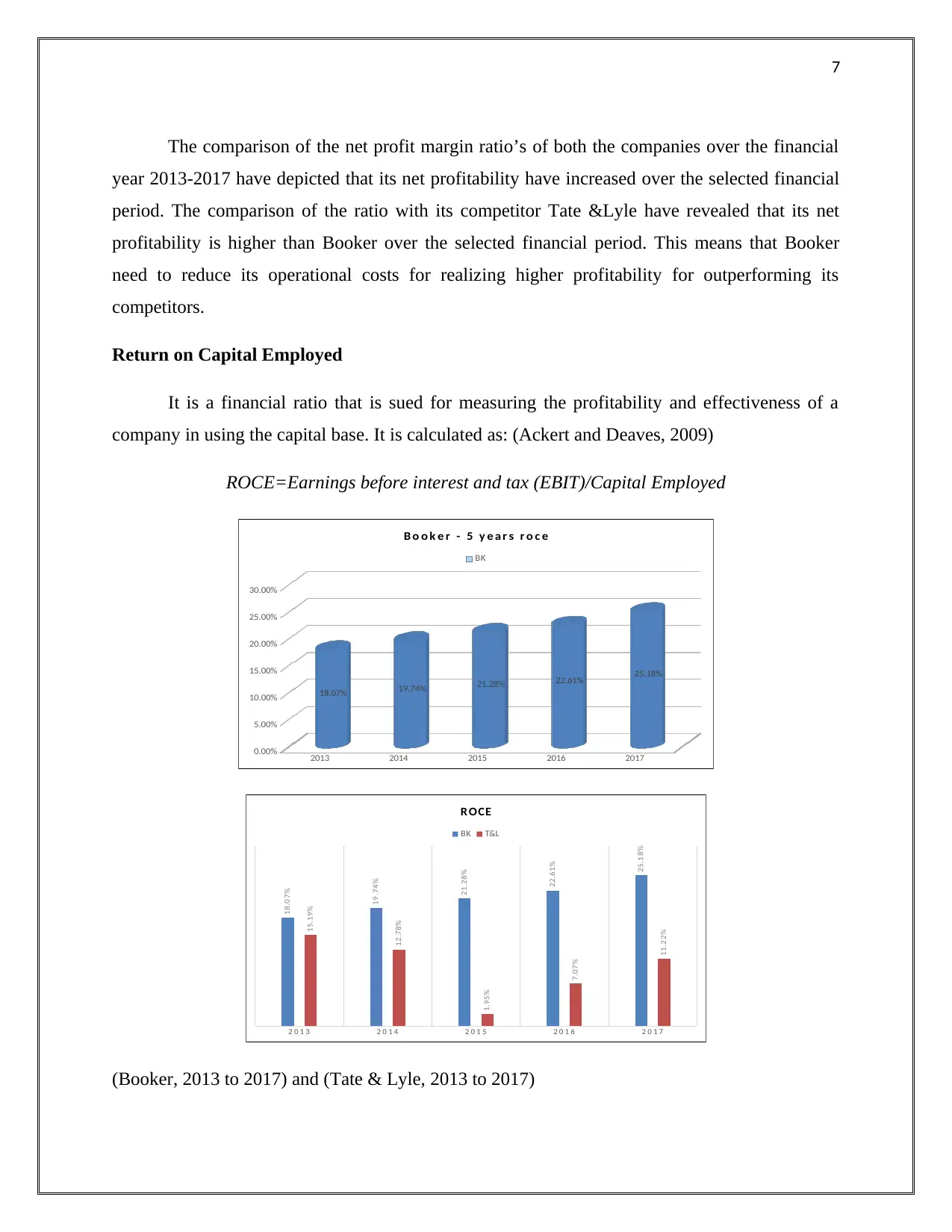

The comparison of the net profit margin ratio’s of both the companies over the financial

year 2013-2017 have depicted that its net profitability have increased over the selected financial

period. The comparison of the ratio with its competitor Tate &Lyle have revealed that its net

profitability is higher than Booker over the selected financial period. This means that Booker

need to reduce its operational costs for realizing higher profitability for outperforming its

competitors.

Return on Capital Employed

It is a financial ratio that is sued for measuring the profitability and effectiveness of a

company in using the capital base. It is calculated as: (Ackert and Deaves, 2009)

ROCE=Earnings before interest and tax (EBIT)/Capital Employed

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

18.07% 19.74% 21.28% 22.61% 25.18%

B o o k e r - 5 y e a r s r o c e

BK

2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7

18.07%

19.74%

21.28%

22.61%

25.18%

15.19%

12.78%

1.95%

7.07%

11.22%

R OCE

BK T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The comparison of the net profit margin ratio’s of both the companies over the financial

year 2013-2017 have depicted that its net profitability have increased over the selected financial

period. The comparison of the ratio with its competitor Tate &Lyle have revealed that its net

profitability is higher than Booker over the selected financial period. This means that Booker

need to reduce its operational costs for realizing higher profitability for outperforming its

competitors.

Return on Capital Employed

It is a financial ratio that is sued for measuring the profitability and effectiveness of a

company in using the capital base. It is calculated as: (Ackert and Deaves, 2009)

ROCE=Earnings before interest and tax (EBIT)/Capital Employed

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

18.07% 19.74% 21.28% 22.61% 25.18%

B o o k e r - 5 y e a r s r o c e

BK

2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7

18.07%

19.74%

21.28%

22.61%

25.18%

15.19%

12.78%

1.95%

7.07%

11.22%

R OCE

BK T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

The ratio of the company BK has increased from 2013-2017 stating that its efficiency to

use capital for generating profits is on increase. On the other hand, the ratio of the company Tate

&Lyle is lower in comparison to BK depicting that its efficiency to utilize capital base is not so

effective in comparison to Booker. Booker is having high capital turnover which indicates that it

trades more for each dollar of capital invested. Tate & Lyle has realized a constant decrease in its

ROCE despite of increase in the net profitability which can be linked to its poor management by

the Chief Financial Officer.

3.1.2: Liquidity Analysis

Current Ratio

It measures the ability of a company to meet effectively its financial obligations from the

asset base and can be calculated as: (Moles and Kidwekk, 2011)

Current Ratio=Current Assets/Current Liabilities

2013 2014 2015 2016 2017

0.75

0.80

0.85

0.90

0.95

1.00

1.05

0.87

0.98 0.99

0.95

1.01

Booker - 5 years current ratios

BK

The ratio of the company BK has increased from 2013-2017 stating that its efficiency to

use capital for generating profits is on increase. On the other hand, the ratio of the company Tate

&Lyle is lower in comparison to BK depicting that its efficiency to utilize capital base is not so

effective in comparison to Booker. Booker is having high capital turnover which indicates that it

trades more for each dollar of capital invested. Tate & Lyle has realized a constant decrease in its

ROCE despite of increase in the net profitability which can be linked to its poor management by

the Chief Financial Officer.

3.1.2: Liquidity Analysis

Current Ratio

It measures the ability of a company to meet effectively its financial obligations from the

asset base and can be calculated as: (Moles and Kidwekk, 2011)

Current Ratio=Current Assets/Current Liabilities

2013 2014 2015 2016 2017

0.75

0.80

0.85

0.90

0.95

1.00

1.05

0.87

0.98 0.99

0.95

1.01

Booker - 5 years current ratios

BK

9

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

0.87 0.98 0.99 0.95 1.01

2.31

1.50

1.32

1.63

2.10

Current Ratio

BK

T&L

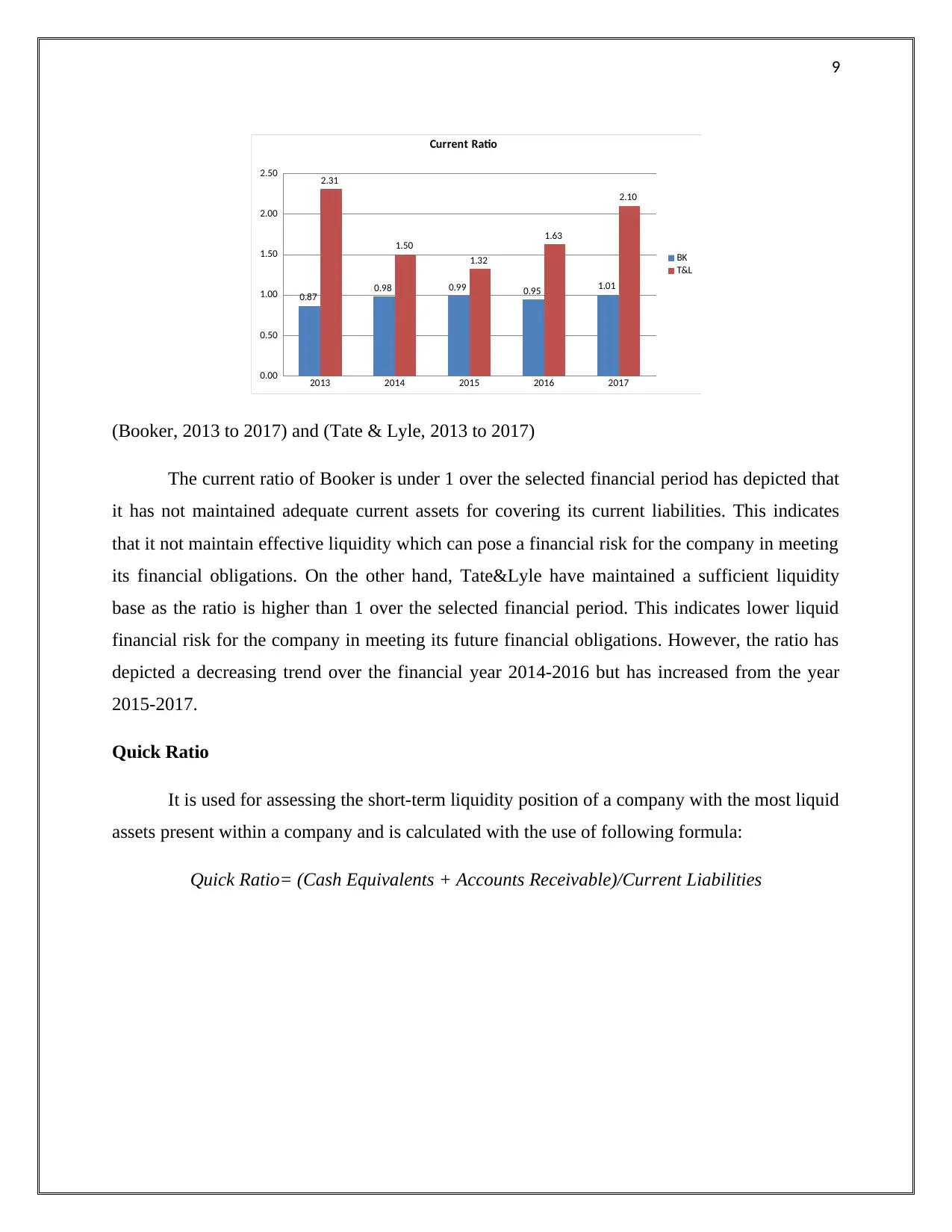

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The current ratio of Booker is under 1 over the selected financial period has depicted that

it has not maintained adequate current assets for covering its current liabilities. This indicates

that it not maintain effective liquidity which can pose a financial risk for the company in meeting

its financial obligations. On the other hand, Tate&Lyle have maintained a sufficient liquidity

base as the ratio is higher than 1 over the selected financial period. This indicates lower liquid

financial risk for the company in meeting its future financial obligations. However, the ratio has

depicted a decreasing trend over the financial year 2014-2016 but has increased from the year

2015-2017.

Quick Ratio

It is used for assessing the short-term liquidity position of a company with the most liquid

assets present within a company and is calculated with the use of following formula:

Quick Ratio= (Cash Equivalents + Accounts Receivable)/Current Liabilities

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

0.87 0.98 0.99 0.95 1.01

2.31

1.50

1.32

1.63

2.10

Current Ratio

BK

T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The current ratio of Booker is under 1 over the selected financial period has depicted that

it has not maintained adequate current assets for covering its current liabilities. This indicates

that it not maintain effective liquidity which can pose a financial risk for the company in meeting

its financial obligations. On the other hand, Tate&Lyle have maintained a sufficient liquidity

base as the ratio is higher than 1 over the selected financial period. This indicates lower liquid

financial risk for the company in meeting its future financial obligations. However, the ratio has

depicted a decreasing trend over the financial year 2014-2016 but has increased from the year

2015-2017.

Quick Ratio

It is used for assessing the short-term liquidity position of a company with the most liquid

assets present within a company and is calculated with the use of following formula:

Quick Ratio= (Cash Equivalents + Accounts Receivable)/Current Liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

2013 2014 2015 2016 2017

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.34

0.44 0.45 0.44 0.46

Booker - 5 years quick ratios

BK

2013 2014 2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.34

0.44 0.45 0.44 0.46

1.44

0.98

0.81

1.03

1.20

Quick Ratio

BK

T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

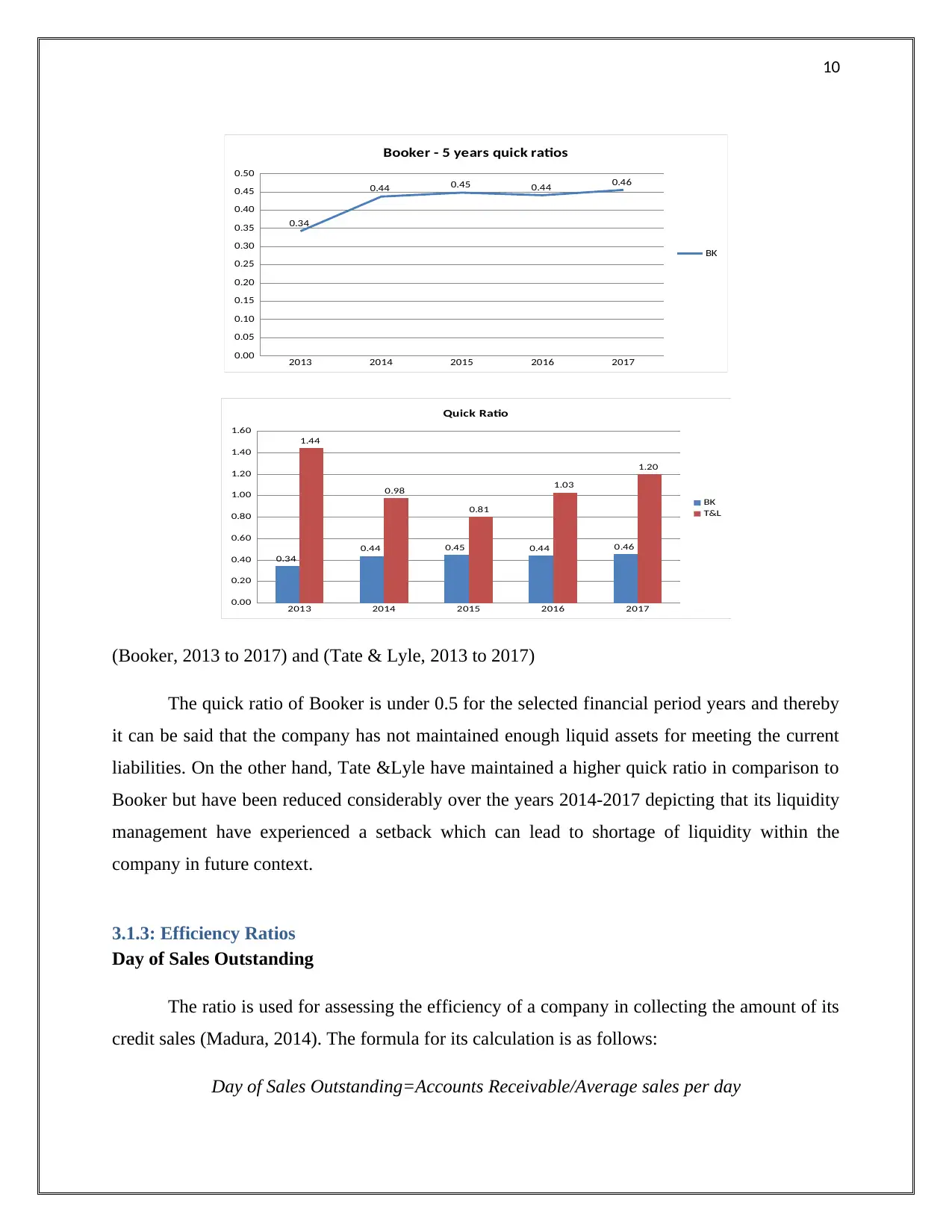

The quick ratio of Booker is under 0.5 for the selected financial period years and thereby

it can be said that the company has not maintained enough liquid assets for meeting the current

liabilities. On the other hand, Tate &Lyle have maintained a higher quick ratio in comparison to

Booker but have been reduced considerably over the years 2014-2017 depicting that its liquidity

management have experienced a setback which can lead to shortage of liquidity within the

company in future context.

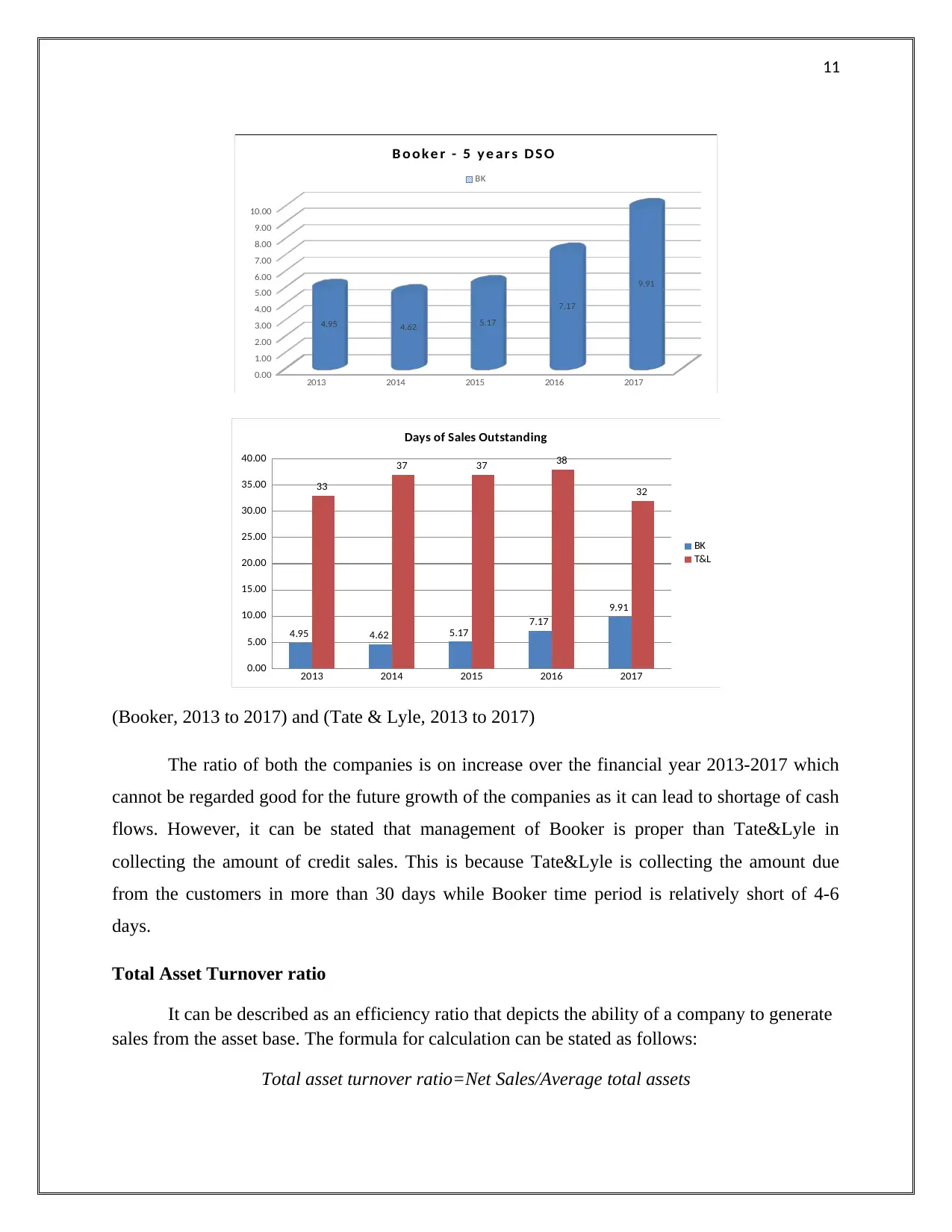

3.1.3: Efficiency Ratios

Day of Sales Outstanding

The ratio is used for assessing the efficiency of a company in collecting the amount of its

credit sales (Madura, 2014). The formula for its calculation is as follows:

Day of Sales Outstanding=Accounts Receivable/Average sales per day

2013 2014 2015 2016 2017

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.34

0.44 0.45 0.44 0.46

Booker - 5 years quick ratios

BK

2013 2014 2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.34

0.44 0.45 0.44 0.46

1.44

0.98

0.81

1.03

1.20

Quick Ratio

BK

T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The quick ratio of Booker is under 0.5 for the selected financial period years and thereby

it can be said that the company has not maintained enough liquid assets for meeting the current

liabilities. On the other hand, Tate &Lyle have maintained a higher quick ratio in comparison to

Booker but have been reduced considerably over the years 2014-2017 depicting that its liquidity

management have experienced a setback which can lead to shortage of liquidity within the

company in future context.

3.1.3: Efficiency Ratios

Day of Sales Outstanding

The ratio is used for assessing the efficiency of a company in collecting the amount of its

credit sales (Madura, 2014). The formula for its calculation is as follows:

Day of Sales Outstanding=Accounts Receivable/Average sales per day

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

2013 2014 2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

4.95 4.62 5.17

7.17

9.91

B o ok e r - 5 y e ar s D S O

BK

2013 2014 2015 2016 2017

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

4.95 4.62 5.17 7.17

9.91

33

37 37 38

32

Days of Sales Outstanding

BK

T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The ratio of both the companies is on increase over the financial year 2013-2017 which

cannot be regarded good for the future growth of the companies as it can lead to shortage of cash

flows. However, it can be stated that management of Booker is proper than Tate&Lyle in

collecting the amount of credit sales. This is because Tate&Lyle is collecting the amount due

from the customers in more than 30 days while Booker time period is relatively short of 4-6

days.

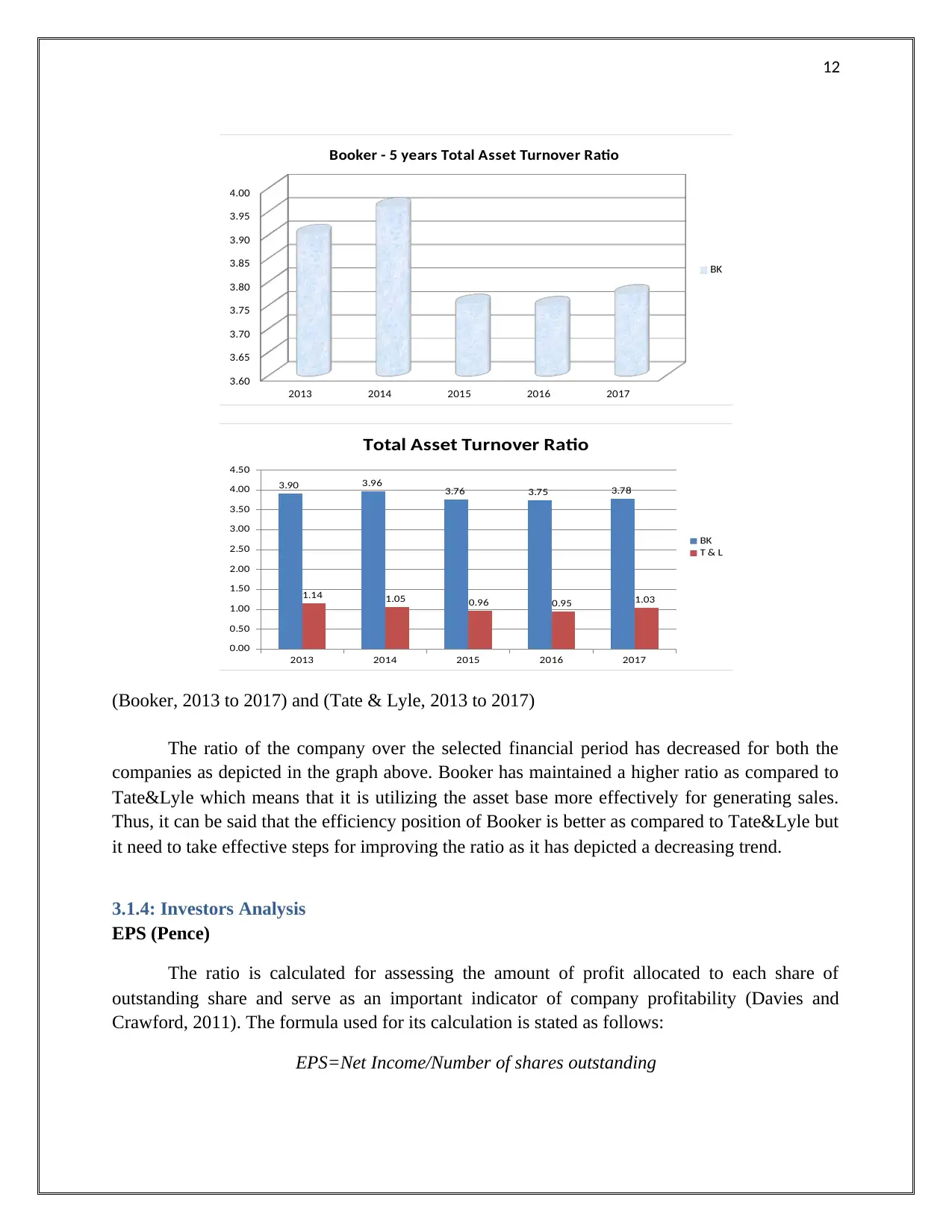

Total Asset Turnover ratio

It can be described as an efficiency ratio that depicts the ability of a company to generate

sales from the asset base. The formula for calculation can be stated as follows:

Total asset turnover ratio=Net Sales/Average total assets

2013 2014 2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

4.95 4.62 5.17

7.17

9.91

B o ok e r - 5 y e ar s D S O

BK

2013 2014 2015 2016 2017

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

4.95 4.62 5.17 7.17

9.91

33

37 37 38

32

Days of Sales Outstanding

BK

T&L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The ratio of both the companies is on increase over the financial year 2013-2017 which

cannot be regarded good for the future growth of the companies as it can lead to shortage of cash

flows. However, it can be stated that management of Booker is proper than Tate&Lyle in

collecting the amount of credit sales. This is because Tate&Lyle is collecting the amount due

from the customers in more than 30 days while Booker time period is relatively short of 4-6

days.

Total Asset Turnover ratio

It can be described as an efficiency ratio that depicts the ability of a company to generate

sales from the asset base. The formula for calculation can be stated as follows:

Total asset turnover ratio=Net Sales/Average total assets

12

2013 2014 2015 2016 2017

3.60

3.65

3.70

3.75

3.80

3.85

3.90

3.95

4.00

Booker - 5 years Total Asset Turnover Ratio

BK

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

3.90 3.96 3.76 3.75 3.78

1.14 1.05 0.96 0.95 1.03

Total Asset Turnover Ratio

BK

T & L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The ratio of the company over the selected financial period has decreased for both the

companies as depicted in the graph above. Booker has maintained a higher ratio as compared to

Tate&Lyle which means that it is utilizing the asset base more effectively for generating sales.

Thus, it can be said that the efficiency position of Booker is better as compared to Tate&Lyle but

it need to take effective steps for improving the ratio as it has depicted a decreasing trend.

3.1.4: Investors Analysis

EPS (Pence)

The ratio is calculated for assessing the amount of profit allocated to each share of

outstanding share and serve as an important indicator of company profitability (Davies and

Crawford, 2011). The formula used for its calculation is stated as follows:

EPS=Net Income/Number of shares outstanding

2013 2014 2015 2016 2017

3.60

3.65

3.70

3.75

3.80

3.85

3.90

3.95

4.00

Booker - 5 years Total Asset Turnover Ratio

BK

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

3.90 3.96 3.76 3.75 3.78

1.14 1.05 0.96 0.95 1.03

Total Asset Turnover Ratio

BK

T & L

(Booker, 2013 to 2017) and (Tate & Lyle, 2013 to 2017)

The ratio of the company over the selected financial period has decreased for both the

companies as depicted in the graph above. Booker has maintained a higher ratio as compared to

Tate&Lyle which means that it is utilizing the asset base more effectively for generating sales.

Thus, it can be said that the efficiency position of Booker is better as compared to Tate&Lyle but

it need to take effective steps for improving the ratio as it has depicted a decreasing trend.

3.1.4: Investors Analysis

EPS (Pence)

The ratio is calculated for assessing the amount of profit allocated to each share of

outstanding share and serve as an important indicator of company profitability (Davies and

Crawford, 2011). The formula used for its calculation is stated as follows:

EPS=Net Income/Number of shares outstanding

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 69

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.