Financial Performance Evaluation of Boral Ltd: A Detailed Analysis

VerifiedAdded on 2021/05/31

|19

|4359

|349

Report

AI Summary

This report presents a comprehensive financial analysis of Boral Ltd, evaluating its performance based on various financial ratios, including short-term and long-term solvency, asset utilization, profitability, and market value. The analysis includes the ownership and governance structure, identifying key shareholders and their influence. The report examines the movement of Boral Ltd's share price against the all ordinary index, identifying significant factors impacting share price. Furthermore, it employs the Capital Asset Pricing Model (CAPM) to determine the required rate of return and assesses the weighted average cost of capital (WACC). The debt and dividend policies are also reviewed to understand the company's capital structure and financial strategy. The report concludes with investment recommendations.

Running head: FINANCE FOR BUSINESS

Finance for Business

Name of the Student

Name of the University

Authors Note

Course ID

Finance for Business

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR BUSINESS

Table of Contents

Introduction:...............................................................................................................................3

Description of the company:......................................................................................................4

Ownership-Governance Structure of Boral Ltd:........................................................................4

Main substantial Shareholders:..............................................................................................4

Main People involved in Governance:...................................................................................5

Calculations of the Fundamental Ratios:...................................................................................6

Short-Term Solvency Ratios:.................................................................................................6

Long Term Solvency Ratios:.................................................................................................6

Asset Utilization Ratios:........................................................................................................7

Profitability Ratios:................................................................................................................7

Market Value Ratios:.............................................................................................................7

Graphical Description of Share Price Results:...........................................................................8

Monthly share price movement analysis:...............................................................................8

Significant factors influencing the share price movement:......................................................10

Calculations of the Beta values and the anticipated Rates of Return using CAPM:................11

Calculated beta of the company:..........................................................................................11

Computation of required rate of return for the company shares:.........................................11

Conservative for Investment:...............................................................................................12

Weighted Average Cost of Capital:.........................................................................................13

Computed WACC:...............................................................................................................13

Table of Contents

Introduction:...............................................................................................................................3

Description of the company:......................................................................................................4

Ownership-Governance Structure of Boral Ltd:........................................................................4

Main substantial Shareholders:..............................................................................................4

Main People involved in Governance:...................................................................................5

Calculations of the Fundamental Ratios:...................................................................................6

Short-Term Solvency Ratios:.................................................................................................6

Long Term Solvency Ratios:.................................................................................................6

Asset Utilization Ratios:........................................................................................................7

Profitability Ratios:................................................................................................................7

Market Value Ratios:.............................................................................................................7

Graphical Description of Share Price Results:...........................................................................8

Monthly share price movement analysis:...............................................................................8

Significant factors influencing the share price movement:......................................................10

Calculations of the Beta values and the anticipated Rates of Return using CAPM:................11

Calculated beta of the company:..........................................................................................11

Computation of required rate of return for the company shares:.........................................11

Conservative for Investment:...............................................................................................12

Weighted Average Cost of Capital:.........................................................................................13

Computed WACC:...............................................................................................................13

2FINANCE FOR BUSINESS

Implications of higher weighted average cost of capitals from management perspective:..13

Debt Ratio:...............................................................................................................................13

Dividend Policy:.......................................................................................................................14

Letter of Recommendations.....................................................................................................14

Conclusion:..............................................................................................................................15

References................................................................................................................................16

Implications of higher weighted average cost of capitals from management perspective:..13

Debt Ratio:...............................................................................................................................13

Dividend Policy:.......................................................................................................................14

Letter of Recommendations.....................................................................................................14

Conclusion:..............................................................................................................................15

References................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR BUSINESS

Introduction:

The current report is based on understanding the financial performance of the Boral

Ltd and investigating into the possibility of making investment in the company. The study

would be opening up with brief description of the company by outlining the core activities of

the organizations the market in which the company operates and the factors that contributes

to the history of the company. The report would be taking into the consideration the

ownership governance structure of the company and the main substantial shareholders that

are involved in the business. Based on the proportion of the shareholdings of the company an

argument would be presented to distinguish between the family and the non-family

indulgence on the firm’s governance.

To better understand the financial position of the company a computation of the

financial ratios would be performed that would be assessing the areas of short term and long

term financial standings of the company. Additionally the report would be considering the

efficiency, profitability and market value ratios to better gain an understanding of the firm’s

financial position.

A comparative analysis of the share price movement against the all ordinary index

would be performed to understand whether the share price are above or below volatility

range. The report would be considering the major factors that contributes to the share price

movement of the organization. The tools of capital asset pricing model will be employed to

understand the require rate of return for the company along with the conservative nature of

making an investment in Boral Ltd. The debt structure and the dividend structure would be

also gauged to understand whether the company is appropriately maintained the capital

structure. A letter of recommendations would be accompanied with valuable

recommendations relating to the possibility of making investment in the company.

Introduction:

The current report is based on understanding the financial performance of the Boral

Ltd and investigating into the possibility of making investment in the company. The study

would be opening up with brief description of the company by outlining the core activities of

the organizations the market in which the company operates and the factors that contributes

to the history of the company. The report would be taking into the consideration the

ownership governance structure of the company and the main substantial shareholders that

are involved in the business. Based on the proportion of the shareholdings of the company an

argument would be presented to distinguish between the family and the non-family

indulgence on the firm’s governance.

To better understand the financial position of the company a computation of the

financial ratios would be performed that would be assessing the areas of short term and long

term financial standings of the company. Additionally the report would be considering the

efficiency, profitability and market value ratios to better gain an understanding of the firm’s

financial position.

A comparative analysis of the share price movement against the all ordinary index

would be performed to understand whether the share price are above or below volatility

range. The report would be considering the major factors that contributes to the share price

movement of the organization. The tools of capital asset pricing model will be employed to

understand the require rate of return for the company along with the conservative nature of

making an investment in Boral Ltd. The debt structure and the dividend structure would be

also gauged to understand whether the company is appropriately maintained the capital

structure. A letter of recommendations would be accompanied with valuable

recommendations relating to the possibility of making investment in the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR BUSINESS

Description of the company:

Boral Ltd is an international building products and construction material company

that has three strong division. It is regarded as one of the Australia’s fast growing company

with ventures across the Asia, Australia, Middle East and northern America (Boral 2018).

The company was founded in the year 1946 and has it’s headquarter in Sydney. The company

exclusively deals in manufacturing, supply of construction building materials.

Ownership-Governance Structure of Boral Ltd:

Main substantial Shareholders:

Name of the Shareholders Total Number of Shares

Black Rock In and Subsidiaries 58,821,314

Capital Group of Companies 61,918,012

As evident from the above stated representation that the substantial shareholders for

the company stood Black Rock Inc and Subsidiaries that held 58,821,314. While the other

substantial shareholders for the company stood Capital Group of Companies that held

61,918,012 of the total number of ordinary shares that were issued by the company (Boral

2018). As understood none of the substantial shareholders of the company held more than

20% of the shareholders nor any of the substantial shareholder of Boral Ltd held greater than

5% of the total share holdings.

Apart from the above stated substantial shareholders there are other largest

shareholders of Boral Ltd is stated below;

Name of the Shareholders Total Ordinary Shares Percentage of Ordinary

Shares

HSBC CUSTODY 339,668,286 28.96%

Description of the company:

Boral Ltd is an international building products and construction material company

that has three strong division. It is regarded as one of the Australia’s fast growing company

with ventures across the Asia, Australia, Middle East and northern America (Boral 2018).

The company was founded in the year 1946 and has it’s headquarter in Sydney. The company

exclusively deals in manufacturing, supply of construction building materials.

Ownership-Governance Structure of Boral Ltd:

Main substantial Shareholders:

Name of the Shareholders Total Number of Shares

Black Rock In and Subsidiaries 58,821,314

Capital Group of Companies 61,918,012

As evident from the above stated representation that the substantial shareholders for

the company stood Black Rock Inc and Subsidiaries that held 58,821,314. While the other

substantial shareholders for the company stood Capital Group of Companies that held

61,918,012 of the total number of ordinary shares that were issued by the company (Boral

2018). As understood none of the substantial shareholders of the company held more than

20% of the shareholders nor any of the substantial shareholder of Boral Ltd held greater than

5% of the total share holdings.

Apart from the above stated substantial shareholders there are other largest

shareholders of Boral Ltd is stated below;

Name of the Shareholders Total Ordinary Shares Percentage of Ordinary

Shares

HSBC CUSTODY 339,668,286 28.96%

5FINANCE FOR BUSINESS

NOMINEES

CITICORP NOMINEES

PTY LTD

263,107,753 22.44%

J P MORGAN NOMINEES

AUSTRALIA LTD

128,772,299 10.98%

NATIONAL NOMINEES

LTD

92,810,758 7.92%

BNP PARIBAS NOMS

PTY LTD

69,315,230 5.91%

The major shareholders for the company stood HSBC Custody Nominees as it held

333,668,286 that sums up 28.97% of the total shareholdings for Boral Ltd. The other

shareholders that held more than 20% is the J P Morgan Nominees Australia Pty Ltd with

263,107,753 of total ordinary shares with 22.44% of the ordinary shares (Boral 2018).

Among the other shares holders for the Boral Ltd were the Citi Corp Nominees Pty Ltd,

National Nominees Ltd and BNP Paribas Nominees Pty that held 10.98%, 7.92% and 5.91%

each.

Main People involved in Governance:

Name Position Held Number of Shares Held

Catherine Brenner Independent Director 48,405

Brian Clark Non-Executive Director 109,595

Elleen Doyle Independent Director 39,948

Kathryn Fagg Independent Director 38,582

Mike Kane Independent Director 946,043

NOMINEES

CITICORP NOMINEES

PTY LTD

263,107,753 22.44%

J P MORGAN NOMINEES

AUSTRALIA LTD

128,772,299 10.98%

NATIONAL NOMINEES

LTD

92,810,758 7.92%

BNP PARIBAS NOMS

PTY LTD

69,315,230 5.91%

The major shareholders for the company stood HSBC Custody Nominees as it held

333,668,286 that sums up 28.97% of the total shareholdings for Boral Ltd. The other

shareholders that held more than 20% is the J P Morgan Nominees Australia Pty Ltd with

263,107,753 of total ordinary shares with 22.44% of the ordinary shares (Boral 2018).

Among the other shares holders for the Boral Ltd were the Citi Corp Nominees Pty Ltd,

National Nominees Ltd and BNP Paribas Nominees Pty that held 10.98%, 7.92% and 5.91%

each.

Main People involved in Governance:

Name Position Held Number of Shares Held

Catherine Brenner Independent Director 48,405

Brian Clark Non-Executive Director 109,595

Elleen Doyle Independent Director 39,948

Kathryn Fagg Independent Director 38,582

Mike Kane Independent Director 946,043

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR BUSINESS

John Marlay Independent Director 39,310

Karen Moses Independent Director 21,757

Paul Rayner Non-Executive Director 100,555

As evident from the above stated tabular representation it can be stated that none of

the Independent Directors and the Non-Executive directors held greater than 20% of the total

shareholdings for Boral Ltd (Boral 2018). Additionally, none of the Independent Directors

and the Non-Executive directors held greater than 5% of the total shareholdings that were

issued by the company. An argument can be bought in this regard by stating that there is no

such existence of the family members in the governance of the organization.

Calculations of the Fundamental Ratios:

Short-Term Solvency Ratios:

Particulars` 2017 2016

(Amount $m) (Amount $m)

Current Assets A 1763.7 1684.2

Current Liabilities B 1468.3 1181.7

Inventory C 606.6 556.9

Other Assets D 41.9 32.4

Cash & Cash equivalents E 237.8 452.1

Current Ratio F=A/B 1.20 1.43

Quick Ratio G=(A-C-D)/B 0.76 0.93

Cash Ratio H=E/B 0.16 0.38

Long Term Solvency Ratios:

Particulars` 2017 2016

(Amount $m) (Amount $m)

Total Assets A 9313.6 5800.5

Total Equity B 5440.5 3506.3

Total Liabilities C 3873.1 2294.2

John Marlay Independent Director 39,310

Karen Moses Independent Director 21,757

Paul Rayner Non-Executive Director 100,555

As evident from the above stated tabular representation it can be stated that none of

the Independent Directors and the Non-Executive directors held greater than 20% of the total

shareholdings for Boral Ltd (Boral 2018). Additionally, none of the Independent Directors

and the Non-Executive directors held greater than 5% of the total shareholdings that were

issued by the company. An argument can be bought in this regard by stating that there is no

such existence of the family members in the governance of the organization.

Calculations of the Fundamental Ratios:

Short-Term Solvency Ratios:

Particulars` 2017 2016

(Amount $m) (Amount $m)

Current Assets A 1763.7 1684.2

Current Liabilities B 1468.3 1181.7

Inventory C 606.6 556.9

Other Assets D 41.9 32.4

Cash & Cash equivalents E 237.8 452.1

Current Ratio F=A/B 1.20 1.43

Quick Ratio G=(A-C-D)/B 0.76 0.93

Cash Ratio H=E/B 0.16 0.38

Long Term Solvency Ratios:

Particulars` 2017 2016

(Amount $m) (Amount $m)

Total Assets A 9313.6 5800.5

Total Equity B 5440.5 3506.3

Total Liabilities C 3873.1 2294.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR BUSINESS

Debt-to-Equity Ratio D=C/B 0.71 0.65

Debt Ratio E=C/A 0.42 0.40

Equity Ratio F=B/A 0.58 0.60

Asset Utilization Ratios:

Particulars` 2017 2016

(Amount $m) (Amount $m)

Total Assets A 9313.6 5800.5

Fixed Assets B 2755.7 2517.7

Sales C 4257.8 3945.2

Trade Receivables D 873.6 623.9

Total Asset Turnover Ratio E=C/A 0.46 0.68

Fixed Asset Turnover Ratio F=C/B 1.55 1.57

Receivables Turnover Ratio G=C/D 0.21 0.16

Profitability Ratios:

Particulars` 2017 2016

$m $m

Profit A 296.9 256.0

Sales B 4257.8 3945.2

Total Assets C 9313.6 5800.5

Total Equity D 5440.5 3506.3

Net Profit Margin E= A/B 6.97% 6.49%

Return on Equity (ROE) F=A/D 5.46% 7.30%

Return on Assets G=A/C 3.19% 4.41%

Market Value Ratios:

Particulars` 2017 2016

(Amount $m) (Amount $m)

Earnings per Share A 29.000 31.500

Dividend per Share B 0.24 0.22

Market Value per Share C 6.64 5.76

Dividend Pay-out Ratio D=B/A 0.83% 0.70%

Debt-to-Equity Ratio D=C/B 0.71 0.65

Debt Ratio E=C/A 0.42 0.40

Equity Ratio F=B/A 0.58 0.60

Asset Utilization Ratios:

Particulars` 2017 2016

(Amount $m) (Amount $m)

Total Assets A 9313.6 5800.5

Fixed Assets B 2755.7 2517.7

Sales C 4257.8 3945.2

Trade Receivables D 873.6 623.9

Total Asset Turnover Ratio E=C/A 0.46 0.68

Fixed Asset Turnover Ratio F=C/B 1.55 1.57

Receivables Turnover Ratio G=C/D 0.21 0.16

Profitability Ratios:

Particulars` 2017 2016

$m $m

Profit A 296.9 256.0

Sales B 4257.8 3945.2

Total Assets C 9313.6 5800.5

Total Equity D 5440.5 3506.3

Net Profit Margin E= A/B 6.97% 6.49%

Return on Equity (ROE) F=A/D 5.46% 7.30%

Return on Assets G=A/C 3.19% 4.41%

Market Value Ratios:

Particulars` 2017 2016

(Amount $m) (Amount $m)

Earnings per Share A 29.000 31.500

Dividend per Share B 0.24 0.22

Market Value per Share C 6.64 5.76

Dividend Pay-out Ratio D=B/A 0.83% 0.70%

8FINANCE FOR BUSINESS

Dividend Yield Rate E=B/C 3.61% 3.82%

Price-to-Earnings Ratio F=C/A 0.23 0.18

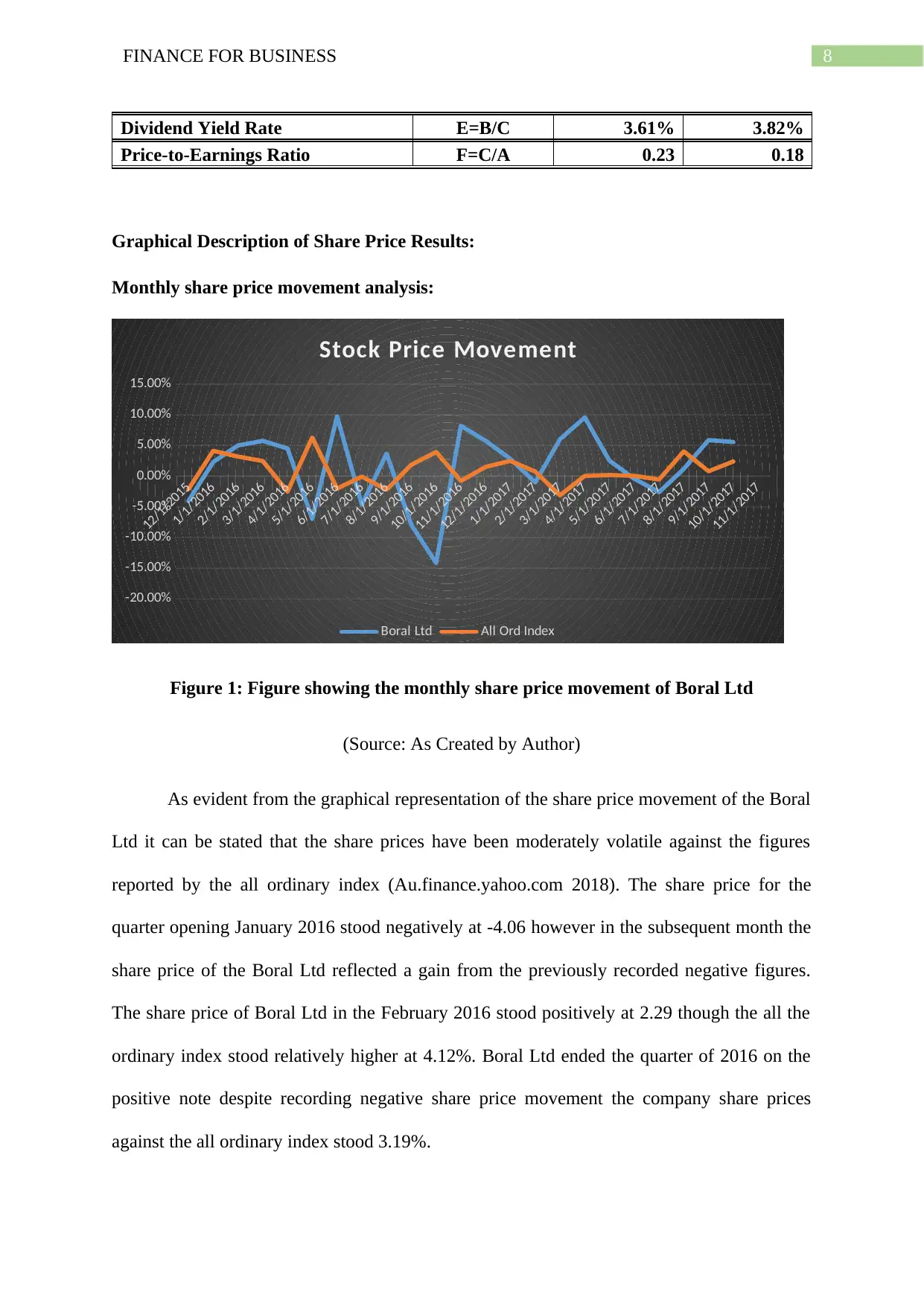

Graphical Description of Share Price Results:

Monthly share price movement analysis:

12/1/2015

1/1/2016

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

1/1/2017

2/1/2017

3/1/2017

4/1/2017

5/1/2017

6/1/2017

7/1/2017

8/1/2017

9/1/2017

10/1/2017

11/1/2017

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Stock Price Movement

Boral Ltd All Ord Index

Figure 1: Figure showing the monthly share price movement of Boral Ltd

(Source: As Created by Author)

As evident from the graphical representation of the share price movement of the Boral

Ltd it can be stated that the share prices have been moderately volatile against the figures

reported by the all ordinary index (Au.finance.yahoo.com 2018). The share price for the

quarter opening January 2016 stood negatively at -4.06 however in the subsequent month the

share price of the Boral Ltd reflected a gain from the previously recorded negative figures.

The share price of Boral Ltd in the February 2016 stood positively at 2.29 though the all the

ordinary index stood relatively higher at 4.12%. Boral Ltd ended the quarter of 2016 on the

positive note despite recording negative share price movement the company share prices

against the all ordinary index stood 3.19%.

Dividend Yield Rate E=B/C 3.61% 3.82%

Price-to-Earnings Ratio F=C/A 0.23 0.18

Graphical Description of Share Price Results:

Monthly share price movement analysis:

12/1/2015

1/1/2016

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

1/1/2017

2/1/2017

3/1/2017

4/1/2017

5/1/2017

6/1/2017

7/1/2017

8/1/2017

9/1/2017

10/1/2017

11/1/2017

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Stock Price Movement

Boral Ltd All Ord Index

Figure 1: Figure showing the monthly share price movement of Boral Ltd

(Source: As Created by Author)

As evident from the graphical representation of the share price movement of the Boral

Ltd it can be stated that the share prices have been moderately volatile against the figures

reported by the all ordinary index (Au.finance.yahoo.com 2018). The share price for the

quarter opening January 2016 stood negatively at -4.06 however in the subsequent month the

share price of the Boral Ltd reflected a gain from the previously recorded negative figures.

The share price of Boral Ltd in the February 2016 stood positively at 2.29 though the all the

ordinary index stood relatively higher at 4.12%. Boral Ltd ended the quarter of 2016 on the

positive note despite recording negative share price movement the company share prices

against the all ordinary index stood 3.19%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE FOR BUSINESS

The subsequent quarter though started on the positive note as unlike the previous

quarter the share prices of Boral Ltd opened positively at 5.75% against the lowly all ordinary

index of 2.48% (Chadha 2018). In the subsequent month of May, the second quarter of 2016

reported a lower share prices but stood positively against the negatively standing all ordinary

index of -2.52. The quarter ending month of June recorded a much volatile share price

movement as the shares of Boral Ltd stood negatively at 6.98% against the positive all

ordinary index of 6.28%. The third quarter of 2016 stood relatively tentative with share price

of Boral Ltd climbing a mountain high of 9.74% highest then the any previous month against

negatively standing all ordinary index of -2.03 while in the subsequent month of August

reported a negatively standing share prices of 4.66%. Gauging into the share price movement

of Boral Ltd it can be stated that there are certain accusations where the share prices have

reflected volatility.

Greater amount of volatility was recorded during the final quarter of 2016 where the

share prices of Boral Ltd dipped as low as -14.15% against the positively standing all

ordinary index of 3.94% (Editorial 2018). However the company reported a positive share

price movement in the final quarter ending of December 2016 where the share prices of Boral

Ltd stood second highest of 8.20% after recording a previous highest of 9.74% in the opening

third quarter of July.

Moving fast forward to the following year of 2017 the share prices of Boral Ltd stood

relatively less volatile except on certain occasion’s primary due to the market forces

(Finance.yahoo.com 2018). The share price of Boral Ltd for the opening month of January

2017 stood positively at 5.73% against the lowly standing all ordinary index of 1.52%.

Though first quarter of 2017 began strongly but the share prices of Boral Ltd dipped to stand

negatively at -1.02 against the lowly standing all ordinary index of 0.74% (Squartini et al.

The subsequent quarter though started on the positive note as unlike the previous

quarter the share prices of Boral Ltd opened positively at 5.75% against the lowly all ordinary

index of 2.48% (Chadha 2018). In the subsequent month of May, the second quarter of 2016

reported a lower share prices but stood positively against the negatively standing all ordinary

index of -2.52. The quarter ending month of June recorded a much volatile share price

movement as the shares of Boral Ltd stood negatively at 6.98% against the positive all

ordinary index of 6.28%. The third quarter of 2016 stood relatively tentative with share price

of Boral Ltd climbing a mountain high of 9.74% highest then the any previous month against

negatively standing all ordinary index of -2.03 while in the subsequent month of August

reported a negatively standing share prices of 4.66%. Gauging into the share price movement

of Boral Ltd it can be stated that there are certain accusations where the share prices have

reflected volatility.

Greater amount of volatility was recorded during the final quarter of 2016 where the

share prices of Boral Ltd dipped as low as -14.15% against the positively standing all

ordinary index of 3.94% (Editorial 2018). However the company reported a positive share

price movement in the final quarter ending of December 2016 where the share prices of Boral

Ltd stood second highest of 8.20% after recording a previous highest of 9.74% in the opening

third quarter of July.

Moving fast forward to the following year of 2017 the share prices of Boral Ltd stood

relatively less volatile except on certain occasion’s primary due to the market forces

(Finance.yahoo.com 2018). The share price of Boral Ltd for the opening month of January

2017 stood positively at 5.73% against the lowly standing all ordinary index of 1.52%.

Though first quarter of 2017 began strongly but the share prices of Boral Ltd dipped to stand

negatively at -1.02 against the lowly standing all ordinary index of 0.74% (Squartini et al.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR BUSINESS

2017). The company reported a strong second quarter of 2017 as the share prices represented

a strong trend in growth.

During the opening second quarter of April 2017 the share prices of Boral Ltd stood

strong at 6.01% against the negatively standing all ordinary index of -3.13%. The share prices

increased too strongly in the following month to stand at 9.53% which was the highest over

the span of 12 months (Newberry 2018). Though an instances of negative growth was

witnessed in the penultimate quarter of 2017 where the share price dipped to a low of -2.61

however in the final quarter of 2017 the share prices gained to close positively at 5.56%

against the low all ordinary index of 2.39%. Based on the above stated analysis it can be

stated the share price of Boral Ltd is moderately volatile.

Significant factors influencing the share price movement:

One of the significant that impacted the share price movement of the price is the

“change in the management focus” of acquisition of the US buildings products for an

amount of US $2.6. This resulted the shareholders to dump the shares based on the

uncertainty surrounding the acquisition (Simply Wall St 2018). An acquisition of such kind

results in creation of uncertainty among the shareholders that explains the probable reason for

influencing the share price of Boral Ltd.

Another factor that creates an influence on the share price movement of the Boral Ltd

is the “Management earnings forecast” the company recently announced the good news to

the shareholders with an increase in the half-yearly profits (Deegan 2013). This provides the

possible reason for a certain rise in the share price of Boral Ltd and might be forecasted

increase in the profits of the company in future may result in significant reaction among the

shareholders (McKay and Haque 2016).

2017). The company reported a strong second quarter of 2017 as the share prices represented

a strong trend in growth.

During the opening second quarter of April 2017 the share prices of Boral Ltd stood

strong at 6.01% against the negatively standing all ordinary index of -3.13%. The share prices

increased too strongly in the following month to stand at 9.53% which was the highest over

the span of 12 months (Newberry 2018). Though an instances of negative growth was

witnessed in the penultimate quarter of 2017 where the share price dipped to a low of -2.61

however in the final quarter of 2017 the share prices gained to close positively at 5.56%

against the low all ordinary index of 2.39%. Based on the above stated analysis it can be

stated the share price of Boral Ltd is moderately volatile.

Significant factors influencing the share price movement:

One of the significant that impacted the share price movement of the price is the

“change in the management focus” of acquisition of the US buildings products for an

amount of US $2.6. This resulted the shareholders to dump the shares based on the

uncertainty surrounding the acquisition (Simply Wall St 2018). An acquisition of such kind

results in creation of uncertainty among the shareholders that explains the probable reason for

influencing the share price of Boral Ltd.

Another factor that creates an influence on the share price movement of the Boral Ltd

is the “Management earnings forecast” the company recently announced the good news to

the shareholders with an increase in the half-yearly profits (Deegan 2013). This provides the

possible reason for a certain rise in the share price of Boral Ltd and might be forecasted

increase in the profits of the company in future may result in significant reaction among the

shareholders (McKay and Haque 2016).

11FINANCE FOR BUSINESS

The “macroeconomic factors” that contributed to the share price movement is the

slowing housing market (Zabarankin, Pavlikov and Uryasev 2014). With slowing amount of

housing market the share price declined on certain occasions however the infrastructure boom

in the US markets have steadied the ship but the share prices of Boral Ltd continue to

underperform against the other market players.

The “changes in the analyst forecast” is another factor that contributed to the share

price movement of the Boral Ltd (Scott 2015). In the report published analyst suggested

Boral as the crème of the large building and construction stocks with forecast share price of

$7.20 in the upcoming twelve months and earnings growth of 31% in the year 2017-18.

The factors suggest that Boral Ltd is a high growth stocks but the lower closing stock

price may some investors wondering whether to make investment in the shares of Boral Ltd

(Schaltegger and Burritt 2017). The investors may be attracted to the high growth potential in

the upcoming future that could be considered as one the viable reason for making an

investment in the shares of Boral Ltd.

Calculations of the Beta values and the anticipated Rates of Return using CAPM:

Calculated beta of the company:

The calculated beta for the Boral Ltd stood 1.18.

Computation of required rate of return for the company shares:

Particulars Amount

Beta of the company A 1.18

Risk Free Rate B 4%

Market Risk Premium C 6%

Required Rate of Return D=B+[AxC] 11.08%

The “macroeconomic factors” that contributed to the share price movement is the

slowing housing market (Zabarankin, Pavlikov and Uryasev 2014). With slowing amount of

housing market the share price declined on certain occasions however the infrastructure boom

in the US markets have steadied the ship but the share prices of Boral Ltd continue to

underperform against the other market players.

The “changes in the analyst forecast” is another factor that contributed to the share

price movement of the Boral Ltd (Scott 2015). In the report published analyst suggested

Boral as the crème of the large building and construction stocks with forecast share price of

$7.20 in the upcoming twelve months and earnings growth of 31% in the year 2017-18.

The factors suggest that Boral Ltd is a high growth stocks but the lower closing stock

price may some investors wondering whether to make investment in the shares of Boral Ltd

(Schaltegger and Burritt 2017). The investors may be attracted to the high growth potential in

the upcoming future that could be considered as one the viable reason for making an

investment in the shares of Boral Ltd.

Calculations of the Beta values and the anticipated Rates of Return using CAPM:

Calculated beta of the company:

The calculated beta for the Boral Ltd stood 1.18.

Computation of required rate of return for the company shares:

Particulars Amount

Beta of the company A 1.18

Risk Free Rate B 4%

Market Risk Premium C 6%

Required Rate of Return D=B+[AxC] 11.08%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.