Financial Statement Analysis Report: BONIA Corp vs PADINI Holdings

VerifiedAdded on 2021/04/17

|22

|3667

|190

Report

AI Summary

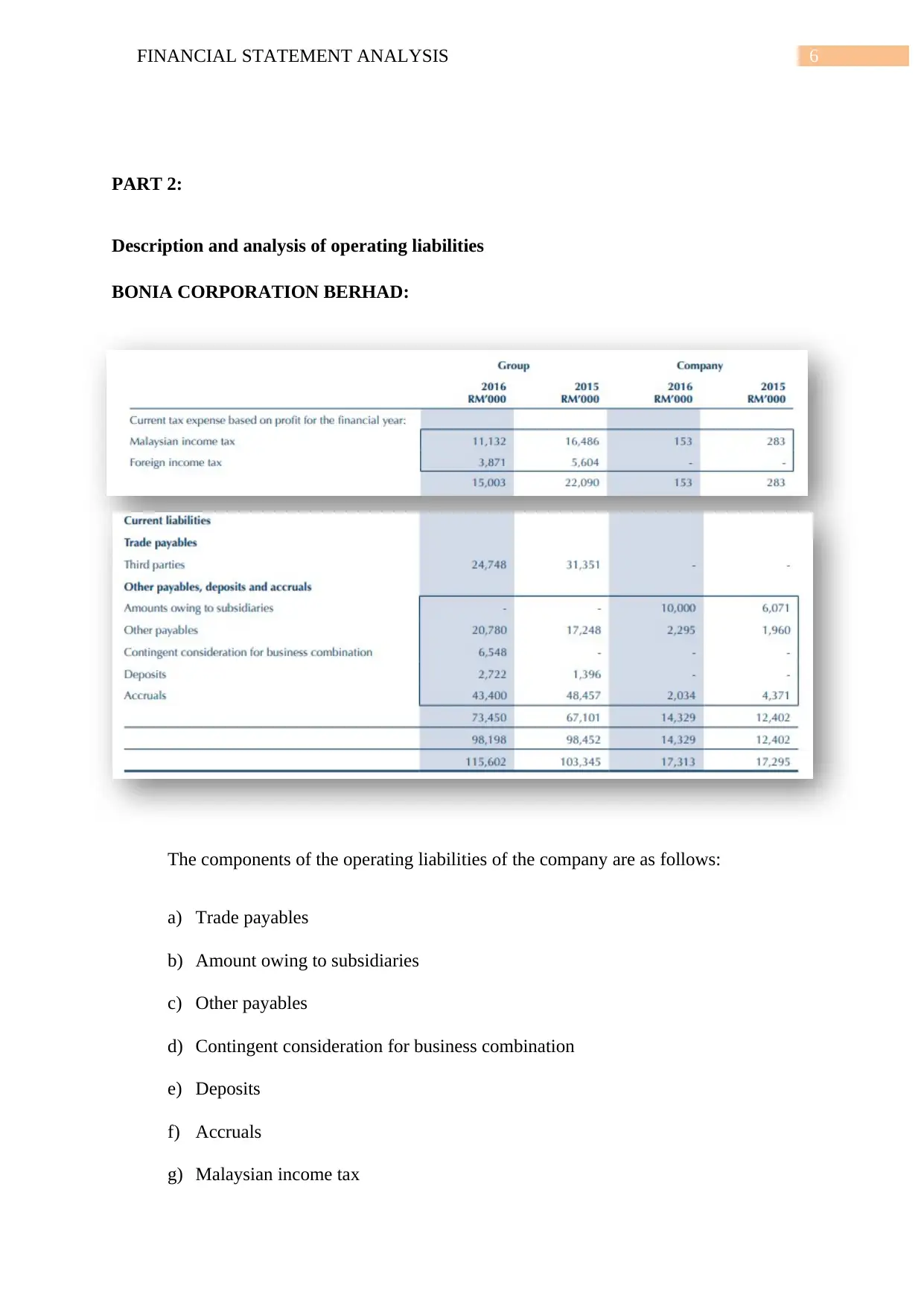

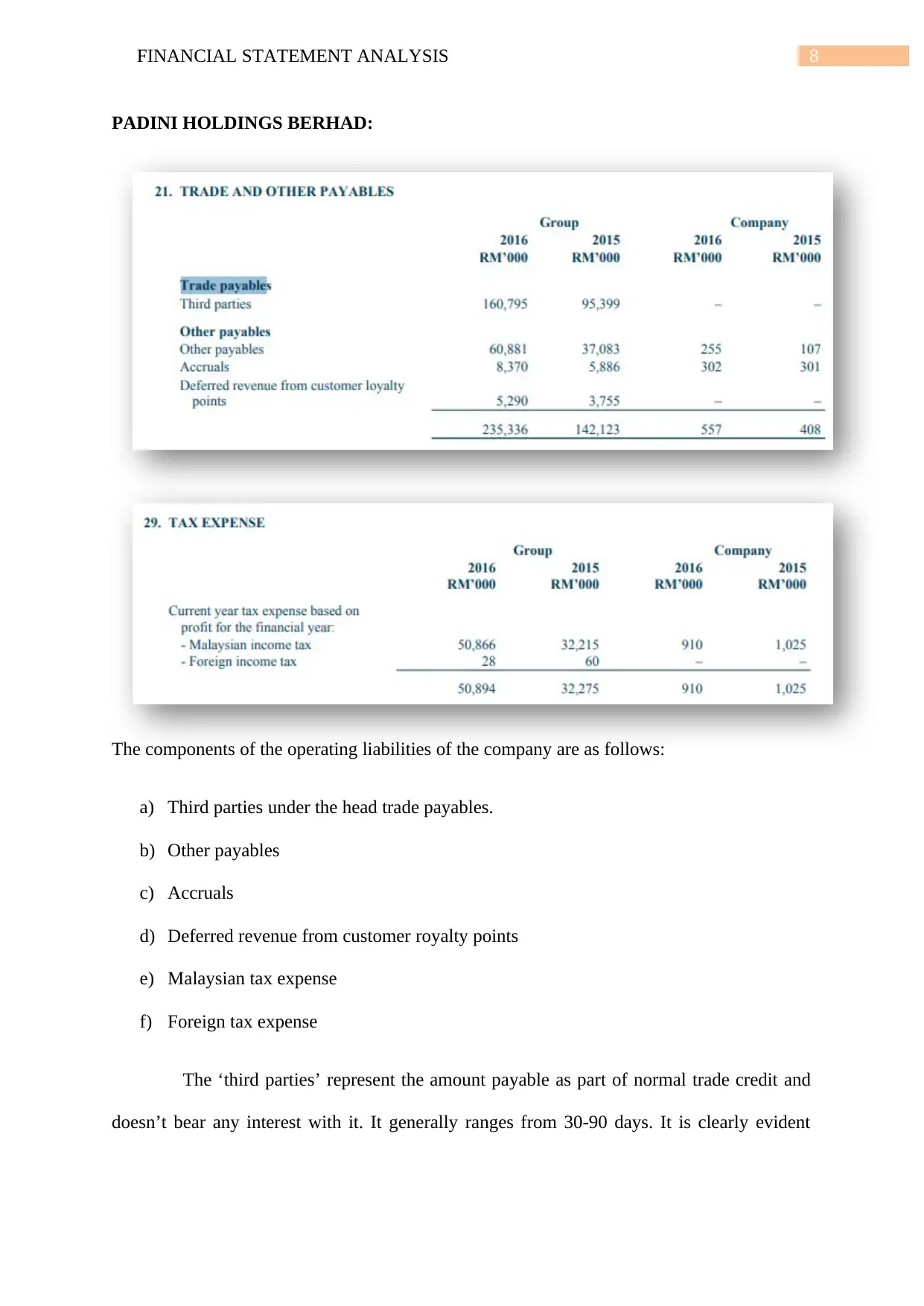

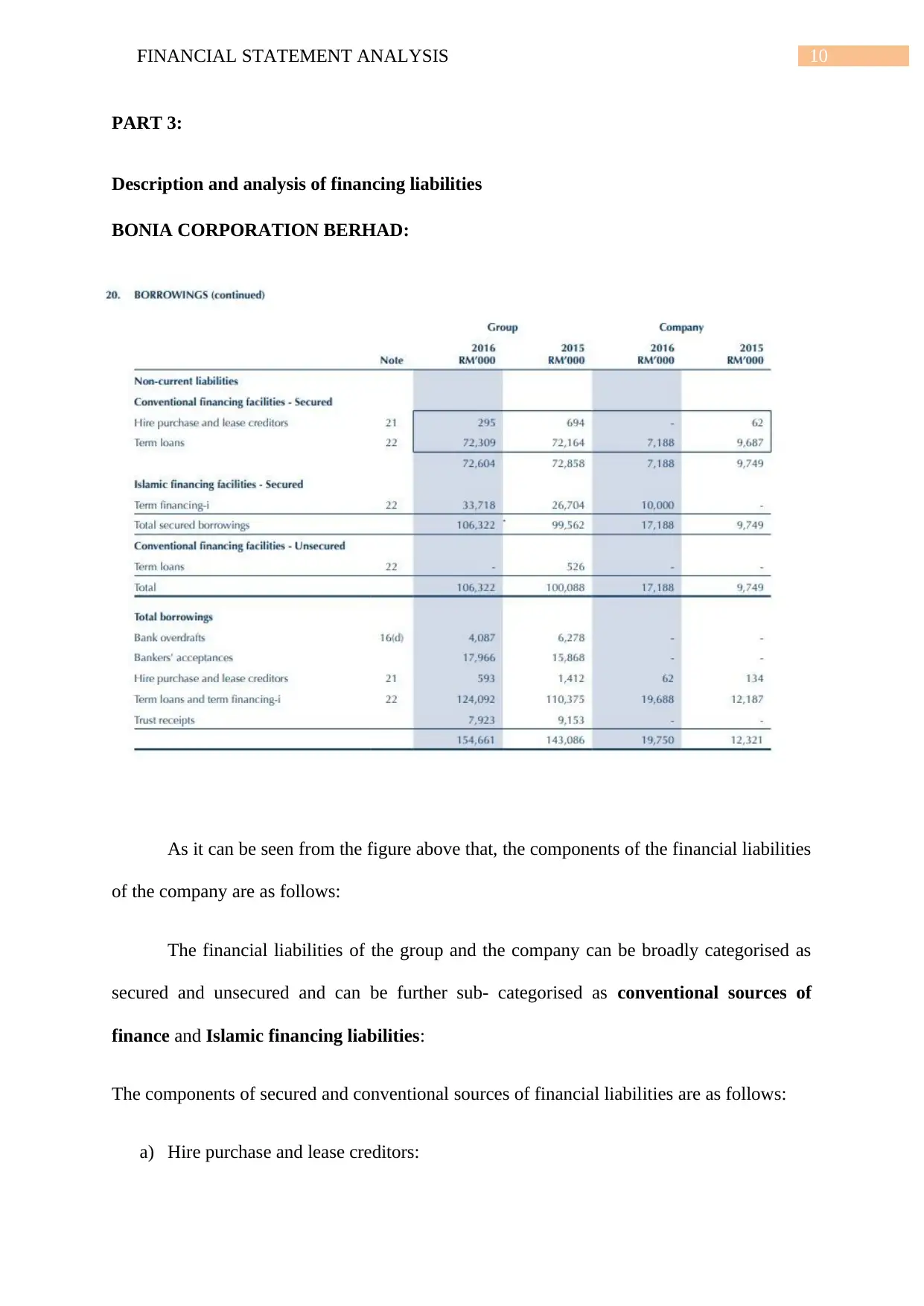

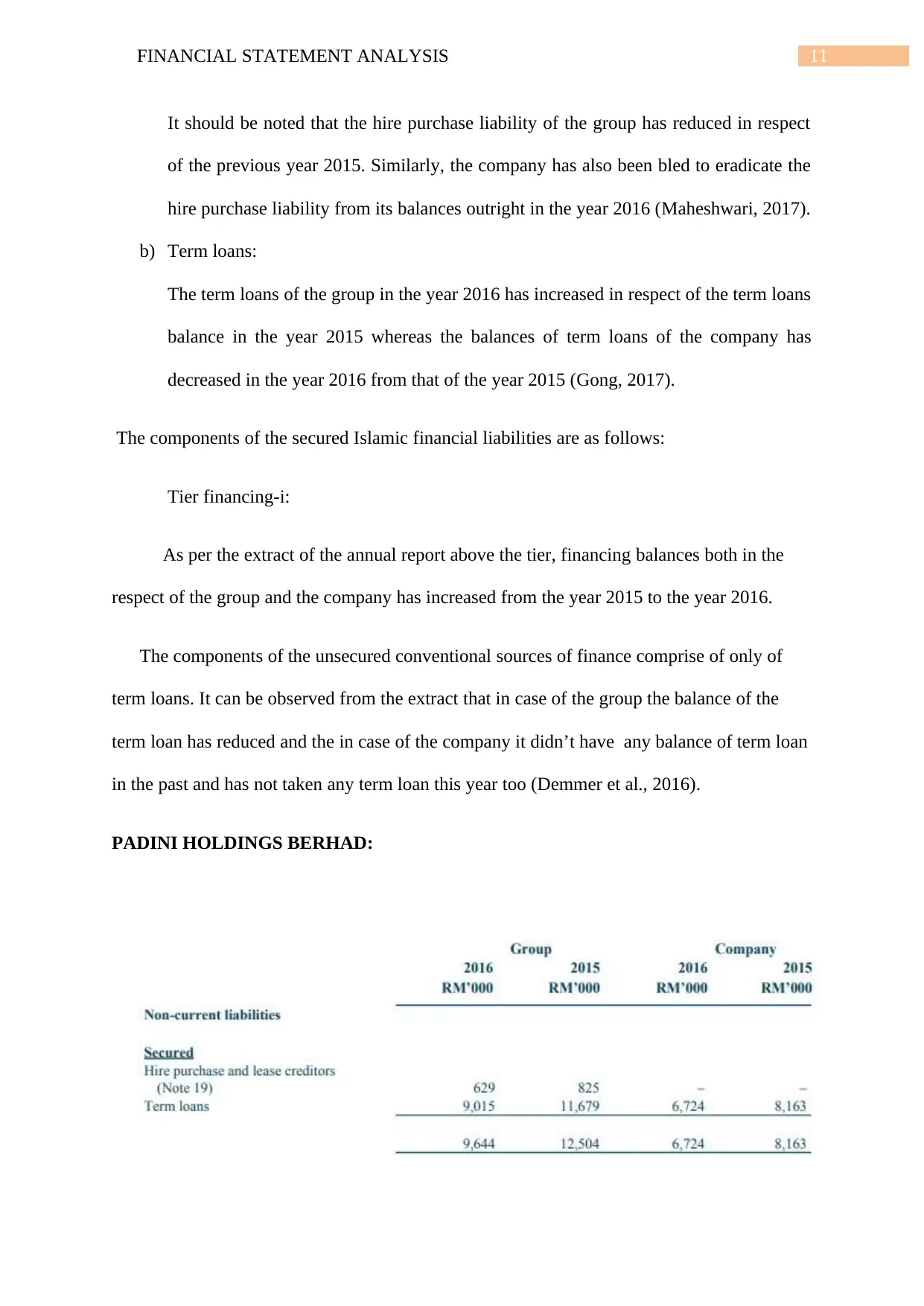

This report provides a comprehensive financial statement analysis of BONIA Corporation Berhad and PADINI Holdings Berhad. It begins with an introduction to both companies, outlining their business activities and corporate structures. The analysis then delves into the companies' operating liabilities, examining components such as trade payables, other payables, and income tax liabilities. Next, the report explores financing liabilities, categorizing them into secured and unsecured, as well as conventional and Islamic financing sources. The analysis covers hire purchase, term loans, and various types of financing. The report also assesses equity financing, including share capital, share premium, treasury shares, and retained earnings. Finally, it compares the financing activities of the two companies, highlighting key differences and similarities in their financial strategies. The report uses financial highlights and extracts from annual reports to support the analysis, providing a detailed overview of the companies' financial positions and performance.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.