HFR603 Hotel Finance: British Airways Investing Potential Analysis

VerifiedAdded on 2023/06/09

|24

|5092

|348

Case Study

AI Summary

This case study provides a financial analysis of British Airways, examining its investment potential over three years (2015-2017). It employs ratio analysis, including profitability, efficiency, liquidity, and capital structure ratios, to assess the company's financial health. Key ratios like return on assets, return on equity, profit margin, inventory turnover, current ratio, and debt-to-equity ratio are calculated and interpreted. The analysis identifies trends and discusses areas of financial risk, capital structure, and profitability. The report concludes with an evaluation of British Airways' financial standing and investment attractiveness. Desklib offers a range of solved assignments and past papers for students.

Running Head: Hotel Finance and revenue

1

Project Report: Hotel Finance and revenue

1

Project Report: Hotel Finance and revenue

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hotel Finance and revenue

2

Contents

Introduction.......................................................................................................................3

Company overview...........................................................................................................3

Analysis and Findings.......................................................................................................3

Profitability ratios.........................................................................................................4

Efficiency ratios............................................................................................................6

Liquidity ratios..............................................................................................................8

Capital structure ratios..................................................................................................9

Investor’s ratios..........................................................................................................10

Discussion.......................................................................................................................12

Conclusion and recommendation...................................................................................12

References.......................................................................................................................14

Appendix.........................................................................................................................16

2

Contents

Introduction.......................................................................................................................3

Company overview...........................................................................................................3

Analysis and Findings.......................................................................................................3

Profitability ratios.........................................................................................................4

Efficiency ratios............................................................................................................6

Liquidity ratios..............................................................................................................8

Capital structure ratios..................................................................................................9

Investor’s ratios..........................................................................................................10

Discussion.......................................................................................................................12

Conclusion and recommendation...................................................................................12

References.......................................................................................................................14

Appendix.........................................................................................................................16

Hotel Finance and revenue

3

Introduction:

Evaluation on the financial statement of an organization is a process that helps the

companies, professionals, investors and the other stakeholders to identify the real

performance of the company and make better choices about the performance and the

investment into the company. In this process, all the financial related entities such as budgets,

projects, financial statement, and financial transactions etc of the business is identified and

evaluated to reach over a conclusion. Basically, these studied are conducted by the different

parties for different purpose. In context with the investors, financial analysis process is done

to measure the stability level, profitability, liquidity, solvency etc level of the business to

make an investment decision into the company (Higgins, 2012). In context with the financial

manager, the financial statement of the company is studied to make an idea about the overall

performance of the company and make the changes into the current policy and strategy of the

company.

Financial analysis process includes various tools and techniques through which the

financial performance of an organization could be evaluated easily as well as the position of

the business could be maintained. In this report paper, ratio analysis, trend analysis etc study

has been conducted on “British airways” to reach over a conclusion about the investment into

the company.

Company overview:

“British airways” is an UK company which has been awarded as largest airline in

2017 in context with the fleet size. The operations and the activities of the company are

handled by the head office of the company which is situated at Waterside at London Heat. It

has been founded in the year of 1974 and from that, the company has merged with other

company to diversify the market and manage the performance of the company. the company

is offering its products and the services at international destinations which also include the

Australian destinations. The current report explains that the company is serving into approx

183 destinations (Home, 2018). The financial analysis and evaluation explains that the

company has faced various phases in last few years however the current performance of the

company has been stable.

Analysis and Findings:

3

Introduction:

Evaluation on the financial statement of an organization is a process that helps the

companies, professionals, investors and the other stakeholders to identify the real

performance of the company and make better choices about the performance and the

investment into the company. In this process, all the financial related entities such as budgets,

projects, financial statement, and financial transactions etc of the business is identified and

evaluated to reach over a conclusion. Basically, these studied are conducted by the different

parties for different purpose. In context with the investors, financial analysis process is done

to measure the stability level, profitability, liquidity, solvency etc level of the business to

make an investment decision into the company (Higgins, 2012). In context with the financial

manager, the financial statement of the company is studied to make an idea about the overall

performance of the company and make the changes into the current policy and strategy of the

company.

Financial analysis process includes various tools and techniques through which the

financial performance of an organization could be evaluated easily as well as the position of

the business could be maintained. In this report paper, ratio analysis, trend analysis etc study

has been conducted on “British airways” to reach over a conclusion about the investment into

the company.

Company overview:

“British airways” is an UK company which has been awarded as largest airline in

2017 in context with the fleet size. The operations and the activities of the company are

handled by the head office of the company which is situated at Waterside at London Heat. It

has been founded in the year of 1974 and from that, the company has merged with other

company to diversify the market and manage the performance of the company. the company

is offering its products and the services at international destinations which also include the

Australian destinations. The current report explains that the company is serving into approx

183 destinations (Home, 2018). The financial analysis and evaluation explains that the

company has faced various phases in last few years however the current performance of the

company has been stable.

Analysis and Findings:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Hotel Finance and revenue

4

The financial evaluation study has been done on the financial statement of “British

airways” to measure the financial performance and the financial changes of the company. the

study of ratio analysis has been done on the company initially to evaluate the stability,

profitability, liquidity, solvency etc level of the business to make an investment decision into

the company. In addition, this study has also been performed to measure the changes into the

financial performance of the company in last 3 years.

The study of ratio analysis is a technical and quantitative analysis that measures the

information and the idea about the financial performance, changes and the position of the

company (Gapenski & Reiter, 2008). This study is used by the investors as well as by the

companies to evaluates and measure the numerous aspect related to the financial performance

of the company. It further explains that how the company is performing in context with the

stability, profitability, liquidity, solvency level. The ratio analysis of British airways is as

follows:

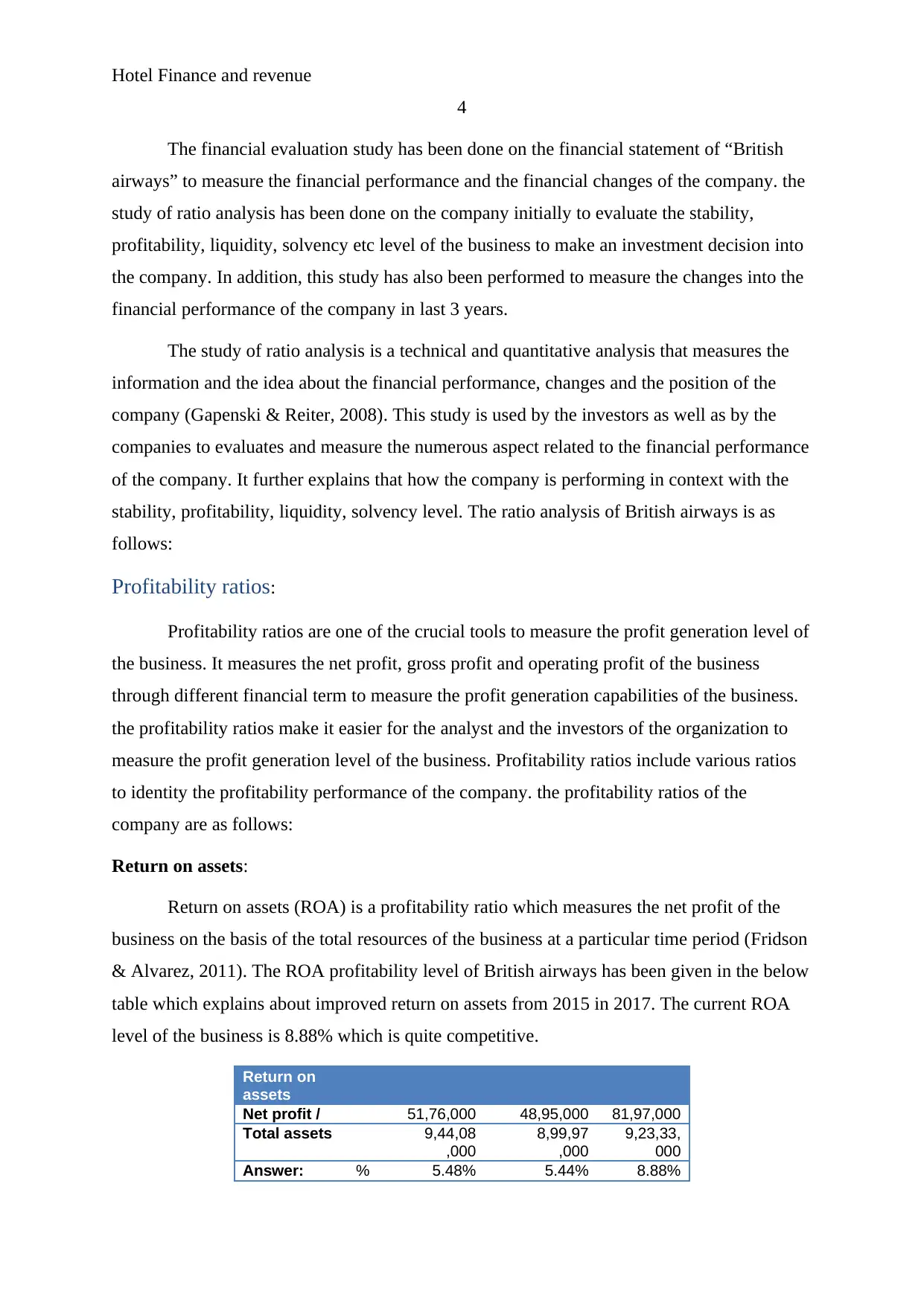

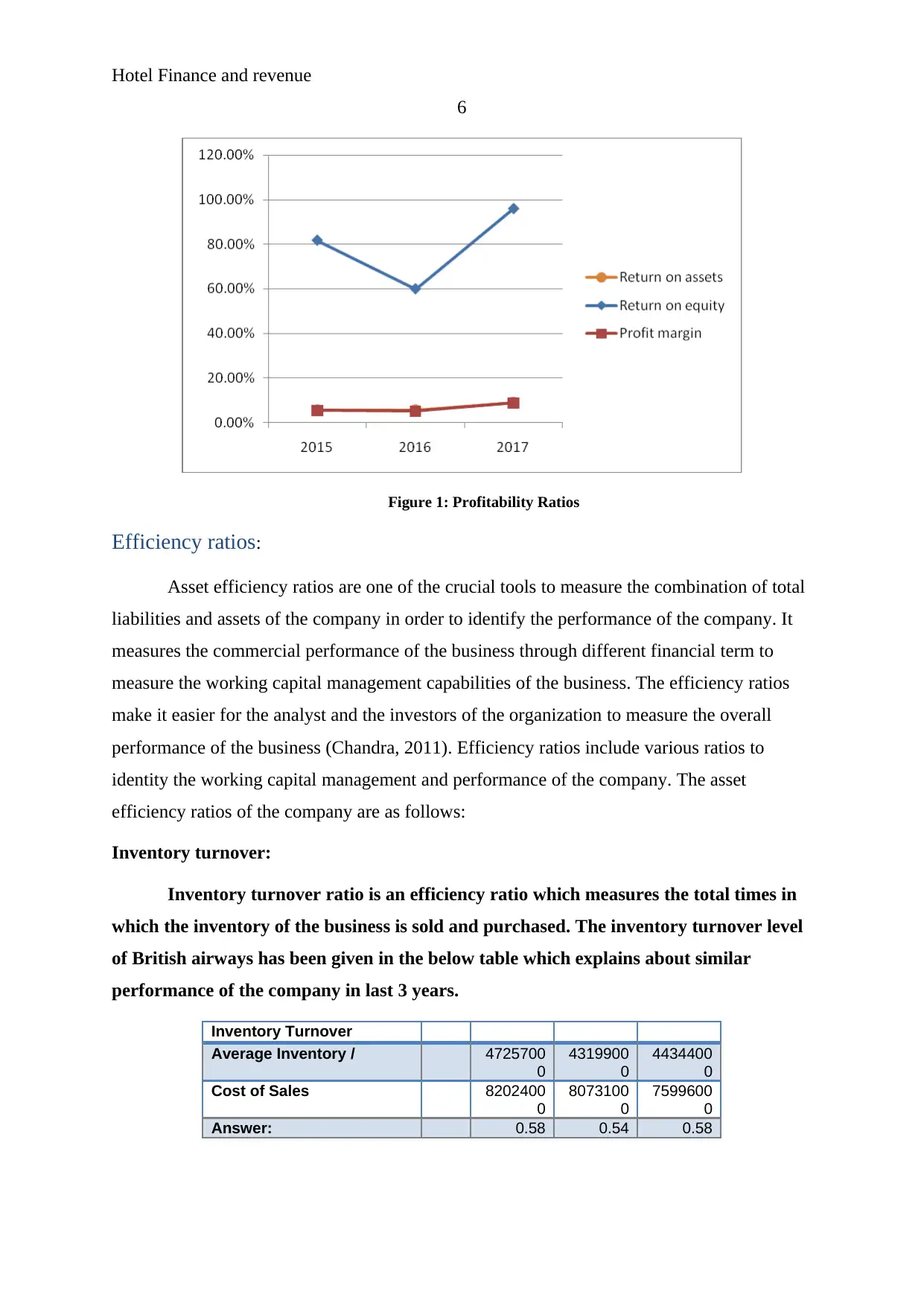

Profitability ratios:

Profitability ratios are one of the crucial tools to measure the profit generation level of

the business. It measures the net profit, gross profit and operating profit of the business

through different financial term to measure the profit generation capabilities of the business.

the profitability ratios make it easier for the analyst and the investors of the organization to

measure the profit generation level of the business. Profitability ratios include various ratios

to identity the profitability performance of the company. the profitability ratios of the

company are as follows:

Return on assets:

Return on assets (ROA) is a profitability ratio which measures the net profit of the

business on the basis of the total resources of the business at a particular time period (Fridson

& Alvarez, 2011). The ROA profitability level of British airways has been given in the below

table which explains about improved return on assets from 2015 in 2017. The current ROA

level of the business is 8.88% which is quite competitive.

Return on

assets

Net profit / 51,76,000 48,95,000 81,97,000

Total assets 9,44,08

,000

8,99,97

,000

9,23,33,

000

Answer: % 5.48% 5.44% 8.88%

4

The financial evaluation study has been done on the financial statement of “British

airways” to measure the financial performance and the financial changes of the company. the

study of ratio analysis has been done on the company initially to evaluate the stability,

profitability, liquidity, solvency etc level of the business to make an investment decision into

the company. In addition, this study has also been performed to measure the changes into the

financial performance of the company in last 3 years.

The study of ratio analysis is a technical and quantitative analysis that measures the

information and the idea about the financial performance, changes and the position of the

company (Gapenski & Reiter, 2008). This study is used by the investors as well as by the

companies to evaluates and measure the numerous aspect related to the financial performance

of the company. It further explains that how the company is performing in context with the

stability, profitability, liquidity, solvency level. The ratio analysis of British airways is as

follows:

Profitability ratios:

Profitability ratios are one of the crucial tools to measure the profit generation level of

the business. It measures the net profit, gross profit and operating profit of the business

through different financial term to measure the profit generation capabilities of the business.

the profitability ratios make it easier for the analyst and the investors of the organization to

measure the profit generation level of the business. Profitability ratios include various ratios

to identity the profitability performance of the company. the profitability ratios of the

company are as follows:

Return on assets:

Return on assets (ROA) is a profitability ratio which measures the net profit of the

business on the basis of the total resources of the business at a particular time period (Fridson

& Alvarez, 2011). The ROA profitability level of British airways has been given in the below

table which explains about improved return on assets from 2015 in 2017. The current ROA

level of the business is 8.88% which is quite competitive.

Return on

assets

Net profit / 51,76,000 48,95,000 81,97,000

Total assets 9,44,08

,000

8,99,97

,000

9,23,33,

000

Answer: % 5.48% 5.44% 8.88%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hotel Finance and revenue

5

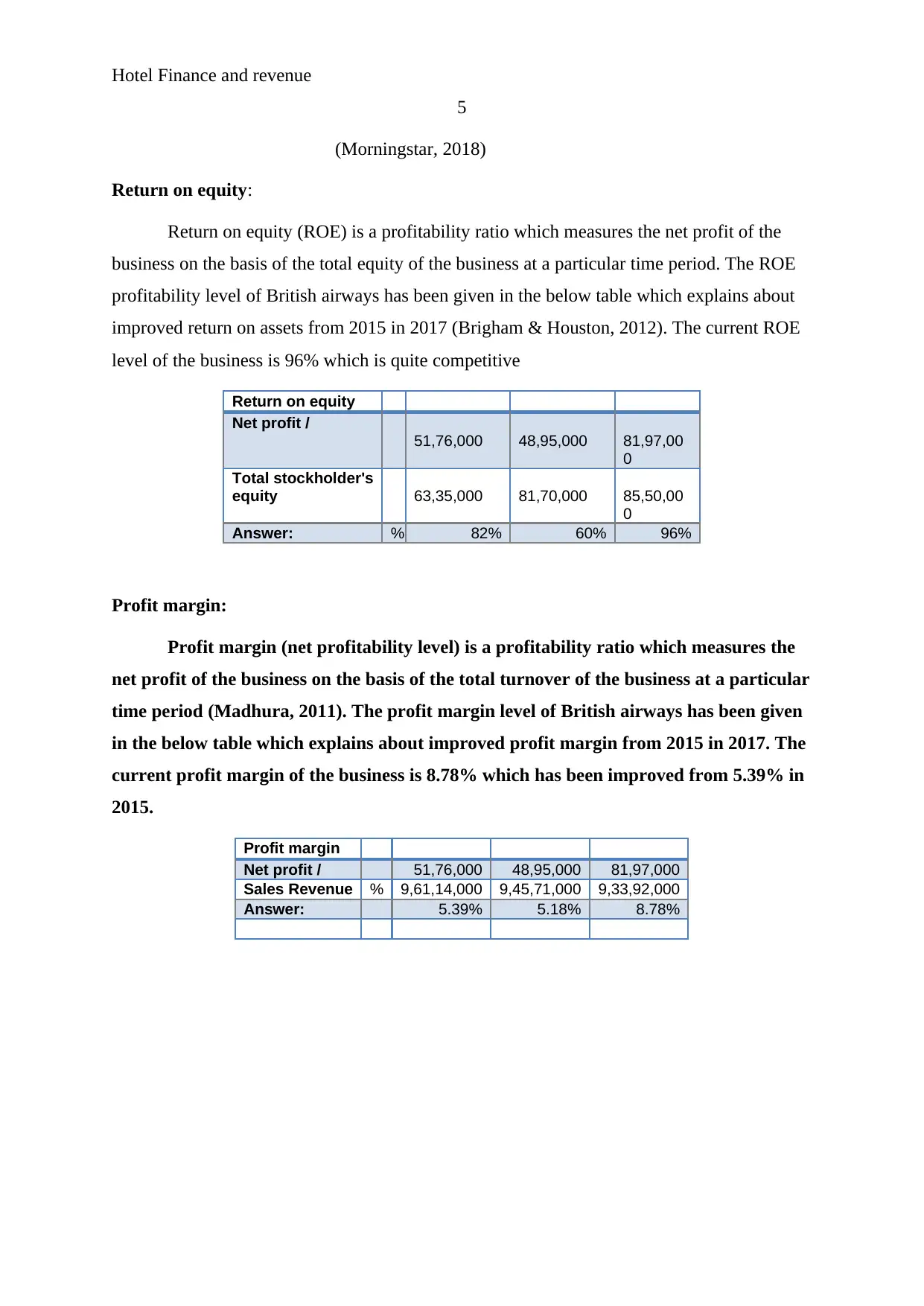

(Morningstar, 2018)

Return on equity:

Return on equity (ROE) is a profitability ratio which measures the net profit of the

business on the basis of the total equity of the business at a particular time period. The ROE

profitability level of British airways has been given in the below table which explains about

improved return on assets from 2015 in 2017 (Brigham & Houston, 2012). The current ROE

level of the business is 96% which is quite competitive

Return on equity

Net profit /

51,76,000 48,95,000 81,97,00

0

Total stockholder's

equity 63,35,000 81,70,000 85,50,00

0

Answer: % 82% 60% 96%

Profit margin:

Profit margin (net profitability level) is a profitability ratio which measures the

net profit of the business on the basis of the total turnover of the business at a particular

time period (Madhura, 2011). The profit margin level of British airways has been given

in the below table which explains about improved profit margin from 2015 in 2017. The

current profit margin of the business is 8.78% which has been improved from 5.39% in

2015.

Profit margin

Net profit / 51,76,000 48,95,000 81,97,000

Sales Revenue % 9,61,14,000 9,45,71,000 9,33,92,000

Answer: 5.39% 5.18% 8.78%

5

(Morningstar, 2018)

Return on equity:

Return on equity (ROE) is a profitability ratio which measures the net profit of the

business on the basis of the total equity of the business at a particular time period. The ROE

profitability level of British airways has been given in the below table which explains about

improved return on assets from 2015 in 2017 (Brigham & Houston, 2012). The current ROE

level of the business is 96% which is quite competitive

Return on equity

Net profit /

51,76,000 48,95,000 81,97,00

0

Total stockholder's

equity 63,35,000 81,70,000 85,50,00

0

Answer: % 82% 60% 96%

Profit margin:

Profit margin (net profitability level) is a profitability ratio which measures the

net profit of the business on the basis of the total turnover of the business at a particular

time period (Madhura, 2011). The profit margin level of British airways has been given

in the below table which explains about improved profit margin from 2015 in 2017. The

current profit margin of the business is 8.78% which has been improved from 5.39% in

2015.

Profit margin

Net profit / 51,76,000 48,95,000 81,97,000

Sales Revenue % 9,61,14,000 9,45,71,000 9,33,92,000

Answer: 5.39% 5.18% 8.78%

Hotel Finance and revenue

6

Figure 1: Profitability Ratios

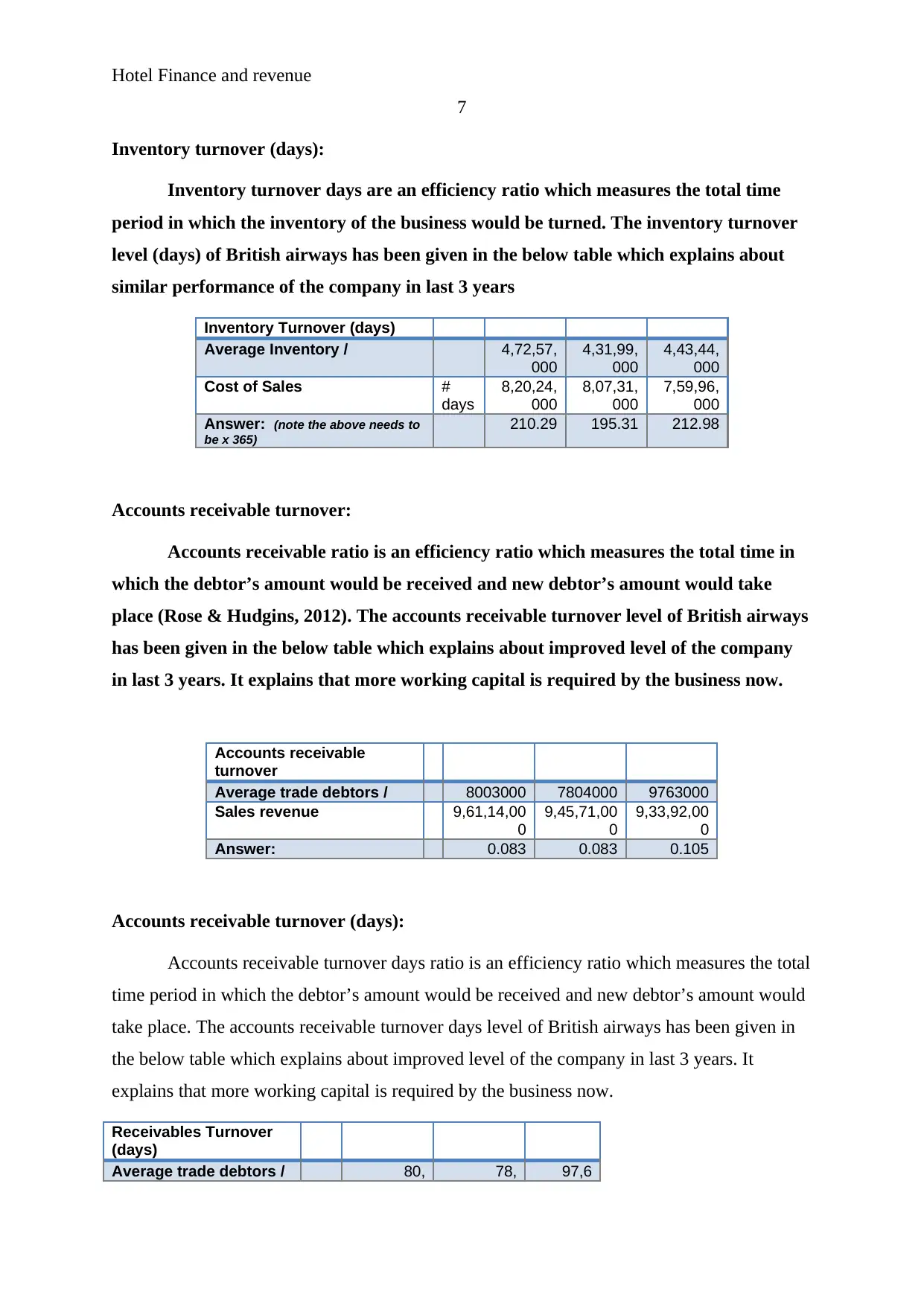

Efficiency ratios:

Asset efficiency ratios are one of the crucial tools to measure the combination of total

liabilities and assets of the company in order to identify the performance of the company. It

measures the commercial performance of the business through different financial term to

measure the working capital management capabilities of the business. The efficiency ratios

make it easier for the analyst and the investors of the organization to measure the overall

performance of the business (Chandra, 2011). Efficiency ratios include various ratios to

identity the working capital management and performance of the company. The asset

efficiency ratios of the company are as follows:

Inventory turnover:

Inventory turnover ratio is an efficiency ratio which measures the total times in

which the inventory of the business is sold and purchased. The inventory turnover level

of British airways has been given in the below table which explains about similar

performance of the company in last 3 years.

Inventory Turnover

Average Inventory / 4725700

0

4319900

0

4434400

0

Cost of Sales 8202400

0

8073100

0

7599600

0

Answer: 0.58 0.54 0.58

6

Figure 1: Profitability Ratios

Efficiency ratios:

Asset efficiency ratios are one of the crucial tools to measure the combination of total

liabilities and assets of the company in order to identify the performance of the company. It

measures the commercial performance of the business through different financial term to

measure the working capital management capabilities of the business. The efficiency ratios

make it easier for the analyst and the investors of the organization to measure the overall

performance of the business (Chandra, 2011). Efficiency ratios include various ratios to

identity the working capital management and performance of the company. The asset

efficiency ratios of the company are as follows:

Inventory turnover:

Inventory turnover ratio is an efficiency ratio which measures the total times in

which the inventory of the business is sold and purchased. The inventory turnover level

of British airways has been given in the below table which explains about similar

performance of the company in last 3 years.

Inventory Turnover

Average Inventory / 4725700

0

4319900

0

4434400

0

Cost of Sales 8202400

0

8073100

0

7599600

0

Answer: 0.58 0.54 0.58

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Hotel Finance and revenue

7

Inventory turnover (days):

Inventory turnover days are an efficiency ratio which measures the total time

period in which the inventory of the business would be turned. The inventory turnover

level (days) of British airways has been given in the below table which explains about

similar performance of the company in last 3 years

Inventory Turnover (days)

Average Inventory / 4,72,57,

000

4,31,99,

000

4,43,44,

000

Cost of Sales #

days

8,20,24,

000

8,07,31,

000

7,59,96,

000

Answer: (note the above needs to

be x 365)

210.29 195.31 212.98

Accounts receivable turnover:

Accounts receivable ratio is an efficiency ratio which measures the total time in

which the debtor’s amount would be received and new debtor’s amount would take

place (Rose & Hudgins, 2012). The accounts receivable turnover level of British airways

has been given in the below table which explains about improved level of the company

in last 3 years. It explains that more working capital is required by the business now.

Accounts receivable

turnover

Average trade debtors / 8003000 7804000 9763000

Sales revenue 9,61,14,00

0

9,45,71,00

0

9,33,92,00

0

Answer: 0.083 0.083 0.105

Accounts receivable turnover (days):

Accounts receivable turnover days ratio is an efficiency ratio which measures the total

time period in which the debtor’s amount would be received and new debtor’s amount would

take place. The accounts receivable turnover days level of British airways has been given in

the below table which explains about improved level of the company in last 3 years. It

explains that more working capital is required by the business now.

Receivables Turnover

(days)

Average trade debtors / 80, 78, 97,6

7

Inventory turnover (days):

Inventory turnover days are an efficiency ratio which measures the total time

period in which the inventory of the business would be turned. The inventory turnover

level (days) of British airways has been given in the below table which explains about

similar performance of the company in last 3 years

Inventory Turnover (days)

Average Inventory / 4,72,57,

000

4,31,99,

000

4,43,44,

000

Cost of Sales #

days

8,20,24,

000

8,07,31,

000

7,59,96,

000

Answer: (note the above needs to

be x 365)

210.29 195.31 212.98

Accounts receivable turnover:

Accounts receivable ratio is an efficiency ratio which measures the total time in

which the debtor’s amount would be received and new debtor’s amount would take

place (Rose & Hudgins, 2012). The accounts receivable turnover level of British airways

has been given in the below table which explains about improved level of the company

in last 3 years. It explains that more working capital is required by the business now.

Accounts receivable

turnover

Average trade debtors / 8003000 7804000 9763000

Sales revenue 9,61,14,00

0

9,45,71,00

0

9,33,92,00

0

Answer: 0.083 0.083 0.105

Accounts receivable turnover (days):

Accounts receivable turnover days ratio is an efficiency ratio which measures the total

time period in which the debtor’s amount would be received and new debtor’s amount would

take place. The accounts receivable turnover days level of British airways has been given in

the below table which explains about improved level of the company in last 3 years. It

explains that more working capital is required by the business now.

Receivables Turnover

(days)

Average trade debtors / 80, 78, 97,6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hotel Finance and revenue

8

03,000 04,000 3,000

Sales revenue (note used

operating revenue)

#

da

ys

9,61

,14,000

9,45

,71,000

9,33,

92,000

Answer: (note the above

needs to be x 365)

30.39 30.12 38.16

Figure 2: Efficiency Ratios

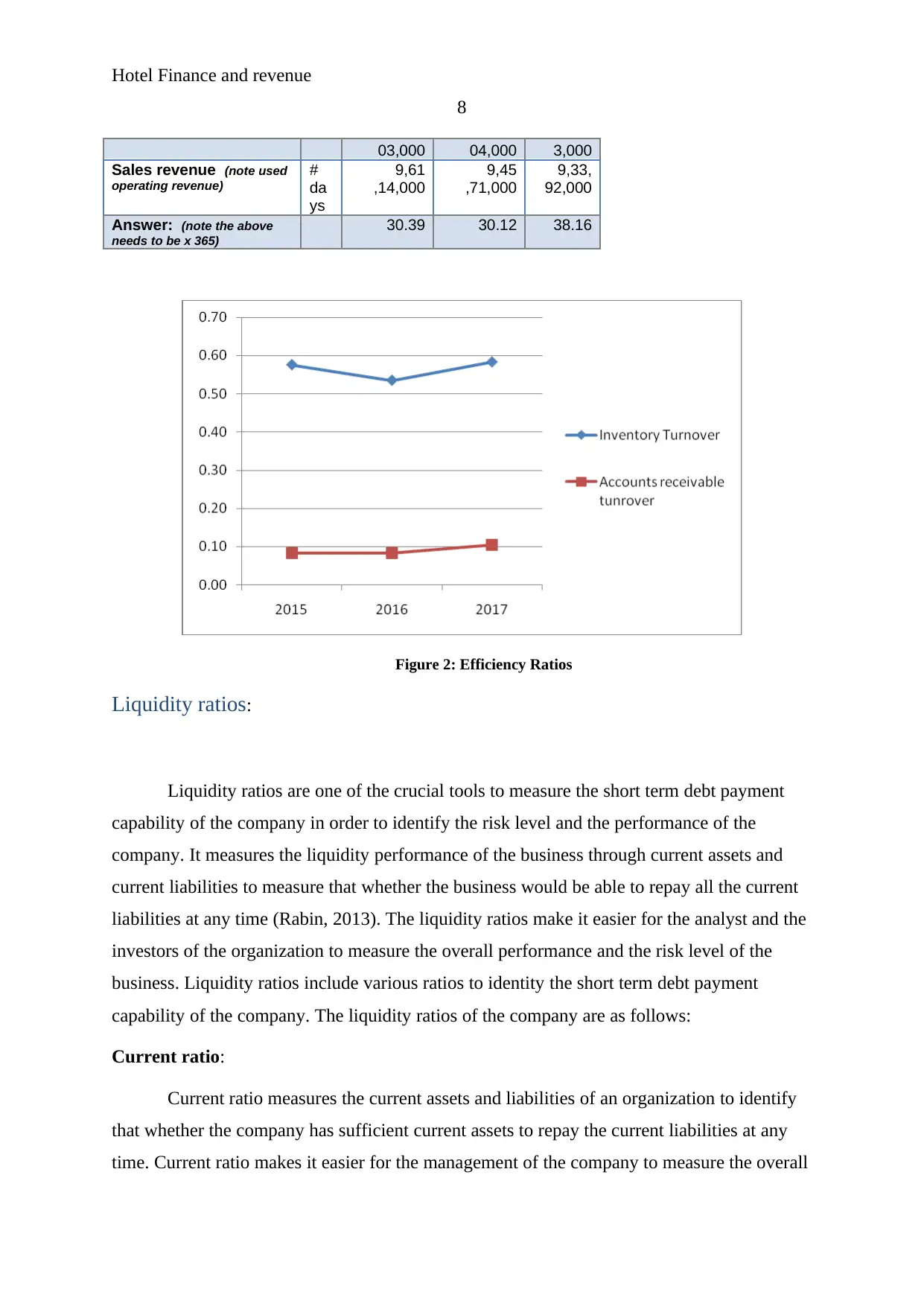

Liquidity ratios:

Liquidity ratios are one of the crucial tools to measure the short term debt payment

capability of the company in order to identify the risk level and the performance of the

company. It measures the liquidity performance of the business through current assets and

current liabilities to measure that whether the business would be able to repay all the current

liabilities at any time (Rabin, 2013). The liquidity ratios make it easier for the analyst and the

investors of the organization to measure the overall performance and the risk level of the

business. Liquidity ratios include various ratios to identity the short term debt payment

capability of the company. The liquidity ratios of the company are as follows:

Current ratio:

Current ratio measures the current assets and liabilities of an organization to identify

that whether the company has sufficient current assets to repay the current liabilities at any

time. Current ratio makes it easier for the management of the company to measure the overall

8

03,000 04,000 3,000

Sales revenue (note used

operating revenue)

#

da

ys

9,61

,14,000

9,45

,71,000

9,33,

92,000

Answer: (note the above

needs to be x 365)

30.39 30.12 38.16

Figure 2: Efficiency Ratios

Liquidity ratios:

Liquidity ratios are one of the crucial tools to measure the short term debt payment

capability of the company in order to identify the risk level and the performance of the

company. It measures the liquidity performance of the business through current assets and

current liabilities to measure that whether the business would be able to repay all the current

liabilities at any time (Rabin, 2013). The liquidity ratios make it easier for the analyst and the

investors of the organization to measure the overall performance and the risk level of the

business. Liquidity ratios include various ratios to identity the short term debt payment

capability of the company. The liquidity ratios of the company are as follows:

Current ratio:

Current ratio measures the current assets and liabilities of an organization to identify

that whether the company has sufficient current assets to repay the current liabilities at any

time. Current ratio makes it easier for the management of the company to measure the overall

Hotel Finance and revenue

9

performance of the company. the current ratio of the company explains about lowered

performance in current year. However, the company could repay the amount easily to the

creditors of the company.

Current Ratio

Current Assets / 6,82,34,00

0

6,24,88,00

0

6,51,61,00

0

Current liabilities 5,04,12,00

0

5,01,34,00

0

5,62,69,00

0

Answer: 1.35 1.25 1.16

Quick ratio:

Quick ratio measures the quick assets and liabilities of an organization to identify that

whether the company has sufficient quick assets to repay the current liabilities at any time.

The quick ratio of the company explains about lowered performance in current year (Porcelli

& Delgado, 2009). It explains that the risk level of the company is higher and company is

required to improve the level of the assets to manage the performance.

Quick ratio

Current Assets -

Inventory /

2,09,77,00

0

1,92,89,00

0

2,08,17,00

0

Current Liabilities 5,04,12,00

0

5,01,34,00

0

5,62,69,00

0

Answer: 0.42 0.38 0.37

Figure 3: Liquidity ratio

9

performance of the company. the current ratio of the company explains about lowered

performance in current year. However, the company could repay the amount easily to the

creditors of the company.

Current Ratio

Current Assets / 6,82,34,00

0

6,24,88,00

0

6,51,61,00

0

Current liabilities 5,04,12,00

0

5,01,34,00

0

5,62,69,00

0

Answer: 1.35 1.25 1.16

Quick ratio:

Quick ratio measures the quick assets and liabilities of an organization to identify that

whether the company has sufficient quick assets to repay the current liabilities at any time.

The quick ratio of the company explains about lowered performance in current year (Porcelli

& Delgado, 2009). It explains that the risk level of the company is higher and company is

required to improve the level of the assets to manage the performance.

Quick ratio

Current Assets -

Inventory /

2,09,77,00

0

1,92,89,00

0

2,08,17,00

0

Current Liabilities 5,04,12,00

0

5,01,34,00

0

5,62,69,00

0

Answer: 0.42 0.38 0.37

Figure 3: Liquidity ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Hotel Finance and revenue

10

(Morningstar, 2018)

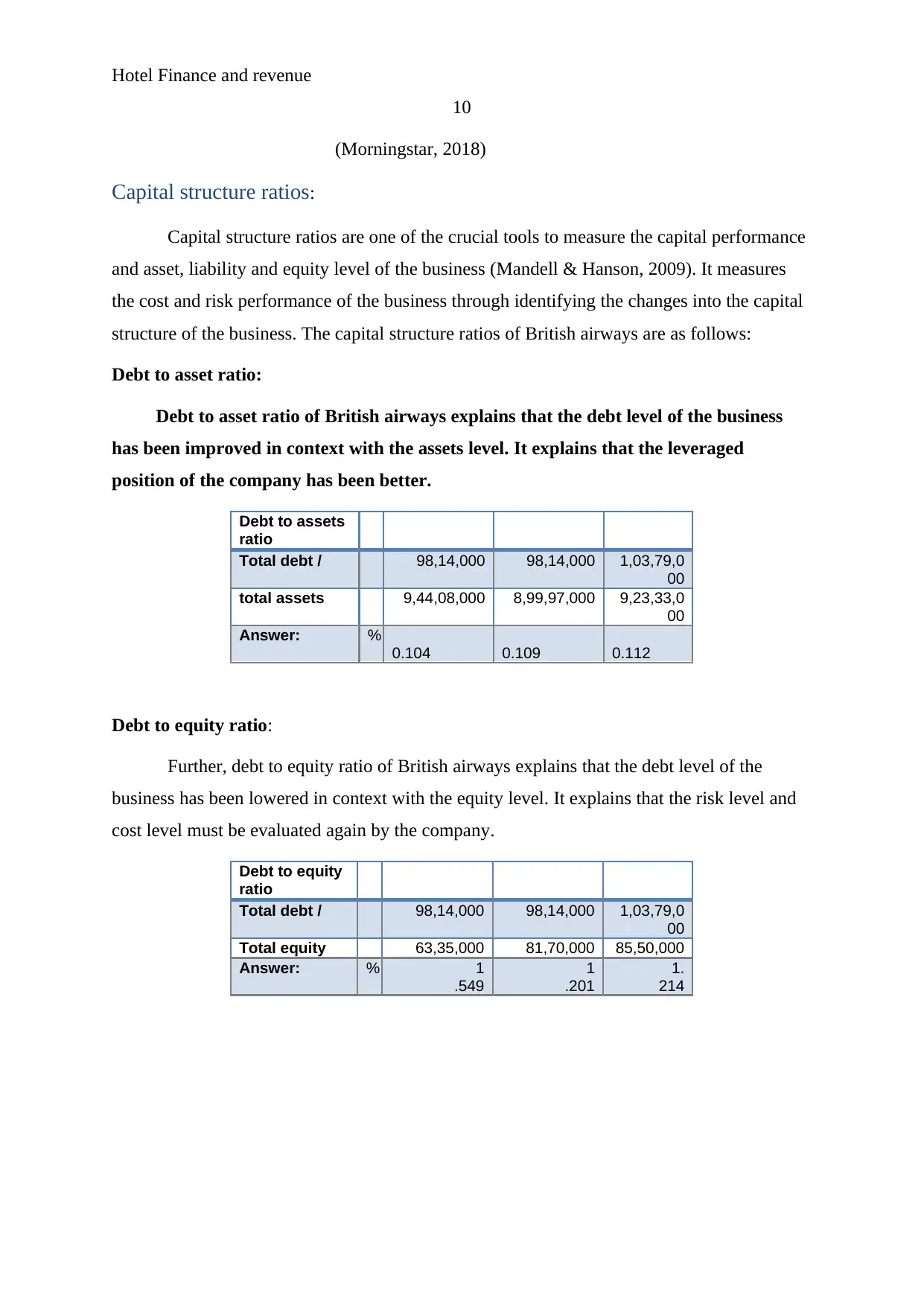

Capital structure ratios:

Capital structure ratios are one of the crucial tools to measure the capital performance

and asset, liability and equity level of the business (Mandell & Hanson, 2009). It measures

the cost and risk performance of the business through identifying the changes into the capital

structure of the business. The capital structure ratios of British airways are as follows:

Debt to asset ratio:

Debt to asset ratio of British airways explains that the debt level of the business

has been improved in context with the assets level. It explains that the leveraged

position of the company has been better.

Debt to assets

ratio

Total debt / 98,14,000 98,14,000 1,03,79,0

00

total assets 9,44,08,000 8,99,97,000 9,23,33,0

00

Answer: %

0.104 0.109 0.112

Debt to equity ratio:

Further, debt to equity ratio of British airways explains that the debt level of the

business has been lowered in context with the equity level. It explains that the risk level and

cost level must be evaluated again by the company.

Debt to equity

ratio

Total debt / 98,14,000 98,14,000 1,03,79,0

00

Total equity 63,35,000 81,70,000 85,50,000

Answer: % 1

.549

1

.201

1.

214

10

(Morningstar, 2018)

Capital structure ratios:

Capital structure ratios are one of the crucial tools to measure the capital performance

and asset, liability and equity level of the business (Mandell & Hanson, 2009). It measures

the cost and risk performance of the business through identifying the changes into the capital

structure of the business. The capital structure ratios of British airways are as follows:

Debt to asset ratio:

Debt to asset ratio of British airways explains that the debt level of the business

has been improved in context with the assets level. It explains that the leveraged

position of the company has been better.

Debt to assets

ratio

Total debt / 98,14,000 98,14,000 1,03,79,0

00

total assets 9,44,08,000 8,99,97,000 9,23,33,0

00

Answer: %

0.104 0.109 0.112

Debt to equity ratio:

Further, debt to equity ratio of British airways explains that the debt level of the

business has been lowered in context with the equity level. It explains that the risk level and

cost level must be evaluated again by the company.

Debt to equity

ratio

Total debt / 98,14,000 98,14,000 1,03,79,0

00

Total equity 63,35,000 81,70,000 85,50,000

Answer: % 1

.549

1

.201

1.

214

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hotel Finance and revenue

11

Figure 4: Debt to equity ratio

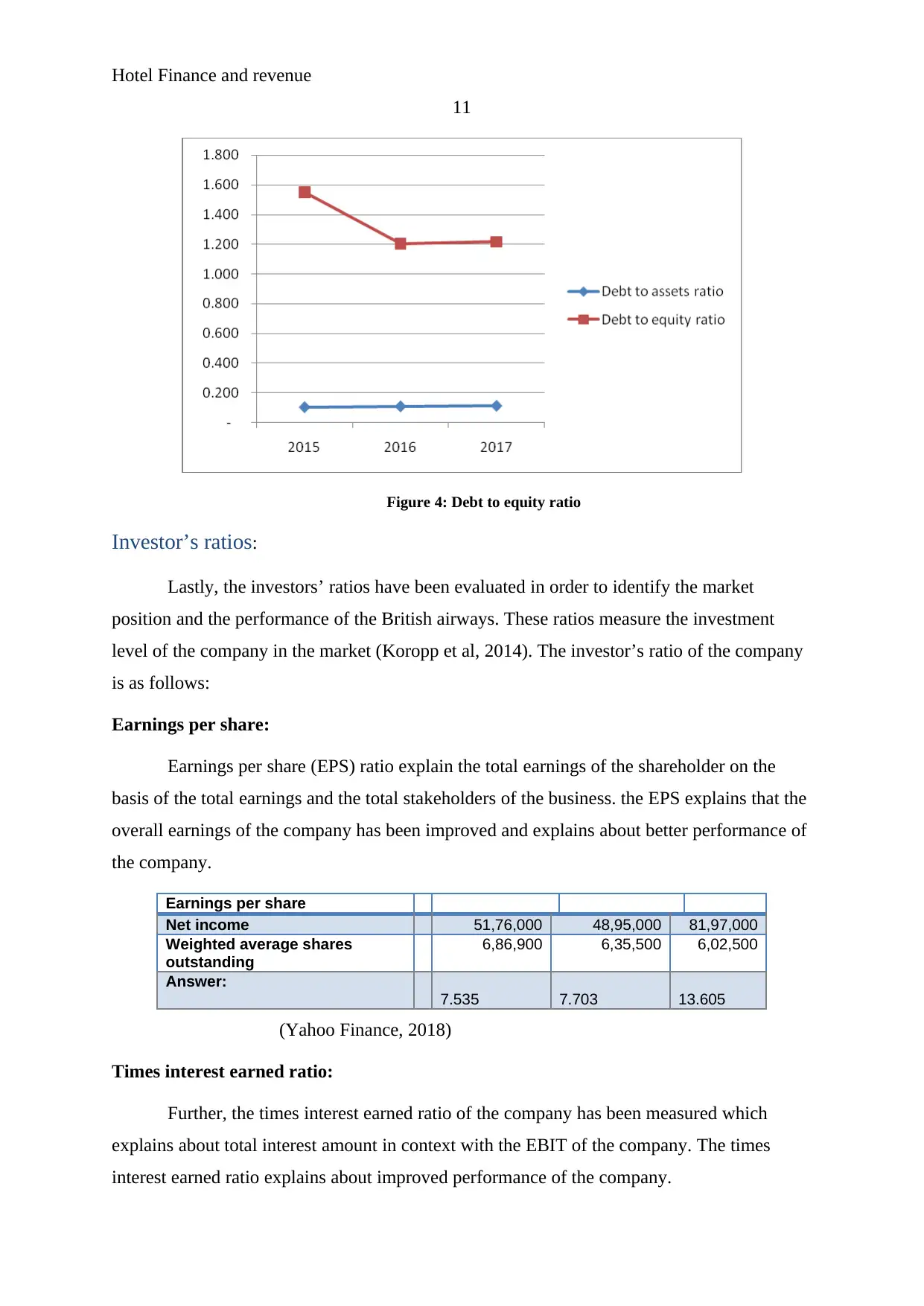

Investor’s ratios:

Lastly, the investors’ ratios have been evaluated in order to identify the market

position and the performance of the British airways. These ratios measure the investment

level of the company in the market (Koropp et al, 2014). The investor’s ratio of the company

is as follows:

Earnings per share:

Earnings per share (EPS) ratio explain the total earnings of the shareholder on the

basis of the total earnings and the total stakeholders of the business. the EPS explains that the

overall earnings of the company has been improved and explains about better performance of

the company.

Earnings per share

Net income 51,76,000 48,95,000 81,97,000

Weighted average shares

outstanding

6,86,900 6,35,500 6,02,500

Answer:

7.535 7.703 13.605

(Yahoo Finance, 2018)

Times interest earned ratio:

Further, the times interest earned ratio of the company has been measured which

explains about total interest amount in context with the EBIT of the company. The times

interest earned ratio explains about improved performance of the company.

11

Figure 4: Debt to equity ratio

Investor’s ratios:

Lastly, the investors’ ratios have been evaluated in order to identify the market

position and the performance of the British airways. These ratios measure the investment

level of the company in the market (Koropp et al, 2014). The investor’s ratio of the company

is as follows:

Earnings per share:

Earnings per share (EPS) ratio explain the total earnings of the shareholder on the

basis of the total earnings and the total stakeholders of the business. the EPS explains that the

overall earnings of the company has been improved and explains about better performance of

the company.

Earnings per share

Net income 51,76,000 48,95,000 81,97,000

Weighted average shares

outstanding

6,86,900 6,35,500 6,02,500

Answer:

7.535 7.703 13.605

(Yahoo Finance, 2018)

Times interest earned ratio:

Further, the times interest earned ratio of the company has been measured which

explains about total interest amount in context with the EBIT of the company. The times

interest earned ratio explains about improved performance of the company.

Hotel Finance and revenue

12

Times interest

earned ratio

EBIT / 72,34,000 55,97,000 1,01,23,0

00

Interest payable 3,39,000 3,65,000 4,30,000

Answer: 2

1.339

1

5.334

23

.542

Figure 5: Investor's ratios

Discussion:

The above calculations and the analysis on the British airways explain that the

company has faced various phases in last 3 years. Various levels of the business have been

measured of last 3 years to identify the overall performance of the company. Firstly, the

profitability position of the company has been studied and it has been found that the overall

profit generation capabilities of the company have been improved. However, it has also been

estimated that the operating expenses of the company are quite higher and due to which the

net profits of the company are lower (DemaMoreno, 2009). If the organization would control

on these expenses than the overall performance of the business would be better in terms of

profitability.

Further, the efficiency ratios have been evaluated and it has been found that the

overall ratios of the company explain that the high working capital is required by the

company in current year to manage the performance of the company. It explains that few

12

Times interest

earned ratio

EBIT / 72,34,000 55,97,000 1,01,23,0

00

Interest payable 3,39,000 3,65,000 4,30,000

Answer: 2

1.339

1

5.334

23

.542

Figure 5: Investor's ratios

Discussion:

The above calculations and the analysis on the British airways explain that the

company has faced various phases in last 3 years. Various levels of the business have been

measured of last 3 years to identify the overall performance of the company. Firstly, the

profitability position of the company has been studied and it has been found that the overall

profit generation capabilities of the company have been improved. However, it has also been

estimated that the operating expenses of the company are quite higher and due to which the

net profits of the company are lower (DemaMoreno, 2009). If the organization would control

on these expenses than the overall performance of the business would be better in terms of

profitability.

Further, the efficiency ratios have been evaluated and it has been found that the

overall ratios of the company explain that the high working capital is required by the

company in current year to manage the performance of the company. It explains that few

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.