Masters in Finance for Business: Company Financial Analysis Report

VerifiedAdded on 2020/05/28

|16

|3410

|55

Report

AI Summary

This report presents a comprehensive financial analysis of Caltex Australia Limited. It begins with a description of the company, followed by an examination of its ownership structure and governance. The report then delves into key financial ratios such as Return on Assets (ROA) and Return on Equity (ROE), providing calculations and interpretations. Analysis of stock movements from the ASX website is included, along with recent company announcements. The calculation of the Weighted Average Cost of Capital (WACC) is presented, along with its implications for management. The report also explores the optimal debt structure and dividend policy of the company, culminating in a final recommendation. The document is a student assignment intended for academic purposes.

Running head: FINANCE FOR BUSINESS - MASTERS

Finance for business – Masters

Name of the student

Name of the university

Author note

Finance for business – Masters

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR BUSINESS – MASTERS

Table of Contents

1. Description of the company................................................................................................2

2. Specification of the structure of ownership governance.....................................................2

3. Key ratios of Caltex............................................................................................................3

4. Information from ASX website..........................................................................................5

5. Recent announcement.........................................................................................................8

6. Stock field...........................................................................................................................8

7. WACC (weighted average cost of capital).........................................................................9

8. Optimal debt structure......................................................................................................11

9. Dividend policy.................................................................................................................12

10. Recommendation...............................................................................................................12

Reference..................................................................................................................................14

Table of Contents

1. Description of the company................................................................................................2

2. Specification of the structure of ownership governance.....................................................2

3. Key ratios of Caltex............................................................................................................3

4. Information from ASX website..........................................................................................5

5. Recent announcement.........................................................................................................8

6. Stock field...........................................................................................................................8

7. WACC (weighted average cost of capital).........................................................................9

8. Optimal debt structure......................................................................................................11

9. Dividend policy.................................................................................................................12

10. Recommendation...............................................................................................................12

Reference..................................................................................................................................14

2FINANCE FOR BUSINESS – MASTERS

1. Description of the company

Caltex Australia limited is the convenience retailer and transport fuel supplier

company based in Australia. Caltex is engaged in business of refining, purchasing, marketing,

distributing the petroleum products and operating the convenience stores all over Australia. It

operates through 2 segments that include Lytton and Supply and Marketing. The supply and

marketing division is the integrated supply chain for transport fuel and it delivers refined

products in international market and sells the lubricants, Caltex fuels and it has speciality

with regard to the convenience store goods and products through national network of Caltex

Woolworths, Caltex and the branded service stations of Ampol along with through non-

equity and company owned resellers and through direct sales. During the year 2016, the

company had 3166 employees in Australia that includes the employees from all the

subsidiaries under the control of the company (Caltex 2017).

2. Specification of the structure of ownership governance

i) Major substantial shareholders

More than 20% holding of shares – from the annual report of Caltex, it is identified

that there are no shareholder holing more than 20% shares.

More than 5% holding of shares – among the substantial shareholders of the company

Lazard Asset Management Pacific Co held 18,810,624 shares that comes to 7.21%,

BlackRock Group held 16,465,153 shares that comes to 6.09% and Westpac Banking

Corporation held 13,902,131 shares that comes to 5.33%.

ii) Name of main people

Chairman – Greig Gailey

Board members

Trevor Bourne – Non-executive director

1. Description of the company

Caltex Australia limited is the convenience retailer and transport fuel supplier

company based in Australia. Caltex is engaged in business of refining, purchasing, marketing,

distributing the petroleum products and operating the convenience stores all over Australia. It

operates through 2 segments that include Lytton and Supply and Marketing. The supply and

marketing division is the integrated supply chain for transport fuel and it delivers refined

products in international market and sells the lubricants, Caltex fuels and it has speciality

with regard to the convenience store goods and products through national network of Caltex

Woolworths, Caltex and the branded service stations of Ampol along with through non-

equity and company owned resellers and through direct sales. During the year 2016, the

company had 3166 employees in Australia that includes the employees from all the

subsidiaries under the control of the company (Caltex 2017).

2. Specification of the structure of ownership governance

i) Major substantial shareholders

More than 20% holding of shares – from the annual report of Caltex, it is identified

that there are no shareholder holing more than 20% shares.

More than 5% holding of shares – among the substantial shareholders of the company

Lazard Asset Management Pacific Co held 18,810,624 shares that comes to 7.21%,

BlackRock Group held 16,465,153 shares that comes to 6.09% and Westpac Banking

Corporation held 13,902,131 shares that comes to 5.33%.

ii) Name of main people

Chairman – Greig Gailey

Board members

Trevor Bourne – Non-executive director

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR BUSINESS – MASTERS

Steven Gregg – Non-executive director

Bruce Morgan – Non-executive director

Penny Winn – Non-executive director

Barbara Ward AM – Non-executive director

CEO – Julian Segal

From the annual report of Caltex, it is recognized that none of the members from the

board holds more than 5% or 20% of shares and therefore does not included in the substantial

shareholder.

3. Key ratios of Caltex

i. Return on assets (ROA) = (NPAT / Total Assets)

Return on Equity (ROE) = (Net profit after tax / Ordinary equity)

Ratio Formula 2016 2015 2014 2013

Return on assets NAPT / Total asset 0.115 0.102 0.004 0.088

Return on equity NPAT / Ordinary equity 0.217 0.187 0.009 0.204

Debt ratio = Total liabilities / Total assets

Ratio Formula 2016 2015 2014 2013

Debt ratio Total liabilities / Total assets 0.470 0.454 0.506 0.569

EBIT/TA * NPAT/EBIT * TA/OE = NPAT/OE

EBIT/TA * NPAT/EBIT * TA/OE = 934,953/5,302,734 * 610,480/934,953 * 5,302,734 /

2,810,215 = 0.22

NPAT/OE = 610,480/2,810,215 = 0.22

Steven Gregg – Non-executive director

Bruce Morgan – Non-executive director

Penny Winn – Non-executive director

Barbara Ward AM – Non-executive director

CEO – Julian Segal

From the annual report of Caltex, it is recognized that none of the members from the

board holds more than 5% or 20% of shares and therefore does not included in the substantial

shareholder.

3. Key ratios of Caltex

i. Return on assets (ROA) = (NPAT / Total Assets)

Return on Equity (ROE) = (Net profit after tax / Ordinary equity)

Ratio Formula 2016 2015 2014 2013

Return on assets NAPT / Total asset 0.115 0.102 0.004 0.088

Return on equity NPAT / Ordinary equity 0.217 0.187 0.009 0.204

Debt ratio = Total liabilities / Total assets

Ratio Formula 2016 2015 2014 2013

Debt ratio Total liabilities / Total assets 0.470 0.454 0.506 0.569

EBIT/TA * NPAT/EBIT * TA/OE = NPAT/OE

EBIT/TA * NPAT/EBIT * TA/OE = 934,953/5,302,734 * 610,480/934,953 * 5,302,734 /

2,810,215 = 0.22

NPAT/OE = 610,480/2,810,215 = 0.22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR BUSINESS – MASTERS

Therefore, it is proved from the above computation that –

EBIT/TA * NPAT/EBIT * TA/OE = NPAT/OE

ii. Phenomenon captured by the variable TA/OE

The phenomenon for TA/OE states the company’s total asset as compared to the

ordinary equity of the company. It states the insolvency risks of the company and also reveals

the risks associated with the total assets of the company that is faced by the shareholders

(Akeem et al. 2014). The significance of total asset of the company in comparison to the

equity depends on the revenue of the company, economic status of the company, industry to

which it belongs and various other factors. When the total assets of the company increase it

will decrease the company’s return on assets and vice versa (Macdonald-Smith 2015).

Though no ideal value is there for total asset to ordinary equity ratio, a high ratio represents

that the entity is highly leveraged. Reason for high level of leverage is the higher level of

borrowed capital in the capital structure of the company (Baños-Caballero, García-Teruel and

Martínez-Solano 2014). However, high asset to equity ratio represents that the company is

exposed to sustainability risk as the higher level of risk will expose the company to interest

risk. On the contrary, if the company has lower total asset to ordinary equity ratio, it

represent that the company is lower leveraged and has strong position (Naser, Nuseibeh and

Al-Hadeya 2013). However, lower ratio represents that the company is missing out on the

business opportunities and is of conservative nature.

iii. Reasons for higher ROE as compared to ROA

As both ROA as well as ROE measure the return of the company at 1st glance both

look similar. Both measure the ability of the company to generate the earnings from

investment. However, they are not exactly same and have some key differences among them.

Therefore, it is proved from the above computation that –

EBIT/TA * NPAT/EBIT * TA/OE = NPAT/OE

ii. Phenomenon captured by the variable TA/OE

The phenomenon for TA/OE states the company’s total asset as compared to the

ordinary equity of the company. It states the insolvency risks of the company and also reveals

the risks associated with the total assets of the company that is faced by the shareholders

(Akeem et al. 2014). The significance of total asset of the company in comparison to the

equity depends on the revenue of the company, economic status of the company, industry to

which it belongs and various other factors. When the total assets of the company increase it

will decrease the company’s return on assets and vice versa (Macdonald-Smith 2015).

Though no ideal value is there for total asset to ordinary equity ratio, a high ratio represents

that the entity is highly leveraged. Reason for high level of leverage is the higher level of

borrowed capital in the capital structure of the company (Baños-Caballero, García-Teruel and

Martínez-Solano 2014). However, high asset to equity ratio represents that the company is

exposed to sustainability risk as the higher level of risk will expose the company to interest

risk. On the contrary, if the company has lower total asset to ordinary equity ratio, it

represent that the company is lower leveraged and has strong position (Naser, Nuseibeh and

Al-Hadeya 2013). However, lower ratio represents that the company is missing out on the

business opportunities and is of conservative nature.

iii. Reasons for higher ROE as compared to ROA

As both ROA as well as ROE measure the return of the company at 1st glance both

look similar. Both measure the ability of the company to generate the earnings from

investment. However, they are not exactly same and have some key differences among them.

5FINANCE FOR BUSINESS – MASTERS

However, they both together provide clear picture of the company’s performance. When the

shareholder’s equity is lower as compared to the total assets of the company, the ROE of the

company becomes higher than the ROA. The fundamental equation of the balance sheet is –

Assets = Shareholder’s equity + Liabilities. Therefore, the company takes on the financial

leverage, its ROE will be higher as compared to ROA. In other words, if the debt increases,

the equity decreases and as the equity is placed in the denominator of ROE, the ROE in turn

increases. Likewise, when the company taken on the debt, the denominator of ROA that is the

total asset will increase which in turn represents that the ROE will increase as compared to

ROA.

4. Information from ASX website

i. Monthly stock movement for last 2 years

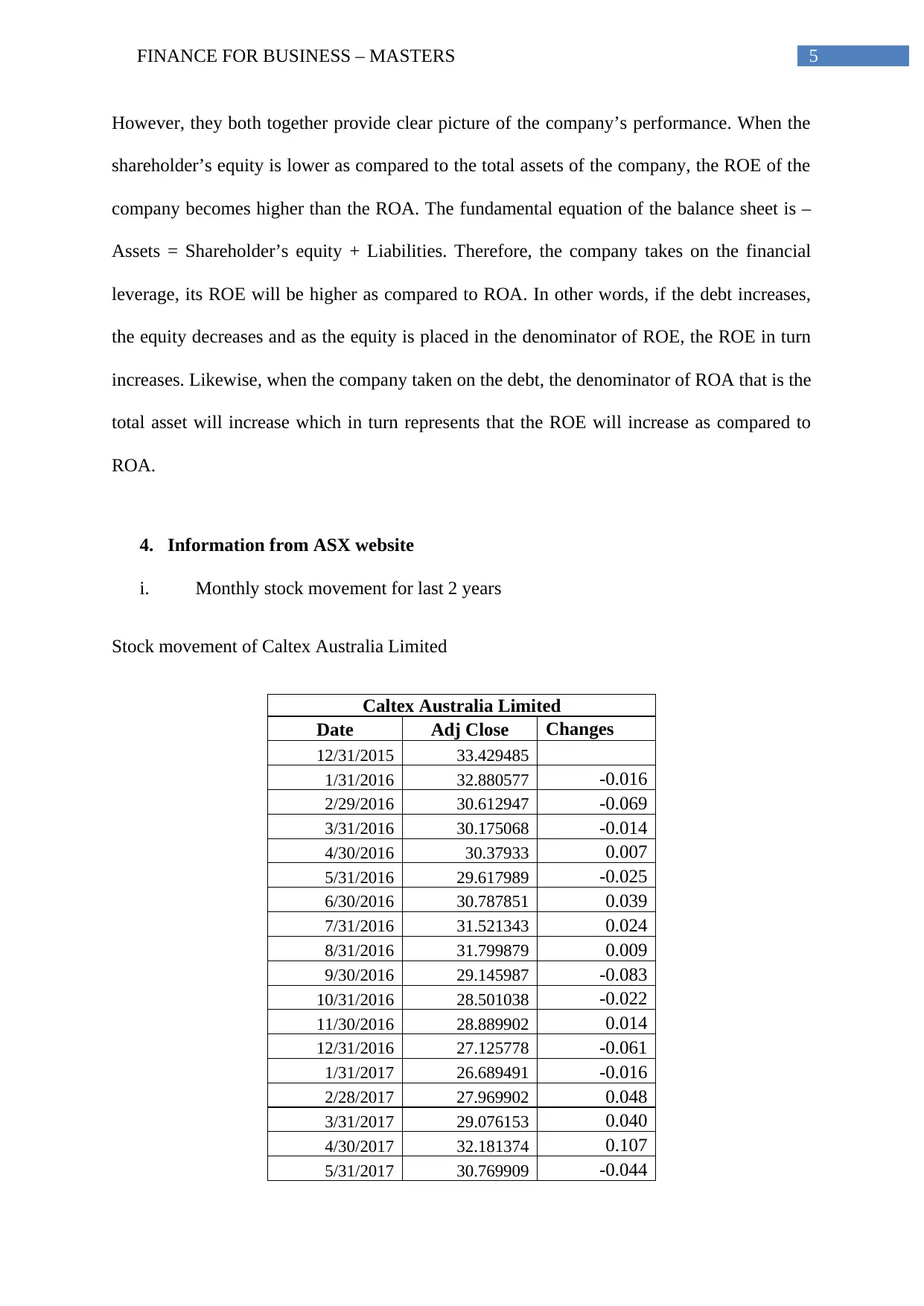

Stock movement of Caltex Australia Limited

Caltex Australia Limited

Date Adj Close Changes

12/31/2015 33.429485

1/31/2016 32.880577 -0.016

2/29/2016 30.612947 -0.069

3/31/2016 30.175068 -0.014

4/30/2016 30.37933 0.007

5/31/2016 29.617989 -0.025

6/30/2016 30.787851 0.039

7/31/2016 31.521343 0.024

8/31/2016 31.799879 0.009

9/30/2016 29.145987 -0.083

10/31/2016 28.501038 -0.022

11/30/2016 28.889902 0.014

12/31/2016 27.125778 -0.061

1/31/2017 26.689491 -0.016

2/28/2017 27.969902 0.048

3/31/2017 29.076153 0.040

4/30/2017 32.181374 0.107

5/31/2017 30.769909 -0.044

However, they both together provide clear picture of the company’s performance. When the

shareholder’s equity is lower as compared to the total assets of the company, the ROE of the

company becomes higher than the ROA. The fundamental equation of the balance sheet is –

Assets = Shareholder’s equity + Liabilities. Therefore, the company takes on the financial

leverage, its ROE will be higher as compared to ROA. In other words, if the debt increases,

the equity decreases and as the equity is placed in the denominator of ROE, the ROE in turn

increases. Likewise, when the company taken on the debt, the denominator of ROA that is the

total asset will increase which in turn represents that the ROE will increase as compared to

ROA.

4. Information from ASX website

i. Monthly stock movement for last 2 years

Stock movement of Caltex Australia Limited

Caltex Australia Limited

Date Adj Close Changes

12/31/2015 33.429485

1/31/2016 32.880577 -0.016

2/29/2016 30.612947 -0.069

3/31/2016 30.175068 -0.014

4/30/2016 30.37933 0.007

5/31/2016 29.617989 -0.025

6/30/2016 30.787851 0.039

7/31/2016 31.521343 0.024

8/31/2016 31.799879 0.009

9/30/2016 29.145987 -0.083

10/31/2016 28.501038 -0.022

11/30/2016 28.889902 0.014

12/31/2016 27.125778 -0.061

1/31/2017 26.689491 -0.016

2/28/2017 27.969902 0.048

3/31/2017 29.076153 0.040

4/30/2017 32.181374 0.107

5/31/2017 30.769909 -0.044

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR BUSINESS – MASTERS

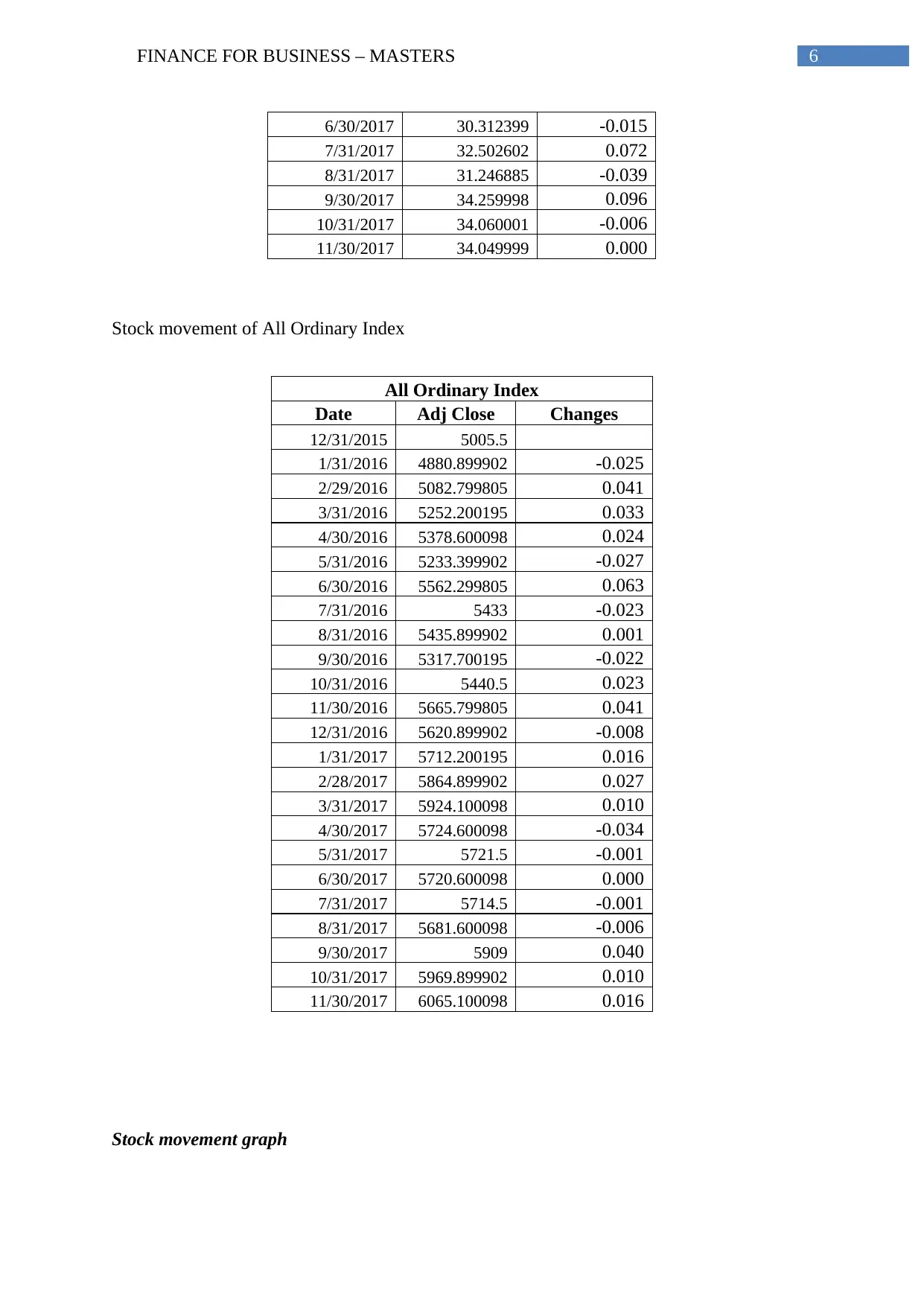

6/30/2017 30.312399 -0.015

7/31/2017 32.502602 0.072

8/31/2017 31.246885 -0.039

9/30/2017 34.259998 0.096

10/31/2017 34.060001 -0.006

11/30/2017 34.049999 0.000

Stock movement of All Ordinary Index

All Ordinary Index

Date Adj Close Changes

12/31/2015 5005.5

1/31/2016 4880.899902 -0.025

2/29/2016 5082.799805 0.041

3/31/2016 5252.200195 0.033

4/30/2016 5378.600098 0.024

5/31/2016 5233.399902 -0.027

6/30/2016 5562.299805 0.063

7/31/2016 5433 -0.023

8/31/2016 5435.899902 0.001

9/30/2016 5317.700195 -0.022

10/31/2016 5440.5 0.023

11/30/2016 5665.799805 0.041

12/31/2016 5620.899902 -0.008

1/31/2017 5712.200195 0.016

2/28/2017 5864.899902 0.027

3/31/2017 5924.100098 0.010

4/30/2017 5724.600098 -0.034

5/31/2017 5721.5 -0.001

6/30/2017 5720.600098 0.000

7/31/2017 5714.5 -0.001

8/31/2017 5681.600098 -0.006

9/30/2017 5909 0.040

10/31/2017 5969.899902 0.010

11/30/2017 6065.100098 0.016

Stock movement graph

6/30/2017 30.312399 -0.015

7/31/2017 32.502602 0.072

8/31/2017 31.246885 -0.039

9/30/2017 34.259998 0.096

10/31/2017 34.060001 -0.006

11/30/2017 34.049999 0.000

Stock movement of All Ordinary Index

All Ordinary Index

Date Adj Close Changes

12/31/2015 5005.5

1/31/2016 4880.899902 -0.025

2/29/2016 5082.799805 0.041

3/31/2016 5252.200195 0.033

4/30/2016 5378.600098 0.024

5/31/2016 5233.399902 -0.027

6/30/2016 5562.299805 0.063

7/31/2016 5433 -0.023

8/31/2016 5435.899902 0.001

9/30/2016 5317.700195 -0.022

10/31/2016 5440.5 0.023

11/30/2016 5665.799805 0.041

12/31/2016 5620.899902 -0.008

1/31/2017 5712.200195 0.016

2/28/2017 5864.899902 0.027

3/31/2017 5924.100098 0.010

4/30/2017 5724.600098 -0.034

5/31/2017 5721.5 -0.001

6/30/2017 5720.600098 0.000

7/31/2017 5714.5 -0.001

8/31/2017 5681.600098 -0.006

9/30/2017 5909 0.040

10/31/2017 5969.899902 0.010

11/30/2017 6065.100098 0.016

Stock movement graph

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR BUSINESS – MASTERS

01/12/2015

01/02/2016

01/04/2016

01/06/2016

01/08/2016

01/10/2016

01/12/2016

01/02/2017

01/04/2017

01/06/2017

01/08/2017

01/10/2017

0

5

10

15

20

25

30

35

40

Caltex Australia Limited

Adj Close

01/12/2015

01/02/2016

01/04/2016

01/06/2016

01/08/2016

01/10/2016

01/12/2016

01/02/2017

01/04/2017

01/06/2017

01/08/2017

01/10/2017

0

1000

2000

3000

4000

5000

6000

7000

All Ordinary Index

Adj Close

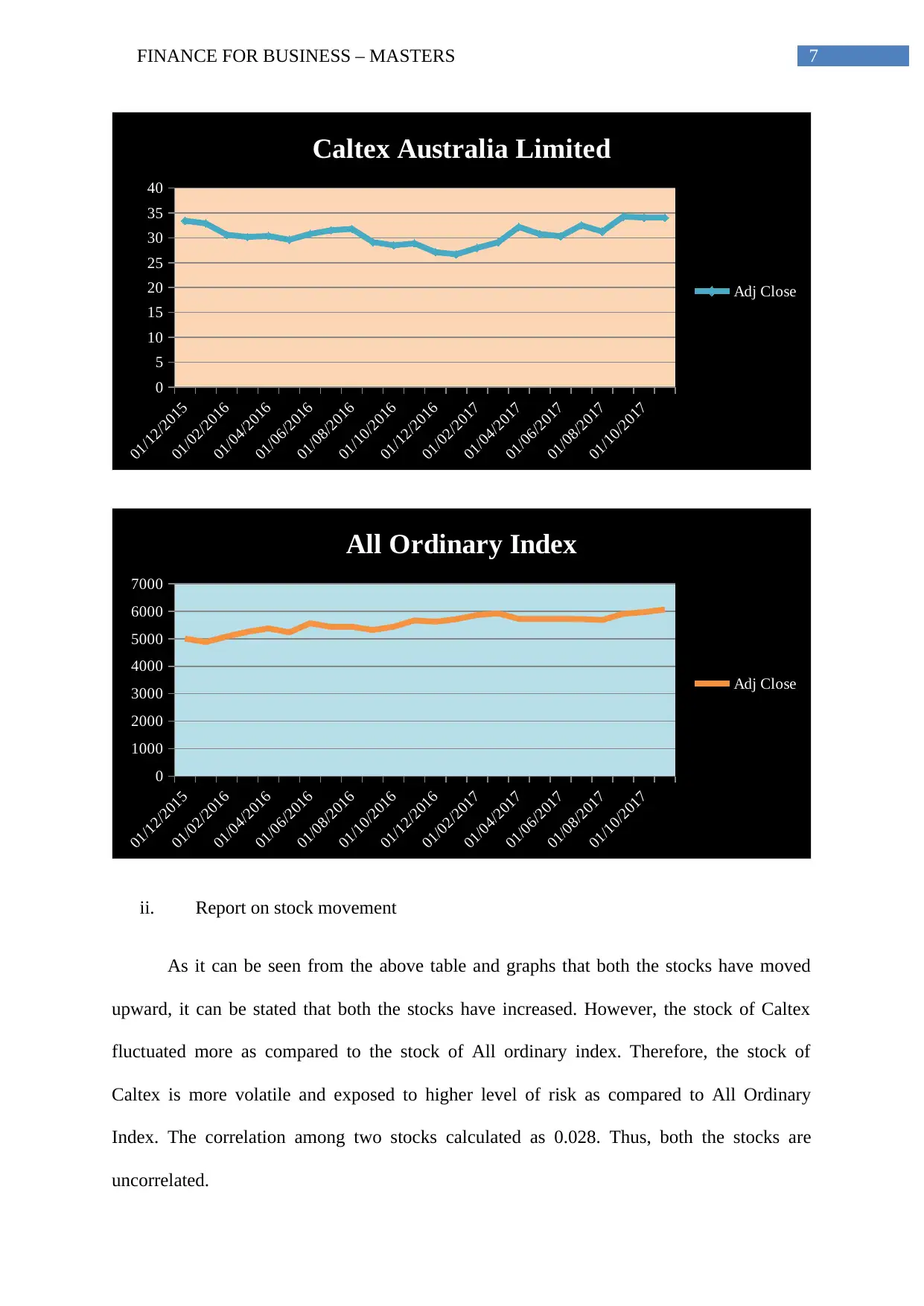

ii. Report on stock movement

As it can be seen from the above table and graphs that both the stocks have moved

upward, it can be stated that both the stocks have increased. However, the stock of Caltex

fluctuated more as compared to the stock of All ordinary index. Therefore, the stock of

Caltex is more volatile and exposed to higher level of risk as compared to All Ordinary

Index. The correlation among two stocks calculated as 0.028. Thus, both the stocks are

uncorrelated.

01/12/2015

01/02/2016

01/04/2016

01/06/2016

01/08/2016

01/10/2016

01/12/2016

01/02/2017

01/04/2017

01/06/2017

01/08/2017

01/10/2017

0

5

10

15

20

25

30

35

40

Caltex Australia Limited

Adj Close

01/12/2015

01/02/2016

01/04/2016

01/06/2016

01/08/2016

01/10/2016

01/12/2016

01/02/2017

01/04/2017

01/06/2017

01/08/2017

01/10/2017

0

1000

2000

3000

4000

5000

6000

7000

All Ordinary Index

Adj Close

ii. Report on stock movement

As it can be seen from the above table and graphs that both the stocks have moved

upward, it can be stated that both the stocks have increased. However, the stock of Caltex

fluctuated more as compared to the stock of All ordinary index. Therefore, the stock of

Caltex is more volatile and exposed to higher level of risk as compared to All Ordinary

Index. The correlation among two stocks calculated as 0.028. Thus, both the stocks are

uncorrelated.

8FINANCE FOR BUSINESS – MASTERS

5. Recent announcement

Towards the end of 4th quarter the company announced its 1st overseas acquisition that

is the purchase of the independent retailer of fuel Gull New Zealand. Entry in the

geographically advanced market of New Zealand is considered to be the logical

growth step for the company.

During August the company announced the commencement of construction for

upgrading $ 75 million investment which will be completed by end of the year 2017.

It is expected to increase the storage capacity of the company by additional 40 million

litres.

The company received the global innovation award for providing remediation facility

of Sydney soil. The facility was build and designed by Australian fuel supplier Caltex

for treating the contaminated soil.

The company opened a jet fuel pipeline amounting to $ 16 million for servicing the

Brisbane airport which is expected to underpin rapid expansion of international

aviation hub in next 20 years.

6. Stock field

i. Calculated beta of the company is 0.05

ii. Risk free rate = Rf = 4%, Market risk premium = Rm = 6%

Therefore, required rate of return of the company’s share =

R = Rf + β ( Rm – Rf )

R = 4% + 0.05* (6% – 4%) = 4.1%

iii. Conservative investment

5. Recent announcement

Towards the end of 4th quarter the company announced its 1st overseas acquisition that

is the purchase of the independent retailer of fuel Gull New Zealand. Entry in the

geographically advanced market of New Zealand is considered to be the logical

growth step for the company.

During August the company announced the commencement of construction for

upgrading $ 75 million investment which will be completed by end of the year 2017.

It is expected to increase the storage capacity of the company by additional 40 million

litres.

The company received the global innovation award for providing remediation facility

of Sydney soil. The facility was build and designed by Australian fuel supplier Caltex

for treating the contaminated soil.

The company opened a jet fuel pipeline amounting to $ 16 million for servicing the

Brisbane airport which is expected to underpin rapid expansion of international

aviation hub in next 20 years.

6. Stock field

i. Calculated beta of the company is 0.05

ii. Risk free rate = Rf = 4%, Market risk premium = Rm = 6%

Therefore, required rate of return of the company’s share =

R = Rf + β ( Rm – Rf )

R = 4% + 0.05* (6% – 4%) = 4.1%

iii. Conservative investment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE FOR BUSINESS – MASTERS

It is the investment approach under which the value of the investment portfolio is

preserved through investment in the lower risks associated securities. An investment option

with regular income and fixed market securities are considered as conservative investment. a

conservative investment is also associated with higher return, lower beta and regular payment

for dividend (Heikal, Khaddafi and Ummah 2014). It is recognized from the above details

that the company’s beta is 0.05 which can be considered as low. Further, the company’s ROE

is better than the ROA. Further, the target payout ratio for dividend is 40 to 60% of RCOP

NPAT. To match this target it declared final dividend of 52 cents per share for 2 nd half of

2016 in addition to 50 cents per share for 1st half. This made the total dividend of 102 cents of

dividend per share for the year 2016 as compared to 117 cents dividend per share for the year

2015. Therefore, it can be stated that the company is regular in paying the dividend.

Therefore, Caltex Australia Limited will be regarded as conservative investment.

7. WACC (weighted average cost of capital)

i. Computation of WACC

WACC of the company calculated through proportionately weighting each category

of capital under the capital structure. For this purpose, all types of capital like equity capital,

preferred capital, common stock, bonds and long-term liabilities are taken into consideration

(Zabarankin, Pavlikov and Uryasev 2014). The weighted average cost of the capital for any

company increases with the increase in the beta as well as the return on equity rate. However,

if the WACC of the company goes up, the valuation of the company goes down and at the

same time the capital risk of the company increases. The WACC is computed as follows –

WACC = E/V * Re +D/V * Rd * (1-Tc), Where,

E/V = Equity percentage in the capital structure

It is the investment approach under which the value of the investment portfolio is

preserved through investment in the lower risks associated securities. An investment option

with regular income and fixed market securities are considered as conservative investment. a

conservative investment is also associated with higher return, lower beta and regular payment

for dividend (Heikal, Khaddafi and Ummah 2014). It is recognized from the above details

that the company’s beta is 0.05 which can be considered as low. Further, the company’s ROE

is better than the ROA. Further, the target payout ratio for dividend is 40 to 60% of RCOP

NPAT. To match this target it declared final dividend of 52 cents per share for 2 nd half of

2016 in addition to 50 cents per share for 1st half. This made the total dividend of 102 cents of

dividend per share for the year 2016 as compared to 117 cents dividend per share for the year

2015. Therefore, it can be stated that the company is regular in paying the dividend.

Therefore, Caltex Australia Limited will be regarded as conservative investment.

7. WACC (weighted average cost of capital)

i. Computation of WACC

WACC of the company calculated through proportionately weighting each category

of capital under the capital structure. For this purpose, all types of capital like equity capital,

preferred capital, common stock, bonds and long-term liabilities are taken into consideration

(Zabarankin, Pavlikov and Uryasev 2014). The weighted average cost of the capital for any

company increases with the increase in the beta as well as the return on equity rate. However,

if the WACC of the company goes up, the valuation of the company goes down and at the

same time the capital risk of the company increases. The WACC is computed as follows –

WACC = E/V * Re +D/V * Rd * (1-Tc), Where,

E/V = Equity percentage in the capital structure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR BUSINESS – MASTERS

D/V = Debt percentage in the capital structure

Re = Cost of equity = 4.10%

Rd = Rate of debt = 13.9%

Tc = corporate tax rate = 30%

The given information for computation of WACC are as follows –

Amount in $'000

Amount of Debt 4,53,617.00

Amount of Equity 28,10,215.00

Total 32,63,832.00

Percentage of debt 14%

Percentage of equity 86%

Thus, WACC = 86*4.10% + 14*13.9% (1- 0.30)

= 3.526 + 1.362 = 4.89%

ii. Implication that the higher WACC has on the evaluation of management

Weighted average cost of the capital that is known as WACC, is the rate at which the

entity projects to pay on average to their shareholders for the purpose of asset financing. In

other words, it is the cost of capital for the company. It represents the firm’s cost for

financing the projects that may acquire by the firm for the purpose of growth. The WACC is

subjective to the external market condition and it is not decided by the management of the

company (Zhang 2014). Finance is raised either through debt or through equity and both the

sources are raised in exchange of costs. For instance, if the finance is raised through debt the

cost is the interest and on the contrary if the finance is raised through equity the cost is the

dividend or the share of the company. If the WACC of the company is higher, it represents

that the company is exposed to higher capital risk and the management try to raise fund from

D/V = Debt percentage in the capital structure

Re = Cost of equity = 4.10%

Rd = Rate of debt = 13.9%

Tc = corporate tax rate = 30%

The given information for computation of WACC are as follows –

Amount in $'000

Amount of Debt 4,53,617.00

Amount of Equity 28,10,215.00

Total 32,63,832.00

Percentage of debt 14%

Percentage of equity 86%

Thus, WACC = 86*4.10% + 14*13.9% (1- 0.30)

= 3.526 + 1.362 = 4.89%

ii. Implication that the higher WACC has on the evaluation of management

Weighted average cost of the capital that is known as WACC, is the rate at which the

entity projects to pay on average to their shareholders for the purpose of asset financing. In

other words, it is the cost of capital for the company. It represents the firm’s cost for

financing the projects that may acquire by the firm for the purpose of growth. The WACC is

subjective to the external market condition and it is not decided by the management of the

company (Zhang 2014). Finance is raised either through debt or through equity and both the

sources are raised in exchange of costs. For instance, if the finance is raised through debt the

cost is the interest and on the contrary if the finance is raised through equity the cost is the

dividend or the share of the company. If the WACC of the company is higher, it represents

that the company is exposed to higher capital risk and the management try to raise fund from

11FINANCE FOR BUSINESS – MASTERS

cheaper source. It further indicates that the company is losing its worth and shall find for

more profitable and lower risk associated projects for investment.

8. Optimal debt structure

i. Optimal structure for capital

Debt ratio Total liabilities / Total assets Year 2016 = 0.470 Year 2015 = 0.454

The optimal capital structure is the one at which the company can maximise its value.

It is stated as the one that can maintain the balance among the debt and equity of the firm and

can minimize the capital cost of the company (Albul, Jaffee and Tchistyi 2015.). Generally,

the cost of debt is regarded as low cost source of fund as the cost for debts are deductible

expense under tax whereas the cost of equity is not tax deductible. However, the debt comes

in exchange of interest cost and it increases the company’s risk associated with interest rate

(Harris and Mazibas 2013). The debt ratio of 0.4 or lower is generally regarded as ideal from

the perspective of pure risk. It is recognized from the above calculation of Caltex Limited that

the debt ratio for the year 2016 was 0.57 as compared to 0.45 for the year 2015. Therefore, it

can be stated that the company is maintaining the ideal and stable debt ratio (Renneboog and

Szilagyi 2015).

ii. Gearing ratio

The gearing ratio is the financial ratio that measures the shareholder’s equity as

compared to the debt of the company. It is used for analyzing the company’s capital structure

and is calculated through dividing the owner’s equity by the interest bearing liabilities

(Bodie, Kane and Marcus 2014). The company is considered to be highly geared if the debt is

higher in the capital structure. On the contrary it is considered as low geared if the capital

cheaper source. It further indicates that the company is losing its worth and shall find for

more profitable and lower risk associated projects for investment.

8. Optimal debt structure

i. Optimal structure for capital

Debt ratio Total liabilities / Total assets Year 2016 = 0.470 Year 2015 = 0.454

The optimal capital structure is the one at which the company can maximise its value.

It is stated as the one that can maintain the balance among the debt and equity of the firm and

can minimize the capital cost of the company (Albul, Jaffee and Tchistyi 2015.). Generally,

the cost of debt is regarded as low cost source of fund as the cost for debts are deductible

expense under tax whereas the cost of equity is not tax deductible. However, the debt comes

in exchange of interest cost and it increases the company’s risk associated with interest rate

(Harris and Mazibas 2013). The debt ratio of 0.4 or lower is generally regarded as ideal from

the perspective of pure risk. It is recognized from the above calculation of Caltex Limited that

the debt ratio for the year 2016 was 0.57 as compared to 0.45 for the year 2015. Therefore, it

can be stated that the company is maintaining the ideal and stable debt ratio (Renneboog and

Szilagyi 2015).

ii. Gearing ratio

The gearing ratio is the financial ratio that measures the shareholder’s equity as

compared to the debt of the company. It is used for analyzing the company’s capital structure

and is calculated through dividing the owner’s equity by the interest bearing liabilities

(Bodie, Kane and Marcus 2014). The company is considered to be highly geared if the debt is

higher in the capital structure. On the contrary it is considered as low geared if the capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.