Financial Analysis Assignment: Capital Budgeting and Valuation

VerifiedAdded on 2021/06/15

|6

|1017

|37

Homework Assignment

AI Summary

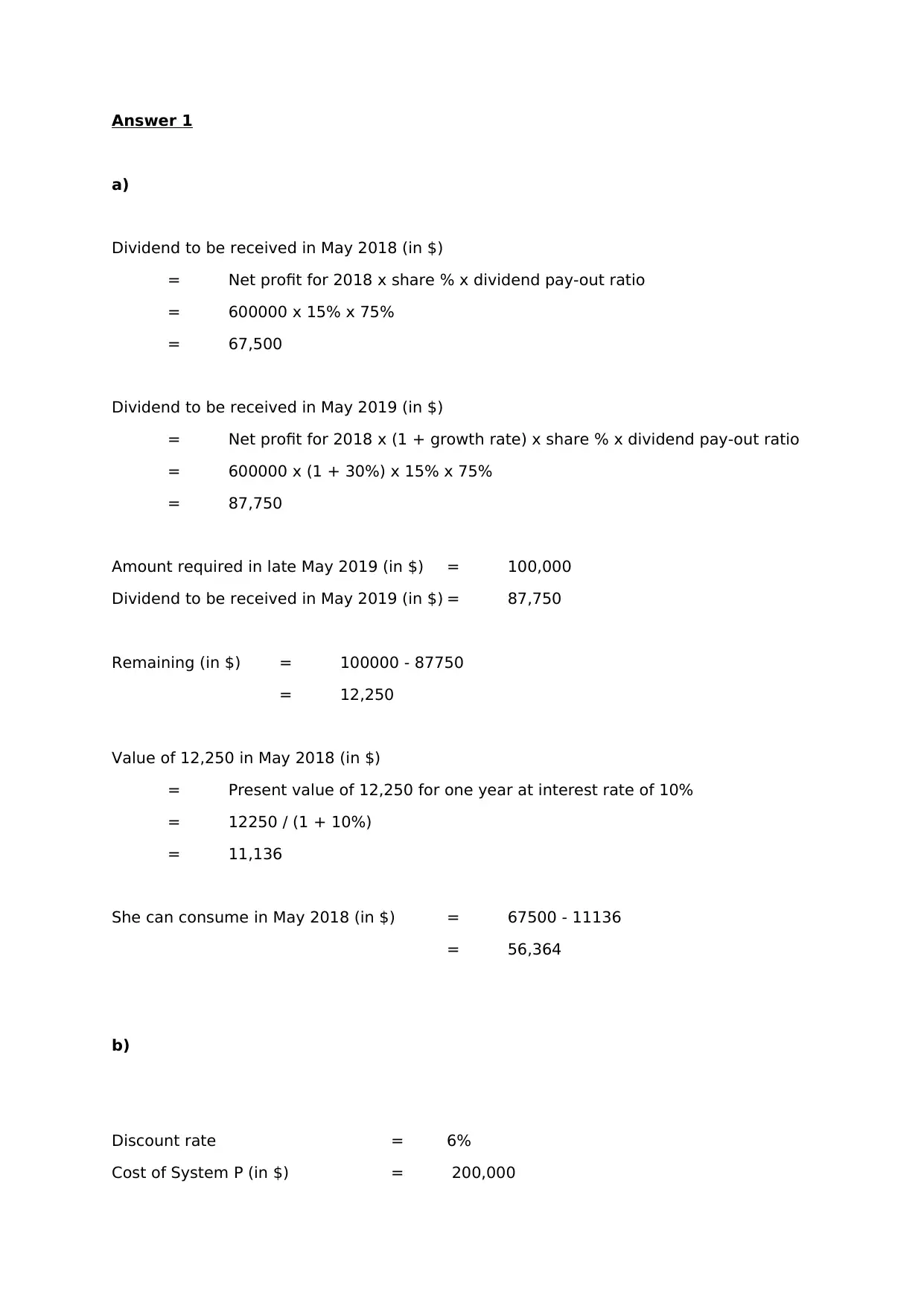

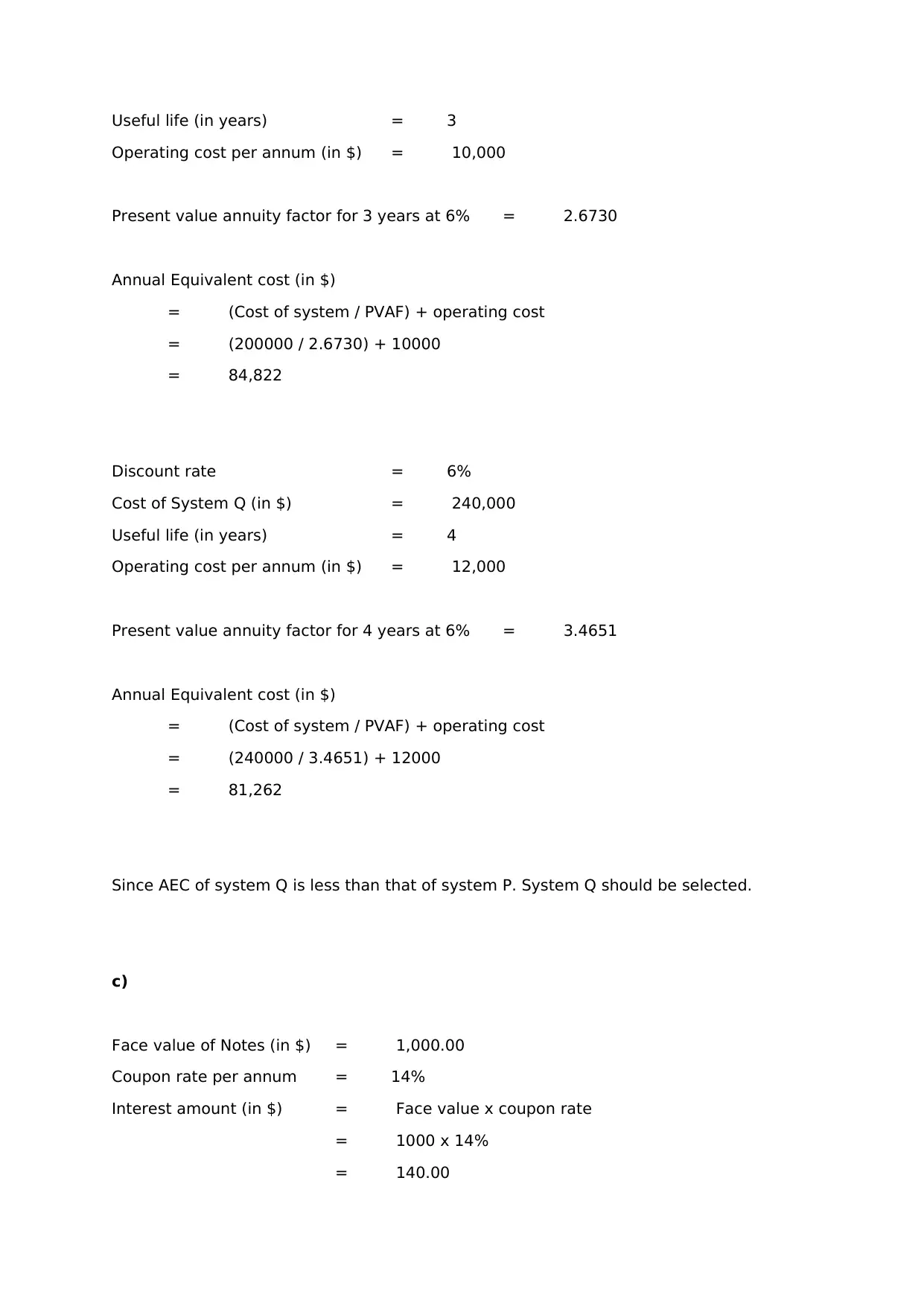

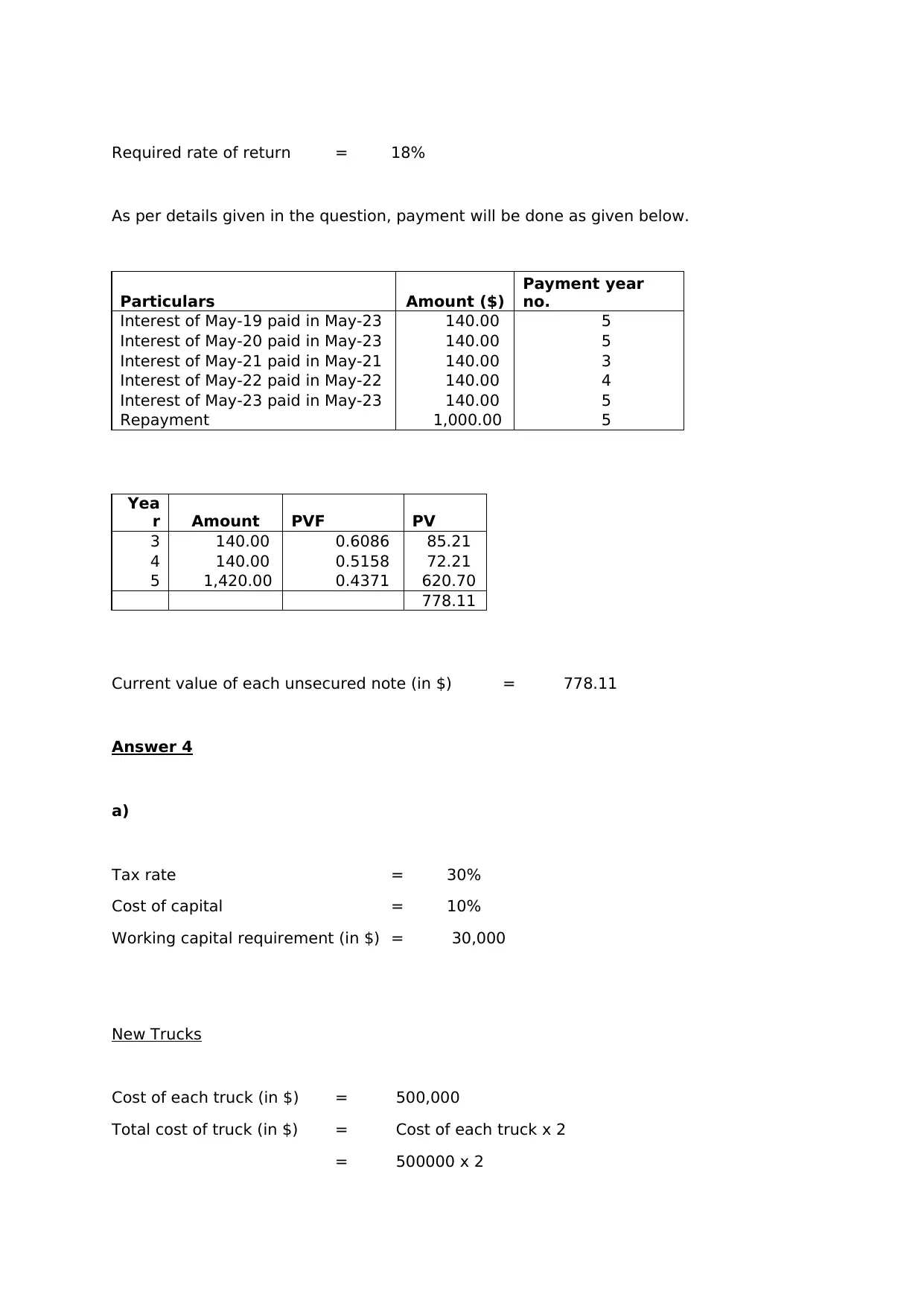

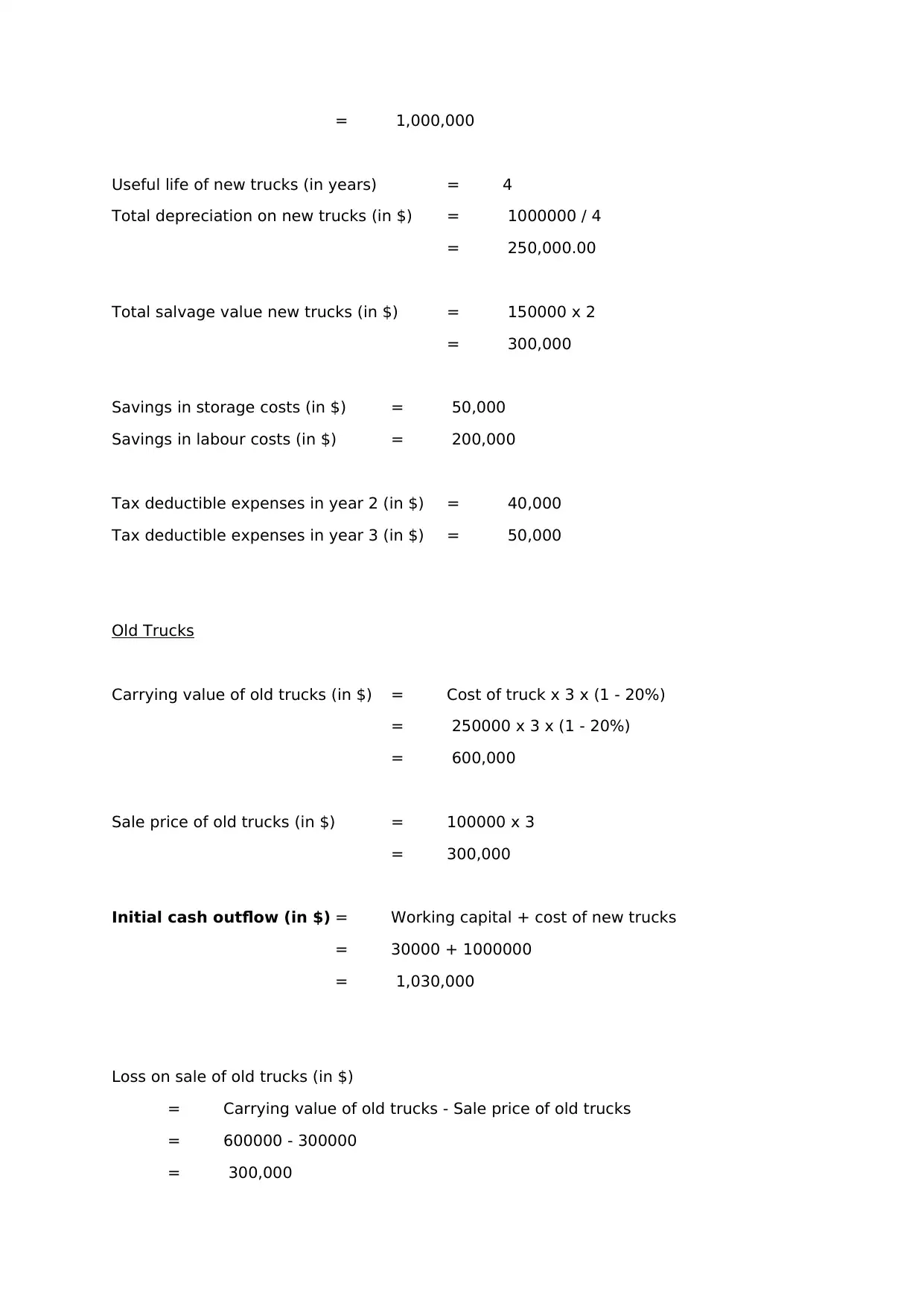

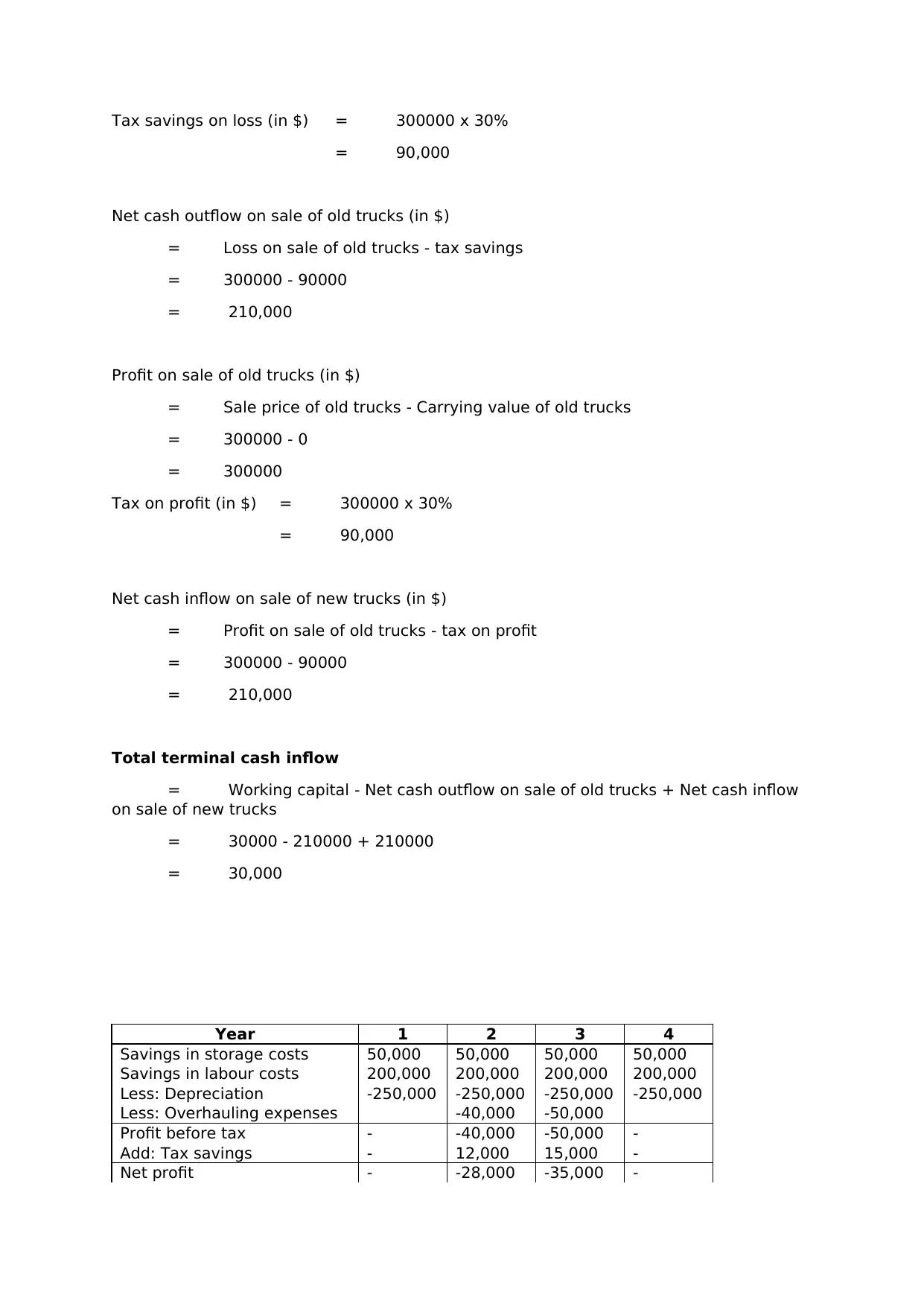

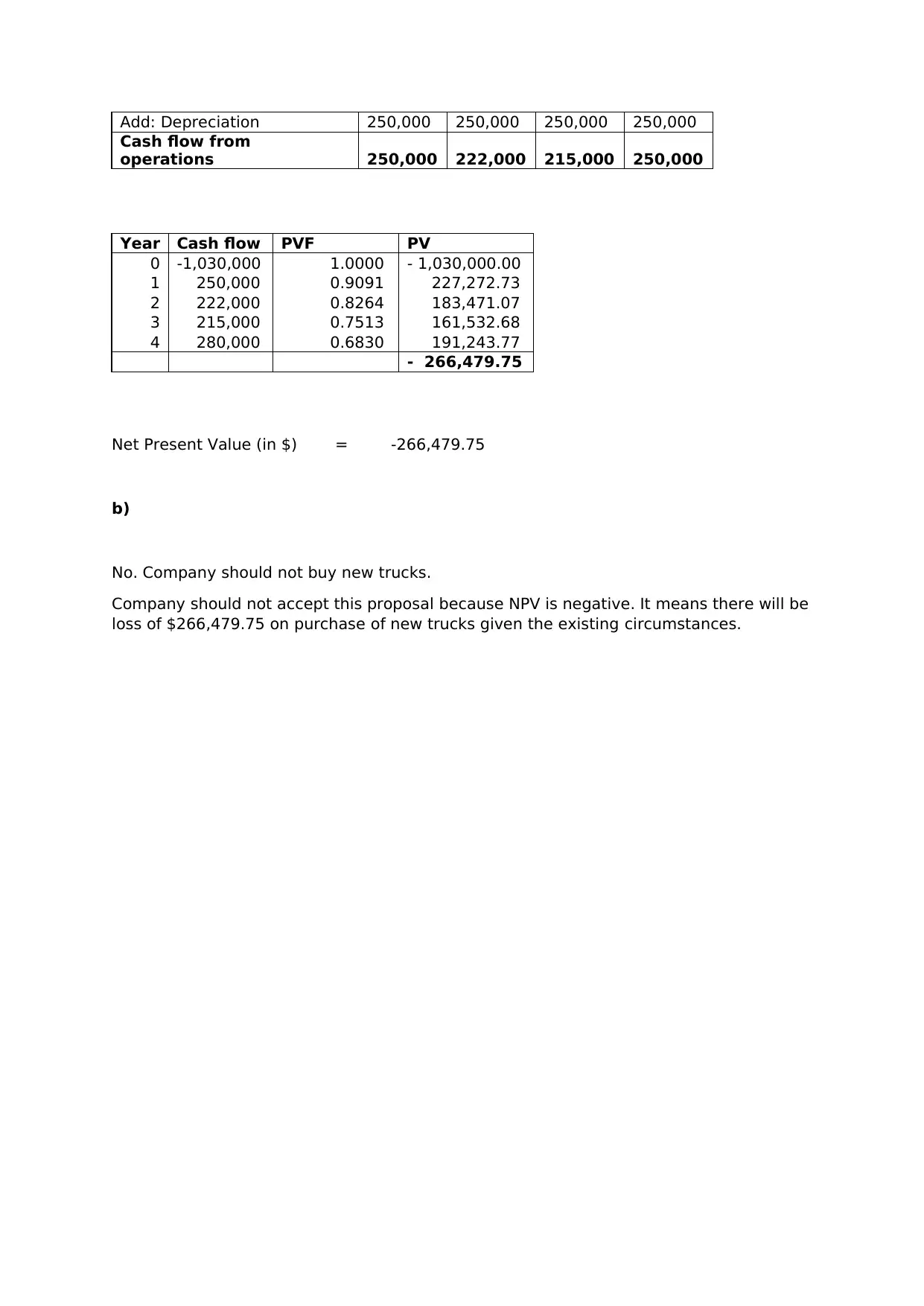

This document contains the solutions to a finance homework assignment. The assignment covers several key financial concepts. The first part of the solution addresses investment valuation, calculating the dividends to be received over time, and determining the amount an investor can consume in the present. It also explores the concept of present value. The second part focuses on capital budgeting, comparing the annual equivalent costs of two different systems and recommending the more cost-effective option. The next part of the solution delves into bond valuation, calculating the current value of an unsecured note based on its coupon rate, required rate of return, and payment schedule. Finally, the assignment addresses a capital budgeting problem involving the purchase of new trucks. The solution analyzes the cash flows associated with the investment, calculates the net present value (NPV), and provides a recommendation on whether the company should proceed with the investment.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.