Financial Analysis of Domino's and RFG: Dollars and Sense Case Study 1

VerifiedAdded on 2022/11/14

|9

|1111

|321

Case Study

AI Summary

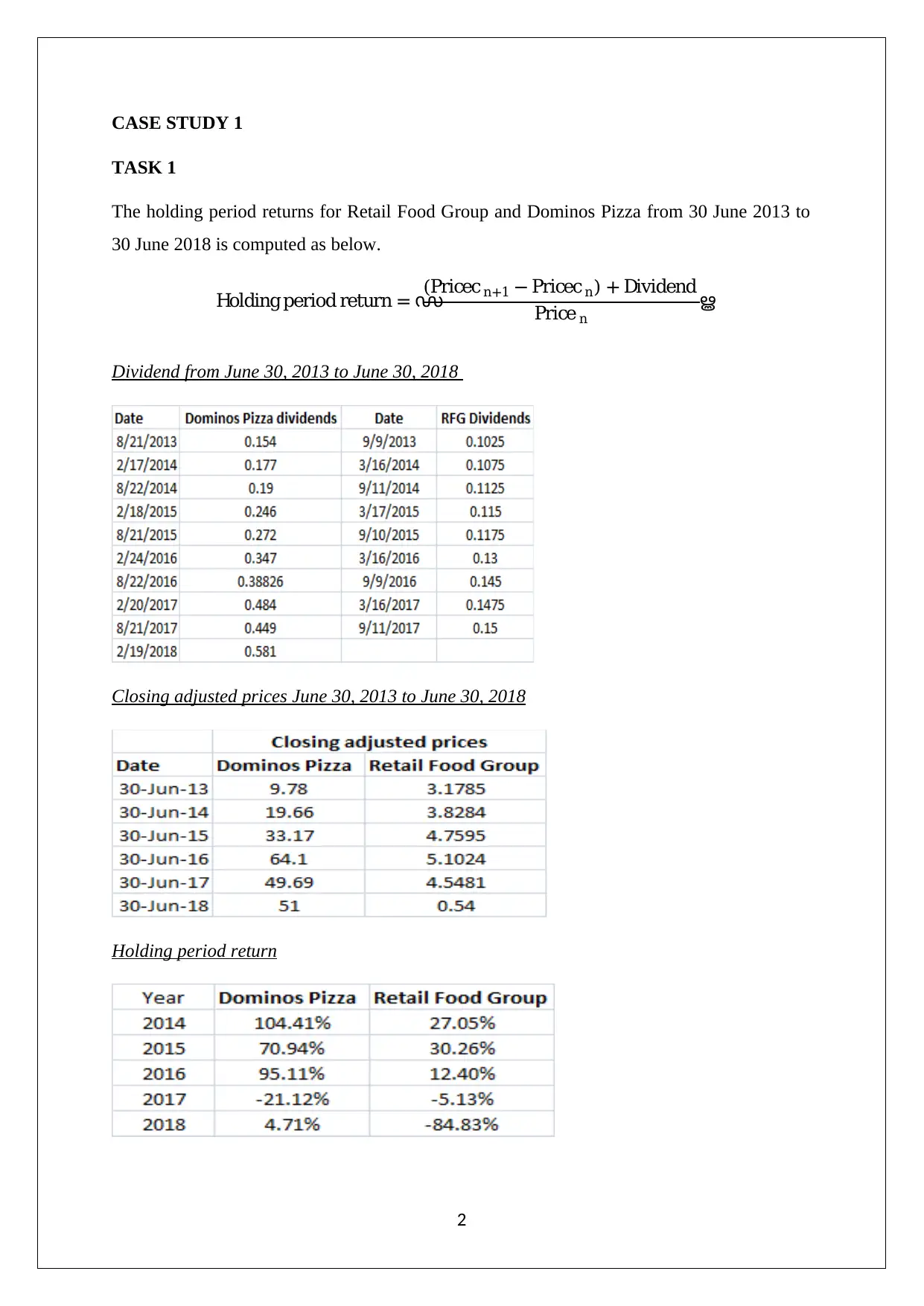

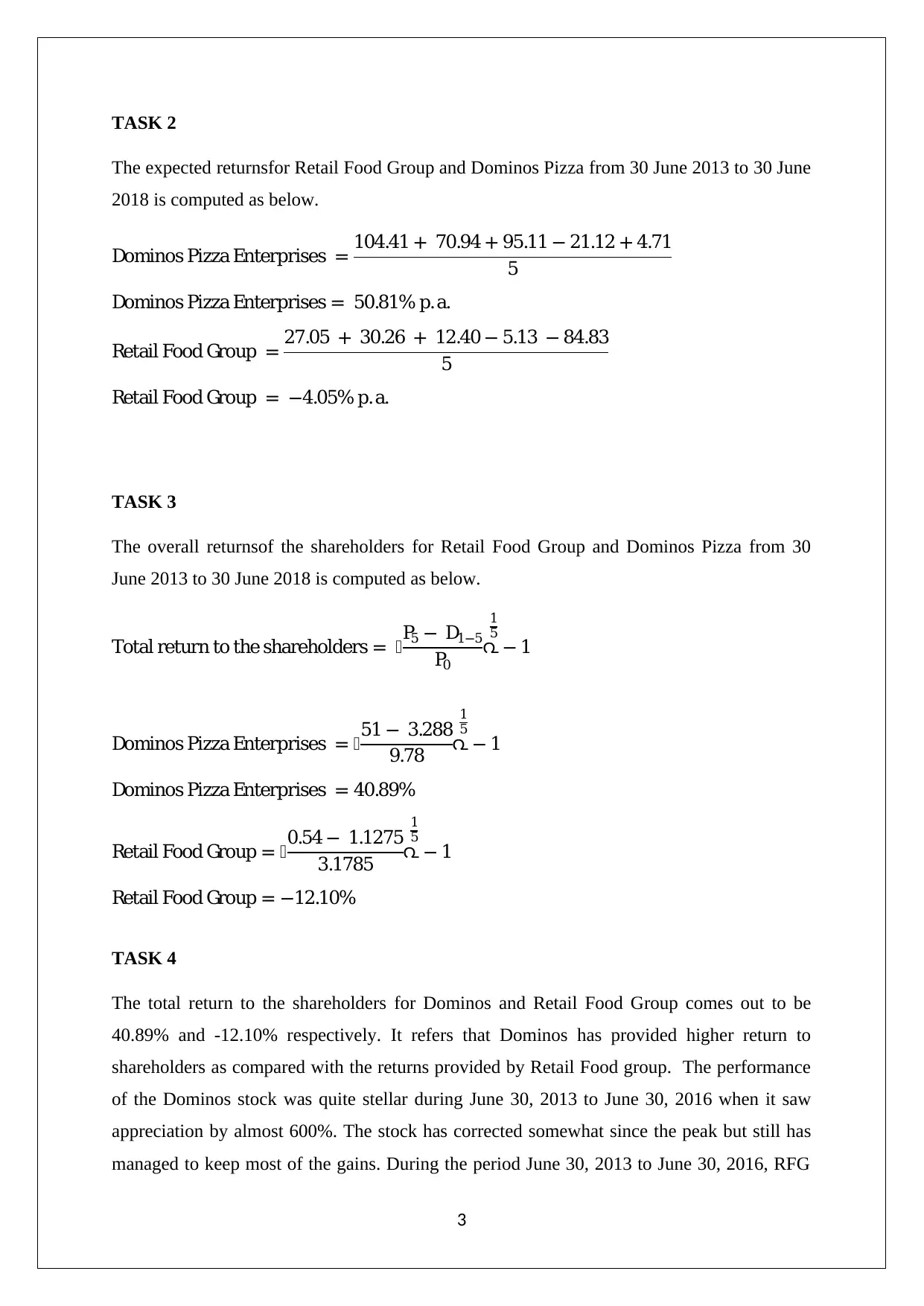

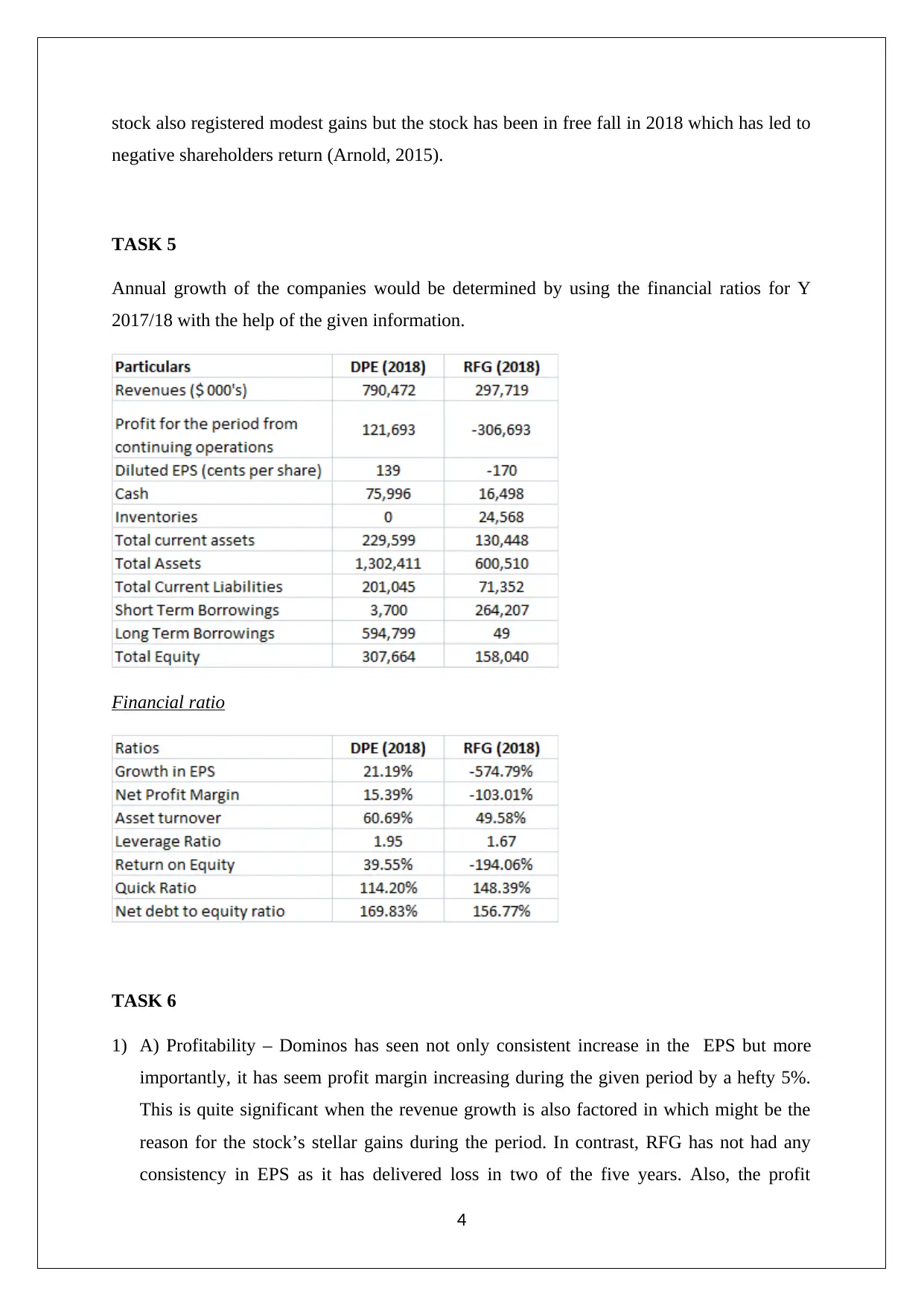

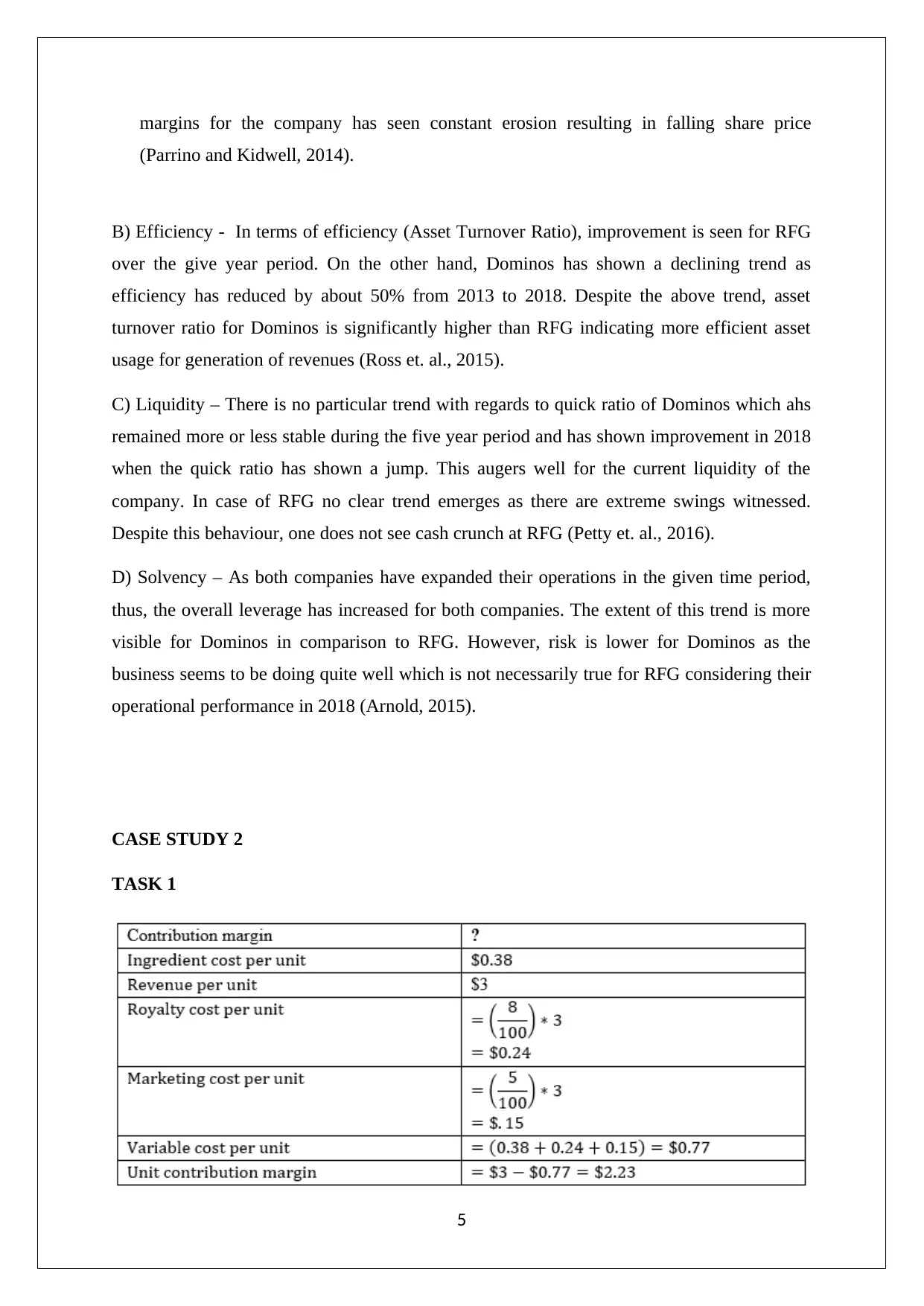

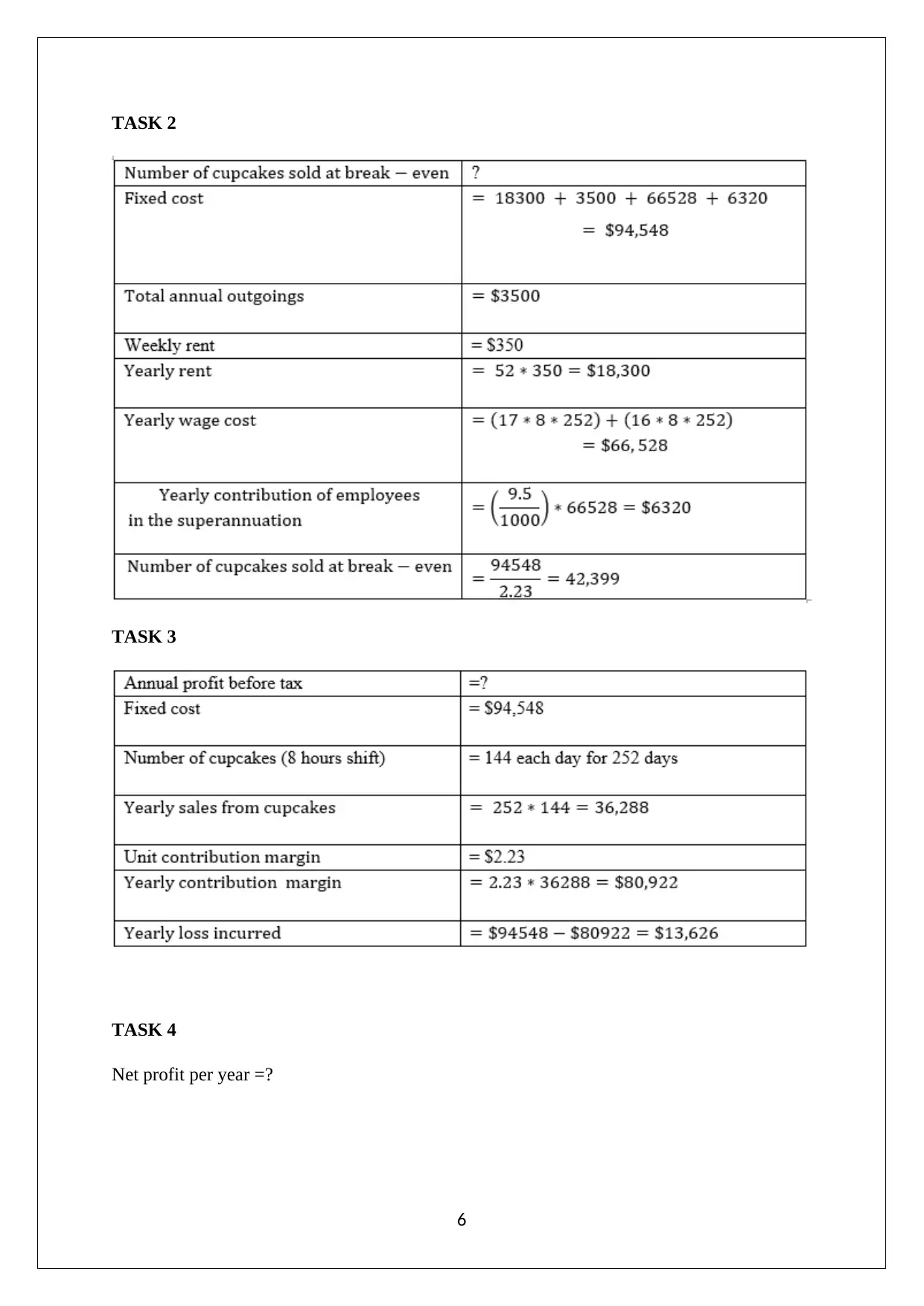

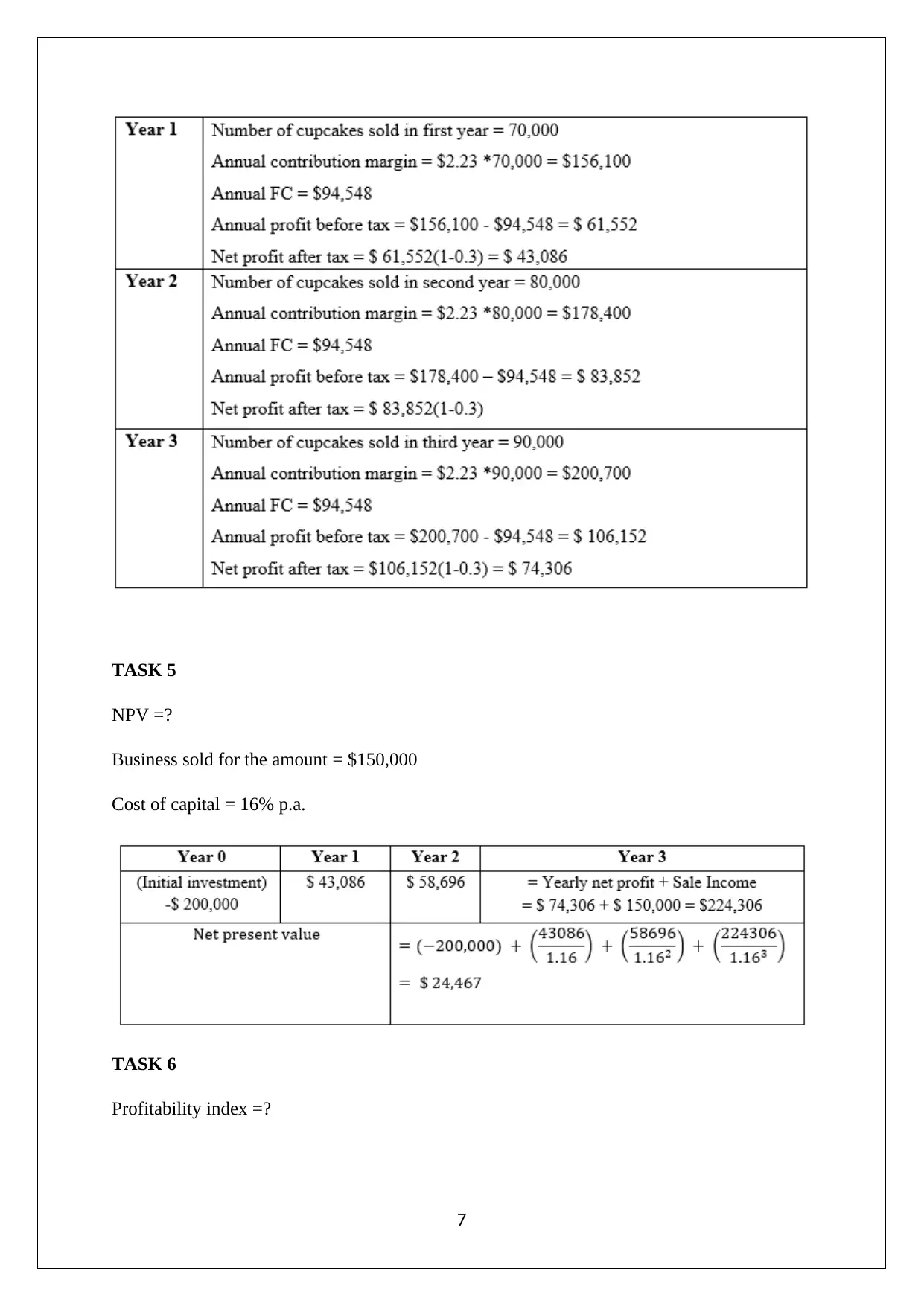

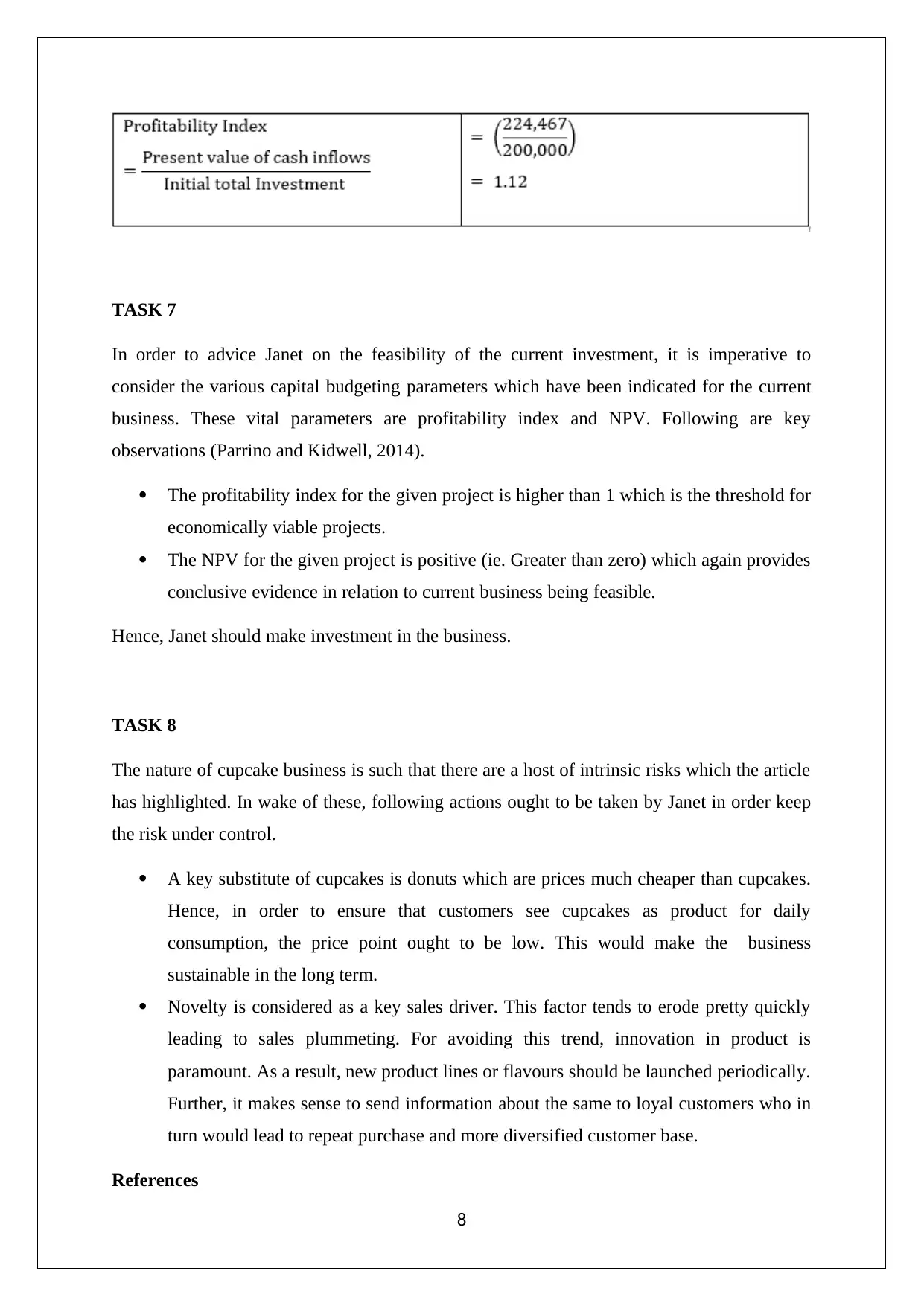

This case study analyzes the financial performance of Retail Food Group (RFG) and Domino's Pizza from June 30, 2013, to June 30, 2018. It begins by calculating holding period returns and expected returns for both companies, followed by an analysis of shareholder returns. The study then delves into financial ratios, including profitability, efficiency, liquidity, and solvency, to determine the annual growth of the companies using 2017/18 financial data. Case Study 2 focuses on capital budgeting, specifically profitability index and NPV calculations, to advise on an investment decision related to a cupcake business. The study concludes with recommendations for managing risks in the cupcake business, such as price adjustments and product innovation.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.