Accounting Financial Analysis: Nordstrom, Cash Flow, DuPont Method

VerifiedAdded on 2023/04/23

|16

|2898

|432

Homework Assignment

AI Summary

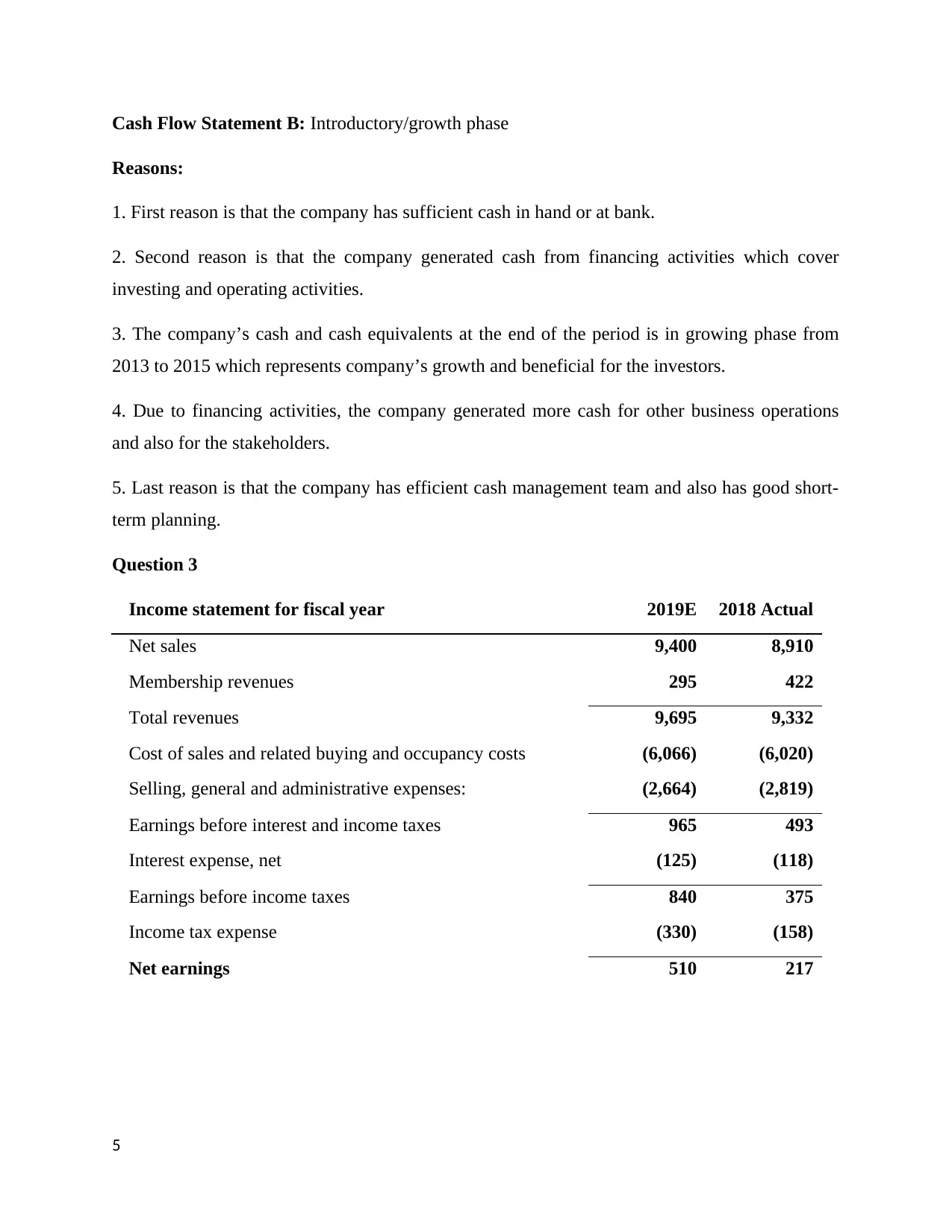

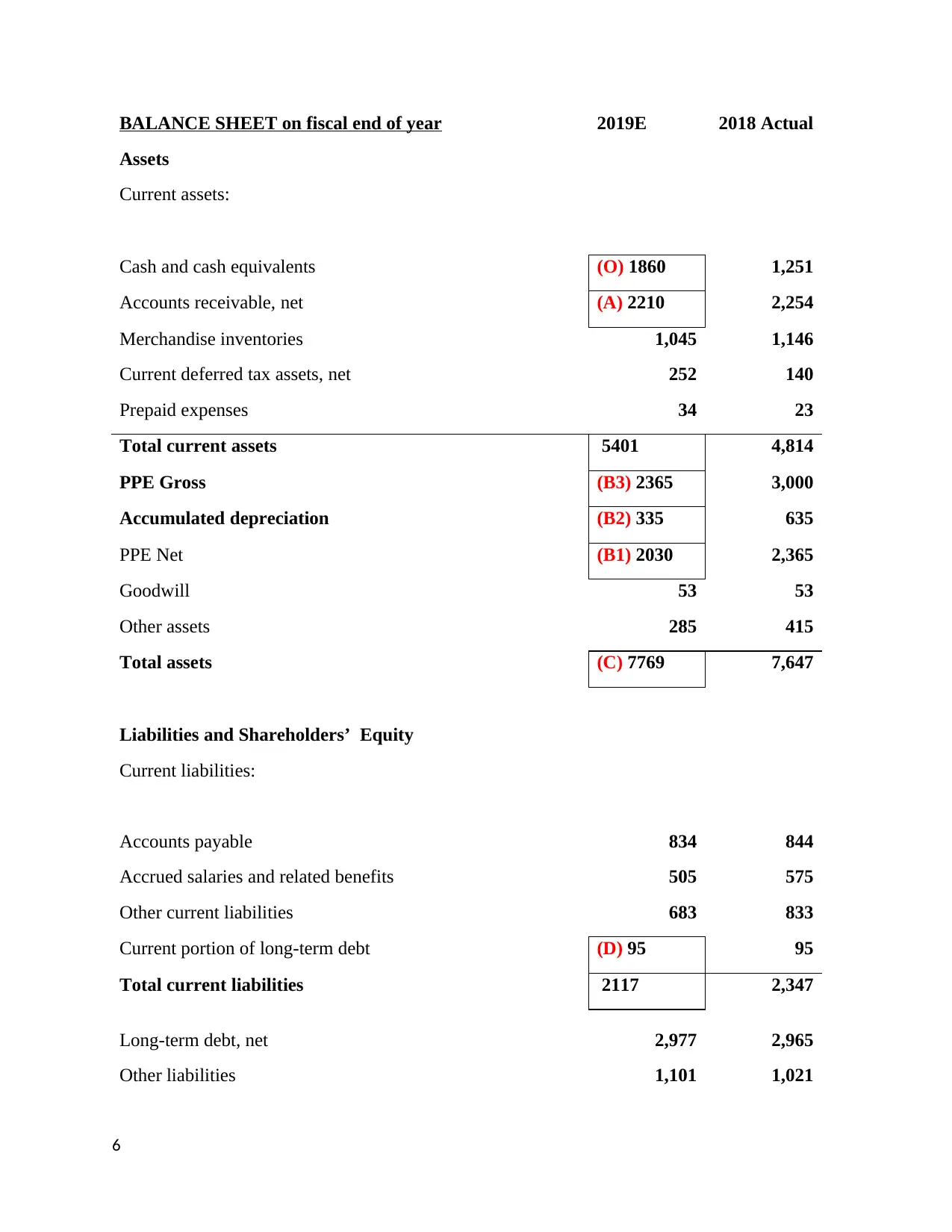

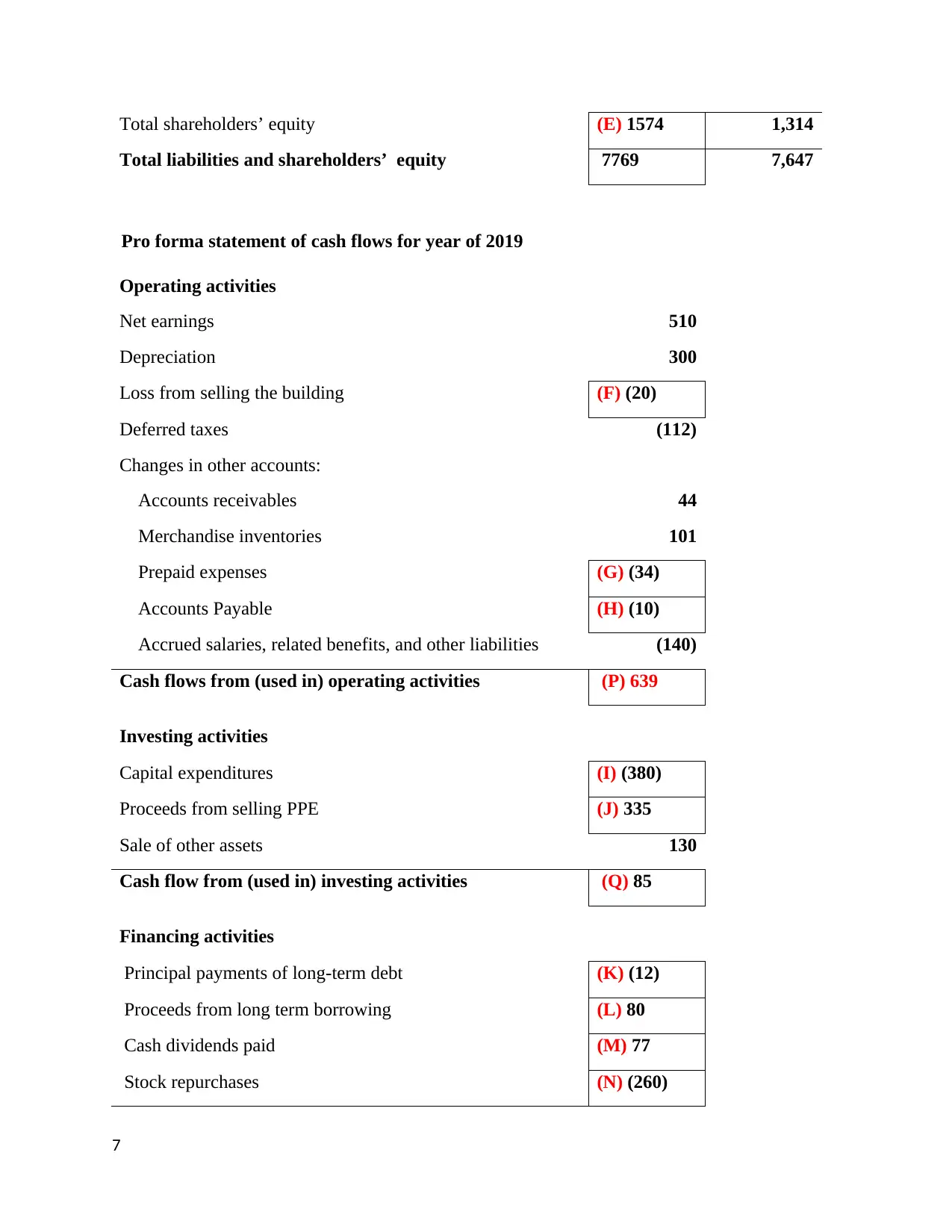

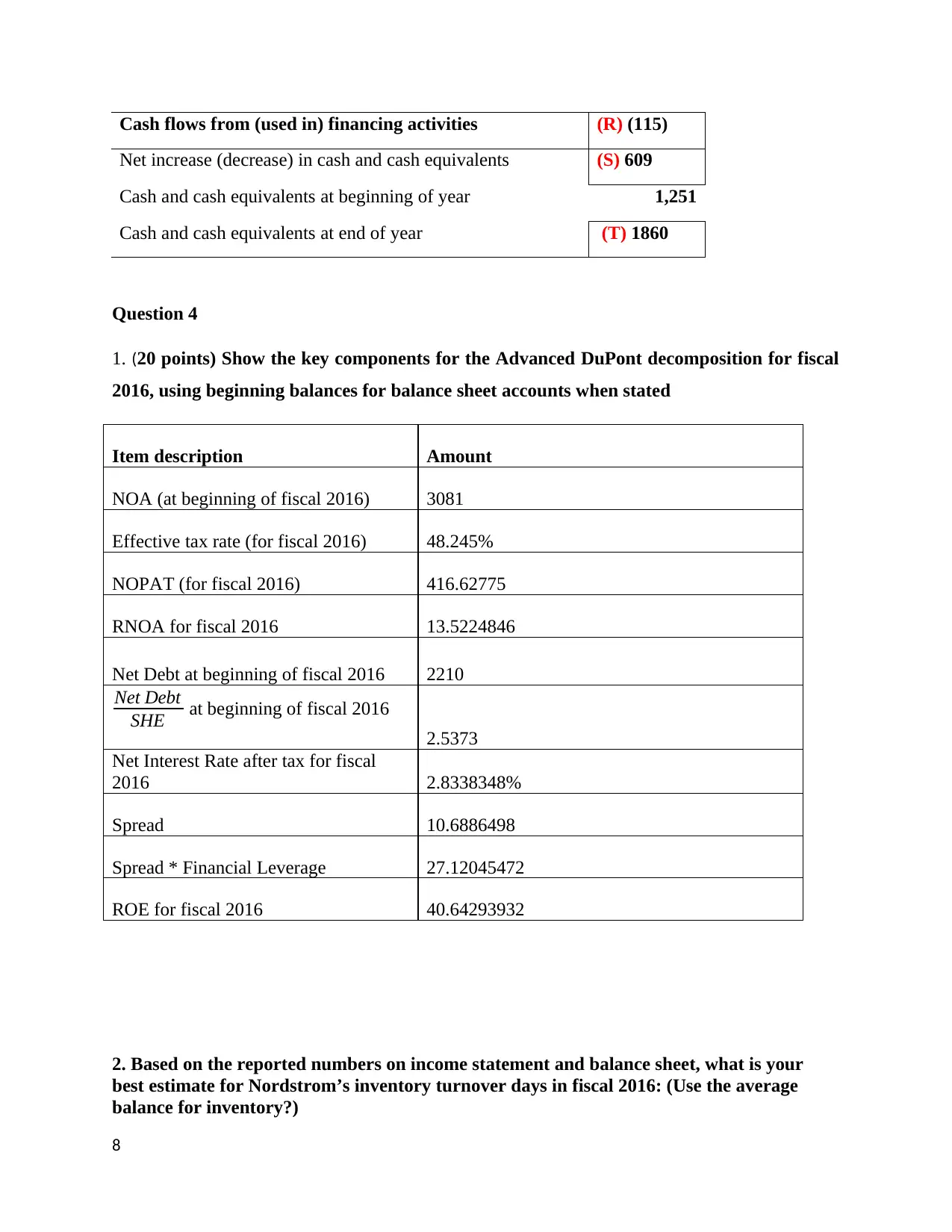

This assignment solution provides a detailed financial analysis report, addressing multiple questions related to accounting principles and financial statement analysis. It covers topics such as the impact of changes in useful life estimates on free cash flow, the interpretation of average days payables outstanding, and the effect of financial leverage on return on equity (ROE). The solution also includes an analysis of cash flow statements, categorizing them into mature/decline and introductory/growth phases based on cash flow patterns. Furthermore, it presents a pro forma income statement, balance sheet, and statement of cash flows for fiscal year 2019E. The report concludes with an evaluation of Nordstrom's financial performance, including a DuPont decomposition analysis, inventory turnover days calculation, cash cycle days, and an assessment of its credit card receivables and free cash flow. The solutions provided here are contributed by students, and Desklib offers a wide array of study tools including past papers and solved assignments to help students excel in their studies.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.