City & Islington College: Financial Budgeting and Analysis Homework

VerifiedAdded on 2022/11/29

|7

|1213

|86

Homework Assignment

AI Summary

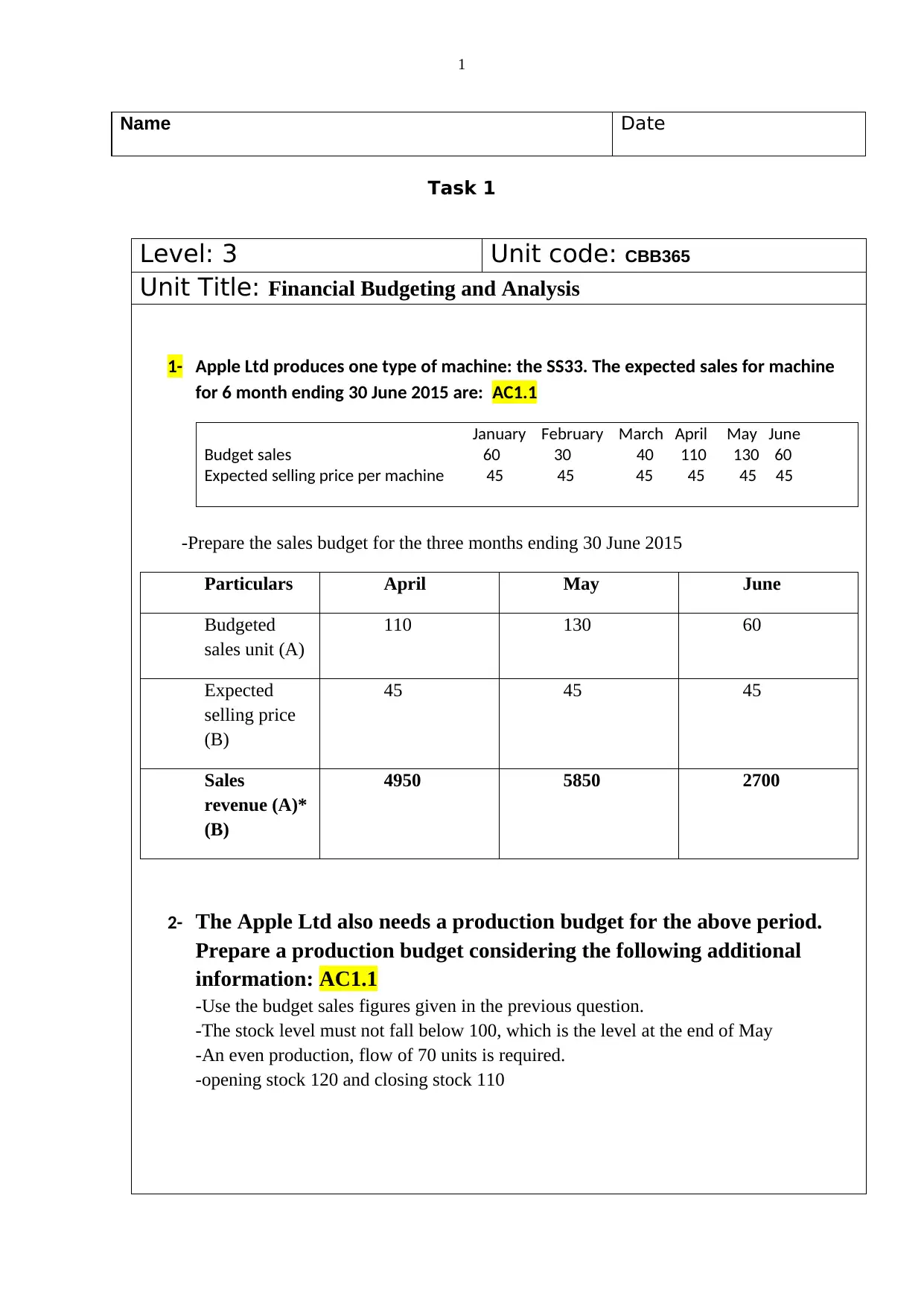

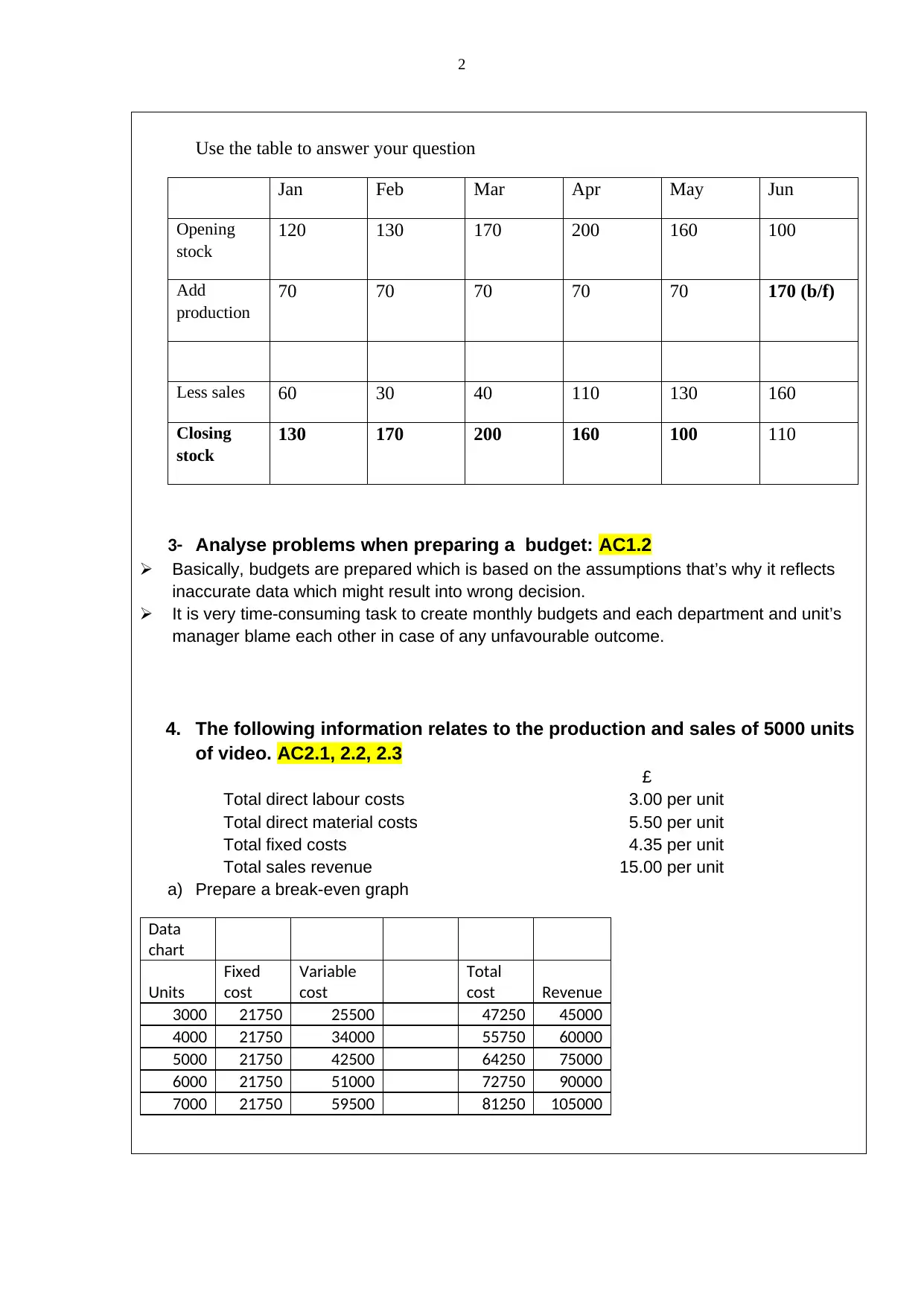

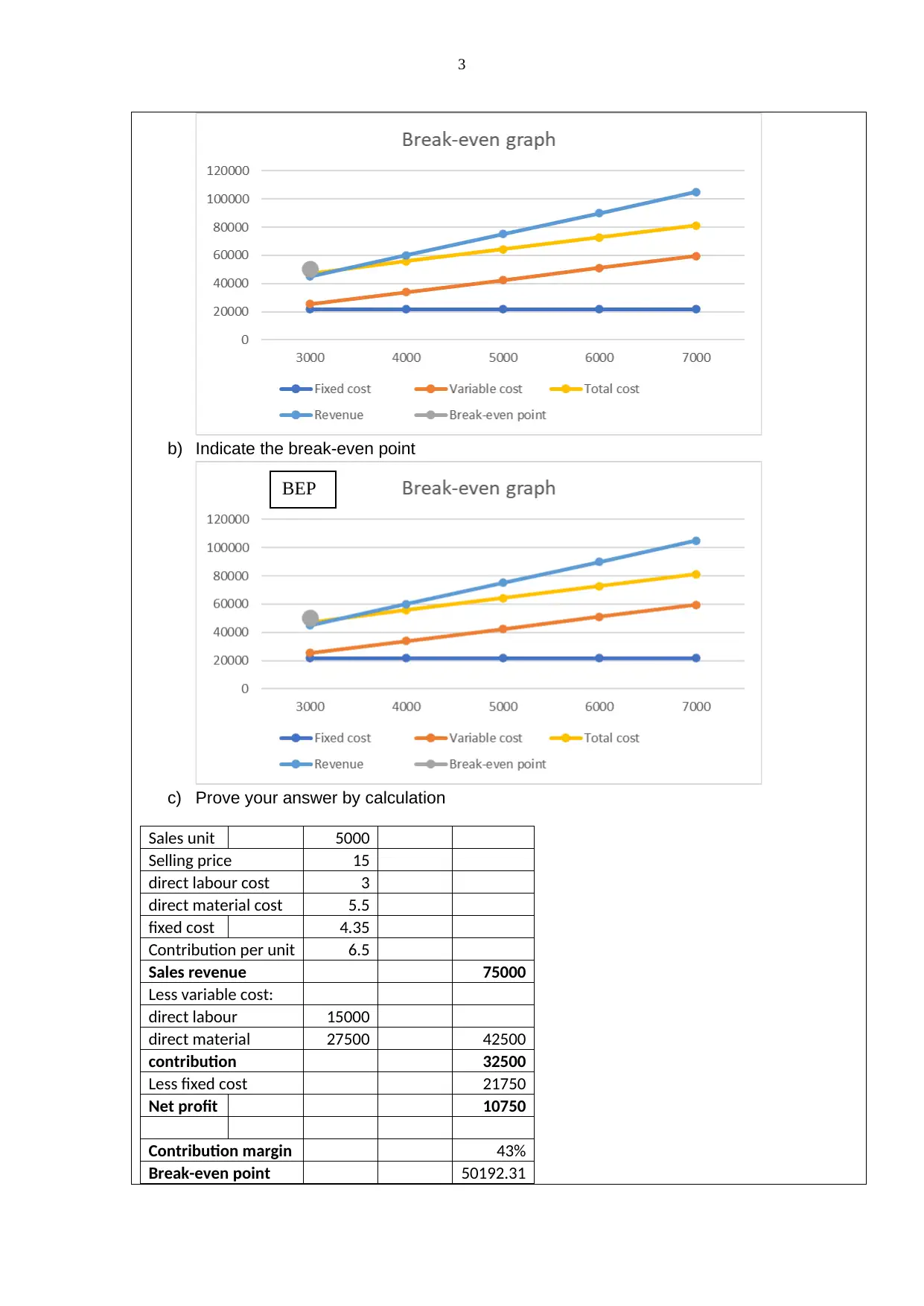

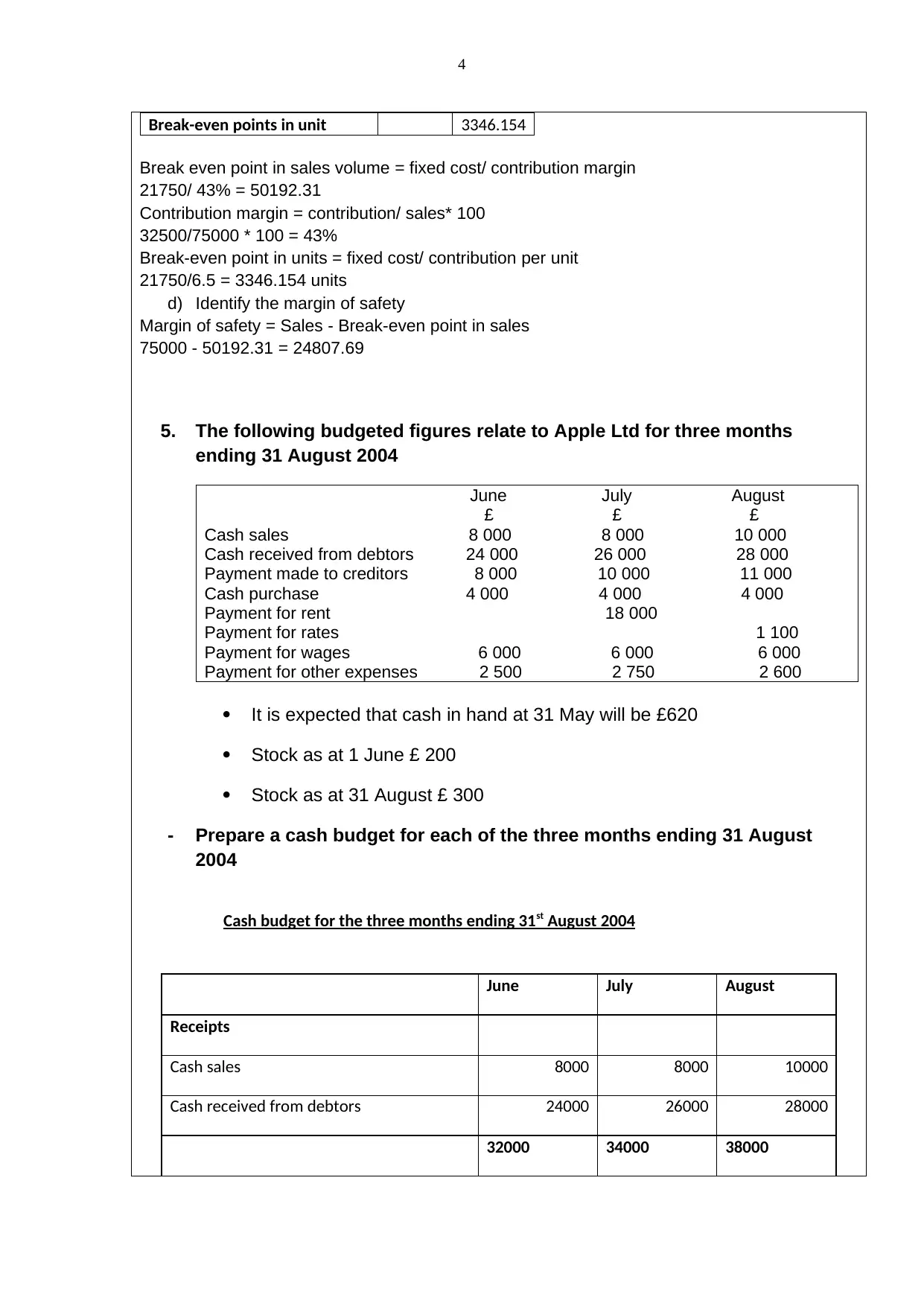

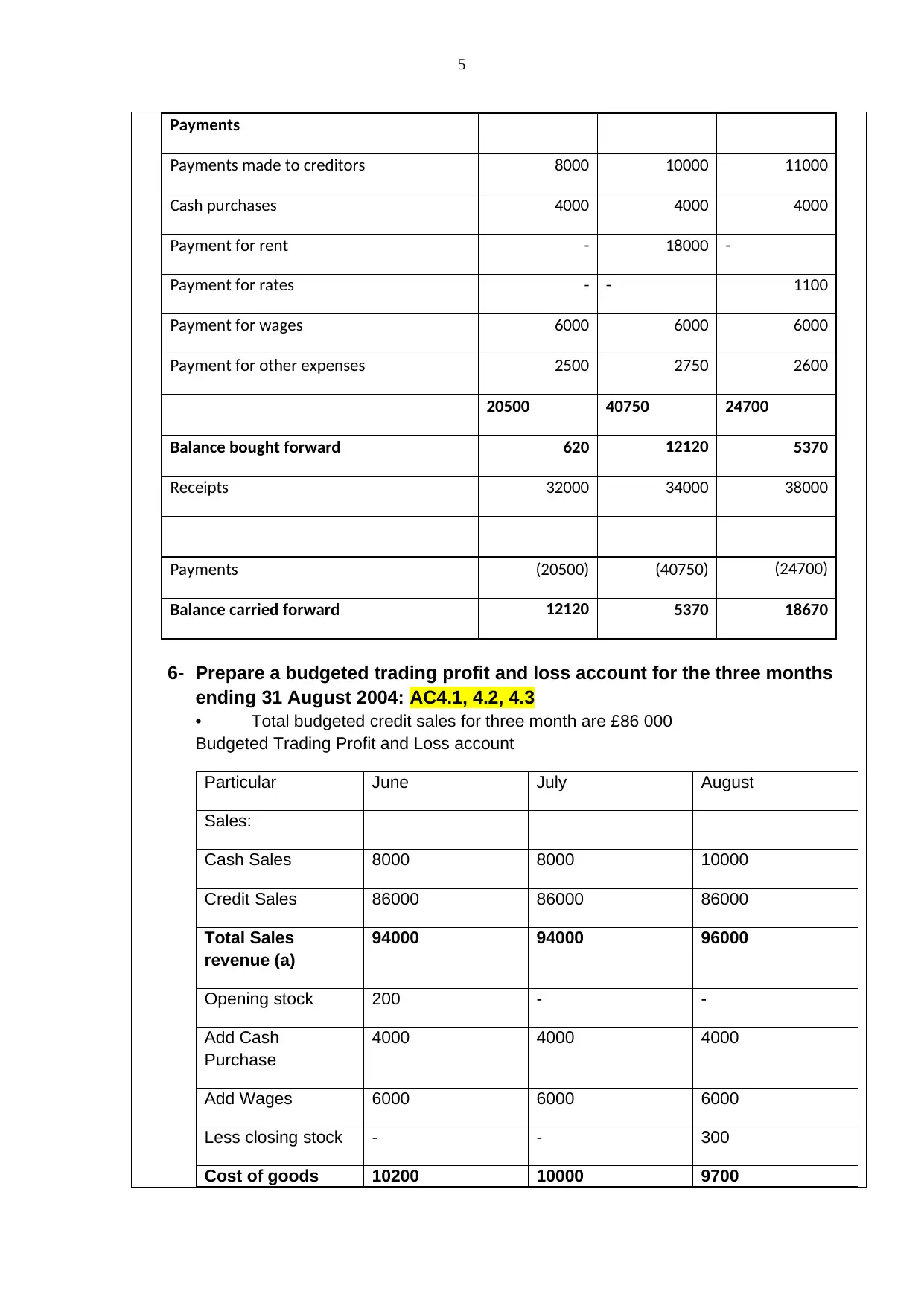

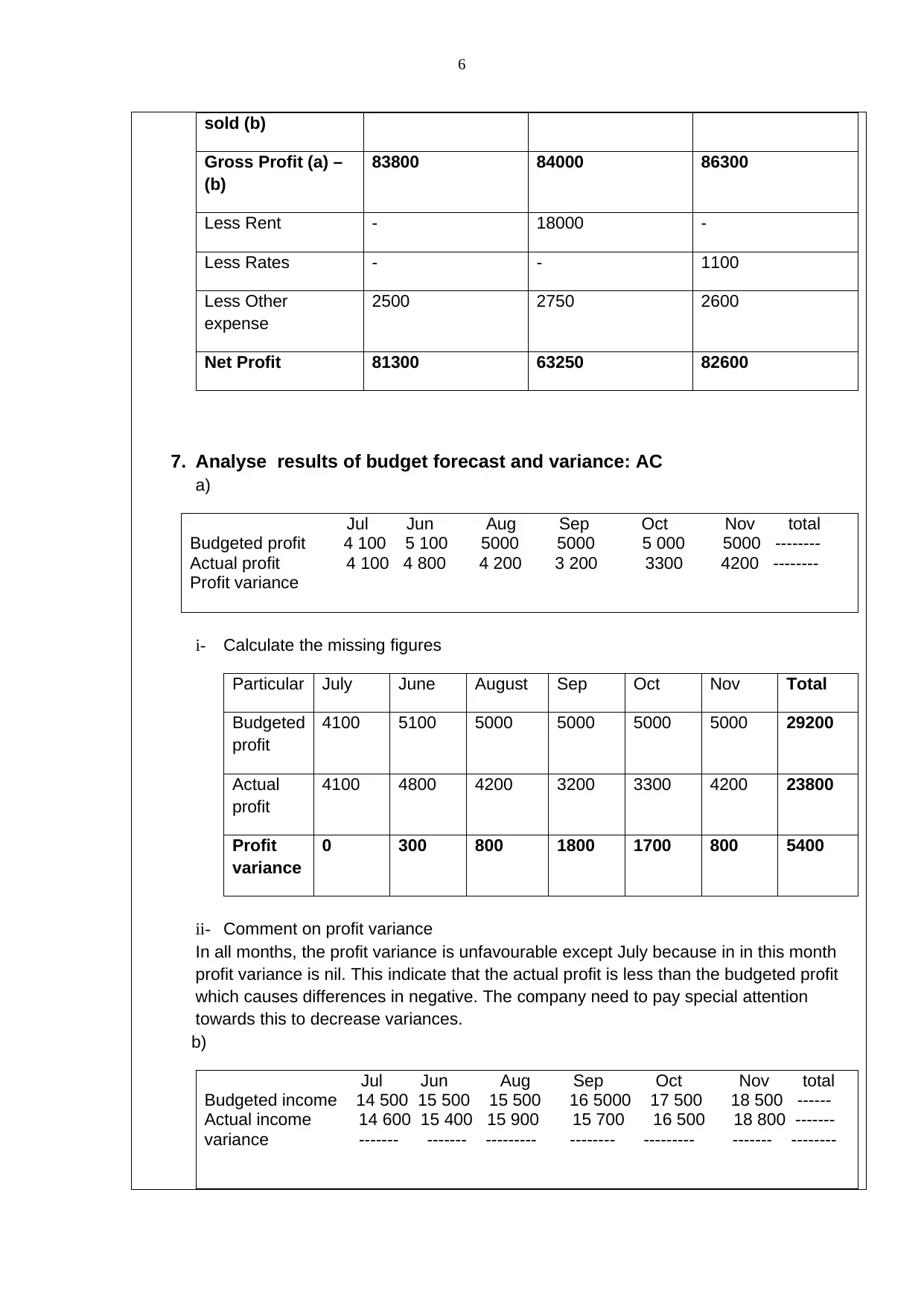

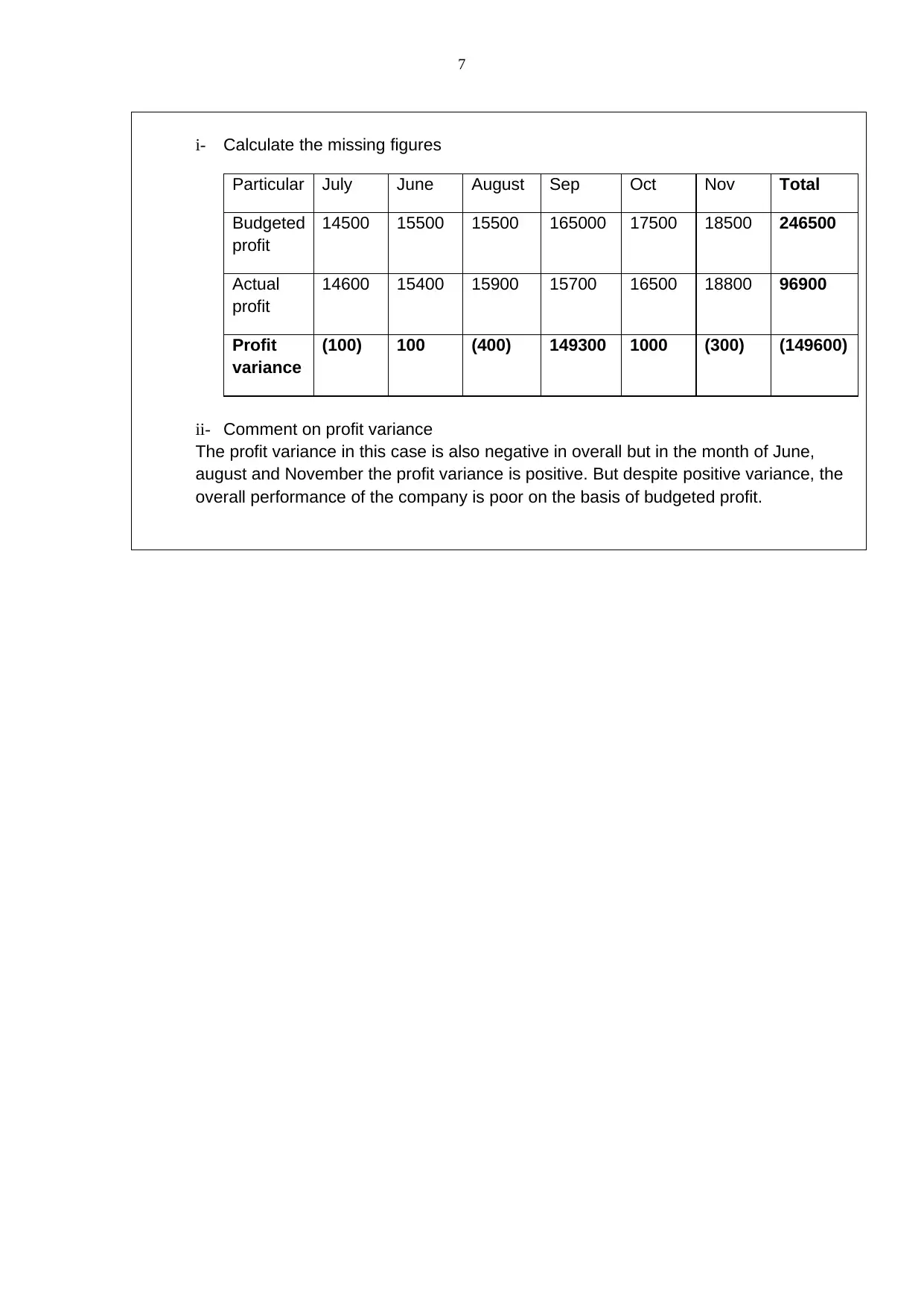

This assignment solution addresses key concepts in financial budgeting and analysis, using Apple Ltd as a case study. It includes the creation of sales and production budgets, along with a break-even analysis to determine profitability. The solution further explores cash budgeting for a three-month period, incorporating cash sales and debtor receipts. A budgeted trading profit and loss account is prepared, and the analysis extends to budget forecast results and variance analysis. The assignment also delves into cost behavior, examining variable, fixed, mixed, and step-variable costs and their impact on budget preparation. It covers marginal costing and provides a detailed breakdown of calculations and interpretations to aid in understanding the practical application of financial planning principles.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.