Managerial Finance Report: Financial Analysis of Coach Inc.

VerifiedAdded on 2020/10/23

|9

|2032

|203

Report

AI Summary

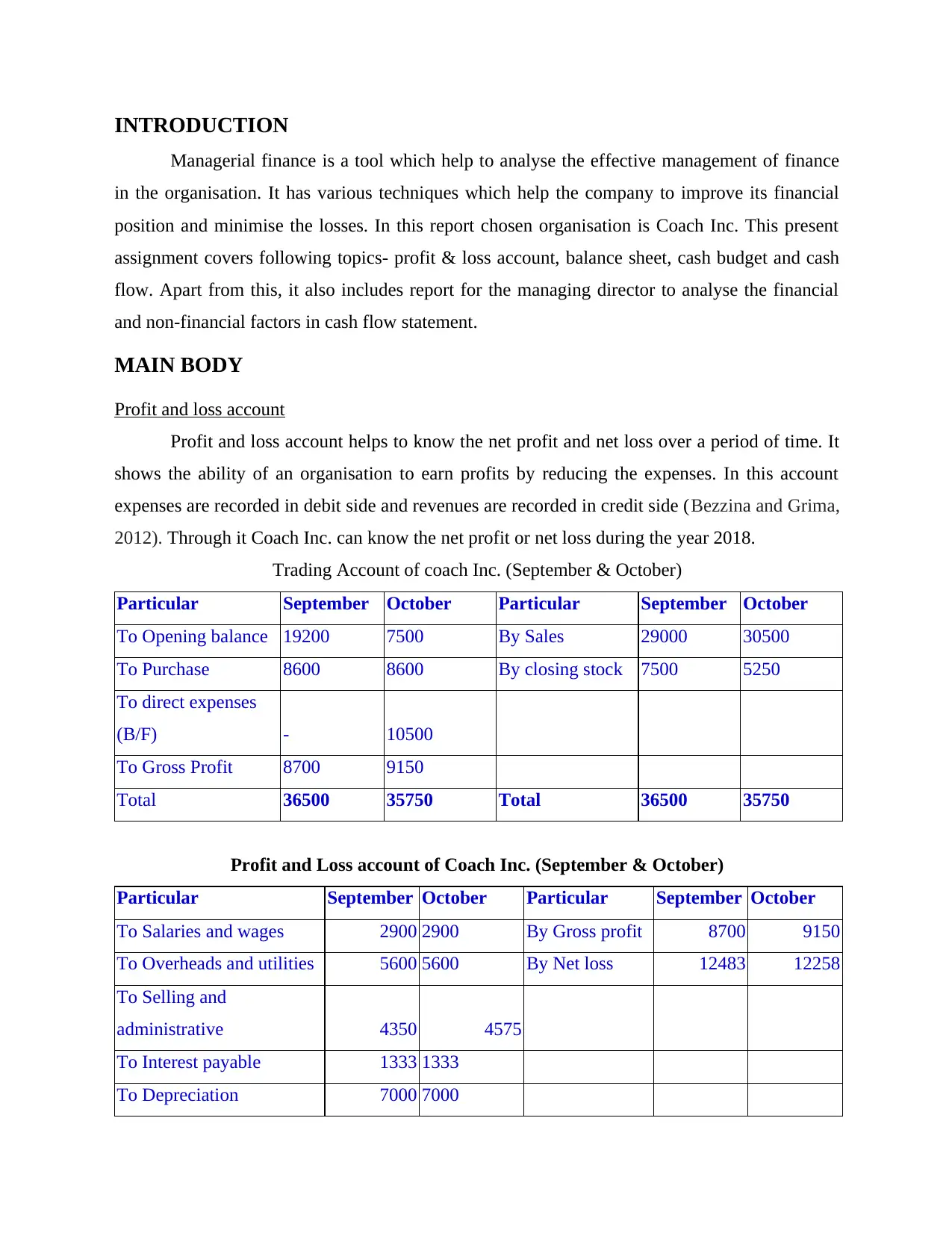

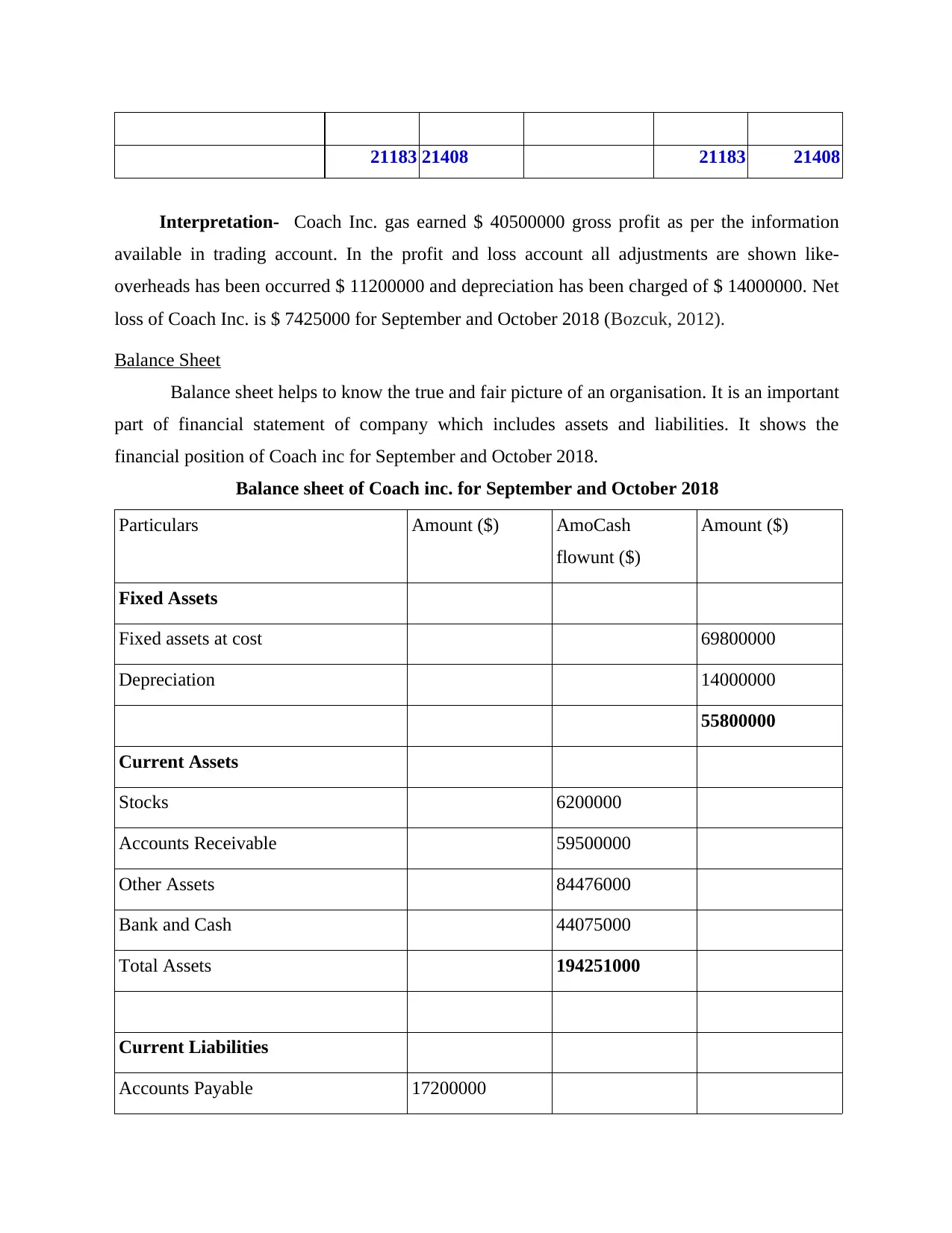

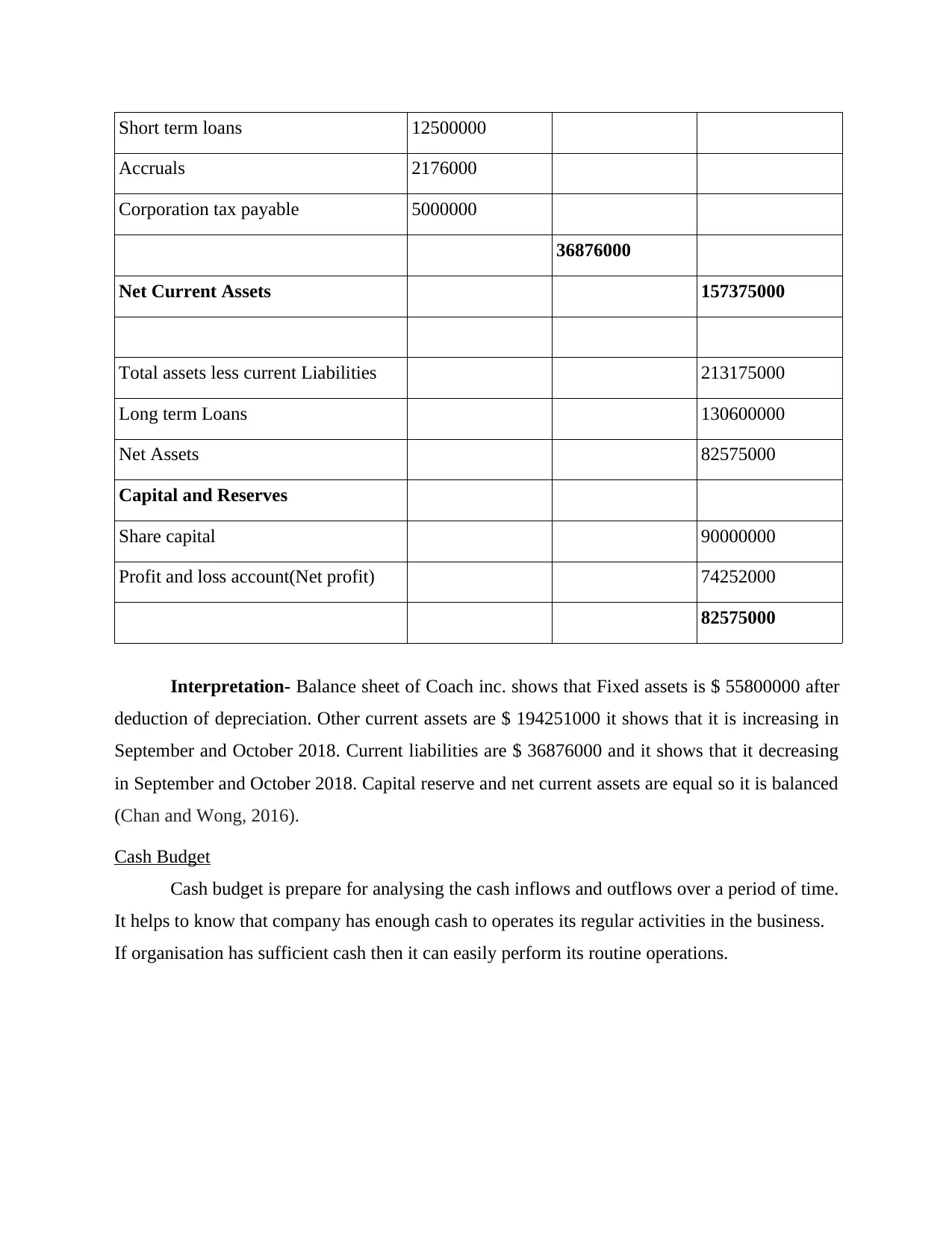

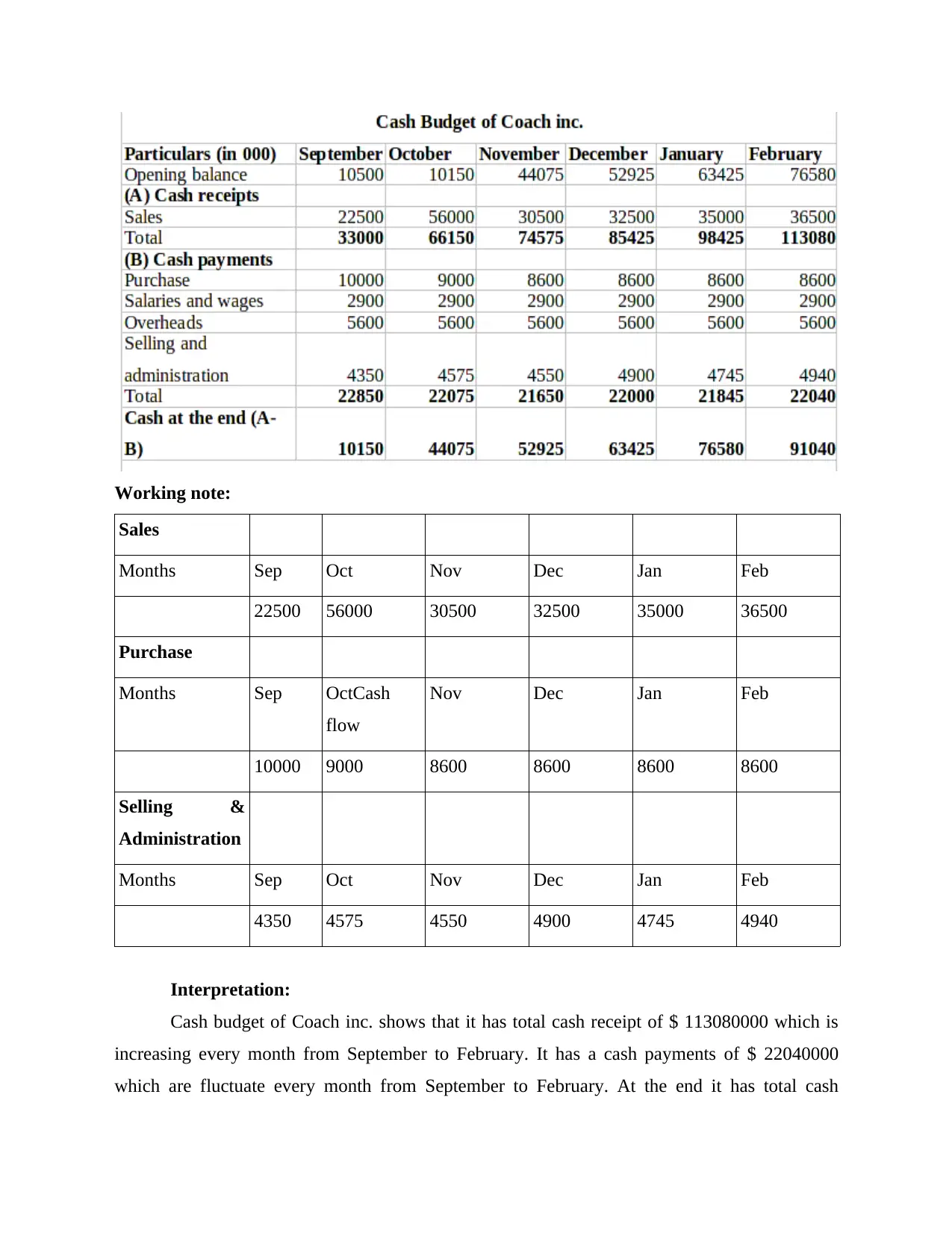

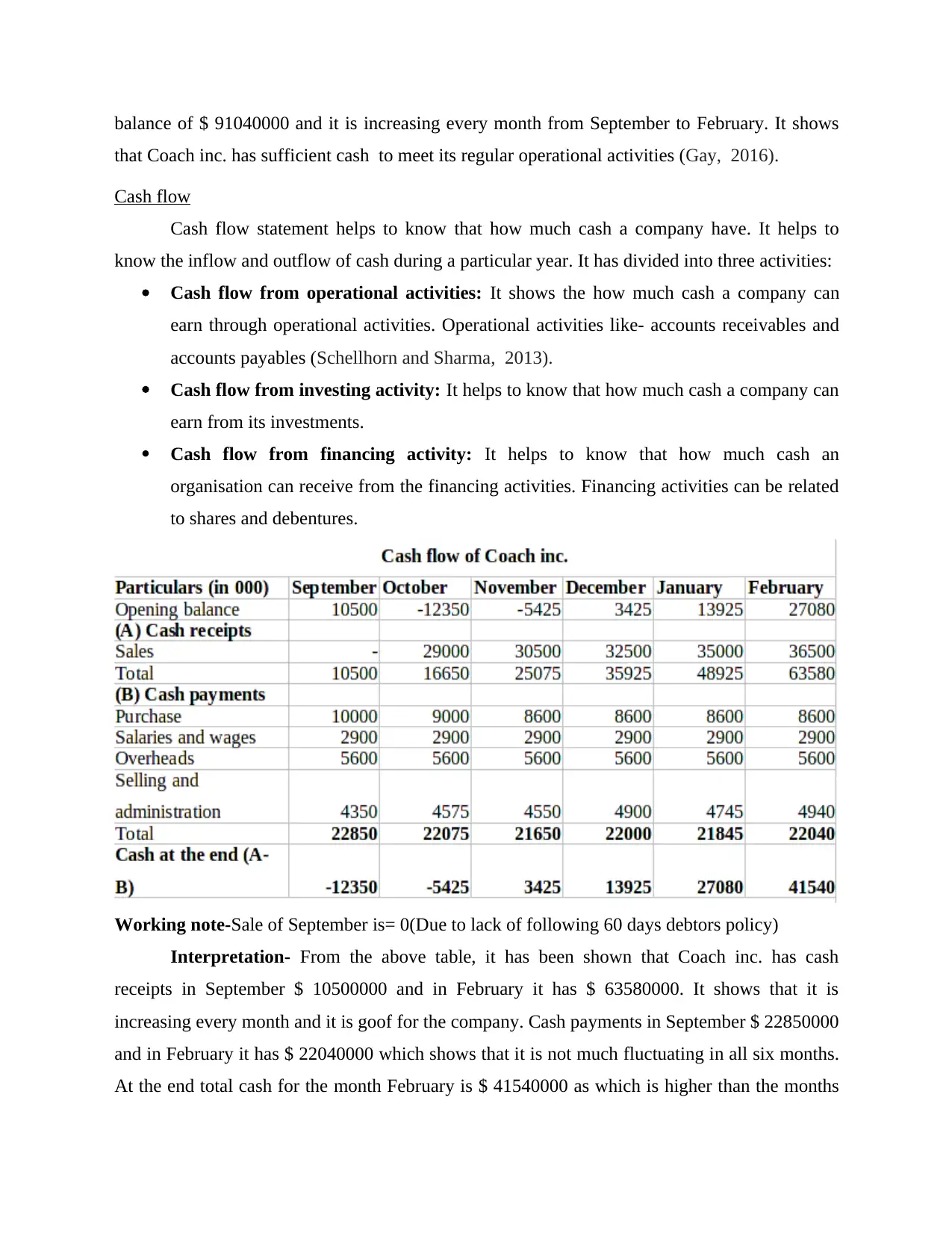

This managerial finance report provides a comprehensive analysis of Coach Inc.'s financial performance. It begins with an introduction to managerial finance and its importance, followed by an examination of Coach Inc.'s profit and loss account, balance sheet, cash budget, and cash flow statement. The report analyzes the company's financial position, including gross profit, net loss, current assets, and liabilities. It also includes a detailed cash budget and cash flow analysis, providing insights into the company's cash inflows and outflows. The report concludes with recommendations for the managing directors, suggesting strategies to improve cash flow management, such as reducing the time for debtors' collection and optimizing payment terms with suppliers. The analysis highlights the importance of effective cash flow management for maintaining operational activities and overall financial health. The report references various financial management concepts and techniques to provide a clear understanding of the company's financial standing and future strategies.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.