Financial Analysis of Coca-Cola: Performance and Competitor Comparison

VerifiedAdded on 2022/08/08

|21

|3423

|17

Report

AI Summary

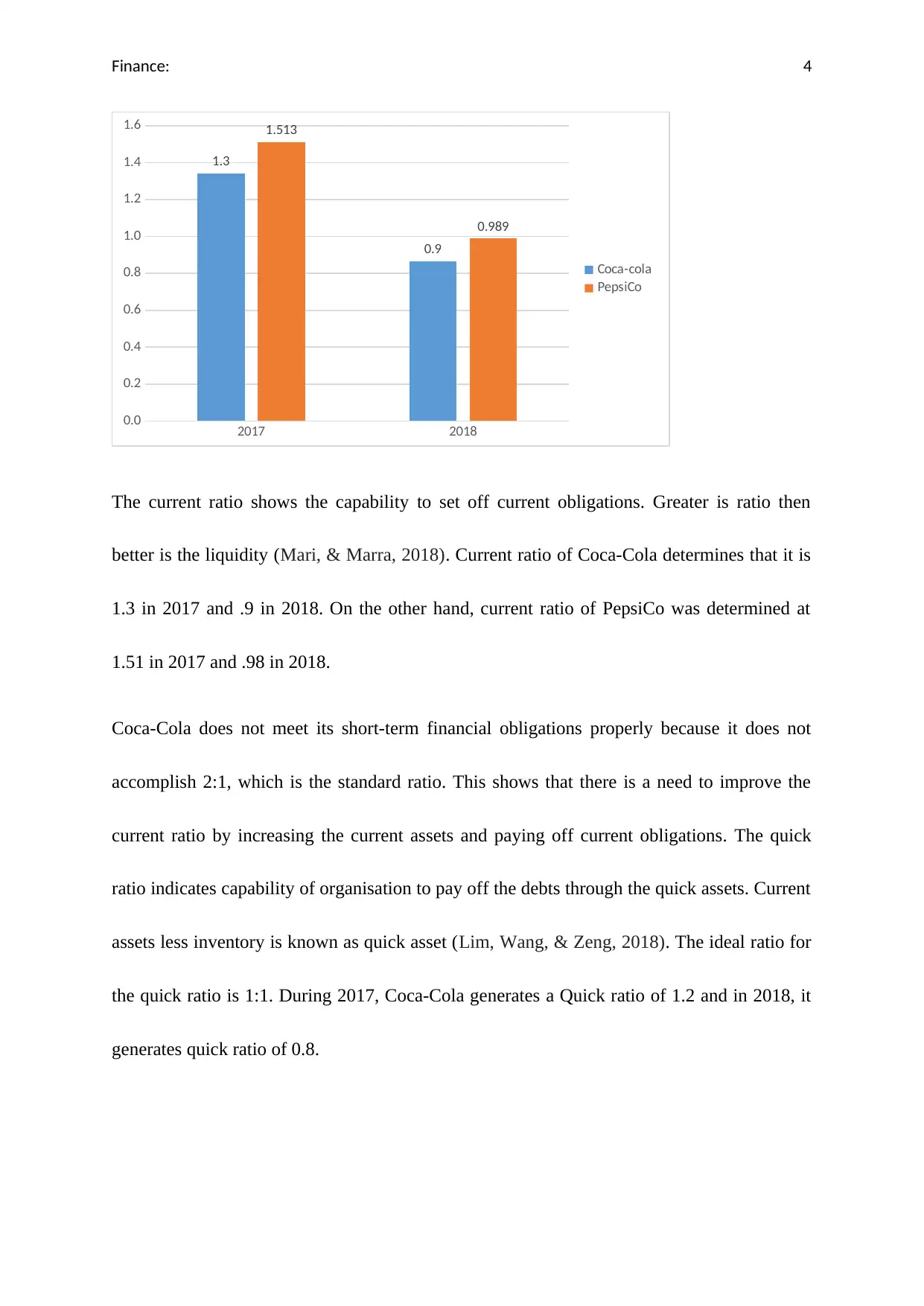

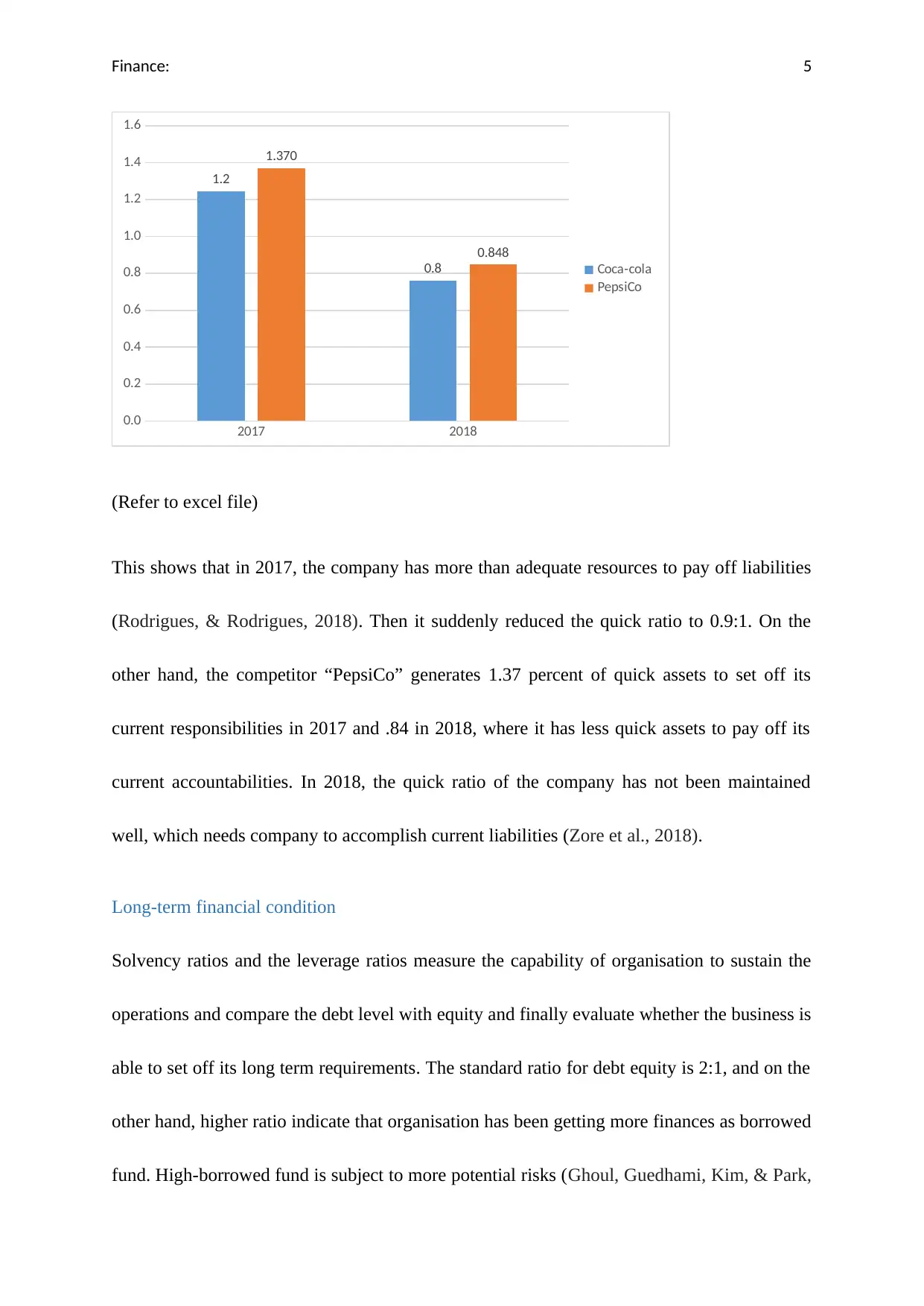

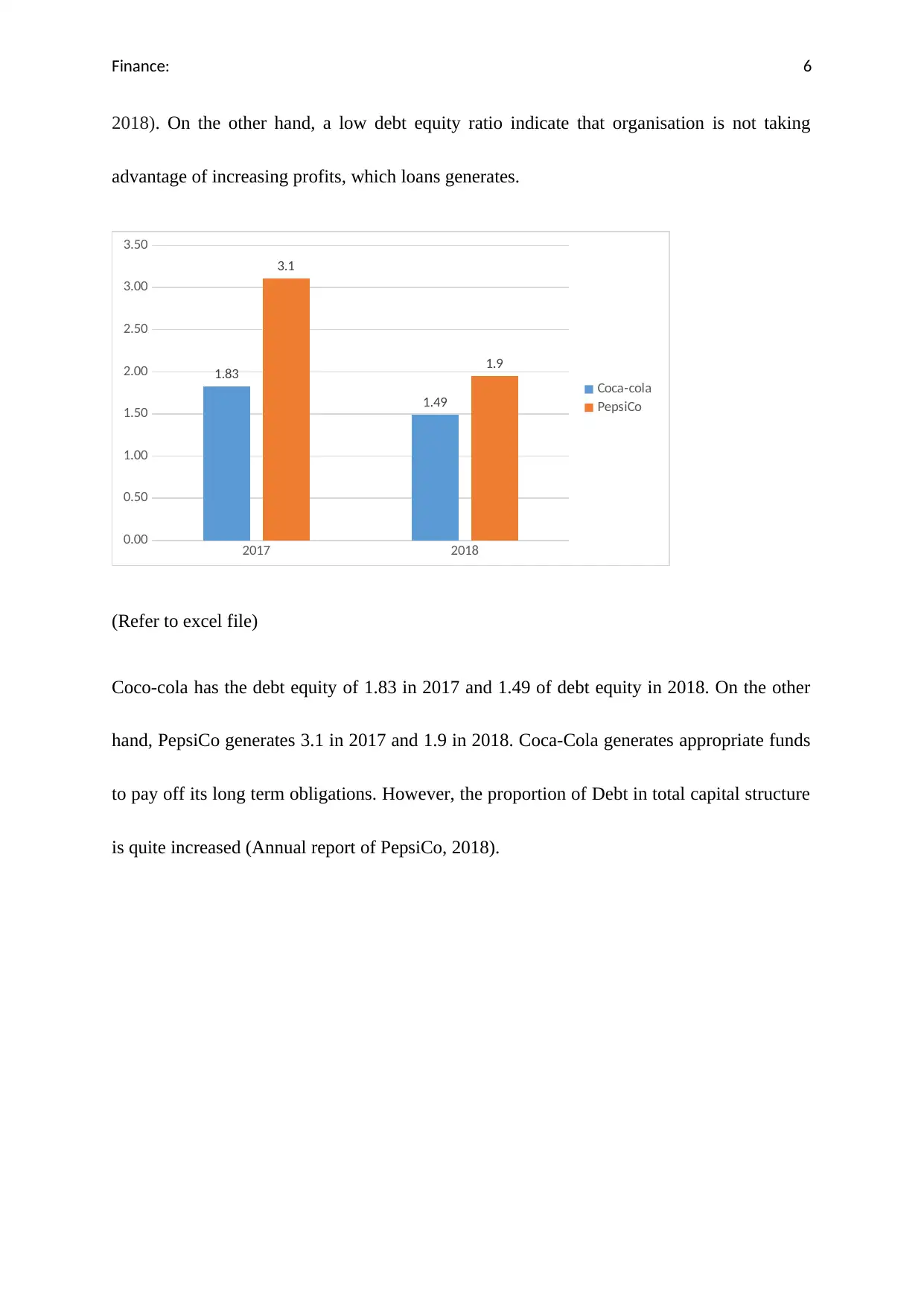

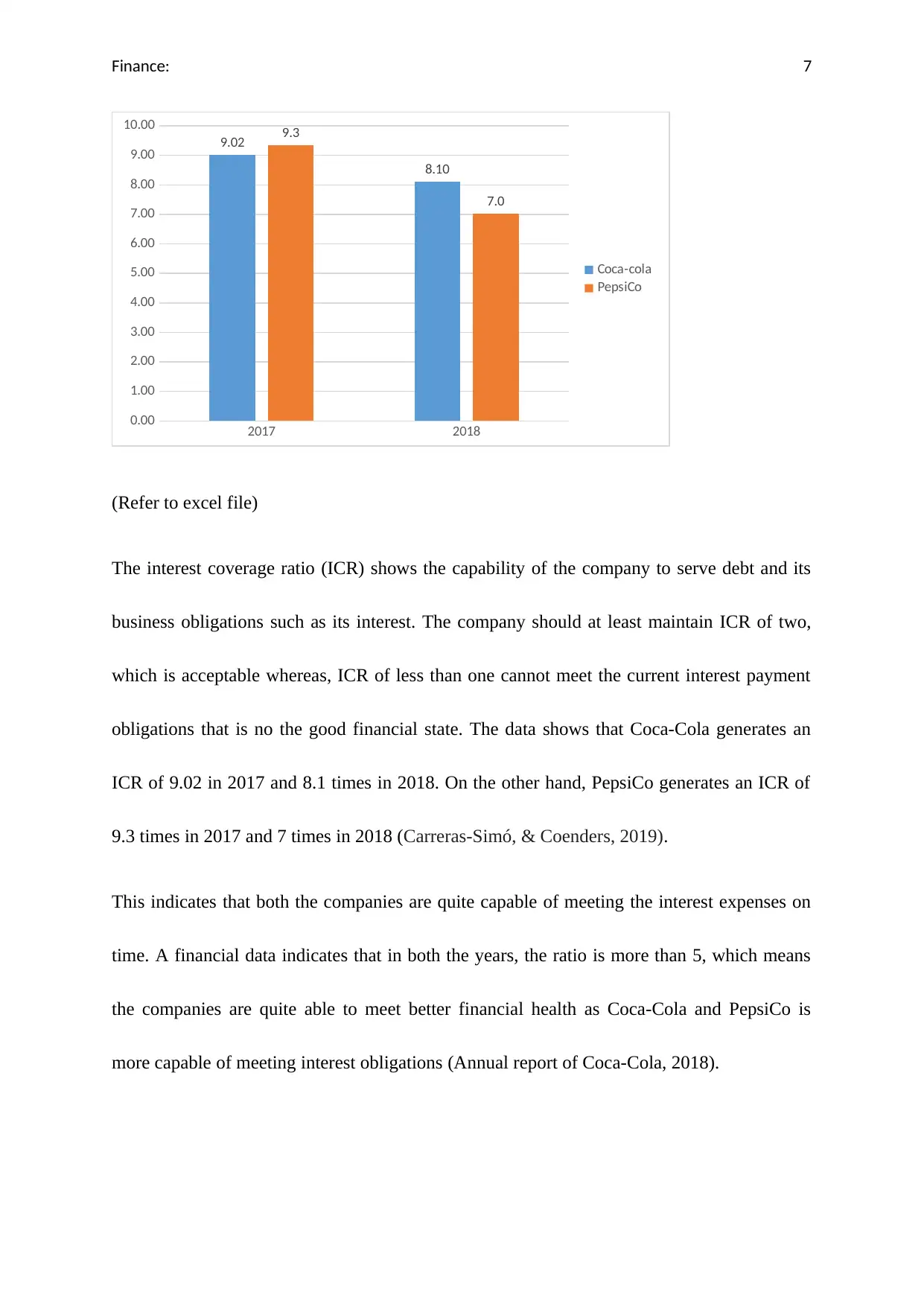

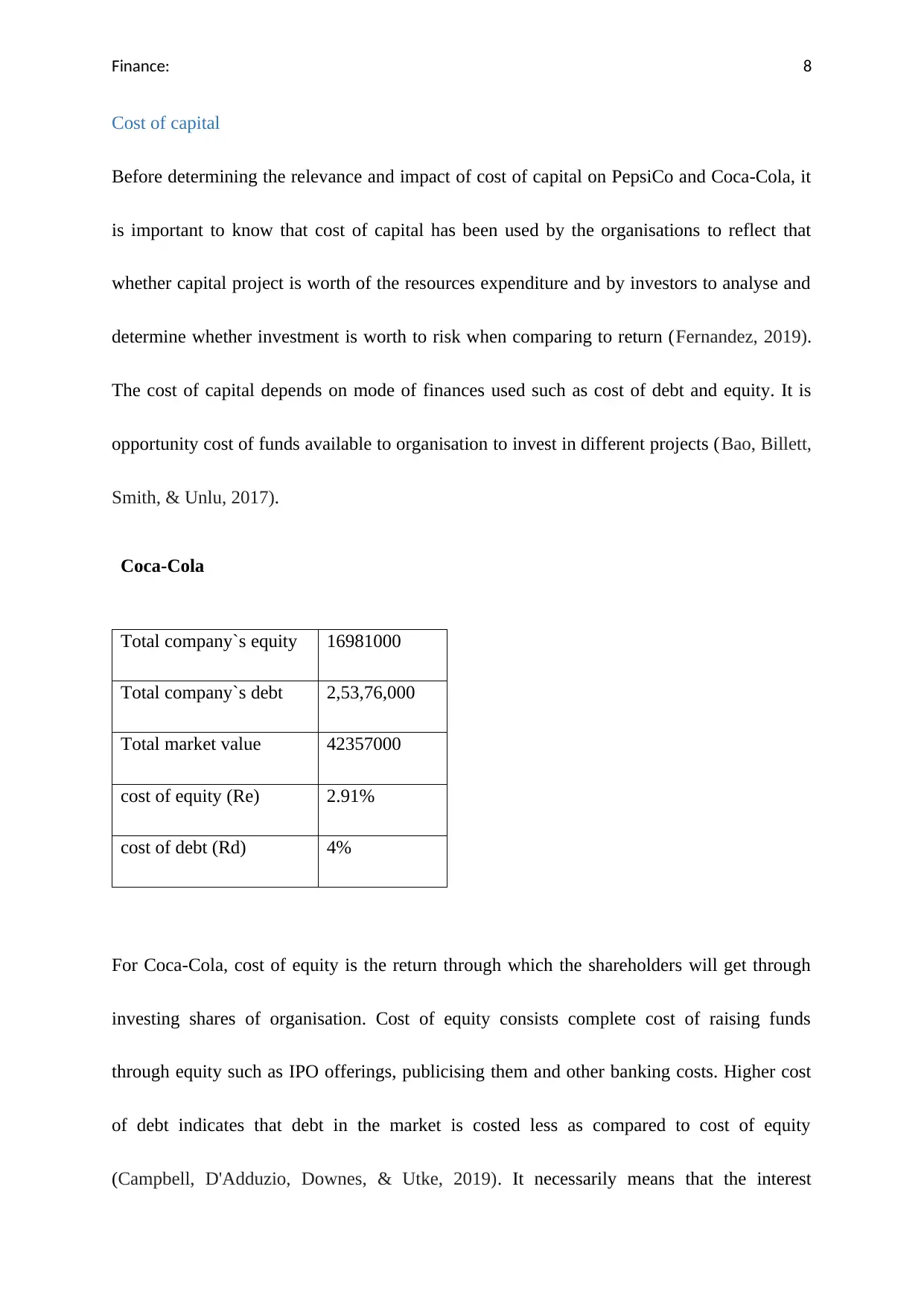

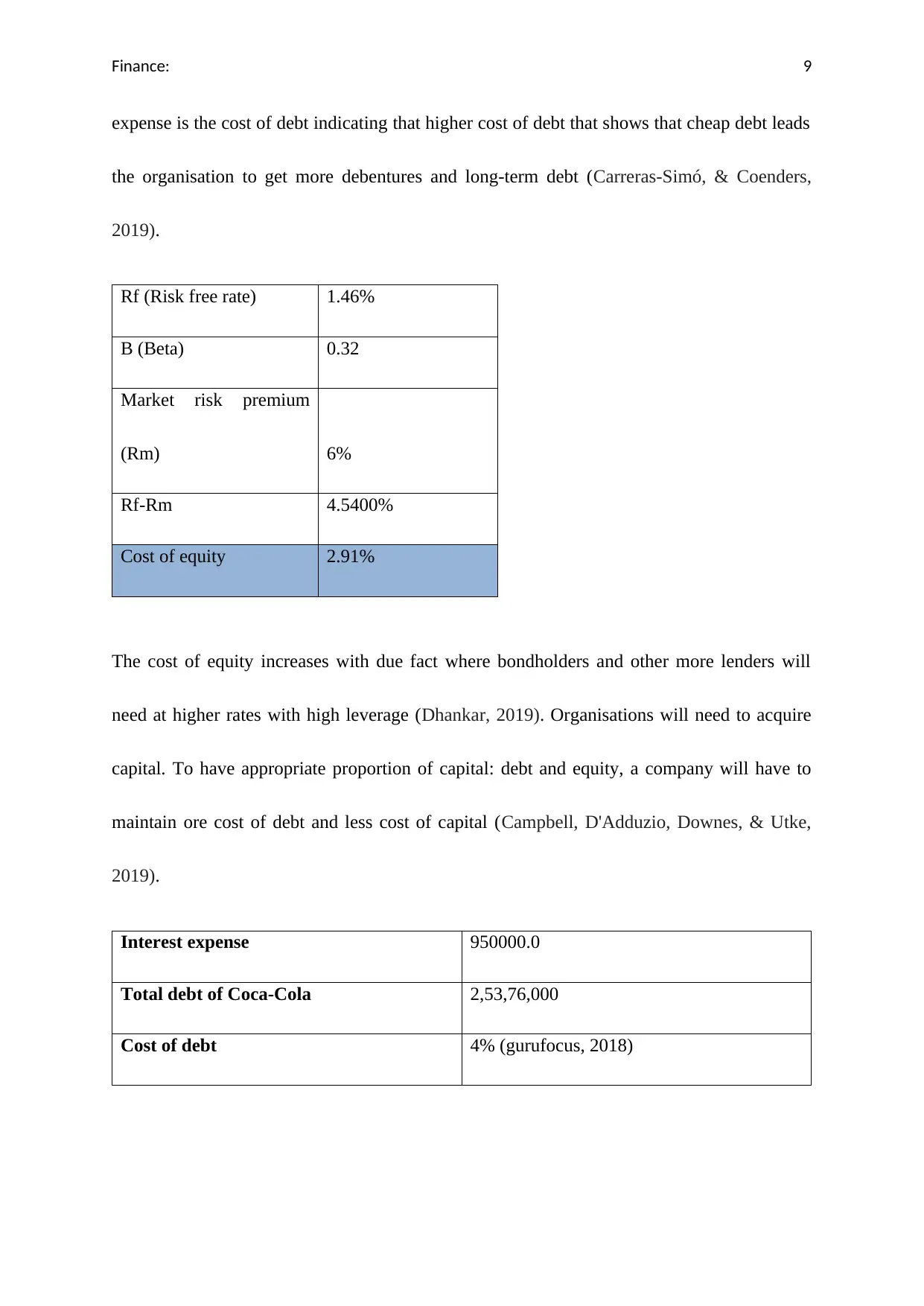

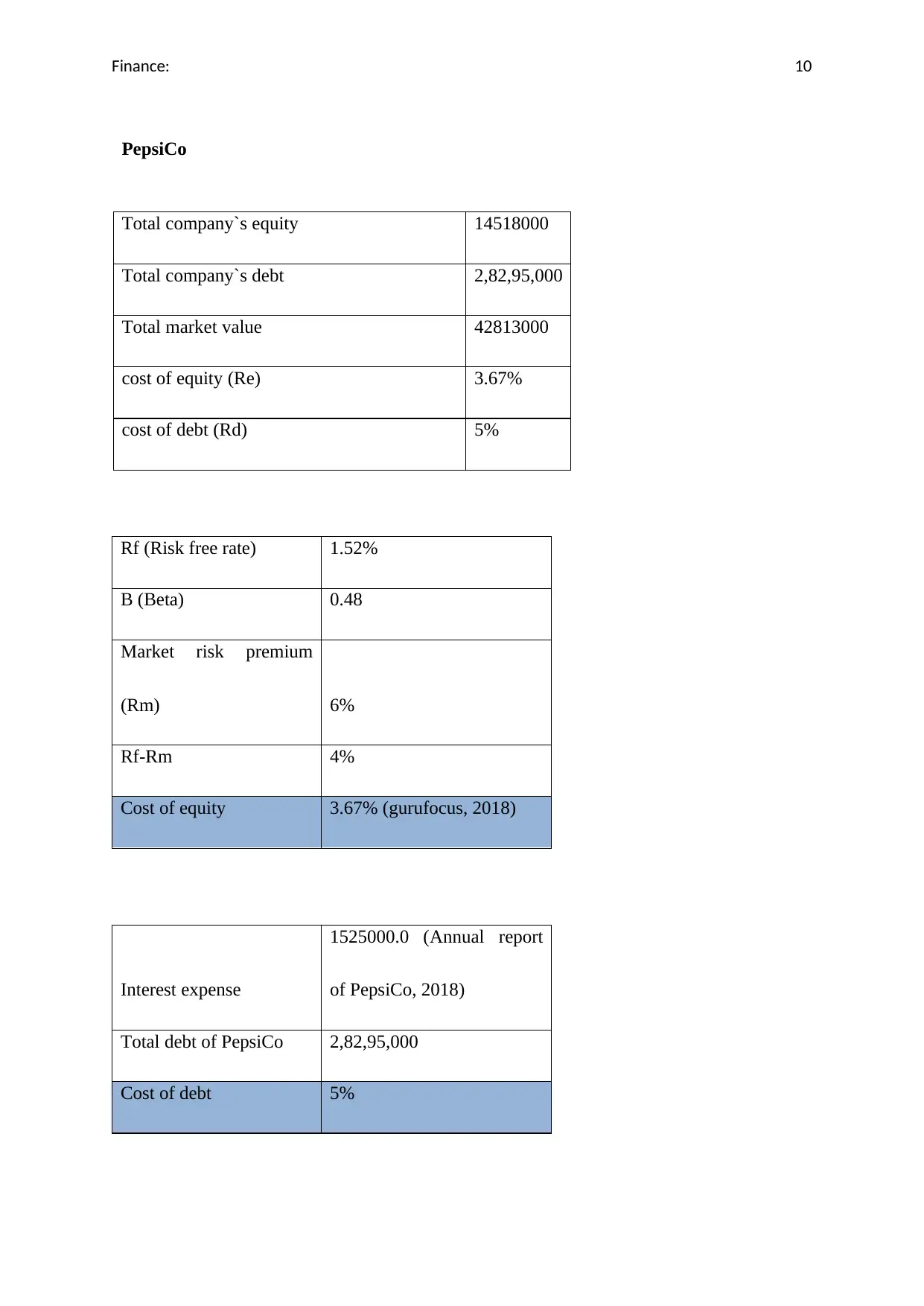

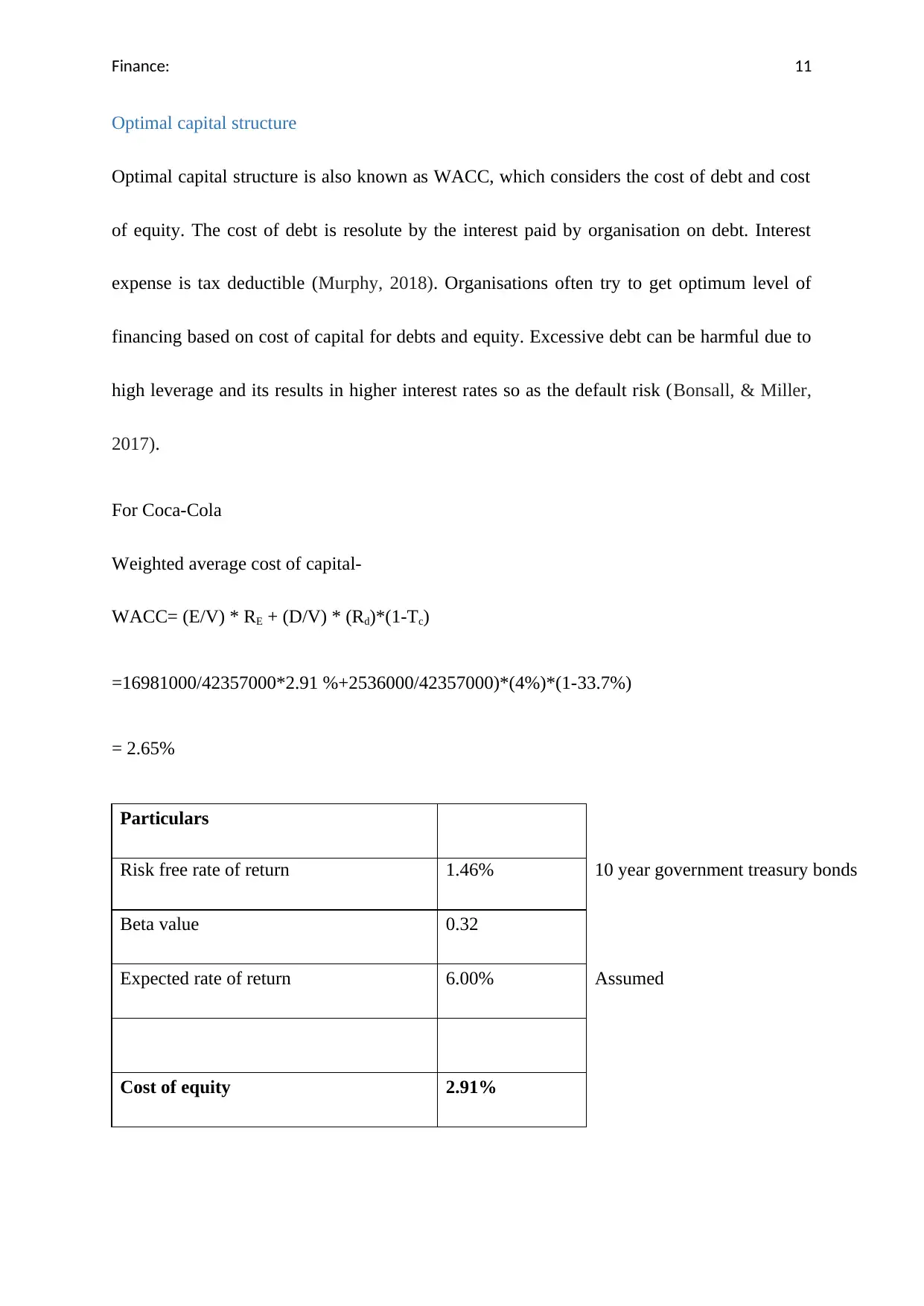

This report presents a detailed financial analysis of Coca-Cola, evaluating its performance and comparing it to its competitor, PepsiCo. The analysis begins with an introduction to the importance of financial statement analysis and the application of financial techniques. The report examines Coca-Cola's short-term and long-term financial conditions using ratio analysis, including liquidity ratios and solvency ratios. Furthermore, it delves into the calculation of the weighted average cost of capital (WACC) to evaluate projected returns for equity and debt holders. The report also assesses the present value of the company's operations. The findings indicate Coca-Cola's financial health, liquidity, and solvency, providing insights into its ability to meet short-term and long-term obligations. The report also includes a comparison of Coca-Cola and PepsiCo's WACC and present value. The conclusion summarizes the key findings and offers insights into the company's overall financial performance.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.