Financial Analysis and Decision Making Report (Module Finance)

VerifiedAdded on 2020/04/21

|17

|4907

|39

Report

AI Summary

This report provides a comprehensive financial analysis of two cases: Splinter Sports Equipment Manufacturing Limited and Cocoaland Holdings Berhad. The first case focuses on cost analysis, specifically addressing a loss-making production process (Round process) and recommends strategies to mitigate losses and improve the cost sheet. The second case involves a detailed financial analysis of Cocoaland Holdings Berhad, employing ratio analysis to assess liquidity, profitability, efficiency, and capital structure. The report aims to provide insights for better decision-making, including whether to discontinue a production process and how to evaluate a company's financial health. It also includes recasting of data and offers recommendations based on the financial analysis performed.

Running Head: Managerial Accounting

1

Project Head: Managerial Accounting

1

Project Head: Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting

2

Contents

Introduction.......................................................................................................................3

Que 1.................................................................................................................................3

Decision about Round process......................................................................................3

Recasting the above data..............................................................................................4

Que 2.................................................................................................................................5

Company overview...........................................................................................................5

Objective of the report......................................................................................................6

Financial statement analysis.............................................................................................6

Liquidity.......................................................................................................................7

Profitability...................................................................................................................8

Efficiency......................................................................................................................9

Capital structure..........................................................................................................10

Findings..........................................................................................................................11

Conclusion:.....................................................................................................................11

References.......................................................................................................................13

Appendix.........................................................................................................................15

2

Contents

Introduction.......................................................................................................................3

Que 1.................................................................................................................................3

Decision about Round process......................................................................................3

Recasting the above data..............................................................................................4

Que 2.................................................................................................................................5

Company overview...........................................................................................................5

Objective of the report......................................................................................................6

Financial statement analysis.............................................................................................6

Liquidity.......................................................................................................................7

Profitability...................................................................................................................8

Efficiency......................................................................................................................9

Capital structure..........................................................................................................10

Findings..........................................................................................................................11

Conclusion:.....................................................................................................................11

References.......................................................................................................................13

Appendix.........................................................................................................................15

Managerial Accounting

3

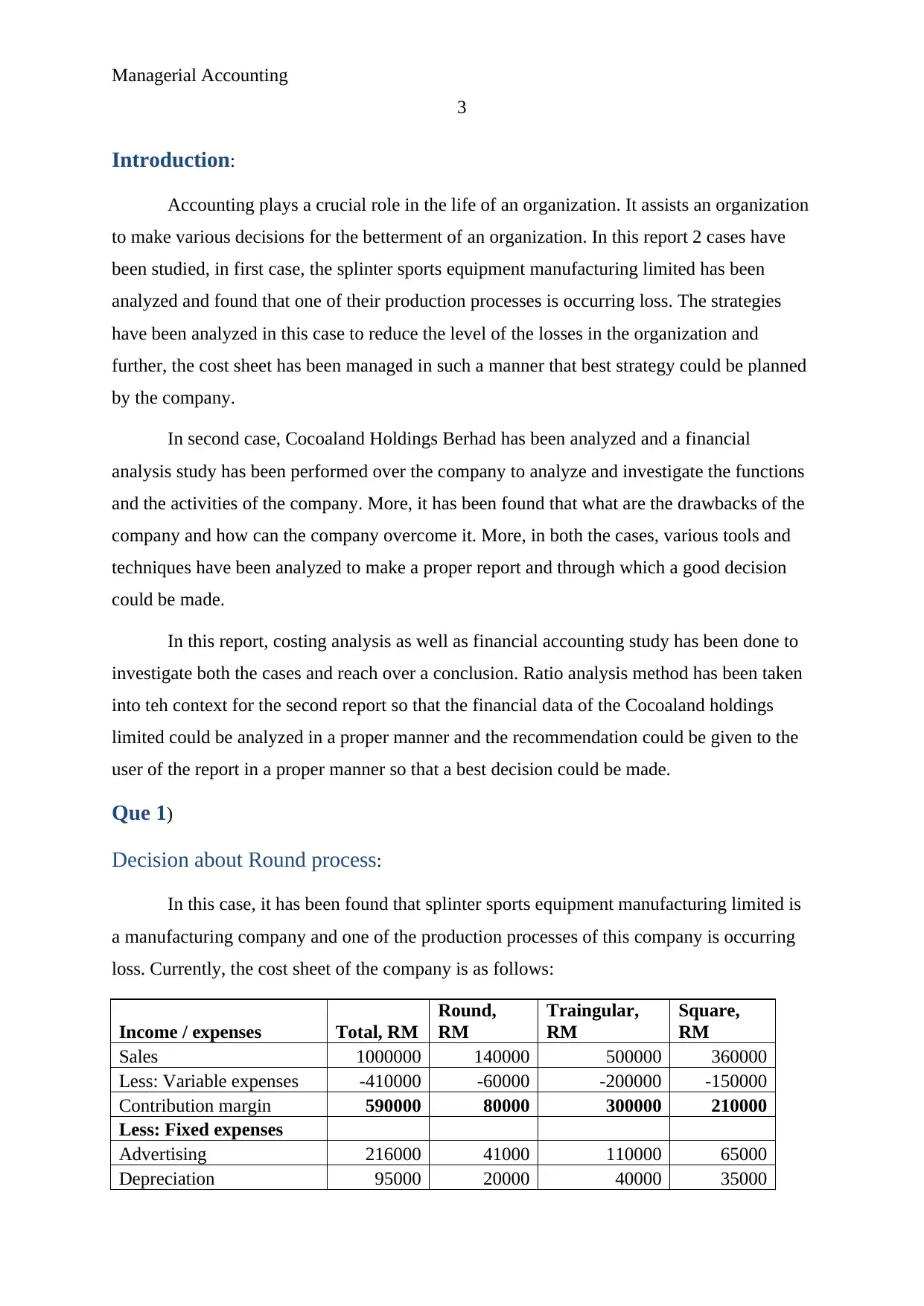

Introduction:

Accounting plays a crucial role in the life of an organization. It assists an organization

to make various decisions for the betterment of an organization. In this report 2 cases have

been studied, in first case, the splinter sports equipment manufacturing limited has been

analyzed and found that one of their production processes is occurring loss. The strategies

have been analyzed in this case to reduce the level of the losses in the organization and

further, the cost sheet has been managed in such a manner that best strategy could be planned

by the company.

In second case, Cocoaland Holdings Berhad has been analyzed and a financial

analysis study has been performed over the company to analyze and investigate the functions

and the activities of the company. More, it has been found that what are the drawbacks of the

company and how can the company overcome it. More, in both the cases, various tools and

techniques have been analyzed to make a proper report and through which a good decision

could be made.

In this report, costing analysis as well as financial accounting study has been done to

investigate both the cases and reach over a conclusion. Ratio analysis method has been taken

into teh context for the second report so that the financial data of the Cocoaland holdings

limited could be analyzed in a proper manner and the recommendation could be given to the

user of the report in a proper manner so that a best decision could be made.

Que 1)

Decision about Round process:

In this case, it has been found that splinter sports equipment manufacturing limited is

a manufacturing company and one of the production processes of this company is occurring

loss. Currently, the cost sheet of the company is as follows:

Income / expenses Total, RM

Round,

RM

Traingular,

RM

Square,

RM

Sales 1000000 140000 500000 360000

Less: Variable expenses -410000 -60000 -200000 -150000

Contribution margin 590000 80000 300000 210000

Less: Fixed expenses

Advertising 216000 41000 110000 65000

Depreciation 95000 20000 40000 35000

3

Introduction:

Accounting plays a crucial role in the life of an organization. It assists an organization

to make various decisions for the betterment of an organization. In this report 2 cases have

been studied, in first case, the splinter sports equipment manufacturing limited has been

analyzed and found that one of their production processes is occurring loss. The strategies

have been analyzed in this case to reduce the level of the losses in the organization and

further, the cost sheet has been managed in such a manner that best strategy could be planned

by the company.

In second case, Cocoaland Holdings Berhad has been analyzed and a financial

analysis study has been performed over the company to analyze and investigate the functions

and the activities of the company. More, it has been found that what are the drawbacks of the

company and how can the company overcome it. More, in both the cases, various tools and

techniques have been analyzed to make a proper report and through which a good decision

could be made.

In this report, costing analysis as well as financial accounting study has been done to

investigate both the cases and reach over a conclusion. Ratio analysis method has been taken

into teh context for the second report so that the financial data of the Cocoaland holdings

limited could be analyzed in a proper manner and the recommendation could be given to the

user of the report in a proper manner so that a best decision could be made.

Que 1)

Decision about Round process:

In this case, it has been found that splinter sports equipment manufacturing limited is

a manufacturing company and one of the production processes of this company is occurring

loss. Currently, the cost sheet of the company is as follows:

Income / expenses Total, RM

Round,

RM

Traingular,

RM

Square,

RM

Sales 1000000 140000 500000 360000

Less: Variable expenses -410000 -60000 -200000 -150000

Contribution margin 590000 80000 300000 210000

Less: Fixed expenses

Advertising 216000 41000 110000 65000

Depreciation 95000 20000 40000 35000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting

4

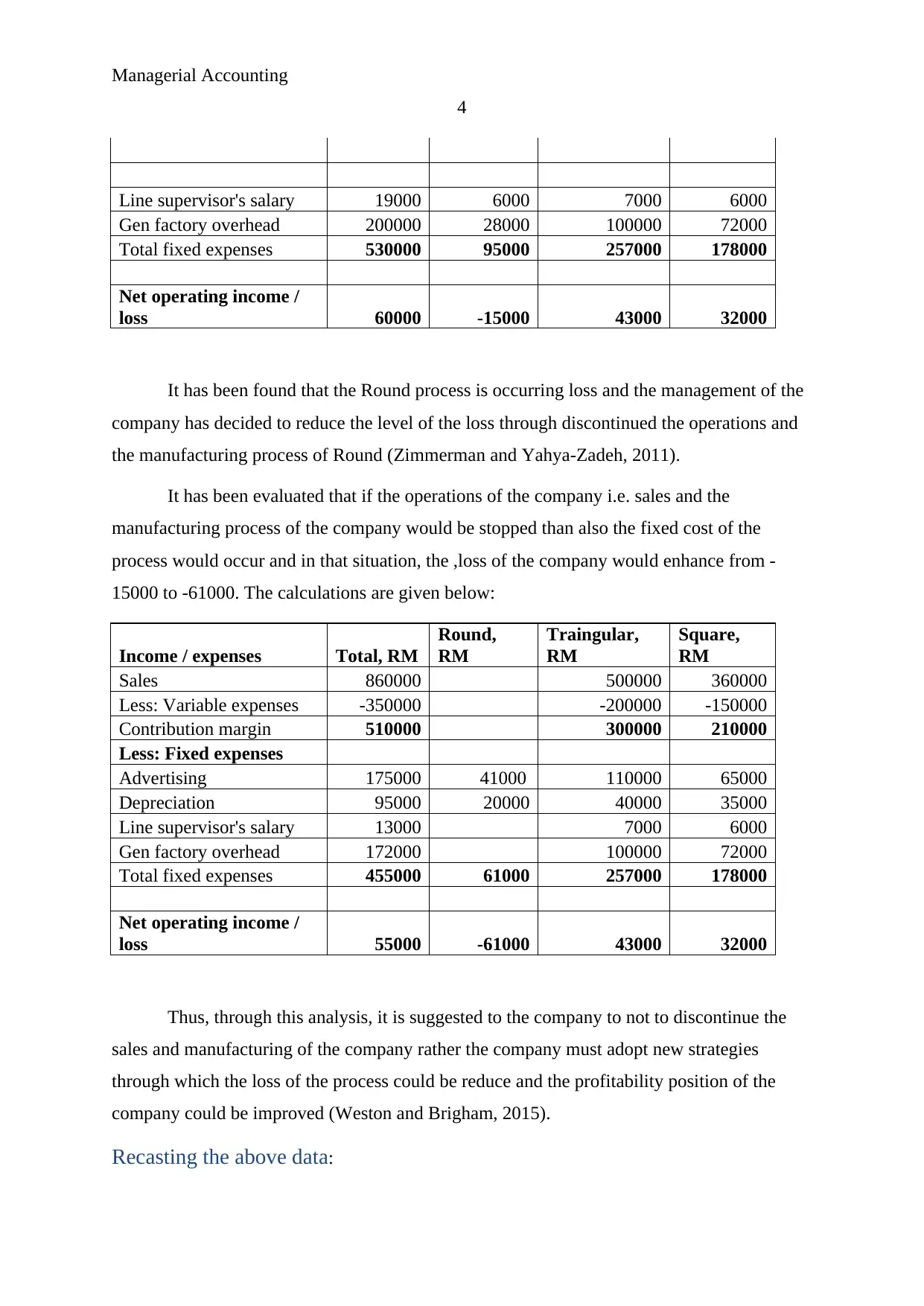

Line supervisor's salary 19000 6000 7000 6000

Gen factory overhead 200000 28000 100000 72000

Total fixed expenses 530000 95000 257000 178000

Net operating income /

loss 60000 -15000 43000 32000

It has been found that the Round process is occurring loss and the management of the

company has decided to reduce the level of the loss through discontinued the operations and

the manufacturing process of Round (Zimmerman and Yahya-Zadeh, 2011).

It has been evaluated that if the operations of the company i.e. sales and the

manufacturing process of the company would be stopped than also the fixed cost of the

process would occur and in that situation, the ,loss of the company would enhance from -

15000 to -61000. The calculations are given below:

Income / expenses Total, RM

Round,

RM

Traingular,

RM

Square,

RM

Sales 860000 500000 360000

Less: Variable expenses -350000 -200000 -150000

Contribution margin 510000 300000 210000

Less: Fixed expenses

Advertising 175000 41000 110000 65000

Depreciation 95000 20000 40000 35000

Line supervisor's salary 13000 7000 6000

Gen factory overhead 172000 100000 72000

Total fixed expenses 455000 61000 257000 178000

Net operating income /

loss 55000 -61000 43000 32000

Thus, through this analysis, it is suggested to the company to not to discontinue the

sales and manufacturing of the company rather the company must adopt new strategies

through which the loss of the process could be reduce and the profitability position of the

company could be improved (Weston and Brigham, 2015).

Recasting the above data:

4

Line supervisor's salary 19000 6000 7000 6000

Gen factory overhead 200000 28000 100000 72000

Total fixed expenses 530000 95000 257000 178000

Net operating income /

loss 60000 -15000 43000 32000

It has been found that the Round process is occurring loss and the management of the

company has decided to reduce the level of the loss through discontinued the operations and

the manufacturing process of Round (Zimmerman and Yahya-Zadeh, 2011).

It has been evaluated that if the operations of the company i.e. sales and the

manufacturing process of the company would be stopped than also the fixed cost of the

process would occur and in that situation, the ,loss of the company would enhance from -

15000 to -61000. The calculations are given below:

Income / expenses Total, RM

Round,

RM

Traingular,

RM

Square,

RM

Sales 860000 500000 360000

Less: Variable expenses -350000 -200000 -150000

Contribution margin 510000 300000 210000

Less: Fixed expenses

Advertising 175000 41000 110000 65000

Depreciation 95000 20000 40000 35000

Line supervisor's salary 13000 7000 6000

Gen factory overhead 172000 100000 72000

Total fixed expenses 455000 61000 257000 178000

Net operating income /

loss 55000 -61000 43000 32000

Thus, through this analysis, it is suggested to the company to not to discontinue the

sales and manufacturing of the company rather the company must adopt new strategies

through which the loss of the process could be reduce and the profitability position of the

company could be improved (Weston and Brigham, 2015).

Recasting the above data:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting

5

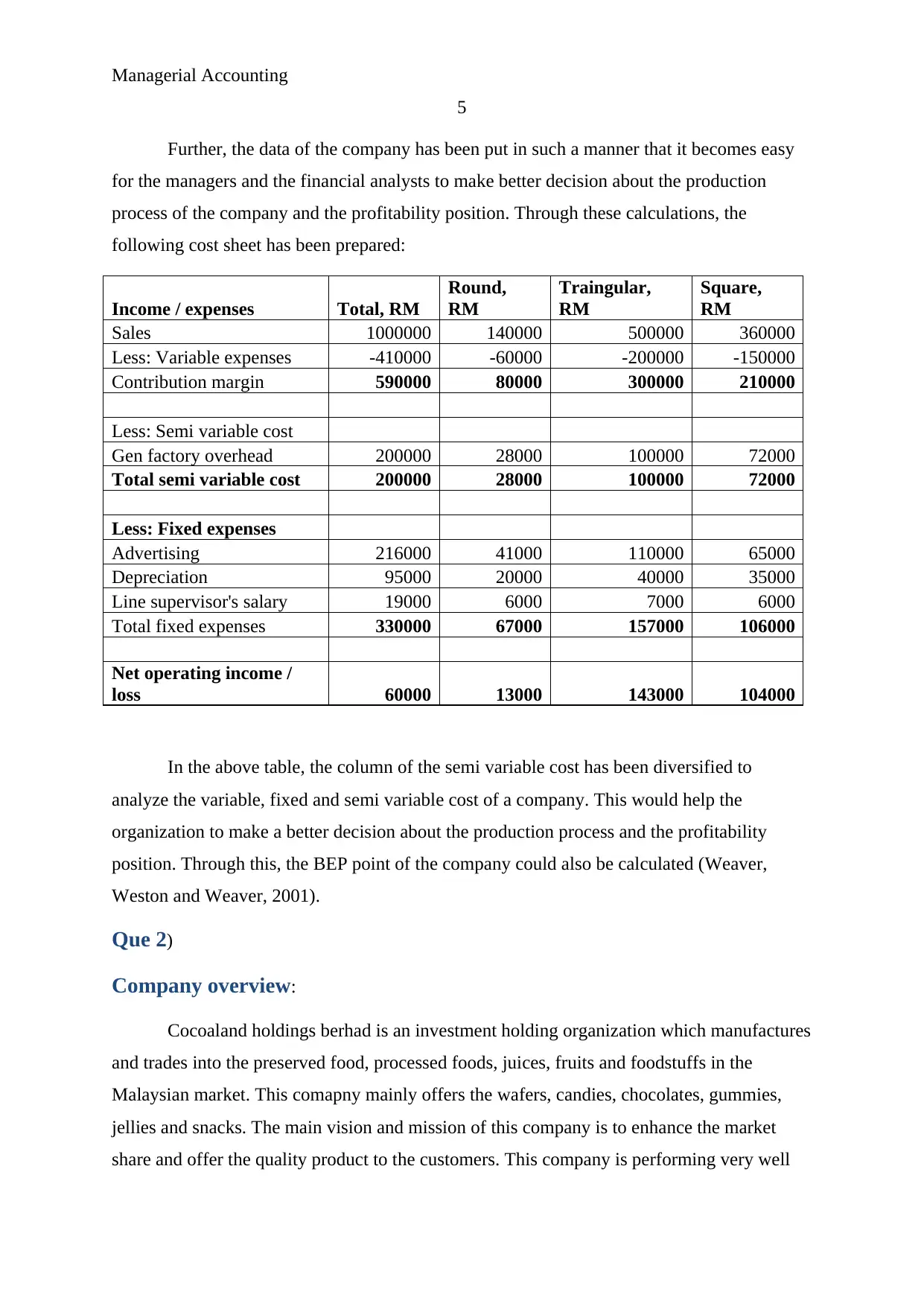

Further, the data of the company has been put in such a manner that it becomes easy

for the managers and the financial analysts to make better decision about the production

process of the company and the profitability position. Through these calculations, the

following cost sheet has been prepared:

Income / expenses Total, RM

Round,

RM

Traingular,

RM

Square,

RM

Sales 1000000 140000 500000 360000

Less: Variable expenses -410000 -60000 -200000 -150000

Contribution margin 590000 80000 300000 210000

Less: Semi variable cost

Gen factory overhead 200000 28000 100000 72000

Total semi variable cost 200000 28000 100000 72000

Less: Fixed expenses

Advertising 216000 41000 110000 65000

Depreciation 95000 20000 40000 35000

Line supervisor's salary 19000 6000 7000 6000

Total fixed expenses 330000 67000 157000 106000

Net operating income /

loss 60000 13000 143000 104000

In the above table, the column of the semi variable cost has been diversified to

analyze the variable, fixed and semi variable cost of a company. This would help the

organization to make a better decision about the production process and the profitability

position. Through this, the BEP point of the company could also be calculated (Weaver,

Weston and Weaver, 2001).

Que 2)

Company overview:

Cocoaland holdings berhad is an investment holding organization which manufactures

and trades into the preserved food, processed foods, juices, fruits and foodstuffs in the

Malaysian market. This comapny mainly offers the wafers, candies, chocolates, gummies,

jellies and snacks. The main vision and mission of this company is to enhance the market

share and offer the quality product to the customers. This company is performing very well

5

Further, the data of the company has been put in such a manner that it becomes easy

for the managers and the financial analysts to make better decision about the production

process of the company and the profitability position. Through these calculations, the

following cost sheet has been prepared:

Income / expenses Total, RM

Round,

RM

Traingular,

RM

Square,

RM

Sales 1000000 140000 500000 360000

Less: Variable expenses -410000 -60000 -200000 -150000

Contribution margin 590000 80000 300000 210000

Less: Semi variable cost

Gen factory overhead 200000 28000 100000 72000

Total semi variable cost 200000 28000 100000 72000

Less: Fixed expenses

Advertising 216000 41000 110000 65000

Depreciation 95000 20000 40000 35000

Line supervisor's salary 19000 6000 7000 6000

Total fixed expenses 330000 67000 157000 106000

Net operating income /

loss 60000 13000 143000 104000

In the above table, the column of the semi variable cost has been diversified to

analyze the variable, fixed and semi variable cost of a company. This would help the

organization to make a better decision about the production process and the profitability

position. Through this, the BEP point of the company could also be calculated (Weaver,

Weston and Weaver, 2001).

Que 2)

Company overview:

Cocoaland holdings berhad is an investment holding organization which manufactures

and trades into the preserved food, processed foods, juices, fruits and foodstuffs in the

Malaysian market. This comapny mainly offers the wafers, candies, chocolates, gummies,

jellies and snacks. The main vision and mission of this company is to enhance the market

share and offer the quality product to the customers. This company is performing very well

Managerial Accounting

6

into Malaysian market and also trying to diversify its market into various new markets

(Home, 2017).

Through the mission statement of the company, it has been found that the main

mission of the company is to grab the international market as well and offer the food to the

international client. The vision of the company is to offer the best of the CSR policies to

manage and maintain the performance and the position of the company (Morningstar, 2017).

The main vision and mission of this company is to offer the quality product to the customers

and enhance the market share. This company is performing very well into Malaysian market

and trying to diversify its market into various new markets.

Objective of the report:

The main objective behind this report is to manage and maintain the performance and

the better position of a company in terms of the finance. Mainly this report has been prepared

to analyze the position of the company so that a better decision could be prepared for the

investors of the company to invest more into the company or not. The main objective of this

report is to analyze the position of the company in terms of the liquid position, solvency

position, profitability position and capital structure of the company.

Financial statement analysis:

Financial statement analysis is a process in which the financial statement of a

company i.e. profit and loss account, balance sheet and the cash flow statement of a company

is analyzed and the performance of a company is analyzed. Financial statement analysis is a

study which is done over a company by its financial manager, financial analyst and the

investors of the company to make decisions about the company (Hillier, Grinblatt and

Titman, 2011).

Financial manager uses this technique to identify the position and the performance of

the company so that the changes could be done into the company to make the financial

position of the company strong whereas Financial analyst and the investors use this technique

to identify the profitability and the performance of the company so that the investment and

divestment decision could be made to enhance the worth of the amount (Higgins, 2012).

In this report, financial statement analysis has been done over COCOALAND

HOLDINGS BERHAD to identify the performance, profitability and the position of the

6

into Malaysian market and also trying to diversify its market into various new markets

(Home, 2017).

Through the mission statement of the company, it has been found that the main

mission of the company is to grab the international market as well and offer the food to the

international client. The vision of the company is to offer the best of the CSR policies to

manage and maintain the performance and the position of the company (Morningstar, 2017).

The main vision and mission of this company is to offer the quality product to the customers

and enhance the market share. This company is performing very well into Malaysian market

and trying to diversify its market into various new markets.

Objective of the report:

The main objective behind this report is to manage and maintain the performance and

the better position of a company in terms of the finance. Mainly this report has been prepared

to analyze the position of the company so that a better decision could be prepared for the

investors of the company to invest more into the company or not. The main objective of this

report is to analyze the position of the company in terms of the liquid position, solvency

position, profitability position and capital structure of the company.

Financial statement analysis:

Financial statement analysis is a process in which the financial statement of a

company i.e. profit and loss account, balance sheet and the cash flow statement of a company

is analyzed and the performance of a company is analyzed. Financial statement analysis is a

study which is done over a company by its financial manager, financial analyst and the

investors of the company to make decisions about the company (Hillier, Grinblatt and

Titman, 2011).

Financial manager uses this technique to identify the position and the performance of

the company so that the changes could be done into the company to make the financial

position of the company strong whereas Financial analyst and the investors use this technique

to identify the profitability and the performance of the company so that the investment and

divestment decision could be made to enhance the worth of the amount (Higgins, 2012).

In this report, financial statement analysis has been done over COCOALAND

HOLDINGS BERHAD to identify the performance, profitability and the position of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting

7

company. In this report, the ratio analysis study has been performed over the financial data of

the company of last 2 years to analyze and identify the changes into the company and also for

identifying the current profitability, liquidity, solvency and the capital structure position. The

study of ratio analysis of the COCOALAND HOLDINGS BERHAD is as follows:

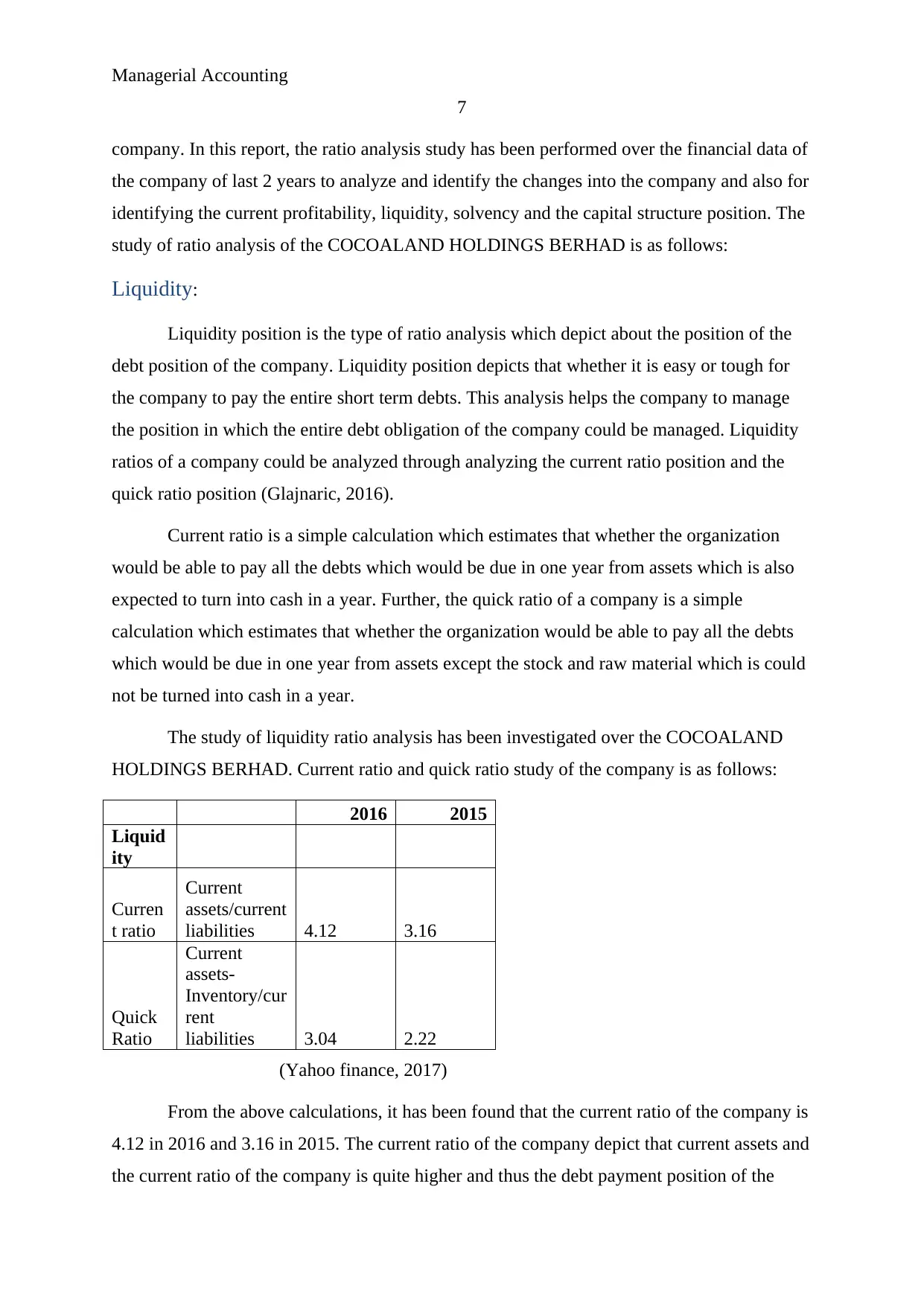

Liquidity:

Liquidity position is the type of ratio analysis which depict about the position of the

debt position of the company. Liquidity position depicts that whether it is easy or tough for

the company to pay the entire short term debts. This analysis helps the company to manage

the position in which the entire debt obligation of the company could be managed. Liquidity

ratios of a company could be analyzed through analyzing the current ratio position and the

quick ratio position (Glajnaric, 2016).

Current ratio is a simple calculation which estimates that whether the organization

would be able to pay all the debts which would be due in one year from assets which is also

expected to turn into cash in a year. Further, the quick ratio of a company is a simple

calculation which estimates that whether the organization would be able to pay all the debts

which would be due in one year from assets except the stock and raw material which is could

not be turned into cash in a year.

The study of liquidity ratio analysis has been investigated over the COCOALAND

HOLDINGS BERHAD. Current ratio and quick ratio study of the company is as follows:

2016 2015

Liquid

ity

Curren

t ratio

Current

assets/current

liabilities 4.12 3.16

Quick

Ratio

Current

assets-

Inventory/cur

rent

liabilities 3.04 2.22

(Yahoo finance, 2017)

From the above calculations, it has been found that the current ratio of the company is

4.12 in 2016 and 3.16 in 2015. The current ratio of the company depict that current assets and

the current ratio of the company is quite higher and thus the debt payment position of the

7

company. In this report, the ratio analysis study has been performed over the financial data of

the company of last 2 years to analyze and identify the changes into the company and also for

identifying the current profitability, liquidity, solvency and the capital structure position. The

study of ratio analysis of the COCOALAND HOLDINGS BERHAD is as follows:

Liquidity:

Liquidity position is the type of ratio analysis which depict about the position of the

debt position of the company. Liquidity position depicts that whether it is easy or tough for

the company to pay the entire short term debts. This analysis helps the company to manage

the position in which the entire debt obligation of the company could be managed. Liquidity

ratios of a company could be analyzed through analyzing the current ratio position and the

quick ratio position (Glajnaric, 2016).

Current ratio is a simple calculation which estimates that whether the organization

would be able to pay all the debts which would be due in one year from assets which is also

expected to turn into cash in a year. Further, the quick ratio of a company is a simple

calculation which estimates that whether the organization would be able to pay all the debts

which would be due in one year from assets except the stock and raw material which is could

not be turned into cash in a year.

The study of liquidity ratio analysis has been investigated over the COCOALAND

HOLDINGS BERHAD. Current ratio and quick ratio study of the company is as follows:

2016 2015

Liquid

ity

Curren

t ratio

Current

assets/current

liabilities 4.12 3.16

Quick

Ratio

Current

assets-

Inventory/cur

rent

liabilities 3.04 2.22

(Yahoo finance, 2017)

From the above calculations, it has been found that the current ratio of the company is

4.12 in 2016 and 3.16 in 2015. The current ratio of the company depict that current assets and

the current ratio of the company is quite higher and thus the debt payment position of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting

8

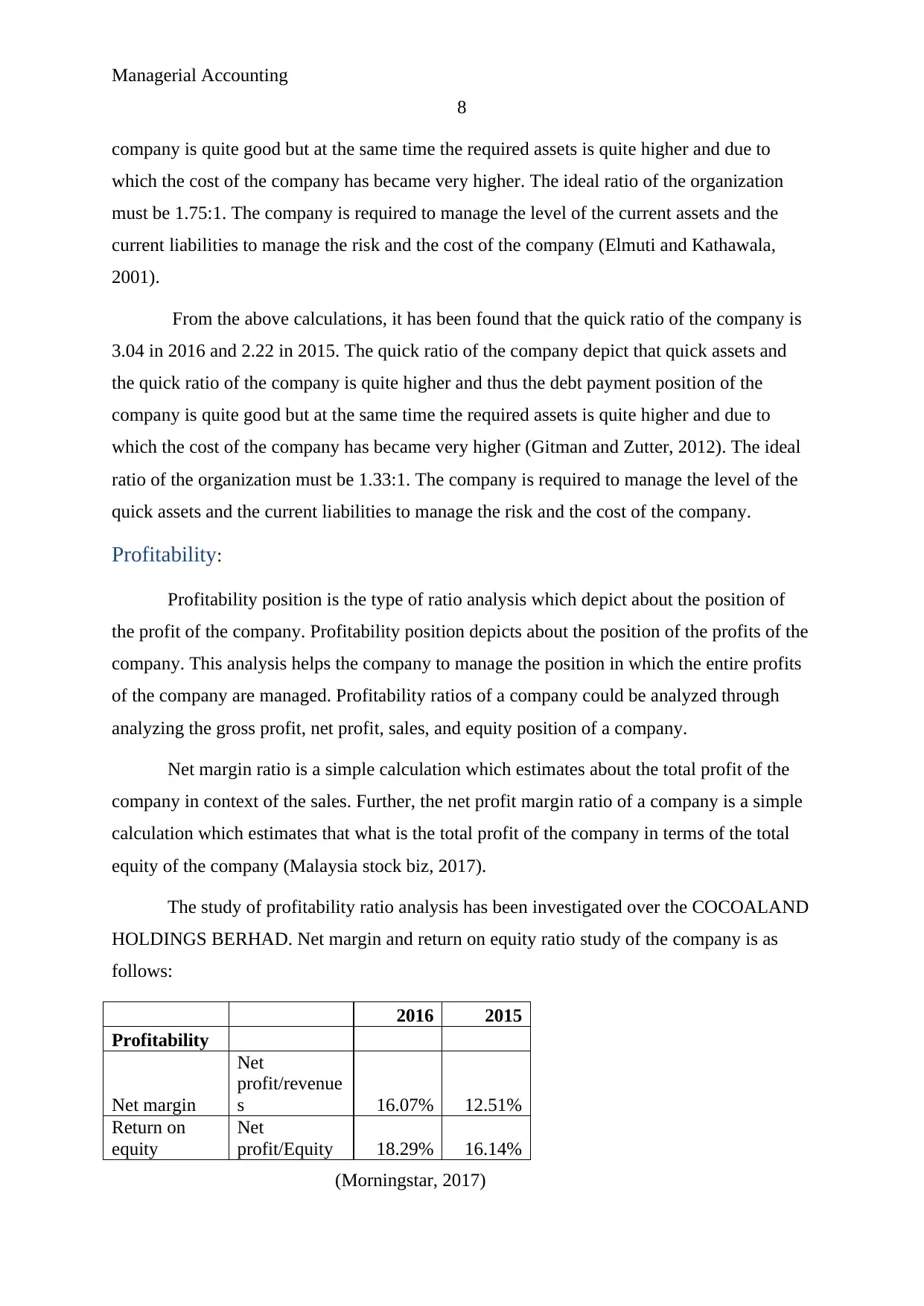

company is quite good but at the same time the required assets is quite higher and due to

which the cost of the company has became very higher. The ideal ratio of the organization

must be 1.75:1. The company is required to manage the level of the current assets and the

current liabilities to manage the risk and the cost of the company (Elmuti and Kathawala,

2001).

From the above calculations, it has been found that the quick ratio of the company is

3.04 in 2016 and 2.22 in 2015. The quick ratio of the company depict that quick assets and

the quick ratio of the company is quite higher and thus the debt payment position of the

company is quite good but at the same time the required assets is quite higher and due to

which the cost of the company has became very higher (Gitman and Zutter, 2012). The ideal

ratio of the organization must be 1.33:1. The company is required to manage the level of the

quick assets and the current liabilities to manage the risk and the cost of the company.

Profitability:

Profitability position is the type of ratio analysis which depict about the position of

the profit of the company. Profitability position depicts about the position of the profits of the

company. This analysis helps the company to manage the position in which the entire profits

of the company are managed. Profitability ratios of a company could be analyzed through

analyzing the gross profit, net profit, sales, and equity position of a company.

Net margin ratio is a simple calculation which estimates about the total profit of the

company in context of the sales. Further, the net profit margin ratio of a company is a simple

calculation which estimates that what is the total profit of the company in terms of the total

equity of the company (Malaysia stock biz, 2017).

The study of profitability ratio analysis has been investigated over the COCOALAND

HOLDINGS BERHAD. Net margin and return on equity ratio study of the company is as

follows:

2016 2015

Profitability

Net margin

Net

profit/revenue

s 16.07% 12.51%

Return on

equity

Net

profit/Equity 18.29% 16.14%

(Morningstar, 2017)

8

company is quite good but at the same time the required assets is quite higher and due to

which the cost of the company has became very higher. The ideal ratio of the organization

must be 1.75:1. The company is required to manage the level of the current assets and the

current liabilities to manage the risk and the cost of the company (Elmuti and Kathawala,

2001).

From the above calculations, it has been found that the quick ratio of the company is

3.04 in 2016 and 2.22 in 2015. The quick ratio of the company depict that quick assets and

the quick ratio of the company is quite higher and thus the debt payment position of the

company is quite good but at the same time the required assets is quite higher and due to

which the cost of the company has became very higher (Gitman and Zutter, 2012). The ideal

ratio of the organization must be 1.33:1. The company is required to manage the level of the

quick assets and the current liabilities to manage the risk and the cost of the company.

Profitability:

Profitability position is the type of ratio analysis which depict about the position of

the profit of the company. Profitability position depicts about the position of the profits of the

company. This analysis helps the company to manage the position in which the entire profits

of the company are managed. Profitability ratios of a company could be analyzed through

analyzing the gross profit, net profit, sales, and equity position of a company.

Net margin ratio is a simple calculation which estimates about the total profit of the

company in context of the sales. Further, the net profit margin ratio of a company is a simple

calculation which estimates that what is the total profit of the company in terms of the total

equity of the company (Malaysia stock biz, 2017).

The study of profitability ratio analysis has been investigated over the COCOALAND

HOLDINGS BERHAD. Net margin and return on equity ratio study of the company is as

follows:

2016 2015

Profitability

Net margin

Net

profit/revenue

s 16.07% 12.51%

Return on

equity

Net

profit/Equity 18.29% 16.14%

(Morningstar, 2017)

Managerial Accounting

9

From the above calculations, it has been found that the net margin ratio of the

company is 16.07% in 2016 and 12.15% in 2015. The net profit margin ratio of the company

depict that net profit and the sales of the company has became higher from last year and thus

the net profit position of the company has became better. This depict that the company is

performing very well in the market.

From the above calculations, it has been found that the return on equity ratio of the

company is 18.29% in 2016 and 16.14% in 2015 (Fulin, 2011). The return on equity ratio of

the company depicts that net profit and the equity of the company has become higher from

last year and thus the return on equity of the company has become better. This depict that the

company is performing very well in the market. And thus the return offered to the investors

of the company would also be higher.

Efficiency:

Efficiency position is the type of ratio analysis which depict about the position of the

cash collection of the company. Efficiency position depicts about the position of the turnover

of the inventory, debtors, creditors and the assets of the company. This analysis helps the

company to manage the position in which the entire turnover cost of the company is

managed. Efficiency ratios of a company could be analyzed through analyzing the receivable,

payable and the asset turnover position of a company (Gurufocus, 2017).

Receivable collection period ratio is a simple calculation which estimates about the

debtors’ collection time. Further, the payable collection period ratio is a simple calculation

which estimates about the creditor’s payment time and lastly, asset turnover ratio is a simple

calculation which estimates about the turnover in the assets of the company.

The study of efficiency ratio analysis has been investigated over the COCOALAND

HOLDINGS BERHAD. Receivable collection period, payable collection period and asset

turnover ratio study of the company is as follows:

2016 2015

Efficienc

y

Receivab

les

collectio

n period

Receivabl

es/ Total

sales*365 74.41 58.84

Payables Payables/

9

From the above calculations, it has been found that the net margin ratio of the

company is 16.07% in 2016 and 12.15% in 2015. The net profit margin ratio of the company

depict that net profit and the sales of the company has became higher from last year and thus

the net profit position of the company has became better. This depict that the company is

performing very well in the market.

From the above calculations, it has been found that the return on equity ratio of the

company is 18.29% in 2016 and 16.14% in 2015 (Fulin, 2011). The return on equity ratio of

the company depicts that net profit and the equity of the company has become higher from

last year and thus the return on equity of the company has become better. This depict that the

company is performing very well in the market. And thus the return offered to the investors

of the company would also be higher.

Efficiency:

Efficiency position is the type of ratio analysis which depict about the position of the

cash collection of the company. Efficiency position depicts about the position of the turnover

of the inventory, debtors, creditors and the assets of the company. This analysis helps the

company to manage the position in which the entire turnover cost of the company is

managed. Efficiency ratios of a company could be analyzed through analyzing the receivable,

payable and the asset turnover position of a company (Gurufocus, 2017).

Receivable collection period ratio is a simple calculation which estimates about the

debtors’ collection time. Further, the payable collection period ratio is a simple calculation

which estimates about the creditor’s payment time and lastly, asset turnover ratio is a simple

calculation which estimates about the turnover in the assets of the company.

The study of efficiency ratio analysis has been investigated over the COCOALAND

HOLDINGS BERHAD. Receivable collection period, payable collection period and asset

turnover ratio study of the company is as follows:

2016 2015

Efficienc

y

Receivab

les

collectio

n period

Receivabl

es/ Total

sales*365 74.41 58.84

Payables Payables/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting

10

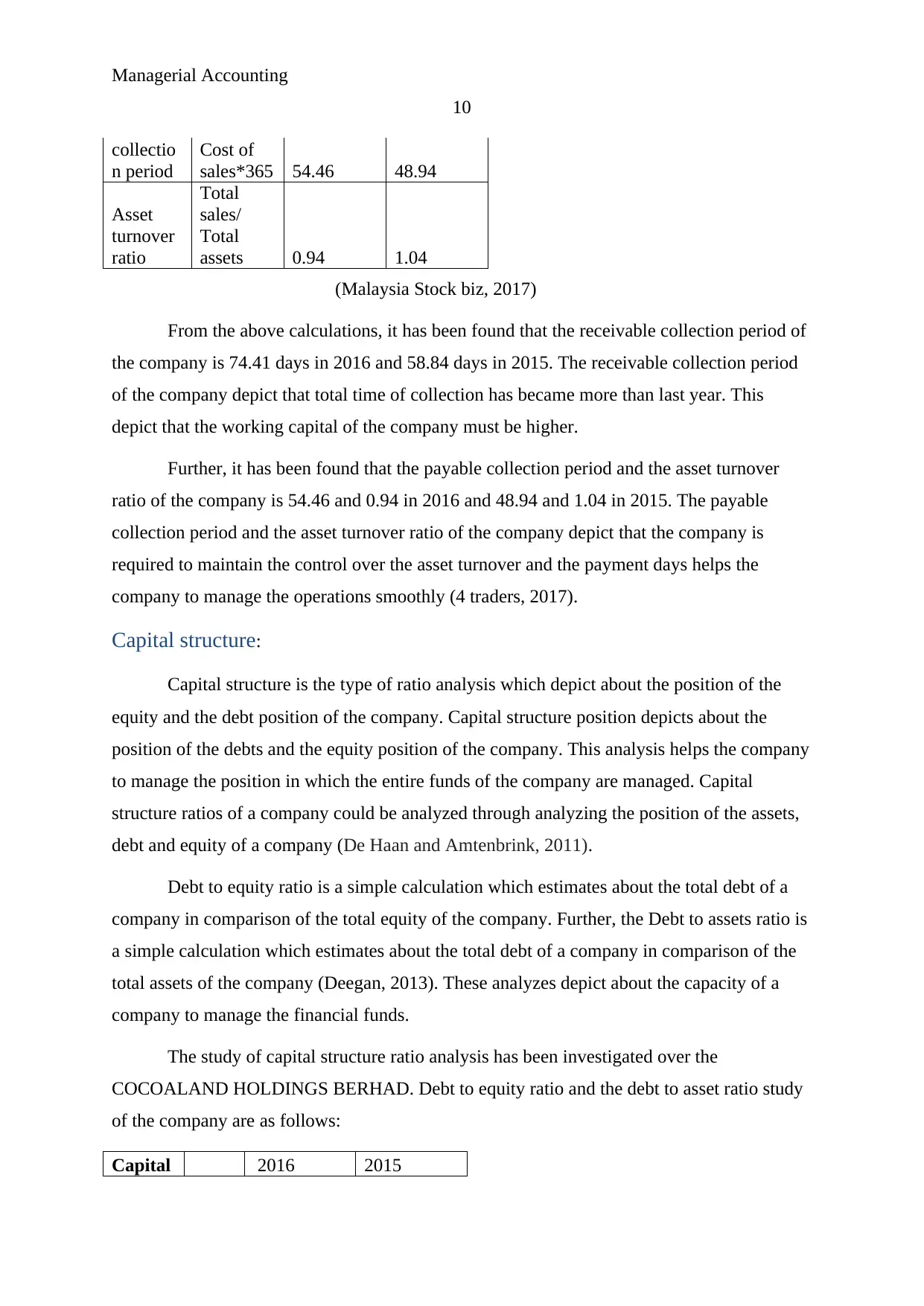

collectio

n period

Cost of

sales*365 54.46 48.94

Asset

turnover

ratio

Total

sales/

Total

assets 0.94 1.04

(Malaysia Stock biz, 2017)

From the above calculations, it has been found that the receivable collection period of

the company is 74.41 days in 2016 and 58.84 days in 2015. The receivable collection period

of the company depict that total time of collection has became more than last year. This

depict that the working capital of the company must be higher.

Further, it has been found that the payable collection period and the asset turnover

ratio of the company is 54.46 and 0.94 in 2016 and 48.94 and 1.04 in 2015. The payable

collection period and the asset turnover ratio of the company depict that the company is

required to maintain the control over the asset turnover and the payment days helps the

company to manage the operations smoothly (4 traders, 2017).

Capital structure:

Capital structure is the type of ratio analysis which depict about the position of the

equity and the debt position of the company. Capital structure position depicts about the

position of the debts and the equity position of the company. This analysis helps the company

to manage the position in which the entire funds of the company are managed. Capital

structure ratios of a company could be analyzed through analyzing the position of the assets,

debt and equity of a company (De Haan and Amtenbrink, 2011).

Debt to equity ratio is a simple calculation which estimates about the total debt of a

company in comparison of the total equity of the company. Further, the Debt to assets ratio is

a simple calculation which estimates about the total debt of a company in comparison of the

total assets of the company (Deegan, 2013). These analyzes depict about the capacity of a

company to manage the financial funds.

The study of capital structure ratio analysis has been investigated over the

COCOALAND HOLDINGS BERHAD. Debt to equity ratio and the debt to asset ratio study

of the company are as follows:

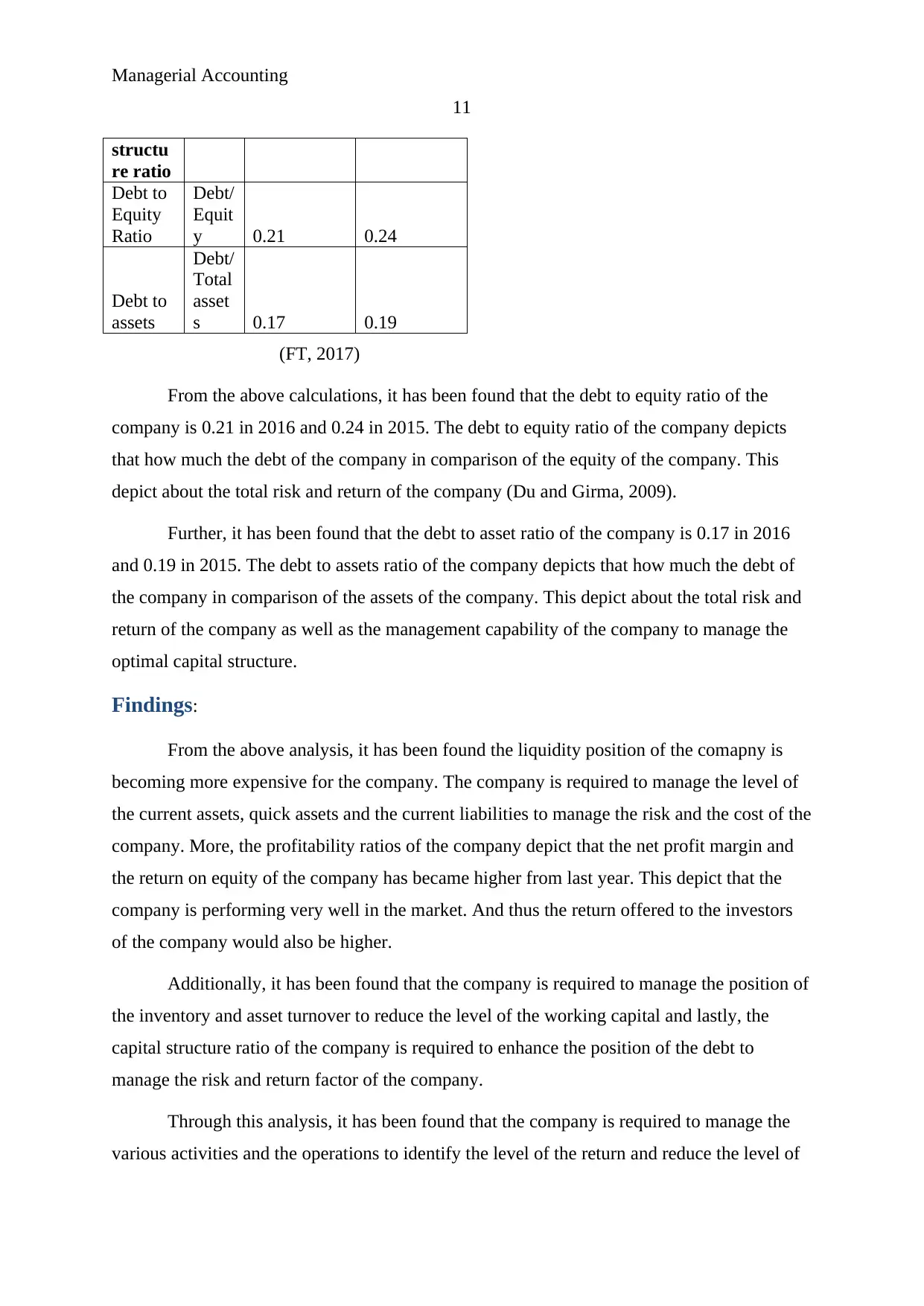

Capital 2016 2015

10

collectio

n period

Cost of

sales*365 54.46 48.94

Asset

turnover

ratio

Total

sales/

Total

assets 0.94 1.04

(Malaysia Stock biz, 2017)

From the above calculations, it has been found that the receivable collection period of

the company is 74.41 days in 2016 and 58.84 days in 2015. The receivable collection period

of the company depict that total time of collection has became more than last year. This

depict that the working capital of the company must be higher.

Further, it has been found that the payable collection period and the asset turnover

ratio of the company is 54.46 and 0.94 in 2016 and 48.94 and 1.04 in 2015. The payable

collection period and the asset turnover ratio of the company depict that the company is

required to maintain the control over the asset turnover and the payment days helps the

company to manage the operations smoothly (4 traders, 2017).

Capital structure:

Capital structure is the type of ratio analysis which depict about the position of the

equity and the debt position of the company. Capital structure position depicts about the

position of the debts and the equity position of the company. This analysis helps the company

to manage the position in which the entire funds of the company are managed. Capital

structure ratios of a company could be analyzed through analyzing the position of the assets,

debt and equity of a company (De Haan and Amtenbrink, 2011).

Debt to equity ratio is a simple calculation which estimates about the total debt of a

company in comparison of the total equity of the company. Further, the Debt to assets ratio is

a simple calculation which estimates about the total debt of a company in comparison of the

total assets of the company (Deegan, 2013). These analyzes depict about the capacity of a

company to manage the financial funds.

The study of capital structure ratio analysis has been investigated over the

COCOALAND HOLDINGS BERHAD. Debt to equity ratio and the debt to asset ratio study

of the company are as follows:

Capital 2016 2015

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting

11

structu

re ratio

Debt to

Equity

Ratio

Debt/

Equit

y 0.21 0.24

Debt to

assets

Debt/

Total

asset

s 0.17 0.19

(FT, 2017)

From the above calculations, it has been found that the debt to equity ratio of the

company is 0.21 in 2016 and 0.24 in 2015. The debt to equity ratio of the company depicts

that how much the debt of the company in comparison of the equity of the company. This

depict about the total risk and return of the company (Du and Girma, 2009).

Further, it has been found that the debt to asset ratio of the company is 0.17 in 2016

and 0.19 in 2015. The debt to assets ratio of the company depicts that how much the debt of

the company in comparison of the assets of the company. This depict about the total risk and

return of the company as well as the management capability of the company to manage the

optimal capital structure.

Findings:

From the above analysis, it has been found the liquidity position of the comapny is

becoming more expensive for the company. The company is required to manage the level of

the current assets, quick assets and the current liabilities to manage the risk and the cost of the

company. More, the profitability ratios of the company depict that the net profit margin and

the return on equity of the company has became higher from last year. This depict that the

company is performing very well in the market. And thus the return offered to the investors

of the company would also be higher.

Additionally, it has been found that the company is required to manage the position of

the inventory and asset turnover to reduce the level of the working capital and lastly, the

capital structure ratio of the company is required to enhance the position of the debt to

manage the risk and return factor of the company.

Through this analysis, it has been found that the company is required to manage the

various activities and the operations to identify the level of the return and reduce the level of

11

structu

re ratio

Debt to

Equity

Ratio

Debt/

Equit

y 0.21 0.24

Debt to

assets

Debt/

Total

asset

s 0.17 0.19

(FT, 2017)

From the above calculations, it has been found that the debt to equity ratio of the

company is 0.21 in 2016 and 0.24 in 2015. The debt to equity ratio of the company depicts

that how much the debt of the company in comparison of the equity of the company. This

depict about the total risk and return of the company (Du and Girma, 2009).

Further, it has been found that the debt to asset ratio of the company is 0.17 in 2016

and 0.19 in 2015. The debt to assets ratio of the company depicts that how much the debt of

the company in comparison of the assets of the company. This depict about the total risk and

return of the company as well as the management capability of the company to manage the

optimal capital structure.

Findings:

From the above analysis, it has been found the liquidity position of the comapny is

becoming more expensive for the company. The company is required to manage the level of

the current assets, quick assets and the current liabilities to manage the risk and the cost of the

company. More, the profitability ratios of the company depict that the net profit margin and

the return on equity of the company has became higher from last year. This depict that the

company is performing very well in the market. And thus the return offered to the investors

of the company would also be higher.

Additionally, it has been found that the company is required to manage the position of

the inventory and asset turnover to reduce the level of the working capital and lastly, the

capital structure ratio of the company is required to enhance the position of the debt to

manage the risk and return factor of the company.

Through this analysis, it has been found that the company is required to manage the

various activities and the operations to identify the level of the return and reduce the level of

Managerial Accounting

12

the risk. The current position of the company depict that the investors would get higher return

from the company and thus it is a good option for the investors to invest the amount in the

COCOALAND HOLDINGS BERHAD for long term as well as short term.

Conclusion:

To conclude, the liquidity position of the comapny is becoming worst day by day for

the company as well as the investors of the company. The company is required to manage the

level of the current assets, quick assets and the current liabilities to manage the risk and the

cost of the company. The profitability ratios, liquidity ratios, solvent ratios, efficiency ratios

and the capital structure ratios of the company are depicting about the different position of

the company.

Profitability ratios are depicting about the good performance of the company and

depicting that the performance and position of the company are in the favour the investors

and would offer high return to the company. Further, the efficiency ratios are depicting about

the good performance of the working capital management and depicting that the performance

and position of the company are in the favour the investors and would offer high return to the

company. Lastly, the capital structure ratios are depicting about the debt and equity position

of the company and also depict that the comapny must make a control over the performance

and the position of the company.

Through this analysis, it has been found that the company is required to manage the

various activities and the operations to identify the level of the return and reduce the level of

the risk. The current position of the company depict that the investors would get higher return

from the company and thus it is a good option for the investors to invest the amount in the

COCOALAND HOLDINGS BERHAD for long term as well as short term.

12

the risk. The current position of the company depict that the investors would get higher return

from the company and thus it is a good option for the investors to invest the amount in the

COCOALAND HOLDINGS BERHAD for long term as well as short term.

Conclusion:

To conclude, the liquidity position of the comapny is becoming worst day by day for

the company as well as the investors of the company. The company is required to manage the

level of the current assets, quick assets and the current liabilities to manage the risk and the

cost of the company. The profitability ratios, liquidity ratios, solvent ratios, efficiency ratios

and the capital structure ratios of the company are depicting about the different position of

the company.

Profitability ratios are depicting about the good performance of the company and

depicting that the performance and position of the company are in the favour the investors

and would offer high return to the company. Further, the efficiency ratios are depicting about

the good performance of the working capital management and depicting that the performance

and position of the company are in the favour the investors and would offer high return to the

company. Lastly, the capital structure ratios are depicting about the debt and equity position

of the company and also depict that the comapny must make a control over the performance

and the position of the company.

Through this analysis, it has been found that the company is required to manage the

various activities and the operations to identify the level of the return and reduce the level of

the risk. The current position of the company depict that the investors would get higher return

from the company and thus it is a good option for the investors to invest the amount in the

COCOALAND HOLDINGS BERHAD for long term as well as short term.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.