Accounting Principles Report: A2 Milk and Bellamy's Financial Analysis

VerifiedAdded on 2022/11/19

|14

|3566

|127

Report

AI Summary

This report provides a comprehensive financial analysis of A2 Milk Company Pty Ltd and Bellamy’s Australia Ltd, both operating in the Australian dairy and food and beverage industries, respectively. The analysis includes an overview of the industry and the companies, examining their strategies, market positions, and financial performance. The report delves into key financial aspects such as cash, receivables, inventory, property, plant, and equipment (PPE), current and non-current liabilities, and shareholder's equity. It incorporates ratio analysis, including current ratio, quick ratio, average daily sales, inventory turnover, debt ratio, times interest earned ratio, and return on equity, to assess the companies' liquidity, efficiency, solvency, and profitability. The report also highlights the auditor's letters and statements of cash flows, culminating in an overall analysis of the financial health of both companies, drawing conclusions about their strengths, weaknesses, and potential for future growth. The study is based on the financial reports for the years 2017 and 2018, offering a comparative perspective on their financial standing and operational performance.

Running head: ACCOUNTING PRINCIPLES

Accounting Principles

Name of the Student

Name of the University

Author’s Note

Accounting Principles

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING PRINCIPLES

Table of Contents

Industry and Company Overview..............................................................................................2

Industry..................................................................................................................................2

Company................................................................................................................................2

Cash............................................................................................................................................3

Receivable..................................................................................................................................3

Inventory....................................................................................................................................4

Property, Plant and Equipment (PPE)........................................................................................5

Current Liabilities......................................................................................................................6

Non-Current Liabilities..............................................................................................................6

Shareholder’s Equity..................................................................................................................7

Auditor’s Letter..........................................................................................................................7

Statement of Cash Flows............................................................................................................8

Ratio Analysis............................................................................................................................8

Overall Analysis.......................................................................................................................11

References................................................................................................................................12

Table of Contents

Industry and Company Overview..............................................................................................2

Industry..................................................................................................................................2

Company................................................................................................................................2

Cash............................................................................................................................................3

Receivable..................................................................................................................................3

Inventory....................................................................................................................................4

Property, Plant and Equipment (PPE)........................................................................................5

Current Liabilities......................................................................................................................6

Non-Current Liabilities..............................................................................................................6

Shareholder’s Equity..................................................................................................................7

Auditor’s Letter..........................................................................................................................7

Statement of Cash Flows............................................................................................................8

Ratio Analysis............................................................................................................................8

Overall Analysis.......................................................................................................................11

References................................................................................................................................12

2ACCOUNTING PRINCIPLES

Industry and Company Overview

Industry

A2 Milk Company Pty Ltd – A2 Milk Company Pvt Ltd (A2 Milk) operates in the

Australian dairy industry. Australia is considered as a small producer of milk, but the

Australian dairy industry is responsible for being the third largest dairy exporter since the

country exports 50% of their production. Australian dairy industry has a gross value of $4

billion and it is Australia’s third largest rural industry. The main produced dairy product in

this industry are milk, milk powder, butter, yogurt and cheese (pwc.com.au 2019).

Bellamy’s Australia Ltd – Bellamy’s Australia Ltd operates in the food and beverage

industry of Australia which is considered as the largest manufacturing sector of Australia.

This industry is a key employer and is the fastest growing manufacturing employer of

regional Australia. In the current years, total amount of revenue from this industry is

US$1,443 million. The Australian food and beverage industry is the major user of the

country’s agricultural products. The main manufacturing products of this industry are meats,

beverages, dairy products, fruits and vegetables, sugar, bakery products, seafood, pet food,

confectionary, flour and cereal products and others (statista.com 2019).

Company

A2 Milk Company Pty Ltd – The main aim of A2 Milk is in producing their customers with

high quality as well as superior brand of dairy products that will contain the A2 protein.

There are two types of protein in the conventional cow’s milk which are A2 protein and A1

protein. The milk of A2 Milk is different because it is free of A1 protein. Three major

strategies of the company are to develop a product portfolio of branded and nutritious

products, to invest in the attractive market and to extend their expertise in A2 protein. A2

Milk has all the capabilities to take the advantage of the major macro-consumer trends which

are growth demand of the consumers in health and wellness products, safety of food,

attribution and naturalness and key growth in middle class in Asia. A2 Milk has three major

markets which yields the majority portion of revenue for the firm; they are United States and

United Kingdom with a revenue of 32.4 million, Australia and New Zealand with a revenue

of 656.6 million and China and other Asia with a revenue of $233.6 million. The ability of

A2 Milk to make A1 protein free milk provides the company with the major competitive

advantage (thea2milkcompany.com 2019).

Industry and Company Overview

Industry

A2 Milk Company Pty Ltd – A2 Milk Company Pvt Ltd (A2 Milk) operates in the

Australian dairy industry. Australia is considered as a small producer of milk, but the

Australian dairy industry is responsible for being the third largest dairy exporter since the

country exports 50% of their production. Australian dairy industry has a gross value of $4

billion and it is Australia’s third largest rural industry. The main produced dairy product in

this industry are milk, milk powder, butter, yogurt and cheese (pwc.com.au 2019).

Bellamy’s Australia Ltd – Bellamy’s Australia Ltd operates in the food and beverage

industry of Australia which is considered as the largest manufacturing sector of Australia.

This industry is a key employer and is the fastest growing manufacturing employer of

regional Australia. In the current years, total amount of revenue from this industry is

US$1,443 million. The Australian food and beverage industry is the major user of the

country’s agricultural products. The main manufacturing products of this industry are meats,

beverages, dairy products, fruits and vegetables, sugar, bakery products, seafood, pet food,

confectionary, flour and cereal products and others (statista.com 2019).

Company

A2 Milk Company Pty Ltd – The main aim of A2 Milk is in producing their customers with

high quality as well as superior brand of dairy products that will contain the A2 protein.

There are two types of protein in the conventional cow’s milk which are A2 protein and A1

protein. The milk of A2 Milk is different because it is free of A1 protein. Three major

strategies of the company are to develop a product portfolio of branded and nutritious

products, to invest in the attractive market and to extend their expertise in A2 protein. A2

Milk has all the capabilities to take the advantage of the major macro-consumer trends which

are growth demand of the consumers in health and wellness products, safety of food,

attribution and naturalness and key growth in middle class in Asia. A2 Milk has three major

markets which yields the majority portion of revenue for the firm; they are United States and

United Kingdom with a revenue of 32.4 million, Australia and New Zealand with a revenue

of 656.6 million and China and other Asia with a revenue of $233.6 million. The ability of

A2 Milk to make A1 protein free milk provides the company with the major competitive

advantage (thea2milkcompany.com 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING PRINCIPLES

Bellamy’s Australia Ltd – Bellamy’s Australia Ltd is considered as a leading Australian

food and beverage company and it is the parent company of Bellamy’s Organic. More

specifically, Bellamy’s Australia is regarded as a major company for infant nutrition in the

markets of Australia and China. The company did not perform well in the financial year of

2017. However, the adopted plan of the company for the year 2018 has provided positive

tangible result in the area of growth in revenue, profitability, balance sheet and cash flows. In

the current years, Bellamy’s Australia has brought certain changes in their business model for

overcoming the difficulties; such as consolidation of sales and distribution channels,

diversification of ingredient procurement, optimization of manufacturing and production

decision, investments in the areas of marketing and branding, improvements in investment,

control and provenance and initiation of crucial future growth engines. The main strategic

focus of the company is perusing long-term premium brand strategy where growth in volume

is targeted for the expansion of the business over the five years. However, the main focus of

Bellamy’s Australia has been the development of the core businesses in Australia to the full

potential (investors.bellamysorganic.com.au 2019).

Cash

1. Cash and cash equivalent can be found in two statements; they are statement of

financial position or balance sheet and statement of cash flows.

2. A2 Milk has cash and cash equivalent of $340,455,000 in 2018, $121,020,000 in 2017

and $69,361,000 in 2016. Bellamy’s Australia has $87,634,000 in 2018, $17,479,000

in 2017 and $32,295,000 in 2016 as cash and cash equivalent.

3. The cash and cash equivalent of A2 Milk has increased in 2018 from 2017; and the

same situation can be seen in case of Bellamy’s Australia since the cash and cash

equivalent has increased in 2018 from 2017.

Receivable

1. A2 Milk has the receivables of trade receivable, impairment allowance and other

receivables. The types of receivable in Bellamy’s Australia are trade receivables, loss

allowance provision and other receivable.

2. A2 Milk does not have any allowance for uncollectible accounts. In case of Bellamy’s

Australia, $116,000 and $100,000 are the loss allowance provision in 2018 and 2017

respectively. Bellamy’s Australia call this as ‘Loss Allowance Provision’. This

information can be found under Note 8 of the financial statements of the firm.

Bellamy’s Australia Ltd – Bellamy’s Australia Ltd is considered as a leading Australian

food and beverage company and it is the parent company of Bellamy’s Organic. More

specifically, Bellamy’s Australia is regarded as a major company for infant nutrition in the

markets of Australia and China. The company did not perform well in the financial year of

2017. However, the adopted plan of the company for the year 2018 has provided positive

tangible result in the area of growth in revenue, profitability, balance sheet and cash flows. In

the current years, Bellamy’s Australia has brought certain changes in their business model for

overcoming the difficulties; such as consolidation of sales and distribution channels,

diversification of ingredient procurement, optimization of manufacturing and production

decision, investments in the areas of marketing and branding, improvements in investment,

control and provenance and initiation of crucial future growth engines. The main strategic

focus of the company is perusing long-term premium brand strategy where growth in volume

is targeted for the expansion of the business over the five years. However, the main focus of

Bellamy’s Australia has been the development of the core businesses in Australia to the full

potential (investors.bellamysorganic.com.au 2019).

Cash

1. Cash and cash equivalent can be found in two statements; they are statement of

financial position or balance sheet and statement of cash flows.

2. A2 Milk has cash and cash equivalent of $340,455,000 in 2018, $121,020,000 in 2017

and $69,361,000 in 2016. Bellamy’s Australia has $87,634,000 in 2018, $17,479,000

in 2017 and $32,295,000 in 2016 as cash and cash equivalent.

3. The cash and cash equivalent of A2 Milk has increased in 2018 from 2017; and the

same situation can be seen in case of Bellamy’s Australia since the cash and cash

equivalent has increased in 2018 from 2017.

Receivable

1. A2 Milk has the receivables of trade receivable, impairment allowance and other

receivables. The types of receivable in Bellamy’s Australia are trade receivables, loss

allowance provision and other receivable.

2. A2 Milk does not have any allowance for uncollectible accounts. In case of Bellamy’s

Australia, $116,000 and $100,000 are the loss allowance provision in 2018 and 2017

respectively. Bellamy’s Australia call this as ‘Loss Allowance Provision’. This

information can be found under Note 8 of the financial statements of the firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING PRINCIPLES

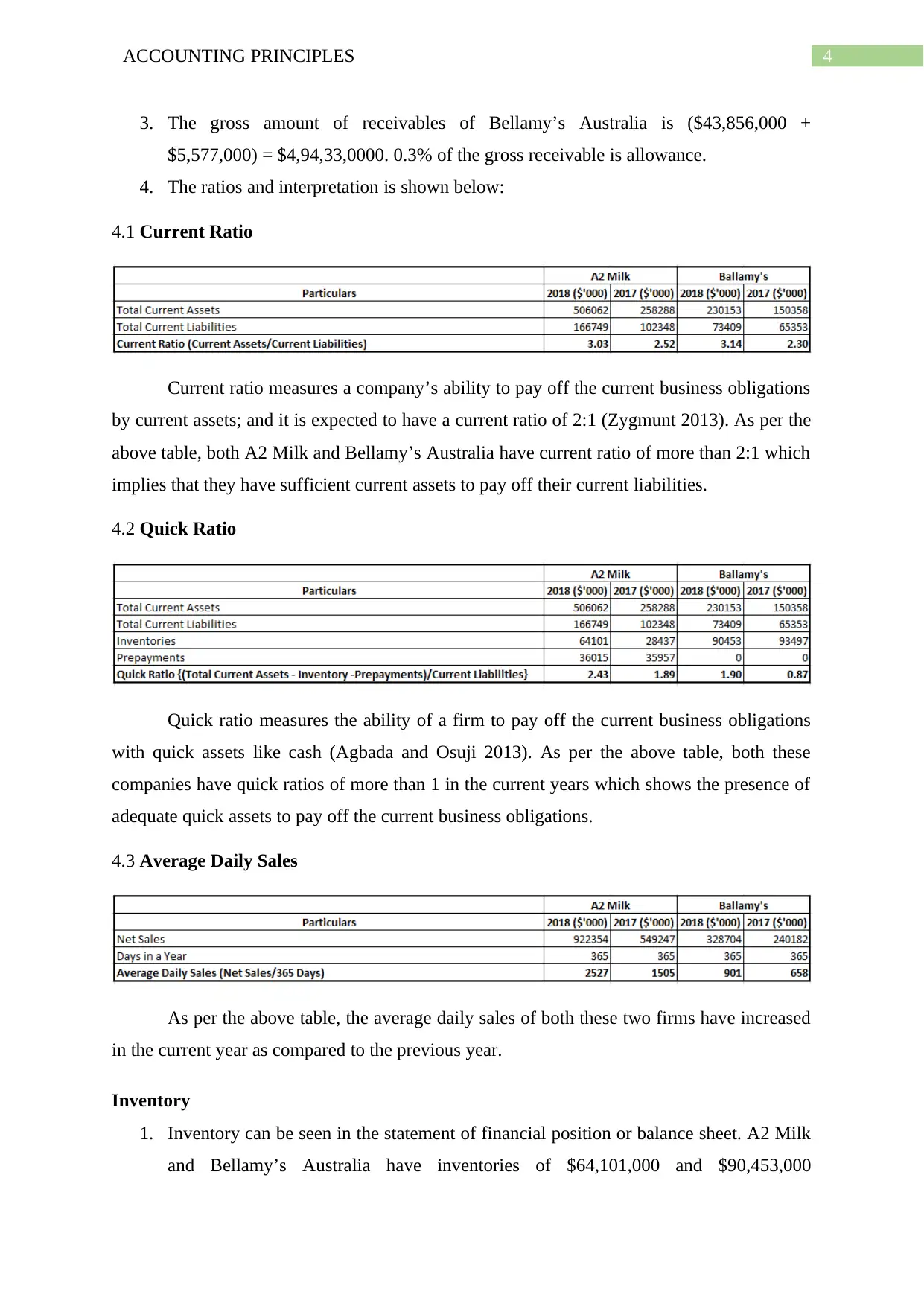

3. The gross amount of receivables of Bellamy’s Australia is ($43,856,000 +

$5,577,000) = $4,94,33,0000. 0.3% of the gross receivable is allowance.

4. The ratios and interpretation is shown below:

4.1 Current Ratio

Current ratio measures a company’s ability to pay off the current business obligations

by current assets; and it is expected to have a current ratio of 2:1 (Zygmunt 2013). As per the

above table, both A2 Milk and Bellamy’s Australia have current ratio of more than 2:1 which

implies that they have sufficient current assets to pay off their current liabilities.

4.2 Quick Ratio

Quick ratio measures the ability of a firm to pay off the current business obligations

with quick assets like cash (Agbada and Osuji 2013). As per the above table, both these

companies have quick ratios of more than 1 in the current years which shows the presence of

adequate quick assets to pay off the current business obligations.

4.3 Average Daily Sales

As per the above table, the average daily sales of both these two firms have increased

in the current year as compared to the previous year.

Inventory

1. Inventory can be seen in the statement of financial position or balance sheet. A2 Milk

and Bellamy’s Australia have inventories of $64,101,000 and $90,453,000

3. The gross amount of receivables of Bellamy’s Australia is ($43,856,000 +

$5,577,000) = $4,94,33,0000. 0.3% of the gross receivable is allowance.

4. The ratios and interpretation is shown below:

4.1 Current Ratio

Current ratio measures a company’s ability to pay off the current business obligations

by current assets; and it is expected to have a current ratio of 2:1 (Zygmunt 2013). As per the

above table, both A2 Milk and Bellamy’s Australia have current ratio of more than 2:1 which

implies that they have sufficient current assets to pay off their current liabilities.

4.2 Quick Ratio

Quick ratio measures the ability of a firm to pay off the current business obligations

with quick assets like cash (Agbada and Osuji 2013). As per the above table, both these

companies have quick ratios of more than 1 in the current years which shows the presence of

adequate quick assets to pay off the current business obligations.

4.3 Average Daily Sales

As per the above table, the average daily sales of both these two firms have increased

in the current year as compared to the previous year.

Inventory

1. Inventory can be seen in the statement of financial position or balance sheet. A2 Milk

and Bellamy’s Australia have inventories of $64,101,000 and $90,453,000

5ACCOUNTING PRINCIPLES

respectively in the current year. The inventory values are provided in thousands (Gaur

and Kesavan 2015).

2. Cost of goods sold can be found in consolidated statement of comprehensive income

or consolidated Statement of Profit or Loss and Other Comprehensive Income. The

page number is 70 for A2 Milk and 49 for Bellamy’s Australia. The cost of goods

sold for A2 Milk and Bellamy’s in the recent year are $458,005,000 and

$199,830,000 respectively and the values are given in thousands.

3. In case of both of the companies, inventories are valued at lower of the cost and net

realisable value. This information can be found in note C2 and note 9 of the financial

statements of A2 Milk and Bellamy’s Australia respectively.

4. Lowe of cost of inventory refers to the fact that a firm must record the cost of

inventory at whichever cost of lower that are the current market price or the original

cost.

5. The inventory turnover ratio is as follows:

As per the above table, A2 Milk has been able in selling their inventory 9.90 times in

a year where Bellamy’s Australia has been able in clearing their inventory for 2.17 times.

Property, Plant and Equipment (PPE)

1. PPE can be found in the statement of financial position or balance sheet. Both A2

Milk and Bellamy’s Australia use the ‘Property, Plant and Machinery’ as names. The

PPE of A2 Milk includes Office and computer, Furniture & fittings, Leasehold

improvements and Plant & equipment. The PPE of Bellamy’s Australia includes Plant

& equipment and Leasehold improvements. The PPE of A2 Milk and Bellamy’s

Australia at the end of 2018 are $9,701,000 and $3,784,000 respectively. The

accumulated depreciation of A2 Milk and Bellamy’s are $7,042,000 and $2,141,000

respectively.

2. As per the notes, The PPE of A2 Milk includes Office and computer, Furniture &

fittings, Leasehold improvements and Plant & equipment. The PPE of Bellamy’s

Australia includes Plant & equipment and Leasehold improvements.

3. Both the companies have used straight-line method for depreciation.

respectively in the current year. The inventory values are provided in thousands (Gaur

and Kesavan 2015).

2. Cost of goods sold can be found in consolidated statement of comprehensive income

or consolidated Statement of Profit or Loss and Other Comprehensive Income. The

page number is 70 for A2 Milk and 49 for Bellamy’s Australia. The cost of goods

sold for A2 Milk and Bellamy’s in the recent year are $458,005,000 and

$199,830,000 respectively and the values are given in thousands.

3. In case of both of the companies, inventories are valued at lower of the cost and net

realisable value. This information can be found in note C2 and note 9 of the financial

statements of A2 Milk and Bellamy’s Australia respectively.

4. Lowe of cost of inventory refers to the fact that a firm must record the cost of

inventory at whichever cost of lower that are the current market price or the original

cost.

5. The inventory turnover ratio is as follows:

As per the above table, A2 Milk has been able in selling their inventory 9.90 times in

a year where Bellamy’s Australia has been able in clearing their inventory for 2.17 times.

Property, Plant and Equipment (PPE)

1. PPE can be found in the statement of financial position or balance sheet. Both A2

Milk and Bellamy’s Australia use the ‘Property, Plant and Machinery’ as names. The

PPE of A2 Milk includes Office and computer, Furniture & fittings, Leasehold

improvements and Plant & equipment. The PPE of Bellamy’s Australia includes Plant

& equipment and Leasehold improvements. The PPE of A2 Milk and Bellamy’s

Australia at the end of 2018 are $9,701,000 and $3,784,000 respectively. The

accumulated depreciation of A2 Milk and Bellamy’s are $7,042,000 and $2,141,000

respectively.

2. As per the notes, The PPE of A2 Milk includes Office and computer, Furniture &

fittings, Leasehold improvements and Plant & equipment. The PPE of Bellamy’s

Australia includes Plant & equipment and Leasehold improvements.

3. Both the companies have used straight-line method for depreciation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING PRINCIPLES

4. Both the companies have depreciate their plant assets over the useful lives.

5. The intangible assets of A2 Milk are patents, trademarks, software, project

development and goodwill; and the intangible assets of Bellamy’s Australia are

goodwill, licences and customer contracts, production accesses, other intangibles. In

case of A2 Milk, software, patents and trademarks are subject to amortization on

straight line basis, but trademarks are tested for impairment. Goodwill is recognized at

cost and are measured at cost less any accumulated depreciation. For Bellamy’s

Australia, licences and customer contracts are measured at fair value and goodwill is

allocated to cash-generating units.

Current Liabilities

Current liabilities can be found in the statement of financial position or balance sheet.

The current liabilities of A2 Milk contains trade and other payable and income tax

payable. The current liabilities of Bellamy’s Australia include trade and other

payable, borrowings, provisions, derivatives and current tax liabilities (Laux 2013).

A2 Milk does not have any contingent liability in 2018 and this can be seen in Note

D9 of the financial statements. As per the Note 24 of the financial statements of

Bellamy’s Australia, the company has a contingent liability where due to the

proceedings of Staler and Gordon on 23 February 2017 and Maurice Blackburn on 8

March 2017 in the Federal Court of Australia. The claim is related to the allegation of

contravention of the Corporations Act 2001 (Cth) regarding depictive conduct and

obligation for continuous disclosure.

Non-Current Liabilities

1. Non-current liabilities can be found in the statement of financial position or balance

sheet. The non-current liabilities of A2 Milk includes only trade and other payable.

The non-current liabilities of Bellamy’s include only provision.

2. The notes of financial statement of A2 Milk states that employee entitlement is the

non-current liability of the firm; it also includes the value and description of the same.

The notes of Bellamy’s Australia shows the employee benefit is the non-current

liability of the firm. It also contains the description of the same.

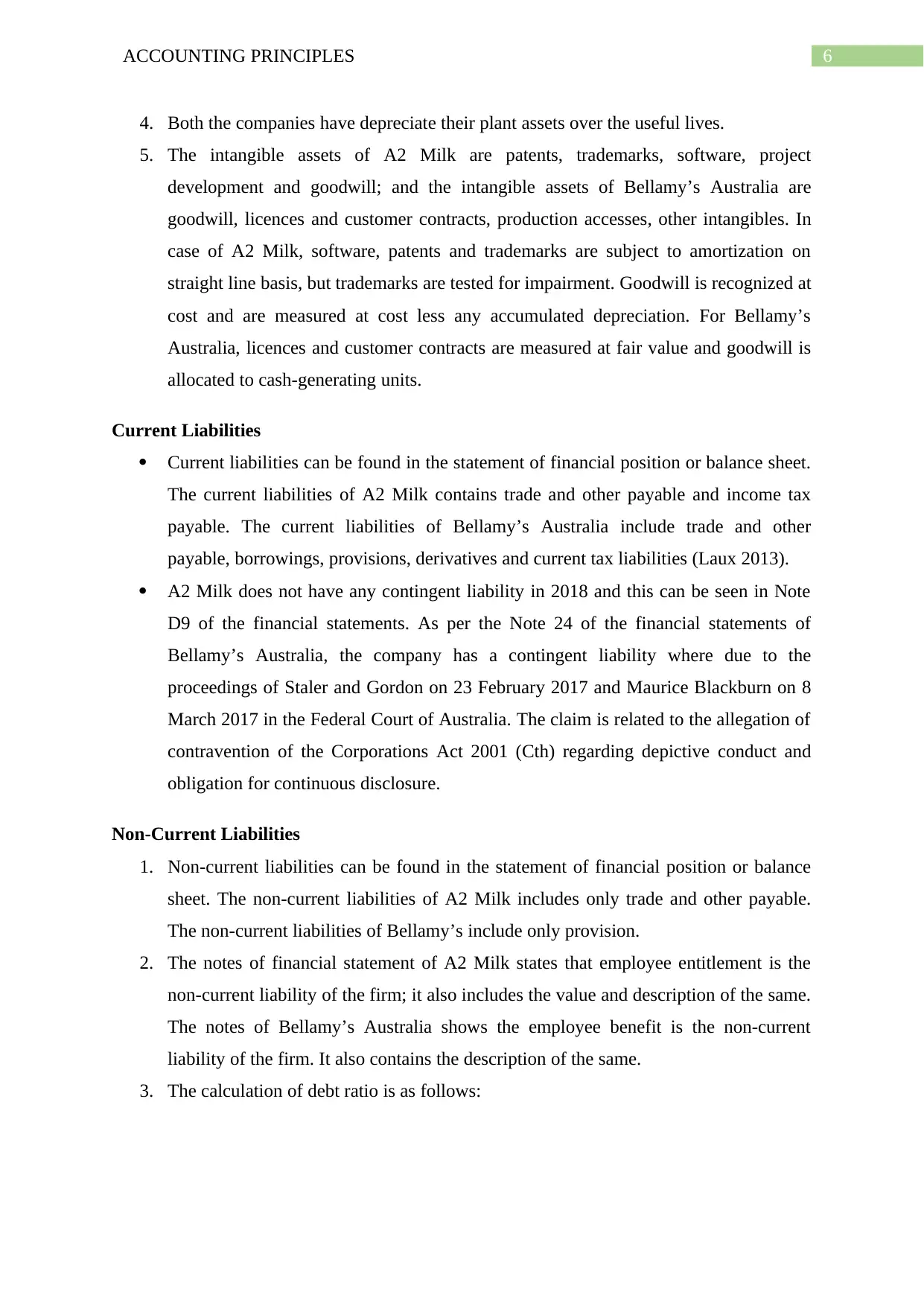

3. The calculation of debt ratio is as follows:

4. Both the companies have depreciate their plant assets over the useful lives.

5. The intangible assets of A2 Milk are patents, trademarks, software, project

development and goodwill; and the intangible assets of Bellamy’s Australia are

goodwill, licences and customer contracts, production accesses, other intangibles. In

case of A2 Milk, software, patents and trademarks are subject to amortization on

straight line basis, but trademarks are tested for impairment. Goodwill is recognized at

cost and are measured at cost less any accumulated depreciation. For Bellamy’s

Australia, licences and customer contracts are measured at fair value and goodwill is

allocated to cash-generating units.

Current Liabilities

Current liabilities can be found in the statement of financial position or balance sheet.

The current liabilities of A2 Milk contains trade and other payable and income tax

payable. The current liabilities of Bellamy’s Australia include trade and other

payable, borrowings, provisions, derivatives and current tax liabilities (Laux 2013).

A2 Milk does not have any contingent liability in 2018 and this can be seen in Note

D9 of the financial statements. As per the Note 24 of the financial statements of

Bellamy’s Australia, the company has a contingent liability where due to the

proceedings of Staler and Gordon on 23 February 2017 and Maurice Blackburn on 8

March 2017 in the Federal Court of Australia. The claim is related to the allegation of

contravention of the Corporations Act 2001 (Cth) regarding depictive conduct and

obligation for continuous disclosure.

Non-Current Liabilities

1. Non-current liabilities can be found in the statement of financial position or balance

sheet. The non-current liabilities of A2 Milk includes only trade and other payable.

The non-current liabilities of Bellamy’s include only provision.

2. The notes of financial statement of A2 Milk states that employee entitlement is the

non-current liability of the firm; it also includes the value and description of the same.

The notes of Bellamy’s Australia shows the employee benefit is the non-current

liability of the firm. It also contains the description of the same.

3. The calculation of debt ratio is as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING PRINCIPLES

As per the above table, A2 Milk has 0.23 and 0.30 debt ration which implies that the

firm has around four times and three times as many assets as it has liabilities in 2018 and

2017 respectively. In case of Bellamy’s Australia, the firm has around four times and more

than two times as many assets as it has liabilities in 2018 and 2017 respectively.

4. The times interest earned ratio is show below:

The above table shows that A2 Milk can make interest payment of many times since

they have small interest expenses as compared to their EBIT. However, in case of Bellamy’s

Australia, the company did not have the required EBIT to make the interest payment even for

once.

Shareholder’s Equity

1. Shareholder’s equity is in the last section of the statement of financial position of both

the companies (Bloom, Sadun and Van Reenen 2015).

2. A2 Milk and Bellamy’s Australia have issued only ordinary equity shares. Both A2

Milk and Bellamy’s Australia have issued 731,539,067 shares and 113,316,104 shares

respectively. Both these companies do not have any outstanding share in the current

year. These numbers are in millions.

3. A2 Milk did not issue any new share in 2018 where Bellamy’s Australia issued

12,928,292 number of shares in the current year.

4. Both of these companies have not declared any dividend in the current year.

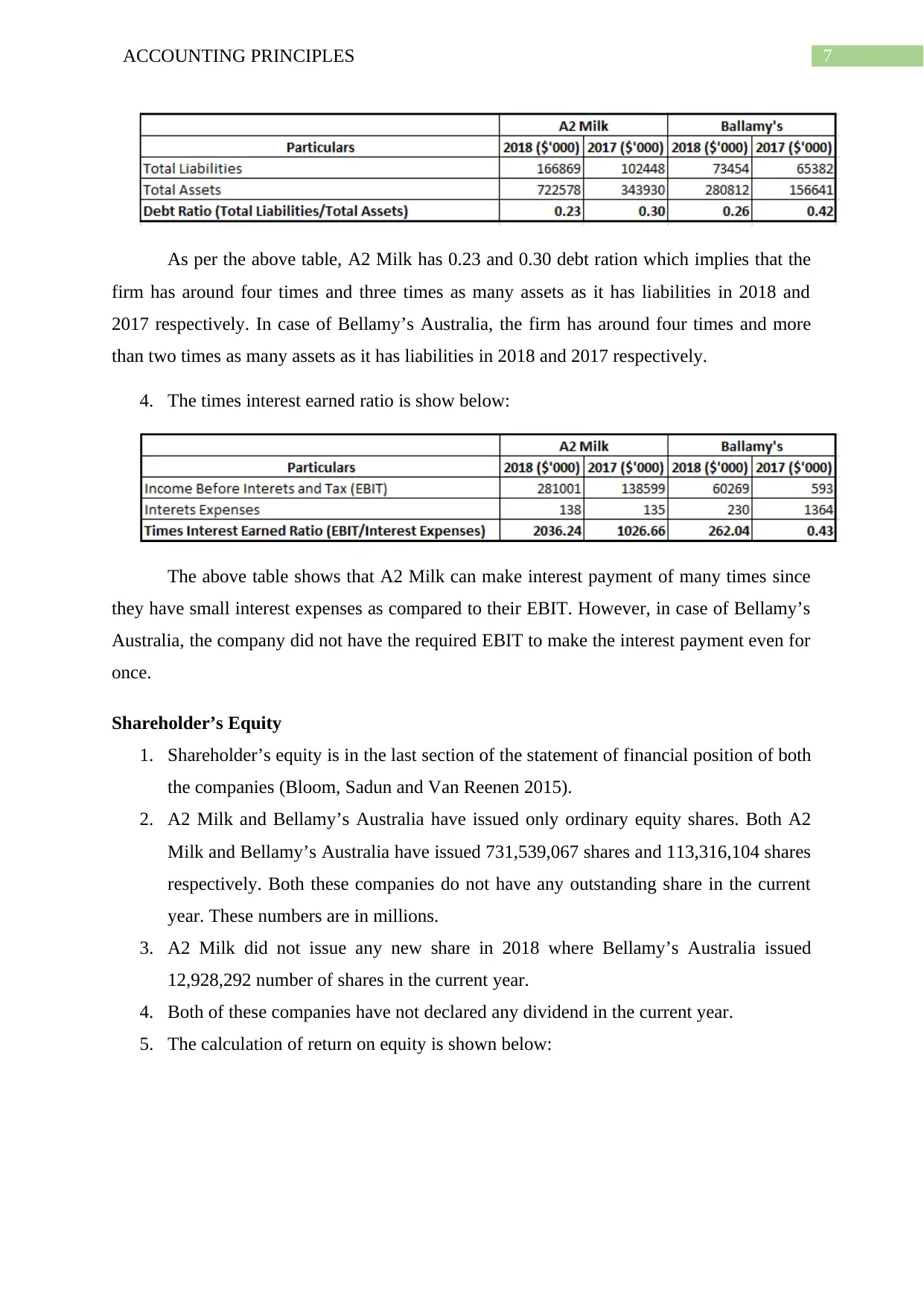

5. The calculation of return on equity is shown below:

As per the above table, A2 Milk has 0.23 and 0.30 debt ration which implies that the

firm has around four times and three times as many assets as it has liabilities in 2018 and

2017 respectively. In case of Bellamy’s Australia, the firm has around four times and more

than two times as many assets as it has liabilities in 2018 and 2017 respectively.

4. The times interest earned ratio is show below:

The above table shows that A2 Milk can make interest payment of many times since

they have small interest expenses as compared to their EBIT. However, in case of Bellamy’s

Australia, the company did not have the required EBIT to make the interest payment even for

once.

Shareholder’s Equity

1. Shareholder’s equity is in the last section of the statement of financial position of both

the companies (Bloom, Sadun and Van Reenen 2015).

2. A2 Milk and Bellamy’s Australia have issued only ordinary equity shares. Both A2

Milk and Bellamy’s Australia have issued 731,539,067 shares and 113,316,104 shares

respectively. Both these companies do not have any outstanding share in the current

year. These numbers are in millions.

3. A2 Milk did not issue any new share in 2018 where Bellamy’s Australia issued

12,928,292 number of shares in the current year.

4. Both of these companies have not declared any dividend in the current year.

5. The calculation of return on equity is shown below:

8ACCOUNTING PRINCIPLES

Auditor’s Letter

1. Both these two companies can have an internal control of Physical Audit of Assets

which includes hand-counting cash and tracking of physical assets in the accounting

system like material, tools, inventory and others. A part of the accounts department is

responsible for this control and this control includes the periodic observation of the

above-mentioned aspects.

2. For both of these two companies, the auditor’s report can be seen under the

Independent Auditor’s Report. In case of both of these two companies, the auditors

have mentioned that the directors have complied with the necessary accounting

standards of AASB, Australian Accounting Standards, Corporation Act 2001, IASB

and IFRS for maintaining the internal control of financial reporting.

Statement of Cash Flows

1. The statement of cash flows can be seen in page 73 of A2 Milk and page 52 of

Bellamy’s Australia (Williams and Dobelman 2017).

2. Both these companies have used direct method for cash flow since they have not used

net income as the base.

3. A2 has bought more property, plant and equipment in 2018 than 2017 since the

payment for the same is $2,526,000 in 2018 and $1,650,000 in 2017. The same can be

seen in case of Bellamy’s Australian since the purchase of property, plant and

equipment is $2,028,000 in 2018 and $273,000 in 2017.

4. Both of these companies have not made any buyback of shares and have not pay any

dividend.

5. In case of A2 Milk, operating activities have generated more cash flow which implies

that the company has generated most of cash from its operating activities. In case of

Bellamy’s Australia, financing activities have generated most cash which implies that

the company has generated most cash flow from financing activities like proceeds

from share issues.

Auditor’s Letter

1. Both these two companies can have an internal control of Physical Audit of Assets

which includes hand-counting cash and tracking of physical assets in the accounting

system like material, tools, inventory and others. A part of the accounts department is

responsible for this control and this control includes the periodic observation of the

above-mentioned aspects.

2. For both of these two companies, the auditor’s report can be seen under the

Independent Auditor’s Report. In case of both of these two companies, the auditors

have mentioned that the directors have complied with the necessary accounting

standards of AASB, Australian Accounting Standards, Corporation Act 2001, IASB

and IFRS for maintaining the internal control of financial reporting.

Statement of Cash Flows

1. The statement of cash flows can be seen in page 73 of A2 Milk and page 52 of

Bellamy’s Australia (Williams and Dobelman 2017).

2. Both these companies have used direct method for cash flow since they have not used

net income as the base.

3. A2 has bought more property, plant and equipment in 2018 than 2017 since the

payment for the same is $2,526,000 in 2018 and $1,650,000 in 2017. The same can be

seen in case of Bellamy’s Australian since the purchase of property, plant and

equipment is $2,028,000 in 2018 and $273,000 in 2017.

4. Both of these companies have not made any buyback of shares and have not pay any

dividend.

5. In case of A2 Milk, operating activities have generated more cash flow which implies

that the company has generated most of cash from its operating activities. In case of

Bellamy’s Australia, financing activities have generated most cash which implies that

the company has generated most cash flow from financing activities like proceeds

from share issues.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING PRINCIPLES

Ratio Analysis

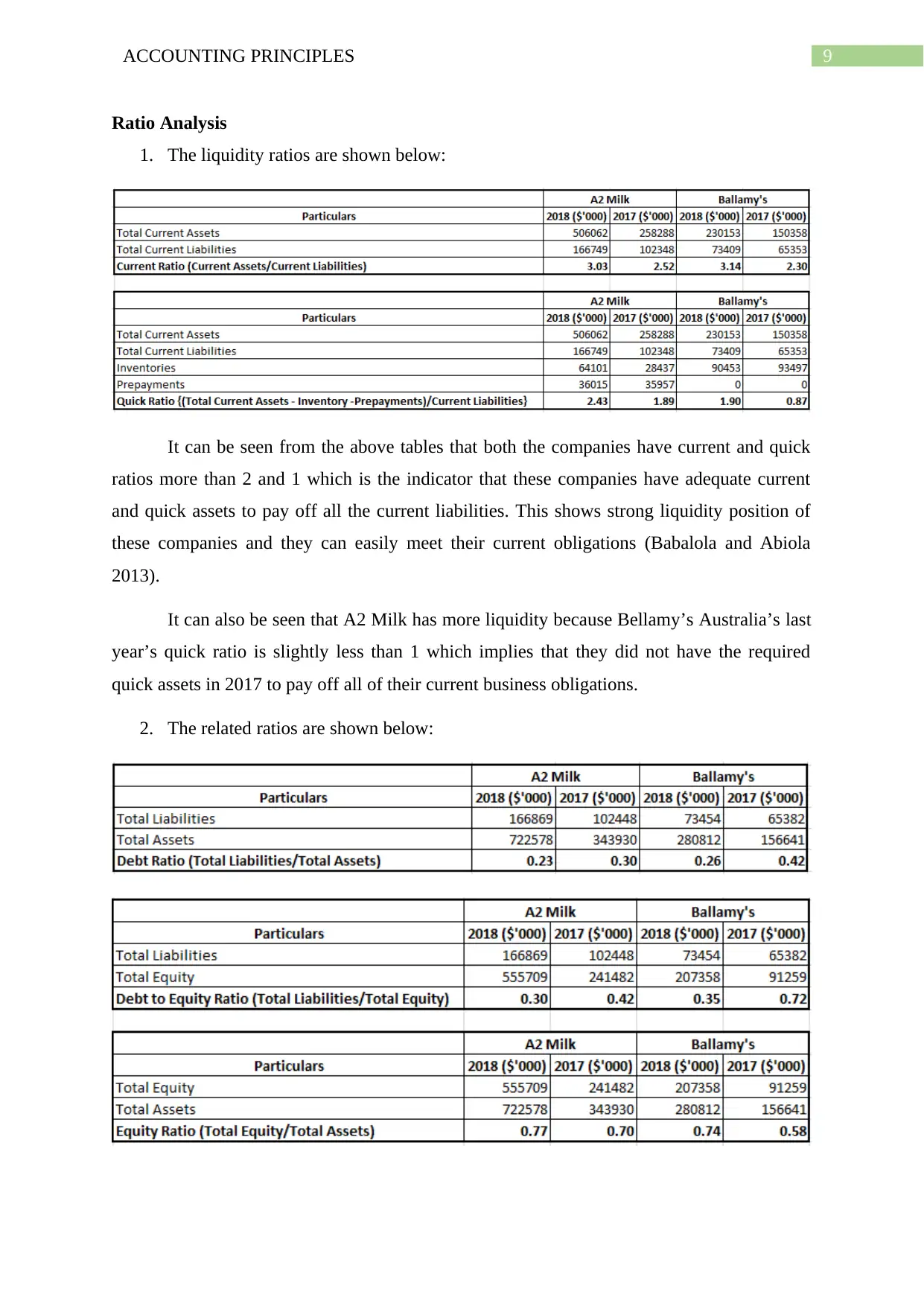

1. The liquidity ratios are shown below:

It can be seen from the above tables that both the companies have current and quick

ratios more than 2 and 1 which is the indicator that these companies have adequate current

and quick assets to pay off all the current liabilities. This shows strong liquidity position of

these companies and they can easily meet their current obligations (Babalola and Abiola

2013).

It can also be seen that A2 Milk has more liquidity because Bellamy’s Australia’s last

year’s quick ratio is slightly less than 1 which implies that they did not have the required

quick assets in 2017 to pay off all of their current business obligations.

2. The related ratios are shown below:

Ratio Analysis

1. The liquidity ratios are shown below:

It can be seen from the above tables that both the companies have current and quick

ratios more than 2 and 1 which is the indicator that these companies have adequate current

and quick assets to pay off all the current liabilities. This shows strong liquidity position of

these companies and they can easily meet their current obligations (Babalola and Abiola

2013).

It can also be seen that A2 Milk has more liquidity because Bellamy’s Australia’s last

year’s quick ratio is slightly less than 1 which implies that they did not have the required

quick assets in 2017 to pay off all of their current business obligations.

2. The related ratios are shown below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING PRINCIPLES

It can be seen from the above tables that both A2 Milk and Bellamy’s Australia has

less amount of debts as compare to total assets. It can also be seen that these companies have

emphasized on equity shares for raising capital. All these aspects indicates towards the fact

that it is easy for these two companies to meet their long-term obligations due to the presence

of less amount of debts as compared to total assets.

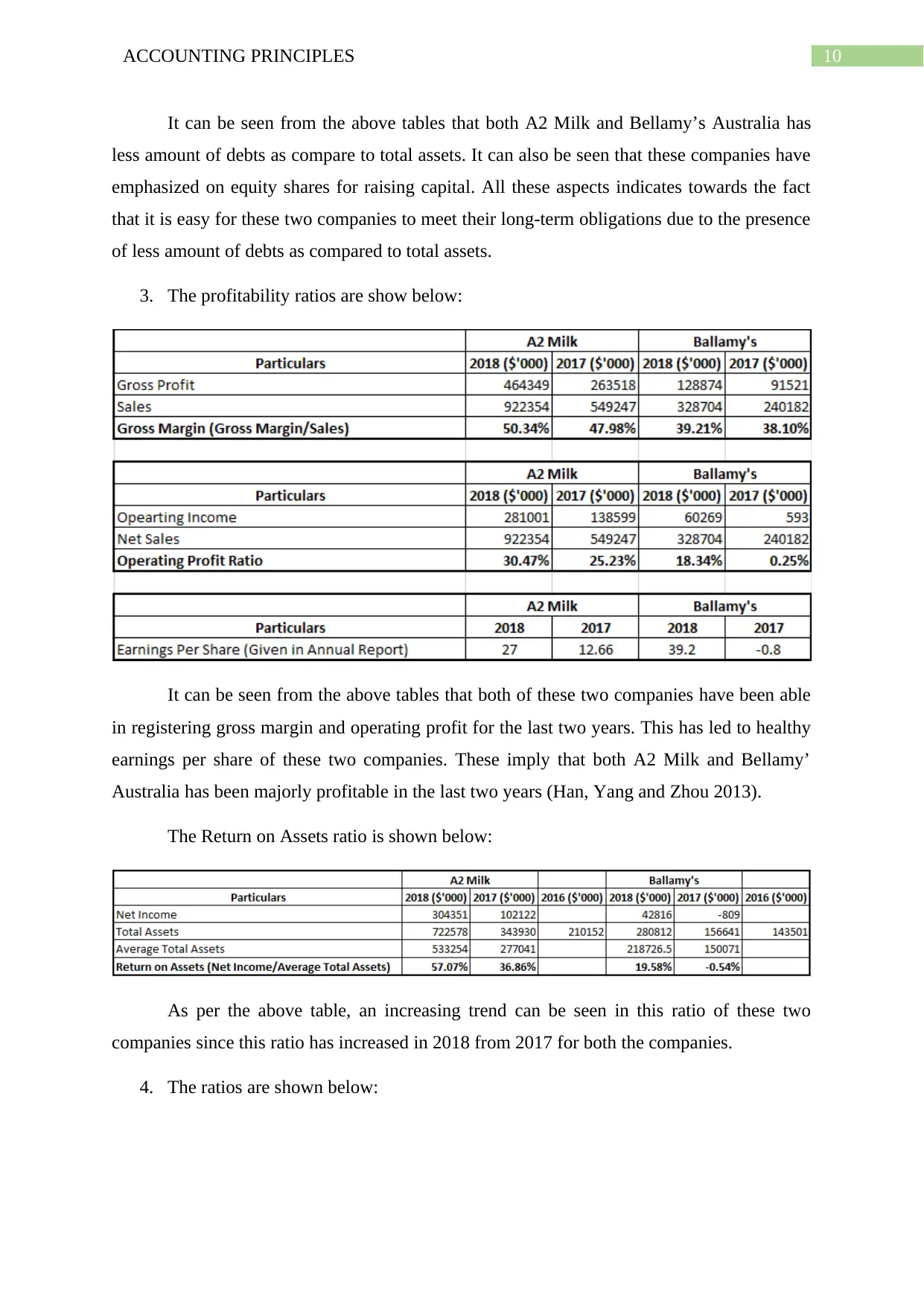

3. The profitability ratios are show below:

It can be seen from the above tables that both of these two companies have been able

in registering gross margin and operating profit for the last two years. This has led to healthy

earnings per share of these two companies. These imply that both A2 Milk and Bellamy’

Australia has been majorly profitable in the last two years (Han, Yang and Zhou 2013).

The Return on Assets ratio is shown below:

As per the above table, an increasing trend can be seen in this ratio of these two

companies since this ratio has increased in 2018 from 2017 for both the companies.

4. The ratios are shown below:

It can be seen from the above tables that both A2 Milk and Bellamy’s Australia has

less amount of debts as compare to total assets. It can also be seen that these companies have

emphasized on equity shares for raising capital. All these aspects indicates towards the fact

that it is easy for these two companies to meet their long-term obligations due to the presence

of less amount of debts as compared to total assets.

3. The profitability ratios are show below:

It can be seen from the above tables that both of these two companies have been able

in registering gross margin and operating profit for the last two years. This has led to healthy

earnings per share of these two companies. These imply that both A2 Milk and Bellamy’

Australia has been majorly profitable in the last two years (Han, Yang and Zhou 2013).

The Return on Assets ratio is shown below:

As per the above table, an increasing trend can be seen in this ratio of these two

companies since this ratio has increased in 2018 from 2017 for both the companies.

4. The ratios are shown below:

11ACCOUNTING PRINCIPLES

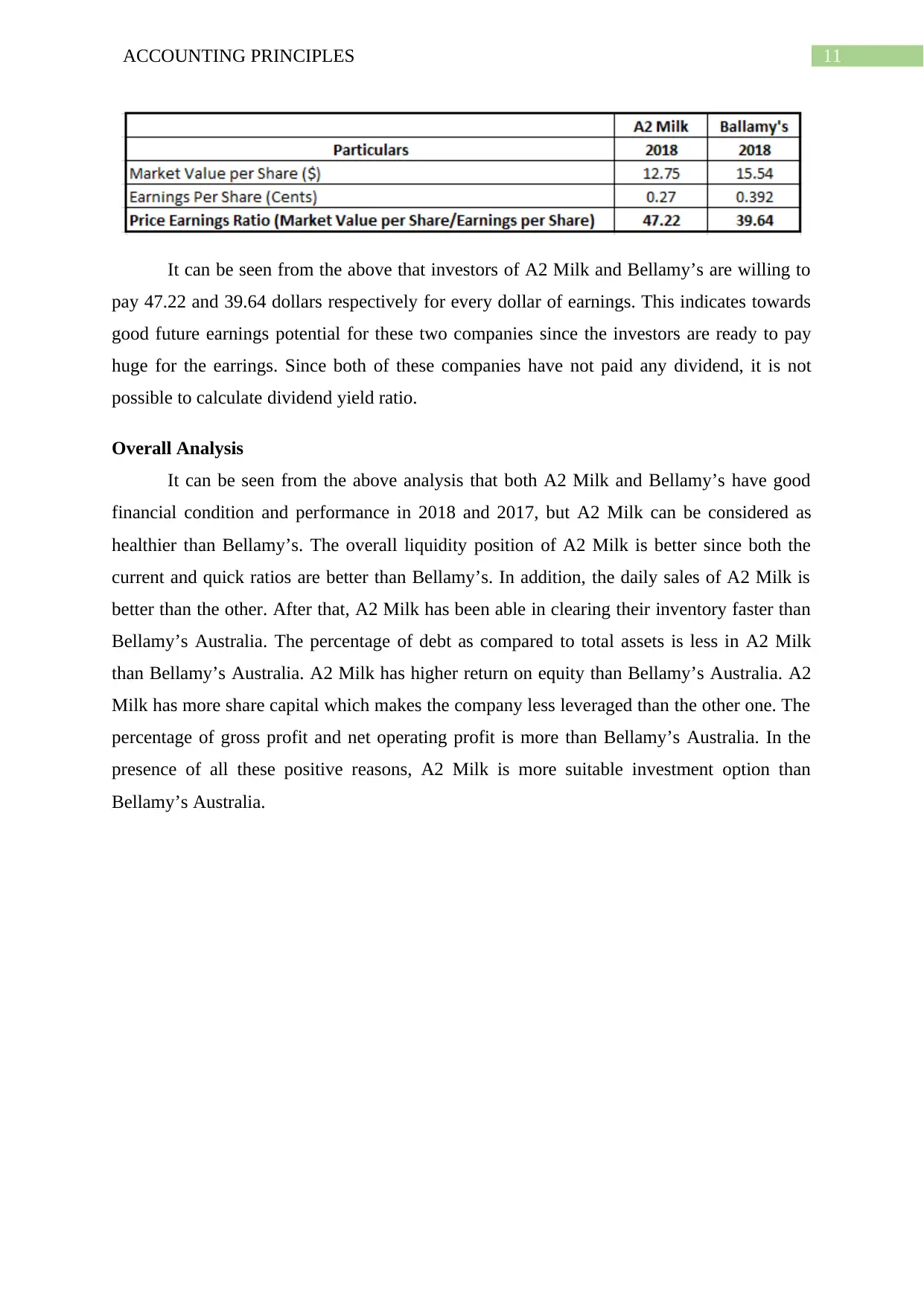

It can be seen from the above that investors of A2 Milk and Bellamy’s are willing to

pay 47.22 and 39.64 dollars respectively for every dollar of earnings. This indicates towards

good future earnings potential for these two companies since the investors are ready to pay

huge for the earrings. Since both of these companies have not paid any dividend, it is not

possible to calculate dividend yield ratio.

Overall Analysis

It can be seen from the above analysis that both A2 Milk and Bellamy’s have good

financial condition and performance in 2018 and 2017, but A2 Milk can be considered as

healthier than Bellamy’s. The overall liquidity position of A2 Milk is better since both the

current and quick ratios are better than Bellamy’s. In addition, the daily sales of A2 Milk is

better than the other. After that, A2 Milk has been able in clearing their inventory faster than

Bellamy’s Australia. The percentage of debt as compared to total assets is less in A2 Milk

than Bellamy’s Australia. A2 Milk has higher return on equity than Bellamy’s Australia. A2

Milk has more share capital which makes the company less leveraged than the other one. The

percentage of gross profit and net operating profit is more than Bellamy’s Australia. In the

presence of all these positive reasons, A2 Milk is more suitable investment option than

Bellamy’s Australia.

It can be seen from the above that investors of A2 Milk and Bellamy’s are willing to

pay 47.22 and 39.64 dollars respectively for every dollar of earnings. This indicates towards

good future earnings potential for these two companies since the investors are ready to pay

huge for the earrings. Since both of these companies have not paid any dividend, it is not

possible to calculate dividend yield ratio.

Overall Analysis

It can be seen from the above analysis that both A2 Milk and Bellamy’s have good

financial condition and performance in 2018 and 2017, but A2 Milk can be considered as

healthier than Bellamy’s. The overall liquidity position of A2 Milk is better since both the

current and quick ratios are better than Bellamy’s. In addition, the daily sales of A2 Milk is

better than the other. After that, A2 Milk has been able in clearing their inventory faster than

Bellamy’s Australia. The percentage of debt as compared to total assets is less in A2 Milk

than Bellamy’s Australia. A2 Milk has higher return on equity than Bellamy’s Australia. A2

Milk has more share capital which makes the company less leveraged than the other one. The

percentage of gross profit and net operating profit is more than Bellamy’s Australia. In the

presence of all these positive reasons, A2 Milk is more suitable investment option than

Bellamy’s Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.