Detailed Financial Analysis of Crystal Hotel: Management Accounting

VerifiedAdded on 2023/06/10

|11

|2203

|257

Report

AI Summary

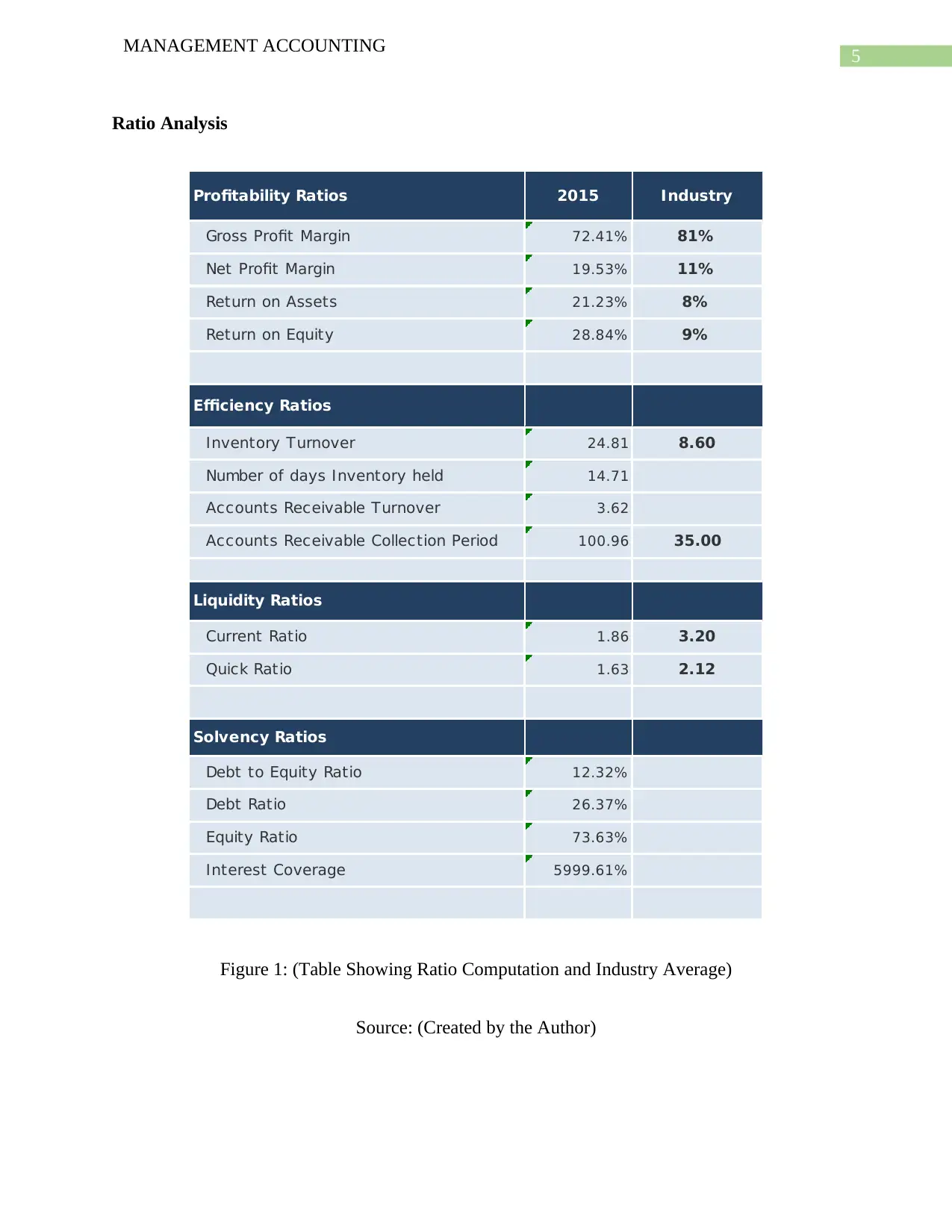

This report presents a detailed financial analysis of Crystal Hotel, employing vertical analysis of the income statement and ratio analysis to assess the hotel's performance against industry benchmarks. The vertical analysis reveals that Crystal Hotel excels in room revenue but lags in cost of sales, indicating a need for improved internal controls. Ratio analysis highlights strong profitability metrics, including net profit margin, return on assets, and return on equity, significantly exceeding industry averages. However, liquidity ratios suggest room for improvement, and the credit policy appears lenient. The report recommends strategies to enhance food and beverage services, reduce costs, and optimize capital structure. Additional industry-specific benchmarks, such as market valuation, star ratings, and customer satisfaction, are suggested for comprehensive performance evaluation. Desklib offers a wealth of similar solved assignments and past papers for students seeking to deepen their understanding of financial analysis and management accounting.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.