Financial Statement Analysis, Investment Appraisal and CVP Technique

VerifiedAdded on 2023/06/18

|16

|4198

|479

Report

AI Summary

This finance report provides a detailed analysis of various financial concepts and techniques. It begins with a critical discussion of the 'comply or explain' model in corporate governance, followed by an identification and explanation of the characteristics of approaches used for filing financial statements in the UK. The report then evaluates the payback technique and accounting rate of return (ARR) for two companies, Edinburgh and Newcastle, including an analysis of their respective advantages and disadvantages. Furthermore, it delves into the concept of contribution and its significance to the Cost-Volume-Profit (CVP) technique, examining its usefulness in decision-making scenarios such as dropping a product or service and special contracts. The report also provides a critical evaluation of the CVP technique and its limitations. Finally, the report includes the preparation of an opening statement of financial position and a monthly cash flow forecast, considering additional expenses that necessitate financial assistance. Desklib offers a variety of solved assignments and past papers for students.

Introduction to finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

Critical discussion of 'comply or explain' model........................................................................3

Identification and explanation of characteristics of approaches used for filing of financial

statements in UK.........................................................................................................................4

TASK 2............................................................................................................................................4

Critical evaluation of payback technique:...................................................................................6

Characteristics of investment appraisal as well as advantages and disadvantages of IRR:........7

TASK 3............................................................................................................................................8

Concept of contribution and its significance to CVP technique:................................................8

Nature of 'dropping a product or service' and 'special contract' decisions for usefulness of CVP

technique:....................................................................................................................................9

Critical evaluation of CVP technique and its limitations:.........................................................10

TASK 4..........................................................................................................................................10

Preparation of opening statement of financial position:...........................................................10

Preparation of monthly cash flow forecast:..............................................................................11

Additional expense taken into account to need financial assistance:........................................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

Critical discussion of 'comply or explain' model........................................................................3

Identification and explanation of characteristics of approaches used for filing of financial

statements in UK.........................................................................................................................4

TASK 2............................................................................................................................................4

Critical evaluation of payback technique:...................................................................................6

Characteristics of investment appraisal as well as advantages and disadvantages of IRR:........7

TASK 3............................................................................................................................................8

Concept of contribution and its significance to CVP technique:................................................8

Nature of 'dropping a product or service' and 'special contract' decisions for usefulness of CVP

technique:....................................................................................................................................9

Critical evaluation of CVP technique and its limitations:.........................................................10

TASK 4..........................................................................................................................................10

Preparation of opening statement of financial position:...........................................................10

Preparation of monthly cash flow forecast:..............................................................................11

Additional expense taken into account to need financial assistance:........................................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The term finance is related to sources of funds used within a company to operates its

business activities. Finance is a process that provides assistance in formation of capital of an

organisation and helps in making better business decisions. Financial decision facilitates in

analysing benefits and drawbacks of a specific business activity and also helps in identifying

transactions that are generating losses within the company. Within present portfolio, there are

four task in which first one is discussing about comply or explain model of corporate governance

(Braumann, C. A., 2019). This task is also including characteristics of approaches used for filling

financial statements. Next section is about calculation of Payback period and accounting rate of

return along with their evaluation. Third part is describing CVP technique and its limitation in

context to different interpretations. Final section is about preparation of opening statement of

financial position and a monthly cash flow forecast.

TASK 1

Critical discussion of 'comply or explain' model.

'Comply or explain' model is a tool that is used by organisations under corporate

governance code. This model explains that the company has to comply with rules and regulations

mentioned under it. If it is not following mentioned rules and regulations then it has to explain

reasons behind not following it. Primary objective of this model is to present true and good

corporate governance within the firm. Comply or explain model helps company by providing

flexible environment of whether working according to these codes or not. This model demands

complete transparency from firms that adhere to these codes as well as asks for reasons in case of

any failure to such rules. Companies have to mention the options pursued by them to integrate

well structured governance within organisation (Rethel, L. and Thurbon, E., 2020). With given

clarification if investors of company are not satisfied, then they have right to sell the shares of

company by generating a market warrant. It forbids the company to deal any kind of transaction

with that entity. It acts as a fine for not performing according to needs of corportate governance.

Other than 'comply or explain' model, there is an another approach also that is relevant to

corporate governance code and are also adopted in the global world. That another approach is

comply-or-else' model in which official controller of regulatuions and rules directed some codes

that has to be adhered by firms. If a company is not following those rules then it will be liable to

pay penalty which can be in the form of imprisonment or fines. Most of the time companies

The term finance is related to sources of funds used within a company to operates its

business activities. Finance is a process that provides assistance in formation of capital of an

organisation and helps in making better business decisions. Financial decision facilitates in

analysing benefits and drawbacks of a specific business activity and also helps in identifying

transactions that are generating losses within the company. Within present portfolio, there are

four task in which first one is discussing about comply or explain model of corporate governance

(Braumann, C. A., 2019). This task is also including characteristics of approaches used for filling

financial statements. Next section is about calculation of Payback period and accounting rate of

return along with their evaluation. Third part is describing CVP technique and its limitation in

context to different interpretations. Final section is about preparation of opening statement of

financial position and a monthly cash flow forecast.

TASK 1

Critical discussion of 'comply or explain' model.

'Comply or explain' model is a tool that is used by organisations under corporate

governance code. This model explains that the company has to comply with rules and regulations

mentioned under it. If it is not following mentioned rules and regulations then it has to explain

reasons behind not following it. Primary objective of this model is to present true and good

corporate governance within the firm. Comply or explain model helps company by providing

flexible environment of whether working according to these codes or not. This model demands

complete transparency from firms that adhere to these codes as well as asks for reasons in case of

any failure to such rules. Companies have to mention the options pursued by them to integrate

well structured governance within organisation (Rethel, L. and Thurbon, E., 2020). With given

clarification if investors of company are not satisfied, then they have right to sell the shares of

company by generating a market warrant. It forbids the company to deal any kind of transaction

with that entity. It acts as a fine for not performing according to needs of corportate governance.

Other than 'comply or explain' model, there is an another approach also that is relevant to

corporate governance code and are also adopted in the global world. That another approach is

comply-or-else' model in which official controller of regulatuions and rules directed some codes

that has to be adhered by firms. If a company is not following those rules then it will be liable to

pay penalty which can be in the form of imprisonment or fines. Most of the time companies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

follow 'comply or explain' model in which they have choices for adopting governance codes or

explain reasons for not adhering the codes.

Identification and explanation of characteristics of approaches used for filing of financial

statements in UK.

All companies in UK are directed to compile their financial statements to Londom stock

Exchange and companies house according to responsibilities imposed by Financial Conduct

Authority (FCA) (Landström, H., 2017). As per Companies Act 2006 of UK, there are some

obligations under section 441-443 in which a company has to perform those responsibilities for

filing its accounts by company's registrar ( Filing reuirements for UK companies, 2021).

There are different approaches for filing financial statements and some of them are

described below with their characteristics:

Public sector companies are requied to file their reports and accounts within a duration of

six months at the end of their financial period (Shabbir, M. S., Ghazi, M. S. and Akhtar,

T., 2016). This time duration can also increase or decrease with the help of certain

provisions having power to variate time period.

Private sector companies are required to file their statements and accounts within a

duration of nine months at the end of their financial period (Filing requirements UK

companies, 2021). There are some another provisions also which have authority to

decrease or increase this time duration.

If there is any delay in filing of statements, then firm has to make application with its

registered number explaining the reason behind taking extra time and documents attached

with application.

Companies have to completely disclose their several statements with implying relevant

rules on it including amounts of interest on capital, interest of directors, payment of taxes,

inclusion of another companies and many more.

TASK 2

Calculation of Payback Period for both companies:

For Edinburgh,

Total Investments = 8700 + 4120= 12820

Years £000

explain reasons for not adhering the codes.

Identification and explanation of characteristics of approaches used for filing of financial

statements in UK.

All companies in UK are directed to compile their financial statements to Londom stock

Exchange and companies house according to responsibilities imposed by Financial Conduct

Authority (FCA) (Landström, H., 2017). As per Companies Act 2006 of UK, there are some

obligations under section 441-443 in which a company has to perform those responsibilities for

filing its accounts by company's registrar ( Filing reuirements for UK companies, 2021).

There are different approaches for filing financial statements and some of them are

described below with their characteristics:

Public sector companies are requied to file their reports and accounts within a duration of

six months at the end of their financial period (Shabbir, M. S., Ghazi, M. S. and Akhtar,

T., 2016). This time duration can also increase or decrease with the help of certain

provisions having power to variate time period.

Private sector companies are required to file their statements and accounts within a

duration of nine months at the end of their financial period (Filing requirements UK

companies, 2021). There are some another provisions also which have authority to

decrease or increase this time duration.

If there is any delay in filing of statements, then firm has to make application with its

registered number explaining the reason behind taking extra time and documents attached

with application.

Companies have to completely disclose their several statements with implying relevant

rules on it including amounts of interest on capital, interest of directors, payment of taxes,

inclusion of another companies and many more.

TASK 2

Calculation of Payback Period for both companies:

For Edinburgh,

Total Investments = 8700 + 4120= 12820

Years £000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

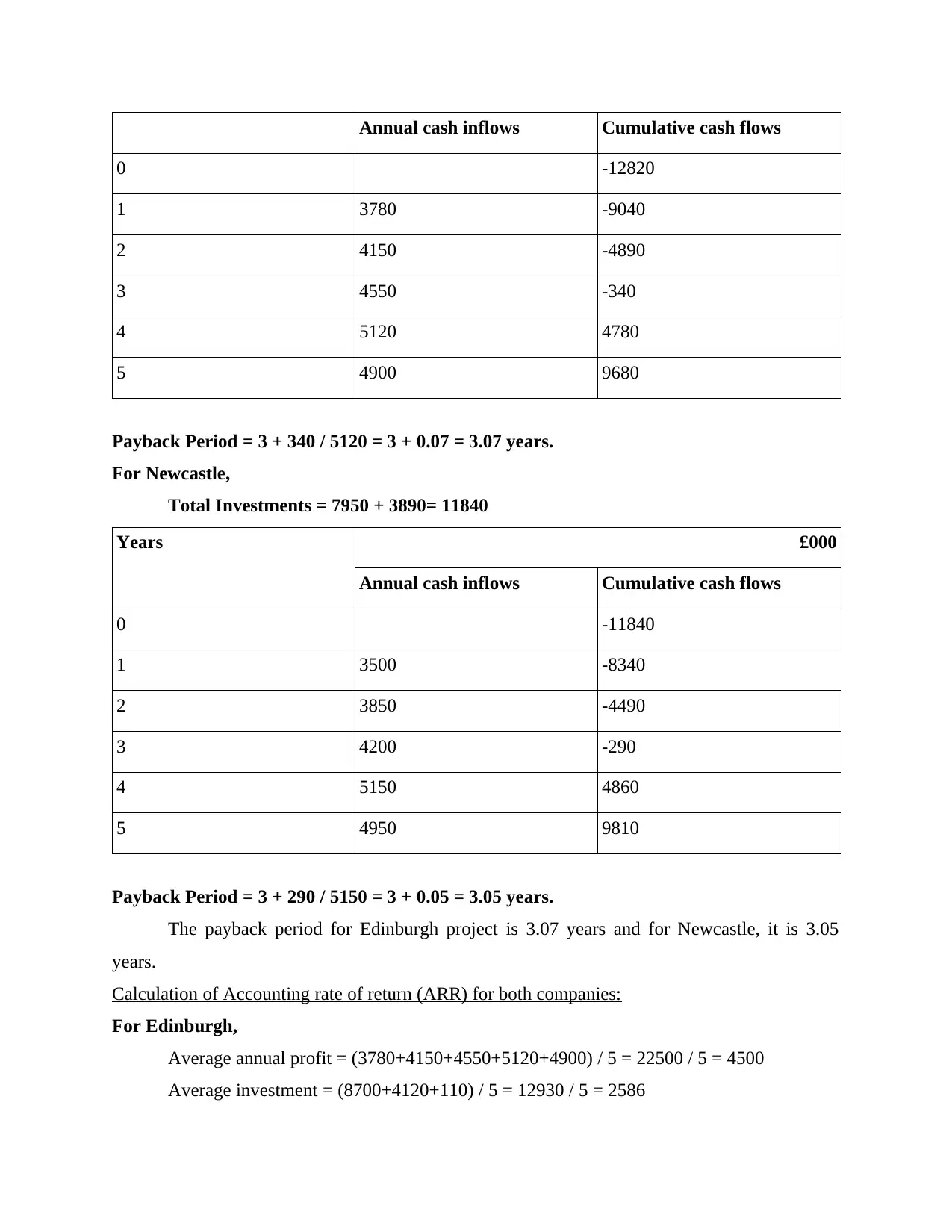

Annual cash inflows Cumulative cash flows

0 -12820

1 3780 -9040

2 4150 -4890

3 4550 -340

4 5120 4780

5 4900 9680

Payback Period = 3 + 340 / 5120 = 3 + 0.07 = 3.07 years.

For Newcastle,

Total Investments = 7950 + 3890= 11840

Years £000

Annual cash inflows Cumulative cash flows

0 -11840

1 3500 -8340

2 3850 -4490

3 4200 -290

4 5150 4860

5 4950 9810

Payback Period = 3 + 290 / 5150 = 3 + 0.05 = 3.05 years.

The payback period for Edinburgh project is 3.07 years and for Newcastle, it is 3.05

years.

Calculation of Accounting rate of return (ARR) for both companies:

For Edinburgh,

Average annual profit = (3780+4150+4550+5120+4900) / 5 = 22500 / 5 = 4500

Average investment = (8700+4120+110) / 5 = 12930 / 5 = 2586

0 -12820

1 3780 -9040

2 4150 -4890

3 4550 -340

4 5120 4780

5 4900 9680

Payback Period = 3 + 340 / 5120 = 3 + 0.07 = 3.07 years.

For Newcastle,

Total Investments = 7950 + 3890= 11840

Years £000

Annual cash inflows Cumulative cash flows

0 -11840

1 3500 -8340

2 3850 -4490

3 4200 -290

4 5150 4860

5 4950 9810

Payback Period = 3 + 290 / 5150 = 3 + 0.05 = 3.05 years.

The payback period for Edinburgh project is 3.07 years and for Newcastle, it is 3.05

years.

Calculation of Accounting rate of return (ARR) for both companies:

For Edinburgh,

Average annual profit = (3780+4150+4550+5120+4900) / 5 = 22500 / 5 = 4500

Average investment = (8700+4120+110) / 5 = 12930 / 5 = 2586

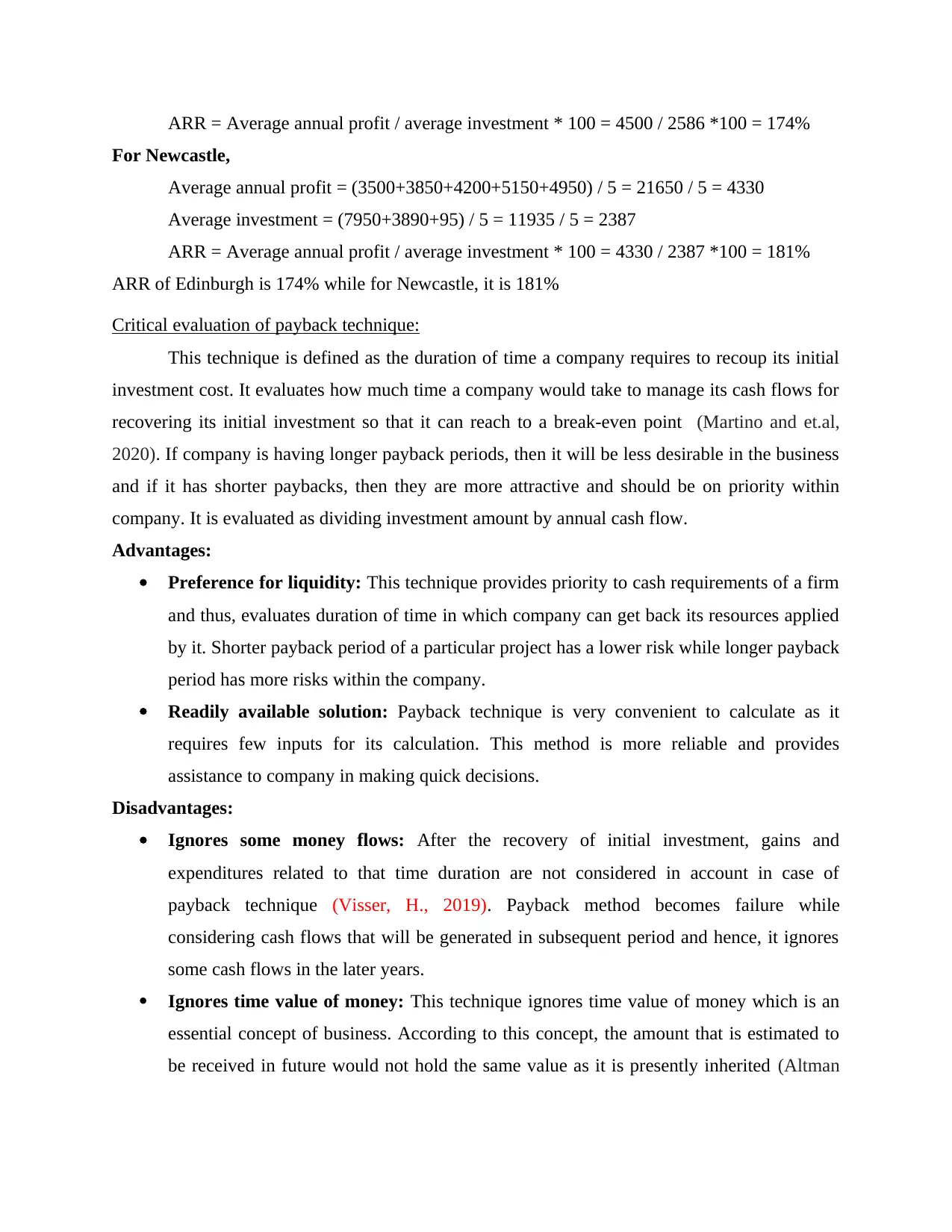

ARR = Average annual profit / average investment * 100 = 4500 / 2586 *100 = 174%

For Newcastle,

Average annual profit = (3500+3850+4200+5150+4950) / 5 = 21650 / 5 = 4330

Average investment = (7950+3890+95) / 5 = 11935 / 5 = 2387

ARR = Average annual profit / average investment * 100 = 4330 / 2387 *100 = 181%

ARR of Edinburgh is 174% while for Newcastle, it is 181%

Critical evaluation of payback technique:

This technique is defined as the duration of time a company requires to recoup its initial

investment cost. It evaluates how much time a company would take to manage its cash flows for

recovering its initial investment so that it can reach to a break-even point (Martino and et.al,

2020). If company is having longer payback periods, then it will be less desirable in the business

and if it has shorter paybacks, then they are more attractive and should be on priority within

company. It is evaluated as dividing investment amount by annual cash flow.

Advantages:

Preference for liquidity: This technique provides priority to cash requirements of a firm

and thus, evaluates duration of time in which company can get back its resources applied

by it. Shorter payback period of a particular project has a lower risk while longer payback

period has more risks within the company.

Readily available solution: Payback technique is very convenient to calculate as it

requires few inputs for its calculation. This method is more reliable and provides

assistance to company in making quick decisions.

Disadvantages:

Ignores some money flows: After the recovery of initial investment, gains and

expenditures related to that time duration are not considered in account in case of

payback technique (Visser, H., 2019). Payback method becomes failure while

considering cash flows that will be generated in subsequent period and hence, it ignores

some cash flows in the later years.

Ignores time value of money: This technique ignores time value of money which is an

essential concept of business. According to this concept, the amount that is estimated to

be received in future would not hold the same value as it is presently inherited (Altman

For Newcastle,

Average annual profit = (3500+3850+4200+5150+4950) / 5 = 21650 / 5 = 4330

Average investment = (7950+3890+95) / 5 = 11935 / 5 = 2387

ARR = Average annual profit / average investment * 100 = 4330 / 2387 *100 = 181%

ARR of Edinburgh is 174% while for Newcastle, it is 181%

Critical evaluation of payback technique:

This technique is defined as the duration of time a company requires to recoup its initial

investment cost. It evaluates how much time a company would take to manage its cash flows for

recovering its initial investment so that it can reach to a break-even point (Martino and et.al,

2020). If company is having longer payback periods, then it will be less desirable in the business

and if it has shorter paybacks, then they are more attractive and should be on priority within

company. It is evaluated as dividing investment amount by annual cash flow.

Advantages:

Preference for liquidity: This technique provides priority to cash requirements of a firm

and thus, evaluates duration of time in which company can get back its resources applied

by it. Shorter payback period of a particular project has a lower risk while longer payback

period has more risks within the company.

Readily available solution: Payback technique is very convenient to calculate as it

requires few inputs for its calculation. This method is more reliable and provides

assistance to company in making quick decisions.

Disadvantages:

Ignores some money flows: After the recovery of initial investment, gains and

expenditures related to that time duration are not considered in account in case of

payback technique (Visser, H., 2019). Payback method becomes failure while

considering cash flows that will be generated in subsequent period and hence, it ignores

some cash flows in the later years.

Ignores time value of money: This technique ignores time value of money which is an

essential concept of business. According to this concept, the amount that is estimated to

be received in future would not hold the same value as it is presently inherited (Altman

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and et.al, 2019). If a company looks only at a single factor, then there is a possibility of

missing the expected investments.

Payback technique is very convenient to apply as well as also facilitates the company in

formulating fast business decisions. However, there is a disadvantage of this method that it

cannot be used in separation of large projects. Discounted cash flow factor will necessarily

required to represent the influence of time on cash values. In this technique, conditions of

business environment that carries the capacity to make the environment of business dynamic are

not taken into account.

Characteristics of investment appraisal as well as advantages and disadvantages of IRR:

From Chang Ying's point of view, all decisions of investments carry some characteristics

with them and it is essential to understand those characteristics if their approach is correct

towards appraisal techniques.

Advice to Flyers plc's senior executive team:

Investment appraisal techniques are those techniques that are mainly meant for

performance appraisal of a new project (Boissay and et.al, 2021). It includes techniques such as

payback period, net present value, accounting rate of return, internal rate of return and

profitability index. These techniques helps the senior executives of Flyers plc in evaluation of a

project from different aspects and also helps them in checking its viability.

Characteristics of investment appraisal:

This technique provides assistance to firm in taking decision related to a project and its

profit. It helps business to know whether a project is profitable or not and also allow them to

calculate about part of profit required to recover the cost. This technique allow managers of

company to estimate the advantages of transactions with its whole life. It allow firms to know

real values of cash flow with implementation of discounting factor. Investment appraisal helps

company to represent position of business in future with interpreting potential job. With the help

of this technique, managers of company can plan improvements in its future operations.

According to Travis van Reimsdyk, IRR technique has both advantages and

disadvantages and it is very important to know them for making business decisions within the

company (Habib, A. and Hasan, M. M., 2019). Here are some of the strengths and weaknesses of

IRR that are described as under:

missing the expected investments.

Payback technique is very convenient to apply as well as also facilitates the company in

formulating fast business decisions. However, there is a disadvantage of this method that it

cannot be used in separation of large projects. Discounted cash flow factor will necessarily

required to represent the influence of time on cash values. In this technique, conditions of

business environment that carries the capacity to make the environment of business dynamic are

not taken into account.

Characteristics of investment appraisal as well as advantages and disadvantages of IRR:

From Chang Ying's point of view, all decisions of investments carry some characteristics

with them and it is essential to understand those characteristics if their approach is correct

towards appraisal techniques.

Advice to Flyers plc's senior executive team:

Investment appraisal techniques are those techniques that are mainly meant for

performance appraisal of a new project (Boissay and et.al, 2021). It includes techniques such as

payback period, net present value, accounting rate of return, internal rate of return and

profitability index. These techniques helps the senior executives of Flyers plc in evaluation of a

project from different aspects and also helps them in checking its viability.

Characteristics of investment appraisal:

This technique provides assistance to firm in taking decision related to a project and its

profit. It helps business to know whether a project is profitable or not and also allow them to

calculate about part of profit required to recover the cost. This technique allow managers of

company to estimate the advantages of transactions with its whole life. It allow firms to know

real values of cash flow with implementation of discounting factor. Investment appraisal helps

company to represent position of business in future with interpreting potential job. With the help

of this technique, managers of company can plan improvements in its future operations.

According to Travis van Reimsdyk, IRR technique has both advantages and

disadvantages and it is very important to know them for making business decisions within the

company (Habib, A. and Hasan, M. M., 2019). Here are some of the strengths and weaknesses of

IRR that are described as under:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IRR stands for internal rate of return used in estimation of profitability of prospective

investments. It is a discount rate which makes all cash flows' NPV zero in analysis of discounted

cash flow.

Advantage of IRR:

It is important for managers to understand advantage of internal rate of return before

application of this technique in specific projects. Some of advantage of this analysis is mentioned

below:

Find time value: It can be measured with calculation of interest rate at current values of

succeeding cash flow which is equal to capital investment. Benefits of it is that it allow to

consider timing of cash flow of upcoming years. So, all cash flow is providing equal weight with

use of time value of money.

Simple and easy to understand: It is one of simple method which can be calculated

easily. It allow an organisation to compare values of different project (Van Bortel and et.al,

2018). It provide quick review of capital project to business owner and allow them to identify

which project has more potential.

Hurdle rate not require: Hurdle rate of return in budget analysis refers to a rate at

which investors are ready to provide funds to a project. It can either a rough estimate or a

subjective figure. IRR does not needed hurdle rate as in this project can be selected by managers

if IRR exceed cost of capital.

Disadvantage of IRR:

Ignore size of project: This method of budget analysis ignore size of project while

comparing project. In this, cash flows are compared to the amount of capital outlay which is

generating those cash flows.

Ignore future cost: IRR ignore future cost of a project and only focus on cash generate

with capital injection (Çizakça, M., 2011). Due to this, managers of company are unable to

planning for future period of time and cannot able to made future forecast.

Ignore reinvestment rate: IRR helps business managers to calculate values of

succeeding future cash flow which allow them to made implicit assumption for those cash flows

that can be again invested at same rate.

investments. It is a discount rate which makes all cash flows' NPV zero in analysis of discounted

cash flow.

Advantage of IRR:

It is important for managers to understand advantage of internal rate of return before

application of this technique in specific projects. Some of advantage of this analysis is mentioned

below:

Find time value: It can be measured with calculation of interest rate at current values of

succeeding cash flow which is equal to capital investment. Benefits of it is that it allow to

consider timing of cash flow of upcoming years. So, all cash flow is providing equal weight with

use of time value of money.

Simple and easy to understand: It is one of simple method which can be calculated

easily. It allow an organisation to compare values of different project (Van Bortel and et.al,

2018). It provide quick review of capital project to business owner and allow them to identify

which project has more potential.

Hurdle rate not require: Hurdle rate of return in budget analysis refers to a rate at

which investors are ready to provide funds to a project. It can either a rough estimate or a

subjective figure. IRR does not needed hurdle rate as in this project can be selected by managers

if IRR exceed cost of capital.

Disadvantage of IRR:

Ignore size of project: This method of budget analysis ignore size of project while

comparing project. In this, cash flows are compared to the amount of capital outlay which is

generating those cash flows.

Ignore future cost: IRR ignore future cost of a project and only focus on cash generate

with capital injection (Çizakça, M., 2011). Due to this, managers of company are unable to

planning for future period of time and cannot able to made future forecast.

Ignore reinvestment rate: IRR helps business managers to calculate values of

succeeding future cash flow which allow them to made implicit assumption for those cash flows

that can be again invested at same rate.

TASK 3

Concept of contribution and its significance to CVP technique:

An amount which is left after deducting all variable costs from revenues of a business is

termed as contribution. This amount is used to make payments for any fixed costs incurred

within a business over a particular period of time (Lubin, D., 2018). When fixed costs are

deducted from contribution then the left amount is termed as profit of company. Contribution

facilitates a firm in assessing the entire impact of a unit on the business as different determinants

such as change in variable costs.

Uses of Contribution:

It helps in determining the break-even point of goods that assists firms in deciding the

smallest number of units that is required to be sold to recoup its entire expenditure.

Contribution provides assistance in ascertainment of lowest price which is required to be

charged for goods. It helps in understanding the strengths and weaknesses of product or

business and also facilitates in recovering the fixed and variable costs.

Cost volume profit (CVP) is a technique that helps in ascertaining effect of costs and

sales on profits of a firm (Emerson and et.al, 2019). This tool provides assistance to company in

determining the break-even point of different structure of costs and sales and helps

administrators of company in making business decisions within a short notice. CVP facilitates in

making various assumptions including that fixed and variable costs as well as selling price per

unit remains constant.

Importance of contribution to CVP technique:

Helps in evaluating impact of different costs on profits: By using this tool, impact of

all expenses on profits can be well determined through changes in values of these

benefits. This technique facilitates managers in taking corrective action for controlling

these type of costs to attain profitability level.

Provides assistance in knowing minimum required sales: It helps in determining

minimum units of sales to avoid risks or losses within the company. It also assists

administrators of company in formulating plans for expanding sales volume.

Concept of contribution and its significance to CVP technique:

An amount which is left after deducting all variable costs from revenues of a business is

termed as contribution. This amount is used to make payments for any fixed costs incurred

within a business over a particular period of time (Lubin, D., 2018). When fixed costs are

deducted from contribution then the left amount is termed as profit of company. Contribution

facilitates a firm in assessing the entire impact of a unit on the business as different determinants

such as change in variable costs.

Uses of Contribution:

It helps in determining the break-even point of goods that assists firms in deciding the

smallest number of units that is required to be sold to recoup its entire expenditure.

Contribution provides assistance in ascertainment of lowest price which is required to be

charged for goods. It helps in understanding the strengths and weaknesses of product or

business and also facilitates in recovering the fixed and variable costs.

Cost volume profit (CVP) is a technique that helps in ascertaining effect of costs and

sales on profits of a firm (Emerson and et.al, 2019). This tool provides assistance to company in

determining the break-even point of different structure of costs and sales and helps

administrators of company in making business decisions within a short notice. CVP facilitates in

making various assumptions including that fixed and variable costs as well as selling price per

unit remains constant.

Importance of contribution to CVP technique:

Helps in evaluating impact of different costs on profits: By using this tool, impact of

all expenses on profits can be well determined through changes in values of these

benefits. This technique facilitates managers in taking corrective action for controlling

these type of costs to attain profitability level.

Provides assistance in knowing minimum required sales: It helps in determining

minimum units of sales to avoid risks or losses within the company. It also assists

administrators of company in formulating plans for expanding sales volume.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Nature of 'dropping a product or service' and 'special contract' decisions for usefulness of CVP

technique:

Dropping a project refers to a choice of either not to undertake any specific transaction or

making a pause while continuing project. According to finance, it happens when product is not

having potentiality to generate profits or is not in demand of customers or could not recoup its

cost (Blackwell, T. and Kohl, S., 2018). To make such decisions, administration of a company

uses CVP technique to make process of selection simple.

While taking such decisions, an analysis of different costs is to be conducted by firm for

using CVP tool in this. It will help in dividing all expenses and evaluates its effect on

profitability as well as determines the units to be sold to recover the amount invested in it. If

actual sales are less as compared to budgeted sales then decision of dropping that product is

taken.

Special contracts are those type of deals that a firm has to decide whether to accept offer

made by different customers or not. These deals generally need some special processes

demanding low price. It helps in making projects beneficial in some aspects still demanding

analysis before acceptance of these contracts. By using CVP technique, expenses on each

production process can be determined (Morris, J. H., 2018). It facilitates in evaluating entire

profitability of particular contract and if profitability level is attained through those contracts

then decision of carrying on that contract is taken otherwise not.

Critical evaluation of CVP technique and its limitations:

CVP is a tool that determines influence of cost and sales on profit of company as well as

ascertains break-even point at different level of sales and cost. With the help of this tool,

managers of firm takes decisions in a very short period of time (Brusov and et.al, 2015). CVP is

having two different approaches, that are, accountant's and economic.

In accounting approach, cost function is considered as linear whereas in economic

approach, it is curvilinear. This is because accounting approach deals with small level of

work while economic approach operates on large level that may effect efficiency of

operations.

There are two break-even points in economic approach in which first level is of

recouping the losses to gains while another moves towards dropping of demand of

technique:

Dropping a project refers to a choice of either not to undertake any specific transaction or

making a pause while continuing project. According to finance, it happens when product is not

having potentiality to generate profits or is not in demand of customers or could not recoup its

cost (Blackwell, T. and Kohl, S., 2018). To make such decisions, administration of a company

uses CVP technique to make process of selection simple.

While taking such decisions, an analysis of different costs is to be conducted by firm for

using CVP tool in this. It will help in dividing all expenses and evaluates its effect on

profitability as well as determines the units to be sold to recover the amount invested in it. If

actual sales are less as compared to budgeted sales then decision of dropping that product is

taken.

Special contracts are those type of deals that a firm has to decide whether to accept offer

made by different customers or not. These deals generally need some special processes

demanding low price. It helps in making projects beneficial in some aspects still demanding

analysis before acceptance of these contracts. By using CVP technique, expenses on each

production process can be determined (Morris, J. H., 2018). It facilitates in evaluating entire

profitability of particular contract and if profitability level is attained through those contracts

then decision of carrying on that contract is taken otherwise not.

Critical evaluation of CVP technique and its limitations:

CVP is a tool that determines influence of cost and sales on profit of company as well as

ascertains break-even point at different level of sales and cost. With the help of this tool,

managers of firm takes decisions in a very short period of time (Brusov and et.al, 2015). CVP is

having two different approaches, that are, accountant's and economic.

In accounting approach, cost function is considered as linear whereas in economic

approach, it is curvilinear. This is because accounting approach deals with small level of

work while economic approach operates on large level that may effect efficiency of

operations.

There are two break-even points in economic approach in which first level is of

recouping the losses to gains while another moves towards dropping of demand of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

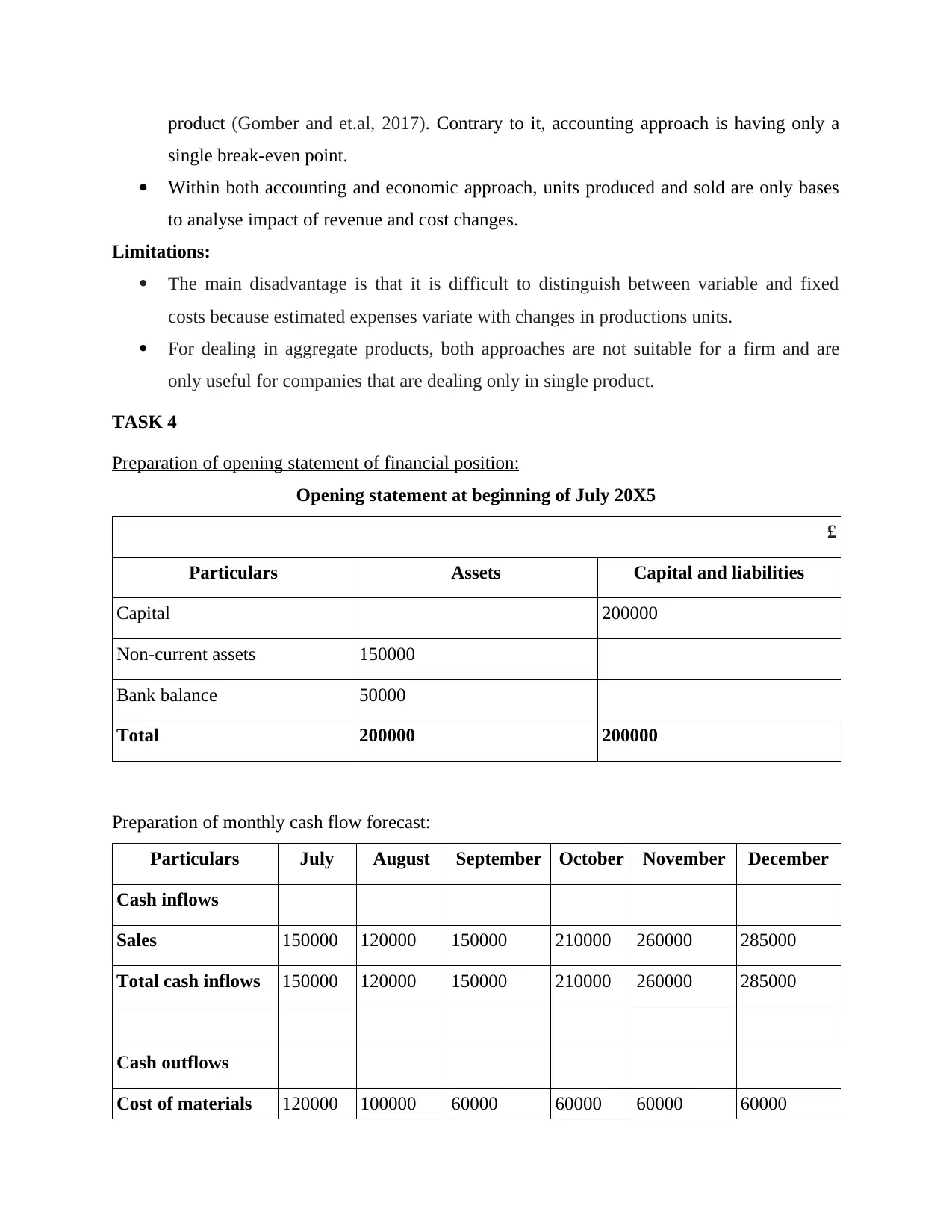

product (Gomber and et.al, 2017). Contrary to it, accounting approach is having only a

single break-even point.

Within both accounting and economic approach, units produced and sold are only bases

to analyse impact of revenue and cost changes.

Limitations:

The main disadvantage is that it is difficult to distinguish between variable and fixed

costs because estimated expenses variate with changes in productions units.

For dealing in aggregate products, both approaches are not suitable for a firm and are

only useful for companies that are dealing only in single product.

TASK 4

Preparation of opening statement of financial position:

Opening statement at beginning of July 20X5

£

Particulars Assets Capital and liabilities

Capital 200000

Non-current assets 150000

Bank balance 50000

Total 200000 200000

Preparation of monthly cash flow forecast:

Particulars July August September October November December

Cash inflows

Sales 150000 120000 150000 210000 260000 285000

Total cash inflows 150000 120000 150000 210000 260000 285000

Cash outflows

Cost of materials 120000 100000 60000 60000 60000 60000

single break-even point.

Within both accounting and economic approach, units produced and sold are only bases

to analyse impact of revenue and cost changes.

Limitations:

The main disadvantage is that it is difficult to distinguish between variable and fixed

costs because estimated expenses variate with changes in productions units.

For dealing in aggregate products, both approaches are not suitable for a firm and are

only useful for companies that are dealing only in single product.

TASK 4

Preparation of opening statement of financial position:

Opening statement at beginning of July 20X5

£

Particulars Assets Capital and liabilities

Capital 200000

Non-current assets 150000

Bank balance 50000

Total 200000 200000

Preparation of monthly cash flow forecast:

Particulars July August September October November December

Cash inflows

Sales 150000 120000 150000 210000 260000 285000

Total cash inflows 150000 120000 150000 210000 260000 285000

Cash outflows

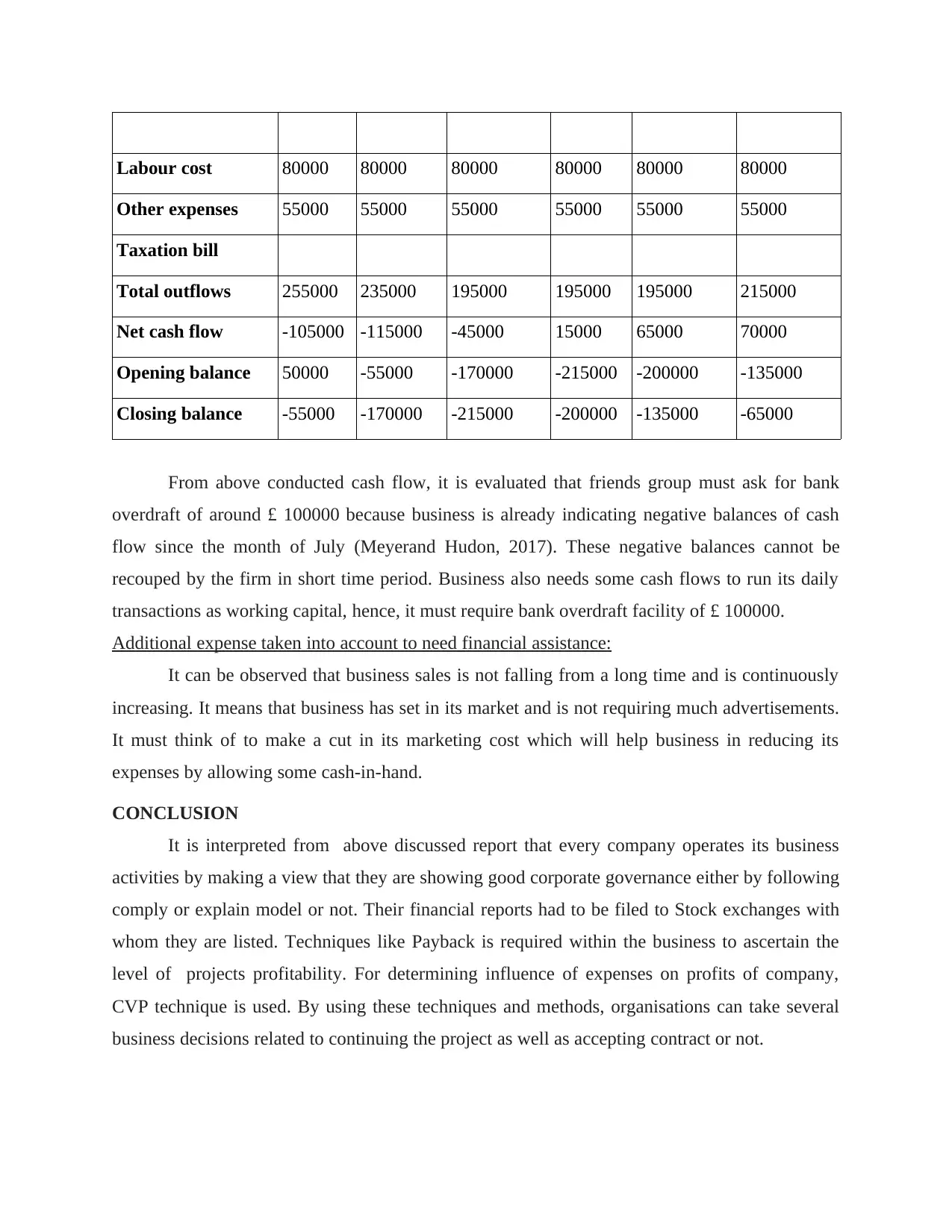

Cost of materials 120000 100000 60000 60000 60000 60000

Labour cost 80000 80000 80000 80000 80000 80000

Other expenses 55000 55000 55000 55000 55000 55000

Taxation bill

Total outflows 255000 235000 195000 195000 195000 215000

Net cash flow -105000 -115000 -45000 15000 65000 70000

Opening balance 50000 -55000 -170000 -215000 -200000 -135000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

From above conducted cash flow, it is evaluated that friends group must ask for bank

overdraft of around £ 100000 because business is already indicating negative balances of cash

flow since the month of July (Meyerand Hudon, 2017). These negative balances cannot be

recouped by the firm in short time period. Business also needs some cash flows to run its daily

transactions as working capital, hence, it must require bank overdraft facility of £ 100000.

Additional expense taken into account to need financial assistance:

It can be observed that business sales is not falling from a long time and is continuously

increasing. It means that business has set in its market and is not requiring much advertisements.

It must think of to make a cut in its marketing cost which will help business in reducing its

expenses by allowing some cash-in-hand.

CONCLUSION

It is interpreted from above discussed report that every company operates its business

activities by making a view that they are showing good corporate governance either by following

comply or explain model or not. Their financial reports had to be filed to Stock exchanges with

whom they are listed. Techniques like Payback is required within the business to ascertain the

level of projects profitability. For determining influence of expenses on profits of company,

CVP technique is used. By using these techniques and methods, organisations can take several

business decisions related to continuing the project as well as accepting contract or not.

Other expenses 55000 55000 55000 55000 55000 55000

Taxation bill

Total outflows 255000 235000 195000 195000 195000 215000

Net cash flow -105000 -115000 -45000 15000 65000 70000

Opening balance 50000 -55000 -170000 -215000 -200000 -135000

Closing balance -55000 -170000 -215000 -200000 -135000 -65000

From above conducted cash flow, it is evaluated that friends group must ask for bank

overdraft of around £ 100000 because business is already indicating negative balances of cash

flow since the month of July (Meyerand Hudon, 2017). These negative balances cannot be

recouped by the firm in short time period. Business also needs some cash flows to run its daily

transactions as working capital, hence, it must require bank overdraft facility of £ 100000.

Additional expense taken into account to need financial assistance:

It can be observed that business sales is not falling from a long time and is continuously

increasing. It means that business has set in its market and is not requiring much advertisements.

It must think of to make a cut in its marketing cost which will help business in reducing its

expenses by allowing some cash-in-hand.

CONCLUSION

It is interpreted from above discussed report that every company operates its business

activities by making a view that they are showing good corporate governance either by following

comply or explain model or not. Their financial reports had to be filed to Stock exchanges with

whom they are listed. Techniques like Payback is required within the business to ascertain the

level of projects profitability. For determining influence of expenses on profits of company,

CVP technique is used. By using these techniques and methods, organisations can take several

business decisions related to continuing the project as well as accepting contract or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.