Sports Limited Financial Analysis Report: Finance CW2 Assignment

VerifiedAdded on 2023/04/21

|14

|3775

|200

Report

AI Summary

This report provides a comprehensive financial analysis of Sports Limited, evaluating its future prospects and financial viability. It utilizes investment appraisal techniques, including Net Present Value (NPV), to assess the profitability of potential projects like the Capital Suite and Capital Platform software. The report also conducts capital budgeting, cash flow analysis, and break-even analysis to assess the financial performance of a new shop over a three-month period. Sources of finance, such as bank loans, preference shares, and asset securitization, are explored to support the company's expansion. The analysis includes detailed financial data, cash flow statements, and budget projections, offering insights into the minimum sales required for break-even and the overall financial health of Sports Limited. The report concludes with recommendations for investment strategies and capital allocation, emphasizing the importance of financial planning for sustainable growth.

Running head: FINANCE

Finance-CW2

Name of the Student:

Name of the University:

Authors Note:

Finance-CW2

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

1

Executive Summary:

Investment appraisal techniques are been used in the assessment to identify the

financial viability of the future prospects that is presented to the organisation. In

addition, adequate capital budgeting, cash flows analysis and breakeven analysis

has also been conducted for analysing the performance of the company for the

tenure of 3 months. The capital budgeting has directly indicated a positive cash flow

for the new shop of the organization. The break-even analysis and the cash flow

created for the new shop as indicated a positive attributes of the new opportunity,

which can increase profitability of the organization. The break has stated the

minimum amount of revenues or units that needs to be produced by the new shop

for achieving no profit no loss. However, the cash flow analysis indicators and

negative closing cash balance for the new shop.

1

Executive Summary:

Investment appraisal techniques are been used in the assessment to identify the

financial viability of the future prospects that is presented to the organisation. In

addition, adequate capital budgeting, cash flows analysis and breakeven analysis

has also been conducted for analysing the performance of the company for the

tenure of 3 months. The capital budgeting has directly indicated a positive cash flow

for the new shop of the organization. The break-even analysis and the cash flow

created for the new shop as indicated a positive attributes of the new opportunity,

which can increase profitability of the organization. The break has stated the

minimum amount of revenues or units that needs to be produced by the new shop

for achieving no profit no loss. However, the cash flow analysis indicators and

negative closing cash balance for the new shop.

FINANCE

2

Table of Contents

Introduction:..................................................................................................................3

Literature review to support the accounting models used:...........................................3

Sources of Finance:......................................................................................................4

Investment Appraisal technique:..................................................................................5

Capital Budgeting:........................................................................................................7

Breakeven analysis:......................................................................................................8

Evaluation:..................................................................................................................10

Conclusion and recommendation:..............................................................................10

Reference and Bibliography:......................................................................................12

2

Table of Contents

Introduction:..................................................................................................................3

Literature review to support the accounting models used:...........................................3

Sources of Finance:......................................................................................................4

Investment Appraisal technique:..................................................................................5

Capital Budgeting:........................................................................................................7

Breakeven analysis:......................................................................................................8

Evaluation:..................................................................................................................10

Conclusion and recommendation:..............................................................................10

Reference and Bibliography:......................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

3

Introduction:

The assessment aims in evaluating the future prospects that is presented to

Sports Limited. Investment appraisal techniques are been used in the assessment to

identify the financial viability of the future prospects that is presented to the

organisation. In addition, adequate capital budgeting, cash flows analysis and

breakeven analysis has also been conducted for analysing the performance of the

company for the tenure of 3 months. Moreover, adequate evaluation is mainly

conducted for identifying the accurate level of income that can be generated from an

investment. The accounting models and the source of finance that can be used by

the organisation is mainly identified in the assessment.

Literature review to support the accounting models used:

There are different accounting models used for analysing the proposed

projects presented to Sports Limited. The investment appraisal technique Net

present value is mainly used for analysing the projects that is presented to the

company. In addition, the net present value provides adequate information regarding

the future incomes by scrutinising the cash flow under time value of money. This

measure can eventually help in selecting the project, which can provide the highest

level of income from investment in the long run. Caglayan and Demir (2014)

mentioned that investment appraisal techniques allow the management to select the

most appropriate investments, which can boost their sales in the long run.

Moreover, the other accounting models used in the analysis are cash flows

statement, budget and breakeven analysis. The budget is used for preparing the 3-

month projected income of the new shop, which can help ion detecting the income

that can be generated from the investment. On the other hand, the breakeven

analysis is conducted to determine the level of minimum sales that is required by the

new shop for obtaining no profit no loss scenario. This breakeven analysis helps in

understanding the minimum level of sales that needs to be conducted by the

company to continue its operations without hindering the invested capital. Lastly, the

cash flow statement has provided adequate information regarding the cash position

of the organisation during the three-month period.

3

Introduction:

The assessment aims in evaluating the future prospects that is presented to

Sports Limited. Investment appraisal techniques are been used in the assessment to

identify the financial viability of the future prospects that is presented to the

organisation. In addition, adequate capital budgeting, cash flows analysis and

breakeven analysis has also been conducted for analysing the performance of the

company for the tenure of 3 months. Moreover, adequate evaluation is mainly

conducted for identifying the accurate level of income that can be generated from an

investment. The accounting models and the source of finance that can be used by

the organisation is mainly identified in the assessment.

Literature review to support the accounting models used:

There are different accounting models used for analysing the proposed

projects presented to Sports Limited. The investment appraisal technique Net

present value is mainly used for analysing the projects that is presented to the

company. In addition, the net present value provides adequate information regarding

the future incomes by scrutinising the cash flow under time value of money. This

measure can eventually help in selecting the project, which can provide the highest

level of income from investment in the long run. Caglayan and Demir (2014)

mentioned that investment appraisal techniques allow the management to select the

most appropriate investments, which can boost their sales in the long run.

Moreover, the other accounting models used in the analysis are cash flows

statement, budget and breakeven analysis. The budget is used for preparing the 3-

month projected income of the new shop, which can help ion detecting the income

that can be generated from the investment. On the other hand, the breakeven

analysis is conducted to determine the level of minimum sales that is required by the

new shop for obtaining no profit no loss scenario. This breakeven analysis helps in

understanding the minimum level of sales that needs to be conducted by the

company to continue its operations without hindering the invested capital. Lastly, the

cash flow statement has provided adequate information regarding the cash position

of the organisation during the three-month period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

4

Sources of Finance:

There are specific sources of finance that can be used by the Sports Limited

organisation for complementing the planned expansion program. The organisation

has been successfully operating for the past 10 years, while making adequate profits

from the operations. From the relevant evaluation, it can be detected that the

organisation can access different sources of finance for supporting its financial

expansion, while accommodating the level of operations, which can increase its

performance in the long run. Khan (2015) mentioned that available source of the

finance is considered to be a blessing for the organisation during cash crunch or

expansion, as it provides the management adequate liberty to make appropriate

decision to fulfil their financial goals. There are specific sources of finance that is

available for Sports Limited, which are depicted as follows.

Bank Loan:

Bank loan is one of the best and quickest sources of finance that is available

to Sports Limited, as loan from banks can be provided for initial year with low interest

rate. Moreover, bank loans have certain limitations and advantages for the

organisation, who is interested in selecting the source of finance. Bank loan is

considered to be one of the quickest forms of finance that can be used by the

organisation for supporting it cash crunch. However, the increment in bank loan can

raise the level of interest payments, which can negatively affect the actual profits of

the organisation (Carbo‐Valverde et al. 2016).

Preference Shares:

The second-best option for Sports Limited is the issue of preference shares,

as it can allows the management to acquire the adequate level of capital for

supporting its operations. The major advantage of Preference shares is the security

it provides to investors, which allow the company to acquire the capital quickly from

investors. However, the preference shares reduce the retained income of the

organisation, as constant payments need to be conducted to the investors.

Asset Securitization:

The third finance source that is available to Sports Limited is asset

securitizations, as it allows the management to get the required money quickly after

4

Sources of Finance:

There are specific sources of finance that can be used by the Sports Limited

organisation for complementing the planned expansion program. The organisation

has been successfully operating for the past 10 years, while making adequate profits

from the operations. From the relevant evaluation, it can be detected that the

organisation can access different sources of finance for supporting its financial

expansion, while accommodating the level of operations, which can increase its

performance in the long run. Khan (2015) mentioned that available source of the

finance is considered to be a blessing for the organisation during cash crunch or

expansion, as it provides the management adequate liberty to make appropriate

decision to fulfil their financial goals. There are specific sources of finance that is

available for Sports Limited, which are depicted as follows.

Bank Loan:

Bank loan is one of the best and quickest sources of finance that is available

to Sports Limited, as loan from banks can be provided for initial year with low interest

rate. Moreover, bank loans have certain limitations and advantages for the

organisation, who is interested in selecting the source of finance. Bank loan is

considered to be one of the quickest forms of finance that can be used by the

organisation for supporting it cash crunch. However, the increment in bank loan can

raise the level of interest payments, which can negatively affect the actual profits of

the organisation (Carbo‐Valverde et al. 2016).

Preference Shares:

The second-best option for Sports Limited is the issue of preference shares,

as it can allows the management to acquire the adequate level of capital for

supporting its operations. The major advantage of Preference shares is the security

it provides to investors, which allow the company to acquire the capital quickly from

investors. However, the preference shares reduce the retained income of the

organisation, as constant payments need to be conducted to the investors.

Asset Securitization:

The third finance source that is available to Sports Limited is asset

securitizations, as it allows the management to get the required money quickly after

FINANCE

5

providing assets as mortgage to the loan. Mortgage based loan is considered to

have low level of interest due to the security provided to the loan provider. However,

there is major limitation to the asset securitization method, as the company might

lose the asset If adequate repayments and interest is not been provided to the

lender. This is a major risk, which might hinder the progress and continuity of the

company (Peirson et al. 2014).

Investment Appraisal technique:

Year 0 1 2 3 4 5

New software cost 8,800,000£

Working capital 900,000£ 618,000£ 824,000£ 309,000£ 721,000£

Change in WC 282,000£ 206,000-£ 515,000£ 412,000-£ 721,000£

Sales revenue 3,300,000£ 6,592,000£ 7,931,000£ 8,961,000£ 9,991,000£

Less

Module 1 432,600-£ 618,000-£ 824,000-£ 927,000-£ 1,133,000-£

Module 2 1,040,300-£ 1,442,000-£ 1,648,000-£ 2,163,000-£ 1,957,000-£

Overhead 236,900-£ 247,200-£ 339,900-£ 309,000-£ 309,000-£

Hours 1,300£ 1,274£ 1,249£ 1,224£ 1,199£

Per hour 130£ 134£ 138£ 142£ 146£

TE 1 169,000-£ 170,589-£ 172,192-£ 173,811-£ 175,445-£

Hours 1,300£ 1,261£ 1,223£ 1,186£ 1,151£

Per hour 115£ 118£ 122£ 126£ 129£

TE 2 149,500-£ 149,365-£ 149,231-£ 149,097-£ 148,963-£

Total cash flow 9,700,000-£ 1,553,700£ 3,758,846£ 5,312,677£ 4,827,093£ 6,988,593£

NPV 5,962,222

Capital Suite

The above figure provides relevant information regarding the Capital Suite

software that is proposed to Sports Limited. From the evaluation, it is mainly

detected that the after calculating the initial investment with the cash inflows and

outflows the relevant financial viability of the project is mainly detected. In addition,

the investment appraisal technique has indicated that the project will provide a total

return of £5,962,222 from an investment of only £9,700,000. On the other hand,

Harris (2017) mentioned that economic value added has been used when life of the

two mutually exclusive projects are not similar, as it helps in detecting the most

beneficial project for the organisation.

5

providing assets as mortgage to the loan. Mortgage based loan is considered to

have low level of interest due to the security provided to the loan provider. However,

there is major limitation to the asset securitization method, as the company might

lose the asset If adequate repayments and interest is not been provided to the

lender. This is a major risk, which might hinder the progress and continuity of the

company (Peirson et al. 2014).

Investment Appraisal technique:

Year 0 1 2 3 4 5

New software cost 8,800,000£

Working capital 900,000£ 618,000£ 824,000£ 309,000£ 721,000£

Change in WC 282,000£ 206,000-£ 515,000£ 412,000-£ 721,000£

Sales revenue 3,300,000£ 6,592,000£ 7,931,000£ 8,961,000£ 9,991,000£

Less

Module 1 432,600-£ 618,000-£ 824,000-£ 927,000-£ 1,133,000-£

Module 2 1,040,300-£ 1,442,000-£ 1,648,000-£ 2,163,000-£ 1,957,000-£

Overhead 236,900-£ 247,200-£ 339,900-£ 309,000-£ 309,000-£

Hours 1,300£ 1,274£ 1,249£ 1,224£ 1,199£

Per hour 130£ 134£ 138£ 142£ 146£

TE 1 169,000-£ 170,589-£ 172,192-£ 173,811-£ 175,445-£

Hours 1,300£ 1,261£ 1,223£ 1,186£ 1,151£

Per hour 115£ 118£ 122£ 126£ 129£

TE 2 149,500-£ 149,365-£ 149,231-£ 149,097-£ 148,963-£

Total cash flow 9,700,000-£ 1,553,700£ 3,758,846£ 5,312,677£ 4,827,093£ 6,988,593£

NPV 5,962,222

Capital Suite

The above figure provides relevant information regarding the Capital Suite

software that is proposed to Sports Limited. From the evaluation, it is mainly

detected that the after calculating the initial investment with the cash inflows and

outflows the relevant financial viability of the project is mainly detected. In addition,

the investment appraisal technique has indicated that the project will provide a total

return of £5,962,222 from an investment of only £9,700,000. On the other hand,

Harris (2017) mentioned that economic value added has been used when life of the

two mutually exclusive projects are not similar, as it helps in detecting the most

beneficial project for the organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

6

Year 0 1 2 3 4 5

New software cost 8,600,000£

Working capital 500,000£ 672,590£ 830,180£ 987,770£ 1,145,360£

Change in WC 172,590-£ 157,590-£ 157,590-£ 157,590-£ 1,145,360£

Sales revenue 5,650,000£ 6,983,400£ 9,311,200£ 11,057,050£ 11,639,000£

Less

Module 1 351,230-£ 544,870-£ 834,300-£ 1,084,590-£ 1,484,230-£

Module 2 1,359,600-£ 1,931,250-£ 2,317,500-£ 2,804,690-£ 3,033,350-£

Overhead 191,580-£ 233,810-£ 278,100-£ 325,480-£ 370,800-£

Hours 1,300£ 1,274£ 1,249£ 1,224£ 1,199£

Per hour 130£ 134£ 138£ 142£ 146£

TE 1 169,000-£ 170,589-£ 172,192-£ 173,811-£ 175,445-£

Hours 1,300£ 1,261£ 1,223£ 1,186£ 1,151£

Per hour 115£ 118£ 122£ 126£ 129£

TE 2 149,500-£ 149,365-£ 149,231-£ 149,097-£ 148,963-£

Total cash flow 9,100,000-£ 3,256,500£ 3,795,926£ 5,402,287£ 6,361,793£ 7,571,573£

NPV 9,548,818

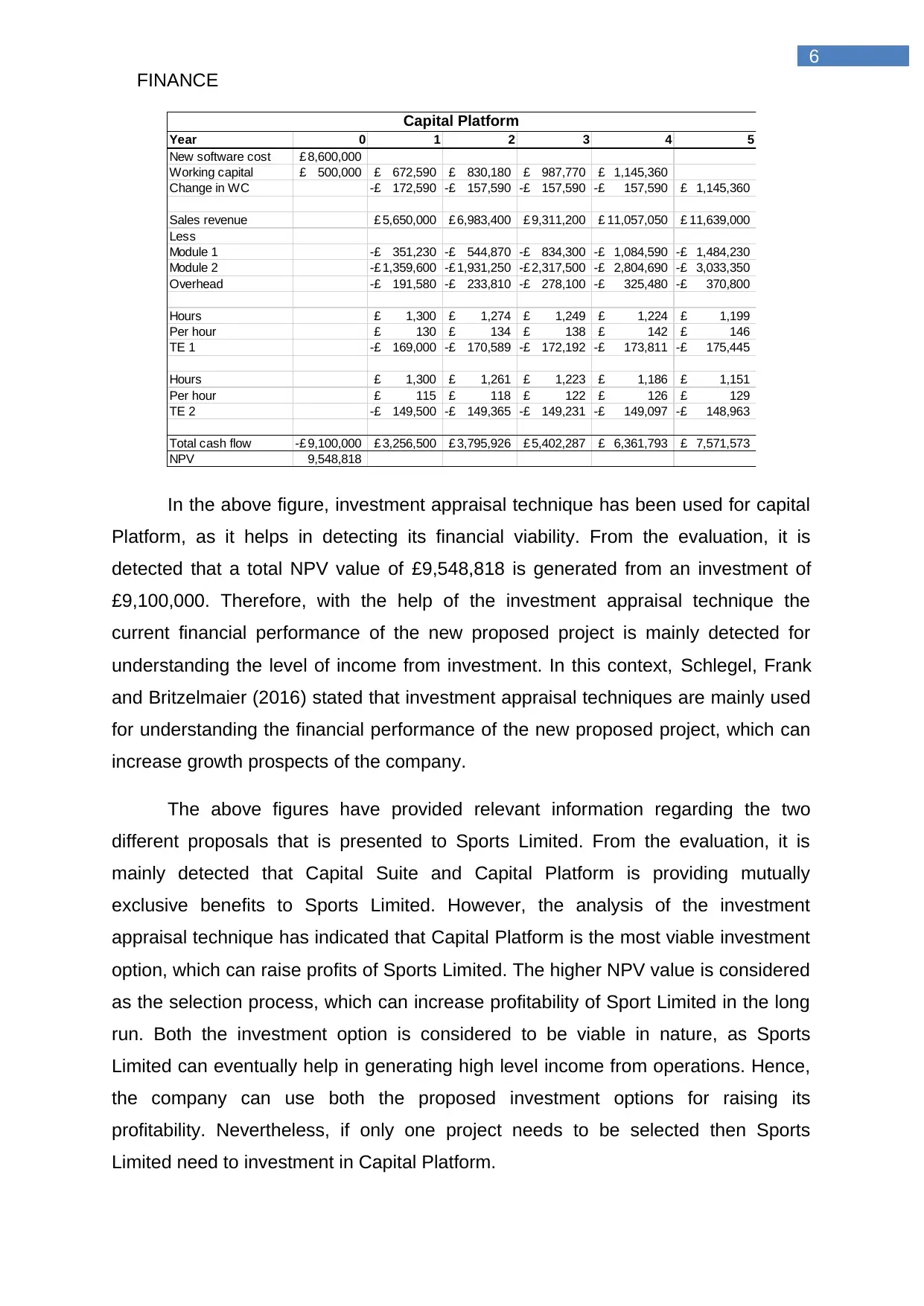

Capital Platform

In the above figure, investment appraisal technique has been used for capital

Platform, as it helps in detecting its financial viability. From the evaluation, it is

detected that a total NPV value of £9,548,818 is generated from an investment of

£9,100,000. Therefore, with the help of the investment appraisal technique the

current financial performance of the new proposed project is mainly detected for

understanding the level of income from investment. In this context, Schlegel, Frank

and Britzelmaier (2016) stated that investment appraisal techniques are mainly used

for understanding the financial performance of the new proposed project, which can

increase growth prospects of the company.

The above figures have provided relevant information regarding the two

different proposals that is presented to Sports Limited. From the evaluation, it is

mainly detected that Capital Suite and Capital Platform is providing mutually

exclusive benefits to Sports Limited. However, the analysis of the investment

appraisal technique has indicated that Capital Platform is the most viable investment

option, which can raise profits of Sports Limited. The higher NPV value is considered

as the selection process, which can increase profitability of Sport Limited in the long

run. Both the investment option is considered to be viable in nature, as Sports

Limited can eventually help in generating high level income from operations. Hence,

the company can use both the proposed investment options for raising its

profitability. Nevertheless, if only one project needs to be selected then Sports

Limited need to investment in Capital Platform.

6

Year 0 1 2 3 4 5

New software cost 8,600,000£

Working capital 500,000£ 672,590£ 830,180£ 987,770£ 1,145,360£

Change in WC 172,590-£ 157,590-£ 157,590-£ 157,590-£ 1,145,360£

Sales revenue 5,650,000£ 6,983,400£ 9,311,200£ 11,057,050£ 11,639,000£

Less

Module 1 351,230-£ 544,870-£ 834,300-£ 1,084,590-£ 1,484,230-£

Module 2 1,359,600-£ 1,931,250-£ 2,317,500-£ 2,804,690-£ 3,033,350-£

Overhead 191,580-£ 233,810-£ 278,100-£ 325,480-£ 370,800-£

Hours 1,300£ 1,274£ 1,249£ 1,224£ 1,199£

Per hour 130£ 134£ 138£ 142£ 146£

TE 1 169,000-£ 170,589-£ 172,192-£ 173,811-£ 175,445-£

Hours 1,300£ 1,261£ 1,223£ 1,186£ 1,151£

Per hour 115£ 118£ 122£ 126£ 129£

TE 2 149,500-£ 149,365-£ 149,231-£ 149,097-£ 148,963-£

Total cash flow 9,100,000-£ 3,256,500£ 3,795,926£ 5,402,287£ 6,361,793£ 7,571,573£

NPV 9,548,818

Capital Platform

In the above figure, investment appraisal technique has been used for capital

Platform, as it helps in detecting its financial viability. From the evaluation, it is

detected that a total NPV value of £9,548,818 is generated from an investment of

£9,100,000. Therefore, with the help of the investment appraisal technique the

current financial performance of the new proposed project is mainly detected for

understanding the level of income from investment. In this context, Schlegel, Frank

and Britzelmaier (2016) stated that investment appraisal techniques are mainly used

for understanding the financial performance of the new proposed project, which can

increase growth prospects of the company.

The above figures have provided relevant information regarding the two

different proposals that is presented to Sports Limited. From the evaluation, it is

mainly detected that Capital Suite and Capital Platform is providing mutually

exclusive benefits to Sports Limited. However, the analysis of the investment

appraisal technique has indicated that Capital Platform is the most viable investment

option, which can raise profits of Sports Limited. The higher NPV value is considered

as the selection process, which can increase profitability of Sport Limited in the long

run. Both the investment option is considered to be viable in nature, as Sports

Limited can eventually help in generating high level income from operations. Hence,

the company can use both the proposed investment options for raising its

profitability. Nevertheless, if only one project needs to be selected then Sports

Limited need to investment in Capital Platform.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

7

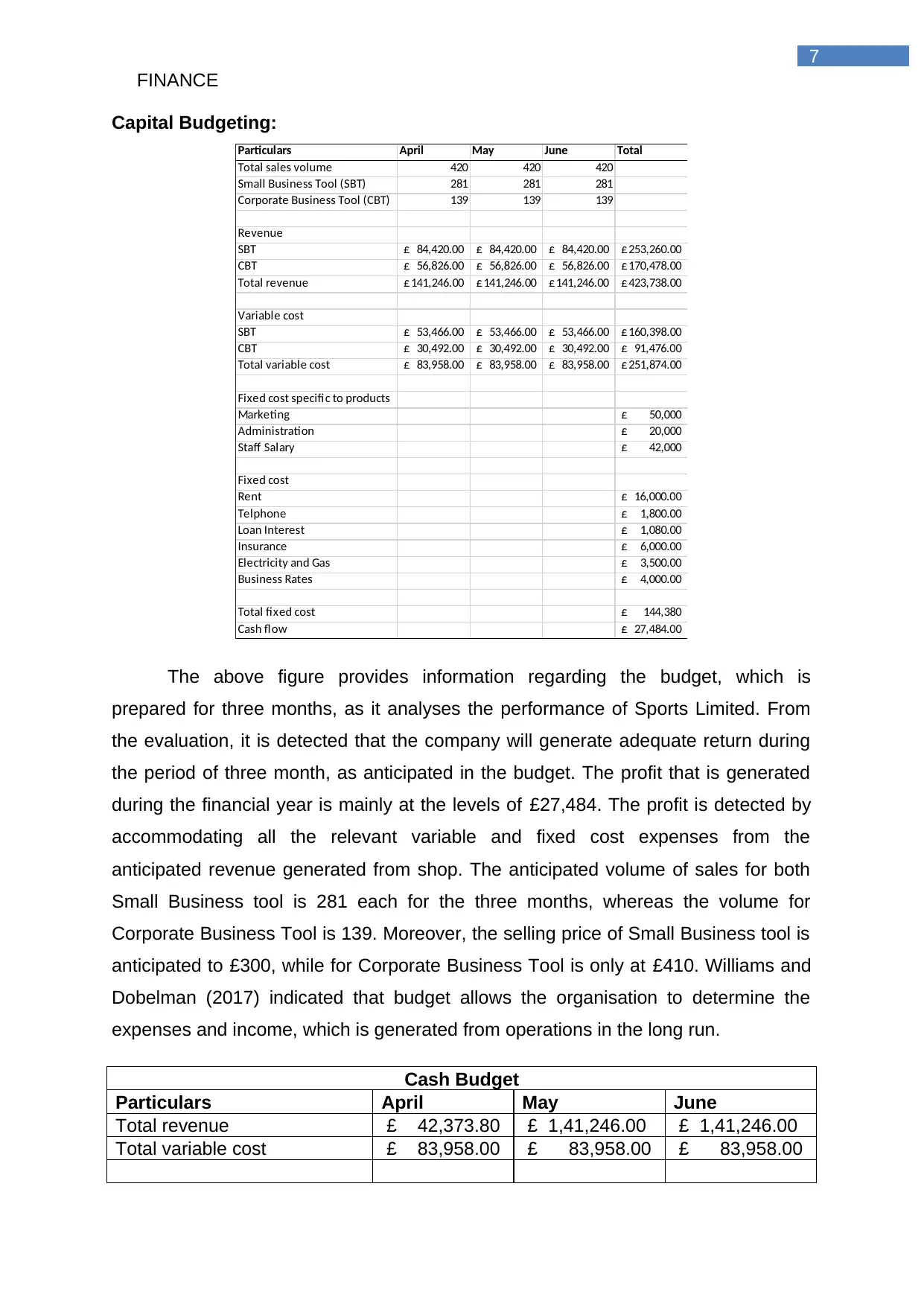

Capital Budgeting:

Particulars April May June Total

Total sales volume 420 420 420

Small Business Tool (SBT) 281 281 281

Corporate Business Tool (CBT) 139 139 139

Revenue

SBT 84,420.00£ 84,420.00£ 84,420.00£ 253,260.00£

CBT 56,826.00£ 56,826.00£ 56,826.00£ 170,478.00£

Total revenue 141,246.00£ 141,246.00£ 141,246.00£ 423,738.00£

Variable cost

SBT 53,466.00£ 53,466.00£ 53,466.00£ 160,398.00£

CBT 30,492.00£ 30,492.00£ 30,492.00£ 91,476.00£

Total variable cost 83,958.00£ 83,958.00£ 83,958.00£ 251,874.00£

Fixed cost specific to products

Marketing 50,000£

Administration 20,000£

Staff Salary 42,000£

Fixed cost

Rent 16,000.00£

Telphone 1,800.00£

Loan Interest 1,080.00£

Insurance 6,000.00£

Electricity and Gas 3,500.00£

Business Rates 4,000.00£

Total fixed cost 144,380£

Cash flow 27,484.00£

The above figure provides information regarding the budget, which is

prepared for three months, as it analyses the performance of Sports Limited. From

the evaluation, it is detected that the company will generate adequate return during

the period of three month, as anticipated in the budget. The profit that is generated

during the financial year is mainly at the levels of £27,484. The profit is detected by

accommodating all the relevant variable and fixed cost expenses from the

anticipated revenue generated from shop. The anticipated volume of sales for both

Small Business tool is 281 each for the three months, whereas the volume for

Corporate Business Tool is 139. Moreover, the selling price of Small Business tool is

anticipated to £300, while for Corporate Business Tool is only at £410. Williams and

Dobelman (2017) indicated that budget allows the organisation to determine the

expenses and income, which is generated from operations in the long run.

Cash Budget

Particulars April May June

Total revenue £ 42,373.80 £ 1,41,246.00 £ 1,41,246.00

Total variable cost £ 83,958.00 £ 83,958.00 £ 83,958.00

7

Capital Budgeting:

Particulars April May June Total

Total sales volume 420 420 420

Small Business Tool (SBT) 281 281 281

Corporate Business Tool (CBT) 139 139 139

Revenue

SBT 84,420.00£ 84,420.00£ 84,420.00£ 253,260.00£

CBT 56,826.00£ 56,826.00£ 56,826.00£ 170,478.00£

Total revenue 141,246.00£ 141,246.00£ 141,246.00£ 423,738.00£

Variable cost

SBT 53,466.00£ 53,466.00£ 53,466.00£ 160,398.00£

CBT 30,492.00£ 30,492.00£ 30,492.00£ 91,476.00£

Total variable cost 83,958.00£ 83,958.00£ 83,958.00£ 251,874.00£

Fixed cost specific to products

Marketing 50,000£

Administration 20,000£

Staff Salary 42,000£

Fixed cost

Rent 16,000.00£

Telphone 1,800.00£

Loan Interest 1,080.00£

Insurance 6,000.00£

Electricity and Gas 3,500.00£

Business Rates 4,000.00£

Total fixed cost 144,380£

Cash flow 27,484.00£

The above figure provides information regarding the budget, which is

prepared for three months, as it analyses the performance of Sports Limited. From

the evaluation, it is detected that the company will generate adequate return during

the period of three month, as anticipated in the budget. The profit that is generated

during the financial year is mainly at the levels of £27,484. The profit is detected by

accommodating all the relevant variable and fixed cost expenses from the

anticipated revenue generated from shop. The anticipated volume of sales for both

Small Business tool is 281 each for the three months, whereas the volume for

Corporate Business Tool is 139. Moreover, the selling price of Small Business tool is

anticipated to £300, while for Corporate Business Tool is only at £410. Williams and

Dobelman (2017) indicated that budget allows the organisation to determine the

expenses and income, which is generated from operations in the long run.

Cash Budget

Particulars April May June

Total revenue £ 42,373.80 £ 1,41,246.00 £ 1,41,246.00

Total variable cost £ 83,958.00 £ 83,958.00 £ 83,958.00

FINANCE

8

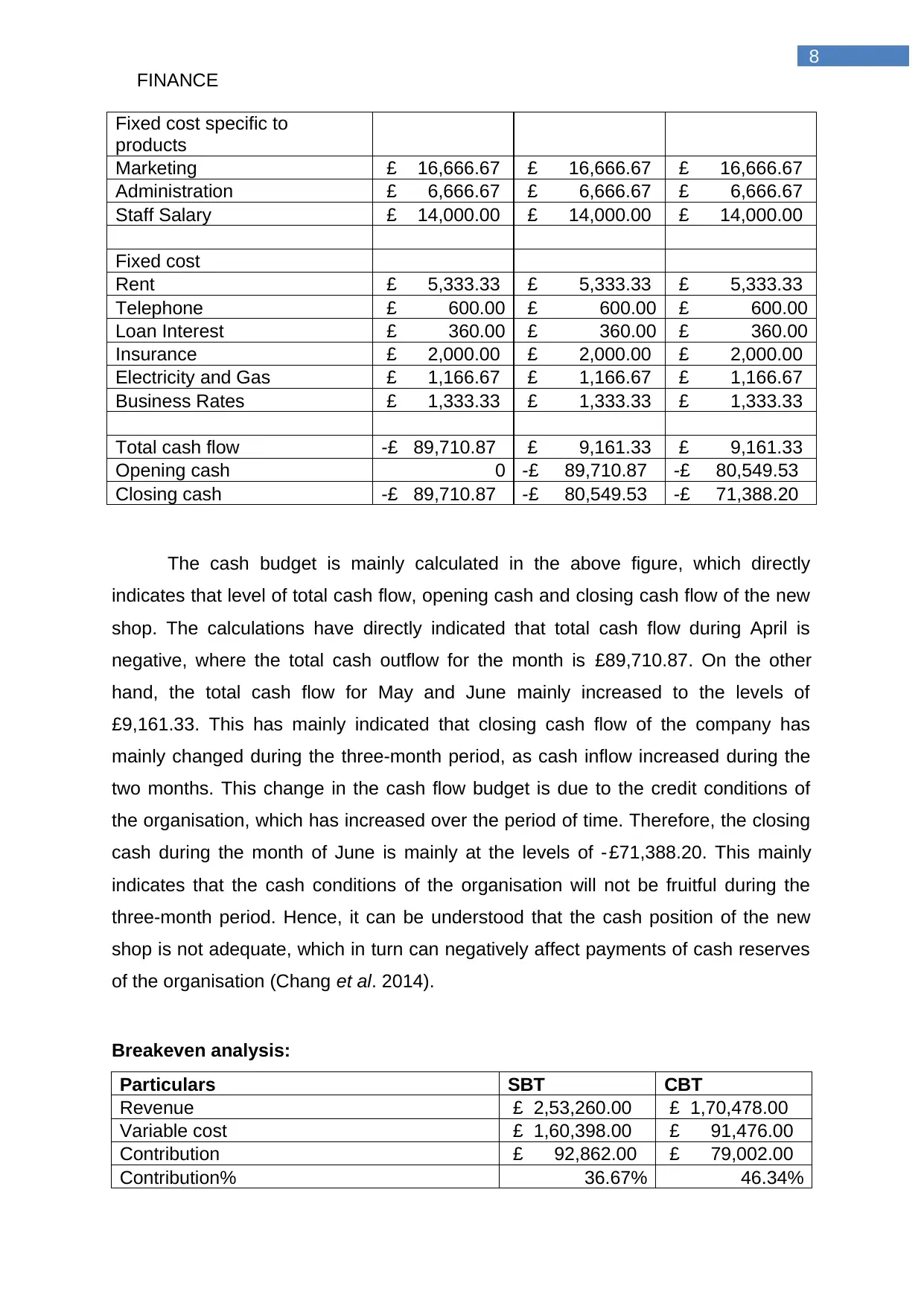

Fixed cost specific to

products

Marketing £ 16,666.67 £ 16,666.67 £ 16,666.67

Administration £ 6,666.67 £ 6,666.67 £ 6,666.67

Staff Salary £ 14,000.00 £ 14,000.00 £ 14,000.00

Fixed cost

Rent £ 5,333.33 £ 5,333.33 £ 5,333.33

Telephone £ 600.00 £ 600.00 £ 600.00

Loan Interest £ 360.00 £ 360.00 £ 360.00

Insurance £ 2,000.00 £ 2,000.00 £ 2,000.00

Electricity and Gas £ 1,166.67 £ 1,166.67 £ 1,166.67

Business Rates £ 1,333.33 £ 1,333.33 £ 1,333.33

Total cash flow -£ 89,710.87 £ 9,161.33 £ 9,161.33

Opening cash 0 -£ 89,710.87 -£ 80,549.53

Closing cash -£ 89,710.87 -£ 80,549.53 -£ 71,388.20

The cash budget is mainly calculated in the above figure, which directly

indicates that level of total cash flow, opening cash and closing cash flow of the new

shop. The calculations have directly indicated that total cash flow during April is

negative, where the total cash outflow for the month is £89,710.87. On the other

hand, the total cash flow for May and June mainly increased to the levels of

£9,161.33. This has mainly indicated that closing cash flow of the company has

mainly changed during the three-month period, as cash inflow increased during the

two months. This change in the cash flow budget is due to the credit conditions of

the organisation, which has increased over the period of time. Therefore, the closing

cash during the month of June is mainly at the levels of -£71,388.20. This mainly

indicates that the cash conditions of the organisation will not be fruitful during the

three-month period. Hence, it can be understood that the cash position of the new

shop is not adequate, which in turn can negatively affect payments of cash reserves

of the organisation (Chang et al. 2014).

Breakeven analysis:

Particulars SBT CBT

Revenue £ 2,53,260.00 £ 1,70,478.00

Variable cost £ 1,60,398.00 £ 91,476.00

Contribution £ 92,862.00 £ 79,002.00

Contribution% 36.67% 46.34%

8

Fixed cost specific to

products

Marketing £ 16,666.67 £ 16,666.67 £ 16,666.67

Administration £ 6,666.67 £ 6,666.67 £ 6,666.67

Staff Salary £ 14,000.00 £ 14,000.00 £ 14,000.00

Fixed cost

Rent £ 5,333.33 £ 5,333.33 £ 5,333.33

Telephone £ 600.00 £ 600.00 £ 600.00

Loan Interest £ 360.00 £ 360.00 £ 360.00

Insurance £ 2,000.00 £ 2,000.00 £ 2,000.00

Electricity and Gas £ 1,166.67 £ 1,166.67 £ 1,166.67

Business Rates £ 1,333.33 £ 1,333.33 £ 1,333.33

Total cash flow -£ 89,710.87 £ 9,161.33 £ 9,161.33

Opening cash 0 -£ 89,710.87 -£ 80,549.53

Closing cash -£ 89,710.87 -£ 80,549.53 -£ 71,388.20

The cash budget is mainly calculated in the above figure, which directly

indicates that level of total cash flow, opening cash and closing cash flow of the new

shop. The calculations have directly indicated that total cash flow during April is

negative, where the total cash outflow for the month is £89,710.87. On the other

hand, the total cash flow for May and June mainly increased to the levels of

£9,161.33. This has mainly indicated that closing cash flow of the company has

mainly changed during the three-month period, as cash inflow increased during the

two months. This change in the cash flow budget is due to the credit conditions of

the organisation, which has increased over the period of time. Therefore, the closing

cash during the month of June is mainly at the levels of -£71,388.20. This mainly

indicates that the cash conditions of the organisation will not be fruitful during the

three-month period. Hence, it can be understood that the cash position of the new

shop is not adequate, which in turn can negatively affect payments of cash reserves

of the organisation (Chang et al. 2014).

Breakeven analysis:

Particulars SBT CBT

Revenue £ 2,53,260.00 £ 1,70,478.00

Variable cost £ 1,60,398.00 £ 91,476.00

Contribution £ 92,862.00 £ 79,002.00

Contribution% 36.67% 46.34%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

9

Fixed cost specific to products

Marketing £ 24,000 £ 26,000

Administration £ 8,000 £ 12,000

Staff Salary £ 18,000 £ 24,000

Fixed cost

Rent £ 8,000.00 £ 8,000.00

Telephone £ 900.00 £ 900.00

Loan Interest £ 540.00 £ 540.00

Insurance £ 3,000.00 £ 3,000.00

Electricity and Gas £ 1,750.00 £ 1,750.00

Business Rates £ 2,000.00 £ 2,000.00

Total Fixed cost £ 66,190 £ 78,190

Breakeven sales required £ 1,80,518.18 £ 1,68,725.79

Breakeven sales units required 602 412

Breakeven sales units required per

month 201 137

The above calculation provides an in-depth analysis of the breakeven sales

and sales per unit that is required by the organisation for maintaining no profit no

loss conditions. This analysis is conducted for providing adequate information to

Sports Limited regarding the minimum number of revenue or sales that needs to be

conducted in the new shop. From the analysis, it can be detected that the breakeven

sales required for Small Business Tool is mainly at the levels of £180,518.18 for the

period of three months. Hence, total revenue that needs to be generated by Small

Business Tool for three-month period. Further evaluation has indicated that

Corporate Business Tool requires a sales amount of £168,725.79 for achieving no

profit no loss. There is a separate calculation conducted for both Small Business

Tool and Corporate Business Tool, which can help in deciding the minimum amount

of revenue that needs to be generated by the new shop for achieving no profit and

no loss (Morano and Tajani 2017).

The calculation also provides information regarding the sales unit that is

required by Small Business Tool and Corporate Business Tool to achieve

sustainability in business during the financial year. From the evaluation, it has also

indicated that minimum of 602 units needs to be sold in three months for Small

Business Tool, where at least 201 unit sale in required per month. Moreover, the

calculation for Corporate Business Tool indicates that minimum total sales of 137

needs to be conducted for achieving no profit no loss. Hence, the breakeven

9

Fixed cost specific to products

Marketing £ 24,000 £ 26,000

Administration £ 8,000 £ 12,000

Staff Salary £ 18,000 £ 24,000

Fixed cost

Rent £ 8,000.00 £ 8,000.00

Telephone £ 900.00 £ 900.00

Loan Interest £ 540.00 £ 540.00

Insurance £ 3,000.00 £ 3,000.00

Electricity and Gas £ 1,750.00 £ 1,750.00

Business Rates £ 2,000.00 £ 2,000.00

Total Fixed cost £ 66,190 £ 78,190

Breakeven sales required £ 1,80,518.18 £ 1,68,725.79

Breakeven sales units required 602 412

Breakeven sales units required per

month 201 137

The above calculation provides an in-depth analysis of the breakeven sales

and sales per unit that is required by the organisation for maintaining no profit no

loss conditions. This analysis is conducted for providing adequate information to

Sports Limited regarding the minimum number of revenue or sales that needs to be

conducted in the new shop. From the analysis, it can be detected that the breakeven

sales required for Small Business Tool is mainly at the levels of £180,518.18 for the

period of three months. Hence, total revenue that needs to be generated by Small

Business Tool for three-month period. Further evaluation has indicated that

Corporate Business Tool requires a sales amount of £168,725.79 for achieving no

profit no loss. There is a separate calculation conducted for both Small Business

Tool and Corporate Business Tool, which can help in deciding the minimum amount

of revenue that needs to be generated by the new shop for achieving no profit and

no loss (Morano and Tajani 2017).

The calculation also provides information regarding the sales unit that is

required by Small Business Tool and Corporate Business Tool to achieve

sustainability in business during the financial year. From the evaluation, it has also

indicated that minimum of 602 units needs to be sold in three months for Small

Business Tool, where at least 201 unit sale in required per month. Moreover, the

calculation for Corporate Business Tool indicates that minimum total sales of 137

needs to be conducted for achieving no profit no loss. Hence, the breakeven

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

10

analysis indicated volumes and sales that need to be achieved for the new shop for

successfully operating without any kind of loss. Lee et al. (2018) mentioned that

analysis of breakeven units and sales value allows the organisation to conduct

marketing strategies that can increase profits from operations.

Evaluation:

After evaluating the cash budget and break even analysis the organization

can select the proposal for a new shop, as it would eventually help in generating high

level of income for the management. In addition, the break-even analysis would

provide relevant information regarding the measures that needs to be taken by the

management to survive the competitive environment and increasing profitability in

the long run. Moreover, from the investment proposal the Capital Platform needs to

be selected by the organization for increasing the profitability from its operations.

Conclusion and recommendation:

The assessment has adequately evaluated all the relevant options that was

presented to sports Limited for increasing its performance in the long run. the

adequate analysis of the available sources of finance for sports limited has been

identified which can be used by the management to support its future acquisition and

projects. The analysis has also been conducted on investment appraisal project

where capital platform Selected to be the most effective investment option for the

organization. This selected option for sports Limited would eventually help the

organization to increase its revenue in the long run as the NPV value is higher in

comparison to other project. Furthermore, the capital budgeting has directly

indicated a positive cash flow for the new shop of the organization. The break-even

analysis and the cash flow created for the new shop as indicated a positive attributes

of the new opportunity, which can increase profitability of the organization. The break

has stated the minimum amount of revenues or units that needs to be produced by

the new shop for achieving no profit no loss. However, the cash flow analysis

indicators and negative closing cash balance for the new shop.

10

analysis indicated volumes and sales that need to be achieved for the new shop for

successfully operating without any kind of loss. Lee et al. (2018) mentioned that

analysis of breakeven units and sales value allows the organisation to conduct

marketing strategies that can increase profits from operations.

Evaluation:

After evaluating the cash budget and break even analysis the organization

can select the proposal for a new shop, as it would eventually help in generating high

level of income for the management. In addition, the break-even analysis would

provide relevant information regarding the measures that needs to be taken by the

management to survive the competitive environment and increasing profitability in

the long run. Moreover, from the investment proposal the Capital Platform needs to

be selected by the organization for increasing the profitability from its operations.

Conclusion and recommendation:

The assessment has adequately evaluated all the relevant options that was

presented to sports Limited for increasing its performance in the long run. the

adequate analysis of the available sources of finance for sports limited has been

identified which can be used by the management to support its future acquisition and

projects. The analysis has also been conducted on investment appraisal project

where capital platform Selected to be the most effective investment option for the

organization. This selected option for sports Limited would eventually help the

organization to increase its revenue in the long run as the NPV value is higher in

comparison to other project. Furthermore, the capital budgeting has directly

indicated a positive cash flow for the new shop of the organization. The break-even

analysis and the cash flow created for the new shop as indicated a positive attributes

of the new opportunity, which can increase profitability of the organization. The break

has stated the minimum amount of revenues or units that needs to be produced by

the new shop for achieving no profit no loss. However, the cash flow analysis

indicators and negative closing cash balance for the new shop.

FINANCE

11

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.