FINM036 - DBS Bank: Financial Performance and Analysis Report

VerifiedAdded on 2023/04/25

|39

|6458

|102

Report

AI Summary

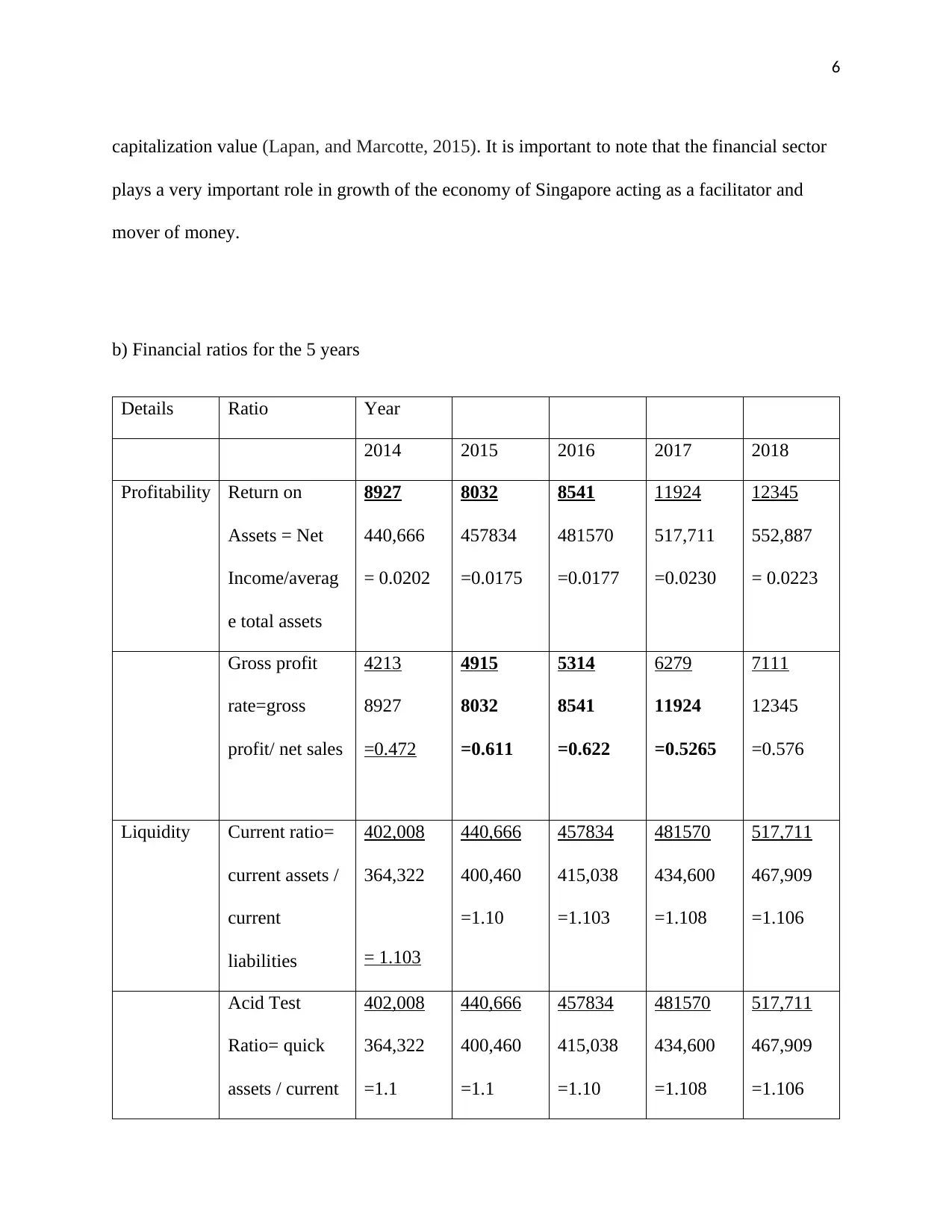

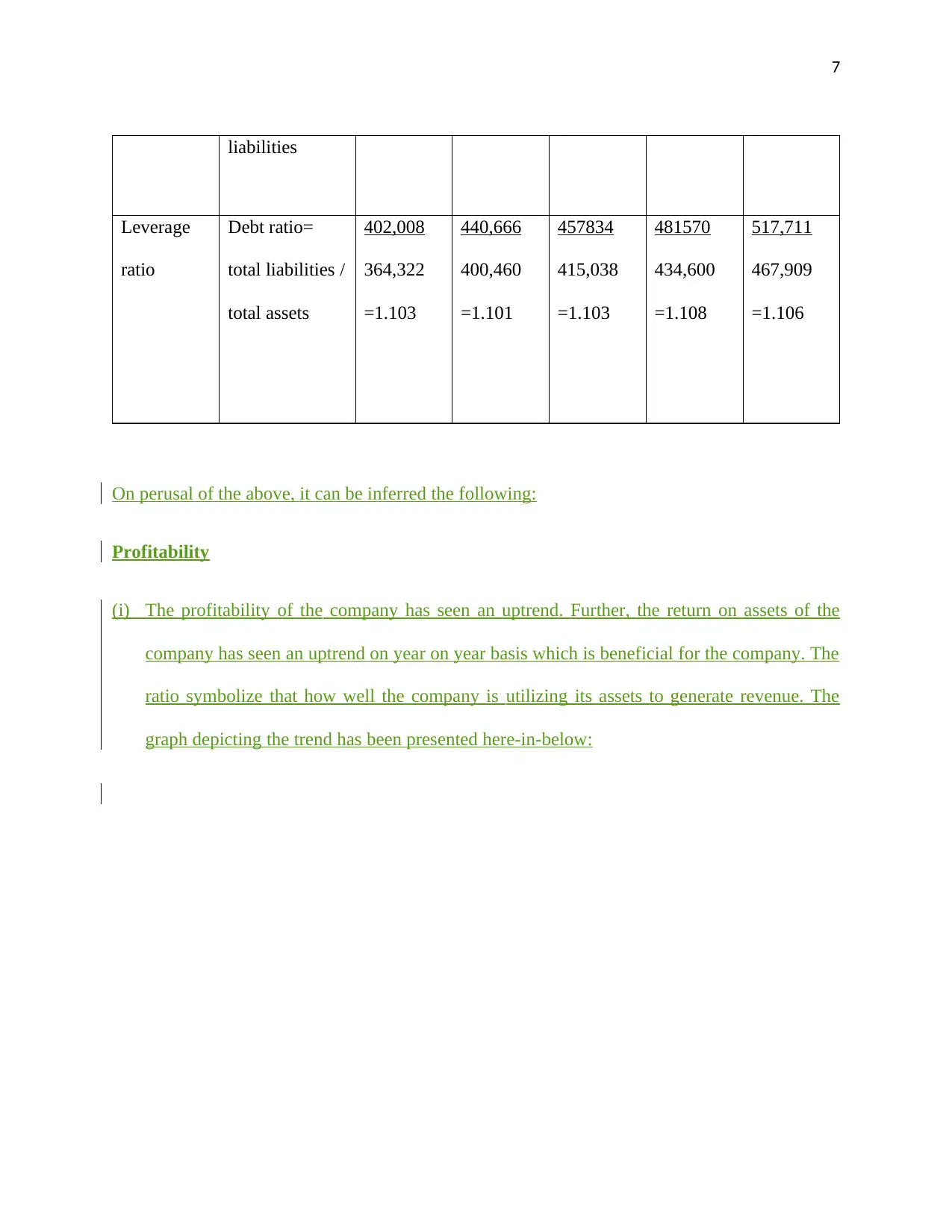

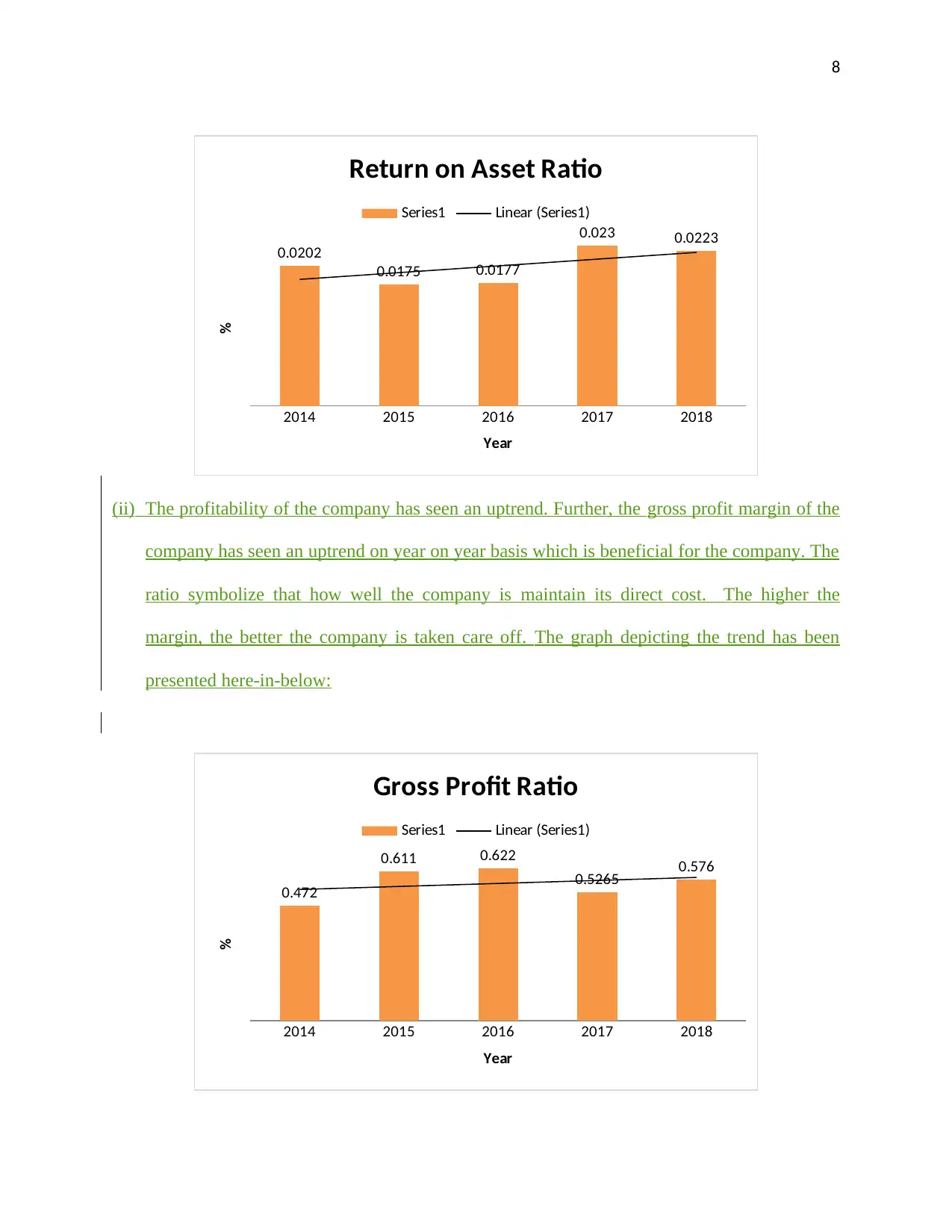

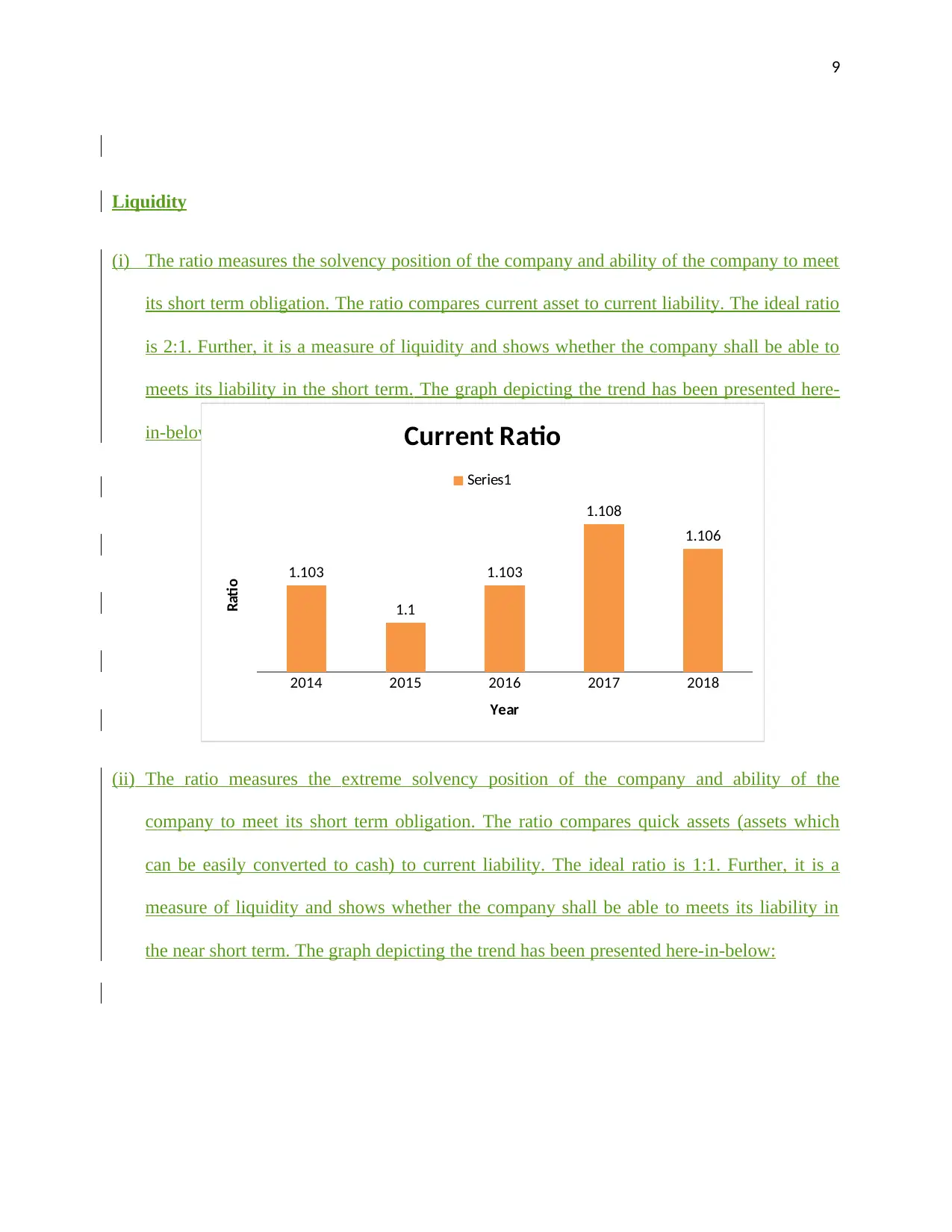

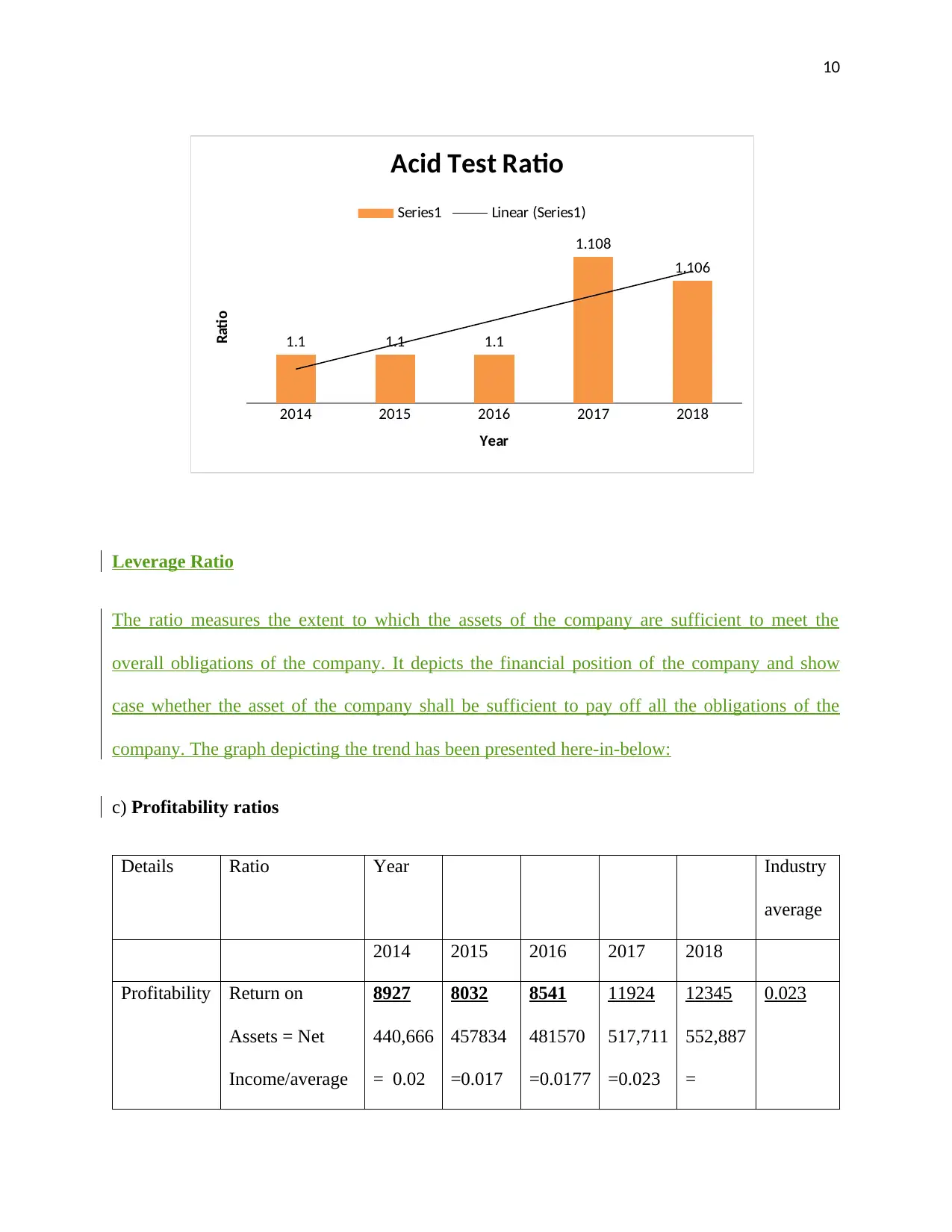

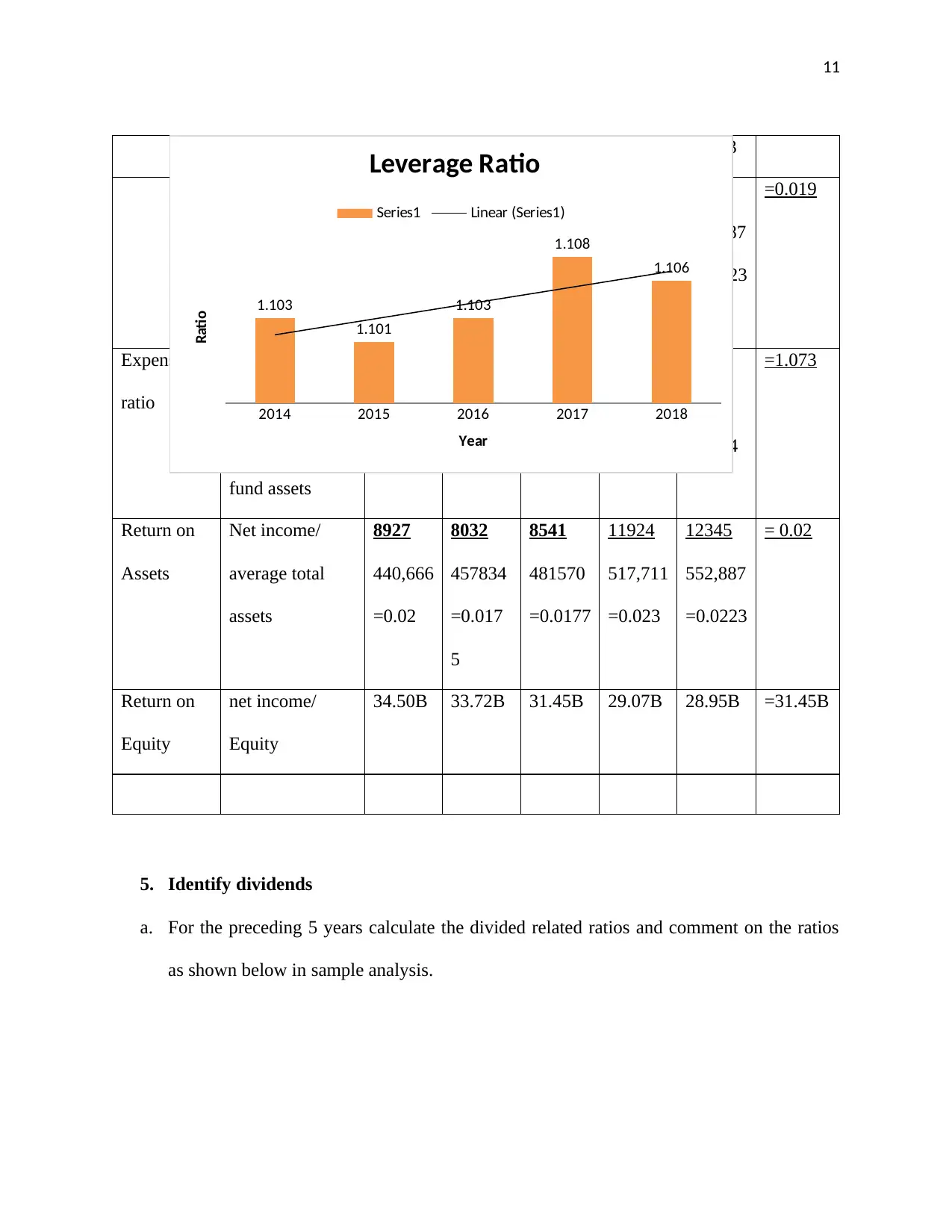

This report provides a thorough financial analysis of DBS Group Holdings Ltd. (DBS Bank), a prominent financial services provider in Singapore. The analysis encompasses horizontal and vertical analysis of the company's profit and loss statements and balance sheets from 2014 to 2018, identifying key trends in interest income, expenses, and net profits. The report examines the economic conditions of the financial sector in Singapore and calculates various financial ratios, including profitability, liquidity, and leverage ratios, to assess DBS Bank's performance. Furthermore, it delves into dividend-related ratios, such as dividend yield and payout ratios, providing insights into the company's dividend policies. The report also includes comments on the company's financial health, including profitability and liquidity, and compares certain ratios to industry averages, offering a comprehensive overview of DBS Bank's financial standing and performance over the specified period. The report is prepared for the board of directors as part of an interview process to assess the candidate's knowledge and understanding of key accounting and corporate finance concepts.

1 out of 39

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.