University Financial Analysis Report: Dreamboat Accountants, 2017

VerifiedAdded on 2020/05/28

|8

|1247

|204

Report

AI Summary

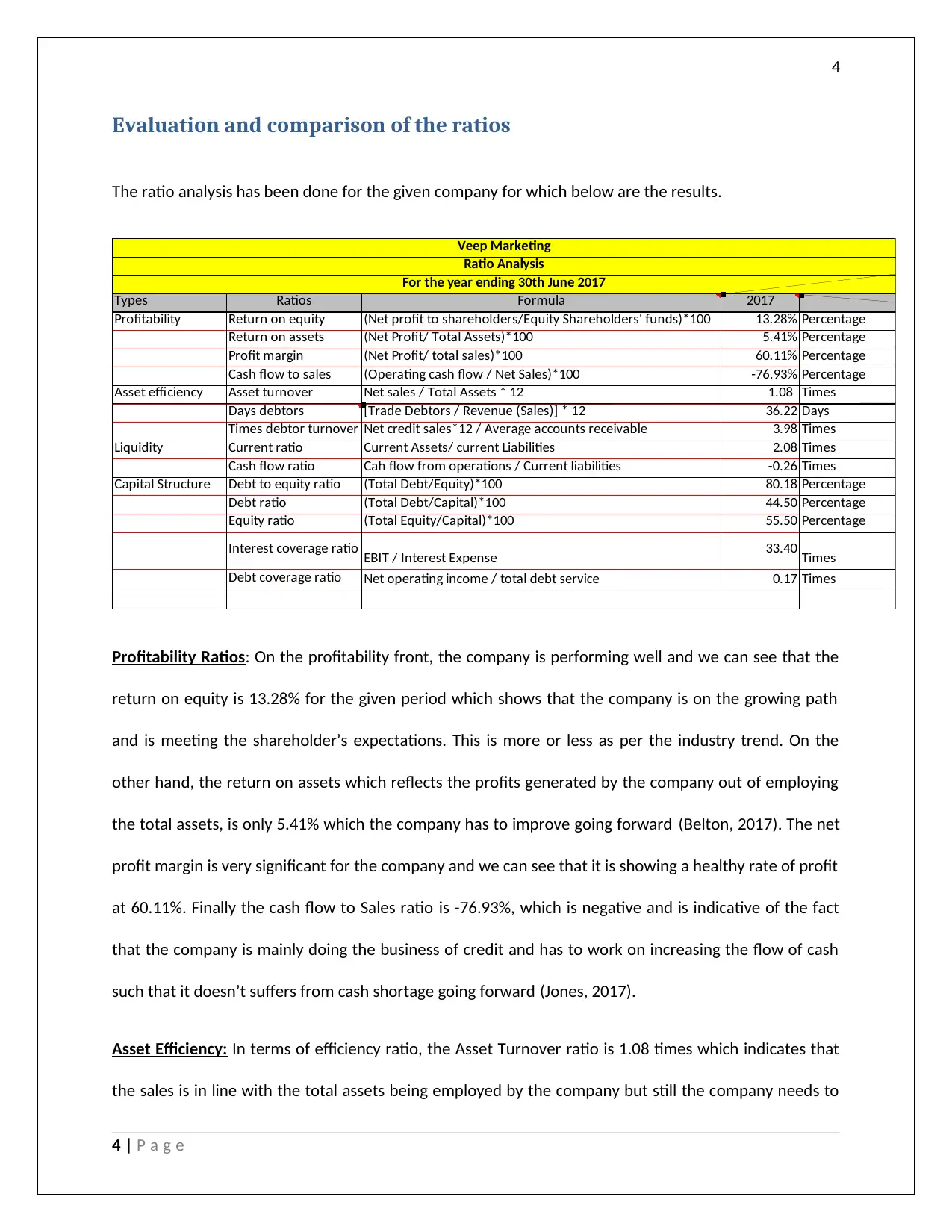

This report provides a financial analysis of Dreamboat Accountants for the period ending May 31, 2017. The analysis, conducted by a student, includes an executive summary, profitability ratios (return on equity, return on assets, net profit margin, cash flow to sales), asset efficiency ratios (asset turnover, debtor days), liquidity ratios, and capital structure ratios (debt to equity, interest coverage). The report highlights the company's strengths, such as a healthy net profit margin and manageable debt, while also pointing out areas for improvement, like negative cash flow from operations and the need to improve the debtor turnover. The analysis concludes with recommendations for the company's future financial strategies and includes limitations of the analysis and references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.