Financial Analysis and Auditing Report: Elmo Software Company Review

VerifiedAdded on 2023/01/03

|9

|1030

|36

Report

AI Summary

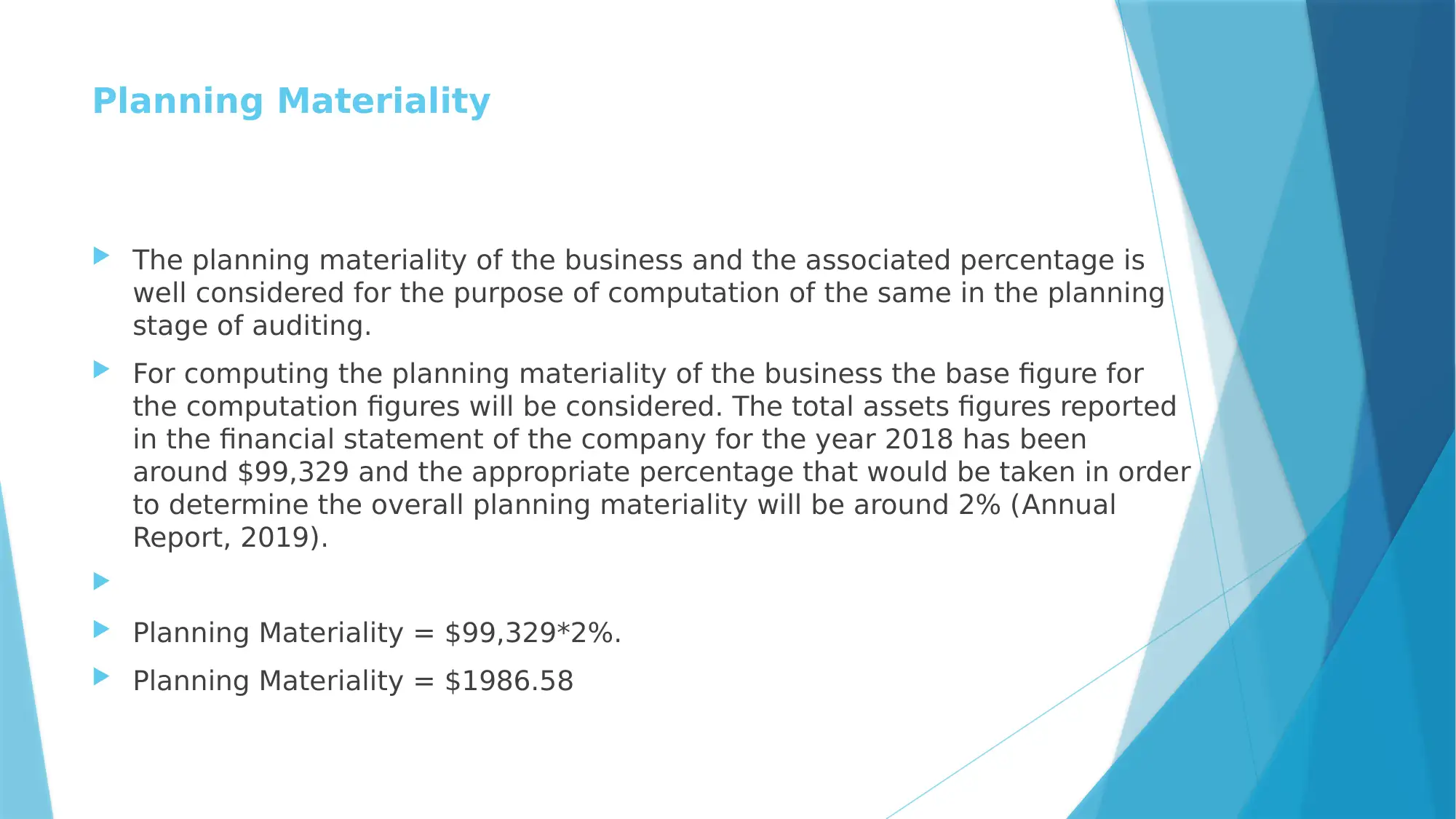

This report presents a comprehensive financial analysis of the Elmo Software Company, focusing on auditing and assurance. The analysis includes a preliminary risk assessment, evaluating the company's financial position through ratio analysis for the year 2018, and determining planning materiality. Key aspects covered involve assessing the company's financial performance, liquidity ratios, and associated business risks. The report also delves into the quality and effectiveness of independent audits, emphasizing the auditor's role in ensuring financial statement accuracy and addressing audit concerns by regulators. The analysis utilizes the company's annual report and relevant research papers to support its findings, offering insights into the company's financial health and the significance of auditing practices.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.