Comprehensive Financial Statement Analysis Report: Example Corporation

VerifiedAdded on 2023/01/20

|14

|3396

|74

Report

AI Summary

This report presents a financial statement analysis of Example Corporation, evaluating its financial performance through profitability and liquidity ratios. It begins with an executive summary and table of contents, followed by an introduction to financial statements, their components, and accounting equations. The report then delves into the essential components of financial statements, including the balance sheet, income statement, and cash flow statement, along with their usage and limitations. It discusses the three main accounting equations and two key accounting assumptions: going concern and materiality. The core of the report involves calculating and interpreting various financial ratios, such as current ratio, quick ratio, working capital ratio, and time interest earned ratio, to assess the company's financial health. The report also compares the calculated values with industry averages. Finally, the report offers recommendations based on the analysis and concludes with a summary of findings and a list of references.

Running head: FINANCIAL STATEMENT ANALYSIS

FINANCIAL STATEMENT ANALYSIS

Name of the Student

Name of the University

Author Note

FINANCIAL STATEMENT ANALYSIS

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL STATEMENT ANALYSIS

Executive Summary

The report is prepared to demonstrate the evaluation of the financial performance of Example

Corporation. Assessment of the financial position is done by evaluating the profitability and

liquidity position of the company. The interpretation of the financial statements of Example

Corporation is done for evaluating the financial health of the business. Such interpretation is

done by computing various ratios such as profit margin, gross profit margin, time interest earned

ratio, return on shareholders’ investment, working capital, quick ratio and current ratio. In

addition to this, report also demonstrates the comparison of the values computed with that of

industry value to measure the performance of company with that of industry.

FINANCIAL STATEMENT ANALYSIS

Executive Summary

The report is prepared to demonstrate the evaluation of the financial performance of Example

Corporation. Assessment of the financial position is done by evaluating the profitability and

liquidity position of the company. The interpretation of the financial statements of Example

Corporation is done for evaluating the financial health of the business. Such interpretation is

done by computing various ratios such as profit margin, gross profit margin, time interest earned

ratio, return on shareholders’ investment, working capital, quick ratio and current ratio. In

addition to this, report also demonstrates the comparison of the values computed with that of

industry value to measure the performance of company with that of industry.

2

FINANCIAL STATEMENT ANALYSIS

Table of Contents

Introduction......................................................................................................................................3

Essential components of financial statements and their usage........................................................3

Three main accounting equations....................................................................................................5

Two assumptions used in Accounting.............................................................................................6

Summary of the finding from calculations:.....................................................................................7

Comparing with the industrial values:...........................................................................................10

Recommendations:........................................................................................................................11

Conclusion:....................................................................................................................................12

References list:...............................................................................................................................13

FINANCIAL STATEMENT ANALYSIS

Table of Contents

Introduction......................................................................................................................................3

Essential components of financial statements and their usage........................................................3

Three main accounting equations....................................................................................................5

Two assumptions used in Accounting.............................................................................................6

Summary of the finding from calculations:.....................................................................................7

Comparing with the industrial values:...........................................................................................10

Recommendations:........................................................................................................................11

Conclusion:....................................................................................................................................12

References list:...............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL STATEMENT ANALYSIS

Introduction

A financial statement can be defined as an instrument, which is used to record the

financial performance of a company and provides information about the financial and operating

position of a company (insert citation). Various parties like external auditors, government

agencies and others audit these. The accuracy of these statements is of primary importance to all

their users as any misleading information can lead to bad decisions. They also suffer from other

inherent limitations like assumptions, unavailability of information at the time of preparation and

variations of interpretations among its users. It is universally accepted that great care should be

taken in the preparation of financial statements. Like every scientific approach, preparation of

financial statements is done using accounting equations which are the basis for the double entry

system. It also considers certain assumptions which are useful in the classification of items and

their treatment in the financial statements.

Essential components of financial statements and their usage

There are various types of financial statements prepared by a company in a given

financial year which record different aspects of a business. Some of the most prominent financial

statements are Balance Sheet, Income statement and statement of cash flow. The balance sheet

keeps a record of the assets, liabilities and the total equity of the company at a specific point in

time. It is used mostly to determine the net worth of the company which means how much is the

value of the company after meeting all of its liabilities with its current resources. Although it is

considered to be a very reliable source of information, it suffers from its own limitations. One of

them is the time factor. The balance sheet provides information only for a specific period of time.

Hence its usefulness diminishes with the passage of time and it is needed to be prepared again

for a different period. Another limitation is the accounting system used in the preparation of all

FINANCIAL STATEMENT ANALYSIS

Introduction

A financial statement can be defined as an instrument, which is used to record the

financial performance of a company and provides information about the financial and operating

position of a company (insert citation). Various parties like external auditors, government

agencies and others audit these. The accuracy of these statements is of primary importance to all

their users as any misleading information can lead to bad decisions. They also suffer from other

inherent limitations like assumptions, unavailability of information at the time of preparation and

variations of interpretations among its users. It is universally accepted that great care should be

taken in the preparation of financial statements. Like every scientific approach, preparation of

financial statements is done using accounting equations which are the basis for the double entry

system. It also considers certain assumptions which are useful in the classification of items and

their treatment in the financial statements.

Essential components of financial statements and their usage

There are various types of financial statements prepared by a company in a given

financial year which record different aspects of a business. Some of the most prominent financial

statements are Balance Sheet, Income statement and statement of cash flow. The balance sheet

keeps a record of the assets, liabilities and the total equity of the company at a specific point in

time. It is used mostly to determine the net worth of the company which means how much is the

value of the company after meeting all of its liabilities with its current resources. Although it is

considered to be a very reliable source of information, it suffers from its own limitations. One of

them is the time factor. The balance sheet provides information only for a specific period of time.

Hence its usefulness diminishes with the passage of time and it is needed to be prepared again

for a different period. Another limitation is the accounting system used in the preparation of all

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL STATEMENT ANALYSIS

the financial statements. Depreciation and amortisation and other items differ on the basis of the

accounting treatment and hence they vary on a company basis. Income statement records the

revenue generated and expenses incurred by the company in a given financial year. It is

considered to be more dynamic than the balance sheet and is used by the users to obtain more

current information. One of the limitations of income statement is that it fails to keep track of the

cash flow involved in the business. Due to the nature of accrual concept, income statement is the

most manipulated financial statement in order to present a positive picture of the financial

position of a company. It also suffers from other limitations like that of the balance sheet.

Statement of cash flow records only those activities which involve the inflow and outflow of

cash and its equivalents. Cash flow statement is highly useful in determining the liquidity of the

company. It is also helpful in the areas of budgeting, planning and controlling of the cash outlay

produced in a given period. Some of the limitations suffered by cash flow statement are due to its

nature. It does not show the profit earned by a company in a given year and also does not help in

the process of capital management. Like all financial statements, its usage in the real world is

limited by the time factor and it can only be used to interpret results. There is no chance to obtain

fully reliable results using this statement.

Operational decisions are those activities which are essential for the efficient functioning of the

business on a daily basis. Though these are in agreement with the long term strategies and aims

of the business, they are arrived at in a very short span of time.

Every financial statement consists of many smaller components which are highly useful in the

process of decision making. Balance sheet consists of stock lying at the end of the year which

can be useful in preparing the sales strategy for the current year. The amount can be used to sell

previous year’s stock first. Balance sheet also consists of debtors which is useful in preparing the

FINANCIAL STATEMENT ANALYSIS

the financial statements. Depreciation and amortisation and other items differ on the basis of the

accounting treatment and hence they vary on a company basis. Income statement records the

revenue generated and expenses incurred by the company in a given financial year. It is

considered to be more dynamic than the balance sheet and is used by the users to obtain more

current information. One of the limitations of income statement is that it fails to keep track of the

cash flow involved in the business. Due to the nature of accrual concept, income statement is the

most manipulated financial statement in order to present a positive picture of the financial

position of a company. It also suffers from other limitations like that of the balance sheet.

Statement of cash flow records only those activities which involve the inflow and outflow of

cash and its equivalents. Cash flow statement is highly useful in determining the liquidity of the

company. It is also helpful in the areas of budgeting, planning and controlling of the cash outlay

produced in a given period. Some of the limitations suffered by cash flow statement are due to its

nature. It does not show the profit earned by a company in a given year and also does not help in

the process of capital management. Like all financial statements, its usage in the real world is

limited by the time factor and it can only be used to interpret results. There is no chance to obtain

fully reliable results using this statement.

Operational decisions are those activities which are essential for the efficient functioning of the

business on a daily basis. Though these are in agreement with the long term strategies and aims

of the business, they are arrived at in a very short span of time.

Every financial statement consists of many smaller components which are highly useful in the

process of decision making. Balance sheet consists of stock lying at the end of the year which

can be useful in preparing the sales strategy for the current year. The amount can be used to sell

previous year’s stock first. Balance sheet also consists of debtors which is useful in preparing the

5

FINANCIAL STATEMENT ANALYSIS

credit policy for this year. The effectiveness of the measures adopted in the previous year are

also understood through this value. Income statement is the most useful tool when there is a

necessity for comparison with other companies of same industry. Some of the useful components

of Income statement are cost of goods sold, depreciation, gross profit, EBITDA and general and

administrative expenses incurred. The main role played by these statements is that they provide

information about the costs incurred by the company. It is helpful to the managers in identifying

areas where the costs are more and in coming up with measures to reduce such costs. The most

important financial statement with regard to operational decision making is the cash flow

statement. While income statement and balance sheet contain items which may not have been

received but have been accrued, the cash flow statement gives a clear indication about a

company’s ability to sustain operations. It indicates whether the company can meet any short

term expenses within a short notice or not. Any fall in the cash flow ratios is a warning to the

managers. It is an indication to them that there is something wrong with one of the aspects of the

business and it needs to be worked on to improve the operational position.

Three main accounting equations

Accounting equations is a tool, which explains the relationship between different

components of the financial statements. One of the most popular accounting equations is Assets

= Liabilities + Owner’s equity. This equation can be derived from the balance sheet and is the

basis for the double entry system of accounting. It is also known as the basic accounting

equation. It explains that the assets of a company are always equal to the liabilities of it as equity

is a liability to the business.

Another important equation is Net Revenue = Revenue – Expenses. This is important because it

just does not suggest the amount of revenue but also considers the expenses incurred to earn that

FINANCIAL STATEMENT ANALYSIS

credit policy for this year. The effectiveness of the measures adopted in the previous year are

also understood through this value. Income statement is the most useful tool when there is a

necessity for comparison with other companies of same industry. Some of the useful components

of Income statement are cost of goods sold, depreciation, gross profit, EBITDA and general and

administrative expenses incurred. The main role played by these statements is that they provide

information about the costs incurred by the company. It is helpful to the managers in identifying

areas where the costs are more and in coming up with measures to reduce such costs. The most

important financial statement with regard to operational decision making is the cash flow

statement. While income statement and balance sheet contain items which may not have been

received but have been accrued, the cash flow statement gives a clear indication about a

company’s ability to sustain operations. It indicates whether the company can meet any short

term expenses within a short notice or not. Any fall in the cash flow ratios is a warning to the

managers. It is an indication to them that there is something wrong with one of the aspects of the

business and it needs to be worked on to improve the operational position.

Three main accounting equations

Accounting equations is a tool, which explains the relationship between different

components of the financial statements. One of the most popular accounting equations is Assets

= Liabilities + Owner’s equity. This equation can be derived from the balance sheet and is the

basis for the double entry system of accounting. It is also known as the basic accounting

equation. It explains that the assets of a company are always equal to the liabilities of it as equity

is a liability to the business.

Another important equation is Net Revenue = Revenue – Expenses. This is important because it

just does not suggest the amount of revenue but also considers the expenses incurred to earn that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL STATEMENT ANALYSIS

revenue. It also shows costs in proportion to the revenue and is helpful to the managers in setting

up financial goals for the future like increasing revenues and reducing costs.

The final equation is Net Margin = Net Profit/Sales. This equation is a better measure than gross

margin because it is arrived at after deducting all the expenses that directly or indirectly

contribute towards achieving the sales. Gross margin is calculated by deducting only the cost of

goods. This is not a good measure as it does not consider other expenses like salaries of

employees, office expenses and other indirect expenses. The higher the net margin, the better is

the financial performance of the company.

Two assumptions used in Accounting

Assumptions is defined as something that is assumed as true even without the existence

of a proper proof to support it. The most used assumption in the preparation of the financial

statements is the going concern assumption. As suggested by the name itself, this concept

assumes that a business intends to carry on conducting its business for the near future and has no

immediate plans of winding up. This assumption is the reason that instead of writing off all

expenses in a given year, some of them are amortized due to their nature of providing benefits

for more than a single financial year. Some of the items, which are accounted for using the going

concern concept, are deferred revenue, depreciation, and advertisement expenditure.

Materiality is another accounting assumption that plays an important role in determining how an

item is presented in the financial statements. The main aspect, which is considered while

determining the materiality of an item, is the nature of the item and the impact it would have on

the financial statements. This assumption is the reason for considering the purchase of a dustbin

as a petty expense rather than as an investment in an asset.

FINANCIAL STATEMENT ANALYSIS

revenue. It also shows costs in proportion to the revenue and is helpful to the managers in setting

up financial goals for the future like increasing revenues and reducing costs.

The final equation is Net Margin = Net Profit/Sales. This equation is a better measure than gross

margin because it is arrived at after deducting all the expenses that directly or indirectly

contribute towards achieving the sales. Gross margin is calculated by deducting only the cost of

goods. This is not a good measure as it does not consider other expenses like salaries of

employees, office expenses and other indirect expenses. The higher the net margin, the better is

the financial performance of the company.

Two assumptions used in Accounting

Assumptions is defined as something that is assumed as true even without the existence

of a proper proof to support it. The most used assumption in the preparation of the financial

statements is the going concern assumption. As suggested by the name itself, this concept

assumes that a business intends to carry on conducting its business for the near future and has no

immediate plans of winding up. This assumption is the reason that instead of writing off all

expenses in a given year, some of them are amortized due to their nature of providing benefits

for more than a single financial year. Some of the items, which are accounted for using the going

concern concept, are deferred revenue, depreciation, and advertisement expenditure.

Materiality is another accounting assumption that plays an important role in determining how an

item is presented in the financial statements. The main aspect, which is considered while

determining the materiality of an item, is the nature of the item and the impact it would have on

the financial statements. This assumption is the reason for considering the purchase of a dustbin

as a petty expense rather than as an investment in an asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL STATEMENT ANALYSIS

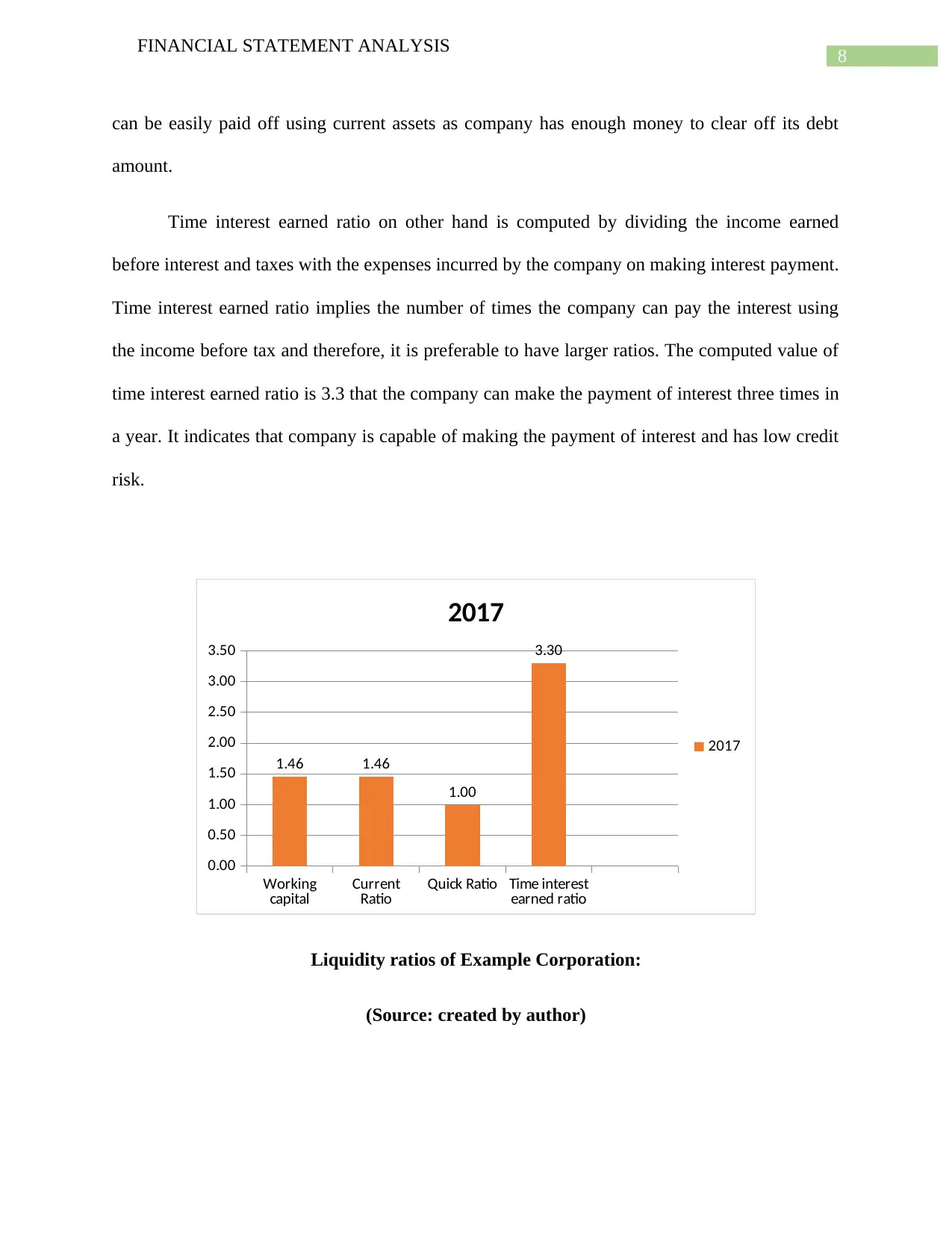

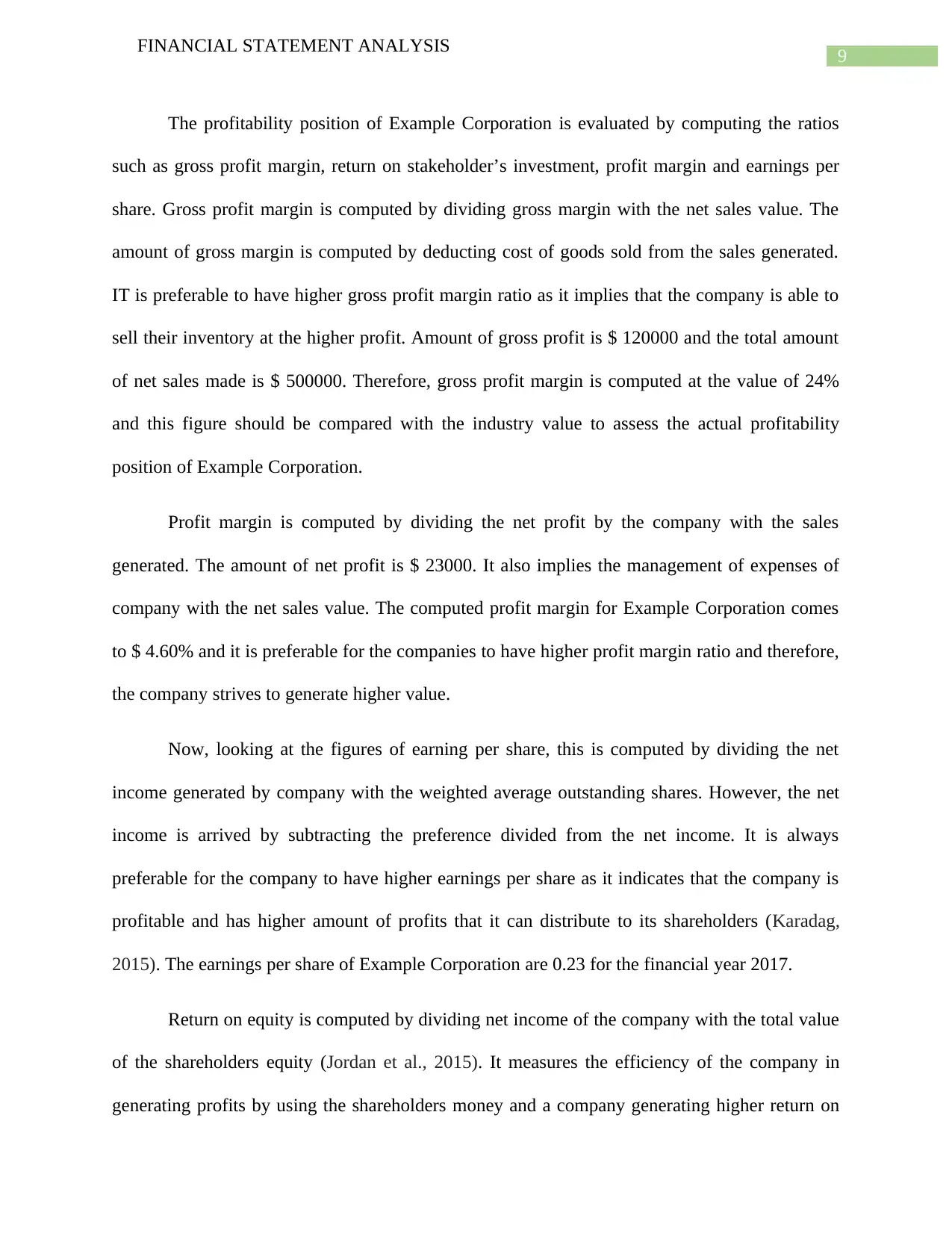

Summary of the finding from calculations:

In this section of the report, the financial position of Example Corporation is evaluated by

the computation of different ratios along with presenting the working of the calculated values.

All the ratios have been calculated based on the financial year ending 2017. The computation of

all the ratios is presented graphically based on which the interpretations have been done.

Current ratio of Example Corporation is obtained by dividing current assets by current

liabilities. The value of current assets and current liabilities is recorded at $ 89000 and $ 61000

respectively. Current ratio obtained by the computation is 1.46 and working capital is same as

current ratio and the figure comes as same as 1.46. It is favorable for the organization to have

higher current ratio because it implies that the company is making enough money from

operations to settle its current liabilities. For understanding the concept of working capital, it

indicates that the current assets have more than the current liabilities and therefore firm is not

required to sell its assets to pay off its current liabilities (Kidwell et al., 2016). However, it is

required to compare the values with industry average to determine the accuracy of the financial

position.

Quick ratio is computed by subtracting inventories from current assets and dividing it by

current liabilities. Value of quick ratio of Example Corporation is 1 which indicates that the

company has as many quick assets as current liabilities and liabilities can be easily paid of suing

quick assets.

Working capital ratio is computed by dividing current assets by current liabilities and it is

considered desirable to have higher working capital ratio. Working capital ratio of Example

Corporation is 1.46 which is more than 1 and this has the implication that the current liabilities

FINANCIAL STATEMENT ANALYSIS

Summary of the finding from calculations:

In this section of the report, the financial position of Example Corporation is evaluated by

the computation of different ratios along with presenting the working of the calculated values.

All the ratios have been calculated based on the financial year ending 2017. The computation of

all the ratios is presented graphically based on which the interpretations have been done.

Current ratio of Example Corporation is obtained by dividing current assets by current

liabilities. The value of current assets and current liabilities is recorded at $ 89000 and $ 61000

respectively. Current ratio obtained by the computation is 1.46 and working capital is same as

current ratio and the figure comes as same as 1.46. It is favorable for the organization to have

higher current ratio because it implies that the company is making enough money from

operations to settle its current liabilities. For understanding the concept of working capital, it

indicates that the current assets have more than the current liabilities and therefore firm is not

required to sell its assets to pay off its current liabilities (Kidwell et al., 2016). However, it is

required to compare the values with industry average to determine the accuracy of the financial

position.

Quick ratio is computed by subtracting inventories from current assets and dividing it by

current liabilities. Value of quick ratio of Example Corporation is 1 which indicates that the

company has as many quick assets as current liabilities and liabilities can be easily paid of suing

quick assets.

Working capital ratio is computed by dividing current assets by current liabilities and it is

considered desirable to have higher working capital ratio. Working capital ratio of Example

Corporation is 1.46 which is more than 1 and this has the implication that the current liabilities

8

FINANCIAL STATEMENT ANALYSIS

can be easily paid off using current assets as company has enough money to clear off its debt

amount.

Time interest earned ratio on other hand is computed by dividing the income earned

before interest and taxes with the expenses incurred by the company on making interest payment.

Time interest earned ratio implies the number of times the company can pay the interest using

the income before tax and therefore, it is preferable to have larger ratios. The computed value of

time interest earned ratio is 3.3 that the company can make the payment of interest three times in

a year. It indicates that company is capable of making the payment of interest and has low credit

risk.

Working

capital Current

Ratio Quick Ratio Time interest

earned ratio

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1.46 1.46

1.00

3.30

2017

2017

Liquidity ratios of Example Corporation:

(Source: created by author)

FINANCIAL STATEMENT ANALYSIS

can be easily paid off using current assets as company has enough money to clear off its debt

amount.

Time interest earned ratio on other hand is computed by dividing the income earned

before interest and taxes with the expenses incurred by the company on making interest payment.

Time interest earned ratio implies the number of times the company can pay the interest using

the income before tax and therefore, it is preferable to have larger ratios. The computed value of

time interest earned ratio is 3.3 that the company can make the payment of interest three times in

a year. It indicates that company is capable of making the payment of interest and has low credit

risk.

Working

capital Current

Ratio Quick Ratio Time interest

earned ratio

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1.46 1.46

1.00

3.30

2017

2017

Liquidity ratios of Example Corporation:

(Source: created by author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL STATEMENT ANALYSIS

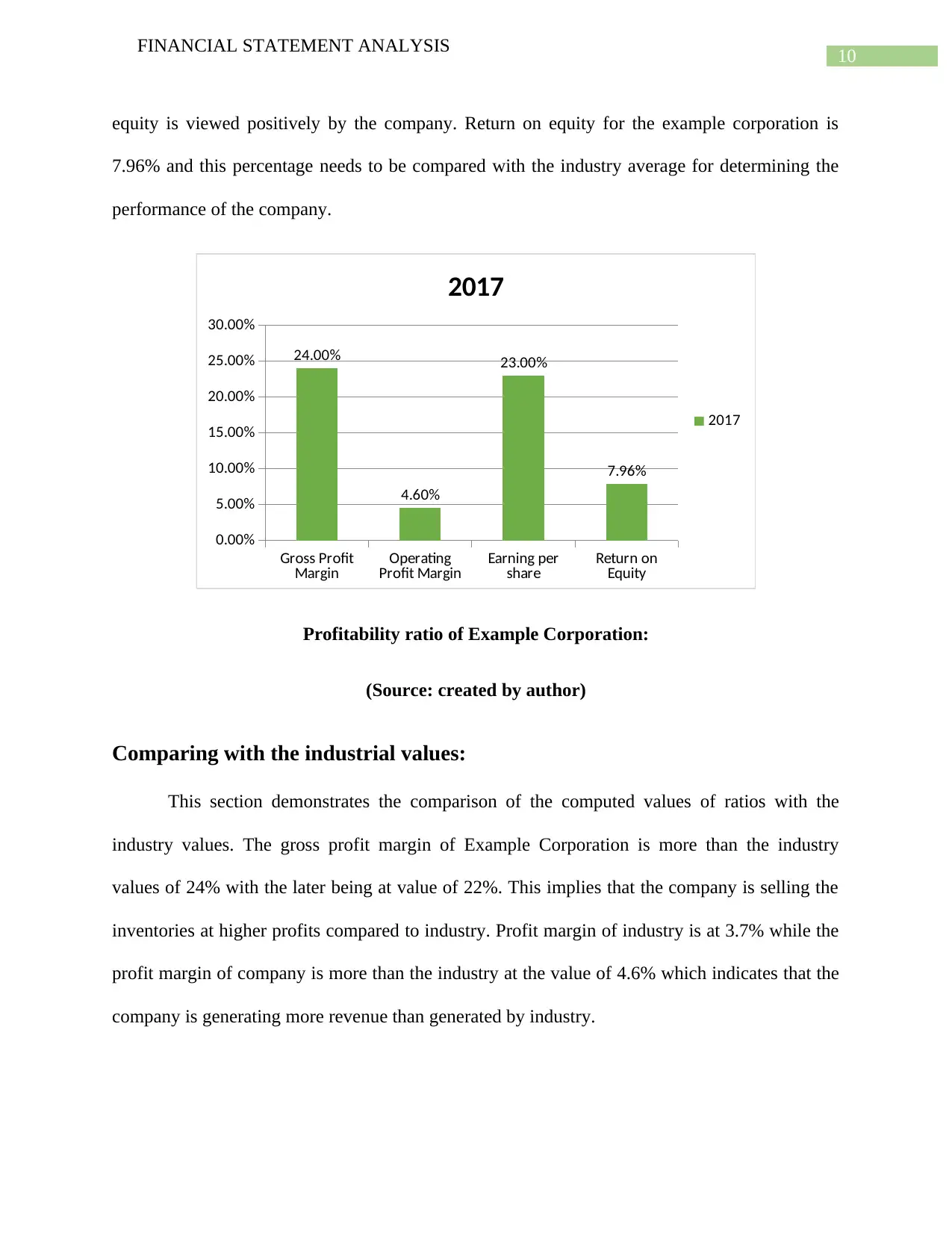

The profitability position of Example Corporation is evaluated by computing the ratios

such as gross profit margin, return on stakeholder’s investment, profit margin and earnings per

share. Gross profit margin is computed by dividing gross margin with the net sales value. The

amount of gross margin is computed by deducting cost of goods sold from the sales generated.

IT is preferable to have higher gross profit margin ratio as it implies that the company is able to

sell their inventory at the higher profit. Amount of gross profit is $ 120000 and the total amount

of net sales made is $ 500000. Therefore, gross profit margin is computed at the value of 24%

and this figure should be compared with the industry value to assess the actual profitability

position of Example Corporation.

Profit margin is computed by dividing the net profit by the company with the sales

generated. The amount of net profit is $ 23000. It also implies the management of expenses of

company with the net sales value. The computed profit margin for Example Corporation comes

to $ 4.60% and it is preferable for the companies to have higher profit margin ratio and therefore,

the company strives to generate higher value.

Now, looking at the figures of earning per share, this is computed by dividing the net

income generated by company with the weighted average outstanding shares. However, the net

income is arrived by subtracting the preference divided from the net income. It is always

preferable for the company to have higher earnings per share as it indicates that the company is

profitable and has higher amount of profits that it can distribute to its shareholders (Karadag,

2015). The earnings per share of Example Corporation are 0.23 for the financial year 2017.

Return on equity is computed by dividing net income of the company with the total value

of the shareholders equity (Jordan et al., 2015). It measures the efficiency of the company in

generating profits by using the shareholders money and a company generating higher return on

FINANCIAL STATEMENT ANALYSIS

The profitability position of Example Corporation is evaluated by computing the ratios

such as gross profit margin, return on stakeholder’s investment, profit margin and earnings per

share. Gross profit margin is computed by dividing gross margin with the net sales value. The

amount of gross margin is computed by deducting cost of goods sold from the sales generated.

IT is preferable to have higher gross profit margin ratio as it implies that the company is able to

sell their inventory at the higher profit. Amount of gross profit is $ 120000 and the total amount

of net sales made is $ 500000. Therefore, gross profit margin is computed at the value of 24%

and this figure should be compared with the industry value to assess the actual profitability

position of Example Corporation.

Profit margin is computed by dividing the net profit by the company with the sales

generated. The amount of net profit is $ 23000. It also implies the management of expenses of

company with the net sales value. The computed profit margin for Example Corporation comes

to $ 4.60% and it is preferable for the companies to have higher profit margin ratio and therefore,

the company strives to generate higher value.

Now, looking at the figures of earning per share, this is computed by dividing the net

income generated by company with the weighted average outstanding shares. However, the net

income is arrived by subtracting the preference divided from the net income. It is always

preferable for the company to have higher earnings per share as it indicates that the company is

profitable and has higher amount of profits that it can distribute to its shareholders (Karadag,

2015). The earnings per share of Example Corporation are 0.23 for the financial year 2017.

Return on equity is computed by dividing net income of the company with the total value

of the shareholders equity (Jordan et al., 2015). It measures the efficiency of the company in

generating profits by using the shareholders money and a company generating higher return on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL STATEMENT ANALYSIS

equity is viewed positively by the company. Return on equity for the example corporation is

7.96% and this percentage needs to be compared with the industry average for determining the

performance of the company.

Gross Profit

Margin Operating

Profit Margin Earning per

share Return on

Equity

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

24.00%

4.60%

23.00%

7.96%

2017

2017

Profitability ratio of Example Corporation:

(Source: created by author)

Comparing with the industrial values:

This section demonstrates the comparison of the computed values of ratios with the

industry values. The gross profit margin of Example Corporation is more than the industry

values of 24% with the later being at value of 22%. This implies that the company is selling the

inventories at higher profits compared to industry. Profit margin of industry is at 3.7% while the

profit margin of company is more than the industry at the value of 4.6% which indicates that the

company is generating more revenue than generated by industry.

FINANCIAL STATEMENT ANALYSIS

equity is viewed positively by the company. Return on equity for the example corporation is

7.96% and this percentage needs to be compared with the industry average for determining the

performance of the company.

Gross Profit

Margin Operating

Profit Margin Earning per

share Return on

Equity

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

24.00%

4.60%

23.00%

7.96%

2017

2017

Profitability ratio of Example Corporation:

(Source: created by author)

Comparing with the industrial values:

This section demonstrates the comparison of the computed values of ratios with the

industry values. The gross profit margin of Example Corporation is more than the industry

values of 24% with the later being at value of 22%. This implies that the company is selling the

inventories at higher profits compared to industry. Profit margin of industry is at 3.7% while the

profit margin of company is more than the industry at the value of 4.6% which indicates that the

company is generating more revenue than generated by industry.

11

FINANCIAL STATEMENT ANALYSIS

Now, looking at the value of earning per share, the industry value is $ 0.24 compared to

earnings per share for Example corporation at $ 0.23. This indicates that the profitability aspect

of the company is less than the industry. Time interest earned ratio of the company is 3.3 which

are more that the industry average of 3. Higher value of time interest earned ratio of company

compared to industry value, implies that the number of time company is making payment of

interest frequently than the industry. Higher ratio is considered favorable as it is viewed by the

creditors that the company is less risky and they can lend to the company (Brigham et al., 2016).

Return on the shareholder investment generated by industry is 6% while that generated

by the company is 7.96%. It is always consider desirable for the company to have higher return

on equity as it is considered profitable for the investors. Therefore, the performance o f company

in terms of generating return on the investment made by the shareholders is better than the return

generated by the industry.

Recommendations:

It is observed that the earnings per share of the company is lower than the industry values

It is therefore recommended to the company to increase its earnings per share. Example

Corporation can increase its earnings per share by repurchasing their own stocks.

It is also observed from the financial figures of the company that the total amount of

expenses is increasing with higher figures reported in year 2017 as against 2016.

Example Corporation is recommended to reduce the overall expenses so as to increase

the total amount of net profits generated by the company.

FINANCIAL STATEMENT ANALYSIS

Now, looking at the value of earning per share, the industry value is $ 0.24 compared to

earnings per share for Example corporation at $ 0.23. This indicates that the profitability aspect

of the company is less than the industry. Time interest earned ratio of the company is 3.3 which

are more that the industry average of 3. Higher value of time interest earned ratio of company

compared to industry value, implies that the number of time company is making payment of

interest frequently than the industry. Higher ratio is considered favorable as it is viewed by the

creditors that the company is less risky and they can lend to the company (Brigham et al., 2016).

Return on the shareholder investment generated by industry is 6% while that generated

by the company is 7.96%. It is always consider desirable for the company to have higher return

on equity as it is considered profitable for the investors. Therefore, the performance o f company

in terms of generating return on the investment made by the shareholders is better than the return

generated by the industry.

Recommendations:

It is observed that the earnings per share of the company is lower than the industry values

It is therefore recommended to the company to increase its earnings per share. Example

Corporation can increase its earnings per share by repurchasing their own stocks.

It is also observed from the financial figures of the company that the total amount of

expenses is increasing with higher figures reported in year 2017 as against 2016.

Example Corporation is recommended to reduce the overall expenses so as to increase

the total amount of net profits generated by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.