Comprehensive Financial Analysis of Flight Centre Travel Group (FCTG)

VerifiedAdded on 2021/04/22

|22

|3926

|25

Report

AI Summary

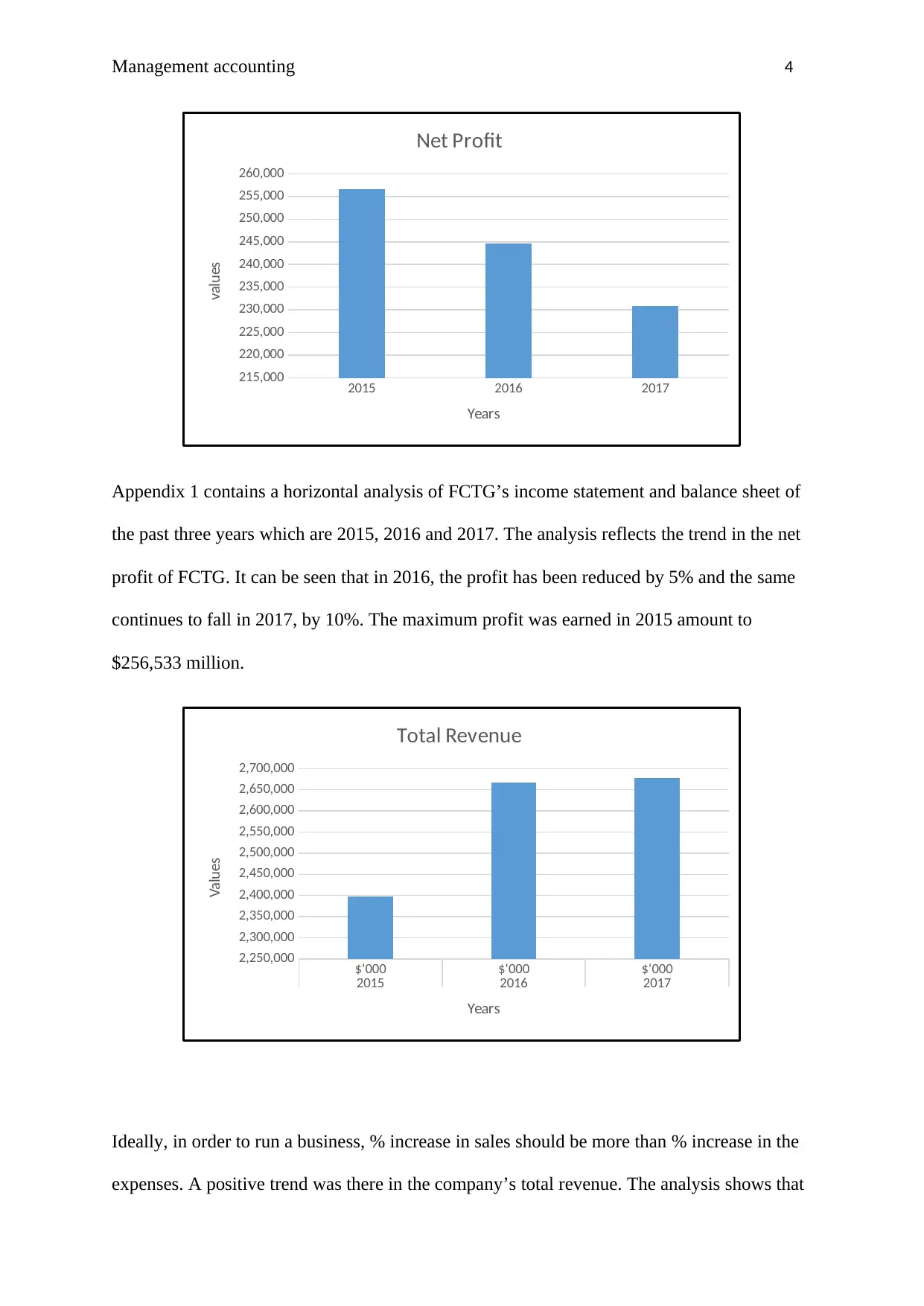

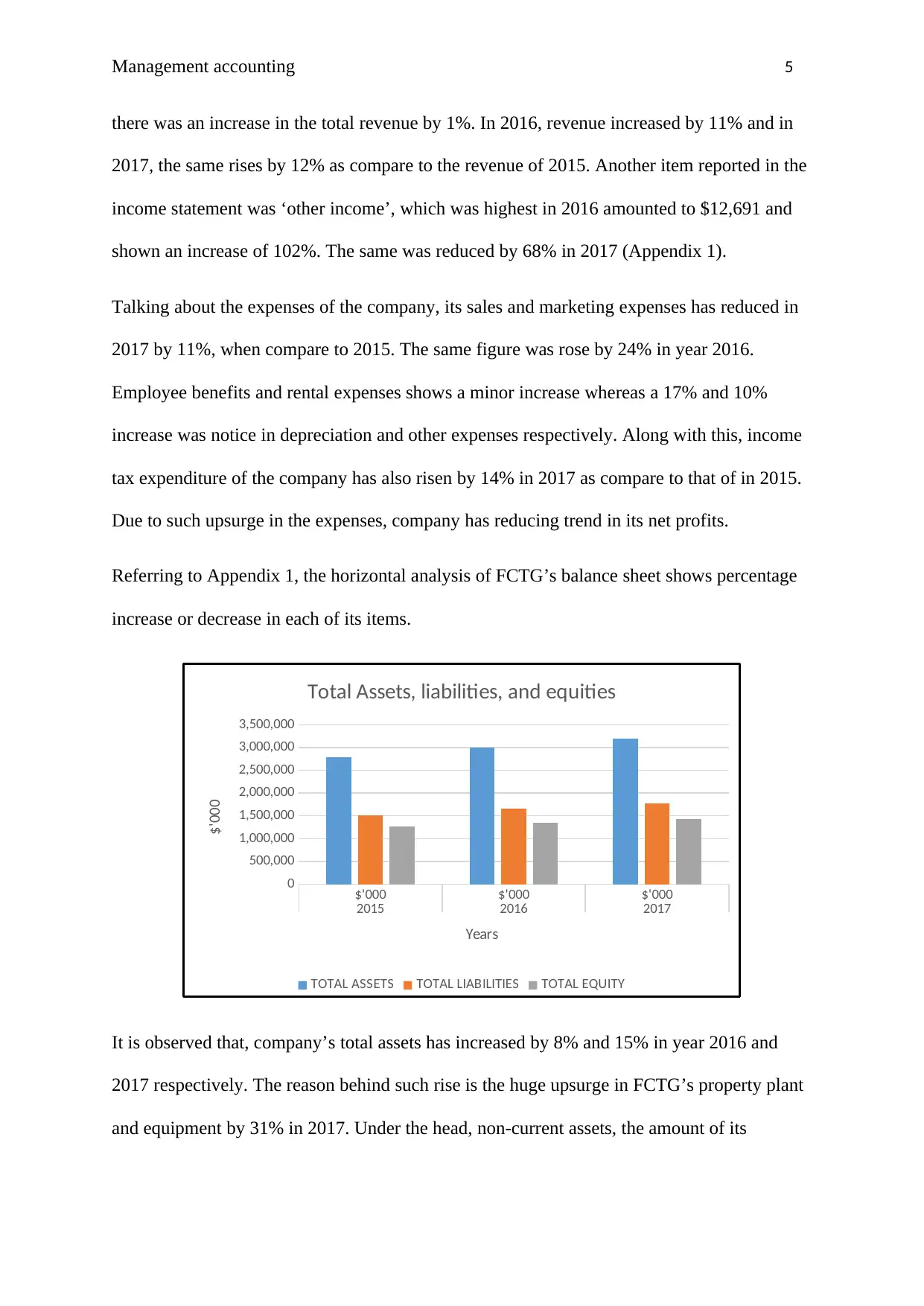

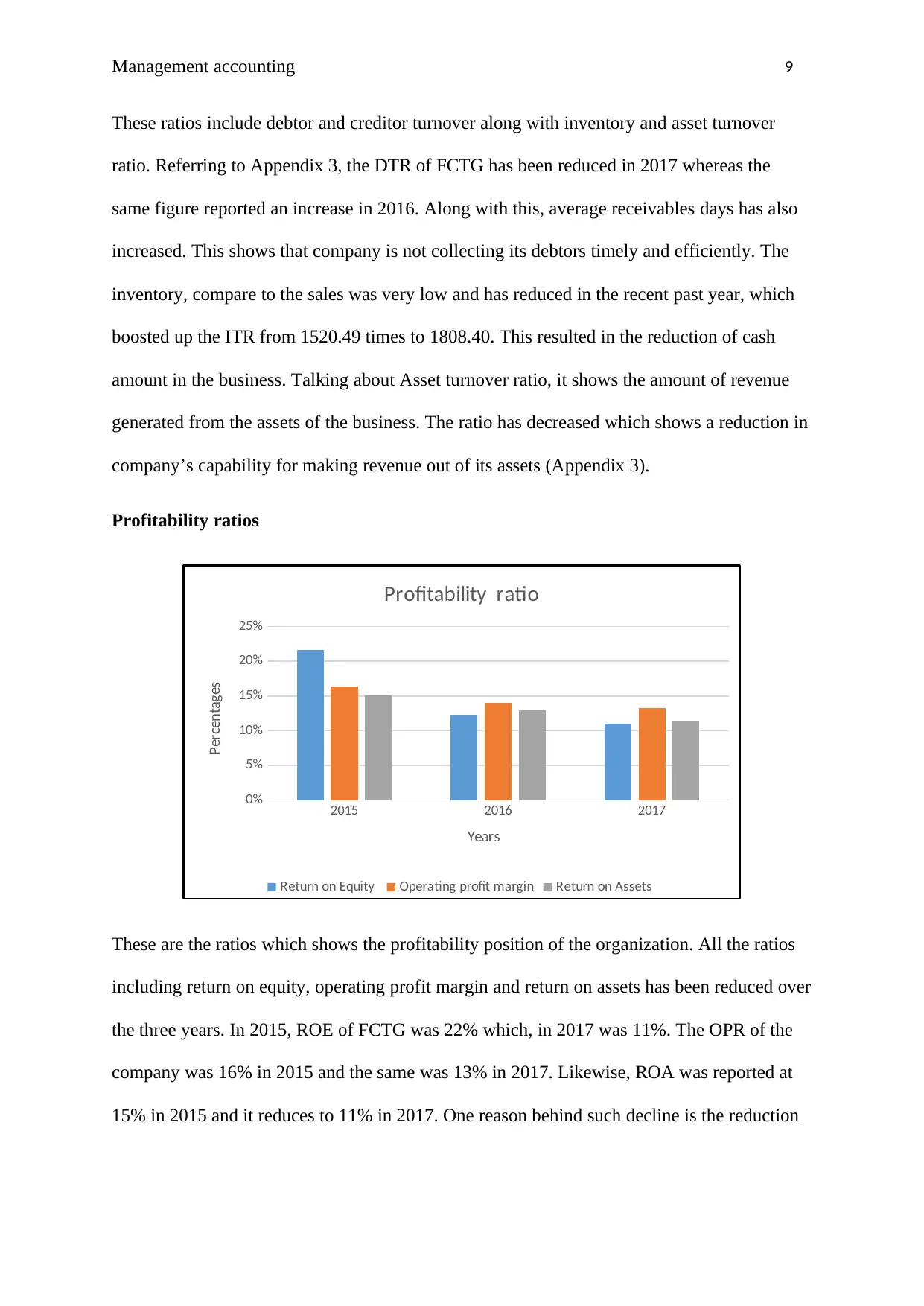

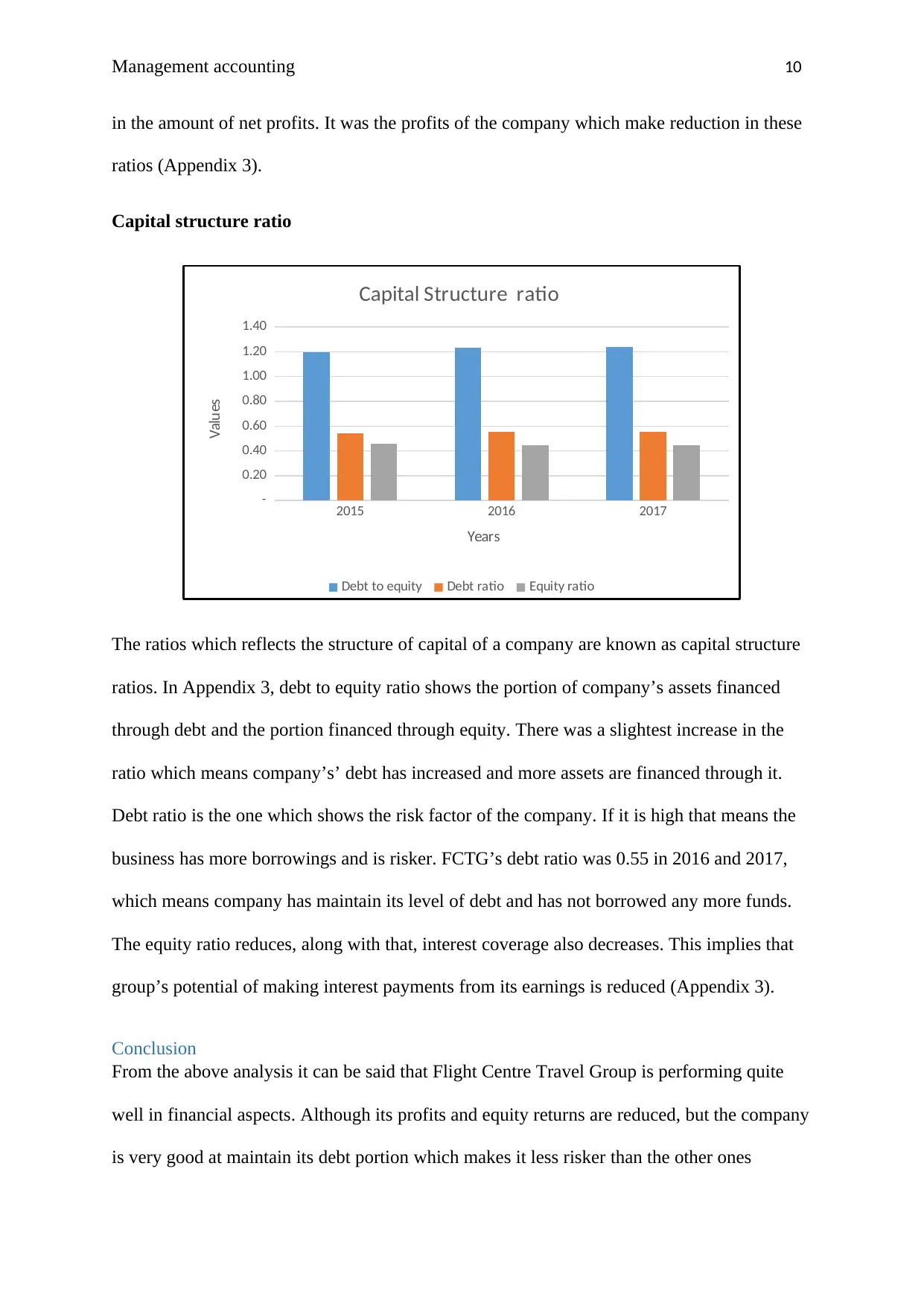

This report presents a comprehensive financial analysis of Flight Centre Travel Group (FCTG), a major travel agency in Australia, examining its performance over three years (2015-2017). The analysis begins with an executive summary and an introduction to FCTG's business operations and market position. The report then delves into the financial statements, employing both horizontal and vertical analysis to assess trends and relationships within the income statement and balance sheet. Horizontal analysis reveals year-over-year changes in financial statement items, highlighting revenue growth, expense fluctuations, and profit trends. Vertical analysis expresses each item as a percentage of a base figure, providing insights into the relative size and composition of financial statement components. The analysis also incorporates a detailed ratio analysis, covering liquidity, efficiency, profitability, and capital structure ratios. Liquidity ratios such as current and quick ratios, and cash ratios are examined to assess the company's short-term solvency. Efficiency ratios, including debtor turnover and inventory turnover, are evaluated to gauge how efficiently the company utilizes its assets. Profitability ratios such as return on equity, operating profit margin, and return on assets are analyzed to measure the company's financial performance. Capital structure ratios, including debt-to-equity and debt ratios, are used to assess the company's leverage and financial risk. The report concludes with a summary of key findings, including the company's financial strengths and weaknesses, and includes appendices containing supporting financial data and calculations. The analysis indicates FCTG is performing well, although profitability and equity returns have declined, the company effectively manages its debt, positioning it as a less risky investment.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.