Financial Feasibility Evaluation: Hattie's Geodes Business Plan

VerifiedAdded on 2021/03/25

|24

|3706

|182

Report

AI Summary

This report assesses the financial feasibility of Hattie's proposed geodes retail business. It includes a comprehensive analysis encompassing breakeven analysis, profit and loss statements, balance sheets, and monthly and annual cash flow projections. The report evaluates two scenarios: online sales of geodes and sales of cabinets to a friend. It calculates key financial metrics, including the break-even point, and performs sensitivity analysis to assess the impact of various factors on profitability. The analysis reveals that online sales of geodes are highly profitable, while the cabinet sales proposal is not financially viable. The report also calculates the maximum upfront fee that could be offered and provides conclusions and recommendations, suggesting Hattie should proceed with the online sales plan but reject the cabinet proposal. The report also includes critical reflection and references.

Evaluation of financial feasibility

of proposed venture

1 | P a g e

of proposed venture

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Executive Summary................................................................................................... 3

Main Report................................................................................................................ 4

Break even Analysis................................................................................................ 4

Profit and loss statement for the 1st year of operations...........................................8

Balance Sheet at the end of first year...................................................................12

Monthly Cash flow for the first year of operation..................................................13

Annual Cash Flow.................................................................................................. 16

Amount of Cash the business would need to get started......................................18

Sensitivity Analysis................................................................................................ 19

Calculation of maximum amount that could be offered as upfront fee.................24

Conclusions and recommendations.......................................................................26

Critical Reflection..................................................................................................... 26

References............................................................................................................... 27

2 | P a g e

Executive Summary................................................................................................... 3

Main Report................................................................................................................ 4

Break even Analysis................................................................................................ 4

Profit and loss statement for the 1st year of operations...........................................8

Balance Sheet at the end of first year...................................................................12

Monthly Cash flow for the first year of operation..................................................13

Annual Cash Flow.................................................................................................. 16

Amount of Cash the business would need to get started......................................18

Sensitivity Analysis................................................................................................ 19

Calculation of maximum amount that could be offered as upfront fee.................24

Conclusions and recommendations.......................................................................26

Critical Reflection..................................................................................................... 26

References............................................................................................................... 27

2 | P a g e

Executive Summary

This report conducts an evaluation of the proposed business opportunity of retailing

of geodes that is available to Hattie. The evaluation has been done by performing

various calculations such as breakeven analysis, computation of profit/loss for the

first year of business, preparation of balance sheet for the first year of business,

monthly cash flow for the first year of operations. The report also shows calculation

of Annual Cash flow, Maximum amount that can be offered as upfront fee,

Calculation of Net Present value of Cash Inflows and Sensitivity Analysis of the

business opportunity. The results of these calculations and analysis of those results

have led to the conclusion that Hattie should go ahead with the plan of online sale

of geodes as it is highly profitable but should not accept the proposal of supply of

cabinets to Ian as it would not prove profitable to her.

3 | P a g e

This report conducts an evaluation of the proposed business opportunity of retailing

of geodes that is available to Hattie. The evaluation has been done by performing

various calculations such as breakeven analysis, computation of profit/loss for the

first year of business, preparation of balance sheet for the first year of business,

monthly cash flow for the first year of operations. The report also shows calculation

of Annual Cash flow, Maximum amount that can be offered as upfront fee,

Calculation of Net Present value of Cash Inflows and Sensitivity Analysis of the

business opportunity. The results of these calculations and analysis of those results

have led to the conclusion that Hattie should go ahead with the plan of online sale

of geodes as it is highly profitable but should not accept the proposal of supply of

cabinets to Ian as it would not prove profitable to her.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Main Report

This report will do an evaluation of the financial feasibility of the venture that Hattie

intends to start. Various calculations have been performed so as to support in

analysis of the business opportunity. Since Hattie would get the exclusive rights for

dealing in geodes for a period of 6 years only, the business will be existence for the

aforesaid period of 6 years only.

(All amounts are in GBP)

Break even Analysis

Breakeven point is that point at which the revenue generated by the business is

equal to the total costs incurred by the business. i.e., there is a situation of no

profit, no loss. At the breakeven point, the net profit earned by the business is equal

to zero. Breakeven point shows the quantity of product that should be sold by the

business so as to be able to cover its fixed costs as well as variable costs. It is

important for the business to know its beak even point so as to ensure that the

actual quantity or the number of units sold by it are not less than the breakeven

point for the business. Breakeven point is calculated by dividing fixed costs by

contribution per unit

In the given case, the breakeven point will be calculated for 2 scenarios – (i) Online

sale of geodes (ii) Sale of Cabinets (each equivalent to 1.5 kg of Geodes) to Hattie’s

friend Ian.

i. Online sale of geodes

In order to arrive at the breakeven point for online sales geodes, contribution per

unit will required to be calculated.

Calculation of contribution for each kg of geodes

4 | P a g e

This report will do an evaluation of the financial feasibility of the venture that Hattie

intends to start. Various calculations have been performed so as to support in

analysis of the business opportunity. Since Hattie would get the exclusive rights for

dealing in geodes for a period of 6 years only, the business will be existence for the

aforesaid period of 6 years only.

(All amounts are in GBP)

Break even Analysis

Breakeven point is that point at which the revenue generated by the business is

equal to the total costs incurred by the business. i.e., there is a situation of no

profit, no loss. At the breakeven point, the net profit earned by the business is equal

to zero. Breakeven point shows the quantity of product that should be sold by the

business so as to be able to cover its fixed costs as well as variable costs. It is

important for the business to know its beak even point so as to ensure that the

actual quantity or the number of units sold by it are not less than the breakeven

point for the business. Breakeven point is calculated by dividing fixed costs by

contribution per unit

In the given case, the breakeven point will be calculated for 2 scenarios – (i) Online

sale of geodes (ii) Sale of Cabinets (each equivalent to 1.5 kg of Geodes) to Hattie’s

friend Ian.

i. Online sale of geodes

In order to arrive at the breakeven point for online sales geodes, contribution per

unit will required to be calculated.

Calculation of contribution for each kg of geodes

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

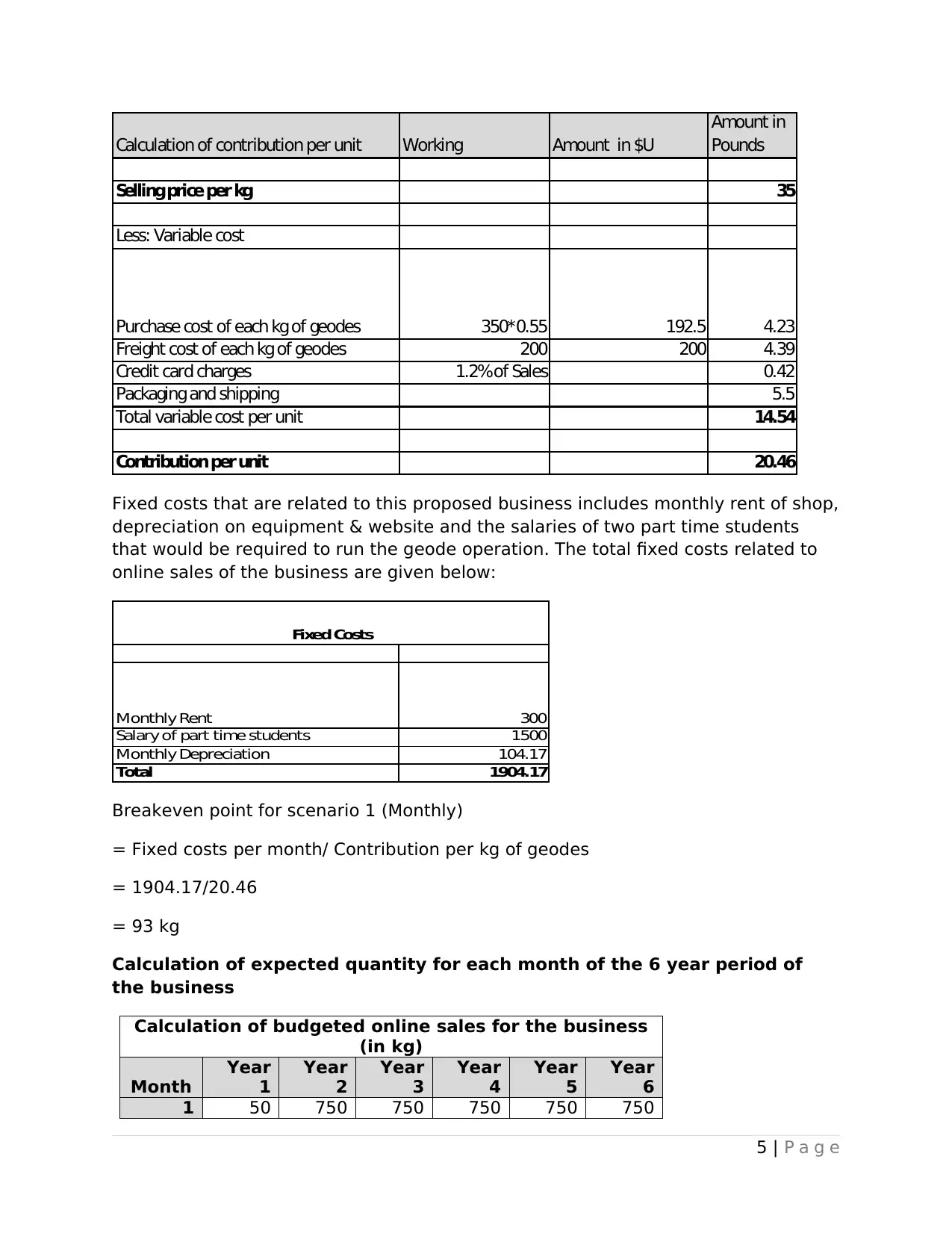

Calculation of contribution per unit Working Amount in $U

Amount in

Pounds

Sellingprice per kg 35

Less: Variable cost

Purchase cost of each kg of geodes 350*0.55 192.5 4.23

Freight cost of each kg of geodes 200 200 4.39

Credit card charges 1.2%of Sales 0.42

Packaging and shipping 5.5

Total variable cost per unit 14.54

Contribution per unit 20.46

Fixed costs that are related to this proposed business includes monthly rent of shop,

depreciation on equipment & website and the salaries of two part time students

that would be required to run the geode operation. The total fixed costs related to

online sales of the business are given below:

Monthly Rent 300

Salary of part time students 1500

Monthly Depreciation 104.17

Total 1904.17

Fixed Costs

Breakeven point for scenario 1 (Monthly)

= Fixed costs per month/ Contribution per kg of geodes

= 1904.17/20.46

= 93 kg

Calculation of expected quantity for each month of the 6 year period of

the business

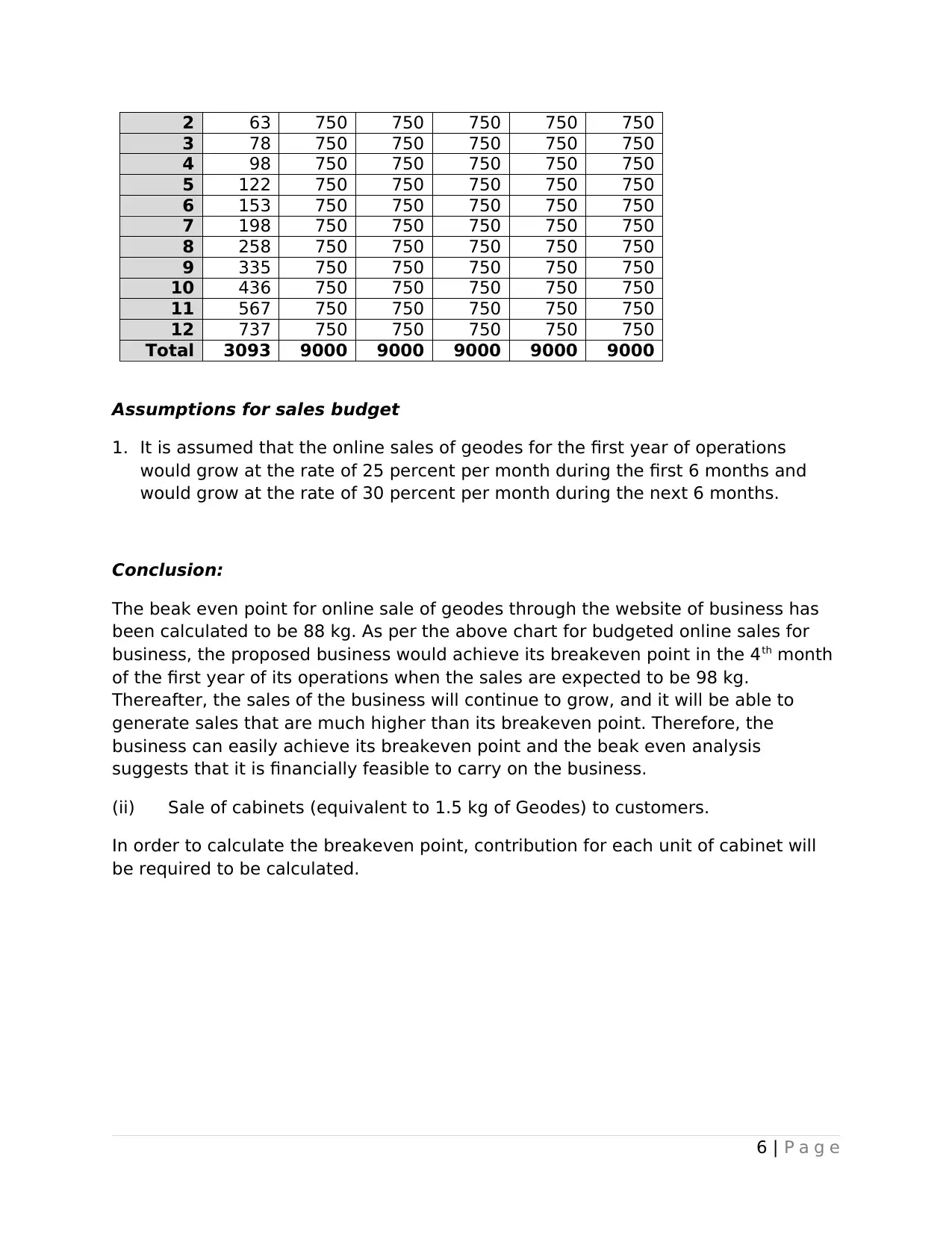

Calculation of budgeted online sales for the business

(in kg)

Month

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

1 50 750 750 750 750 750

5 | P a g e

Amount in

Pounds

Sellingprice per kg 35

Less: Variable cost

Purchase cost of each kg of geodes 350*0.55 192.5 4.23

Freight cost of each kg of geodes 200 200 4.39

Credit card charges 1.2%of Sales 0.42

Packaging and shipping 5.5

Total variable cost per unit 14.54

Contribution per unit 20.46

Fixed costs that are related to this proposed business includes monthly rent of shop,

depreciation on equipment & website and the salaries of two part time students

that would be required to run the geode operation. The total fixed costs related to

online sales of the business are given below:

Monthly Rent 300

Salary of part time students 1500

Monthly Depreciation 104.17

Total 1904.17

Fixed Costs

Breakeven point for scenario 1 (Monthly)

= Fixed costs per month/ Contribution per kg of geodes

= 1904.17/20.46

= 93 kg

Calculation of expected quantity for each month of the 6 year period of

the business

Calculation of budgeted online sales for the business

(in kg)

Month

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

1 50 750 750 750 750 750

5 | P a g e

2 63 750 750 750 750 750

3 78 750 750 750 750 750

4 98 750 750 750 750 750

5 122 750 750 750 750 750

6 153 750 750 750 750 750

7 198 750 750 750 750 750

8 258 750 750 750 750 750

9 335 750 750 750 750 750

10 436 750 750 750 750 750

11 567 750 750 750 750 750

12 737 750 750 750 750 750

Total 3093 9000 9000 9000 9000 9000

Assumptions for sales budget

1. It is assumed that the online sales of geodes for the first year of operations

would grow at the rate of 25 percent per month during the first 6 months and

would grow at the rate of 30 percent per month during the next 6 months.

Conclusion:

The beak even point for online sale of geodes through the website of business has

been calculated to be 88 kg. As per the above chart for budgeted online sales for

business, the proposed business would achieve its breakeven point in the 4th month

of the first year of its operations when the sales are expected to be 98 kg.

Thereafter, the sales of the business will continue to grow, and it will be able to

generate sales that are much higher than its breakeven point. Therefore, the

business can easily achieve its breakeven point and the beak even analysis

suggests that it is financially feasible to carry on the business.

(ii) Sale of cabinets (equivalent to 1.5 kg of Geodes) to customers.

In order to calculate the breakeven point, contribution for each unit of cabinet will

be required to be calculated.

6 | P a g e

3 78 750 750 750 750 750

4 98 750 750 750 750 750

5 122 750 750 750 750 750

6 153 750 750 750 750 750

7 198 750 750 750 750 750

8 258 750 750 750 750 750

9 335 750 750 750 750 750

10 436 750 750 750 750 750

11 567 750 750 750 750 750

12 737 750 750 750 750 750

Total 3093 9000 9000 9000 9000 9000

Assumptions for sales budget

1. It is assumed that the online sales of geodes for the first year of operations

would grow at the rate of 25 percent per month during the first 6 months and

would grow at the rate of 30 percent per month during the next 6 months.

Conclusion:

The beak even point for online sale of geodes through the website of business has

been calculated to be 88 kg. As per the above chart for budgeted online sales for

business, the proposed business would achieve its breakeven point in the 4th month

of the first year of its operations when the sales are expected to be 98 kg.

Thereafter, the sales of the business will continue to grow, and it will be able to

generate sales that are much higher than its breakeven point. Therefore, the

business can easily achieve its breakeven point and the beak even analysis

suggests that it is financially feasible to carry on the business.

(ii) Sale of cabinets (equivalent to 1.5 kg of Geodes) to customers.

In order to calculate the breakeven point, contribution for each unit of cabinet will

be required to be calculated.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

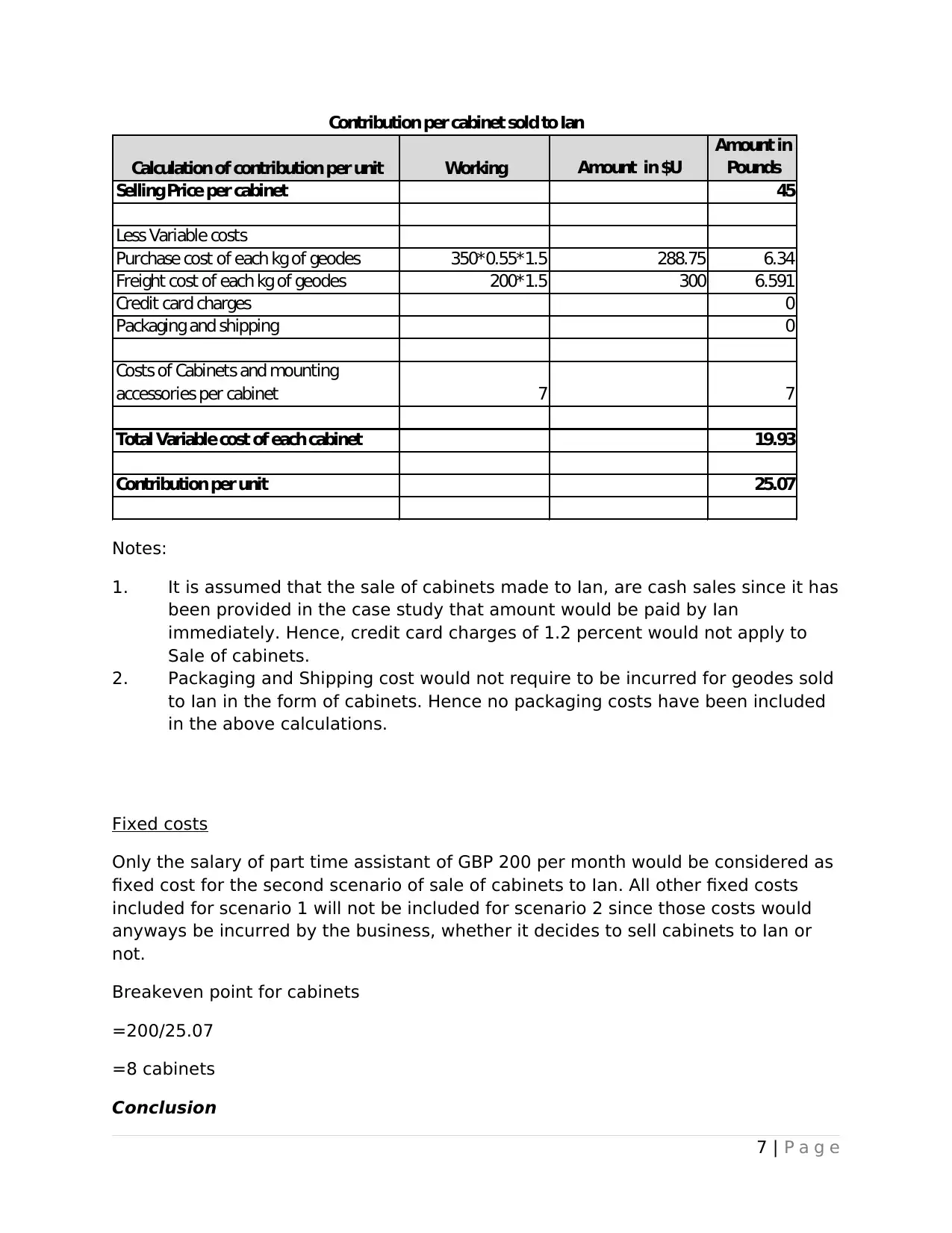

Calculation of contribution per unit Working Amount in $U

Amount in

Pounds

SellingPrice per cabinet 45

Less Variable costs

Purchase cost of each kg of geodes 350*0.55*1.5 288.75 6.34

Freight cost of each kg of geodes 200*1.5 300 6.591

Credit card charges 0

Packaging and shipping 0

Costs of Cabinets and mounting

accessories per cabinet 7 7

Total Variable cost of each cabinet 19.93

Contribution per unit 25.07

Contribution per cabinet sold to Ian

Notes:

1. It is assumed that the sale of cabinets made to Ian, are cash sales since it has

been provided in the case study that amount would be paid by Ian

immediately. Hence, credit card charges of 1.2 percent would not apply to

Sale of cabinets.

2. Packaging and Shipping cost would not require to be incurred for geodes sold

to Ian in the form of cabinets. Hence no packaging costs have been included

in the above calculations.

Fixed costs

Only the salary of part time assistant of GBP 200 per month would be considered as

fixed cost for the second scenario of sale of cabinets to Ian. All other fixed costs

included for scenario 1 will not be included for scenario 2 since those costs would

anyways be incurred by the business, whether it decides to sell cabinets to Ian or

not.

Breakeven point for cabinets

=200/25.07

=8 cabinets

Conclusion

7 | P a g e

Amount in

Pounds

SellingPrice per cabinet 45

Less Variable costs

Purchase cost of each kg of geodes 350*0.55*1.5 288.75 6.34

Freight cost of each kg of geodes 200*1.5 300 6.591

Credit card charges 0

Packaging and shipping 0

Costs of Cabinets and mounting

accessories per cabinet 7 7

Total Variable cost of each cabinet 19.93

Contribution per unit 25.07

Contribution per cabinet sold to Ian

Notes:

1. It is assumed that the sale of cabinets made to Ian, are cash sales since it has

been provided in the case study that amount would be paid by Ian

immediately. Hence, credit card charges of 1.2 percent would not apply to

Sale of cabinets.

2. Packaging and Shipping cost would not require to be incurred for geodes sold

to Ian in the form of cabinets. Hence no packaging costs have been included

in the above calculations.

Fixed costs

Only the salary of part time assistant of GBP 200 per month would be considered as

fixed cost for the second scenario of sale of cabinets to Ian. All other fixed costs

included for scenario 1 will not be included for scenario 2 since those costs would

anyways be incurred by the business, whether it decides to sell cabinets to Ian or

not.

Breakeven point for cabinets

=200/25.07

=8 cabinets

Conclusion

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The breakeven point for cabinets is 8, which means that Hattie must sale at least 8

cabinets every month so as to reach a situation of no profit, no loss. However, as

Ian would purchase only 6 Cabinets every month, Hattie will only be able to sell 6

cabinets every month. Also, the demand for cabinets from Ian will continue to

remain the same for all the months for the six year period of the business, i.e.

Hattie will be able to sell only 6 units for every month in which the business will be

operating. If the business achieves less sales than its breakeven point, the business

would lead to financial losses for its owner. Therefore, it is clearly evident that the

business proposal of sale of cabinets to Ian will not be able to reach the breakeven

point and hence, it would not be feasible for Hattie to go ahead will this proposal of

sale of cabinets to Ian, as she would not be able to reach the beak even point and it

would lead her to suffer financial losses.

Note: The conversion of amounts from UYU to GBP has been done based on the

exchange rate of prevailing on 09.10.2019. (XE Currency Converter, 2019).

Exchange rate

1 UYU 0.02197 GBP

(Exchange rate as on 9/10/2019)

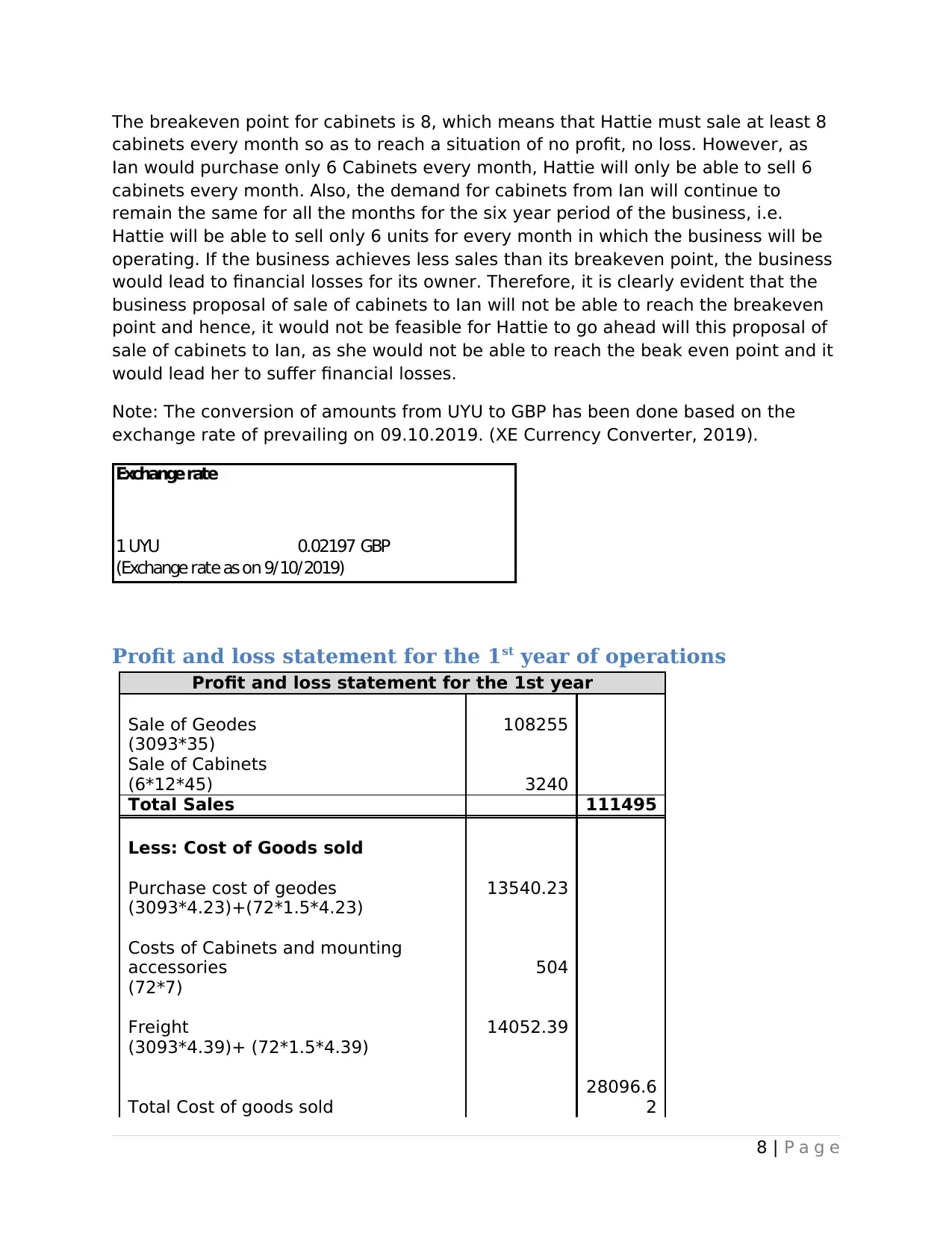

Profit and loss statement for the 1st year of operations

Profit and loss statement for the 1st year

Sale of Geodes 108255

(3093*35)

Sale of Cabinets

(6*12*45) 3240

Total Sales 111495

Less: Cost of Goods sold

Purchase cost of geodes 13540.23

(3093*4.23)+(72*1.5*4.23)

Costs of Cabinets and mounting

accessories 504

(72*7)

Freight 14052.39

(3093*4.39)+ (72*1.5*4.39)

Total Cost of goods sold

28096.6

2

8 | P a g e

cabinets every month so as to reach a situation of no profit, no loss. However, as

Ian would purchase only 6 Cabinets every month, Hattie will only be able to sell 6

cabinets every month. Also, the demand for cabinets from Ian will continue to

remain the same for all the months for the six year period of the business, i.e.

Hattie will be able to sell only 6 units for every month in which the business will be

operating. If the business achieves less sales than its breakeven point, the business

would lead to financial losses for its owner. Therefore, it is clearly evident that the

business proposal of sale of cabinets to Ian will not be able to reach the breakeven

point and hence, it would not be feasible for Hattie to go ahead will this proposal of

sale of cabinets to Ian, as she would not be able to reach the beak even point and it

would lead her to suffer financial losses.

Note: The conversion of amounts from UYU to GBP has been done based on the

exchange rate of prevailing on 09.10.2019. (XE Currency Converter, 2019).

Exchange rate

1 UYU 0.02197 GBP

(Exchange rate as on 9/10/2019)

Profit and loss statement for the 1st year of operations

Profit and loss statement for the 1st year

Sale of Geodes 108255

(3093*35)

Sale of Cabinets

(6*12*45) 3240

Total Sales 111495

Less: Cost of Goods sold

Purchase cost of geodes 13540.23

(3093*4.23)+(72*1.5*4.23)

Costs of Cabinets and mounting

accessories 504

(72*7)

Freight 14052.39

(3093*4.39)+ (72*1.5*4.39)

Total Cost of goods sold

28096.6

2

8 | P a g e

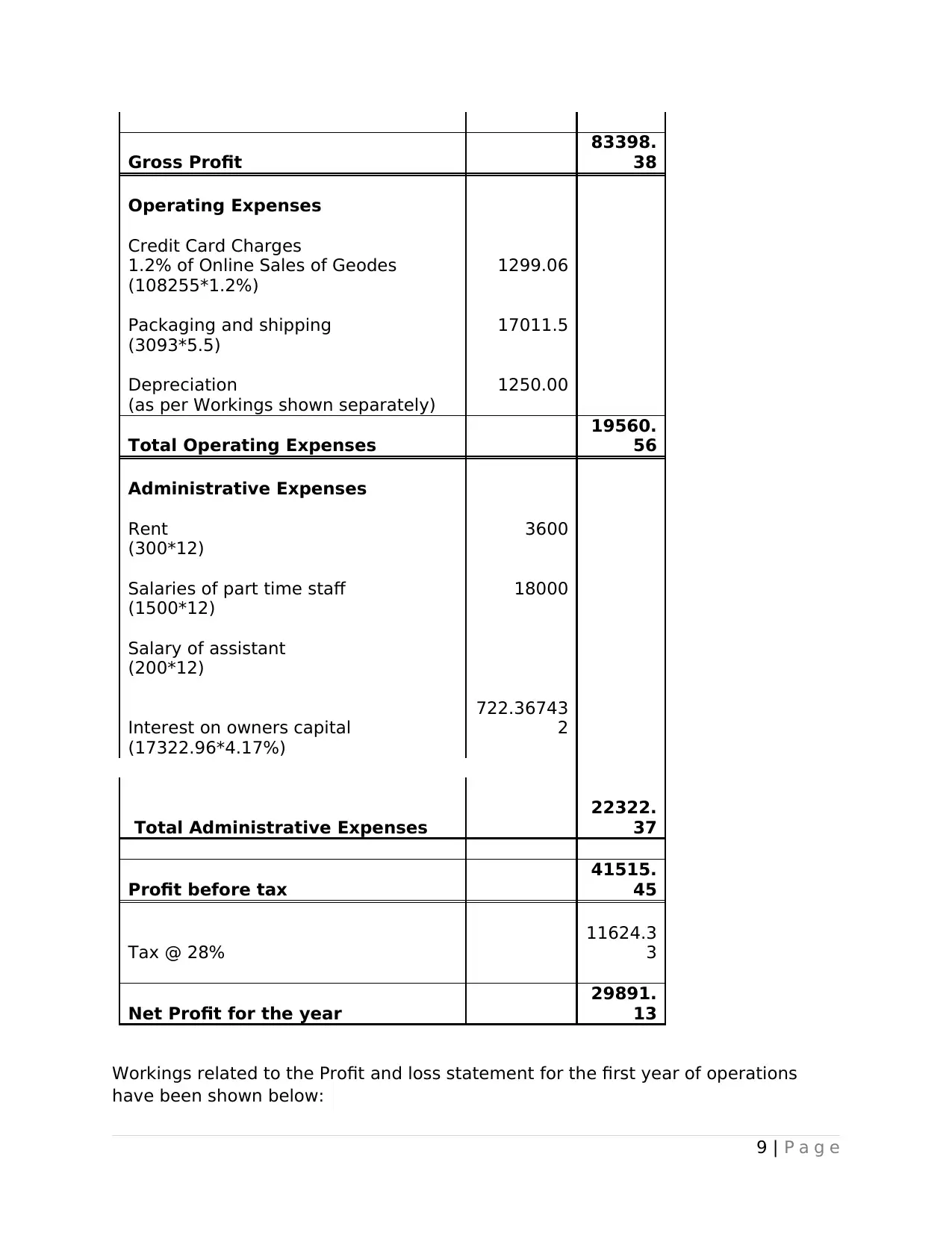

Gross Profit

83398.

38

Operating Expenses

Credit Card Charges

1.2% of Online Sales of Geodes 1299.06

(108255*1.2%)

Packaging and shipping 17011.5

(3093*5.5)

Depreciation 1250.00

(as per Workings shown separately)

Total Operating Expenses

19560.

56

Administrative Expenses

Rent 3600

(300*12)

Salaries of part time staff 18000

(1500*12)

Salary of assistant

(200*12)

Interest on owners capital

722.36743

2

(17322.96*4.17%)

Total Administrative Expenses

22322.

37

Profit before tax

41515.

45

Tax @ 28%

11624.3

3

Net Profit for the year

29891.

13

Workings related to the Profit and loss statement for the first year of operations

have been shown below:

9 | P a g e

83398.

38

Operating Expenses

Credit Card Charges

1.2% of Online Sales of Geodes 1299.06

(108255*1.2%)

Packaging and shipping 17011.5

(3093*5.5)

Depreciation 1250.00

(as per Workings shown separately)

Total Operating Expenses

19560.

56

Administrative Expenses

Rent 3600

(300*12)

Salaries of part time staff 18000

(1500*12)

Salary of assistant

(200*12)

Interest on owners capital

722.36743

2

(17322.96*4.17%)

Total Administrative Expenses

22322.

37

Profit before tax

41515.

45

Tax @ 28%

11624.3

3

Net Profit for the year

29891.

13

Workings related to the Profit and loss statement for the first year of operations

have been shown below:

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

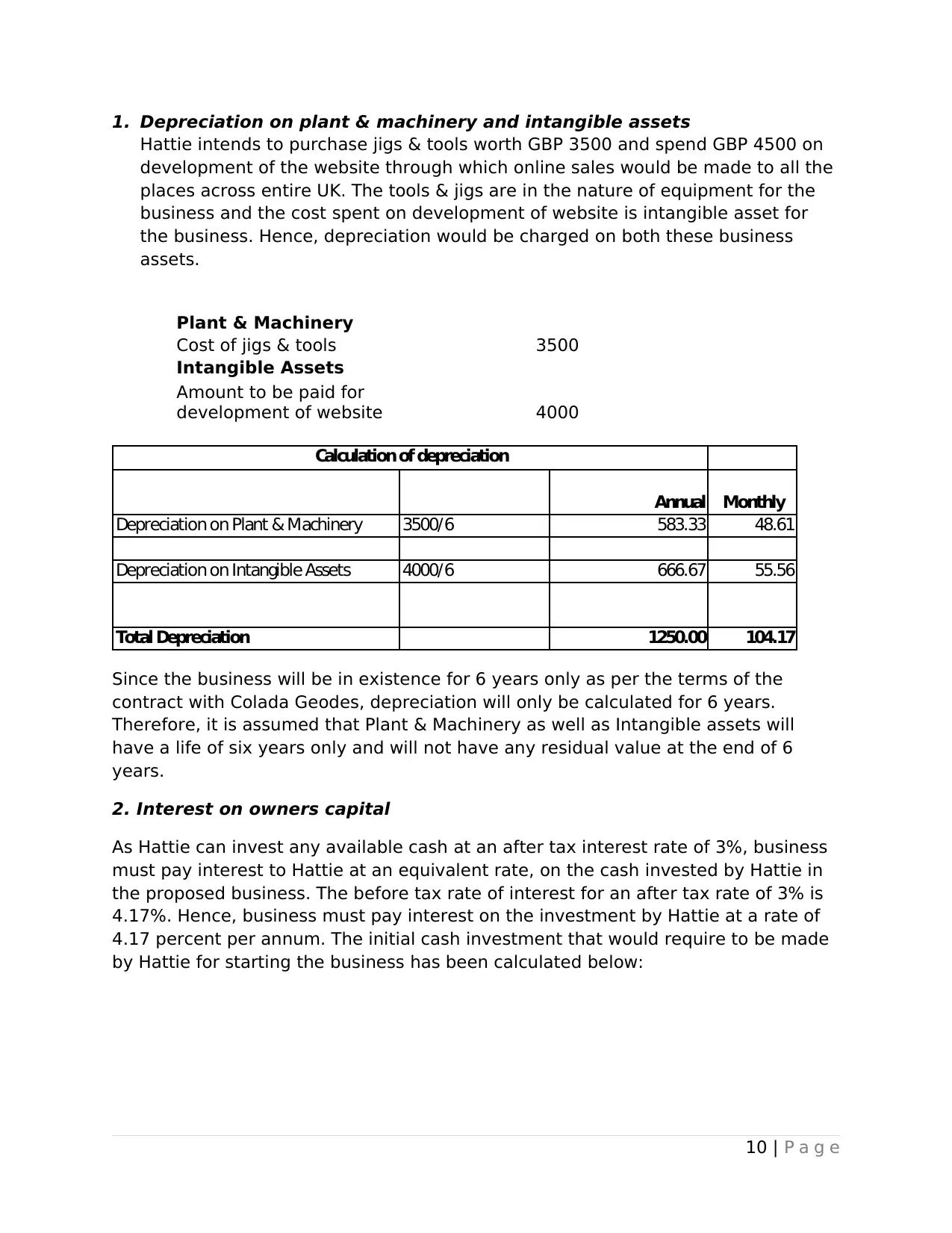

1. Depreciation on plant & machinery and intangible assets

Hattie intends to purchase jigs & tools worth GBP 3500 and spend GBP 4500 on

development of the website through which online sales would be made to all the

places across entire UK. The tools & jigs are in the nature of equipment for the

business and the cost spent on development of website is intangible asset for

the business. Hence, depreciation would be charged on both these business

assets.

Plant & Machinery

Cost of jigs & tools 3500

Intangible Assets

Amount to be paid for

development of website 4000

Annual Monthly

Depreciation on Plant & Machinery 3500/6 583.33 48.61

Depreciation on Intangible Assets 4000/6 666.67 55.56

Total Depreciation 1250.00 104.17

Calculation of depreciation

Since the business will be in existence for 6 years only as per the terms of the

contract with Colada Geodes, depreciation will only be calculated for 6 years.

Therefore, it is assumed that Plant & Machinery as well as Intangible assets will

have a life of six years only and will not have any residual value at the end of 6

years.

2. Interest on owners capital

As Hattie can invest any available cash at an after tax interest rate of 3%, business

must pay interest to Hattie at an equivalent rate, on the cash invested by Hattie in

the proposed business. The before tax rate of interest for an after tax rate of 3% is

4.17%. Hence, business must pay interest on the investment by Hattie at a rate of

4.17 percent per annum. The initial cash investment that would require to be made

by Hattie for starting the business has been calculated below:

10 | P a g e

Hattie intends to purchase jigs & tools worth GBP 3500 and spend GBP 4500 on

development of the website through which online sales would be made to all the

places across entire UK. The tools & jigs are in the nature of equipment for the

business and the cost spent on development of website is intangible asset for

the business. Hence, depreciation would be charged on both these business

assets.

Plant & Machinery

Cost of jigs & tools 3500

Intangible Assets

Amount to be paid for

development of website 4000

Annual Monthly

Depreciation on Plant & Machinery 3500/6 583.33 48.61

Depreciation on Intangible Assets 4000/6 666.67 55.56

Total Depreciation 1250.00 104.17

Calculation of depreciation

Since the business will be in existence for 6 years only as per the terms of the

contract with Colada Geodes, depreciation will only be calculated for 6 years.

Therefore, it is assumed that Plant & Machinery as well as Intangible assets will

have a life of six years only and will not have any residual value at the end of 6

years.

2. Interest on owners capital

As Hattie can invest any available cash at an after tax interest rate of 3%, business

must pay interest to Hattie at an equivalent rate, on the cash invested by Hattie in

the proposed business. The before tax rate of interest for an after tax rate of 3% is

4.17%. Hence, business must pay interest on the investment by Hattie at a rate of

4.17 percent per annum. The initial cash investment that would require to be made

by Hattie for starting the business has been calculated below:

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

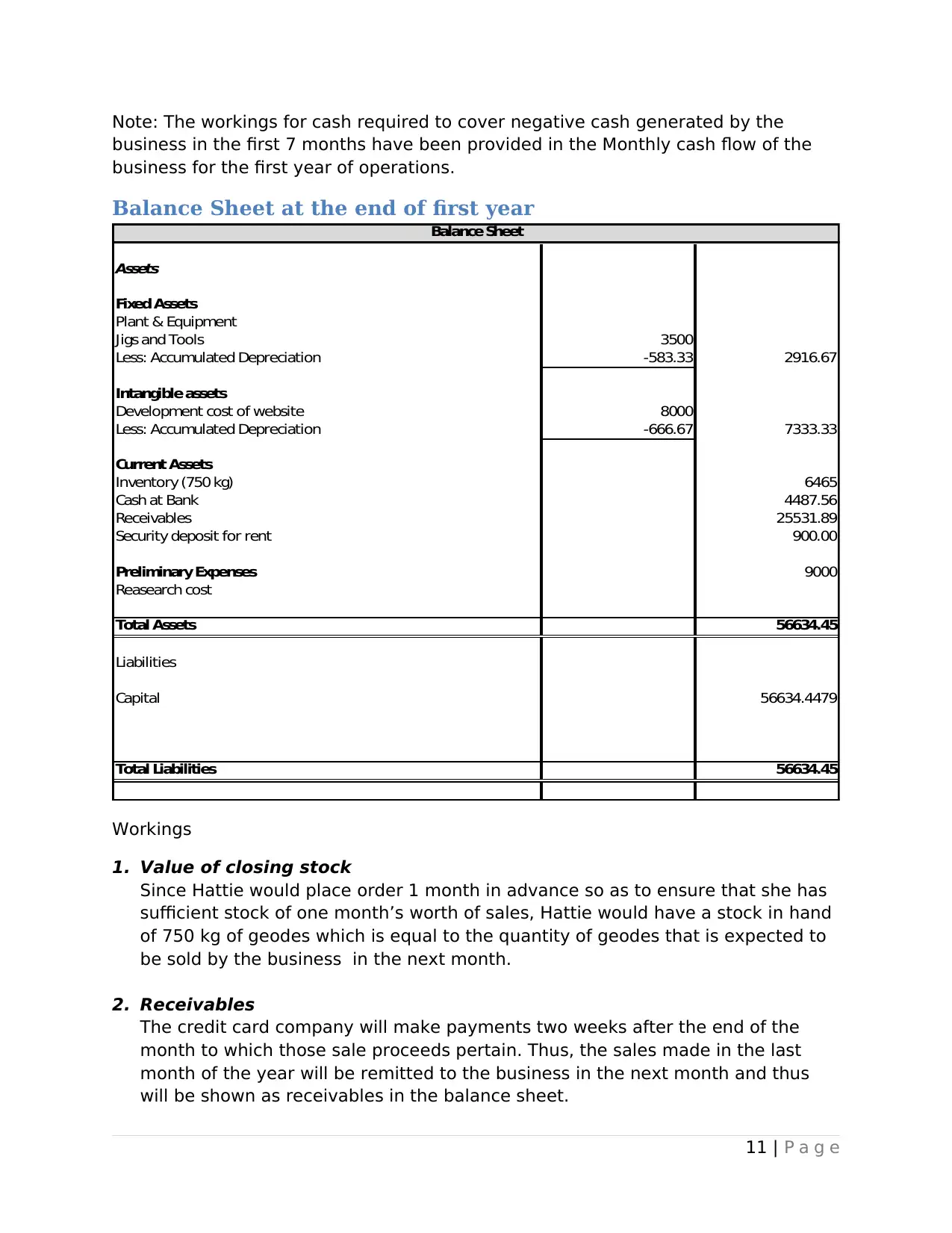

Note: The workings for cash required to cover negative cash generated by the

business in the first 7 months have been provided in the Monthly cash flow of the

business for the first year of operations.

Balance Sheet at the end of first year

Assets

Fixed Assets

Plant & Equipment

Jigs and Tools 3500

Less: Accumulated Depreciation -583.33 2916.67

Intangible assets

Development cost of website 8000

Less: Accumulated Depreciation -666.67 7333.33

Current Assets

Inventory (750 kg) 6465

Cash at Bank 4487.56

Receivables 25531.89

Security deposit for rent 900.00

Preliminary Expenses 9000

Reasearch cost

Total Assets 56634.45

Liabilities

Capital 56634.4479

Total Liabilities 56634.45

Balance Sheet

Workings

1. Value of closing stock

Since Hattie would place order 1 month in advance so as to ensure that she has

sufficient stock of one month’s worth of sales, Hattie would have a stock in hand

of 750 kg of geodes which is equal to the quantity of geodes that is expected to

be sold by the business in the next month.

2. Receivables

The credit card company will make payments two weeks after the end of the

month to which those sale proceeds pertain. Thus, the sales made in the last

month of the year will be remitted to the business in the next month and thus

will be shown as receivables in the balance sheet.

11 | P a g e

business in the first 7 months have been provided in the Monthly cash flow of the

business for the first year of operations.

Balance Sheet at the end of first year

Assets

Fixed Assets

Plant & Equipment

Jigs and Tools 3500

Less: Accumulated Depreciation -583.33 2916.67

Intangible assets

Development cost of website 8000

Less: Accumulated Depreciation -666.67 7333.33

Current Assets

Inventory (750 kg) 6465

Cash at Bank 4487.56

Receivables 25531.89

Security deposit for rent 900.00

Preliminary Expenses 9000

Reasearch cost

Total Assets 56634.45

Liabilities

Capital 56634.4479

Total Liabilities 56634.45

Balance Sheet

Workings

1. Value of closing stock

Since Hattie would place order 1 month in advance so as to ensure that she has

sufficient stock of one month’s worth of sales, Hattie would have a stock in hand

of 750 kg of geodes which is equal to the quantity of geodes that is expected to

be sold by the business in the next month.

2. Receivables

The credit card company will make payments two weeks after the end of the

month to which those sale proceeds pertain. Thus, the sales made in the last

month of the year will be remitted to the business in the next month and thus

will be shown as receivables in the balance sheet.

11 | P a g e

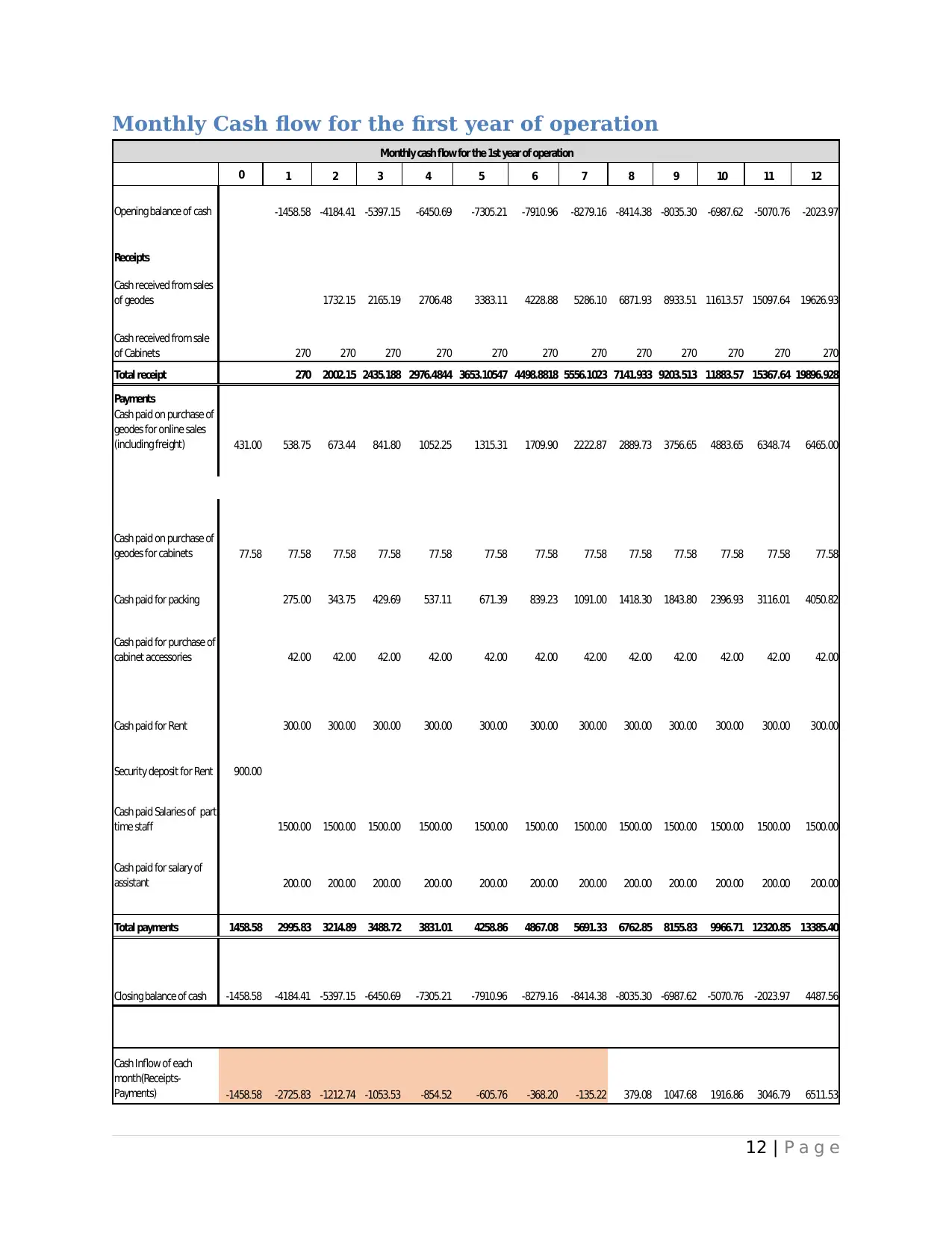

Monthly Cash flow for the first year of operation

0 1 2 3 4 5 6 7 8 9 10 11 12

Opening balance of cash -1458.58 -4184.41 -5397.15 -6450.69 -7305.21 -7910.96 -8279.16 -8414.38 -8035.30 -6987.62 -5070.76 -2023.97

Receipts

Cash received from sales

of geodes 1732.15 2165.19 2706.48 3383.11 4228.88 5286.10 6871.93 8933.51 11613.57 15097.64 19626.93

Cash received from sale

of Cabinets 270 270 270 270 270 270 270 270 270 270 270 270

Total receipt 270 2002.15 2435.188 2976.4844 3653.10547 4498.8818 5556.1023 7141.933 9203.513 11883.57 15367.64 19896.928

Payments

Cash paid on purchase of

geodes for online sales

(including freight) 431.00 538.75 673.44 841.80 1052.25 1315.31 1709.90 2222.87 2889.73 3756.65 4883.65 6348.74 6465.00

50.00 62.50 78.13 97.66 122.07 152.59 198.36 257.87 335.24 435.81 566.55 736.51 750.00

Cash paid on purchase of

geodes for cabinets 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58

Cash paid for packing 275.00 343.75 429.69 537.11 671.39 839.23 1091.00 1418.30 1843.80 2396.93 3116.01 4050.82

Cash paid for purchase of

cabinet accessories 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00

Cash paid for Rent 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00

Security deposit for Rent 900.00

Cash paid Salaries of part

time staff 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00

Cash paid for salary of

assistant 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00

Total payments 1458.58 2995.83 3214.89 3488.72 3831.01 4258.86 4867.08 5691.33 6762.85 8155.83 9966.71 12320.85 13385.40

Closing balance of cash -1458.58 -4184.41 -5397.15 -6450.69 -7305.21 -7910.96 -8279.16 -8414.38 -8035.30 -6987.62 -5070.76 -2023.97 4487.56

Cash Inflow of each

month(Receipts-

Payments) -1458.58 -2725.83 -1212.74 -1053.53 -854.52 -605.76 -368.20 -135.22 379.08 1047.68 1916.86 3046.79 6511.53

Monthly cash flow for the 1st year of operation

12 | P a g e

0 1 2 3 4 5 6 7 8 9 10 11 12

Opening balance of cash -1458.58 -4184.41 -5397.15 -6450.69 -7305.21 -7910.96 -8279.16 -8414.38 -8035.30 -6987.62 -5070.76 -2023.97

Receipts

Cash received from sales

of geodes 1732.15 2165.19 2706.48 3383.11 4228.88 5286.10 6871.93 8933.51 11613.57 15097.64 19626.93

Cash received from sale

of Cabinets 270 270 270 270 270 270 270 270 270 270 270 270

Total receipt 270 2002.15 2435.188 2976.4844 3653.10547 4498.8818 5556.1023 7141.933 9203.513 11883.57 15367.64 19896.928

Payments

Cash paid on purchase of

geodes for online sales

(including freight) 431.00 538.75 673.44 841.80 1052.25 1315.31 1709.90 2222.87 2889.73 3756.65 4883.65 6348.74 6465.00

50.00 62.50 78.13 97.66 122.07 152.59 198.36 257.87 335.24 435.81 566.55 736.51 750.00

Cash paid on purchase of

geodes for cabinets 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58 77.58

Cash paid for packing 275.00 343.75 429.69 537.11 671.39 839.23 1091.00 1418.30 1843.80 2396.93 3116.01 4050.82

Cash paid for purchase of

cabinet accessories 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00 42.00

Cash paid for Rent 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00 300.00

Security deposit for Rent 900.00

Cash paid Salaries of part

time staff 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00 1500.00

Cash paid for salary of

assistant 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00 200.00

Total payments 1458.58 2995.83 3214.89 3488.72 3831.01 4258.86 4867.08 5691.33 6762.85 8155.83 9966.71 12320.85 13385.40

Closing balance of cash -1458.58 -4184.41 -5397.15 -6450.69 -7305.21 -7910.96 -8279.16 -8414.38 -8035.30 -6987.62 -5070.76 -2023.97 4487.56

Cash Inflow of each

month(Receipts-

Payments) -1458.58 -2725.83 -1212.74 -1053.53 -854.52 -605.76 -368.20 -135.22 379.08 1047.68 1916.86 3046.79 6511.53

Monthly cash flow for the 1st year of operation

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.