Managerial Finance: Financial Ratio Analysis of GSK and RB Group

VerifiedAdded on 2023/01/17

|20

|4050

|97

Report

AI Summary

This managerial finance report presents a comparative financial analysis of Glaxo Smith Kline plc (GSK) and Reckitt Benckiser Group plc (RBG), focusing on their financial performance, position, and investment potential. The report calculates and analyzes various financial ratios, including current, quick, net profit margin, gross profit margin, gearing, P/E, EPS, ROCE, inventory turnover, and dividend payout ratios for the years 2017 and 2018. The analysis assesses the short-term liquidity, profitability, efficiency, and solvency of both companies, highlighting their strengths and weaknesses. The report offers recommendations for improving the financial performance of the underperforming business and discusses the limitations of using financial ratios and investment appraisal techniques. The objective is to provide investors with insights to make informed decisions regarding investment viability, contributing to the broader understanding of corporate finance principles.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a) Calculation of different financial ratios for two years (2017 – 2018):..................................3

(b) Analyse the performance, financial position and investment potential of both companies:. 7

(c). Recommendations of how the financial performance of the poorly performing business

can be improved:.......................................................................................................................12

(d) Limitations of financial ratios:............................................................................................12

TASK 2..........................................................................................................................................13

(a). Calculation of financial ratios for two years (2017 - 2018):..............................................13

(b) Limitations of using investment appraisal techniques:.......................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a) Calculation of different financial ratios for two years (2017 – 2018):..................................3

(b) Analyse the performance, financial position and investment potential of both companies:. 7

(c). Recommendations of how the financial performance of the poorly performing business

can be improved:.......................................................................................................................12

(d) Limitations of financial ratios:............................................................................................12

TASK 2..........................................................................................................................................13

(a). Calculation of financial ratios for two years (2017 - 2018):..............................................13

(b) Limitations of using investment appraisal techniques:.......................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

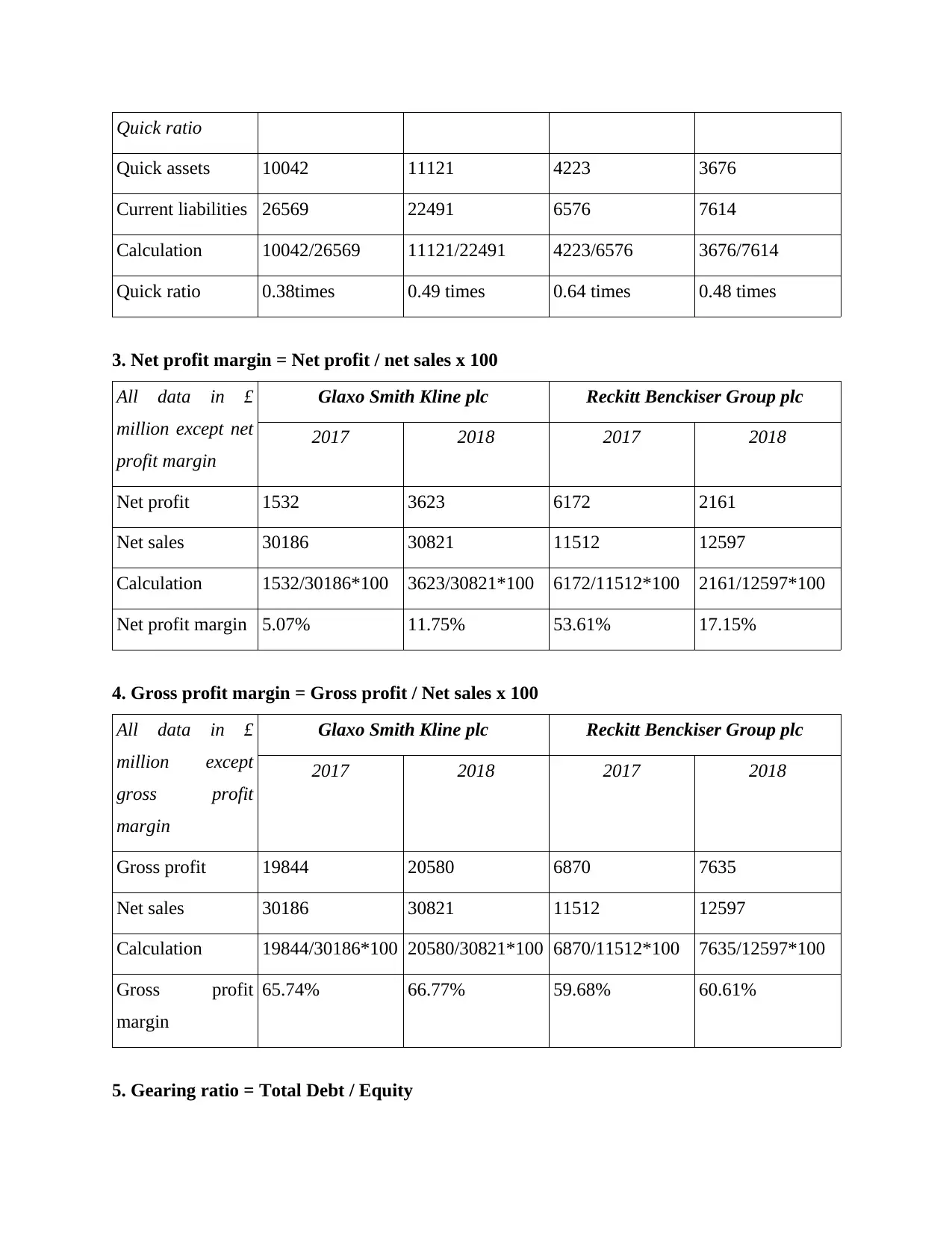

INTRODUCTION

Managerial finance is a type of finance, also classified as corporate finance. This is

aligned with the financial considerations taken on the basis of the financial framework in the

businesses. To order to perform all forms of roles and tasks, it becomes necessary for executives

to take reasonable steps with regard to financial management. The project study is focused on a

contrast between the financial state of company Glaxo Smith Kline plc and company Reckitt

Benckiser Group plc. The British international drug/pharmaceutical manufacturer Glaxo Smith

Kline plc is situated in Brentford, England (About Glaxo Smith Kline plc, 2019). Whereas

Reckitt Benckiser plc is UK's international consumer-goods organization and company has

headquarter in Slough, England. This is a manufacturer of hygiene, health-care and home-

products (About Reckitt Benckiser Group plc, 2019). The objective of this project study is to

support investors in decision-making regrading which company is more viable for investment

purpose. This study further contains computations of different investment-appraisal techniques

and limitations of these techniques in relation to long term decisions making.

TASK 1

(a) Calculation of different financial ratios for two years (2017 – 2018):

1. Current ratio = Current assets / Current liabilities

All data in £

million except

current ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Current assets 15907 16927 5424 4952

Current liabilities 26569 22491 6576 7614

Calculation 15907/26569 16927/22491 5424/6576 4952/7614

Current ratio 0.60 times 0.75 times 0.82 times 0.65 times

2. Quick ratio = Quick assets / Current liabilities

All data in £

million except

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Managerial finance is a type of finance, also classified as corporate finance. This is

aligned with the financial considerations taken on the basis of the financial framework in the

businesses. To order to perform all forms of roles and tasks, it becomes necessary for executives

to take reasonable steps with regard to financial management. The project study is focused on a

contrast between the financial state of company Glaxo Smith Kline plc and company Reckitt

Benckiser Group plc. The British international drug/pharmaceutical manufacturer Glaxo Smith

Kline plc is situated in Brentford, England (About Glaxo Smith Kline plc, 2019). Whereas

Reckitt Benckiser plc is UK's international consumer-goods organization and company has

headquarter in Slough, England. This is a manufacturer of hygiene, health-care and home-

products (About Reckitt Benckiser Group plc, 2019). The objective of this project study is to

support investors in decision-making regrading which company is more viable for investment

purpose. This study further contains computations of different investment-appraisal techniques

and limitations of these techniques in relation to long term decisions making.

TASK 1

(a) Calculation of different financial ratios for two years (2017 – 2018):

1. Current ratio = Current assets / Current liabilities

All data in £

million except

current ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Current assets 15907 16927 5424 4952

Current liabilities 26569 22491 6576 7614

Calculation 15907/26569 16927/22491 5424/6576 4952/7614

Current ratio 0.60 times 0.75 times 0.82 times 0.65 times

2. Quick ratio = Quick assets / Current liabilities

All data in £

million except

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick ratio

Quick assets 10042 11121 4223 3676

Current liabilities 26569 22491 6576 7614

Calculation 10042/26569 11121/22491 4223/6576 3676/7614

Quick ratio 0.38times 0.49 times 0.64 times 0.48 times

3. Net profit margin = Net profit / net sales x 100

All data in £

million except net

profit margin

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net profit 1532 3623 6172 2161

Net sales 30186 30821 11512 12597

Calculation 1532/30186*100 3623/30821*100 6172/11512*100 2161/12597*100

Net profit margin 5.07% 11.75% 53.61% 17.15%

4. Gross profit margin = Gross profit / Net sales x 100

All data in £

million except

gross profit

margin

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Gross profit 19844 20580 6870 7635

Net sales 30186 30821 11512 12597

Calculation 19844/30186*100 20580/30821*100 6870/11512*100 7635/12597*100

Gross profit

margin

65.74% 66.77% 59.68% 60.61%

5. Gearing ratio = Total Debt / Equity

Quick assets 10042 11121 4223 3676

Current liabilities 26569 22491 6576 7614

Calculation 10042/26569 11121/22491 4223/6576 3676/7614

Quick ratio 0.38times 0.49 times 0.64 times 0.48 times

3. Net profit margin = Net profit / net sales x 100

All data in £

million except net

profit margin

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net profit 1532 3623 6172 2161

Net sales 30186 30821 11512 12597

Calculation 1532/30186*100 3623/30821*100 6172/11512*100 2161/12597*100

Net profit margin 5.07% 11.75% 53.61% 17.15%

4. Gross profit margin = Gross profit / Net sales x 100

All data in £

million except

gross profit

margin

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Gross profit 19844 20580 6870 7635

Net sales 30186 30821 11512 12597

Calculation 19844/30186*100 20580/30821*100 6870/11512*100 7635/12597*100

Gross profit

margin

65.74% 66.77% 59.68% 60.61%

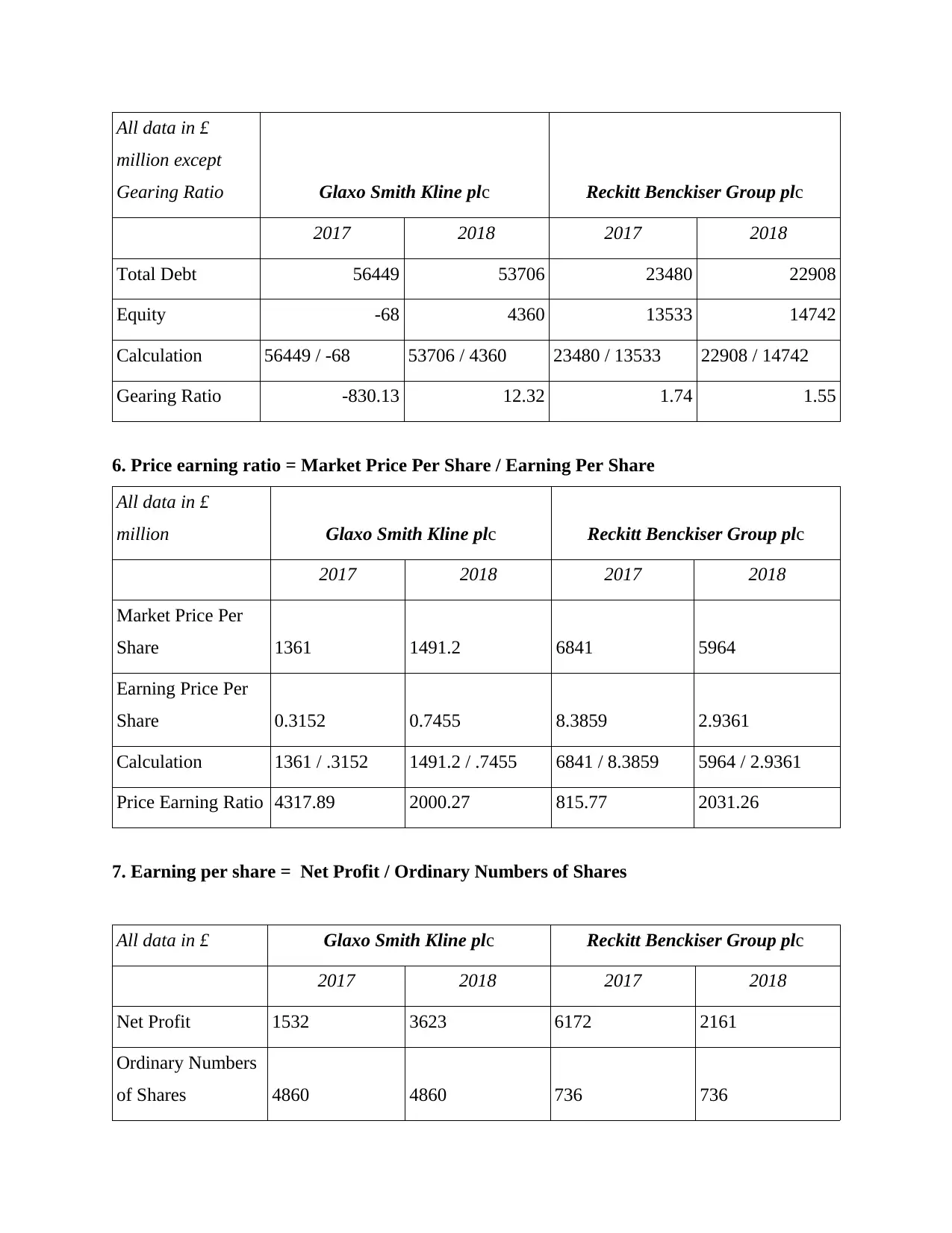

5. Gearing ratio = Total Debt / Equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All data in £

million except

Gearing Ratio Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total Debt 56449 53706 23480 22908

Equity -68 4360 13533 14742

Calculation 56449 / -68 53706 / 4360 23480 / 13533 22908 / 14742

Gearing Ratio -830.13 12.32 1.74 1.55

6. Price earning ratio = Market Price Per Share / Earning Per Share

All data in £

million Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Market Price Per

Share 1361 1491.2 6841 5964

Earning Price Per

Share 0.3152 0.7455 8.3859 2.9361

Calculation 1361 / .3152 1491.2 / .7455 6841 / 8.3859 5964 / 2.9361

Price Earning Ratio 4317.89 2000.27 815.77 2031.26

7. Earning per share = Net Profit / Ordinary Numbers of Shares

All data in £ Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net Profit 1532 3623 6172 2161

Ordinary Numbers

of Shares 4860 4860 736 736

million except

Gearing Ratio Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total Debt 56449 53706 23480 22908

Equity -68 4360 13533 14742

Calculation 56449 / -68 53706 / 4360 23480 / 13533 22908 / 14742

Gearing Ratio -830.13 12.32 1.74 1.55

6. Price earning ratio = Market Price Per Share / Earning Per Share

All data in £

million Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Market Price Per

Share 1361 1491.2 6841 5964

Earning Price Per

Share 0.3152 0.7455 8.3859 2.9361

Calculation 1361 / .3152 1491.2 / .7455 6841 / 8.3859 5964 / 2.9361

Price Earning Ratio 4317.89 2000.27 815.77 2031.26

7. Earning per share = Net Profit / Ordinary Numbers of Shares

All data in £ Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net Profit 1532 3623 6172 2161

Ordinary Numbers

of Shares 4860 4860 736 736

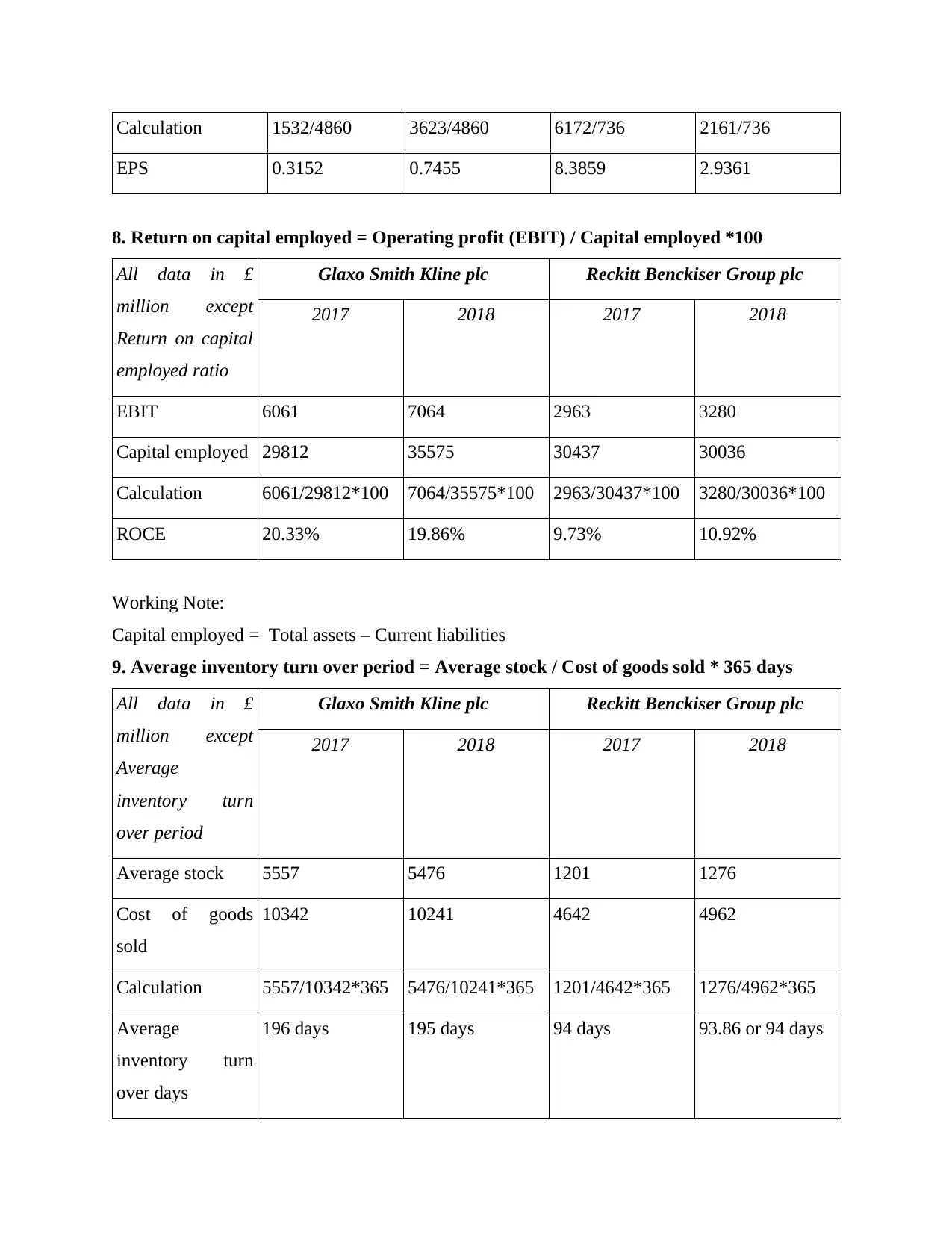

Calculation 1532/4860 3623/4860 6172/736 2161/736

EPS 0.3152 0.7455 8.3859 2.9361

8. Return on capital employed = Operating profit (EBIT) / Capital employed *100

All data in £

million except

Return on capital

employed ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

EBIT 6061 7064 2963 3280

Capital employed 29812 35575 30437 30036

Calculation 6061/29812*100 7064/35575*100 2963/30437*100 3280/30036*100

ROCE 20.33% 19.86% 9.73% 10.92%

Working Note:

Capital employed = Total assets – Current liabilities

9. Average inventory turn over period = Average stock / Cost of goods sold * 365 days

All data in £

million except

Average

inventory turn

over period

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Average stock 5557 5476 1201 1276

Cost of goods

sold

10342 10241 4642 4962

Calculation 5557/10342*365 5476/10241*365 1201/4642*365 1276/4962*365

Average

inventory turn

over days

196 days 195 days 94 days 93.86 or 94 days

EPS 0.3152 0.7455 8.3859 2.9361

8. Return on capital employed = Operating profit (EBIT) / Capital employed *100

All data in £

million except

Return on capital

employed ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

EBIT 6061 7064 2963 3280

Capital employed 29812 35575 30437 30036

Calculation 6061/29812*100 7064/35575*100 2963/30437*100 3280/30036*100

ROCE 20.33% 19.86% 9.73% 10.92%

Working Note:

Capital employed = Total assets – Current liabilities

9. Average inventory turn over period = Average stock / Cost of goods sold * 365 days

All data in £

million except

Average

inventory turn

over period

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Average stock 5557 5476 1201 1276

Cost of goods

sold

10342 10241 4642 4962

Calculation 5557/10342*365 5476/10241*365 1201/4642*365 1276/4962*365

Average

inventory turn

over days

196 days 195 days 94 days 93.86 or 94 days

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

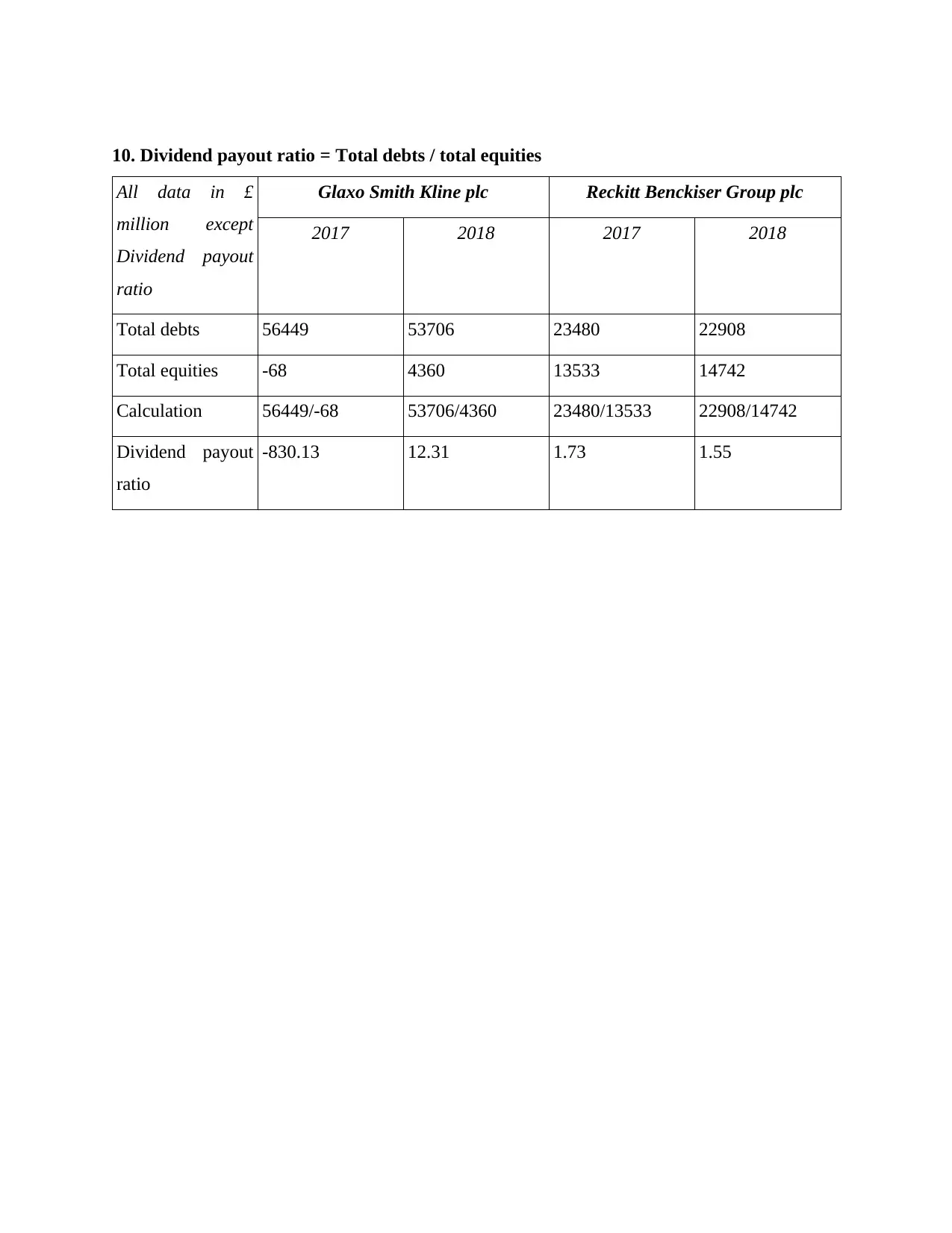

10. Dividend payout ratio = Total debts / total equities

All data in £

million except

Dividend payout

ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total debts 56449 53706 23480 22908

Total equities -68 4360 13533 14742

Calculation 56449/-68 53706/4360 23480/13533 22908/14742

Dividend payout

ratio

-830.13 12.31 1.73 1.55

All data in £

million except

Dividend payout

ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total debts 56449 53706 23480 22908

Total equities -68 4360 13533 14742

Calculation 56449/-68 53706/4360 23480/13533 22908/14742

Dividend payout

ratio

-830.13 12.31 1.73 1.55

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

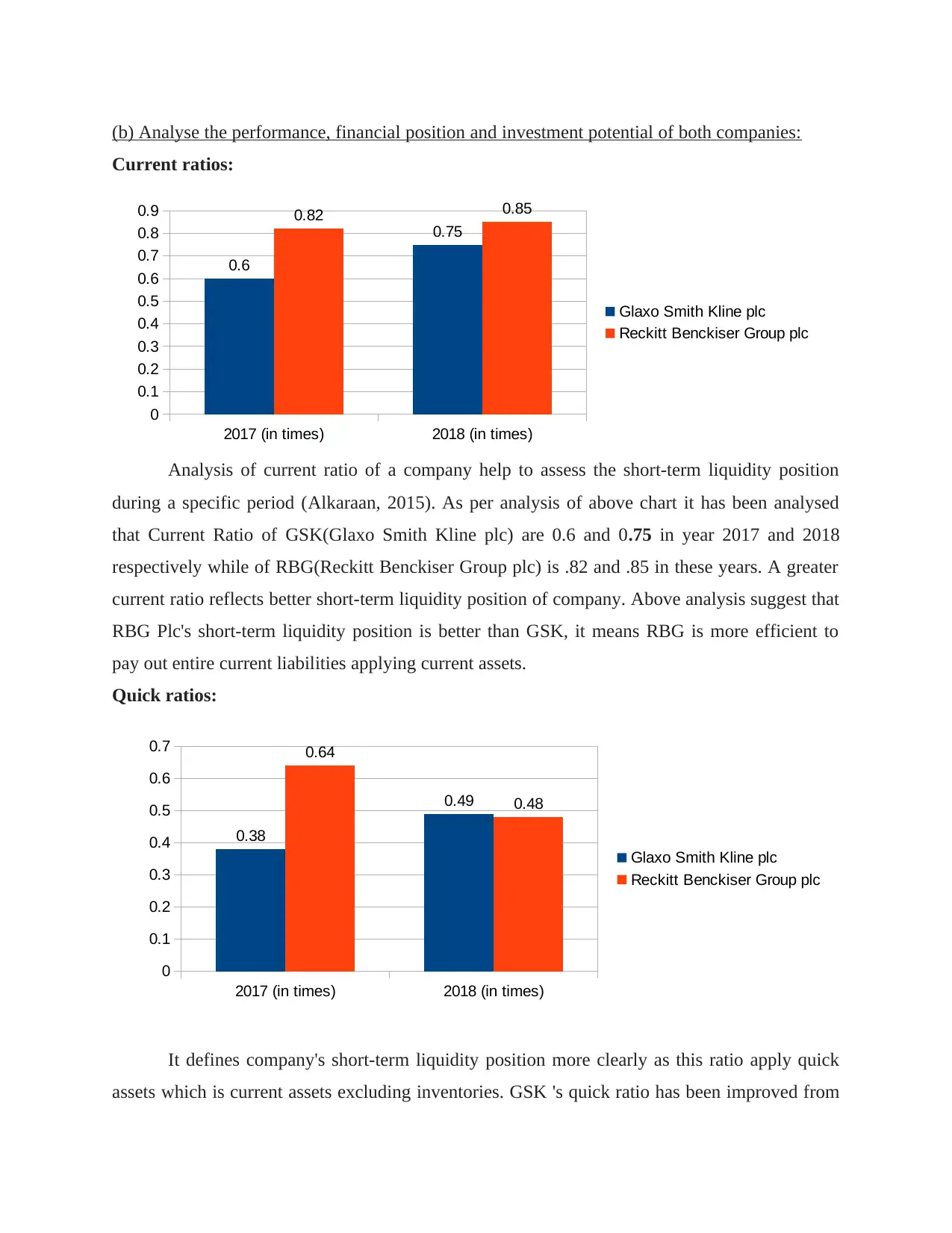

(b) Analyse the performance, financial position and investment potential of both companies:

Current ratios:

Analysis of current ratio of a company help to assess the short-term liquidity position

during a specific period (Alkaraan, 2015). As per analysis of above chart it has been analysed

that Current Ratio of GSK(Glaxo Smith Kline plc) are 0.6 and 0.75 in year 2017 and 2018

respectively while of RBG(Reckitt Benckiser Group plc) is .82 and .85 in these years. A greater

current ratio reflects better short-term liquidity position of company. Above analysis suggest that

RBG Plc's short-term liquidity position is better than GSK, it means RBG is more efficient to

pay out entire current liabilities applying current assets.

Quick ratios:

It defines company's short-term liquidity position more clearly as this ratio apply quick

assets which is current assets excluding inventories. GSK 's quick ratio has been improved from

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.6

0.75

0.82 0.85

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.38

0.49

0.64

0.48

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Current ratios:

Analysis of current ratio of a company help to assess the short-term liquidity position

during a specific period (Alkaraan, 2015). As per analysis of above chart it has been analysed

that Current Ratio of GSK(Glaxo Smith Kline plc) are 0.6 and 0.75 in year 2017 and 2018

respectively while of RBG(Reckitt Benckiser Group plc) is .82 and .85 in these years. A greater

current ratio reflects better short-term liquidity position of company. Above analysis suggest that

RBG Plc's short-term liquidity position is better than GSK, it means RBG is more efficient to

pay out entire current liabilities applying current assets.

Quick ratios:

It defines company's short-term liquidity position more clearly as this ratio apply quick

assets which is current assets excluding inventories. GSK 's quick ratio has been improved from

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.6

0.75

0.82 0.85

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.38

0.49

0.64

0.48

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

0.38 to 0.49 during 2017-2018 . While RBG's quick ratio has been declined from 0.64 to 0.48 in

same period respectively. Although even after a decline in quick ratio RBG's quick ratio is more

better than RBG's.

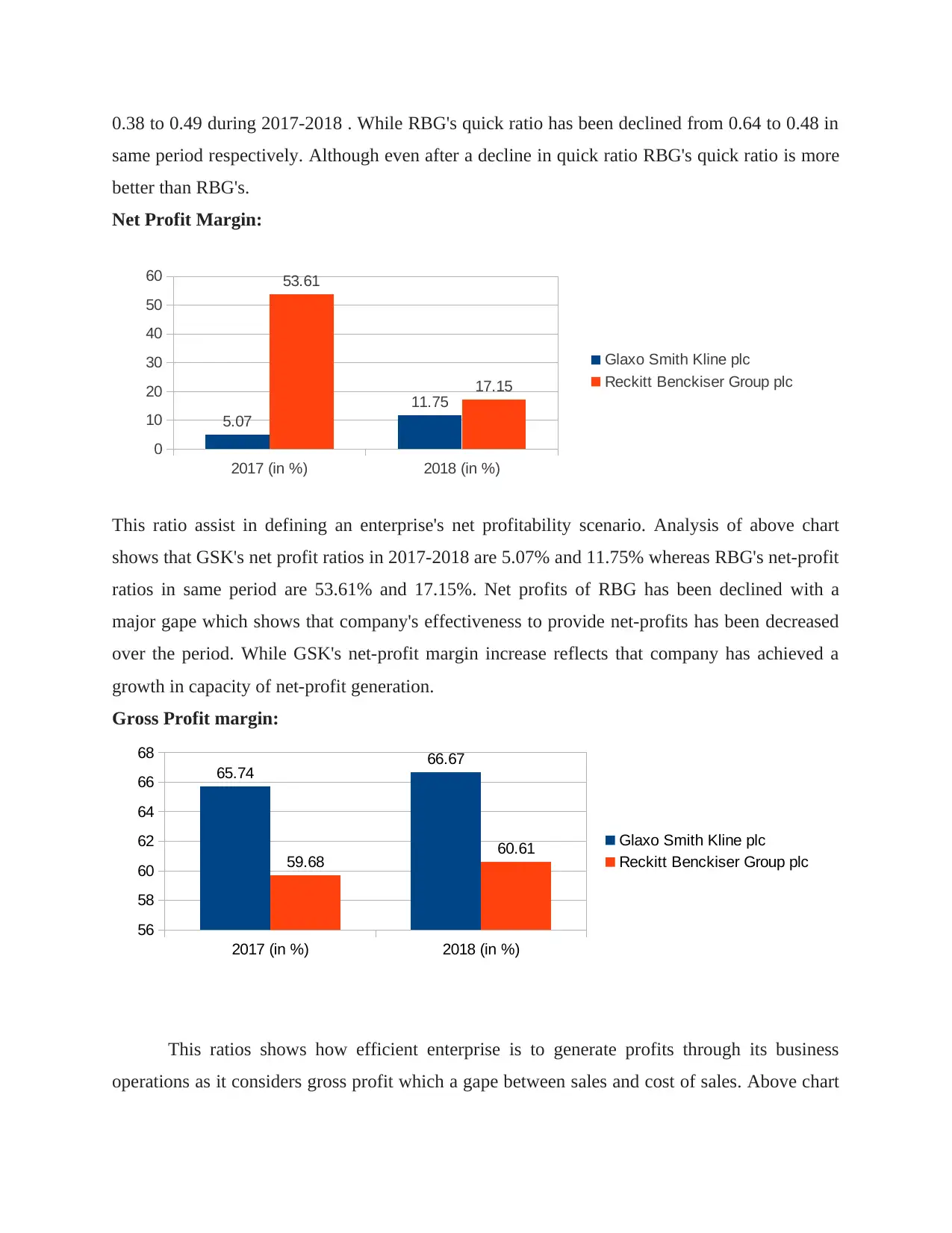

Net Profit Margin:

2017 (in %) 2018 (in %)

0

10

20

30

40

50

60

5.07

11.75

53.61

17.15

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

This ratio assist in defining an enterprise's net profitability scenario. Analysis of above chart

shows that GSK's net profit ratios in 2017-2018 are 5.07% and 11.75% whereas RBG's net-profit

ratios in same period are 53.61% and 17.15%. Net profits of RBG has been declined with a

major gape which shows that company's effectiveness to provide net-profits has been decreased

over the period. While GSK's net-profit margin increase reflects that company has achieved a

growth in capacity of net-profit generation.

Gross Profit margin:

This ratios shows how efficient enterprise is to generate profits through its business

operations as it considers gross profit which a gape between sales and cost of sales. Above chart

2017 (in %) 2018 (in %)

56

58

60

62

64

66

68

65.74 66.67

59.68 60.61 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

same period respectively. Although even after a decline in quick ratio RBG's quick ratio is more

better than RBG's.

Net Profit Margin:

2017 (in %) 2018 (in %)

0

10

20

30

40

50

60

5.07

11.75

53.61

17.15

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

This ratio assist in defining an enterprise's net profitability scenario. Analysis of above chart

shows that GSK's net profit ratios in 2017-2018 are 5.07% and 11.75% whereas RBG's net-profit

ratios in same period are 53.61% and 17.15%. Net profits of RBG has been declined with a

major gape which shows that company's effectiveness to provide net-profits has been decreased

over the period. While GSK's net-profit margin increase reflects that company has achieved a

growth in capacity of net-profit generation.

Gross Profit margin:

This ratios shows how efficient enterprise is to generate profits through its business

operations as it considers gross profit which a gape between sales and cost of sales. Above chart

2017 (in %) 2018 (in %)

56

58

60

62

64

66

68

65.74 66.67

59.68 60.61 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shows that GSK's gross profit margin level is much better than RBG. Gross margin of GSK in

2017-2018 are 65.74% and 66.67% (increase) while of RBG are 59.68% and 60.61% (Increase)

respectively. So in terms of Gross margin generation capacity company GSK is more efficient as

compare to RBG.

Gearing ratios:

*Here GSK's gearing ratio is indicated at zero in chart for better presentation as it is negative i.e.

-830.13.

The gearing ratio of GSK is negative 830.13 in year 2017 which has been improved in

2018 and reached to 12.32%. Negative gearing ratio in year 2017 was due to negative figure of

Equity in company's financial statement. Whereas RBG's gearing ratio was 1.74 in year 2017

which has been further in year 2018 declined to 1.55. Overall analysis of gearing ratio shows that

RBG's gearing ratio is lower than GSK.

P/E ratio:

2017 2018

0

2

4

6

8

10

12

14

0

12.32

1.74 1.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

2017 2018

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

4317.89

2000.27

815.77

2031.36 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

2017-2018 are 65.74% and 66.67% (increase) while of RBG are 59.68% and 60.61% (Increase)

respectively. So in terms of Gross margin generation capacity company GSK is more efficient as

compare to RBG.

Gearing ratios:

*Here GSK's gearing ratio is indicated at zero in chart for better presentation as it is negative i.e.

-830.13.

The gearing ratio of GSK is negative 830.13 in year 2017 which has been improved in

2018 and reached to 12.32%. Negative gearing ratio in year 2017 was due to negative figure of

Equity in company's financial statement. Whereas RBG's gearing ratio was 1.74 in year 2017

which has been further in year 2018 declined to 1.55. Overall analysis of gearing ratio shows that

RBG's gearing ratio is lower than GSK.

P/E ratio:

2017 2018

0

2

4

6

8

10

12

14

0

12.32

1.74 1.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

2017 2018

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

4317.89

2000.27

815.77

2031.36 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A high P / E indicate that the price of a stock is high compared to incomes and may be

overvalued. There is major decline in GSK's PE ratio from 4317.89 to 2000.27 in period 2017 to

2018. While RBG's PE ratio has been improved from 815.77 to 2031.36 during 2017 and 2018

respectively. Comparatively RBG's performance in terms of Gearing Ratio is much better than

GSK as of increase in PE indicates the enhancement of trust of shareholders in company.

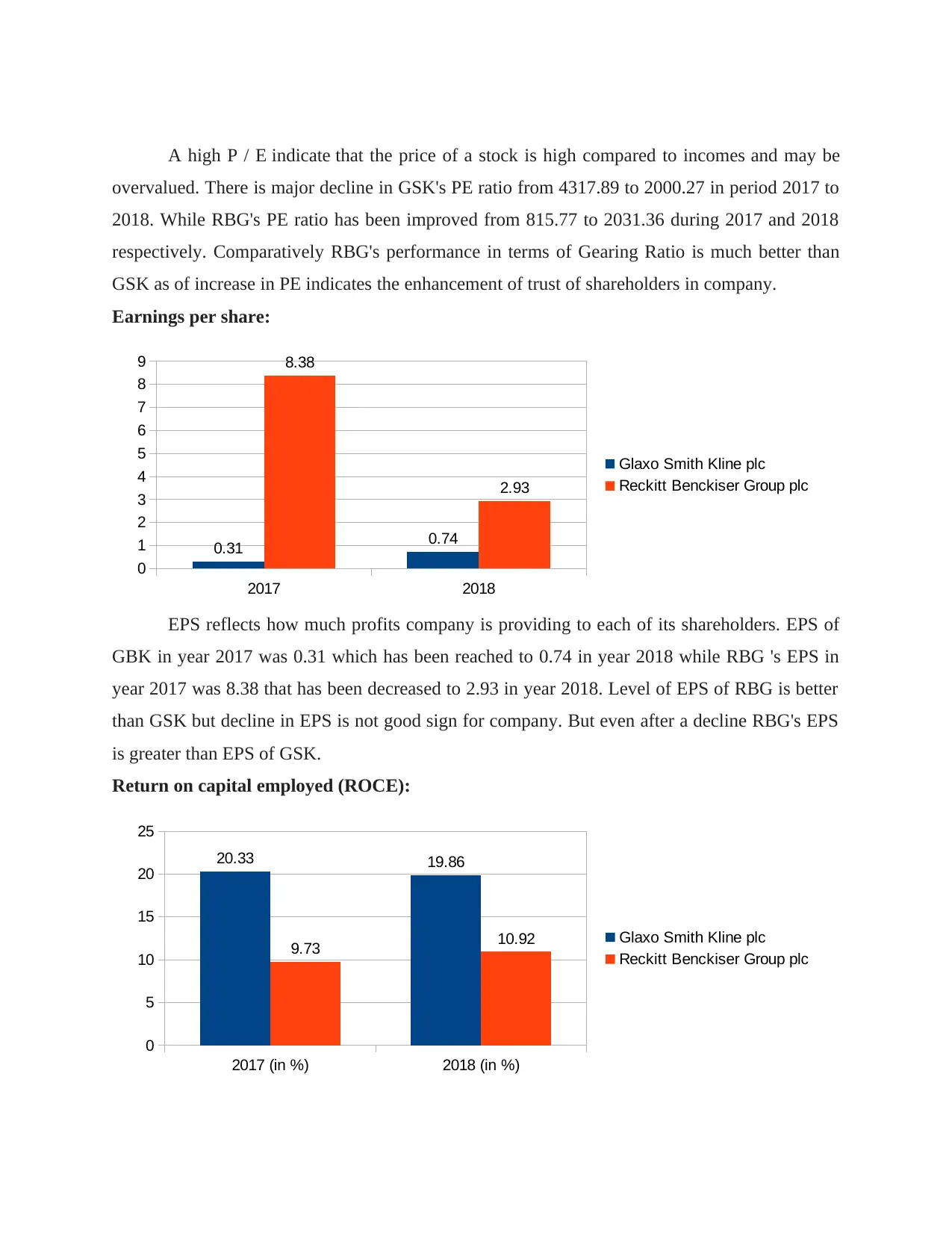

Earnings per share:

EPS reflects how much profits company is providing to each of its shareholders. EPS of

GBK in year 2017 was 0.31 which has been reached to 0.74 in year 2018 while RBG 's EPS in

year 2017 was 8.38 that has been decreased to 2.93 in year 2018. Level of EPS of RBG is better

than GSK but decline in EPS is not good sign for company. But even after a decline RBG's EPS

is greater than EPS of GSK.

Return on capital employed (ROCE):

2017 2018

0

1

2

3

4

5

6

7

8

9

0.31 0.74

8.38

2.93

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

2017 (in %) 2018 (in %)

0

5

10

15

20

25

20.33 19.86

9.73 10.92 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

overvalued. There is major decline in GSK's PE ratio from 4317.89 to 2000.27 in period 2017 to

2018. While RBG's PE ratio has been improved from 815.77 to 2031.36 during 2017 and 2018

respectively. Comparatively RBG's performance in terms of Gearing Ratio is much better than

GSK as of increase in PE indicates the enhancement of trust of shareholders in company.

Earnings per share:

EPS reflects how much profits company is providing to each of its shareholders. EPS of

GBK in year 2017 was 0.31 which has been reached to 0.74 in year 2018 while RBG 's EPS in

year 2017 was 8.38 that has been decreased to 2.93 in year 2018. Level of EPS of RBG is better

than GSK but decline in EPS is not good sign for company. But even after a decline RBG's EPS

is greater than EPS of GSK.

Return on capital employed (ROCE):

2017 2018

0

1

2

3

4

5

6

7

8

9

0.31 0.74

8.38

2.93

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

2017 (in %) 2018 (in %)

0

5

10

15

20

25

20.33 19.86

9.73 10.92 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

This ratio shows an enterprise's efficiency to utilise employed capital in order to provide

effective return on employed-capital (Harris, 2017). ROCE of GSK plc are 20.33 % and 19.86 %

in year 2017 and 2018 respectively while of RBG are 9.73 % and 10.92 % in during same period.

There is a decline in GSK's ROCE but overall level of ROCE is greater than RBG.

Average inventories turnover period:

2017 (in days) 2018 (in days)

0

50

100

150

200

250

196 195

94 93.86 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

This ratio indicates how much time enterprise generally takes to covert their inventories

into sales/cash (Huang, Shieh and Kao, 2016). As above chart shows that GSK's inventories

turnover ratios are 196 days and 195 days in year 2017 and 2018 respectively. Whereas during

the same period RBG's inventory turnover days are 94 and 93.86 respectively. Thus RBG's

inventories turnover ratios are more efficient as compare to GSK.

Dividend payout ratio:

Dividend Payout ratio per share of GSK is 2.55 in year 2017 and 1.08 in year 2018 while

RBG's dividend payout ratio are 0.18 and 0.55 respectively in year 2017 and 2018. This ratio

2017 2018

0

0.5

1

1.5

2

2.5

3

2.55

1.08

0.18

0.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

effective return on employed-capital (Harris, 2017). ROCE of GSK plc are 20.33 % and 19.86 %

in year 2017 and 2018 respectively while of RBG are 9.73 % and 10.92 % in during same period.

There is a decline in GSK's ROCE but overall level of ROCE is greater than RBG.

Average inventories turnover period:

2017 (in days) 2018 (in days)

0

50

100

150

200

250

196 195

94 93.86 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

This ratio indicates how much time enterprise generally takes to covert their inventories

into sales/cash (Huang, Shieh and Kao, 2016). As above chart shows that GSK's inventories

turnover ratios are 196 days and 195 days in year 2017 and 2018 respectively. Whereas during

the same period RBG's inventory turnover days are 94 and 93.86 respectively. Thus RBG's

inventories turnover ratios are more efficient as compare to GSK.

Dividend payout ratio:

Dividend Payout ratio per share of GSK is 2.55 in year 2017 and 1.08 in year 2018 while

RBG's dividend payout ratio are 0.18 and 0.55 respectively in year 2017 and 2018. This ratio

2017 2018

0

0.5

1

1.5

2

2.5

3

2.55

1.08

0.18

0.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.