Management Accounting Report: GSQ Financial Analysis and Costing

VerifiedAdded on 2023/01/12

|14

|3916

|77

Report

AI Summary

This report provides a comprehensive analysis of management accounting concepts, systems, and reporting methods. It delves into the preparation of income statements using marginal and absorption costing techniques, demonstrating their application through examples. The report also explores various management accounting reporting methods, budgetary control tools, and their advantages and disadvantages. Furthermore, it examines the adaptation of different management accounting tools to solve financial problems, using GSQ Limited as a case study to illustrate the practical application of these concepts. The report emphasizes how companies can achieve sustainable success by effectively addressing financial challenges through informed decision-making and strategic financial planning. Excel is utilized for the calculation of costs like production cost per unit etc.

EXECUTIVE SUMMARY

This report consist of concepts of Management accounting, system and reporting. Income

statement is prepared by using different costing methods such as marginal costing and absorption

costing. Excel sheet is used to calculate different costs like production cost per unit, fixed cost

per unit, etc. Overall this report focuses on how a company can achieve sustainable success

through solving financial problems. GSQ is taken as leading company for explaining the

different costs concepts.

This report consist of concepts of Management accounting, system and reporting. Income

statement is prepared by using different costing methods such as marginal costing and absorption

costing. Excel sheet is used to calculate different costs like production cost per unit, fixed cost

per unit, etc. Overall this report focuses on how a company can achieve sustainable success

through solving financial problems. GSQ is taken as leading company for explaining the

different costs concepts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................2

P1. Management accounting concept and essential requirements of different types of

management accounting systems:....................................................................................................2

P2. Management Accounting Reporting concept and different methods used for management

accounting reporting:.......................................................................................................................5

P3. Preparing of Income statement using Marginal costing and absorption costing techniques of

cost analyses:...................................................................................................................................7

P4. Advantages and disadvantages of different tools of budgetary control....................................9

P5. Adapting different Management accounting tools to solve financial problems:.....................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

P1. Management accounting concept and essential requirements of different types of

management accounting systems:....................................................................................................2

P2. Management Accounting Reporting concept and different methods used for management

accounting reporting:.......................................................................................................................5

P3. Preparing of Income statement using Marginal costing and absorption costing techniques of

cost analyses:...................................................................................................................................7

P4. Advantages and disadvantages of different tools of budgetary control....................................9

P5. Adapting different Management accounting tools to solve financial problems:.....................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is the tool which helps higher level managers in taking decisions based

on various reports prepared by accounting managers. As top level managers belong to different

field such as marketing, HR, production and technical. So understanding financial statements is

not an easy task for them and without knowing what figures are saying it is impossible to take

good decisions for the company, hence Management accounting bridges the gap between

financial managers and top level management through its easy to understand report and

interpretation of various graph charts.

This assignment will show how reporting can be helpful tool for management and how it can

applied for solving business problems.

P1. Management accounting concept and essential requirements of

different types of management accounting systems:

Management Accounting: It is the provision of financial data and advice to a company for

use in the organization and development of its business. It useful for financial department

of the organizations, it is different from financial accounting. In Management accounting,

financial statements, ratio analysis, balance sheet, cash flow statement and other financial

information’s are shared with company’s top level management. This top level

management uses this report to make strategy on future expansion of business and taking

make or buy decisions for the business (Adler, 2018).

Management accounting is the tool which helps higher level managers in taking decisions based

on various reports prepared by accounting managers. As top level managers belong to different

field such as marketing, HR, production and technical. So understanding financial statements is

not an easy task for them and without knowing what figures are saying it is impossible to take

good decisions for the company, hence Management accounting bridges the gap between

financial managers and top level management through its easy to understand report and

interpretation of various graph charts.

This assignment will show how reporting can be helpful tool for management and how it can

applied for solving business problems.

P1. Management accounting concept and essential requirements of

different types of management accounting systems:

Management Accounting: It is the provision of financial data and advice to a company for

use in the organization and development of its business. It useful for financial department

of the organizations, it is different from financial accounting. In Management accounting,

financial statements, ratio analysis, balance sheet, cash flow statement and other financial

information’s are shared with company’s top level management. This top level

management uses this report to make strategy on future expansion of business and taking

make or buy decisions for the business (Adler, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting method of accounting system is the recording and presentation

demonstration of information for the benefit of the various stakeholders of an organization.

Management accounting, on the other hand, is the presentation of financial data and

business activities concern natural process for the internal management of the organization,

direction of the establishment (Nørreklit, 2017).

Essential requirements of different types of management accounting systems:

Management accounting systems shows the variance in the performance and also explains

reasons behind this variance. Company required management accounting to identify whether

it is working towards goal set by top level management. Some of the management

accounting system types is discussed below:

1) Cost Accounting System: This system also known as product costing system, company

needs this tool to estimate the cost of item to do profitability analysis, valuation of stock

and controlling cost of the company. Finding actual cost of product is not an easy task. A

firm must know which products are profitable and which of them don't seem to be, and

this will be ascertained only if it's estimated the right cost of the merchandise

(Schaltegger and Burritt, 2017). Further, a product costing system helps in estimating the

closing value of materials inventory, work-in-progress and finished goods inventory for

the aim of monetary statement preparation.

2) Job order costing: It is cost accounting system that gathers manufacturing costs

separately for every job. It’s most appropriate for various companies like on an occasion

management company, a distinct segment furniture producer, a producer of very high

cost air closed-circuit television, etc.

3) Process Costing: It is also the part of cost accounting system which gathers

manufacturing costs of each process separately. It is useful for those products which

process under different departments during manufacturing. Some of the examples of

departments which use process costing are oil refineries, chemical producers, assembling

of parts, etc (Alawattage and Wickramasinghe, 2018).

4) Inventory management systems: It is the combination of hardware and software models, it

processes for maintenance and controlling of inventories in warehouse, it also checks

whether products like company assets, raw materials, supplies and finished products able

demonstration of information for the benefit of the various stakeholders of an organization.

Management accounting, on the other hand, is the presentation of financial data and

business activities concern natural process for the internal management of the organization,

direction of the establishment (Nørreklit, 2017).

Essential requirements of different types of management accounting systems:

Management accounting systems shows the variance in the performance and also explains

reasons behind this variance. Company required management accounting to identify whether

it is working towards goal set by top level management. Some of the management

accounting system types is discussed below:

1) Cost Accounting System: This system also known as product costing system, company

needs this tool to estimate the cost of item to do profitability analysis, valuation of stock

and controlling cost of the company. Finding actual cost of product is not an easy task. A

firm must know which products are profitable and which of them don't seem to be, and

this will be ascertained only if it's estimated the right cost of the merchandise

(Schaltegger and Burritt, 2017). Further, a product costing system helps in estimating the

closing value of materials inventory, work-in-progress and finished goods inventory for

the aim of monetary statement preparation.

2) Job order costing: It is cost accounting system that gathers manufacturing costs

separately for every job. It’s most appropriate for various companies like on an occasion

management company, a distinct segment furniture producer, a producer of very high

cost air closed-circuit television, etc.

3) Process Costing: It is also the part of cost accounting system which gathers

manufacturing costs of each process separately. It is useful for those products which

process under different departments during manufacturing. Some of the examples of

departments which use process costing are oil refineries, chemical producers, assembling

of parts, etc (Alawattage and Wickramasinghe, 2018).

4) Inventory management systems: It is the combination of hardware and software models, it

processes for maintenance and controlling of inventories in warehouse, it also checks

whether products like company assets, raw materials, supplies and finished products able

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to be sent to vendors or end consumers. Some times over stock and under stock creates

problem for the company. To solve this problem a strong tool known as Economic order

quantity or EOQ is helpful in finding how much company should stock so that its overall

holding costs should minimize.

5) Price-Optimizing system: Price optimization is that the process of finding the worth that

maximizes the worth, against the willingness of shoppers to pay. Companies up and

down the provision chain in both B2B and B2C settings have committed a big amount of

your time to the proper price optimization to make sure that their products will sell

quickly at the proper price, while still having one Making good profit. Finding the proper

balance between profit and price is actually what price optimization is all about, and

since the relative value of products and services changes constantly, it's a never-ending

task for many businesses (Malina, 2017).

Benefits of Management Accounting Systems:

Increase efficiency: It boosts the efficiency of operations of the firm through

scientifically evaluate performance and matching it with benchmark set by company.

Management takes promotional decisions, rewards and motivates underperformed

employees to do better next time through management accounting systems.

Maximizes the Net earnings: Through budgetary control and capital expenditure model,

firm can minimize operating and capital expenditures together. This also helps company

in obtaining super profit through reducing price of product and costs of operations.

Make financial statements simple: Financial statement can be complex to study for those

who are not belonging to this field but through management accounting systems it

become easy to understand profit and loss statement and balance sheet simply by reading

its end report. It makes easy for top level management to take decisions by simply read

the facts presented by financial accountants on the basis of financial statements.

Control’s excess cash flow of the business: Accounting manager analyses the sources of

money and also their application within organization. They evaluate to minimize the

unnecessary use of cash flow.

Application of Management Accounting Systems within GSQ Limited:

problem for the company. To solve this problem a strong tool known as Economic order

quantity or EOQ is helpful in finding how much company should stock so that its overall

holding costs should minimize.

5) Price-Optimizing system: Price optimization is that the process of finding the worth that

maximizes the worth, against the willingness of shoppers to pay. Companies up and

down the provision chain in both B2B and B2C settings have committed a big amount of

your time to the proper price optimization to make sure that their products will sell

quickly at the proper price, while still having one Making good profit. Finding the proper

balance between profit and price is actually what price optimization is all about, and

since the relative value of products and services changes constantly, it's a never-ending

task for many businesses (Malina, 2017).

Benefits of Management Accounting Systems:

Increase efficiency: It boosts the efficiency of operations of the firm through

scientifically evaluate performance and matching it with benchmark set by company.

Management takes promotional decisions, rewards and motivates underperformed

employees to do better next time through management accounting systems.

Maximizes the Net earnings: Through budgetary control and capital expenditure model,

firm can minimize operating and capital expenditures together. This also helps company

in obtaining super profit through reducing price of product and costs of operations.

Make financial statements simple: Financial statement can be complex to study for those

who are not belonging to this field but through management accounting systems it

become easy to understand profit and loss statement and balance sheet simply by reading

its end report. It makes easy for top level management to take decisions by simply read

the facts presented by financial accountants on the basis of financial statements.

Control’s excess cash flow of the business: Accounting manager analyses the sources of

money and also their application within organization. They evaluate to minimize the

unnecessary use of cash flow.

Application of Management Accounting Systems within GSQ Limited:

1) Cost accounting system: This tool will help GSQ limited in estimating standard cost at

which company get good profit and compete their rival firms in market. It will also help

in avoiding misuse of funds by reducing non required expenses.

2) Job Order Costing: This tool can be helpful for the company if the company is in

manufacturing or production business. It can reduce cost on the bases of job or activity

like it will focus on that job which is important to run core product of the company.

3) Process costing: Like Job order costing, this tool applicable only for production or

manufacturing companies. It reduces costs through analyzing the methods to reduce step

in operations. It can be more useful for those companies which deal with assembly units.

4) Inventory management system: This tool is useful for warehouse maintenance, either

supplier or producer or whole seller can use this technique to reduce overall holding costs

of the inventories. Sometimes overstock of inventory can increase the risk of excess fund

blockage and heavy loss due to change in customer preferences. Proper inventory

management will help GSQ Limited in keeping its current capacity strong; also company

need not to owe extra space for stock and inventories.

5) Price optimizing system: This system is very important and necessary for GSQ, as

without this company cannot meet the price at which customer is willing to buy the

product and will lose competitive edge in market.

P2. Management Accounting Reporting concept and different methods

used for management accounting reporting:

Management Accounting Reporting: The executives bookkeeping reports show the money

related status of a business at present or over a specific time period. These reports

accumulate money related data from accounting records and can fuse data like trades,

operational costs, thing profit, and neighborhood bargains (Charifzadeh and Taschner,

2017). These reports are made with the objective that heads can choose taught business

decisions. Right when associations rely upon managerial accounting help, they can even

more successfully amass information that helps boss with coordinating the business toward

meeting its goals.

Different methods used for management accounting reporting:

which company get good profit and compete their rival firms in market. It will also help

in avoiding misuse of funds by reducing non required expenses.

2) Job Order Costing: This tool can be helpful for the company if the company is in

manufacturing or production business. It can reduce cost on the bases of job or activity

like it will focus on that job which is important to run core product of the company.

3) Process costing: Like Job order costing, this tool applicable only for production or

manufacturing companies. It reduces costs through analyzing the methods to reduce step

in operations. It can be more useful for those companies which deal with assembly units.

4) Inventory management system: This tool is useful for warehouse maintenance, either

supplier or producer or whole seller can use this technique to reduce overall holding costs

of the inventories. Sometimes overstock of inventory can increase the risk of excess fund

blockage and heavy loss due to change in customer preferences. Proper inventory

management will help GSQ Limited in keeping its current capacity strong; also company

need not to owe extra space for stock and inventories.

5) Price optimizing system: This system is very important and necessary for GSQ, as

without this company cannot meet the price at which customer is willing to buy the

product and will lose competitive edge in market.

P2. Management Accounting Reporting concept and different methods

used for management accounting reporting:

Management Accounting Reporting: The executives bookkeeping reports show the money

related status of a business at present or over a specific time period. These reports

accumulate money related data from accounting records and can fuse data like trades,

operational costs, thing profit, and neighborhood bargains (Charifzadeh and Taschner,

2017). These reports are made with the objective that heads can choose taught business

decisions. Right when associations rely upon managerial accounting help, they can even

more successfully amass information that helps boss with coordinating the business toward

meeting its goals.

Different methods used for management accounting reporting:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting reporting is useful for top line managers to take decisions on many

crucial occasions. There are some important methods which helps accounting managers to

prepare a report for Executive managers:

1) Budget reports: Spending Reports to Analyze Performance: Budget reports assist

business people with inspecting business execution and managers separate their

specialized topic display and control costs. The evaluated spending plan for the period is

regularly established on the authentic expenses from prior years. If the free organization

was extensively over spending plan in a prior year and can't find methods to trim costs,

future spending plans may be extended to a continuously exact level (Singhvi and

BODHANWALA, 2018). Owners and heads can in like manner use spending reports to

offer forces to laborers. At this moment, resources may be given up out as remunerations

to delegates for meeting express cash related destinations.

2) Inventory and Manufacturing: If private endeavor keeps up a physical stock or conveys

things, can use managerial accounting reports to make the amassing structures

progressively compelling. These reports generally consolidate things, for instance, stock

waste, hourly work costs or per-unit overhead costs. You would then have the option to

take a gander at changed mechanical creation frameworks inside your business to

highlight zones for advancement or to offer compensations to the best-performing

workplaces.

3) Job Cost Reporting: It show costs for a specific endeavor financed by free organization.

They are ordinarily planned with a check of salary so you can survey the movement's

profitability. This perceives higher-winning zones of the business so it can focus

additional undertakings there instead of lounging around and money on occupations with

low by and large incomes. Business cost reports are moreover used to explore costs while

the endeavor is in progress can address zones of waste before costs winding (Collis and

Hussey, 2017).

4) Accounts receivable aging: The records of receivable is developing report, it is an

essential instrument for managing salary in the occasion that loosen up credit to

customers of business. This report isolates the customer alters by to what degree they

have been owed. Most developing reports join separate segments for sales that are 30

days late, 60 days late and 90 days late or more. A manager can use the developing report

crucial occasions. There are some important methods which helps accounting managers to

prepare a report for Executive managers:

1) Budget reports: Spending Reports to Analyze Performance: Budget reports assist

business people with inspecting business execution and managers separate their

specialized topic display and control costs. The evaluated spending plan for the period is

regularly established on the authentic expenses from prior years. If the free organization

was extensively over spending plan in a prior year and can't find methods to trim costs,

future spending plans may be extended to a continuously exact level (Singhvi and

BODHANWALA, 2018). Owners and heads can in like manner use spending reports to

offer forces to laborers. At this moment, resources may be given up out as remunerations

to delegates for meeting express cash related destinations.

2) Inventory and Manufacturing: If private endeavor keeps up a physical stock or conveys

things, can use managerial accounting reports to make the amassing structures

progressively compelling. These reports generally consolidate things, for instance, stock

waste, hourly work costs or per-unit overhead costs. You would then have the option to

take a gander at changed mechanical creation frameworks inside your business to

highlight zones for advancement or to offer compensations to the best-performing

workplaces.

3) Job Cost Reporting: It show costs for a specific endeavor financed by free organization.

They are ordinarily planned with a check of salary so you can survey the movement's

profitability. This perceives higher-winning zones of the business so it can focus

additional undertakings there instead of lounging around and money on occupations with

low by and large incomes. Business cost reports are moreover used to explore costs while

the endeavor is in progress can address zones of waste before costs winding (Collis and

Hussey, 2017).

4) Accounts receivable aging: The records of receivable is developing report, it is an

essential instrument for managing salary in the occasion that loosen up credit to

customers of business. This report isolates the customer alters by to what degree they

have been owed. Most developing reports join separate segments for sales that are 30

days late, 60 days late and 90 days late or more. A manager can use the developing report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to find issues with the association's combinations technique. If a critical number of

customers can't pay their adjustments, organizational need to fix its credit systems.

Incidentally analyzing the records receivable developing also shields the groupings office

from disregarding old commitments.

P3. Preparing of Income statement using Marginal costing and

absorption costing techniques of cost analyses:

Marginal Costing: In this method only variable costs are reduced from total revenue to get

contribution. Fixed costs are considered as period costs in this technique.

Absorption Costing: This technique takes all production or manufacturing costs as total

production costs per unit to calculate gross profit, it treats selling and administrative costs

separately to find income from operations (Quinn, and Oliveira, 2018).

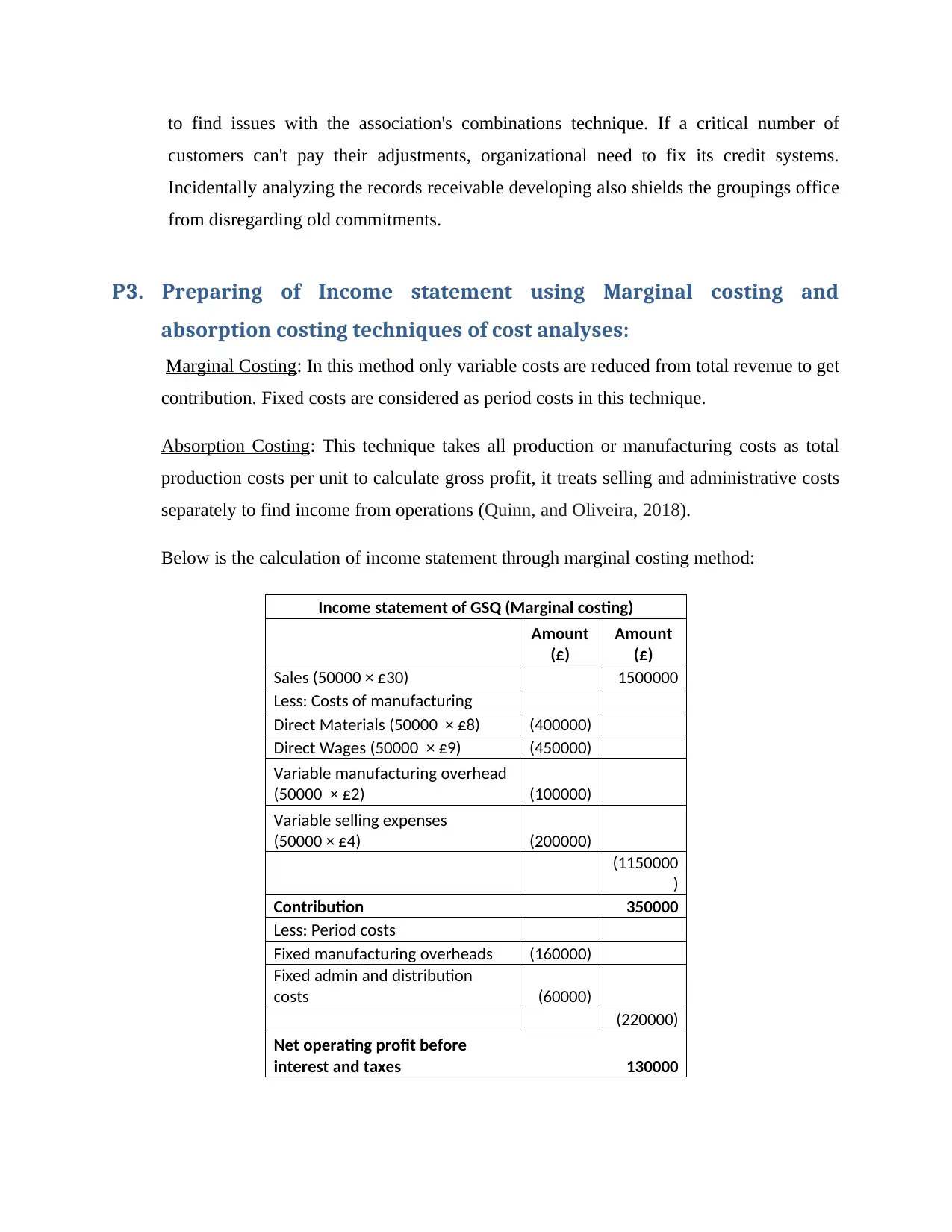

Below is the calculation of income statement through marginal costing method:

Income statement of GSQ (Marginal costing)

Amount

(£)

Amount

(£)

Sales (50000 × £30) 1500000

Less: Costs of manufacturing

Direct Materials (50000 × £8) (400000)

Direct Wages (50000 × £9) (450000)

Variable manufacturing overhead

(50000 × £2) (100000)

Variable selling expenses

(50000 × £4) (200000)

(1150000

)

Contribution 350000

Less: Period costs

Fixed manufacturing overheads (160000)

Fixed admin and distribution

costs (60000)

(220000)

Net operating profit before

interest and taxes 130000

customers can't pay their adjustments, organizational need to fix its credit systems.

Incidentally analyzing the records receivable developing also shields the groupings office

from disregarding old commitments.

P3. Preparing of Income statement using Marginal costing and

absorption costing techniques of cost analyses:

Marginal Costing: In this method only variable costs are reduced from total revenue to get

contribution. Fixed costs are considered as period costs in this technique.

Absorption Costing: This technique takes all production or manufacturing costs as total

production costs per unit to calculate gross profit, it treats selling and administrative costs

separately to find income from operations (Quinn, and Oliveira, 2018).

Below is the calculation of income statement through marginal costing method:

Income statement of GSQ (Marginal costing)

Amount

(£)

Amount

(£)

Sales (50000 × £30) 1500000

Less: Costs of manufacturing

Direct Materials (50000 × £8) (400000)

Direct Wages (50000 × £9) (450000)

Variable manufacturing overhead

(50000 × £2) (100000)

Variable selling expenses

(50000 × £4) (200000)

(1150000

)

Contribution 350000

Less: Period costs

Fixed manufacturing overheads (160000)

Fixed admin and distribution

costs (60000)

(220000)

Net operating profit before

interest and taxes 130000

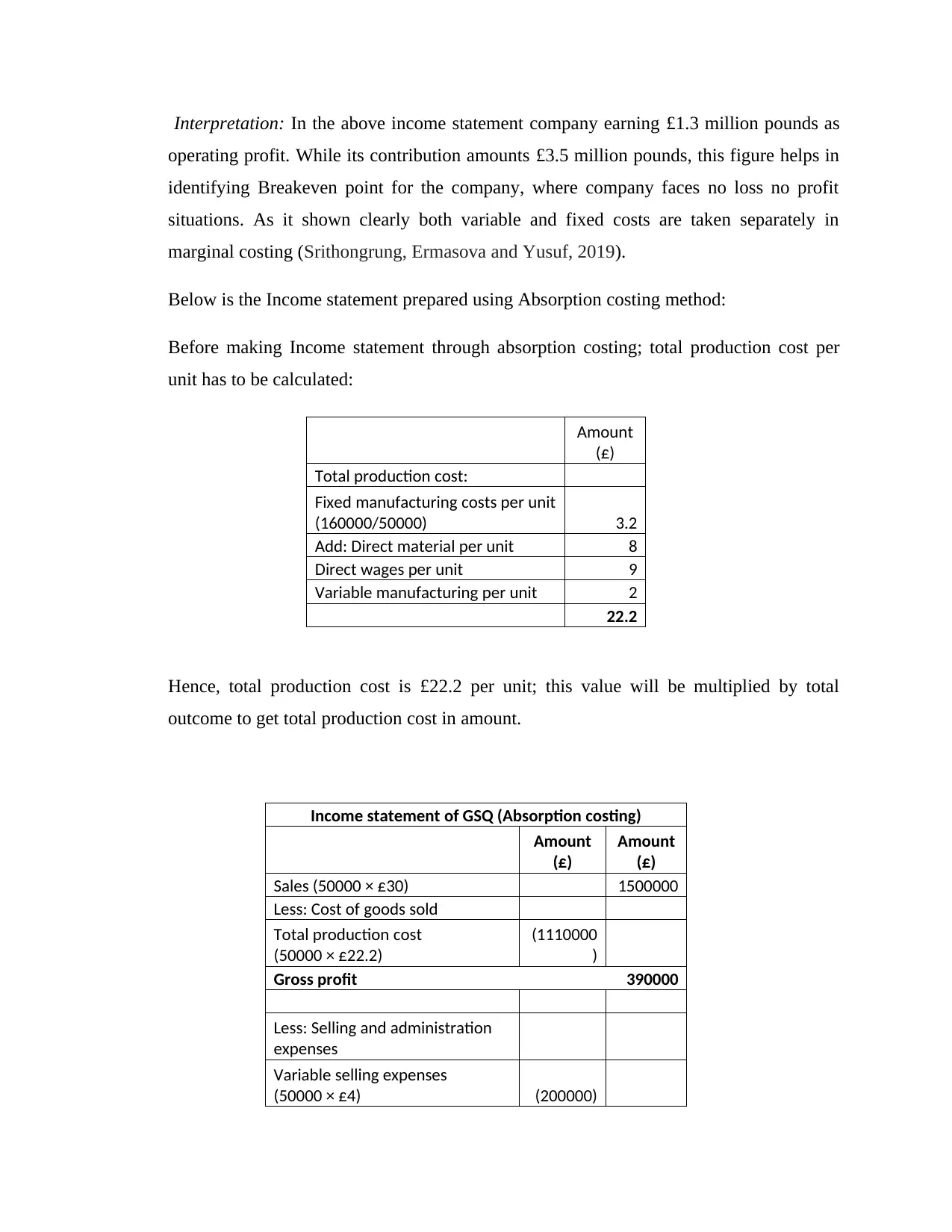

Interpretation: In the above income statement company earning £1.3 million pounds as

operating profit. While its contribution amounts £3.5 million pounds, this figure helps in

identifying Breakeven point for the company, where company faces no loss no profit

situations. As it shown clearly both variable and fixed costs are taken separately in

marginal costing (Srithongrung, Ermasova and Yusuf, 2019).

Below is the Income statement prepared using Absorption costing method:

Before making Income statement through absorption costing; total production cost per

unit has to be calculated:

Amount

(£)

Total production cost:

Fixed manufacturing costs per unit

(160000/50000) 3.2

Add: Direct material per unit 8

Direct wages per unit 9

Variable manufacturing per unit 2

22.2

Hence, total production cost is £22.2 per unit; this value will be multiplied by total

outcome to get total production cost in amount.

Income statement of GSQ (Absorption costing)

Amount

(£)

Amount

(£)

Sales (50000 × £30) 1500000

Less: Cost of goods sold

Total production cost

(50000 × £22.2)

(1110000

)

Gross profit 390000

Less: Selling and administration

expenses

Variable selling expenses

(50000 × £4) (200000)

operating profit. While its contribution amounts £3.5 million pounds, this figure helps in

identifying Breakeven point for the company, where company faces no loss no profit

situations. As it shown clearly both variable and fixed costs are taken separately in

marginal costing (Srithongrung, Ermasova and Yusuf, 2019).

Below is the Income statement prepared using Absorption costing method:

Before making Income statement through absorption costing; total production cost per

unit has to be calculated:

Amount

(£)

Total production cost:

Fixed manufacturing costs per unit

(160000/50000) 3.2

Add: Direct material per unit 8

Direct wages per unit 9

Variable manufacturing per unit 2

22.2

Hence, total production cost is £22.2 per unit; this value will be multiplied by total

outcome to get total production cost in amount.

Income statement of GSQ (Absorption costing)

Amount

(£)

Amount

(£)

Sales (50000 × £30) 1500000

Less: Cost of goods sold

Total production cost

(50000 × £22.2)

(1110000

)

Gross profit 390000

Less: Selling and administration

expenses

Variable selling expenses

(50000 × £4) (200000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed admin and distribution

costs (60000)

Net operating profit 130000

Interpretation: Both marginal costing and absorption costing shows same net operating

profit but have different gross profit and contribution because in absorption costing all

manufacturing costs whether fixed or variable put together to get total cost of

manufacturing product but in Marginal costing only variable cost per unit is considered to

calculate contribution. In Absorption costing method; selling and administrative expenses

are treated separately to calculate net operating profit.

P4. Advantages and disadvantages of different tools of budgetary control

Traditional budgeting: Right now is set up on basic idea. For getting ready spending plan by

conventional methodology, earlier year's information or data of asset report and pay

proclamation is taken as a base and the figures given in fiscal report is adjusted by assessing

expansion rate, future customer request, chance assuming any, rivalry level, and so forth

(Srithongrung, 2019).

Advantages Disadvantages

Gives benchmark to each administrator. It

turns out to be simple for directors to get

data in which course they need to move

(Jones, and et.al. 2018).

Uses undervalued tool such as excel which

shows error while making budget for larger

data.

Offers chance to receive decentralization to

meet set targets.

It is rigid and cannot be changed easily once

made, as lots of time and money consumed

in this process.

It is being utilized by supervisors for

extensive stretch of time; thus it is notable

to them and simplicity to make spending

plans.

Demotivate employees due to less

participation in decision making process by

them.

Rolling budget: In this approach spending plan is supplanted by new spending plan

consistently. Another spending limit is set up before the consummation of old spending

costs (60000)

Net operating profit 130000

Interpretation: Both marginal costing and absorption costing shows same net operating

profit but have different gross profit and contribution because in absorption costing all

manufacturing costs whether fixed or variable put together to get total cost of

manufacturing product but in Marginal costing only variable cost per unit is considered to

calculate contribution. In Absorption costing method; selling and administrative expenses

are treated separately to calculate net operating profit.

P4. Advantages and disadvantages of different tools of budgetary control

Traditional budgeting: Right now is set up on basic idea. For getting ready spending plan by

conventional methodology, earlier year's information or data of asset report and pay

proclamation is taken as a base and the figures given in fiscal report is adjusted by assessing

expansion rate, future customer request, chance assuming any, rivalry level, and so forth

(Srithongrung, 2019).

Advantages Disadvantages

Gives benchmark to each administrator. It

turns out to be simple for directors to get

data in which course they need to move

(Jones, and et.al. 2018).

Uses undervalued tool such as excel which

shows error while making budget for larger

data.

Offers chance to receive decentralization to

meet set targets.

It is rigid and cannot be changed easily once

made, as lots of time and money consumed

in this process.

It is being utilized by supervisors for

extensive stretch of time; thus it is notable

to them and simplicity to make spending

plans.

Demotivate employees due to less

participation in decision making process by

them.

Rolling budget: In this approach spending plan is supplanted by new spending plan

consistently. Another spending limit is set up before the consummation of old spending

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

plan; this helps the board in setting up an in excess of 78 percent exact spending plan. It

tends to be treated as never finished procedure for a business.

Advantages Disadvantages

Make business progressively responsive

towards change in the market.

Just relevant when conditions and

circumstances are continually changing like

blast, swelling, flattening, and so forth.

Due to planning over and again, it permits

association to make spending which is

close to real (Garvey, Book and Covert,

2016).

This methodology requires experts who

charged high sum which makes it costly.

Activity based budget: This methodology takes action based costing to get ready spending

plans. Like zero based planning, it additionally not takes base year for making spending

plan. Other than this it center on different expenses and partitions it into various exercises

after appropriate examinations. This methodology of planning is movement arranged not

work situated (Muennig, and Bounthavong, 2016).

Advantages Disadvantages

It disposes of superfluous exercises and

considers just significant or center exercises

required for maintaining a business

It is perplexing procedure, requires bunches

of profound investigations of expenses. As

expenses are of three kinds fixed, variable

and blended. Blended expenses incorporate

both fixed and variable and requires bunches

of concentrates to isolate it.

It accepts entire association as single units

which help an organization to maintain a

strategic distance from strife circumstances

between various offices.

This financial limit must be set up for

present moment and not valuable for long

haul strategy.

Zero based budgeting: It is entirely unexpected methodology of getting ready spending

plan. Right now base is taken for assessing spending plan, it begins by taking all qualities at

zero. The primary point of this methodology is to cut superfluous costs and expenses

happening at various degrees of tasks. It examination the total data's about the expense

before adding it to spending line.

Advantages Disadvantages

As it take all the costs without any It is tedious procedure.

tends to be treated as never finished procedure for a business.

Advantages Disadvantages

Make business progressively responsive

towards change in the market.

Just relevant when conditions and

circumstances are continually changing like

blast, swelling, flattening, and so forth.

Due to planning over and again, it permits

association to make spending which is

close to real (Garvey, Book and Covert,

2016).

This methodology requires experts who

charged high sum which makes it costly.

Activity based budget: This methodology takes action based costing to get ready spending

plans. Like zero based planning, it additionally not takes base year for making spending

plan. Other than this it center on different expenses and partitions it into various exercises

after appropriate examinations. This methodology of planning is movement arranged not

work situated (Muennig, and Bounthavong, 2016).

Advantages Disadvantages

It disposes of superfluous exercises and

considers just significant or center exercises

required for maintaining a business

It is perplexing procedure, requires bunches

of profound investigations of expenses. As

expenses are of three kinds fixed, variable

and blended. Blended expenses incorporate

both fixed and variable and requires bunches

of concentrates to isolate it.

It accepts entire association as single units

which help an organization to maintain a

strategic distance from strife circumstances

between various offices.

This financial limit must be set up for

present moment and not valuable for long

haul strategy.

Zero based budgeting: It is entirely unexpected methodology of getting ready spending

plan. Right now base is taken for assessing spending plan, it begins by taking all qualities at

zero. The primary point of this methodology is to cut superfluous costs and expenses

happening at various degrees of tasks. It examination the total data's about the expense

before adding it to spending line.

Advantages Disadvantages

As it take all the costs without any It is tedious procedure.

preparation, it turns out to be anything but

difficult to concentrate more on the most

proficient method to decrease costs

Best strategy for settle on or purchase

choices.

Not relevant to small private companies.

P5. Adapting different Management accounting tools to solve financial

problems:

Sustainable success: It means success for longer period of time, as it is difficult to achieve

sustainable success but by solving business financial problems company can achieve success

for longer period of time (Blischke, 2019). There are various types of tools which can help

company in solving financial problem and get sustainable success:

1) Financial statement: Through analyzing financial statement such as Income

statement; GSQ can identify how much earnings it get on its investments or it can

identify return on investment. Other financial statement which is balance sheet

indicates total assets and liabilities available with the company. If more debts are

taken by company, then company needs to maintain its net earnings to pay interest.

On the other hand if company is not able to pay interest on its debts then it should go

for equity to generate funds. This will solve financial issues and attain sustainable

success.

2) Cash flow statement: This statement shows the movement of fund within companies’

different department and operations. Most of the companies facing common

financial issues such as shortage of cash or poor working capital, which results in

crash of that firm. To avoid such situation GSQ requires focusing on its cashflow

and taking steps to improve its working capital.

3) Ratio analyses: These are very useful tool in quick analyses of company’s current

situation. Tools like debt equity ratio, sales turnover ratio, leverage ratio and

earnings per share ratio helps company in quick response to the problems which

affects these ratios. By this it can attain sustainable success.

difficult to concentrate more on the most

proficient method to decrease costs

Best strategy for settle on or purchase

choices.

Not relevant to small private companies.

P5. Adapting different Management accounting tools to solve financial

problems:

Sustainable success: It means success for longer period of time, as it is difficult to achieve

sustainable success but by solving business financial problems company can achieve success

for longer period of time (Blischke, 2019). There are various types of tools which can help

company in solving financial problem and get sustainable success:

1) Financial statement: Through analyzing financial statement such as Income

statement; GSQ can identify how much earnings it get on its investments or it can

identify return on investment. Other financial statement which is balance sheet

indicates total assets and liabilities available with the company. If more debts are

taken by company, then company needs to maintain its net earnings to pay interest.

On the other hand if company is not able to pay interest on its debts then it should go

for equity to generate funds. This will solve financial issues and attain sustainable

success.

2) Cash flow statement: This statement shows the movement of fund within companies’

different department and operations. Most of the companies facing common

financial issues such as shortage of cash or poor working capital, which results in

crash of that firm. To avoid such situation GSQ requires focusing on its cashflow

and taking steps to improve its working capital.

3) Ratio analyses: These are very useful tool in quick analyses of company’s current

situation. Tools like debt equity ratio, sales turnover ratio, leverage ratio and

earnings per share ratio helps company in quick response to the problems which

affects these ratios. By this it can attain sustainable success.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.