Comparative Financial Analysis of Hartalega and Supermax Corporations

VerifiedAdded on 2022/01/19

|15

|3251

|26

Report

AI Summary

This report provides a comparative financial analysis of Hartalega Holdings Bhd and Supermax Corporation Bhd. It begins with an introduction discussing the stock performance of both companies and the factors influencing investor confidence. The report then delves into a detailed comparison of their financial performance, examining key ratios such as current ratio, equity ratio, gross profit margin, and efficiency ratio, using data from their annual reports. The analysis includes calculations and comparisons of these ratios over several years. Furthermore, the report discusses the dividend policies of both companies, highlighting their approaches to dividend payments. It also explores the corporate governance practices of Supermax and Hartalega. The report concludes with an analysis of put options, benefits and drawbacks, and calculations for profit scenarios based on stock price changes. The document is available on Desklib, which provides resources for students.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART A......................................................................................................................................4

1.1. Introduction.................................................................................................................4

1.2. Financial performance comparison of Hartalega Holdings Bhd and Supermax

corporation Bhd......................................................................................................................4

1.2.1. Hartalega Holdings Bhd.......................................................................................4

1.2.1.1. Current ratio..................................................................................................4

1.2.1.2. Equity ratio...................................................................................................5

1.2.1.3. Gross profit margin.......................................................................................5

1.2.1.4. Efficiency ratio.............................................................................................6

1.2.2. Supermax corporation Bhd..................................................................................6

1.2.2.1. Current ratio..................................................................................................6

1.2.2.2. Equity ratio...................................................................................................7

1.2.2.3. Gross profit margin.......................................................................................7

1.2.2.4. Efficiency ratio.............................................................................................7

1.3. Dividend policy...........................................................................................................8

1.3.1. Hartalega..............................................................................................................8

1.3.2. Supermax..............................................................................................................9

1.4. Corporate governance..................................................................................................9

1.4.1. Supermax..............................................................................................................9

1.4.2. Hartalega............................................................................................................10

Part B........................................................................................................................................10

i) Benefits and major drawback....................................................................................10

ii) What will be Ibrahim’s minimum profit if he buys two puts at the indicated price?

10

iii) What if the stock drops to AED 11 per share?......................................................11

b) Differing forms of market efficiency...........................................................................12

2

PART A......................................................................................................................................4

1.1. Introduction.................................................................................................................4

1.2. Financial performance comparison of Hartalega Holdings Bhd and Supermax

corporation Bhd......................................................................................................................4

1.2.1. Hartalega Holdings Bhd.......................................................................................4

1.2.1.1. Current ratio..................................................................................................4

1.2.1.2. Equity ratio...................................................................................................5

1.2.1.3. Gross profit margin.......................................................................................5

1.2.1.4. Efficiency ratio.............................................................................................6

1.2.2. Supermax corporation Bhd..................................................................................6

1.2.2.1. Current ratio..................................................................................................6

1.2.2.2. Equity ratio...................................................................................................7

1.2.2.3. Gross profit margin.......................................................................................7

1.2.2.4. Efficiency ratio.............................................................................................7

1.3. Dividend policy...........................................................................................................8

1.3.1. Hartalega..............................................................................................................8

1.3.2. Supermax..............................................................................................................9

1.4. Corporate governance..................................................................................................9

1.4.1. Supermax..............................................................................................................9

1.4.2. Hartalega............................................................................................................10

Part B........................................................................................................................................10

i) Benefits and major drawback....................................................................................10

ii) What will be Ibrahim’s minimum profit if he buys two puts at the indicated price?

10

iii) What if the stock drops to AED 11 per share?......................................................11

b) Differing forms of market efficiency...........................................................................12

2

i) Weak form.................................................................................................................13

ii) Semi-strong form...................................................................................................13

iii) Strong form............................................................................................................13

References................................................................................................................................14

3

ii) Semi-strong form...................................................................................................13

iii) Strong form............................................................................................................13

References................................................................................................................................14

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART A

1.1. Introduction

According to Lee (2021) stated that the shares of top globe dropped by 17.7% this year while

two of its competitors Hartalega and supermax dropped between 18% and 30%. She added in

comparison with the FTSE Bursa Malaysia KLCI Index it fell by 0.9% during the same time,

the company however stated due to covid-19 its stocks had a significant jump last year due to

the increased demand for medical gloves. One of the factors withholding investor’s

confidence in stocks is the expected fall in the sale price of gloves due to lower demand as a

lot of individuals are being vaccinated. Lee (2021) also mentioned that the jump in the

average selling price of gloves isn’t sustainable as she added the forecast of a 30% to 35%

fall in prices in the year 2022 however the prices will likely remain above the pre-pandemic

levels for the next 2 to 3 years which is due to the demand for gloves expected to remain

elevated in the next coming years.

1.2. Financial performance comparison of Hartalega Holdings Bhd and

Supermax corporation Bhd

According to Hartalega annual report (2020) the revenues in the fiscal year 2020 was RM

2924.3 million from RM 2827.2 million in the fiscal year 2019 in comparison with Supermax

annual report (2020) was RM 2131.8 million in the fiscal year 2020 compared to RM 1538.2

million in the fiscal year 2019.

1.2.1. Hartalega Holdings Bhd

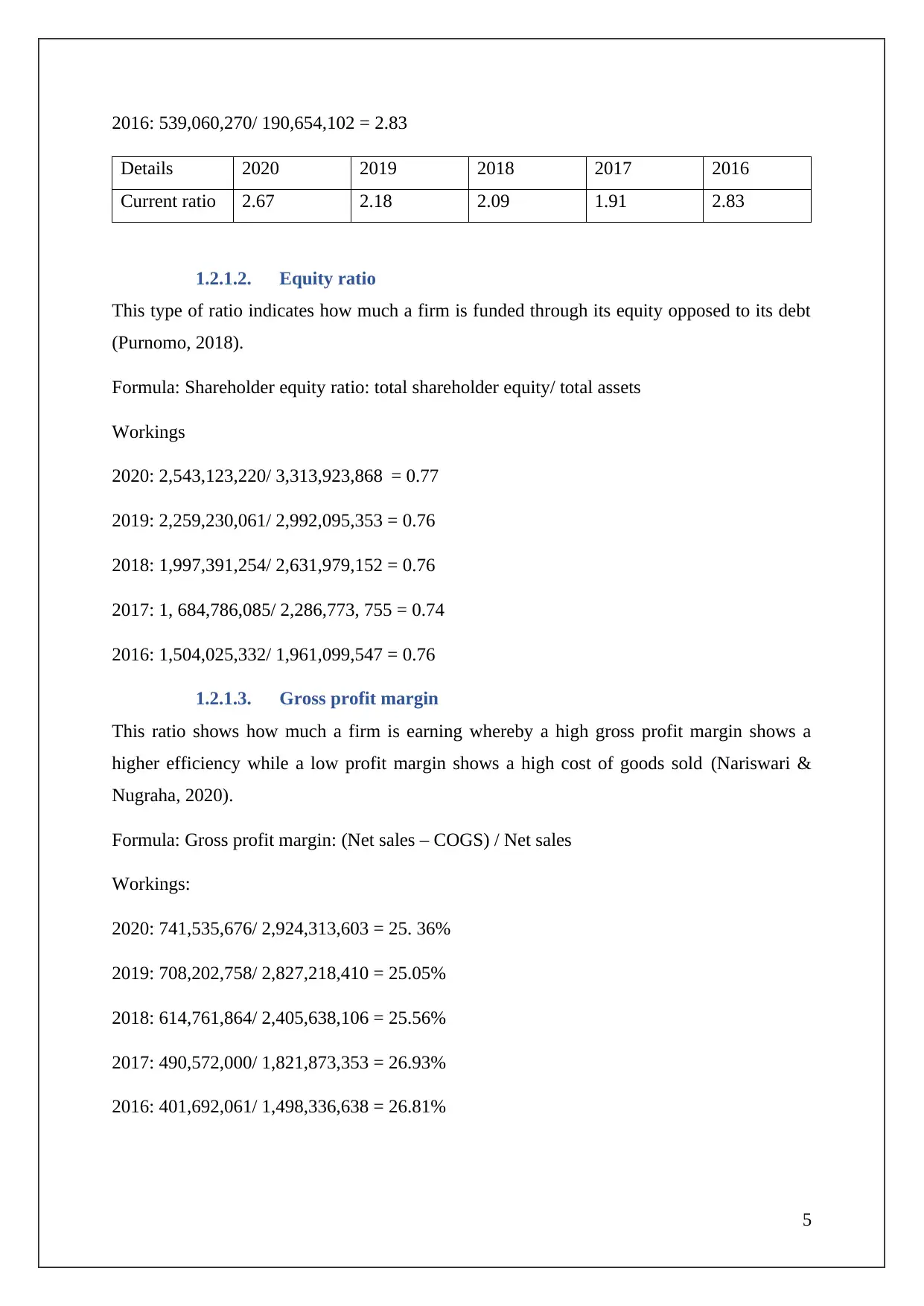

1.2.1.1. Current ratio

This ratio measures the firm’s ability to pay off its current liabilities within one year with its

total current assets (Purnomo, 2018).

Formula: Current ratio: current assets/ current liabilities

Workings:

2020: 1,088,521,433/ 407,039,182 = 2.67

2019: 897,441,784/ 411,888,771 = 2.18

2018: 866,359,157/ 413,552,543 = 2.09

2017: 691,713,291/ 363,016,270 = 1.91

4

1.1. Introduction

According to Lee (2021) stated that the shares of top globe dropped by 17.7% this year while

two of its competitors Hartalega and supermax dropped between 18% and 30%. She added in

comparison with the FTSE Bursa Malaysia KLCI Index it fell by 0.9% during the same time,

the company however stated due to covid-19 its stocks had a significant jump last year due to

the increased demand for medical gloves. One of the factors withholding investor’s

confidence in stocks is the expected fall in the sale price of gloves due to lower demand as a

lot of individuals are being vaccinated. Lee (2021) also mentioned that the jump in the

average selling price of gloves isn’t sustainable as she added the forecast of a 30% to 35%

fall in prices in the year 2022 however the prices will likely remain above the pre-pandemic

levels for the next 2 to 3 years which is due to the demand for gloves expected to remain

elevated in the next coming years.

1.2. Financial performance comparison of Hartalega Holdings Bhd and

Supermax corporation Bhd

According to Hartalega annual report (2020) the revenues in the fiscal year 2020 was RM

2924.3 million from RM 2827.2 million in the fiscal year 2019 in comparison with Supermax

annual report (2020) was RM 2131.8 million in the fiscal year 2020 compared to RM 1538.2

million in the fiscal year 2019.

1.2.1. Hartalega Holdings Bhd

1.2.1.1. Current ratio

This ratio measures the firm’s ability to pay off its current liabilities within one year with its

total current assets (Purnomo, 2018).

Formula: Current ratio: current assets/ current liabilities

Workings:

2020: 1,088,521,433/ 407,039,182 = 2.67

2019: 897,441,784/ 411,888,771 = 2.18

2018: 866,359,157/ 413,552,543 = 2.09

2017: 691,713,291/ 363,016,270 = 1.91

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2016: 539,060,270/ 190,654,102 = 2.83

Details 2020 2019 2018 2017 2016

Current ratio 2.67 2.18 2.09 1.91 2.83

1.2.1.2. Equity ratio

This type of ratio indicates how much a firm is funded through its equity opposed to its debt

(Purnomo, 2018).

Formula: Shareholder equity ratio: total shareholder equity/ total assets

Workings

2020: 2,543,123,220/ 3,313,923,868 = 0.77

2019: 2,259,230,061/ 2,992,095,353 = 0.76

2018: 1,997,391,254/ 2,631,979,152 = 0.76

2017: 1, 684,786,085/ 2,286,773, 755 = 0.74

2016: 1,504,025,332/ 1,961,099,547 = 0.76

1.2.1.3. Gross profit margin

This ratio shows how much a firm is earning whereby a high gross profit margin shows a

higher efficiency while a low profit margin shows a high cost of goods sold (Nariswari &

Nugraha, 2020).

Formula: Gross profit margin: (Net sales – COGS) / Net sales

Workings:

2020: 741,535,676/ 2,924,313,603 = 25. 36%

2019: 708,202,758/ 2,827,218,410 = 25.05%

2018: 614,761,864/ 2,405,638,106 = 25.56%

2017: 490,572,000/ 1,821,873,353 = 26.93%

2016: 401,692,061/ 1,498,336,638 = 26.81%

5

Details 2020 2019 2018 2017 2016

Current ratio 2.67 2.18 2.09 1.91 2.83

1.2.1.2. Equity ratio

This type of ratio indicates how much a firm is funded through its equity opposed to its debt

(Purnomo, 2018).

Formula: Shareholder equity ratio: total shareholder equity/ total assets

Workings

2020: 2,543,123,220/ 3,313,923,868 = 0.77

2019: 2,259,230,061/ 2,992,095,353 = 0.76

2018: 1,997,391,254/ 2,631,979,152 = 0.76

2017: 1, 684,786,085/ 2,286,773, 755 = 0.74

2016: 1,504,025,332/ 1,961,099,547 = 0.76

1.2.1.3. Gross profit margin

This ratio shows how much a firm is earning whereby a high gross profit margin shows a

higher efficiency while a low profit margin shows a high cost of goods sold (Nariswari &

Nugraha, 2020).

Formula: Gross profit margin: (Net sales – COGS) / Net sales

Workings:

2020: 741,535,676/ 2,924,313,603 = 25. 36%

2019: 708,202,758/ 2,827,218,410 = 25.05%

2018: 614,761,864/ 2,405,638,106 = 25.56%

2017: 490,572,000/ 1,821,873,353 = 26.93%

2016: 401,692,061/ 1,498,336,638 = 26.81%

5

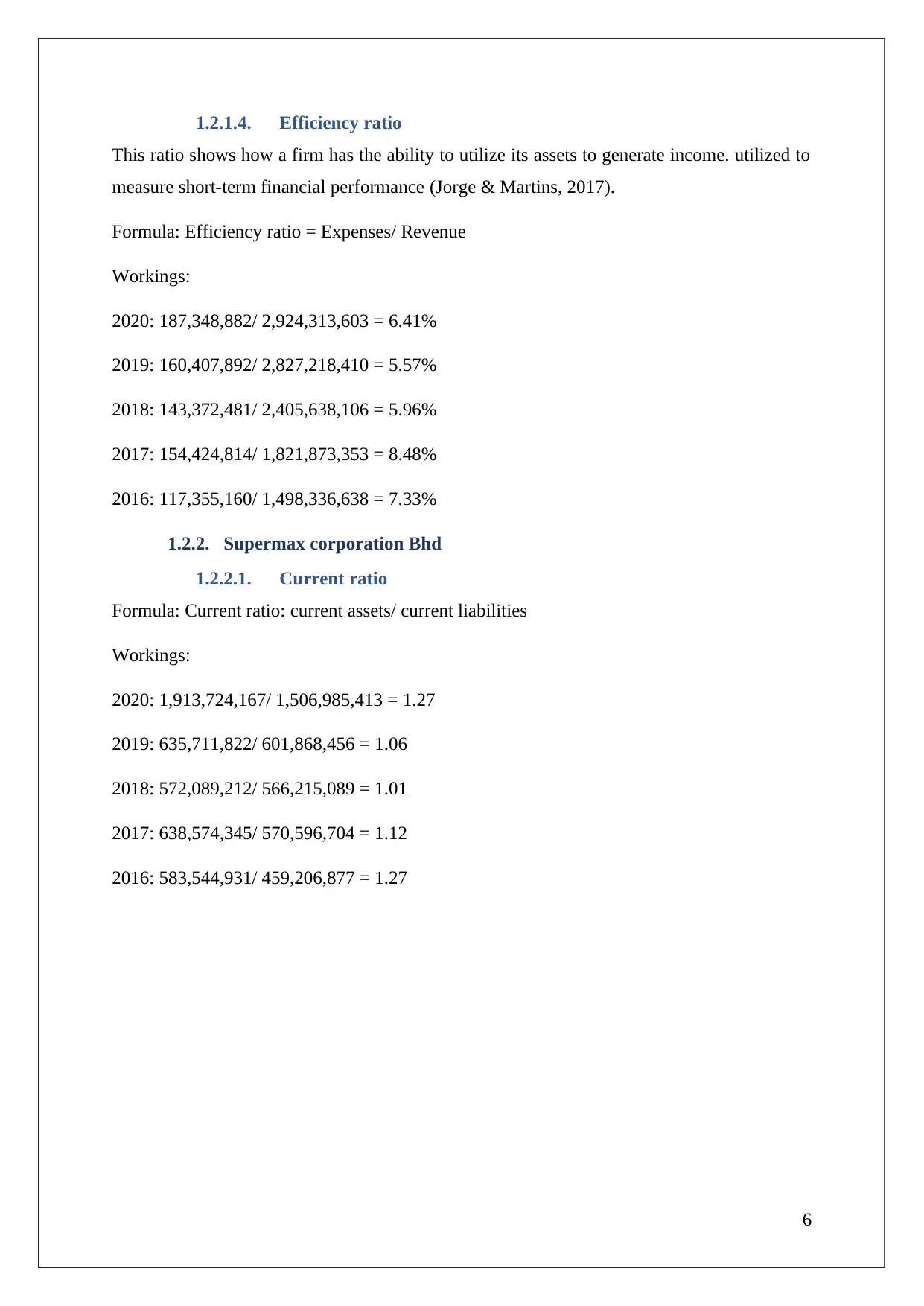

1.2.1.4. Efficiency ratio

This ratio shows how a firm has the ability to utilize its assets to generate income. utilized to

measure short-term financial performance (Jorge & Martins, 2017).

Formula: Efficiency ratio = Expenses/ Revenue

Workings:

2020: 187,348,882/ 2,924,313,603 = 6.41%

2019: 160,407,892/ 2,827,218,410 = 5.57%

2018: 143,372,481/ 2,405,638,106 = 5.96%

2017: 154,424,814/ 1,821,873,353 = 8.48%

2016: 117,355,160/ 1,498,336,638 = 7.33%

1.2.2. Supermax corporation Bhd

1.2.2.1. Current ratio

Formula: Current ratio: current assets/ current liabilities

Workings:

2020: 1,913,724,167/ 1,506,985,413 = 1.27

2019: 635,711,822/ 601,868,456 = 1.06

2018: 572,089,212/ 566,215,089 = 1.01

2017: 638,574,345/ 570,596,704 = 1.12

2016: 583,544,931/ 459,206,877 = 1.27

6

This ratio shows how a firm has the ability to utilize its assets to generate income. utilized to

measure short-term financial performance (Jorge & Martins, 2017).

Formula: Efficiency ratio = Expenses/ Revenue

Workings:

2020: 187,348,882/ 2,924,313,603 = 6.41%

2019: 160,407,892/ 2,827,218,410 = 5.57%

2018: 143,372,481/ 2,405,638,106 = 5.96%

2017: 154,424,814/ 1,821,873,353 = 8.48%

2016: 117,355,160/ 1,498,336,638 = 7.33%

1.2.2. Supermax corporation Bhd

1.2.2.1. Current ratio

Formula: Current ratio: current assets/ current liabilities

Workings:

2020: 1,913,724,167/ 1,506,985,413 = 1.27

2019: 635,711,822/ 601,868,456 = 1.06

2018: 572,089,212/ 566,215,089 = 1.01

2017: 638,574,345/ 570,596,704 = 1.12

2016: 583,544,931/ 459,206,877 = 1.27

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

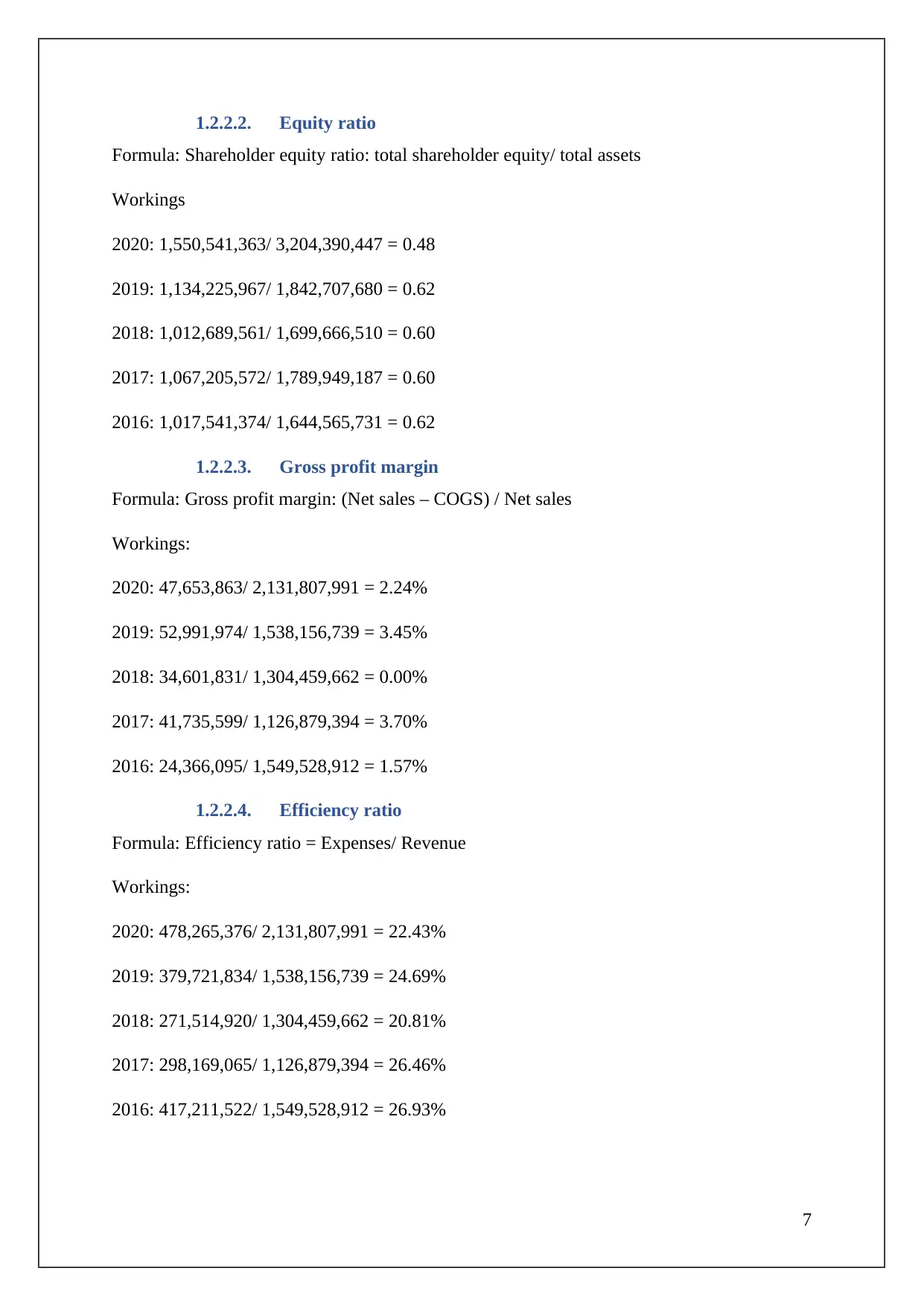

1.2.2.2. Equity ratio

Formula: Shareholder equity ratio: total shareholder equity/ total assets

Workings

2020: 1,550,541,363/ 3,204,390,447 = 0.48

2019: 1,134,225,967/ 1,842,707,680 = 0.62

2018: 1,012,689,561/ 1,699,666,510 = 0.60

2017: 1,067,205,572/ 1,789,949,187 = 0.60

2016: 1,017,541,374/ 1,644,565,731 = 0.62

1.2.2.3. Gross profit margin

Formula: Gross profit margin: (Net sales – COGS) / Net sales

Workings:

2020: 47,653,863/ 2,131,807,991 = 2.24%

2019: 52,991,974/ 1,538,156,739 = 3.45%

2018: 34,601,831/ 1,304,459,662 = 0.00%

2017: 41,735,599/ 1,126,879,394 = 3.70%

2016: 24,366,095/ 1,549,528,912 = 1.57%

1.2.2.4. Efficiency ratio

Formula: Efficiency ratio = Expenses/ Revenue

Workings:

2020: 478,265,376/ 2,131,807,991 = 22.43%

2019: 379,721,834/ 1,538,156,739 = 24.69%

2018: 271,514,920/ 1,304,459,662 = 20.81%

2017: 298,169,065/ 1,126,879,394 = 26.46%

2016: 417,211,522/ 1,549,528,912 = 26.93%

7

Formula: Shareholder equity ratio: total shareholder equity/ total assets

Workings

2020: 1,550,541,363/ 3,204,390,447 = 0.48

2019: 1,134,225,967/ 1,842,707,680 = 0.62

2018: 1,012,689,561/ 1,699,666,510 = 0.60

2017: 1,067,205,572/ 1,789,949,187 = 0.60

2016: 1,017,541,374/ 1,644,565,731 = 0.62

1.2.2.3. Gross profit margin

Formula: Gross profit margin: (Net sales – COGS) / Net sales

Workings:

2020: 47,653,863/ 2,131,807,991 = 2.24%

2019: 52,991,974/ 1,538,156,739 = 3.45%

2018: 34,601,831/ 1,304,459,662 = 0.00%

2017: 41,735,599/ 1,126,879,394 = 3.70%

2016: 24,366,095/ 1,549,528,912 = 1.57%

1.2.2.4. Efficiency ratio

Formula: Efficiency ratio = Expenses/ Revenue

Workings:

2020: 478,265,376/ 2,131,807,991 = 22.43%

2019: 379,721,834/ 1,538,156,739 = 24.69%

2018: 271,514,920/ 1,304,459,662 = 20.81%

2017: 298,169,065/ 1,126,879,394 = 26.46%

2016: 417,211,522/ 1,549,528,912 = 26.93%

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

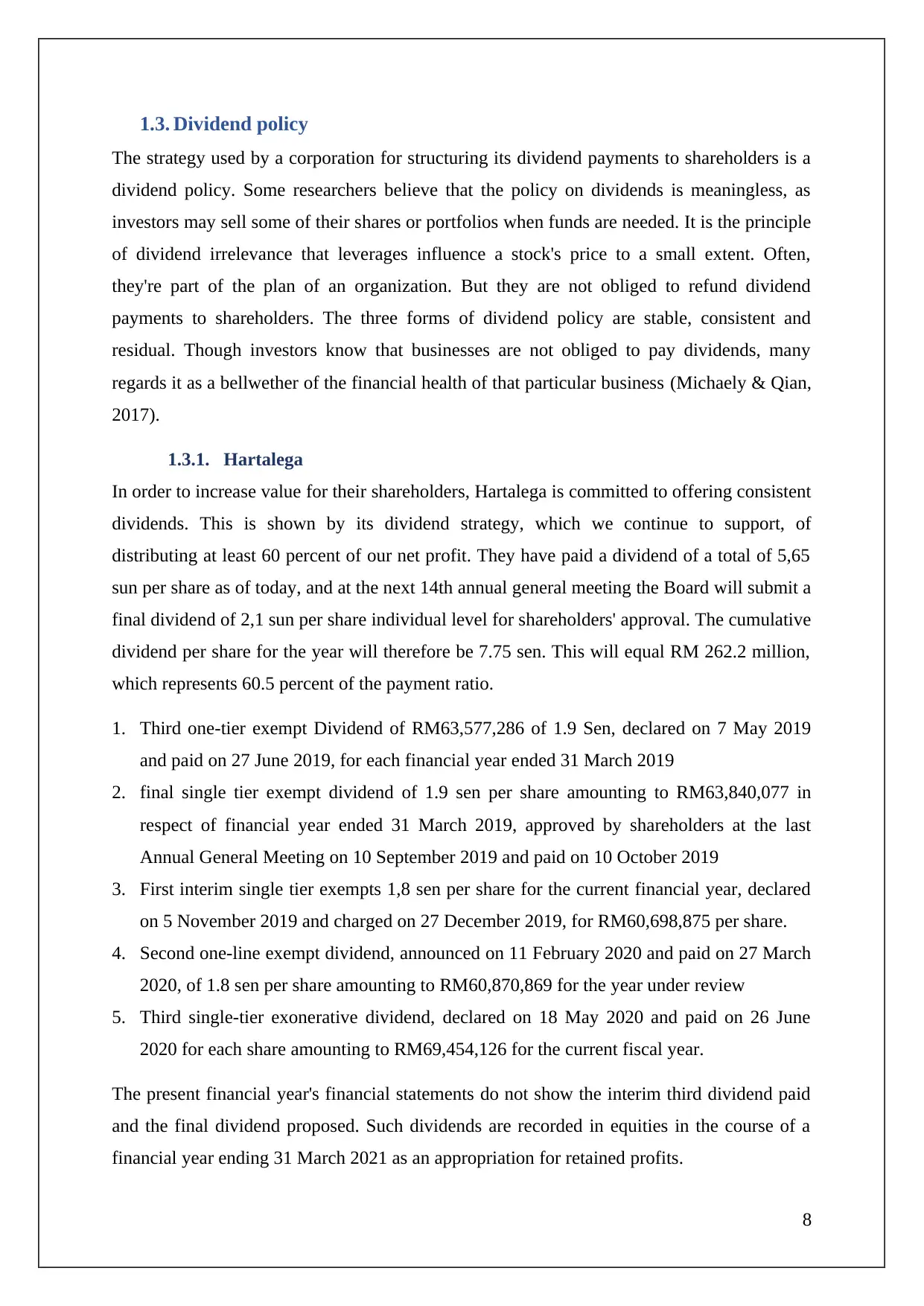

1.3. Dividend policy

The strategy used by a corporation for structuring its dividend payments to shareholders is a

dividend policy. Some researchers believe that the policy on dividends is meaningless, as

investors may sell some of their shares or portfolios when funds are needed. It is the principle

of dividend irrelevance that leverages influence a stock's price to a small extent. Often,

they're part of the plan of an organization. But they are not obliged to refund dividend

payments to shareholders. The three forms of dividend policy are stable, consistent and

residual. Though investors know that businesses are not obliged to pay dividends, many

regards it as a bellwether of the financial health of that particular business (Michaely & Qian,

2017).

1.3.1. Hartalega

In order to increase value for their shareholders, Hartalega is committed to offering consistent

dividends. This is shown by its dividend strategy, which we continue to support, of

distributing at least 60 percent of our net profit. They have paid a dividend of a total of 5,65

sun per share as of today, and at the next 14th annual general meeting the Board will submit a

final dividend of 2,1 sun per share individual level for shareholders' approval. The cumulative

dividend per share for the year will therefore be 7.75 sen. This will equal RM 262.2 million,

which represents 60.5 percent of the payment ratio.

1. Third one-tier exempt Dividend of RM63,577,286 of 1.9 Sen, declared on 7 May 2019

and paid on 27 June 2019, for each financial year ended 31 March 2019

2. final single tier exempt dividend of 1.9 sen per share amounting to RM63,840,077 in

respect of financial year ended 31 March 2019, approved by shareholders at the last

Annual General Meeting on 10 September 2019 and paid on 10 October 2019

3. First interim single tier exempts 1,8 sen per share for the current financial year, declared

on 5 November 2019 and charged on 27 December 2019, for RM60,698,875 per share.

4. Second one-line exempt dividend, announced on 11 February 2020 and paid on 27 March

2020, of 1.8 sen per share amounting to RM60,870,869 for the year under review

5. Third single-tier exonerative dividend, declared on 18 May 2020 and paid on 26 June

2020 for each share amounting to RM69,454,126 for the current fiscal year.

The present financial year's financial statements do not show the interim third dividend paid

and the final dividend proposed. Such dividends are recorded in equities in the course of a

financial year ending 31 March 2021 as an appropriation for retained profits.

8

The strategy used by a corporation for structuring its dividend payments to shareholders is a

dividend policy. Some researchers believe that the policy on dividends is meaningless, as

investors may sell some of their shares or portfolios when funds are needed. It is the principle

of dividend irrelevance that leverages influence a stock's price to a small extent. Often,

they're part of the plan of an organization. But they are not obliged to refund dividend

payments to shareholders. The three forms of dividend policy are stable, consistent and

residual. Though investors know that businesses are not obliged to pay dividends, many

regards it as a bellwether of the financial health of that particular business (Michaely & Qian,

2017).

1.3.1. Hartalega

In order to increase value for their shareholders, Hartalega is committed to offering consistent

dividends. This is shown by its dividend strategy, which we continue to support, of

distributing at least 60 percent of our net profit. They have paid a dividend of a total of 5,65

sun per share as of today, and at the next 14th annual general meeting the Board will submit a

final dividend of 2,1 sun per share individual level for shareholders' approval. The cumulative

dividend per share for the year will therefore be 7.75 sen. This will equal RM 262.2 million,

which represents 60.5 percent of the payment ratio.

1. Third one-tier exempt Dividend of RM63,577,286 of 1.9 Sen, declared on 7 May 2019

and paid on 27 June 2019, for each financial year ended 31 March 2019

2. final single tier exempt dividend of 1.9 sen per share amounting to RM63,840,077 in

respect of financial year ended 31 March 2019, approved by shareholders at the last

Annual General Meeting on 10 September 2019 and paid on 10 October 2019

3. First interim single tier exempts 1,8 sen per share for the current financial year, declared

on 5 November 2019 and charged on 27 December 2019, for RM60,698,875 per share.

4. Second one-line exempt dividend, announced on 11 February 2020 and paid on 27 March

2020, of 1.8 sen per share amounting to RM60,870,869 for the year under review

5. Third single-tier exonerative dividend, declared on 18 May 2020 and paid on 26 June

2020 for each share amounting to RM69,454,126 for the current fiscal year.

The present financial year's financial statements do not show the interim third dividend paid

and the final dividend proposed. Such dividends are recorded in equities in the course of a

financial year ending 31 March 2021 as an appropriation for retained profits.

8

1.3.2. Supermax

The Group strongly supports the value of shareholders. Over the current financial year, it

allocated its shareholders with a final dividend of 20.1 million shares, with a ratio of one

treasury share, for every 65 common equity shares owned on the financial year ended 30 June

2019. It proposed again a distribution of the share dividend from the treasury shares owned

by the Company in the financial year ended 30 June 2020. For every 45 common shares kept

subject to shareholder consent at the next 23rd Annual General Meeting the Board of

Directors proposed this year to have a ratio of 1 treasury share.

They are also aware of the importance of increasing shareholder equity with a strengthened

balance sheet and increased operating capacity. At the next Annual General Assembly for the

financial year ended 30 June 2020, the Board of Directors proposed an equity dividend

payout for shareholders' consent and is further seeking rewarding shareholders for ongoing

support with a special starting dividend for the next financial year ended 30 June 2021.

1.4. Corporate governance

Corporate governance is a code of rules, procedures and practices that determine how the

board of directors of a corporation handles and monitors a company's operations. Corporate

governance covers transparency, accountability and security values. At the very least, poor

corporate governance leads to an unfulfilled business and, at worst, can lead to a company's

dissolution and substantial financial losses for its shareholders. Maybe the recognition of

shareholders is one of the most relevant corporate governance concepts (Lisboa et al., 2020).

1.4.1. Supermax

Supermax also recognizes the importance in the highest standards of corporate governance

across the Group as an essential part of its work in defending and enhancing the value of

stakeholders, and has taken all appropriate measures to guarantee that best practices are

applied and embraced wherever possible. In that context, steps and efforts have been made to

ensure that principles and best practices as provided for in the Malaysian Corporate

Governance Code ('the Code') and Bursa Securities Berhad's ('Boursa Securities') Main

Market Listing Requirement ('MMLR') are adopted and applied in a feasible manner.

9

The Group strongly supports the value of shareholders. Over the current financial year, it

allocated its shareholders with a final dividend of 20.1 million shares, with a ratio of one

treasury share, for every 65 common equity shares owned on the financial year ended 30 June

2019. It proposed again a distribution of the share dividend from the treasury shares owned

by the Company in the financial year ended 30 June 2020. For every 45 common shares kept

subject to shareholder consent at the next 23rd Annual General Meeting the Board of

Directors proposed this year to have a ratio of 1 treasury share.

They are also aware of the importance of increasing shareholder equity with a strengthened

balance sheet and increased operating capacity. At the next Annual General Assembly for the

financial year ended 30 June 2020, the Board of Directors proposed an equity dividend

payout for shareholders' consent and is further seeking rewarding shareholders for ongoing

support with a special starting dividend for the next financial year ended 30 June 2021.

1.4. Corporate governance

Corporate governance is a code of rules, procedures and practices that determine how the

board of directors of a corporation handles and monitors a company's operations. Corporate

governance covers transparency, accountability and security values. At the very least, poor

corporate governance leads to an unfulfilled business and, at worst, can lead to a company's

dissolution and substantial financial losses for its shareholders. Maybe the recognition of

shareholders is one of the most relevant corporate governance concepts (Lisboa et al., 2020).

1.4.1. Supermax

Supermax also recognizes the importance in the highest standards of corporate governance

across the Group as an essential part of its work in defending and enhancing the value of

stakeholders, and has taken all appropriate measures to guarantee that best practices are

applied and embraced wherever possible. In that context, steps and efforts have been made to

ensure that principles and best practices as provided for in the Malaysian Corporate

Governance Code ('the Code') and Bursa Securities Berhad's ('Boursa Securities') Main

Market Listing Requirement ('MMLR') are adopted and applied in a feasible manner.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.4.2. Hartalega

The Board is well aware of the importance of defining clearly defined roles and obligations

for the execution of its duties of trust and governance, including those for the approval of the

Board. By defining the functions, tasks and duties, the Board's corporate governance

standards and practices to be followed and key issues reserved for the Board's approval, the

Board has defined its board of directors’ charter & schedule of matters. Sustainable

development requires good governance at all levels. The Board is committed to the highest

standards of the Group's corporate governance and ethical standards. A whistleblowing

policy and procedure has been developed to provide a forum for the reporting of alleged

misconducted activities that may adversely affect the Group by managers, employees,

shareholders, suppliers or any party with a business relationship with the company. The

Company handles all complaints confidentially and protects anyone who reports those issues

in good faith at the same time.

Part B

i) Benefits and major drawback

Ibrahim has 200*(AED18-AED12) =AED 1200 unrealized capital benefit A person who

wants to preserve his earnings can either sell the stock and profit while losing the stock's

upward potential or he can purchase the stock to lock up his profit. The biggest drawback

with the second choice is that the put costs are 2*AED1.5*100=AED300 plus a brokerage

fee.

ii) What will be Ibrahim’s minimum profit if he buys two puts at the indicated

price?

if Ibrahim buys the two part, the minimum before tax profit he can grasp can be calculated as

follows:

Present market value of the inventory = AED 18*200=AED3,600

Less purchases price of the inventory. =AED 12*200=AED2,400

Capital increase =AED 1,200

Less cost of two put option

Lowest profit = AED 900

10

The Board is well aware of the importance of defining clearly defined roles and obligations

for the execution of its duties of trust and governance, including those for the approval of the

Board. By defining the functions, tasks and duties, the Board's corporate governance

standards and practices to be followed and key issues reserved for the Board's approval, the

Board has defined its board of directors’ charter & schedule of matters. Sustainable

development requires good governance at all levels. The Board is committed to the highest

standards of the Group's corporate governance and ethical standards. A whistleblowing

policy and procedure has been developed to provide a forum for the reporting of alleged

misconducted activities that may adversely affect the Group by managers, employees,

shareholders, suppliers or any party with a business relationship with the company. The

Company handles all complaints confidentially and protects anyone who reports those issues

in good faith at the same time.

Part B

i) Benefits and major drawback

Ibrahim has 200*(AED18-AED12) =AED 1200 unrealized capital benefit A person who

wants to preserve his earnings can either sell the stock and profit while losing the stock's

upward potential or he can purchase the stock to lock up his profit. The biggest drawback

with the second choice is that the put costs are 2*AED1.5*100=AED300 plus a brokerage

fee.

ii) What will be Ibrahim’s minimum profit if he buys two puts at the indicated

price?

if Ibrahim buys the two part, the minimum before tax profit he can grasp can be calculated as

follows:

Present market value of the inventory = AED 18*200=AED3,600

Less purchases price of the inventory. =AED 12*200=AED2,400

Capital increase =AED 1,200

Less cost of two put option

Lowest profit = AED 900

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ibrahim's profit prior to taxes would be AED18-AED12) = AED1,200 if the stock were to be

sold immediately without a hedging. Notice that this year is to be subject to latter taxes

(AED1,200), with the next year being due to latter taxes (AED900).

*200=FD11,200 18 FD12) Notice that the latter tax (AED1,200) is due this year, and the

former tax (AED900) is due the next year.

iii) What if the stock drops to AED 11 per share?

If Ibrahim buys two options and AED25 shifts in stock price, the investment's market value at

the expiry of the option is as follows:

Cost of inventory =200* AED25 = AED5,000

Less: buying cost of inventory =200* AED12= AED2,400

Capital gains =AED2,600

Less cost of puts =2* AED150= AED300

Net profit = AED 2,300

Memo: the put will upon expiration, denoting that Ibrahim will lose the puts.

Ibrahim's stock will incur losses on the stock, but will benefit on the pit when it falls to AED

11 (from its current AED18 price). The following can be computed. Stock:

Value of stock =200* AED11= AED2,200

Less: purchase price =200* AED12=AED2,400

Profit on stock =-AED200 (loss)

Puts

Value of puts = (AED18- AED11) *200= AED1,800

Cost of the puts =2*AED150. =300

Less purchase price =200 * AED12=AED2400

Profit on stock =-AED200(loss)

Puts

Value of put =(AED18-AED11) *200= AED1,800

11

sold immediately without a hedging. Notice that this year is to be subject to latter taxes

(AED1,200), with the next year being due to latter taxes (AED900).

*200=FD11,200 18 FD12) Notice that the latter tax (AED1,200) is due this year, and the

former tax (AED900) is due the next year.

iii) What if the stock drops to AED 11 per share?

If Ibrahim buys two options and AED25 shifts in stock price, the investment's market value at

the expiry of the option is as follows:

Cost of inventory =200* AED25 = AED5,000

Less: buying cost of inventory =200* AED12= AED2,400

Capital gains =AED2,600

Less cost of puts =2* AED150= AED300

Net profit = AED 2,300

Memo: the put will upon expiration, denoting that Ibrahim will lose the puts.

Ibrahim's stock will incur losses on the stock, but will benefit on the pit when it falls to AED

11 (from its current AED18 price). The following can be computed. Stock:

Value of stock =200* AED11= AED2,200

Less: purchase price =200* AED12=AED2,400

Profit on stock =-AED200 (loss)

Puts

Value of puts = (AED18- AED11) *200= AED1,800

Cost of the puts =2*AED150. =300

Less purchase price =200 * AED12=AED2400

Profit on stock =-AED200(loss)

Puts

Value of put =(AED18-AED11) *200= AED1,800

11

Cost of the put =2*AED150=AED300

Profit on put =AED1,500

Total profit =AED1,300

If Ibrahim believes that the market will soon crash, he should buy the puts to protect his

investment's profit but if the future increases the demand. The great benefit of a hedge is that

it enables investment to take advantage of the rising profit potential while at the same time

maintaining the long transaction gains already generated. In the worst case, the hedge will

only lead to the expense of the hedge.

b) Differing forms of market efficiency

Market efficiency relates to the degree to which all relevant knowledge is accessible at

market rates. If all information is successful on markets, it is not possible to "slap" the market

by the fact that undervalued or overvalued securities are not available at this point. The term

is used by economist Eugene Fama in 1970, but Fama recognizes it as a little misleading,

since none of them can fully determine or reliably calculate this so-called market efficiency.

Despite these restrictions, the term refers to what is considered best as the efficient

hypothesis of the market (EMH) (Jarrow & Larsson, 2012).

Market efficiency is at the heart of markets' ability to integrate knowledge that offers

securities sellers and buyers maximum opportunities for conducting transactions without

increasing transaction costs. It's a highly controversial issue among scientists and

professionals, whether or not markets such as the US stock market are successful (Jarrow &

Larsson, 2012).

The theory of the market is generally efficient, but the effective market hypothesis is

generally provided in three versions: faint, half-solid, and strong. The simple market-efficient

hypothesis suggests that the market cannot be overcome as all the relevant determinative

knowledge is incorporated into current share prices. Accordingly, stocks sell at equal value

does not underestimate or over valuate them. The theory determines that it is by solely

specific investments that pose a significant risk that investors will achieve higher returns

upon their investments (Jarrow & Larsson, 2012).

12

Profit on put =AED1,500

Total profit =AED1,300

If Ibrahim believes that the market will soon crash, he should buy the puts to protect his

investment's profit but if the future increases the demand. The great benefit of a hedge is that

it enables investment to take advantage of the rising profit potential while at the same time

maintaining the long transaction gains already generated. In the worst case, the hedge will

only lead to the expense of the hedge.

b) Differing forms of market efficiency

Market efficiency relates to the degree to which all relevant knowledge is accessible at

market rates. If all information is successful on markets, it is not possible to "slap" the market

by the fact that undervalued or overvalued securities are not available at this point. The term

is used by economist Eugene Fama in 1970, but Fama recognizes it as a little misleading,

since none of them can fully determine or reliably calculate this so-called market efficiency.

Despite these restrictions, the term refers to what is considered best as the efficient

hypothesis of the market (EMH) (Jarrow & Larsson, 2012).

Market efficiency is at the heart of markets' ability to integrate knowledge that offers

securities sellers and buyers maximum opportunities for conducting transactions without

increasing transaction costs. It's a highly controversial issue among scientists and

professionals, whether or not markets such as the US stock market are successful (Jarrow &

Larsson, 2012).

The theory of the market is generally efficient, but the effective market hypothesis is

generally provided in three versions: faint, half-solid, and strong. The simple market-efficient

hypothesis suggests that the market cannot be overcome as all the relevant determinative

knowledge is incorporated into current share prices. Accordingly, stocks sell at equal value

does not underestimate or over valuate them. The theory determines that it is by solely

specific investments that pose a significant risk that investors will achieve higher returns

upon their investments (Jarrow & Larsson, 2012).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.