Detailed Financial Analysis Report: Heiniken and Farsons Comparison

VerifiedAdded on 2023/01/18

|24

|3963

|33

Report

AI Summary

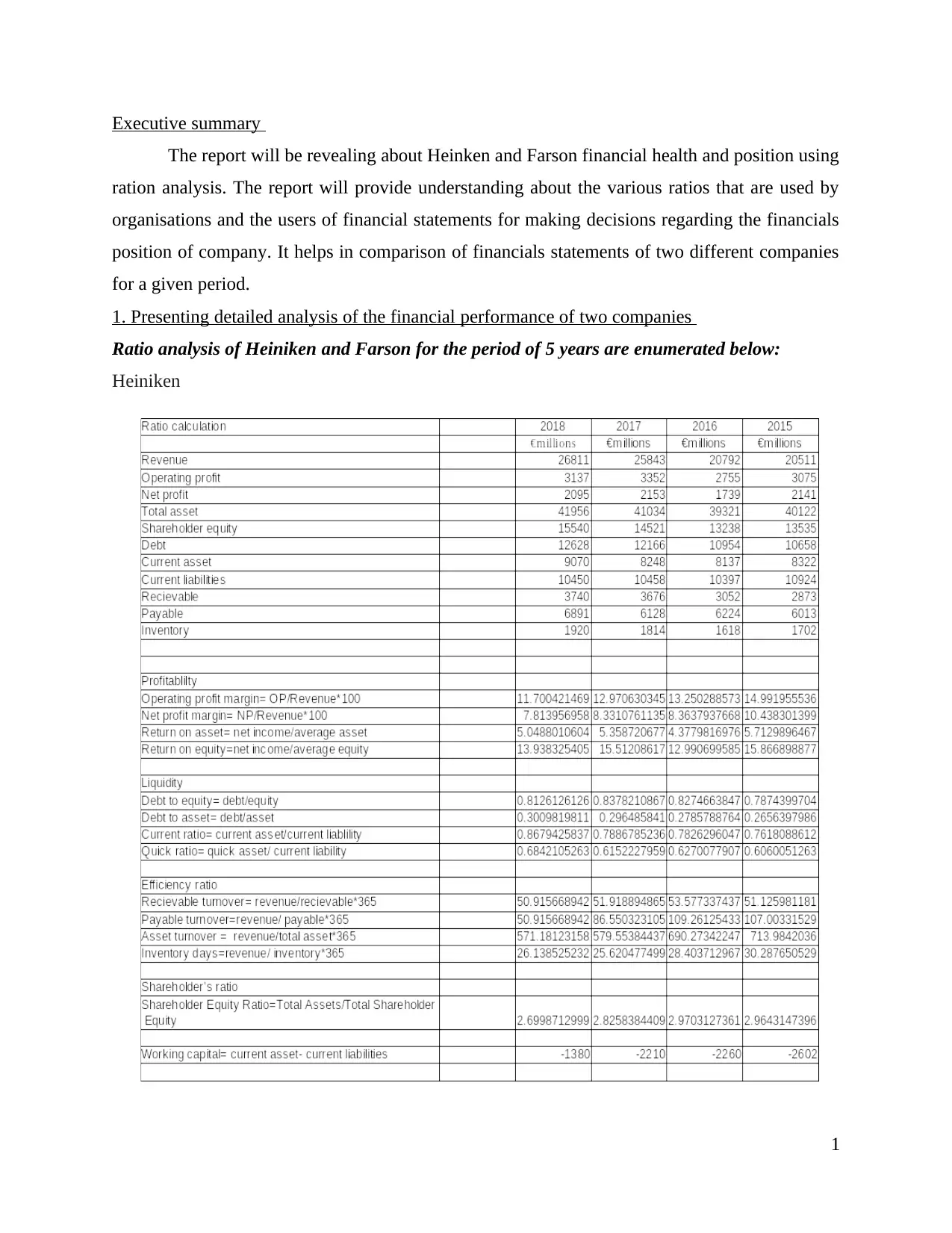

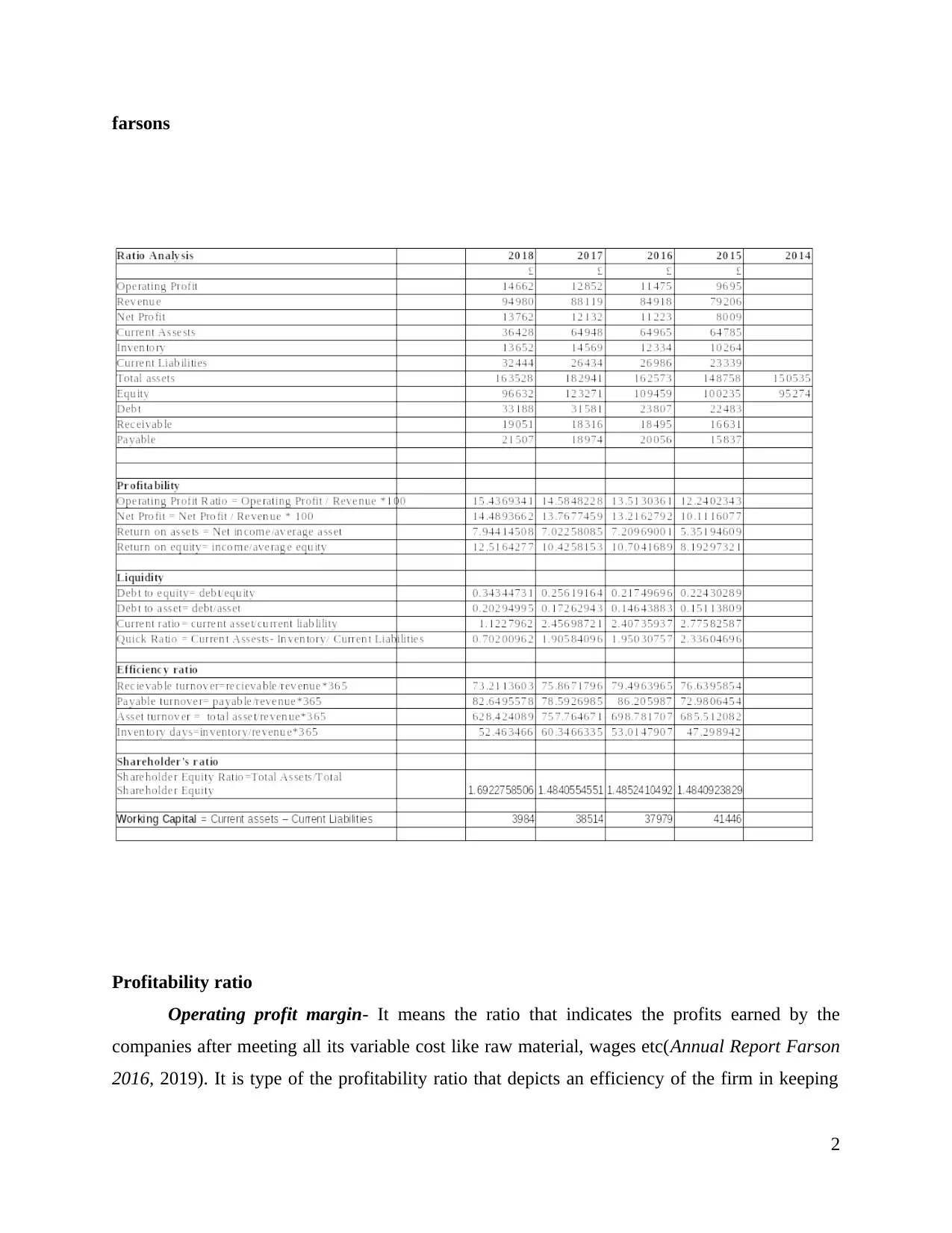

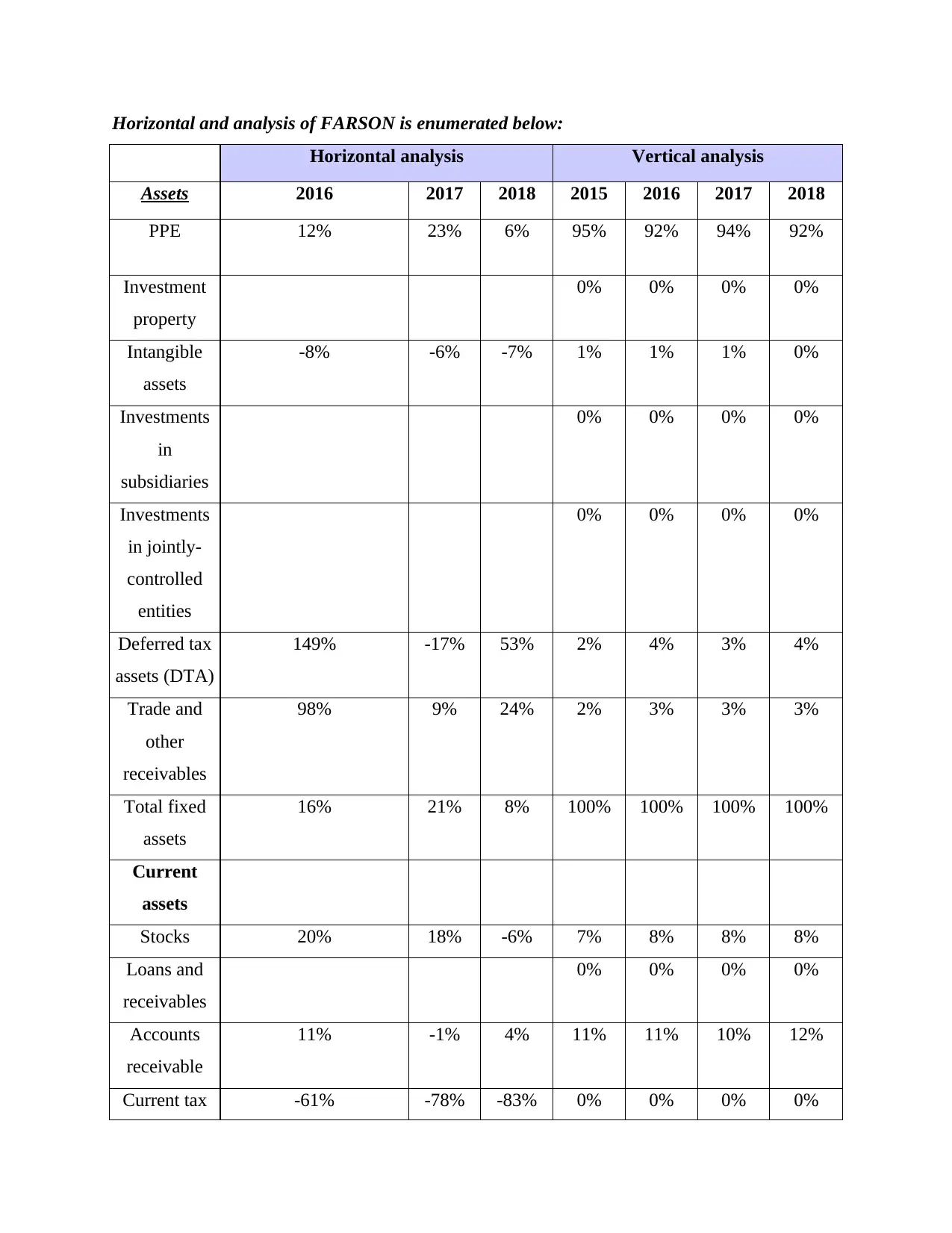

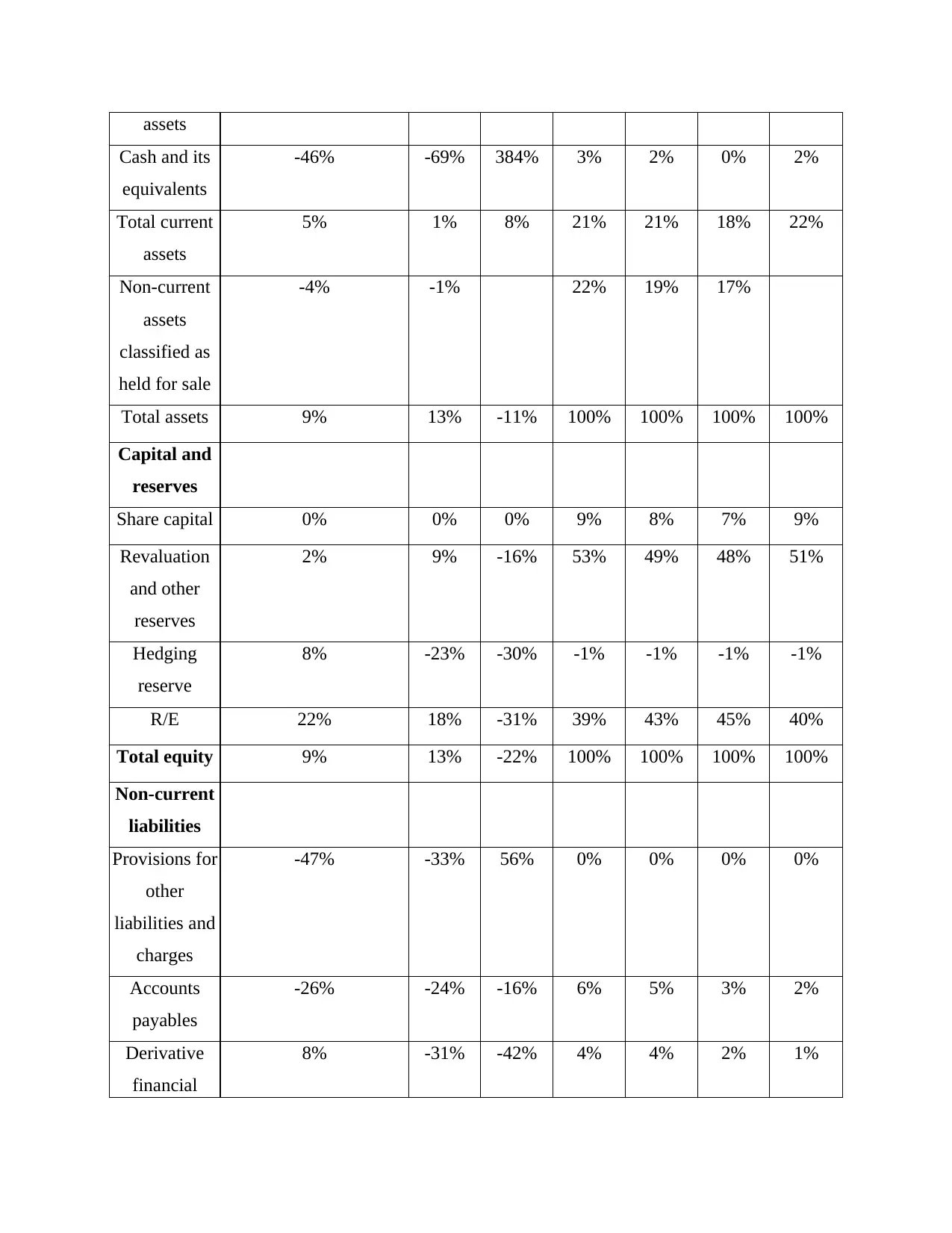

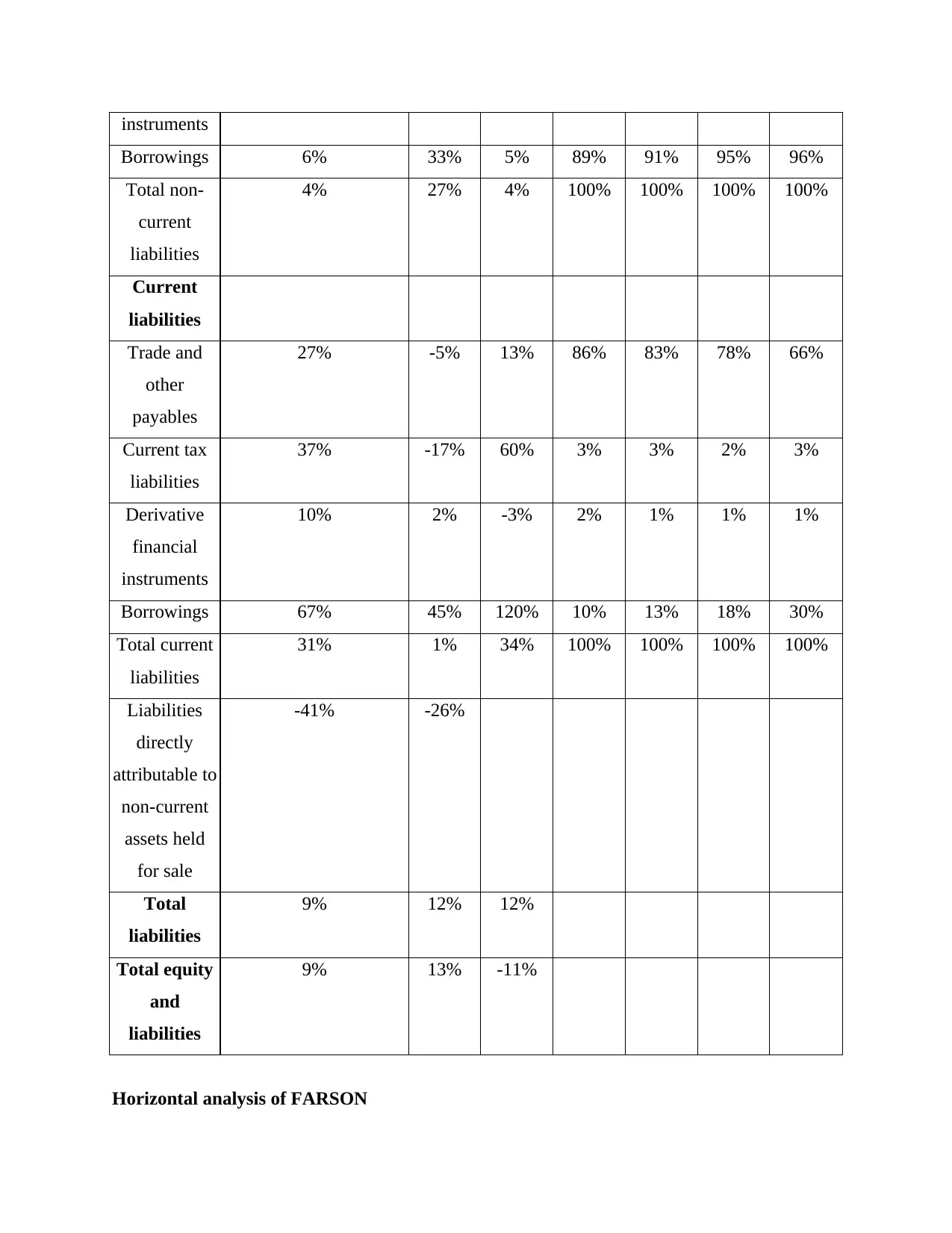

This report provides a comprehensive financial analysis of two companies, Heiniken and Farsons, using ratio analysis to assess their financial health and performance over a five-year period. The analysis includes detailed examinations of profitability ratios (operating profit margin, net profit margin, return on assets, and return on equity), leverage ratios (debt-equity ratio, debt-assets ratio), liquidity ratios (current ratio, quick ratio), efficiency ratios (receivable turnover, payable turnover, asset turnover, and inventory days), and shareholders' ratios. The report also incorporates horizontal and vertical analyses of the profit and loss statements and balance sheets of Farsons and Heiniken, providing a comparative overview of their financial positions and trends. The findings highlight the strengths and weaknesses of each company, offering insights into their operational efficiency, debt management, liquidity, and overall financial performance, concluding with recommendations based on these analyses. This report is a student contribution to Desklib, a platform offering AI-powered study tools and past assignments to help students excel in their academics.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.