Financial Analysis and Comparison of H&M and GAP: MBA Report

VerifiedAdded on 2022/11/28

|16

|3151

|442

Report

AI Summary

This report presents a financial analysis comparing the performance of two major companies, H&M and GAP. The analysis includes an introduction to the companies, followed by a critical comparison of their financial performance over several years. The core of the report focuses on a detailed examination of various financial ratios, including profitability ratios such as gross profit margin and net profit margin, liquidity ratios like the current ratio, and solvency ratios, specifically the debt-to-equity ratio. The report provides a five-year performance summary for both companies, utilizing tables and figures to illustrate trends. The analysis aims to assess the companies' financial health, efficiency, and ability to meet their obligations, ultimately leading to a conclusion regarding their investment potential. The study also addresses limitations and assumptions made during the analysis, providing a comprehensive overview of the financial standing of both companies.

Running head: FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

Name of the Student

Name of the University

Author Note

FINANCIAL ANALYSIS

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS

Table of Contents

Introduction......................................................................................................................................2

GAP.................................................................................................................................................2

H and M...........................................................................................................................................3

Critical comparison and financial performance over the last few years..........................................3

Profitability ratio..............................................................................................................................4

Gross Profit Margin.........................................................................................................................4

Net profit Margin.............................................................................................................................6

Liquidity..........................................................................................................................................7

Current Ratio...................................................................................................................................7

Solvency Ratios...............................................................................................................................9

Debt to Equity Ratio........................................................................................................................9

Earnings Per share.........................................................................................................................10

Choice of the company..................................................................................................................11

Problems, Limitations and assumptions which need to be undertaken.........................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

Table of Contents

Introduction......................................................................................................................................2

GAP.................................................................................................................................................2

H and M...........................................................................................................................................3

Critical comparison and financial performance over the last few years..........................................3

Profitability ratio..............................................................................................................................4

Gross Profit Margin.........................................................................................................................4

Net profit Margin.............................................................................................................................6

Liquidity..........................................................................................................................................7

Current Ratio...................................................................................................................................7

Solvency Ratios...............................................................................................................................9

Debt to Equity Ratio........................................................................................................................9

Earnings Per share.........................................................................................................................10

Choice of the company..................................................................................................................11

Problems, Limitations and assumptions which need to be undertaken.........................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

2FINANCIAL ANALYSIS

Introduction

In order to judge the firm regarding the overall facets of the organization, it can be

considered essentially crucial for the individual analyzing to see to it that, they are being able to

undertake a comprehensive analysis which will assist in determining how the firm is performing

(Bekaert and Hodrick 2017). The Ratio Analysis tends to serve as a manner in which the firm

will successfully be able to analyze its performance and determine the manner in which the firm

can improve its performance. Hence, in regard to this, the given section of the report will analyze

the financial performance of the two chosen companies named H and M and GAP which are

under globally registered stock exchange organizations and analyze the manner in which these

firms have been performing. Based on this analysis, a decision regarding the overall investment

in one of the companies will also be made. It needs to be noted that the major company has been

taken to be the GAP and the competitor is the H and M.

GAP

The GAP is an American worldwide clothing retailer which was found in 1969 by

Donald Fisher and Doris Fisherand is headquartered in California. The firm sells a large number

of products worldwide and has been performing considerably well over the last few years. The

firm is registered under the New York Stock Exchange and the share is priced at $17.19 as per

20th of September, 2019. The main competitors of the firm globally can be taken to be H and M

and Zara among others. The firm sells a large number of products like the kids clothing,

accessories, fashionable items and others. As compared to the competitor H and M, the firm is

performing below H and M.

Introduction

In order to judge the firm regarding the overall facets of the organization, it can be

considered essentially crucial for the individual analyzing to see to it that, they are being able to

undertake a comprehensive analysis which will assist in determining how the firm is performing

(Bekaert and Hodrick 2017). The Ratio Analysis tends to serve as a manner in which the firm

will successfully be able to analyze its performance and determine the manner in which the firm

can improve its performance. Hence, in regard to this, the given section of the report will analyze

the financial performance of the two chosen companies named H and M and GAP which are

under globally registered stock exchange organizations and analyze the manner in which these

firms have been performing. Based on this analysis, a decision regarding the overall investment

in one of the companies will also be made. It needs to be noted that the major company has been

taken to be the GAP and the competitor is the H and M.

GAP

The GAP is an American worldwide clothing retailer which was found in 1969 by

Donald Fisher and Doris Fisherand is headquartered in California. The firm sells a large number

of products worldwide and has been performing considerably well over the last few years. The

firm is registered under the New York Stock Exchange and the share is priced at $17.19 as per

20th of September, 2019. The main competitors of the firm globally can be taken to be H and M

and Zara among others. The firm sells a large number of products like the kids clothing,

accessories, fashionable items and others. As compared to the competitor H and M, the firm is

performing below H and M.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS

H and M

The H and M can be taken to be a Swedish Multinational clothing retail company which

is very popular for its fast fashion clothing for women, men, teenagers and the children. The H

and M operates in more than 62 countries with more than 4500 stores and 132000 employees.

The firm is registered under the Stockholm Stock Exchange and the share price of the firm is

Swedish Krona 189. The organization sells offering which can be considered to be very similar

to that of the competitors GAP and Zara. In line of this, the firm is performing well in terms of

revenue and overall market share.

Hence, from the given analysis it can be rightfully understood that the market positioning

of H and M is better than that of GAP. The given chart mentions the manner

Critical comparison and financial performance over the last few years

Five year performance summary

GAP

The sales of the GAP over the past fiscal year have shown a growth rate of 2%. In

addition to this, the reports have also reflected that there has been a positive increase in the

overall revenue of the firm in this five year period (McKinney 2015). Over the last few years, the

reports are reflecting that the operating margins have gone down considerably. In the given

section various ratios like Gross profit ratio, Net profit ratio, the Earning per share, Debt to

Equity rate and Current Ratio will be made use of in order to examine the manner in which the

firm has been performing (Annualreports.com 2019).

H and M

H and M

The H and M can be taken to be a Swedish Multinational clothing retail company which

is very popular for its fast fashion clothing for women, men, teenagers and the children. The H

and M operates in more than 62 countries with more than 4500 stores and 132000 employees.

The firm is registered under the Stockholm Stock Exchange and the share price of the firm is

Swedish Krona 189. The organization sells offering which can be considered to be very similar

to that of the competitors GAP and Zara. In line of this, the firm is performing well in terms of

revenue and overall market share.

Hence, from the given analysis it can be rightfully understood that the market positioning

of H and M is better than that of GAP. The given chart mentions the manner

Critical comparison and financial performance over the last few years

Five year performance summary

GAP

The sales of the GAP over the past fiscal year have shown a growth rate of 2%. In

addition to this, the reports have also reflected that there has been a positive increase in the

overall revenue of the firm in this five year period (McKinney 2015). Over the last few years, the

reports are reflecting that the operating margins have gone down considerably. In the given

section various ratios like Gross profit ratio, Net profit ratio, the Earning per share, Debt to

Equity rate and Current Ratio will be made use of in order to examine the manner in which the

firm has been performing (Annualreports.com 2019).

H and M

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS

The H and M has improved its overall operations to a great extent. In line of this it can be

rightfully understood that the company has been able to expand into a greater number of

countries and this had not only lead to an increase in the overall operations of the country but in

addition to this, has also lead to an overall increase in the returns of the firm (Hm.com 2019).

The given section will examine the Net profit, gross profit and the current ratio along with the

debt to equity ratio so as to understand how the firm has been performing with respect to the

Profitability ratio

The profitability ratio is the metrics which help in assessing the overall ability of the

business with respect to the different profits which the firm would attain. The ratio helps in

assessing whether the firm is being able to earn adequate profits or not and also assists in

examining whether it will be able to engage in the competitive environment or not. The different

profitability ratios which are commonly used for the analysis are the Gross profit ratio and the

Net profit Ratio.

Gross Profit Margin

The gross profit margin also known as the gross margin can be understood to be the ratio

of gross margin which is expressed as a share of the sales of the firm. The gross margin

determines the extent of profit which is made by a firm after paying off the different cost of

goods sold. It helps in measuring the overall efficiency of the company which makes use of the

various raw materials and also determines the manner in which the firm is able to engage in long

term success (Ge and Weisbach 2019). The higher is the gross profit margin of the firm, the

better the company is performing. The formula for calculating the Gross profit margin of the firm

can be stated to be the gross profits of the firm divided by the Sales of the firm.

The H and M has improved its overall operations to a great extent. In line of this it can be

rightfully understood that the company has been able to expand into a greater number of

countries and this had not only lead to an increase in the overall operations of the country but in

addition to this, has also lead to an overall increase in the returns of the firm (Hm.com 2019).

The given section will examine the Net profit, gross profit and the current ratio along with the

debt to equity ratio so as to understand how the firm has been performing with respect to the

Profitability ratio

The profitability ratio is the metrics which help in assessing the overall ability of the

business with respect to the different profits which the firm would attain. The ratio helps in

assessing whether the firm is being able to earn adequate profits or not and also assists in

examining whether it will be able to engage in the competitive environment or not. The different

profitability ratios which are commonly used for the analysis are the Gross profit ratio and the

Net profit Ratio.

Gross Profit Margin

The gross profit margin also known as the gross margin can be understood to be the ratio

of gross margin which is expressed as a share of the sales of the firm. The gross margin

determines the extent of profit which is made by a firm after paying off the different cost of

goods sold. It helps in measuring the overall efficiency of the company which makes use of the

various raw materials and also determines the manner in which the firm is able to engage in long

term success (Ge and Weisbach 2019). The higher is the gross profit margin of the firm, the

better the company is performing. The formula for calculating the Gross profit margin of the firm

can be stated to be the gross profits of the firm divided by the Sales of the firm.

5FINANCIAL ANALYSIS

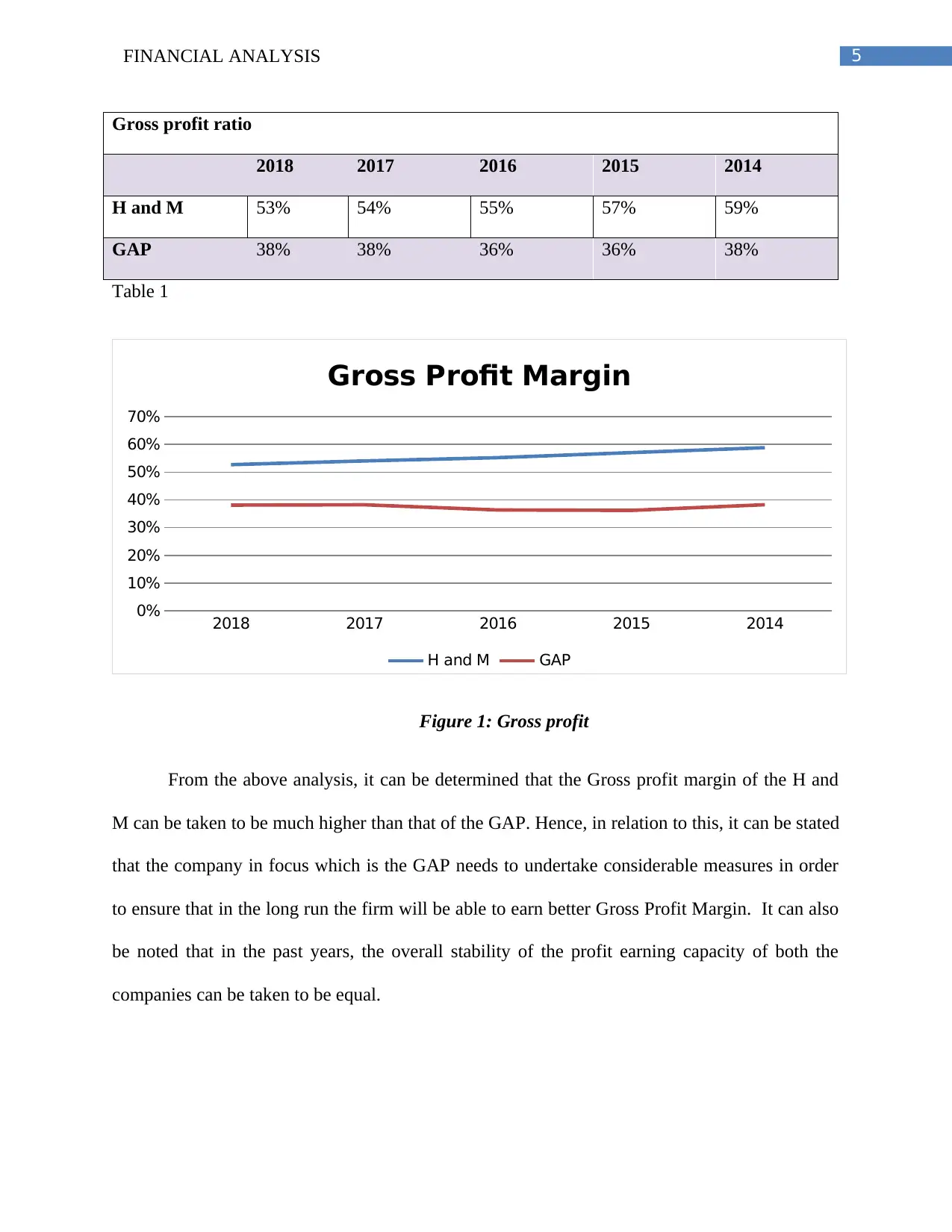

Gross profit ratio

2018 2017 2016 2015 2014

H and M 53% 54% 55% 57% 59%

GAP 38% 38% 36% 36% 38%

Table 1

2018 2017 2016 2015 2014

0%

10%

20%

30%

40%

50%

60%

70%

Gross Profit Margin

H and M GAP

Figure 1: Gross profit

From the above analysis, it can be determined that the Gross profit margin of the H and

M can be taken to be much higher than that of the GAP. Hence, in relation to this, it can be stated

that the company in focus which is the GAP needs to undertake considerable measures in order

to ensure that in the long run the firm will be able to earn better Gross Profit Margin. It can also

be noted that in the past years, the overall stability of the profit earning capacity of both the

companies can be taken to be equal.

Gross profit ratio

2018 2017 2016 2015 2014

H and M 53% 54% 55% 57% 59%

GAP 38% 38% 36% 36% 38%

Table 1

2018 2017 2016 2015 2014

0%

10%

20%

30%

40%

50%

60%

70%

Gross Profit Margin

H and M GAP

Figure 1: Gross profit

From the above analysis, it can be determined that the Gross profit margin of the H and

M can be taken to be much higher than that of the GAP. Hence, in relation to this, it can be stated

that the company in focus which is the GAP needs to undertake considerable measures in order

to ensure that in the long run the firm will be able to earn better Gross Profit Margin. It can also

be noted that in the past years, the overall stability of the profit earning capacity of both the

companies can be taken to be equal.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS

Net profit Margin

The net profit margin can be described as the percentage of revenue which remains after

all the expenses has been deducted from the revenues which have been earnt by the firm. In line

of this, it helps in understanding the extent of profit which a business will be able to extract from

its customers. Moreover, it also assists in understanding the manner in which the business is left

with a considerable share of profits after all the various obligations of the business have been

paid. The amounts which are generally deducted out of the particular set of expenses can be

understood to be the sales expenses and other such measures. Given below is the Net profit

margin of the GAP and the H and M.

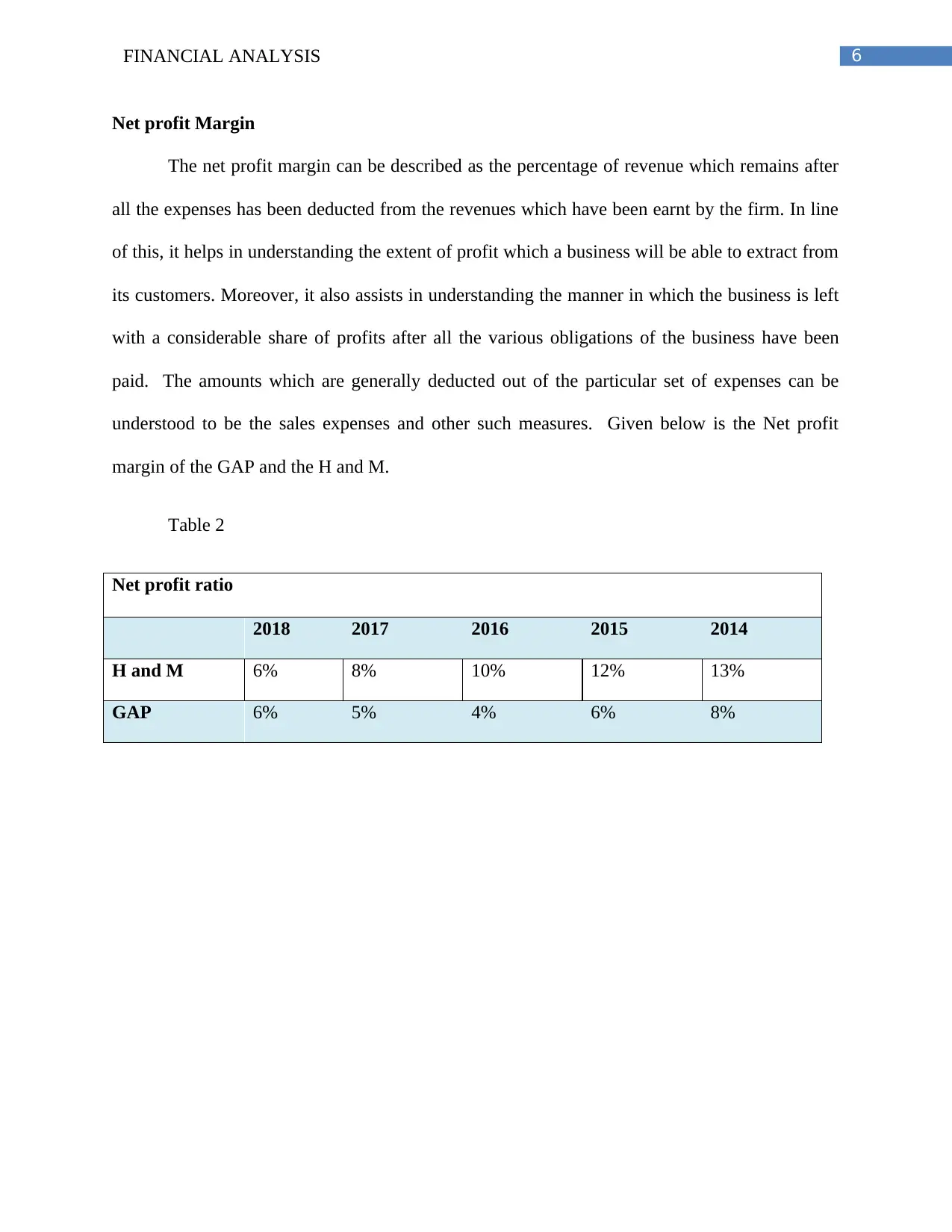

Table 2

Net profit ratio

2018 2017 2016 2015 2014

H and M 6% 8% 10% 12% 13%

GAP 6% 5% 4% 6% 8%

Net profit Margin

The net profit margin can be described as the percentage of revenue which remains after

all the expenses has been deducted from the revenues which have been earnt by the firm. In line

of this, it helps in understanding the extent of profit which a business will be able to extract from

its customers. Moreover, it also assists in understanding the manner in which the business is left

with a considerable share of profits after all the various obligations of the business have been

paid. The amounts which are generally deducted out of the particular set of expenses can be

understood to be the sales expenses and other such measures. Given below is the Net profit

margin of the GAP and the H and M.

Table 2

Net profit ratio

2018 2017 2016 2015 2014

H and M 6% 8% 10% 12% 13%

GAP 6% 5% 4% 6% 8%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS

2018 2017 2016 2015 2014

6%

8%

10%

12%

13%

6% 5% 4%

6%

8%

Net Profit Margin

H and M GAP

Figure 2: Net profit

From the given table and the figure, it can be observed that the Net profit margin of the H

and M can be understood to be considerably higher than that of the GAP. This means that the H

and M as a competitor has been performing considerably well and hence, with respect to this, it

can be rightfully mentioned that this performance has enabled the firm to expand its operations

in various parts of the country. In association of this, it can be mentioned that over the last few

years however, the net profit margin of the firm has been going down whereas the net profit

margin of GAP can be taken to be fairly stable. Therefore, in regard to this, it can be rightfully

mentioned that, stability is integral for any firm and as the overall profit of GAP is consistent, it

can be taken as a good sign.

Liquidity

The liquidity ratios act as an indicator of the fact whether the firm will be able to perform

well in the long run and assist in determining the overall ability of the firm to perform in the long

run (Mohanram, Saiy and Vyas 2018). It assists in ensuring whether the firm will be able to pay

2018 2017 2016 2015 2014

6%

8%

10%

12%

13%

6% 5% 4%

6%

8%

Net Profit Margin

H and M GAP

Figure 2: Net profit

From the given table and the figure, it can be observed that the Net profit margin of the H

and M can be understood to be considerably higher than that of the GAP. This means that the H

and M as a competitor has been performing considerably well and hence, with respect to this, it

can be rightfully mentioned that this performance has enabled the firm to expand its operations

in various parts of the country. In association of this, it can be mentioned that over the last few

years however, the net profit margin of the firm has been going down whereas the net profit

margin of GAP can be taken to be fairly stable. Therefore, in regard to this, it can be rightfully

mentioned that, stability is integral for any firm and as the overall profit of GAP is consistent, it

can be taken as a good sign.

Liquidity

The liquidity ratios act as an indicator of the fact whether the firm will be able to perform

well in the long run and assist in determining the overall ability of the firm to perform in the long

run (Mohanram, Saiy and Vyas 2018). It assists in ensuring whether the firm will be able to pay

8FINANCIAL ANALYSIS

off its debts in the long run or not. In line of this, it becomes very crucial for the firm to ensure

that it will be successfully able to attain a good competitive positioning or not. The liquidity ratio

which has been used here can be understood to be the Current Ratio.

Current Ratio

The current ratio is generally described as a liquidity ratio which assists in measuring the

ability of a company to pay off the short term obligations or those which are due in one year

(Robinson et al. 2015) The current ratio serves as an indicator of the manner in which the firm

will be successfully able to maximize the current assets on the balance sheet and satisfy the debt

which exists along with the different payables. It determines the overall liquidity of the firm.

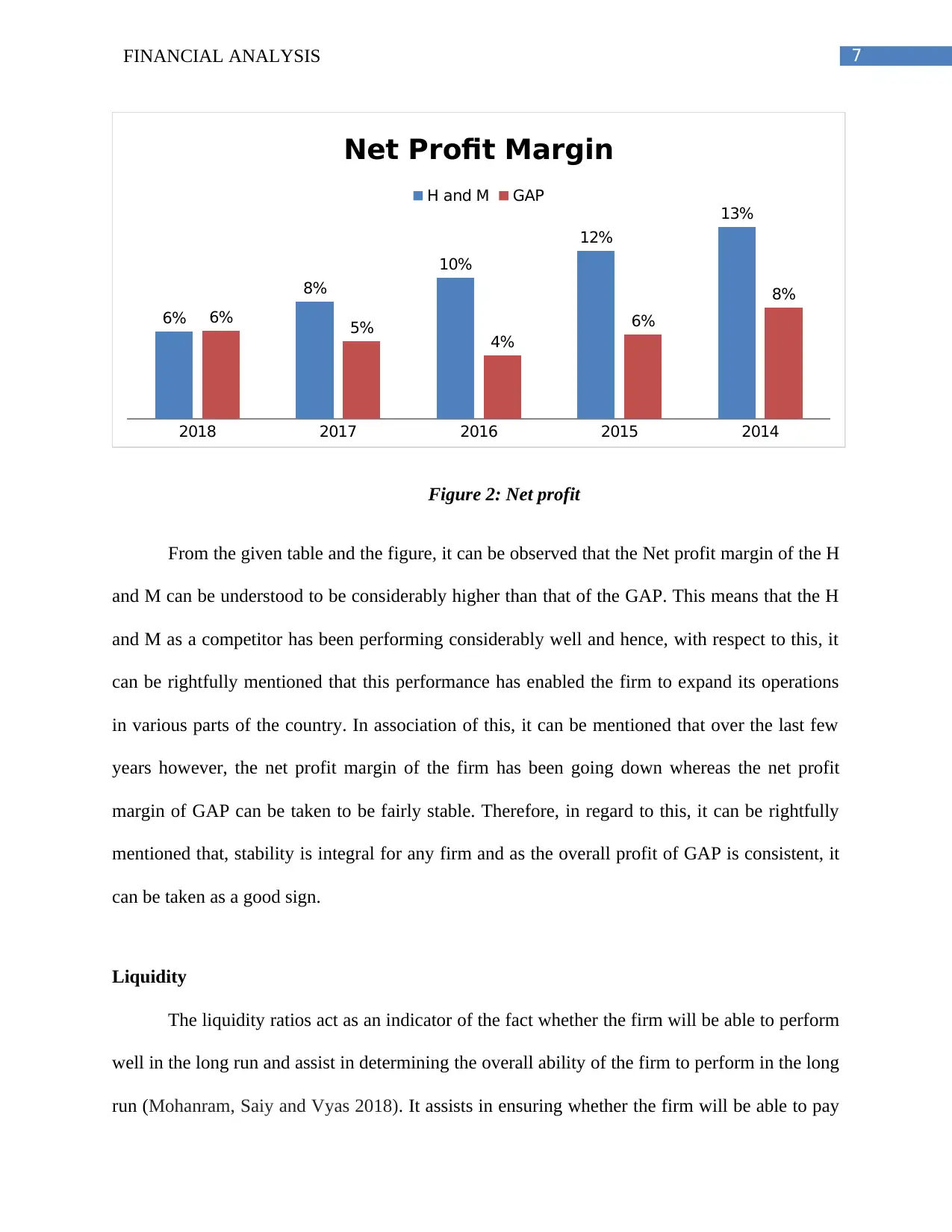

The Current ratio comparison of the GAP and H and M can be stated to be as follows:

2014

2015

2016

2017

2018

0 0.5 1 1.5 2 2.5

Current Ratio

GAP H and M

Figure 3: Current Ratio

Table 3

off its debts in the long run or not. In line of this, it becomes very crucial for the firm to ensure

that it will be successfully able to attain a good competitive positioning or not. The liquidity ratio

which has been used here can be understood to be the Current Ratio.

Current Ratio

The current ratio is generally described as a liquidity ratio which assists in measuring the

ability of a company to pay off the short term obligations or those which are due in one year

(Robinson et al. 2015) The current ratio serves as an indicator of the manner in which the firm

will be successfully able to maximize the current assets on the balance sheet and satisfy the debt

which exists along with the different payables. It determines the overall liquidity of the firm.

The Current ratio comparison of the GAP and H and M can be stated to be as follows:

2014

2015

2016

2017

2018

0 0.5 1 1.5 2 2.5

Current Ratio

GAP H and M

Figure 3: Current Ratio

Table 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS

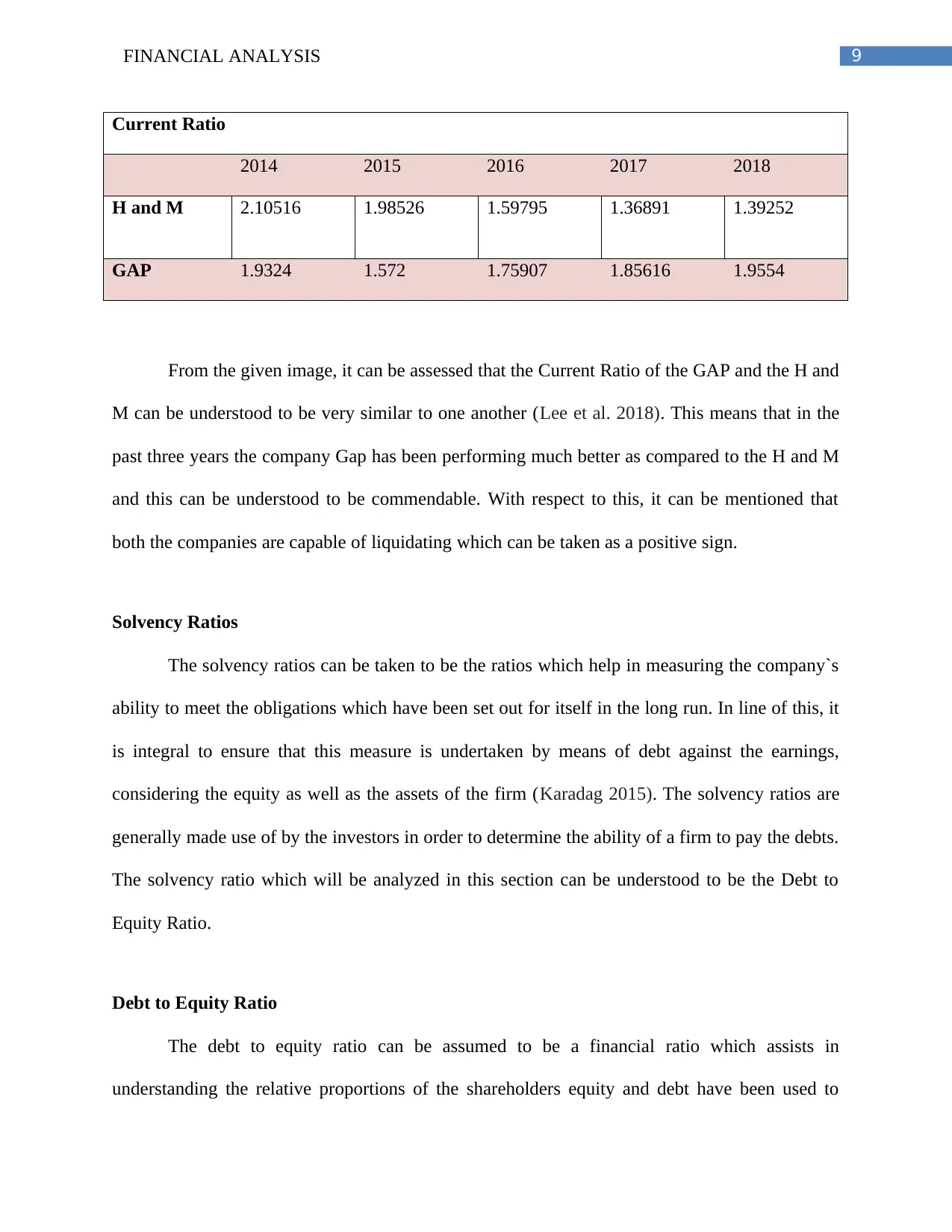

Current Ratio

2014 2015 2016 2017 2018

H and M 2.10516 1.98526 1.59795 1.36891 1.39252

GAP 1.9324 1.572 1.75907 1.85616 1.9554

From the given image, it can be assessed that the Current Ratio of the GAP and the H and

M can be understood to be very similar to one another (Lee et al. 2018). This means that in the

past three years the company Gap has been performing much better as compared to the H and M

and this can be understood to be commendable. With respect to this, it can be mentioned that

both the companies are capable of liquidating which can be taken as a positive sign.

Solvency Ratios

The solvency ratios can be taken to be the ratios which help in measuring the company`s

ability to meet the obligations which have been set out for itself in the long run. In line of this, it

is integral to ensure that this measure is undertaken by means of debt against the earnings,

considering the equity as well as the assets of the firm (Karadag 2015). The solvency ratios are

generally made use of by the investors in order to determine the ability of a firm to pay the debts.

The solvency ratio which will be analyzed in this section can be understood to be the Debt to

Equity Ratio.

Debt to Equity Ratio

The debt to equity ratio can be assumed to be a financial ratio which assists in

understanding the relative proportions of the shareholders equity and debt have been used to

Current Ratio

2014 2015 2016 2017 2018

H and M 2.10516 1.98526 1.59795 1.36891 1.39252

GAP 1.9324 1.572 1.75907 1.85616 1.9554

From the given image, it can be assessed that the Current Ratio of the GAP and the H and

M can be understood to be very similar to one another (Lee et al. 2018). This means that in the

past three years the company Gap has been performing much better as compared to the H and M

and this can be understood to be commendable. With respect to this, it can be mentioned that

both the companies are capable of liquidating which can be taken as a positive sign.

Solvency Ratios

The solvency ratios can be taken to be the ratios which help in measuring the company`s

ability to meet the obligations which have been set out for itself in the long run. In line of this, it

is integral to ensure that this measure is undertaken by means of debt against the earnings,

considering the equity as well as the assets of the firm (Karadag 2015). The solvency ratios are

generally made use of by the investors in order to determine the ability of a firm to pay the debts.

The solvency ratio which will be analyzed in this section can be understood to be the Debt to

Equity Ratio.

Debt to Equity Ratio

The debt to equity ratio can be assumed to be a financial ratio which assists in

understanding the relative proportions of the shareholders equity and debt have been used to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS

finance the assets of the company. In line with this, the ratio can also be known to be the gearing,

leverage and the risk ratio. The debt equity ratio of the firm has been undertaken in the following

analysis

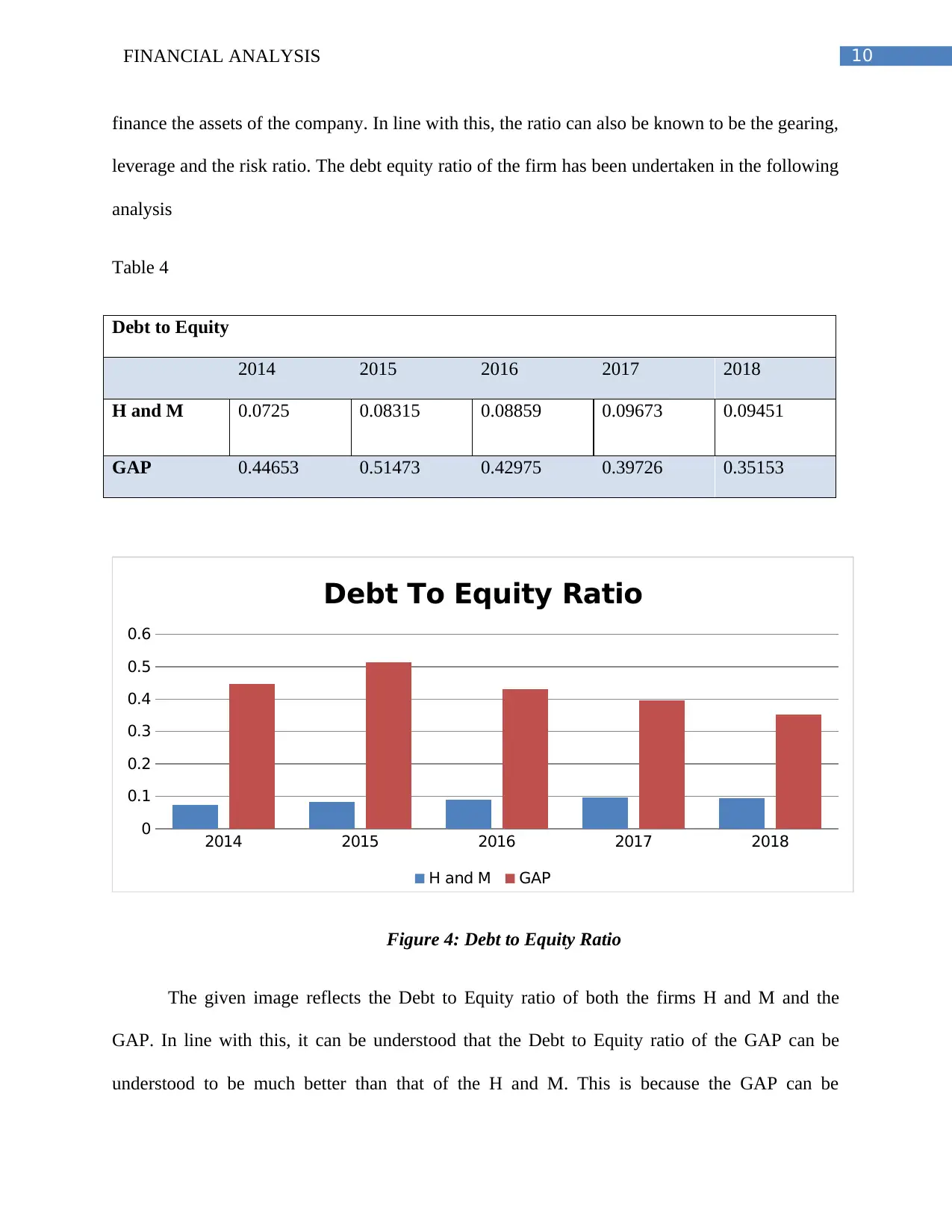

Table 4

Debt to Equity

2014 2015 2016 2017 2018

H and M 0.0725 0.08315 0.08859 0.09673 0.09451

GAP 0.44653 0.51473 0.42975 0.39726 0.35153

2014 2015 2016 2017 2018

0

0.1

0.2

0.3

0.4

0.5

0.6

Debt To Equity Ratio

H and M GAP

Figure 4: Debt to Equity Ratio

The given image reflects the Debt to Equity ratio of both the firms H and M and the

GAP. In line with this, it can be understood that the Debt to Equity ratio of the GAP can be

understood to be much better than that of the H and M. This is because the GAP can be

finance the assets of the company. In line with this, the ratio can also be known to be the gearing,

leverage and the risk ratio. The debt equity ratio of the firm has been undertaken in the following

analysis

Table 4

Debt to Equity

2014 2015 2016 2017 2018

H and M 0.0725 0.08315 0.08859 0.09673 0.09451

GAP 0.44653 0.51473 0.42975 0.39726 0.35153

2014 2015 2016 2017 2018

0

0.1

0.2

0.3

0.4

0.5

0.6

Debt To Equity Ratio

H and M GAP

Figure 4: Debt to Equity Ratio

The given image reflects the Debt to Equity ratio of both the firms H and M and the

GAP. In line with this, it can be understood that the Debt to Equity ratio of the GAP can be

understood to be much better than that of the H and M. This is because the GAP can be

11FINANCIAL ANALYSIS

understood to be managing its overall finances very well (Zietlow et al. 2018). In line of this, the

firm has been performing much better than the competitor can be understood to have been down

to a great extent.

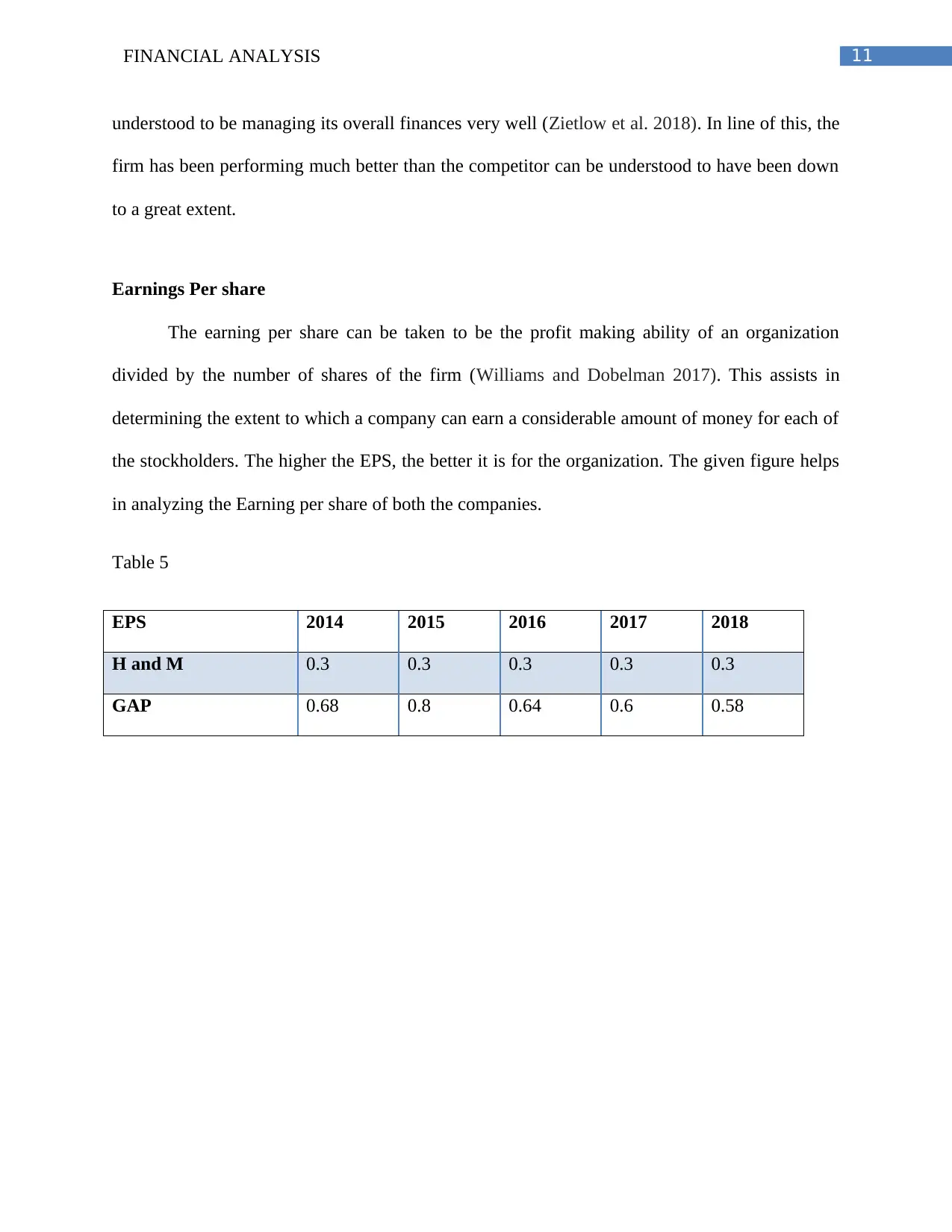

Earnings Per share

The earning per share can be taken to be the profit making ability of an organization

divided by the number of shares of the firm (Williams and Dobelman 2017). This assists in

determining the extent to which a company can earn a considerable amount of money for each of

the stockholders. The higher the EPS, the better it is for the organization. The given figure helps

in analyzing the Earning per share of both the companies.

Table 5

EPS 2014 2015 2016 2017 2018

H and M 0.3 0.3 0.3 0.3 0.3

GAP 0.68 0.8 0.64 0.6 0.58

understood to be managing its overall finances very well (Zietlow et al. 2018). In line of this, the

firm has been performing much better than the competitor can be understood to have been down

to a great extent.

Earnings Per share

The earning per share can be taken to be the profit making ability of an organization

divided by the number of shares of the firm (Williams and Dobelman 2017). This assists in

determining the extent to which a company can earn a considerable amount of money for each of

the stockholders. The higher the EPS, the better it is for the organization. The given figure helps

in analyzing the Earning per share of both the companies.

Table 5

EPS 2014 2015 2016 2017 2018

H and M 0.3 0.3 0.3 0.3 0.3

GAP 0.68 0.8 0.64 0.6 0.58

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.