Comprehensive Financial Analysis of Harvey Norman Holdings

VerifiedAdded on 2021/06/30

|14

|3470

|24

Homework Assignment

AI Summary

This assignment provides a comprehensive financial analysis of Harvey Norman Holdings Limited. It begins by defining and calculating the book value of debt and equity, utilizing data from Harvey Norman's annual report. The analysis then proceeds to determine key financial metrics, including the most recent stock price, market capitalization, and outstanding shares. The assignment explores the applicability of the dividend discount model for Harvey Norman, calculating the cost of equity using the Capital Asset Pricing Model (CAPM). It also delves into the calculation of the cost of debt using both book and market value weights, and finally calculates the weighted average cost of capital (WACC) using different approaches, including book and market value weights, and comparing the results based on data gathered from Yahoo Finance and Westpac. The analysis highlights the importance of market value weights in WACC calculation and explains the implications of a lower cost of capital on net present value.

Assignment 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Question 1 .............................................................................................................................. 3

Question 2 .............................................................................................................................. 4

What is the most recent stock price listed for Harvey Norman? ....................................... 4

What is the market value of equity, or market capitalisation? .......................................... 4

How many shares does Harvey Norman have outstanding?.............................................. 4

What is the most recent annual dividend? ......................................................................... 4

Can you use the dividend discount model in this case? ..................................................... 5

What is the beta for Harvey Norman? ................................................................................ 6

What is the yield on government debt? ............................................................................. 6

What is the cost of equity for Harvey Norman using the CAPM? ...................................... 6

Question 3 .............................................................................................................................. 6

Question 4 ............................................................................................................................ 10

Question 5 ............................................................................................................................ 12

Bibliography .......................................................................................................................... 13

Question 1 .............................................................................................................................. 3

Question 2 .............................................................................................................................. 4

What is the most recent stock price listed for Harvey Norman? ....................................... 4

What is the market value of equity, or market capitalisation? .......................................... 4

How many shares does Harvey Norman have outstanding?.............................................. 4

What is the most recent annual dividend? ......................................................................... 4

Can you use the dividend discount model in this case? ..................................................... 5

What is the beta for Harvey Norman? ................................................................................ 6

What is the yield on government debt? ............................................................................. 6

What is the cost of equity for Harvey Norman using the CAPM? ...................................... 6

Question 3 .............................................................................................................................. 6

Question 4 ............................................................................................................................ 10

Question 5 ............................................................................................................................ 12

Bibliography .......................................................................................................................... 13

Question 1

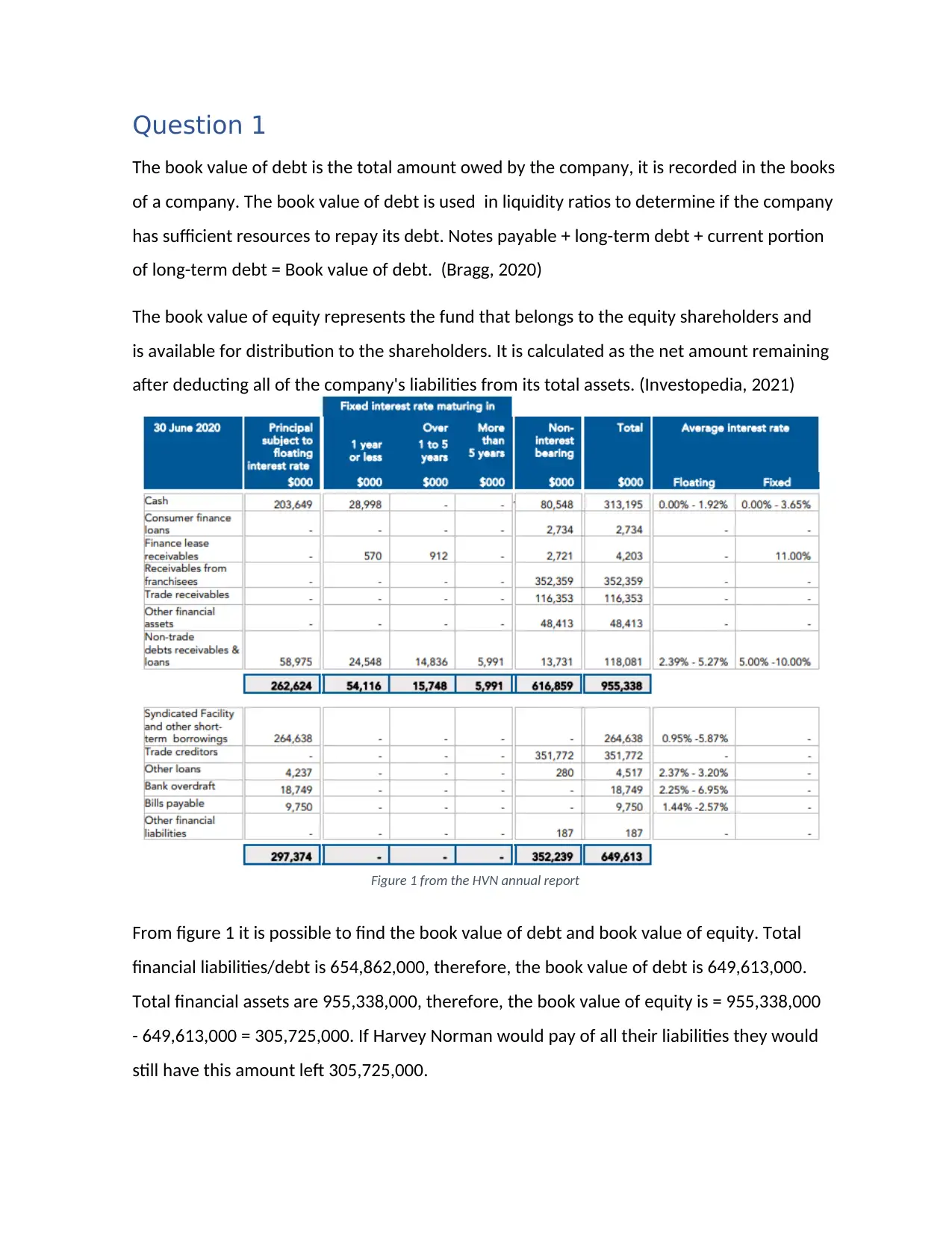

The book value of debt is the total amount owed by the company, it is recorded in the books

of a company. The book value of debt is used in liquidity ratios to determine if the company

has sufficient resources to repay its debt. Notes payable + long-term debt + current portion

of long-term debt = Book value of debt. (Bragg, 2020)

The book value of equity represents the fund that belongs to the equity shareholders and

is available for distribution to the shareholders. It is calculated as the net amount remaining

after deducting all of the company's liabilities from its total assets. (Investopedia, 2021)

From figure 1 it is possible to find the book value of debt and book value of equity. Total

financial liabilities/debt is 654,862,000, therefore, the book value of debt is 649,613,000.

Total financial assets are 955,338,000, therefore, the book value of equity is = 955,338,000

- 649,613,000 = 305,725,000. If Harvey Norman would pay of all their liabilities they would

still have this amount left 305,725,000.

Figure 2 from HVN annual report

Figure 1 from the HVN annual report

The book value of debt is the total amount owed by the company, it is recorded in the books

of a company. The book value of debt is used in liquidity ratios to determine if the company

has sufficient resources to repay its debt. Notes payable + long-term debt + current portion

of long-term debt = Book value of debt. (Bragg, 2020)

The book value of equity represents the fund that belongs to the equity shareholders and

is available for distribution to the shareholders. It is calculated as the net amount remaining

after deducting all of the company's liabilities from its total assets. (Investopedia, 2021)

From figure 1 it is possible to find the book value of debt and book value of equity. Total

financial liabilities/debt is 654,862,000, therefore, the book value of debt is 649,613,000.

Total financial assets are 955,338,000, therefore, the book value of equity is = 955,338,000

- 649,613,000 = 305,725,000. If Harvey Norman would pay of all their liabilities they would

still have this amount left 305,725,000.

Figure 2 from HVN annual report

Figure 1 from the HVN annual report

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2

What is the most recent stock price listed for Harvey Norman?

A stock price is the current price that a share of stock is trading for on the market.

The most recent stock price of Harvey Normal Holdings Limited is 5.93 Australian dollars.

The open stock price is 6,03, the high is 6.09 and the low is 5.89. This information was

collected on 22.03.2021 (@yahoofinanceau, 2021)

What is the market value of equity, or market capitalisation?

The total dollar market value of a company's outstanding shares of stock is referred to as

market capitalization. It is calculated by multiplying the total number of a company's

outstanding shares by the current market price of one share, which is commonly referred

to as "market cap." (Investopedia, 2021)

The market capitalisation for Harvey Norman is 7,39 billion. (@yahoofinanceau, 2021)

How many shares does Harvey Norman have outstanding?

It is possible to calculate the shares outstanding knowing the information on market

capitalisation and the stock price. Like mentioned before shares outstanding is calculated:

stock price * outstanding shares = market cap, therefore, it is possible to change the formula

to market cap/stock price=shares outstanding.

7,390,000,000/5.93=1,246,205,733

It is also possible to gather the information online. Harvey Norman has 1,25 billion

outstanding shares. (@yahoofinanceau, 2021)

What is the most recent annual dividend?

Dividend yield is the amount of money a company pays shareholders for owning a share of

its stock divided by its current stock price and is shown as a percentage. (Investopedia,

2021)

Harvey Normans most recent annual dividend is $0.38 per share and the forward market

dividend yield is 6.51%. (Marketbeat.com, 2021)

What is the most recent stock price listed for Harvey Norman?

A stock price is the current price that a share of stock is trading for on the market.

The most recent stock price of Harvey Normal Holdings Limited is 5.93 Australian dollars.

The open stock price is 6,03, the high is 6.09 and the low is 5.89. This information was

collected on 22.03.2021 (@yahoofinanceau, 2021)

What is the market value of equity, or market capitalisation?

The total dollar market value of a company's outstanding shares of stock is referred to as

market capitalization. It is calculated by multiplying the total number of a company's

outstanding shares by the current market price of one share, which is commonly referred

to as "market cap." (Investopedia, 2021)

The market capitalisation for Harvey Norman is 7,39 billion. (@yahoofinanceau, 2021)

How many shares does Harvey Norman have outstanding?

It is possible to calculate the shares outstanding knowing the information on market

capitalisation and the stock price. Like mentioned before shares outstanding is calculated:

stock price * outstanding shares = market cap, therefore, it is possible to change the formula

to market cap/stock price=shares outstanding.

7,390,000,000/5.93=1,246,205,733

It is also possible to gather the information online. Harvey Norman has 1,25 billion

outstanding shares. (@yahoofinanceau, 2021)

What is the most recent annual dividend?

Dividend yield is the amount of money a company pays shareholders for owning a share of

its stock divided by its current stock price and is shown as a percentage. (Investopedia,

2021)

Harvey Normans most recent annual dividend is $0.38 per share and the forward market

dividend yield is 6.51%. (Marketbeat.com, 2021)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Can you use the dividend discount model in this case?

The dividend discount model is a method used for predicting the price of a company’s stock

that is based on the theory that its current price is worth the sum of all future dividend

payments when discounted back to their present value. It attempts to calculate the fair

value of stock regardless of market conditions and takes dividend pay-out factors and

market expected returns into account. If the dividend discount model is greater than the

current trading price of shares, the stock is undervalued and should be purchased and if the

DDM is less than the current trading price of shares the stock is undervalued and should not

be purchased. (Investopedia, 2021)

The DDM formula is: Value of stock = EDPS/(CCE-DGR)

Where: EDPS = expected dividend per share

CCE = cost of capital equity

DGR = dividend growth rate

It is also common to use the Gordon growth model, it assumes a stable dividend growth

rate. (Investopedia, 2021)

The GGM formula is: Price per share = D/(r-g)

Where: D = the estimated value of next year’s dividend

r = the company’s cost of capital equity

g = the constant growth rate for dividends

It is known that Harvey Norman pays a dividend of 0.38 per share, the price per share is

5.93, the dividend growth is 6.51%. It can be estimated as: r=(D/P)+g =

(0.38/5.93)+6.51%=6.4%+6.51%=12.91%. Now it is possible to use the DDM formula: value

of stock = 0.38/(12.91%-6.51%) = $ 5.9375, therefore, it is possible to use the dividend

discount model for Harvey Norman.

The dividend discount model is a method used for predicting the price of a company’s stock

that is based on the theory that its current price is worth the sum of all future dividend

payments when discounted back to their present value. It attempts to calculate the fair

value of stock regardless of market conditions and takes dividend pay-out factors and

market expected returns into account. If the dividend discount model is greater than the

current trading price of shares, the stock is undervalued and should be purchased and if the

DDM is less than the current trading price of shares the stock is undervalued and should not

be purchased. (Investopedia, 2021)

The DDM formula is: Value of stock = EDPS/(CCE-DGR)

Where: EDPS = expected dividend per share

CCE = cost of capital equity

DGR = dividend growth rate

It is also common to use the Gordon growth model, it assumes a stable dividend growth

rate. (Investopedia, 2021)

The GGM formula is: Price per share = D/(r-g)

Where: D = the estimated value of next year’s dividend

r = the company’s cost of capital equity

g = the constant growth rate for dividends

It is known that Harvey Norman pays a dividend of 0.38 per share, the price per share is

5.93, the dividend growth is 6.51%. It can be estimated as: r=(D/P)+g =

(0.38/5.93)+6.51%=6.4%+6.51%=12.91%. Now it is possible to use the DDM formula: value

of stock = 0.38/(12.91%-6.51%) = $ 5.9375, therefore, it is possible to use the dividend

discount model for Harvey Norman.

What is the beta for Harvey Norman?

Beta is a measurement of a stock risk. If a stock’s beta is above 1 it means that it is more

riskier than stocks that have a beta below 1. High beta stocks are riskier but provide higher

returns and low beta stocks are saver but provide lower returns. (Investopedia, 2021)

The beta for Harvey Norman is 0.71, therefore, buying stock at Harvey Norman provides a

lower risk and lower return than stocks that have beta that is over 1. (@YahooFinance,

2021)

What is the yield on government debt?

The yield on government debt is the percentage that the government pays to borrow

money for different lengths of time.

The Australia 10 year government bond has a 1.742% yield. (World Government Bonds,

2021)

What is the cost of equity for Harvey Norman using the CAPM?

The return of a stock that an investor expects is the cost of equity. (Pike and Neale)

The formula for Capital Asset Pricing Model is: Cost of equity = risk-free rate of return + Beta

of assets * market premium

risk free rate of return = 1.742%

Beta = 0.71

Market premium = 6%

Cost of equity = 1.742% + 0.71 * 6% = 6%

Question 3

The cost of debt is the rate that a company pays back its liabilities or debt. The formula for

cost of debt is: Total interest/total debt=cost of debt. The cost of debt can be calculated

using either market value or book value of debt, the book value is found in the balance

sheet that the company presents and the market value represents the market price

Beta is a measurement of a stock risk. If a stock’s beta is above 1 it means that it is more

riskier than stocks that have a beta below 1. High beta stocks are riskier but provide higher

returns and low beta stocks are saver but provide lower returns. (Investopedia, 2021)

The beta for Harvey Norman is 0.71, therefore, buying stock at Harvey Norman provides a

lower risk and lower return than stocks that have beta that is over 1. (@YahooFinance,

2021)

What is the yield on government debt?

The yield on government debt is the percentage that the government pays to borrow

money for different lengths of time.

The Australia 10 year government bond has a 1.742% yield. (World Government Bonds,

2021)

What is the cost of equity for Harvey Norman using the CAPM?

The return of a stock that an investor expects is the cost of equity. (Pike and Neale)

The formula for Capital Asset Pricing Model is: Cost of equity = risk-free rate of return + Beta

of assets * market premium

risk free rate of return = 1.742%

Beta = 0.71

Market premium = 6%

Cost of equity = 1.742% + 0.71 * 6% = 6%

Question 3

The cost of debt is the rate that a company pays back its liabilities or debt. The formula for

cost of debt is: Total interest/total debt=cost of debt. The cost of debt can be calculated

using either market value or book value of debt, the book value is found in the balance

sheet that the company presents and the market value represents the market price

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

investors would be willing to purchase a company’s debt for, the market value is usually

higher than the book value. (Pike and Neale)

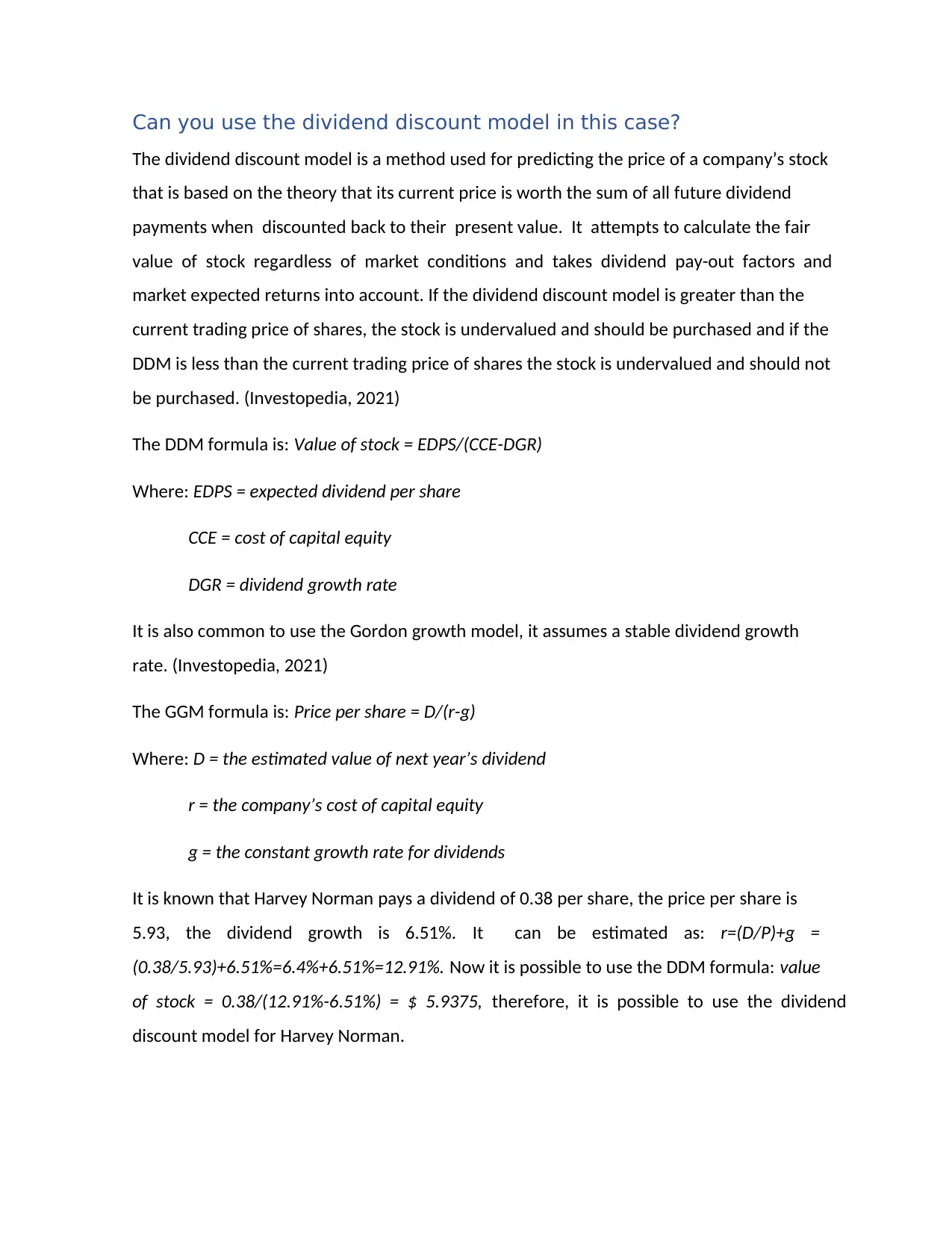

Figure 2 from the HVN annual report

The information that needs to be known in order to calculate the cost of debt is the book

value of debt which is 649,613,000 and the total interest expenses, from figure 2 we can

see that the total interest expenses in June 2020 is 59,794,000, this is the book value.

Cost of debt using book value weights = 59,794,000/649,613,000*100=9.2%

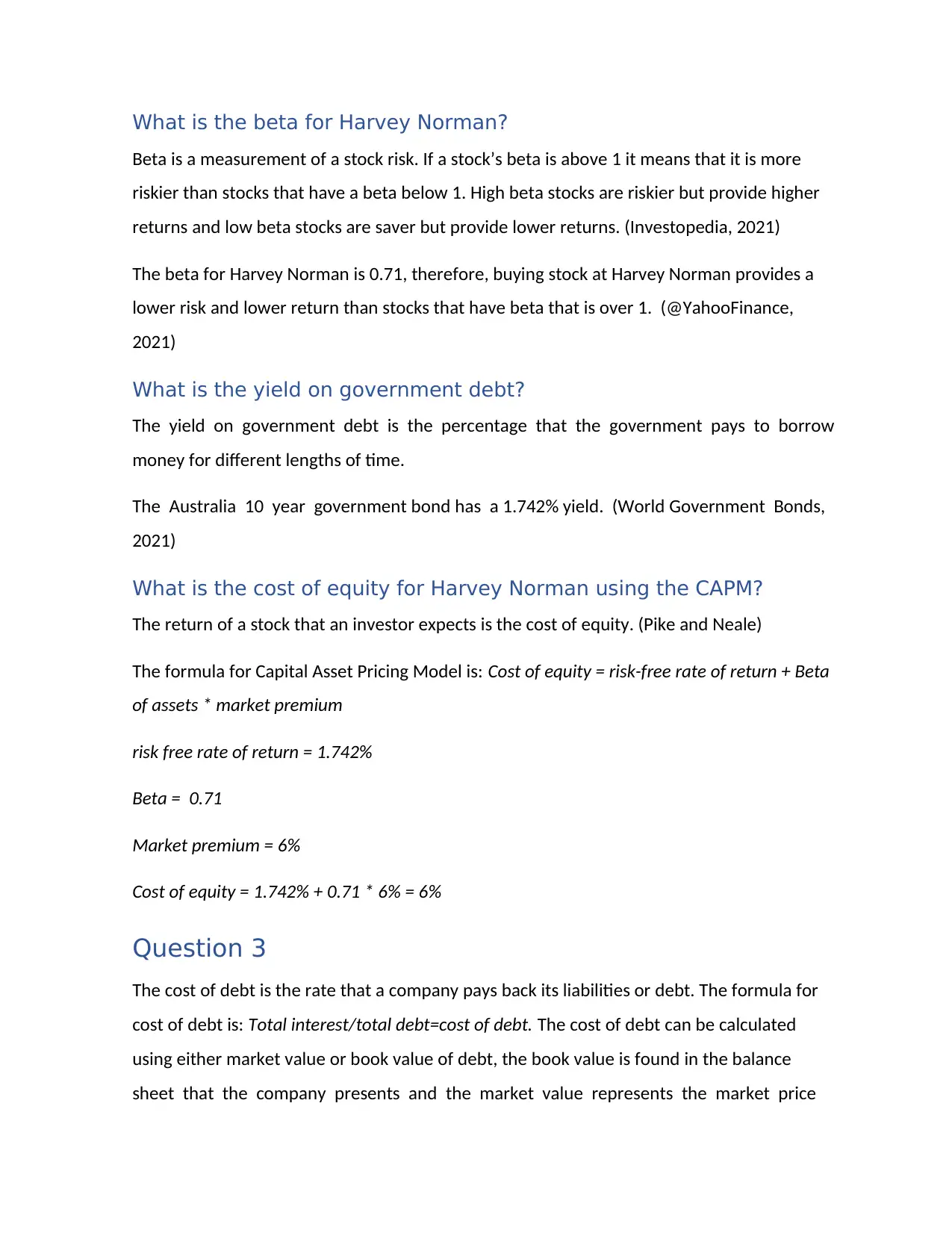

Now in order to find the market value of debt we need to gather information from

Westpac.com and yahoo finance, we know that the market value of equity is 7,39 billion.

Figure 3 from the HVN annual report

higher than the book value. (Pike and Neale)

Figure 2 from the HVN annual report

The information that needs to be known in order to calculate the cost of debt is the book

value of debt which is 649,613,000 and the total interest expenses, from figure 2 we can

see that the total interest expenses in June 2020 is 59,794,000, this is the book value.

Cost of debt using book value weights = 59,794,000/649,613,000*100=9.2%

Now in order to find the market value of debt we need to gather information from

Westpac.com and yahoo finance, we know that the market value of equity is 7,39 billion.

Figure 3 from the HVN annual report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

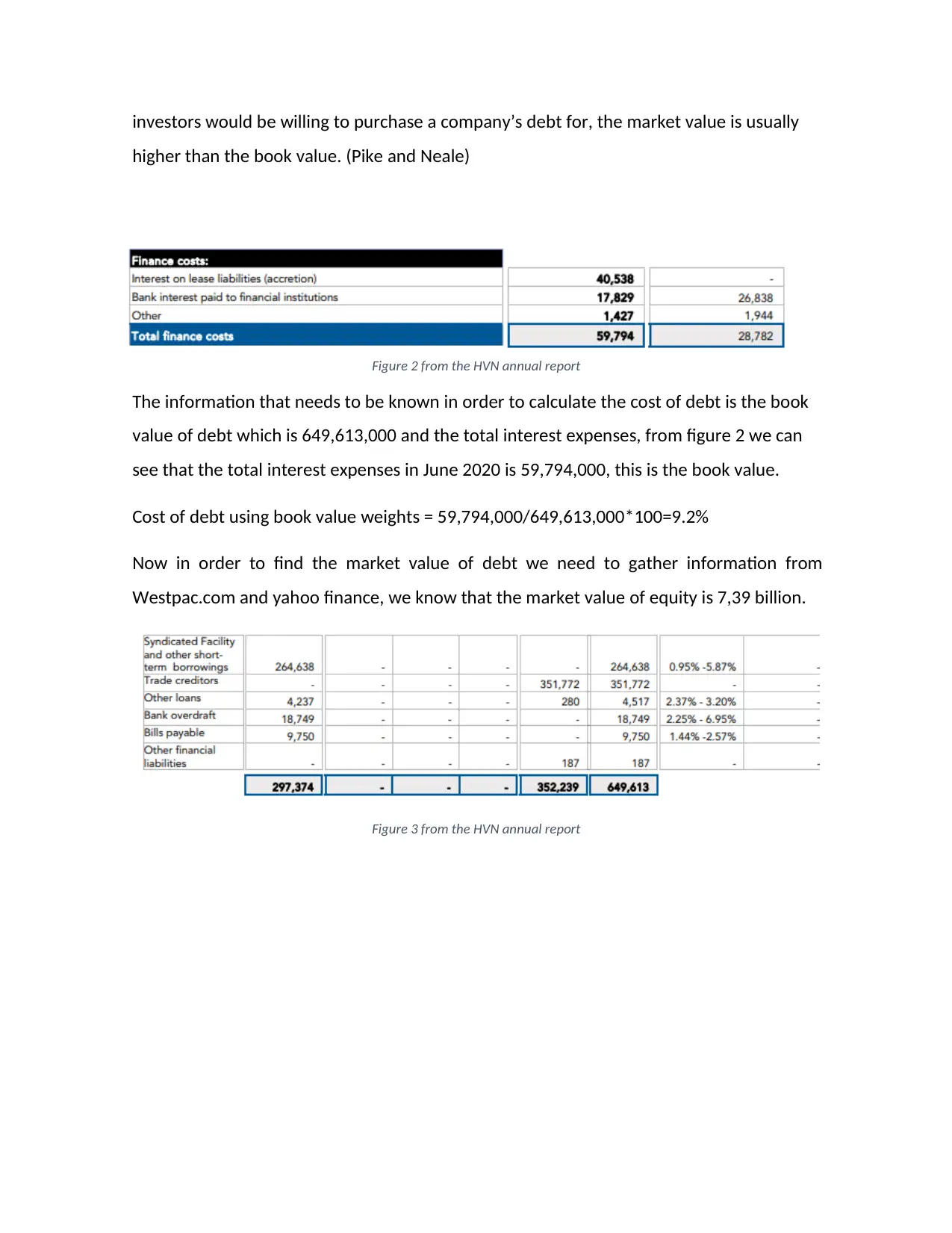

Figure 4 Loan rates from Westpac.com

From figure 3 we can see the debts that Harvey Norman has outstanding, from the

information we have from Westpac.com as seen from figure 4 we can see what the interest

rates is:

Business development rate: 4.77% p.a

From figure 3 we can see the debts that Harvey Norman has outstanding, from the

information we have from Westpac.com as seen from figure 4 we can see what the interest

rates is:

Business development rate: 4.77% p.a

(From here I am not sure what to do and how to find the information to calculate the market value

of debt, however, in order to show my calculations I am going to find some proxy numbers that I

know are not correct just in order to show how I would calculate the market value of debt)

The formula for calculating the market value of debt is:

C((1-(1/((1+KD)t)))/KD)+(FV/((1+KDt))

Where: C = interest expenses = 59,794,000

KD = cost of debt % = 9.2%

T = weighted maturity in years = 10 years (this is what I am guessing)

FV = the total debt = 649,613,000

59,794,000((1-(1/((1+0.092)10)))/0.092)+( 649,613,000/((1+0.09210)) = 649,801,327

So now we have the market value of debt and from that we can calculate the cost of debt

using market value weights.

Cost of debt using market value weights =59,794,000/649,801,327* 100 = 9,2 %

(The information I have gathered from Westpac.com, I am not sure how to use that, I also know that

from yahoo finance it says on the balance sheet that total liabilities are 2,351,277,000, therefore, I

am wondering if that is the number that should be used in the formula for finding the market value

of debt?)

Using the information from yahoo finance where it says that the total debt is 2,351,277,000

the market value of debt is:

59,794,000((1-(1/((1+0.092)10)))/0.092)+( 2,351,277,000/((1+0.09210)) = 1,355,545,705

Cost of debt is then: 59,794,000/2,351,277,000*100=2.54%

As we can see there is a lot of difference between using the total liabilities as shown in the

annual report and then using the total liabilities as shown on yahoo finance.

After I had some difficulties calculating the market value of debt and was not sure what information

to use as I mentioned earlier and after I could not reach you I had a phone call with Dr Tony Stevenson

of debt, however, in order to show my calculations I am going to find some proxy numbers that I

know are not correct just in order to show how I would calculate the market value of debt)

The formula for calculating the market value of debt is:

C((1-(1/((1+KD)t)))/KD)+(FV/((1+KDt))

Where: C = interest expenses = 59,794,000

KD = cost of debt % = 9.2%

T = weighted maturity in years = 10 years (this is what I am guessing)

FV = the total debt = 649,613,000

59,794,000((1-(1/((1+0.092)10)))/0.092)+( 649,613,000/((1+0.09210)) = 649,801,327

So now we have the market value of debt and from that we can calculate the cost of debt

using market value weights.

Cost of debt using market value weights =59,794,000/649,801,327* 100 = 9,2 %

(The information I have gathered from Westpac.com, I am not sure how to use that, I also know that

from yahoo finance it says on the balance sheet that total liabilities are 2,351,277,000, therefore, I

am wondering if that is the number that should be used in the formula for finding the market value

of debt?)

Using the information from yahoo finance where it says that the total debt is 2,351,277,000

the market value of debt is:

59,794,000((1-(1/((1+0.092)10)))/0.092)+( 2,351,277,000/((1+0.09210)) = 1,355,545,705

Cost of debt is then: 59,794,000/2,351,277,000*100=2.54%

As we can see there is a lot of difference between using the total liabilities as shown in the

annual report and then using the total liabilities as shown on yahoo finance.

After I had some difficulties calculating the market value of debt and was not sure what information

to use as I mentioned earlier and after I could not reach you I had a phone call with Dr Tony Stevenson

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and he helped me a lot. I then realized the rate I was searching for on the Westpac website is the

business development rate. He advised me to show multiple calculations as I have done even though

I am not 100% sure that I have collected the correct information.

Question 4

The weighted average cost of capital (WACC) is the average interest rate that a company is

expected to pay to all of its security holders in order to finance its assets. The WACC is also

known as the firm's cost of capital. In general, debt and equity are used to finance a

company's assets. WACC is the average of these sources of financing's costs, which are

weighted by their respective use in the given situation. We can calculate how much interest

the company must pay for each dollar financed by taking a weighted average. (Pike and

Neale)

The formula for WACC is: WACC = E / (E + D) * Cost of equity + D / (E+D) * Cost of debt * (1 – Tax Rate)

Using book value weights: E = equity = 955,338,000

D = Debt = 649,613,000

Cost of equity = 6%

Cost of Debt = 9.2%

Tax rate = 30%

Weight of equity = 955,338,000/(955,338,000+649,613,000)=0.5952

Weight of debt = 649,613,000/(955,338,000+649,613,000)=0.40475

WACC = 0.5952 * 0.06 + 0.40475 * 0.092 * (1-0.30) = 0.06177 = 6.2%

Using market value weights: E = 7,390,000,000

D = 649,801,327

Cost of equity = 6%

Cost of debt = 9.2%

business development rate. He advised me to show multiple calculations as I have done even though

I am not 100% sure that I have collected the correct information.

Question 4

The weighted average cost of capital (WACC) is the average interest rate that a company is

expected to pay to all of its security holders in order to finance its assets. The WACC is also

known as the firm's cost of capital. In general, debt and equity are used to finance a

company's assets. WACC is the average of these sources of financing's costs, which are

weighted by their respective use in the given situation. We can calculate how much interest

the company must pay for each dollar financed by taking a weighted average. (Pike and

Neale)

The formula for WACC is: WACC = E / (E + D) * Cost of equity + D / (E+D) * Cost of debt * (1 – Tax Rate)

Using book value weights: E = equity = 955,338,000

D = Debt = 649,613,000

Cost of equity = 6%

Cost of Debt = 9.2%

Tax rate = 30%

Weight of equity = 955,338,000/(955,338,000+649,613,000)=0.5952

Weight of debt = 649,613,000/(955,338,000+649,613,000)=0.40475

WACC = 0.5952 * 0.06 + 0.40475 * 0.092 * (1-0.30) = 0.06177 = 6.2%

Using market value weights: E = 7,390,000,000

D = 649,801,327

Cost of equity = 6%

Cost of debt = 9.2%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

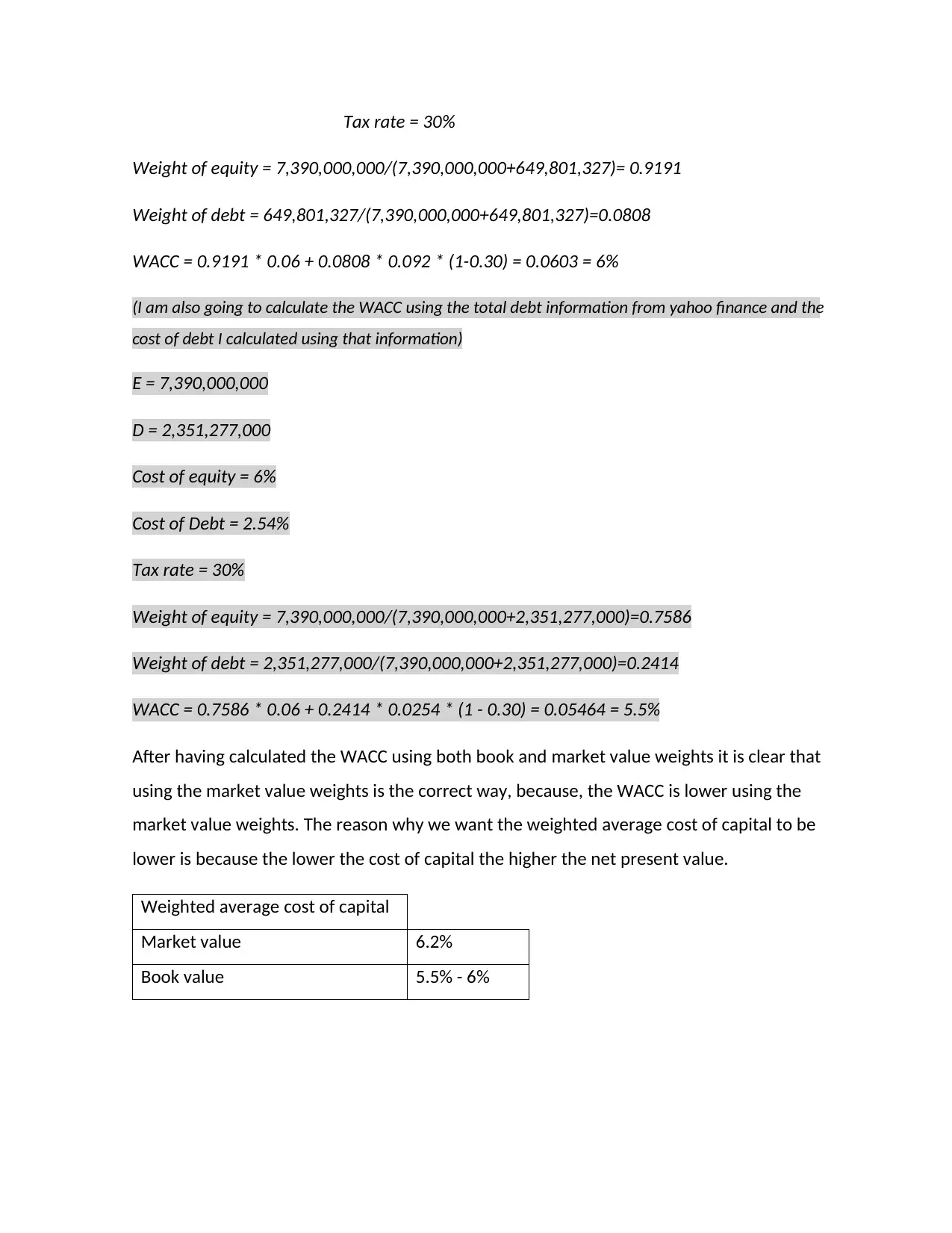

Tax rate = 30%

Weight of equity = 7,390,000,000/(7,390,000,000+649,801,327)= 0.9191

Weight of debt = 649,801,327/(7,390,000,000+649,801,327)=0.0808

WACC = 0.9191 * 0.06 + 0.0808 * 0.092 * (1-0.30) = 0.0603 = 6%

(I am also going to calculate the WACC using the total debt information from yahoo finance and the

cost of debt I calculated using that information)

E = 7,390,000,000

D = 2,351,277,000

Cost of equity = 6%

Cost of Debt = 2.54%

Tax rate = 30%

Weight of equity = 7,390,000,000/(7,390,000,000+2,351,277,000)=0.7586

Weight of debt = 2,351,277,000/(7,390,000,000+2,351,277,000)=0.2414

WACC = 0.7586 * 0.06 + 0.2414 * 0.0254 * (1 - 0.30) = 0.05464 = 5.5%

After having calculated the WACC using both book and market value weights it is clear that

using the market value weights is the correct way, because, the WACC is lower using the

market value weights. The reason why we want the weighted average cost of capital to be

lower is because the lower the cost of capital the higher the net present value.

Weighted average cost of capital

Market value 6.2%

Book value 5.5% - 6%

Weight of equity = 7,390,000,000/(7,390,000,000+649,801,327)= 0.9191

Weight of debt = 649,801,327/(7,390,000,000+649,801,327)=0.0808

WACC = 0.9191 * 0.06 + 0.0808 * 0.092 * (1-0.30) = 0.0603 = 6%

(I am also going to calculate the WACC using the total debt information from yahoo finance and the

cost of debt I calculated using that information)

E = 7,390,000,000

D = 2,351,277,000

Cost of equity = 6%

Cost of Debt = 2.54%

Tax rate = 30%

Weight of equity = 7,390,000,000/(7,390,000,000+2,351,277,000)=0.7586

Weight of debt = 2,351,277,000/(7,390,000,000+2,351,277,000)=0.2414

WACC = 0.7586 * 0.06 + 0.2414 * 0.0254 * (1 - 0.30) = 0.05464 = 5.5%

After having calculated the WACC using both book and market value weights it is clear that

using the market value weights is the correct way, because, the WACC is lower using the

market value weights. The reason why we want the weighted average cost of capital to be

lower is because the lower the cost of capital the higher the net present value.

Weighted average cost of capital

Market value 6.2%

Book value 5.5% - 6%

Question 5

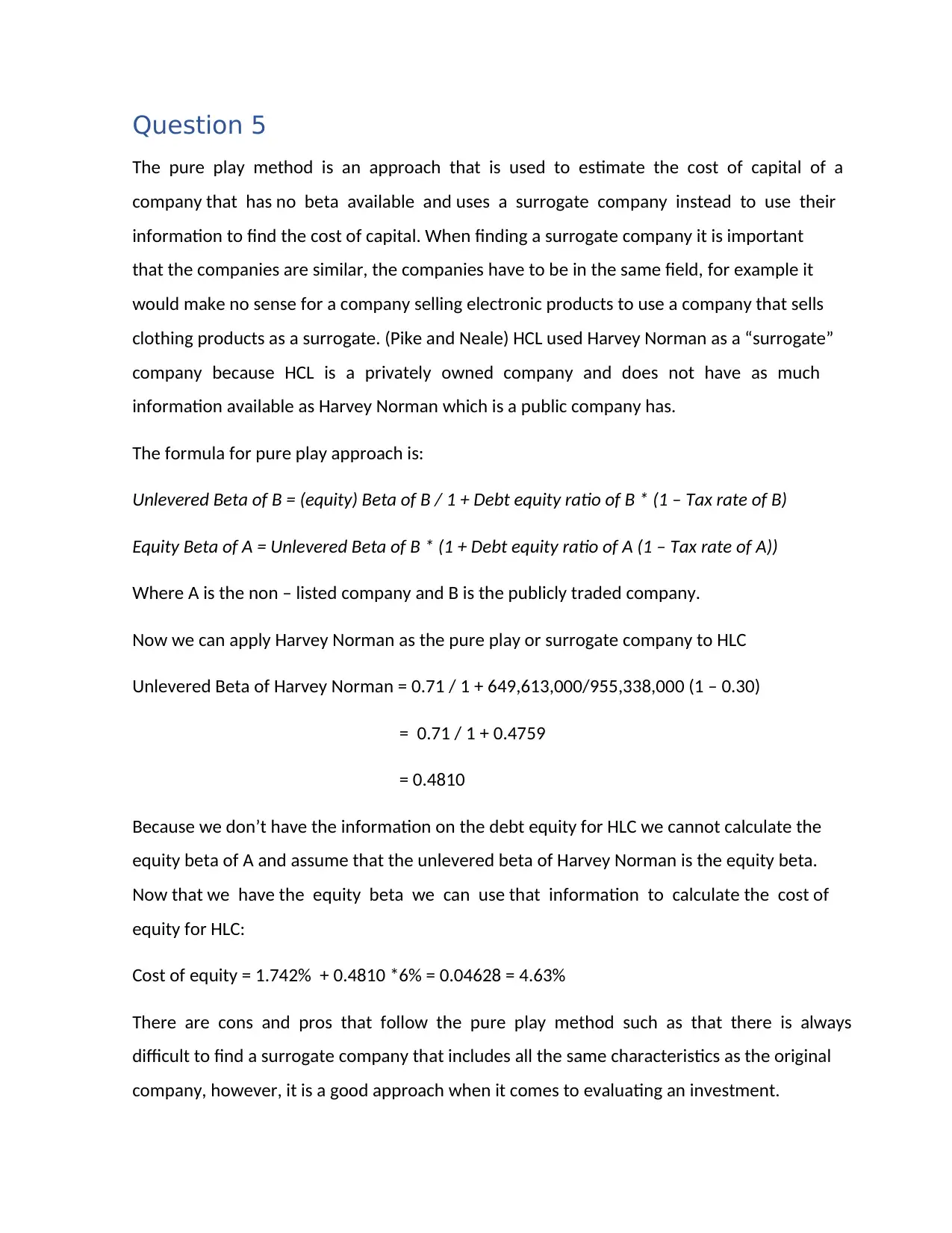

The pure play method is an approach that is used to estimate the cost of capital of a

company that has no beta available and uses a surrogate company instead to use their

information to find the cost of capital. When finding a surrogate company it is important

that the companies are similar, the companies have to be in the same field, for example it

would make no sense for a company selling electronic products to use a company that sells

clothing products as a surrogate. (Pike and Neale) HCL used Harvey Norman as a “surrogate”

company because HCL is a privately owned company and does not have as much

information available as Harvey Norman which is a public company has.

The formula for pure play approach is:

Unlevered Beta of B = (equity) Beta of B / 1 + Debt equity ratio of B * (1 – Tax rate of B)

Equity Beta of A = Unlevered Beta of B * (1 + Debt equity ratio of A (1 – Tax rate of A))

Where A is the non – listed company and B is the publicly traded company.

Now we can apply Harvey Norman as the pure play or surrogate company to HLC

Unlevered Beta of Harvey Norman = 0.71 / 1 + 649,613,000/955,338,000 (1 – 0.30)

= 0.71 / 1 + 0.4759

= 0.4810

Because we don’t have the information on the debt equity for HLC we cannot calculate the

equity beta of A and assume that the unlevered beta of Harvey Norman is the equity beta.

Now that we have the equity beta we can use that information to calculate the cost of

equity for HLC:

Cost of equity = 1.742% + 0.4810 *6% = 0.04628 = 4.63%

There are cons and pros that follow the pure play method such as that there is always

difficult to find a surrogate company that includes all the same characteristics as the original

company, however, it is a good approach when it comes to evaluating an investment.

The pure play method is an approach that is used to estimate the cost of capital of a

company that has no beta available and uses a surrogate company instead to use their

information to find the cost of capital. When finding a surrogate company it is important

that the companies are similar, the companies have to be in the same field, for example it

would make no sense for a company selling electronic products to use a company that sells

clothing products as a surrogate. (Pike and Neale) HCL used Harvey Norman as a “surrogate”

company because HCL is a privately owned company and does not have as much

information available as Harvey Norman which is a public company has.

The formula for pure play approach is:

Unlevered Beta of B = (equity) Beta of B / 1 + Debt equity ratio of B * (1 – Tax rate of B)

Equity Beta of A = Unlevered Beta of B * (1 + Debt equity ratio of A (1 – Tax rate of A))

Where A is the non – listed company and B is the publicly traded company.

Now we can apply Harvey Norman as the pure play or surrogate company to HLC

Unlevered Beta of Harvey Norman = 0.71 / 1 + 649,613,000/955,338,000 (1 – 0.30)

= 0.71 / 1 + 0.4759

= 0.4810

Because we don’t have the information on the debt equity for HLC we cannot calculate the

equity beta of A and assume that the unlevered beta of Harvey Norman is the equity beta.

Now that we have the equity beta we can use that information to calculate the cost of

equity for HLC:

Cost of equity = 1.742% + 0.4810 *6% = 0.04628 = 4.63%

There are cons and pros that follow the pure play method such as that there is always

difficult to find a surrogate company that includes all the same characteristics as the original

company, however, it is a good approach when it comes to evaluating an investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.