Ratio Analysis & Cash Flow Statement: Complete Solution Guide

VerifiedAdded on 2023/06/18

|3

|617

|430

Homework Assignment

AI Summary

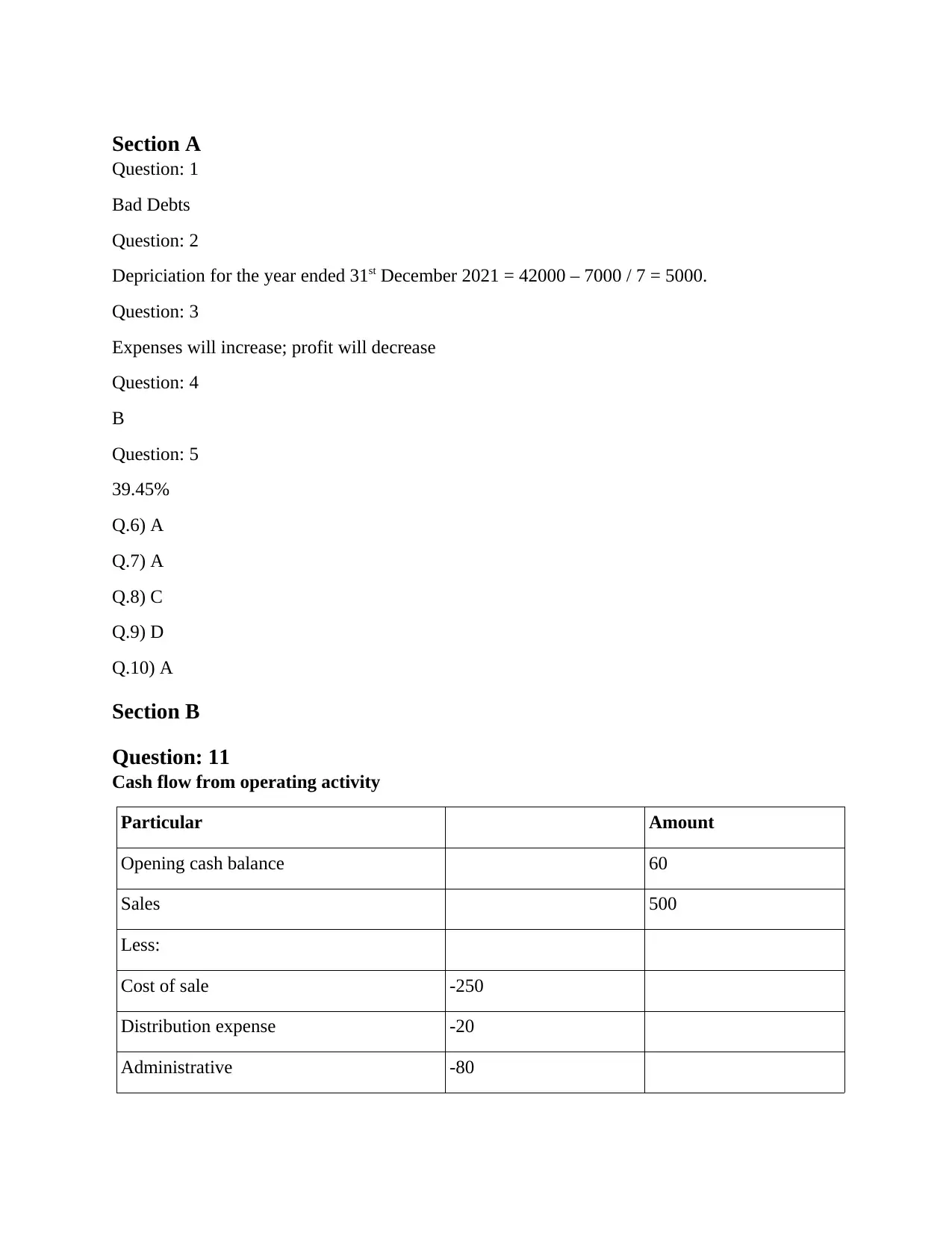

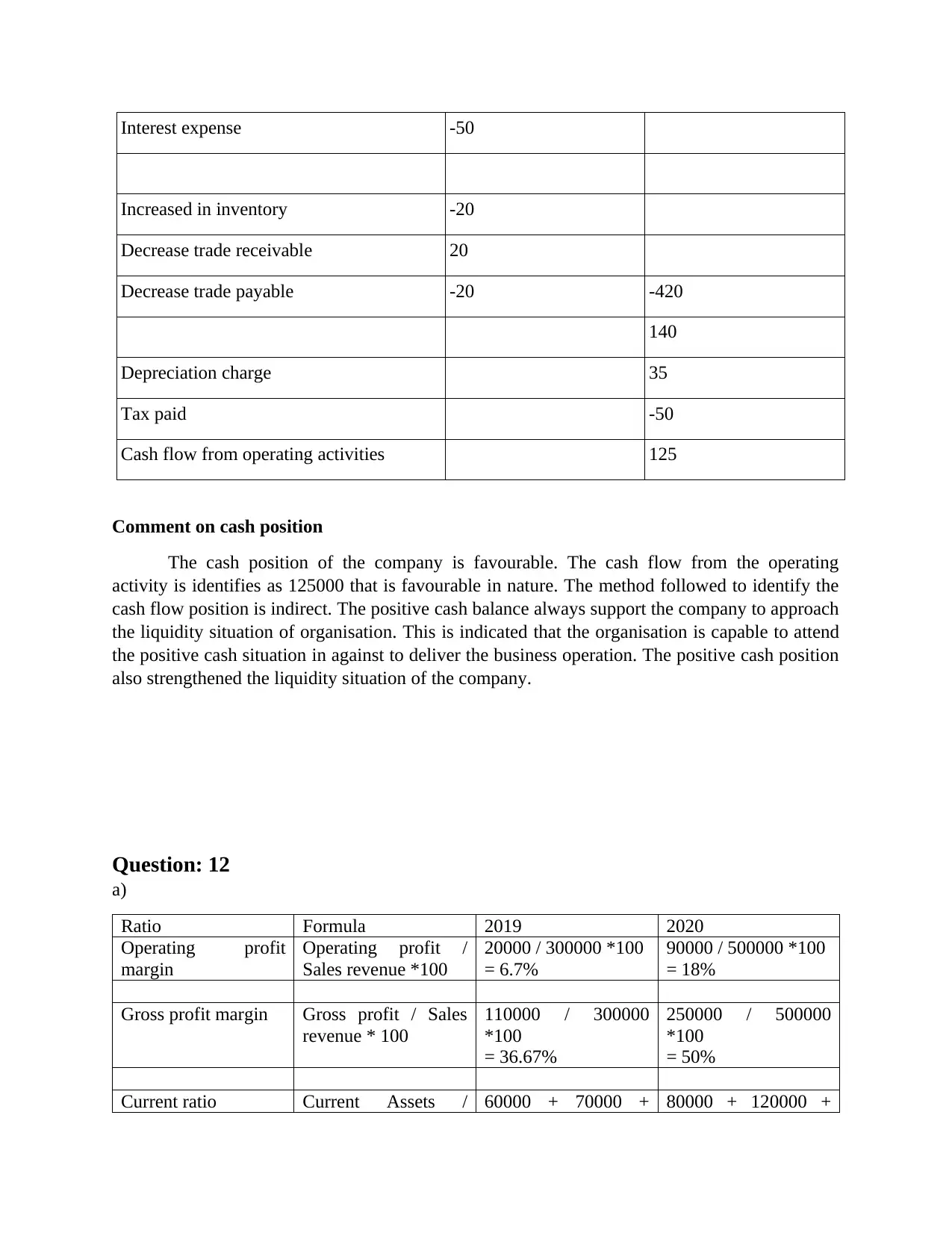

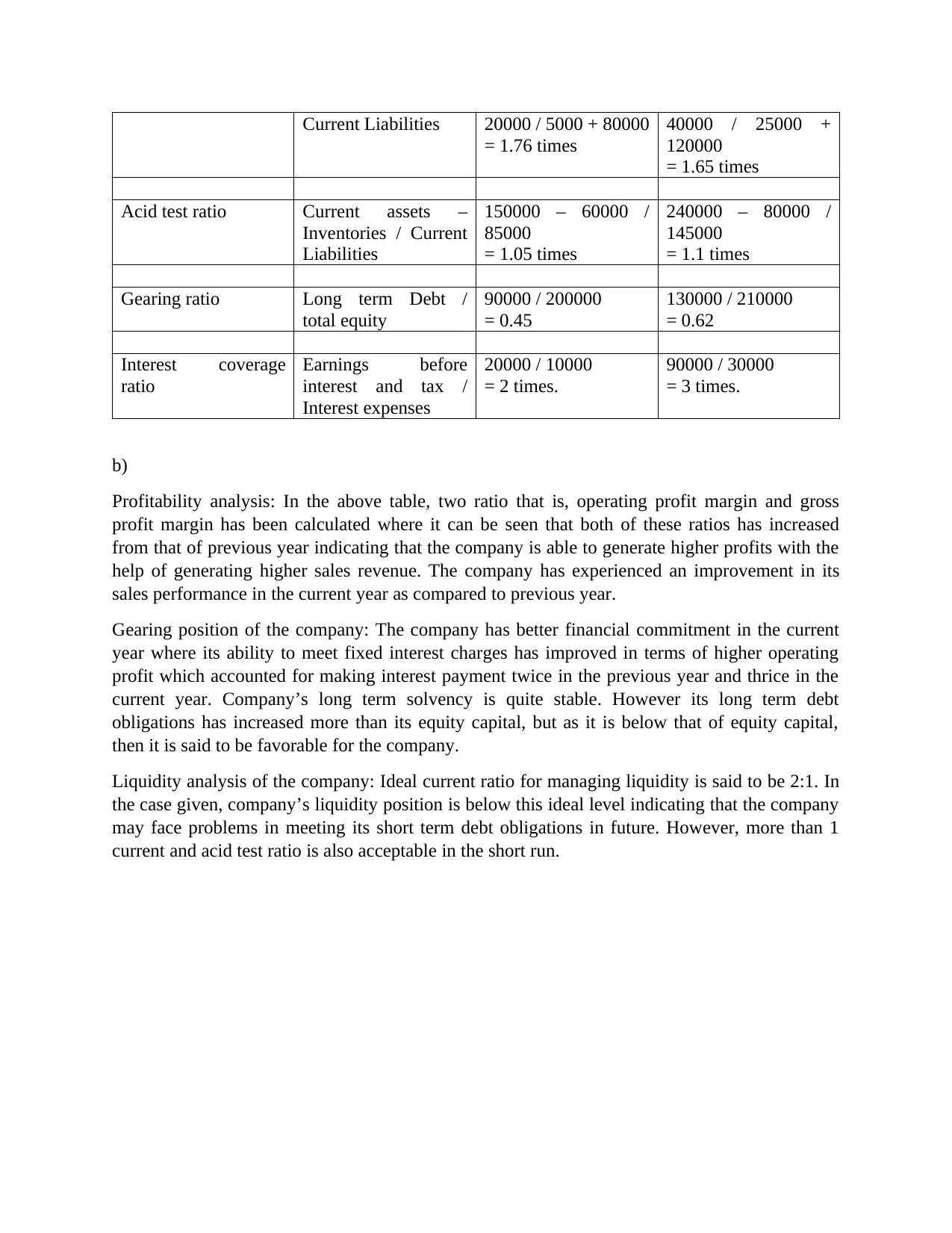

This assignment solution covers key aspects of financial analysis, including ratio calculations and cash flow statement preparation. It begins with multiple-choice questions on topics such as bad debts and depreciation. Section B provides a detailed cash flow statement from operating activities, highlighting a favorable cash position and positive implications for the company's liquidity. The solution includes a ratio analysis, calculating operating profit margin, gross profit margin, current ratio, acid test ratio, gearing ratio, and interest coverage ratio for both 2019 and 2020. The analysis interprets profitability, gearing position, and liquidity, noting improvements in profitability and gearing but potential liquidity concerns. Desklib provides this document and many other solved assignments for students.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.