Financial Statement Analysis, Ratio Calculation, and Reporting

VerifiedAdded on 2020/03/13

|6

|1165

|381

Homework Assignment

AI Summary

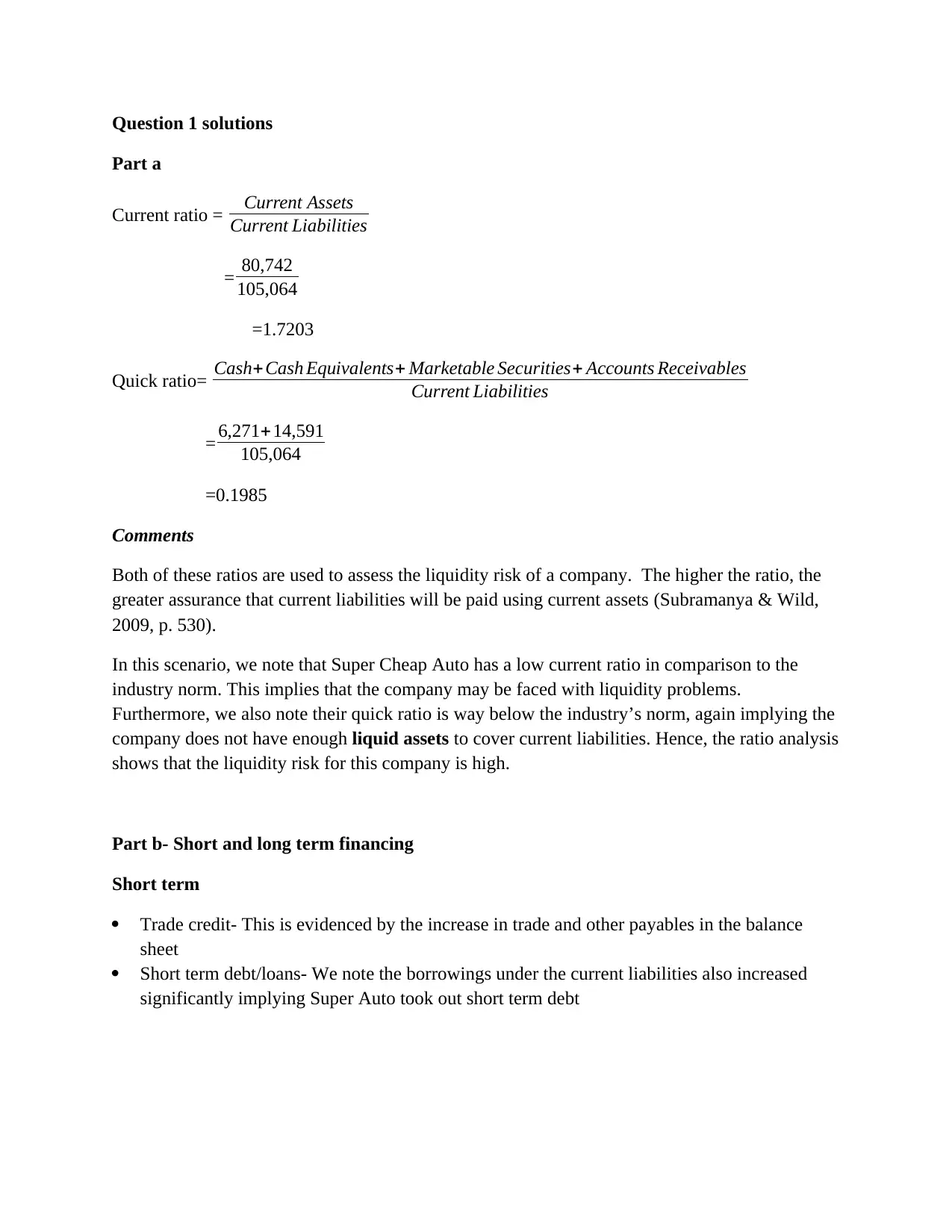

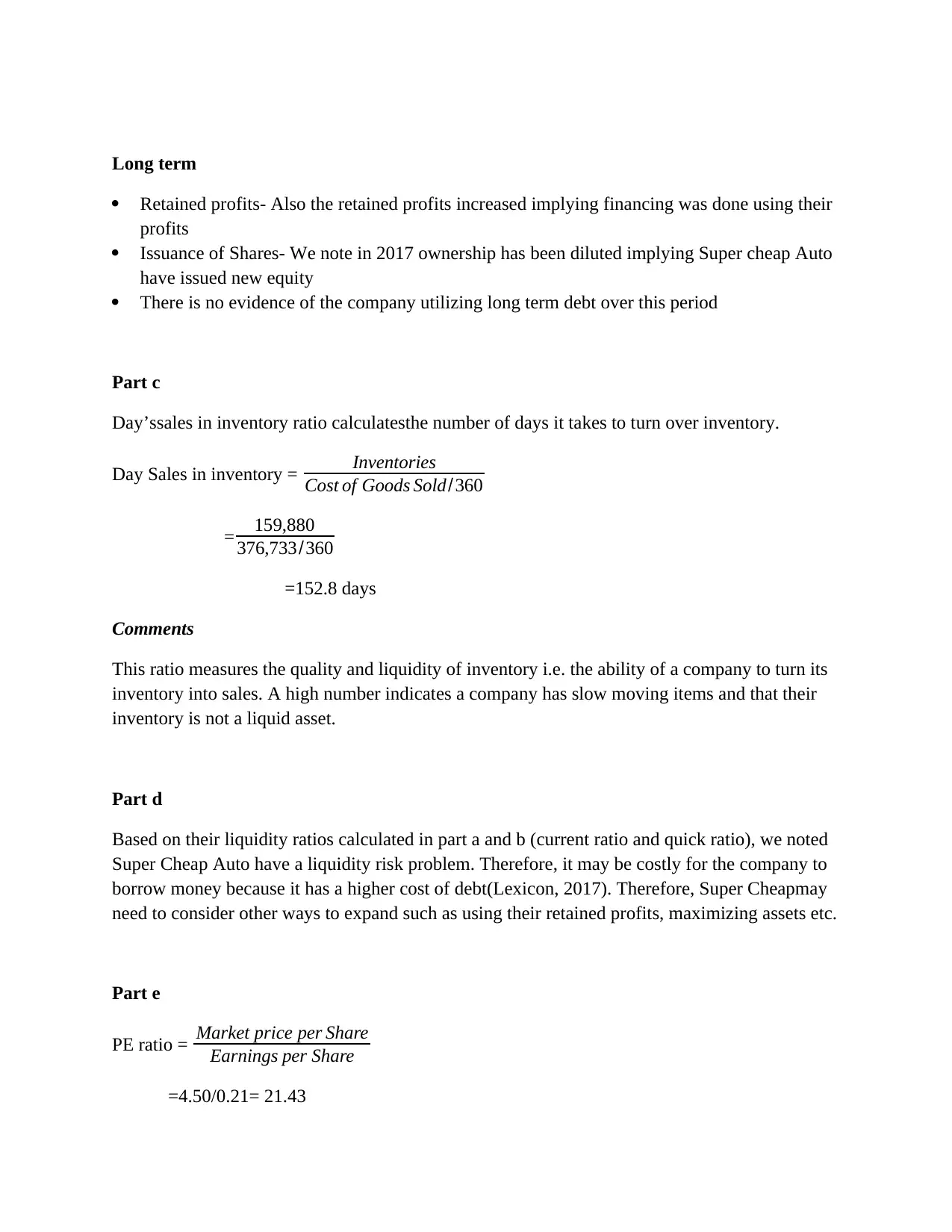

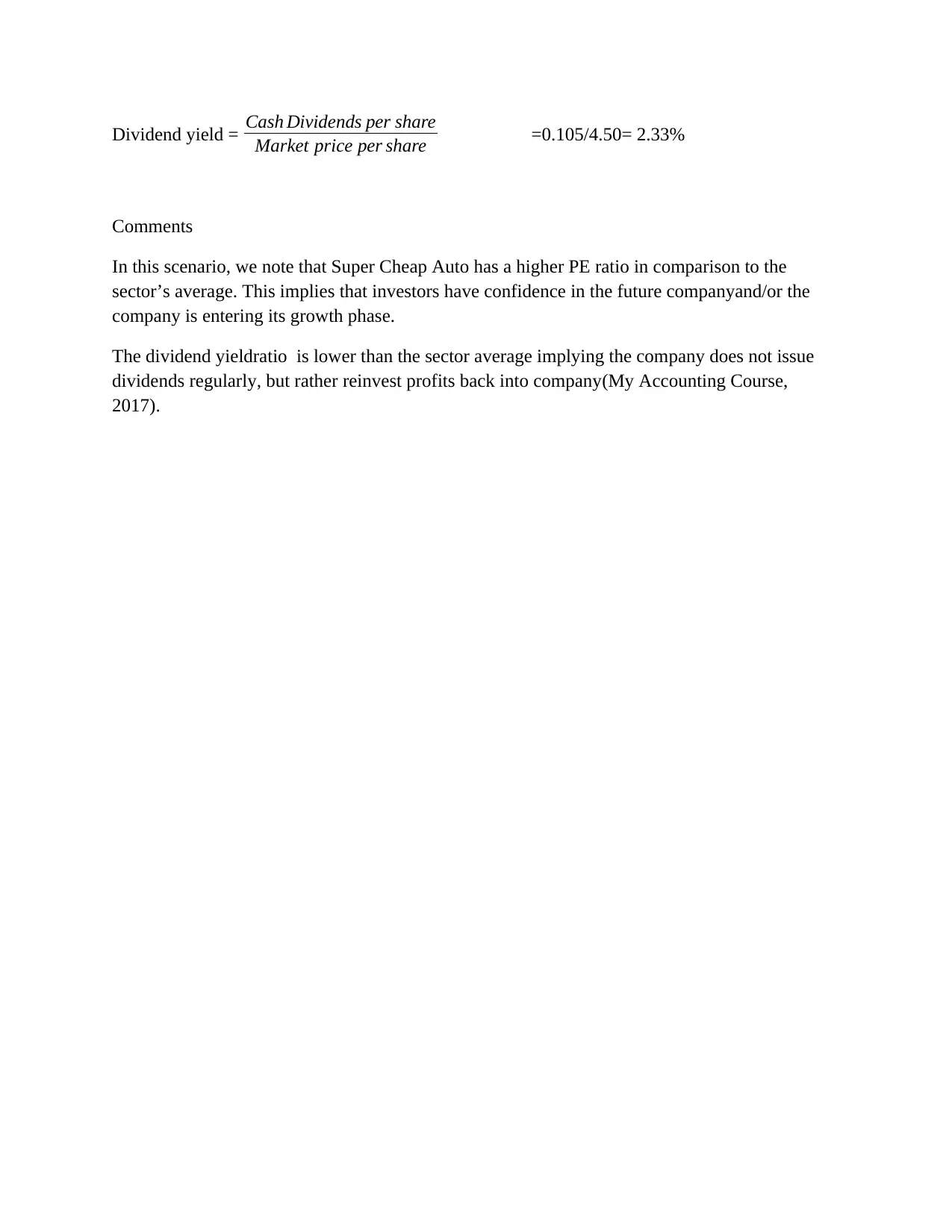

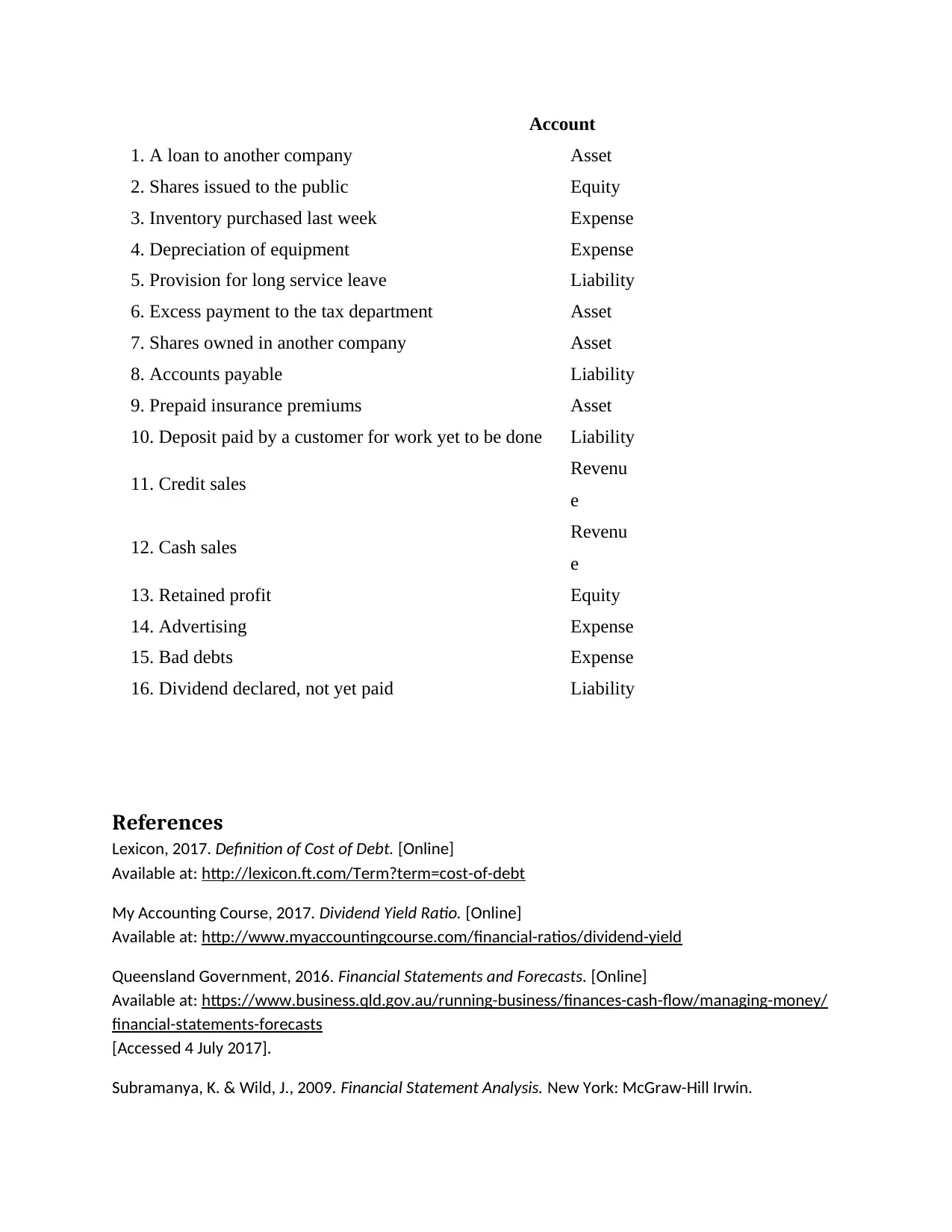

This homework assignment solution addresses key concepts in financial statement analysis. The solution begins with the calculation and interpretation of liquidity ratios, including the current and quick ratios, to assess a company's ability to meet its short-term obligations. It further analyzes short and long-term financing methods, such as trade credit, short-term debt, retained profits, and equity issuance. The solution then calculates the days sales in inventory ratio, providing insights into inventory management efficiency. The assignment also examines profitability ratios, like the PE ratio and dividend yield, and their implications for investors. The solution also identifies the different users of financial statements, their financial needs, benefits, and limitations of financial statement analysis. Finally, the solution categorizes various financial transactions into their appropriate accounting elements, such as assets, liabilities, equity, revenues, and expenses.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.