Evaluating Financial Performance: A Report on Honeywell Plc (2017)

VerifiedAdded on 2020/07/22

|21

|4989

|102

Report

AI Summary

This report presents a comprehensive financial analysis of Honeywell Plc, evaluating its performance through ratio analysis, including profitability, liquidity, gearing, and efficiency ratios. The report highlights the decline in profitability and liquidity in 2016 compared to 2015 and suggests strategic actions to improve financial performance. It calculates the working capital cycle, identifying an increase in working capital days in 2016, and discusses the break-even point (BEP) and margin of safety for Thompson Ltd, along with a critical evaluation of the assumptions associated with the BEP model. The report also assesses internal and external sources of finance and evaluates investment appraisal techniques, providing a detailed overview of financial management principles and their application to real-world business scenarios. The analysis covers various aspects of financial health, offering insights into decision-making and strategic planning for the company.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

1. Preparing a report for BOD of Honeywell Plc in relation to evaluating financial

performance.................................................................................................................................1

To,....................................................................................................................................................1

2. Calculating working capital cycle for Honeywell Plc.............................................................6

PART B...........................................................................................................................................8

1. Calculating BEP and margin of safety for Thompson Ltd......................................................8

2. Critically evaluating the key assumptions that are associated with BEP model.....................8

PART C.........................................................................................................................................10

1. Assessing the internal and external sources of finance that can be undertaken by business.10

2. Critically evaluating the investment appraisal techniques that are available for business....12

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................16

1. Preparing a report for BOD of Honeywell Plc in relation to evaluating financial

performance.................................................................................................................................1

To,....................................................................................................................................................1

2. Calculating working capital cycle for Honeywell Plc.............................................................6

PART B...........................................................................................................................................8

1. Calculating BEP and margin of safety for Thompson Ltd......................................................8

2. Critically evaluating the key assumptions that are associated with BEP model.....................8

PART C.........................................................................................................................................10

1. Assessing the internal and external sources of finance that can be undertaken by business.10

2. Critically evaluating the investment appraisal techniques that are available for business....12

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................16

1. Preparing a report for BOD of Honeywell Plc in relation to evaluating financial performance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

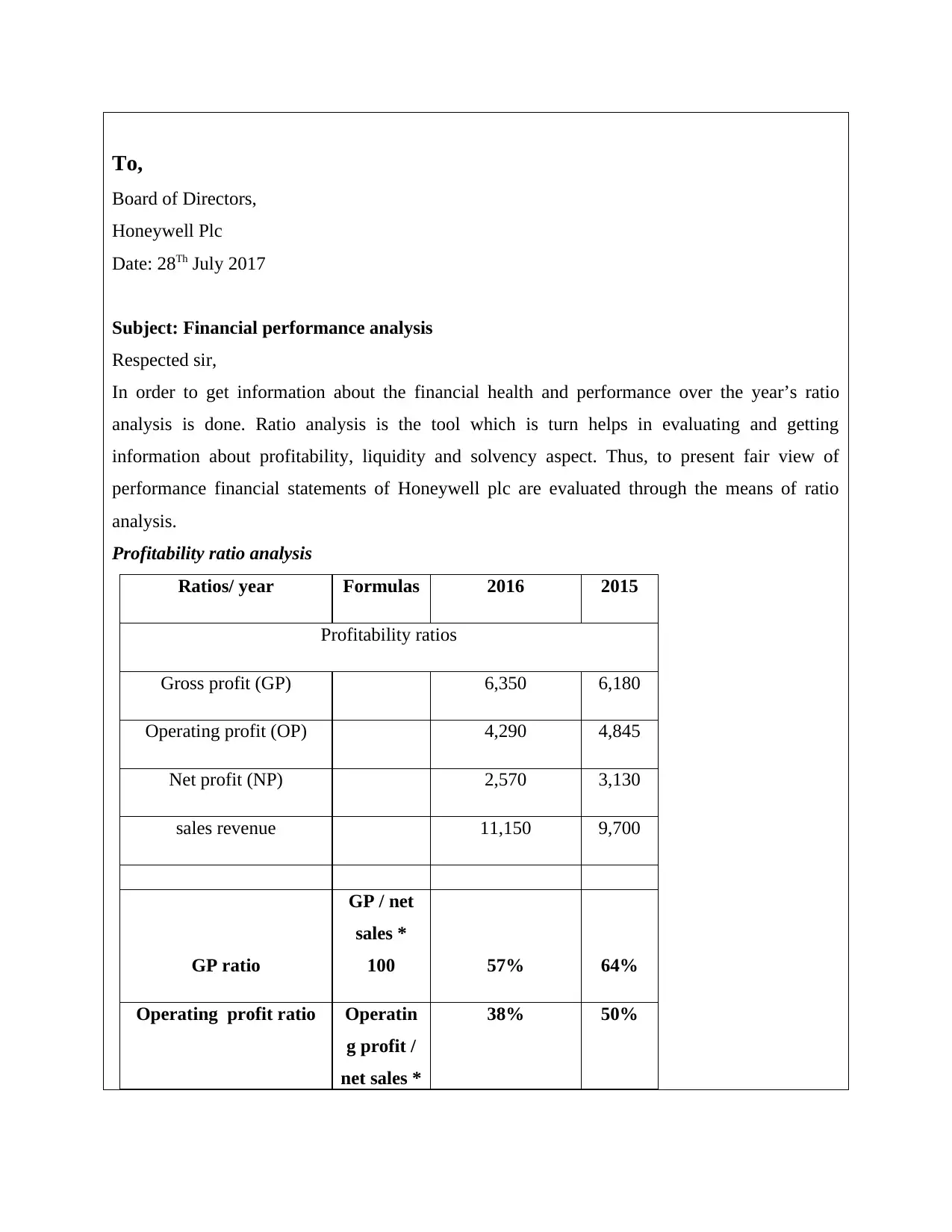

To,

Board of Directors,

Honeywell Plc

Date: 28Th July 2017

Subject: Financial performance analysis

Respected sir,

In order to get information about the financial health and performance over the year’s ratio

analysis is done. Ratio analysis is the tool which is turn helps in evaluating and getting

information about profitability, liquidity and solvency aspect. Thus, to present fair view of

performance financial statements of Honeywell plc are evaluated through the means of ratio

analysis.

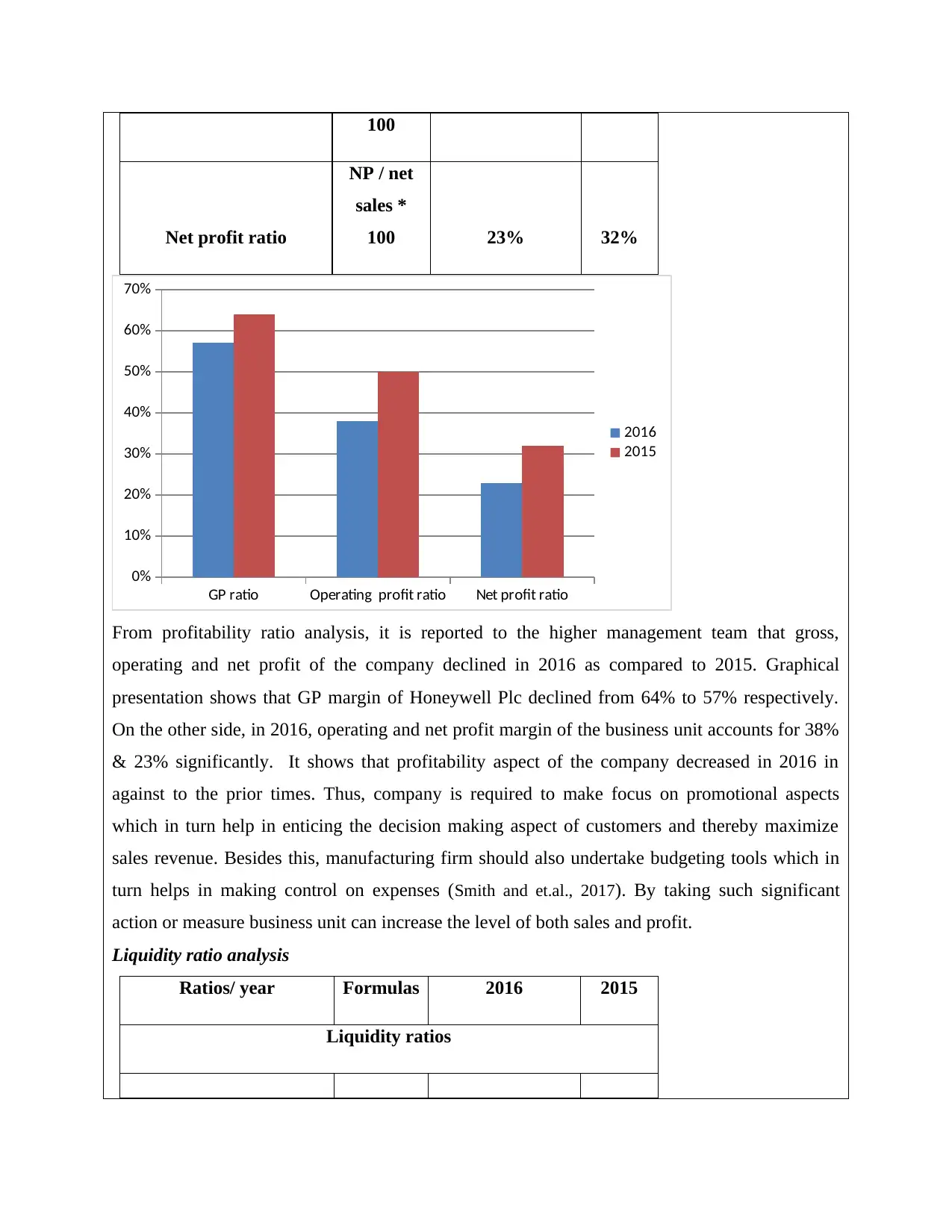

Profitability ratio analysis

Ratios/ year Formulas 2016 2015

Profitability ratios

Gross profit (GP) 6,350 6,180

Operating profit (OP) 4,290 4,845

Net profit (NP) 2,570 3,130

sales revenue 11,150 9,700

GP ratio

GP / net

sales *

100 57% 64%

Operating profit ratio Operatin

g profit /

net sales *

38% 50%

Board of Directors,

Honeywell Plc

Date: 28Th July 2017

Subject: Financial performance analysis

Respected sir,

In order to get information about the financial health and performance over the year’s ratio

analysis is done. Ratio analysis is the tool which is turn helps in evaluating and getting

information about profitability, liquidity and solvency aspect. Thus, to present fair view of

performance financial statements of Honeywell plc are evaluated through the means of ratio

analysis.

Profitability ratio analysis

Ratios/ year Formulas 2016 2015

Profitability ratios

Gross profit (GP) 6,350 6,180

Operating profit (OP) 4,290 4,845

Net profit (NP) 2,570 3,130

sales revenue 11,150 9,700

GP ratio

GP / net

sales *

100 57% 64%

Operating profit ratio Operatin

g profit /

net sales *

38% 50%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

100

Net profit ratio

NP / net

sales *

100 23% 32%

GP ratio Operating profit ratio Net profit ratio

0%

10%

20%

30%

40%

50%

60%

70%

2016

2015

From profitability ratio analysis, it is reported to the higher management team that gross,

operating and net profit of the company declined in 2016 as compared to 2015. Graphical

presentation shows that GP margin of Honeywell Plc declined from 64% to 57% respectively.

On the other side, in 2016, operating and net profit margin of the business unit accounts for 38%

& 23% significantly. It shows that profitability aspect of the company decreased in 2016 in

against to the prior times. Thus, company is required to make focus on promotional aspects

which in turn help in enticing the decision making aspect of customers and thereby maximize

sales revenue. Besides this, manufacturing firm should also undertake budgeting tools which in

turn helps in making control on expenses (Smith and et.al., 2017). By taking such significant

action or measure business unit can increase the level of both sales and profit.

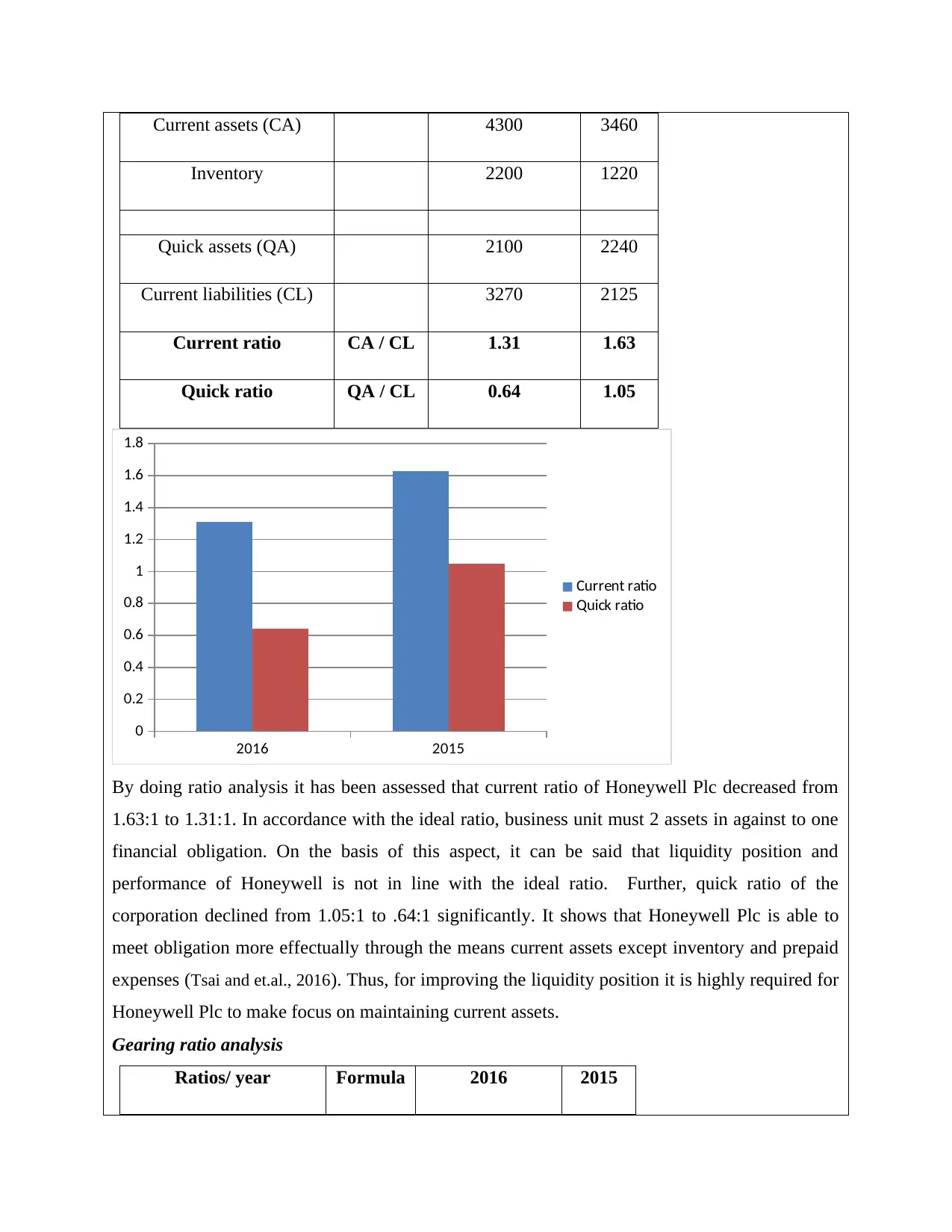

Liquidity ratio analysis

Ratios/ year Formulas 2016 2015

Liquidity ratios

Net profit ratio

NP / net

sales *

100 23% 32%

GP ratio Operating profit ratio Net profit ratio

0%

10%

20%

30%

40%

50%

60%

70%

2016

2015

From profitability ratio analysis, it is reported to the higher management team that gross,

operating and net profit of the company declined in 2016 as compared to 2015. Graphical

presentation shows that GP margin of Honeywell Plc declined from 64% to 57% respectively.

On the other side, in 2016, operating and net profit margin of the business unit accounts for 38%

& 23% significantly. It shows that profitability aspect of the company decreased in 2016 in

against to the prior times. Thus, company is required to make focus on promotional aspects

which in turn help in enticing the decision making aspect of customers and thereby maximize

sales revenue. Besides this, manufacturing firm should also undertake budgeting tools which in

turn helps in making control on expenses (Smith and et.al., 2017). By taking such significant

action or measure business unit can increase the level of both sales and profit.

Liquidity ratio analysis

Ratios/ year Formulas 2016 2015

Liquidity ratios

Current assets (CA) 4300 3460

Inventory 2200 1220

Quick assets (QA) 2100 2240

Current liabilities (CL) 3270 2125

Current ratio CA / CL 1.31 1.63

Quick ratio QA / CL 0.64 1.05

2016 2015

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Current ratio

Quick ratio

By doing ratio analysis it has been assessed that current ratio of Honeywell Plc decreased from

1.63:1 to 1.31:1. In accordance with the ideal ratio, business unit must 2 assets in against to one

financial obligation. On the basis of this aspect, it can be said that liquidity position and

performance of Honeywell is not in line with the ideal ratio. Further, quick ratio of the

corporation declined from 1.05:1 to .64:1 significantly. It shows that Honeywell Plc is able to

meet obligation more effectually through the means current assets except inventory and prepaid

expenses (Tsai and et.al., 2016). Thus, for improving the liquidity position it is highly required for

Honeywell Plc to make focus on maintaining current assets.

Gearing ratio analysis

Ratios/ year Formula 2016 2015

Inventory 2200 1220

Quick assets (QA) 2100 2240

Current liabilities (CL) 3270 2125

Current ratio CA / CL 1.31 1.63

Quick ratio QA / CL 0.64 1.05

2016 2015

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Current ratio

Quick ratio

By doing ratio analysis it has been assessed that current ratio of Honeywell Plc decreased from

1.63:1 to 1.31:1. In accordance with the ideal ratio, business unit must 2 assets in against to one

financial obligation. On the basis of this aspect, it can be said that liquidity position and

performance of Honeywell is not in line with the ideal ratio. Further, quick ratio of the

corporation declined from 1.05:1 to .64:1 significantly. It shows that Honeywell Plc is able to

meet obligation more effectually through the means current assets except inventory and prepaid

expenses (Tsai and et.al., 2016). Thus, for improving the liquidity position it is highly required for

Honeywell Plc to make focus on maintaining current assets.

Gearing ratio analysis

Ratios/ year Formula 2016 2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

s

long-term loan capital 8000 3895

total capital employed

(7330 + 8070 +

8000) = 23400

(7330

+7000

+

3895)

=

18225

Debt-equity ratio

Long-

term loan

capital /

Total

capital

employe

d * 100 34.19%

21.37

%

2016 2015

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Debt-equity ratio

Debt-equity ratio

Outcome of ratio analysis presents that debt-equity ratio of Honeywell Plc inclined from 21.37%

to 34.19% respectively. It shows that debt level of firm increased in the year of 2016 in

comparison to 2015. Besides this, debt-equity position of Honeywell plc is also in line with the

long-term loan capital 8000 3895

total capital employed

(7330 + 8070 +

8000) = 23400

(7330

+7000

+

3895)

=

18225

Debt-equity ratio

Long-

term loan

capital /

Total

capital

employe

d * 100 34.19%

21.37

%

2016 2015

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Debt-equity ratio

Debt-equity ratio

Outcome of ratio analysis presents that debt-equity ratio of Honeywell Plc inclined from 21.37%

to 34.19% respectively. It shows that debt level of firm increased in the year of 2016 in

comparison to 2015. Besides this, debt-equity position of Honeywell plc is also in line with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ideal ratio such as .5:1. Hence, it can be presented that solvency position and performance of

company is sound.

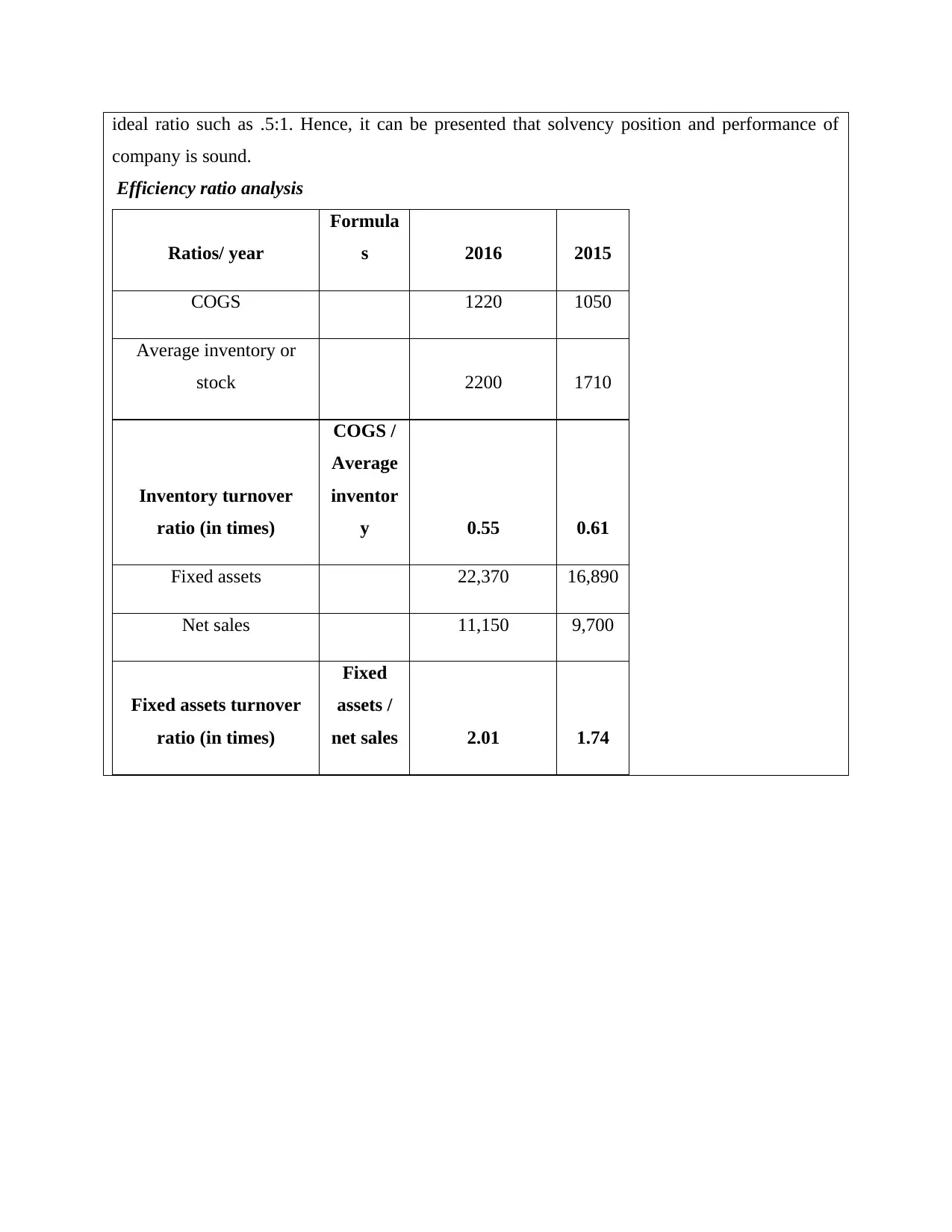

Efficiency ratio analysis

Ratios/ year

Formula

s 2016 2015

COGS 1220 1050

Average inventory or

stock 2200 1710

Inventory turnover

ratio (in times)

COGS /

Average

inventor

y 0.55 0.61

Fixed assets 22,370 16,890

Net sales 11,150 9,700

Fixed assets turnover

ratio (in times)

Fixed

assets /

net sales 2.01 1.74

company is sound.

Efficiency ratio analysis

Ratios/ year

Formula

s 2016 2015

COGS 1220 1050

Average inventory or

stock 2200 1710

Inventory turnover

ratio (in times)

COGS /

Average

inventor

y 0.55 0.61

Fixed assets 22,370 16,890

Net sales 11,150 9,700

Fixed assets turnover

ratio (in times)

Fixed

assets /

net sales 2.01 1.74

2016 2015

0

0.5

1

1.5

2

2.5

Inventory turnover ratio

Fixed assets turnover ratio

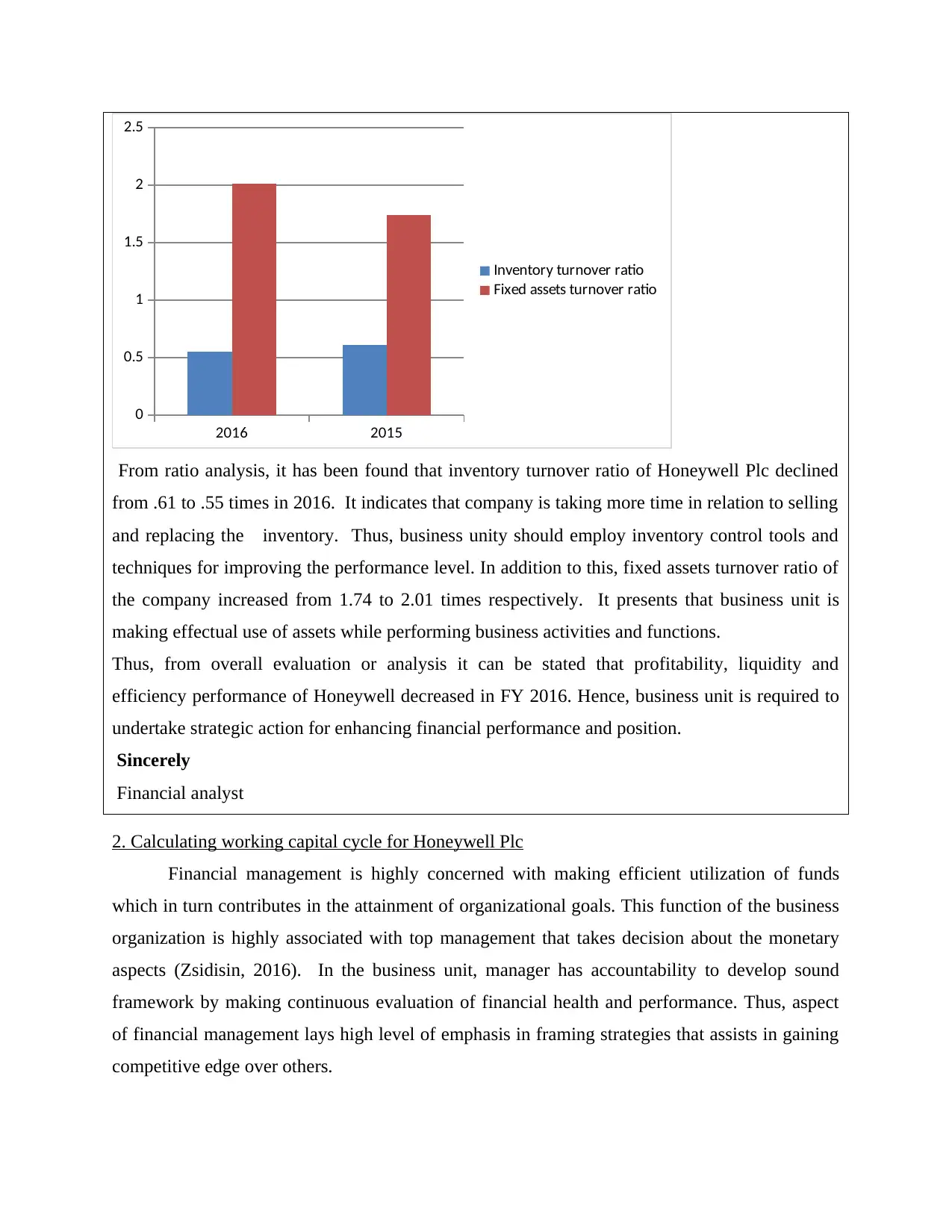

From ratio analysis, it has been found that inventory turnover ratio of Honeywell Plc declined

from .61 to .55 times in 2016. It indicates that company is taking more time in relation to selling

and replacing the inventory. Thus, business unity should employ inventory control tools and

techniques for improving the performance level. In addition to this, fixed assets turnover ratio of

the company increased from 1.74 to 2.01 times respectively. It presents that business unit is

making effectual use of assets while performing business activities and functions.

Thus, from overall evaluation or analysis it can be stated that profitability, liquidity and

efficiency performance of Honeywell decreased in FY 2016. Hence, business unit is required to

undertake strategic action for enhancing financial performance and position.

Sincerely

Financial analyst

2. Calculating working capital cycle for Honeywell Plc

Financial management is highly concerned with making efficient utilization of funds

which in turn contributes in the attainment of organizational goals. This function of the business

organization is highly associated with top management that takes decision about the monetary

aspects (Zsidisin, 2016). In the business unit, manager has accountability to develop sound

framework by making continuous evaluation of financial health and performance. Thus, aspect

of financial management lays high level of emphasis in framing strategies that assists in gaining

competitive edge over others.

0

0.5

1

1.5

2

2.5

Inventory turnover ratio

Fixed assets turnover ratio

From ratio analysis, it has been found that inventory turnover ratio of Honeywell Plc declined

from .61 to .55 times in 2016. It indicates that company is taking more time in relation to selling

and replacing the inventory. Thus, business unity should employ inventory control tools and

techniques for improving the performance level. In addition to this, fixed assets turnover ratio of

the company increased from 1.74 to 2.01 times respectively. It presents that business unit is

making effectual use of assets while performing business activities and functions.

Thus, from overall evaluation or analysis it can be stated that profitability, liquidity and

efficiency performance of Honeywell decreased in FY 2016. Hence, business unit is required to

undertake strategic action for enhancing financial performance and position.

Sincerely

Financial analyst

2. Calculating working capital cycle for Honeywell Plc

Financial management is highly concerned with making efficient utilization of funds

which in turn contributes in the attainment of organizational goals. This function of the business

organization is highly associated with top management that takes decision about the monetary

aspects (Zsidisin, 2016). In the business unit, manager has accountability to develop sound

framework by making continuous evaluation of financial health and performance. Thus, aspect

of financial management lays high level of emphasis in framing strategies that assists in gaining

competitive edge over others.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working capital cycle presents the time which business unit will undertake for converting

the net current assets and liabilities into cash. In this, longer cycle presents that business

organization will have to wait more for generating cash through current assets (Working Capital

Cycle, 2017).

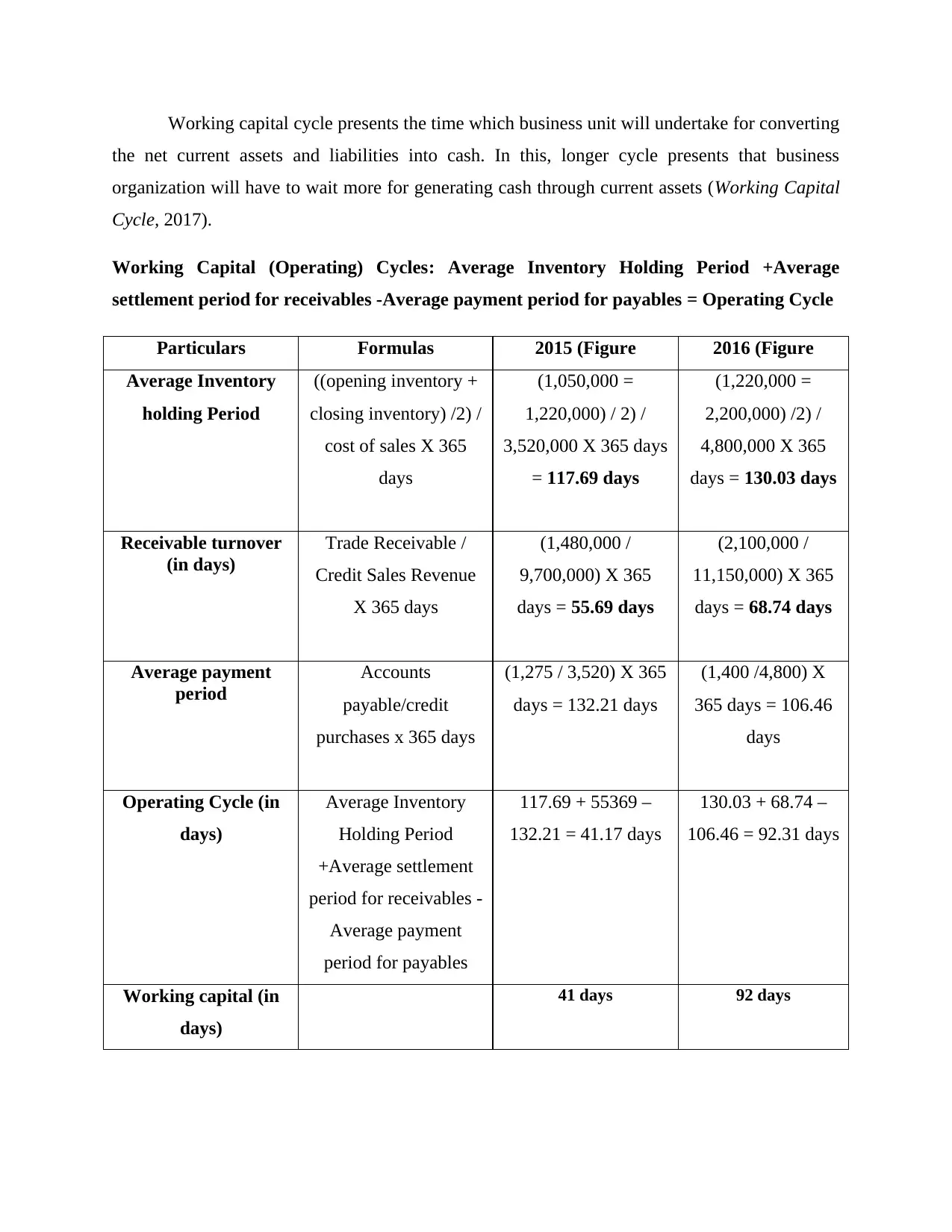

Working Capital (Operating) Cycles: Average Inventory Holding Period +Average

settlement period for receivables -Average payment period for payables = Operating Cycle

Particulars Formulas 2015 (Figure 2016 (Figure

Average Inventory

holding Period

((opening inventory +

closing inventory) /2) /

cost of sales X 365

days

(1,050,000 =

1,220,000) / 2) /

3,520,000 X 365 days

= 117.69 days

(1,220,000 =

2,200,000) /2) /

4,800,000 X 365

days = 130.03 days

Receivable turnover

(in days)

Trade Receivable /

Credit Sales Revenue

X 365 days

(1,480,000 /

9,700,000) X 365

days = 55.69 days

(2,100,000 /

11,150,000) X 365

days = 68.74 days

Average payment

period

Accounts

payable/credit

purchases x 365 days

(1,275 / 3,520) X 365

days = 132.21 days

(1,400 /4,800) X

365 days = 106.46

days

Operating Cycle (in

days)

Average Inventory

Holding Period

+Average settlement

period for receivables -

Average payment

period for payables

117.69 + 55369 –

132.21 = 41.17 days

130.03 + 68.74 –

106.46 = 92.31 days

Working capital (in

days)

41 days 92 days

the net current assets and liabilities into cash. In this, longer cycle presents that business

organization will have to wait more for generating cash through current assets (Working Capital

Cycle, 2017).

Working Capital (Operating) Cycles: Average Inventory Holding Period +Average

settlement period for receivables -Average payment period for payables = Operating Cycle

Particulars Formulas 2015 (Figure 2016 (Figure

Average Inventory

holding Period

((opening inventory +

closing inventory) /2) /

cost of sales X 365

days

(1,050,000 =

1,220,000) / 2) /

3,520,000 X 365 days

= 117.69 days

(1,220,000 =

2,200,000) /2) /

4,800,000 X 365

days = 130.03 days

Receivable turnover

(in days)

Trade Receivable /

Credit Sales Revenue

X 365 days

(1,480,000 /

9,700,000) X 365

days = 55.69 days

(2,100,000 /

11,150,000) X 365

days = 68.74 days

Average payment

period

Accounts

payable/credit

purchases x 365 days

(1,275 / 3,520) X 365

days = 132.21 days

(1,400 /4,800) X

365 days = 106.46

days

Operating Cycle (in

days)

Average Inventory

Holding Period

+Average settlement

period for receivables -

Average payment

period for payables

117.69 + 55369 –

132.21 = 41.17 days

130.03 + 68.74 –

106.46 = 92.31 days

Working capital (in

days)

41 days 92 days

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: By doing analysis, it has been assessed that, working capital days in the

year of 2015 and 2016 accounts for 41 & 92 respectively. Hence, in 2016, working capital days

of Honeywell Plc increased to the significant level. Thus, it can be presented that, in 2016,

company was not in position to convert its working capital into cash within the less time.

However, in 2016, company received money from debtors after more time as compared to 2015.

Further, in the accounting period 2016, business unit was obliged to make payment to creditors

earlier over 2015. Thus, to strengthen the liquidity position or performance Honeywell Plc is

required to revise credit policy pertaining to debtors. Along with this, firm is also needed to

approach the supplier who grants credit for long time or duration. From overall evaluation, it can

be said that liquidity position and performance of Honeywell Plc was not good in 2016. Thus,

business unit should make focus on developing highly strategic and policy framework that

strengthen the liquidity aspect.

PART B

1. Calculating BEP and margin of safety for Thompson Ltd

BEP: From evaluation, it has been identified that in 2014, BEP in sales and units account

for 1050 washing machines & £4020000 significantly. On the other side, in the financial year

2015, BEP level was 11902 units and £5474545.45 respectively. Thus, it can be stated that as per

the selling price and level of fixed cost BEP level is affected to a great extent. Higher BEP in

units are not good because it shows that company will take more time to attain profit.

Margin for safety: Table depicted in appendix clearly shows that margin of safety in the

year of 2014 accounts for 9950 unit & £3980000. In contrast to this, margin of safety was

£3725454.55. Hence, it can be entailed that as per the changes take place in the selling point and

cost level margin of safety is also getting highly influenced.

2. Critically evaluating the key assumptions that are associated with BEP model

Break even point analysis is highly significant which in turn provides high level of

assistance to the firm in determining relationship between cost, volume and profit. Moreover,

such analytical tool entails the point at which business unit will get the situation of no profit and

loss. In other words, it can be stated that BEP analysis helps Thomson Ltd in assessing the units

year of 2015 and 2016 accounts for 41 & 92 respectively. Hence, in 2016, working capital days

of Honeywell Plc increased to the significant level. Thus, it can be presented that, in 2016,

company was not in position to convert its working capital into cash within the less time.

However, in 2016, company received money from debtors after more time as compared to 2015.

Further, in the accounting period 2016, business unit was obliged to make payment to creditors

earlier over 2015. Thus, to strengthen the liquidity position or performance Honeywell Plc is

required to revise credit policy pertaining to debtors. Along with this, firm is also needed to

approach the supplier who grants credit for long time or duration. From overall evaluation, it can

be said that liquidity position and performance of Honeywell Plc was not good in 2016. Thus,

business unit should make focus on developing highly strategic and policy framework that

strengthen the liquidity aspect.

PART B

1. Calculating BEP and margin of safety for Thompson Ltd

BEP: From evaluation, it has been identified that in 2014, BEP in sales and units account

for 1050 washing machines & £4020000 significantly. On the other side, in the financial year

2015, BEP level was 11902 units and £5474545.45 respectively. Thus, it can be stated that as per

the selling price and level of fixed cost BEP level is affected to a great extent. Higher BEP in

units are not good because it shows that company will take more time to attain profit.

Margin for safety: Table depicted in appendix clearly shows that margin of safety in the

year of 2014 accounts for 9950 unit & £3980000. In contrast to this, margin of safety was

£3725454.55. Hence, it can be entailed that as per the changes take place in the selling point and

cost level margin of safety is also getting highly influenced.

2. Critically evaluating the key assumptions that are associated with BEP model

Break even point analysis is highly significant which in turn provides high level of

assistance to the firm in determining relationship between cost, volume and profit. Moreover,

such analytical tool entails the point at which business unit will get the situation of no profit and

loss. In other words, it can be stated that BEP analysis helps Thomson Ltd in assessing the units

of washing machine which they need to offer for recovering all the expenses. BEP analysis is

based on several assumptions such as total costs can be distinguished into two types such as

fixed and variable (Break-Even Analysis: Introduction, Assumptions and Limitations, 2017).

Hence, it completely ignores semi-variable cost which is also one of the main parts of business.

For instance: Electricity expenses are come in the category of semi-variable expenses whose

some part is fixed and other is variable. Further, such method or model assumes that price of the

product is constant. However, on the critical note, it can be said that it is not possible to offer

products to the customers on fix price. Moreover, there are several factors that have direct impact

on the pricing of products or services such as competitor’s strategy, low demand etc (Van der

Stede, 2016). Hence, due to all such aspects it is not possible for Thomson Ltd to follow constant

pricing policy.

Further, BEP model is based on the assumption that volume of sales and production are

equal. It is one of the highly non-realistic approaches because company makes estimation of

production as well as sales on different basis. Besides this, sales level varies as per the changes

take place in the needs, wants and expectation level of customers. Along with this, BEP assumes

that technology is constant and no changes will take place in the efficiency of labour. However,

it is to be critically evaluated that efficiency of labour can be increased through the means of

training & development session (Jung, 2017). Besides this, now technological advancements also

take place with the very high pace. Thus, it can be presented that BEP assumptions are not highly

realistic as per the current business scenario.

Advantages and disadvantages of BEP model are as follows:

Advantages Disadvantages

BEP model assists in measuring profit

or loss on the varied level of production

as well as sales

This model helps in making evaluation

of the effects when changes take place

in selling price.

Business unit can determine suitable

relationship between fixed and variable

Time consuming process

It assumes that variables like

technology, cost, production and sales

are constant which is unrealistic.

It is applicable or suitable only for

single products rather than multiple. ‘

Due to having unrealistic assumptions

it can be served as a planning aid rather

based on several assumptions such as total costs can be distinguished into two types such as

fixed and variable (Break-Even Analysis: Introduction, Assumptions and Limitations, 2017).

Hence, it completely ignores semi-variable cost which is also one of the main parts of business.

For instance: Electricity expenses are come in the category of semi-variable expenses whose

some part is fixed and other is variable. Further, such method or model assumes that price of the

product is constant. However, on the critical note, it can be said that it is not possible to offer

products to the customers on fix price. Moreover, there are several factors that have direct impact

on the pricing of products or services such as competitor’s strategy, low demand etc (Van der

Stede, 2016). Hence, due to all such aspects it is not possible for Thomson Ltd to follow constant

pricing policy.

Further, BEP model is based on the assumption that volume of sales and production are

equal. It is one of the highly non-realistic approaches because company makes estimation of

production as well as sales on different basis. Besides this, sales level varies as per the changes

take place in the needs, wants and expectation level of customers. Along with this, BEP assumes

that technology is constant and no changes will take place in the efficiency of labour. However,

it is to be critically evaluated that efficiency of labour can be increased through the means of

training & development session (Jung, 2017). Besides this, now technological advancements also

take place with the very high pace. Thus, it can be presented that BEP assumptions are not highly

realistic as per the current business scenario.

Advantages and disadvantages of BEP model are as follows:

Advantages Disadvantages

BEP model assists in measuring profit

or loss on the varied level of production

as well as sales

This model helps in making evaluation

of the effects when changes take place

in selling price.

Business unit can determine suitable

relationship between fixed and variable

Time consuming process

It assumes that variables like

technology, cost, production and sales

are constant which is unrealistic.

It is applicable or suitable only for

single products rather than multiple. ‘

Due to having unrealistic assumptions

it can be served as a planning aid rather

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.