Finance in Hospitality: Financial Analysis and Management Decisions

VerifiedAdded on 2020/02/14

|18

|5436

|147

Report

AI Summary

This report provides a comprehensive overview of financial management within the hospitality industry. It begins by exploring various funding sources available to businesses, both internal and external, along with methods to increase income for large restaurant chains. The report then delves into cost elements, gross profit calculations, and selling price determination. It covers inventory and cash control methods, emphasizing the importance of budgetary control, variance analysis, and the decision-making process based on financial data. The report includes a discussion on trial balance, necessary adjustments for profit and loss, and balance sheet, ratio analysis, and recommendations for improving business performance. Finally, the report examines cost behavior (fixed, variable, and semi-variable costs), contribution margin, cost-volume-profit relationships, and the use of break-even analysis to justify short-term management decisions. References are included to support the information provided.

FINANCE IN

HOSPITALITY

HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Funding sources available to business and service industries...................................1

AC 1.2 Contribution made by various methods of generating income for the large chain...2

Restaurant..............................................................................................................................2

TASK 2......................................................................................................................................3

AC 2.1 Elements of cost, gross profit percentage and selling prices....................................3

AC 2.2 Controlling business cash and inventory..................................................................4

TASK 3 .....................................................................................................................................5

AC 3.3 Process and purpose of budgetary control................................................................5

AC 3.4 Variance analysis and appropriate future management decisions............................6

TASK 4......................................................................................................................................7

AC 3.1 Source and structure of trial balance.........................................................................7

AC 3.2 Necessary adjustments to the profit and loss account and balance sheet of R. Riggs

...............................................................................................................................................8

AC 4.1 calculation of ratios for R. Riggs..............................................................................9

AC 4.2 Take necessary decisions to improve the business performance............................10

TASK 5....................................................................................................................................10

AC 5.1 Fixed, variable and semi-variable cost....................................................................10

AC 5.2 calculation of contribution and cost volume profit relationship.............................11

AC 5.3 Justify short term management decisions based on profit/loss potential and break

even......................................................................................................................................12

calculations..........................................................................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Funding sources available to business and service industries...................................1

AC 1.2 Contribution made by various methods of generating income for the large chain...2

Restaurant..............................................................................................................................2

TASK 2......................................................................................................................................3

AC 2.1 Elements of cost, gross profit percentage and selling prices....................................3

AC 2.2 Controlling business cash and inventory..................................................................4

TASK 3 .....................................................................................................................................5

AC 3.3 Process and purpose of budgetary control................................................................5

AC 3.4 Variance analysis and appropriate future management decisions............................6

TASK 4......................................................................................................................................7

AC 3.1 Source and structure of trial balance.........................................................................7

AC 3.2 Necessary adjustments to the profit and loss account and balance sheet of R. Riggs

...............................................................................................................................................8

AC 4.1 calculation of ratios for R. Riggs..............................................................................9

AC 4.2 Take necessary decisions to improve the business performance............................10

TASK 5....................................................................................................................................10

AC 5.1 Fixed, variable and semi-variable cost....................................................................10

AC 5.2 calculation of contribution and cost volume profit relationship.............................11

AC 5.3 Justify short term management decisions based on profit/loss potential and break

even......................................................................................................................................12

calculations..........................................................................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION

Finance is the life blood of every business and service organisation. Successful

business operations depend upon the availability of adequate funds. These sources are

classified into two broad categories that are internal and external sources. Internal sources are

available inside the corporations while external sources are available outside the organization.

Present project report will help us in identifying the type of various sources through which

funds can be generated. Moreover, the report will help us in determining different elements of

business cost, gross profit and selling prices as well. In addition to it, every organization

needs to maintain their inventory and cash availability in order to ensure smooth functioning

of their operations. Furthermore, the report will focus in analysing the business financial

performance through the company’s financial statements.

TASK 1

AC 1.1 Funding sources available to business and service industries

The given scenario depicts that a sole trader business organization desire to purchase

some new machinery costing 50000£. Therefore, he needs to collect the funds from possible

sources which include minimum cost to him. The sources are described below:

Internal finance sources: Every organization has certain amount of funds available

in the organization which is termed as internal finance sources, explained as below:

Ploughing back of profits: One of the most important and regular type of finance is

retained earnings. Businesses earn profits from their operating functions and they do not

distribute all of the profits among the shareholders. Therefore, the undistributed profits of the

business are known as retained earnings (Bernstein, 2015). Thus, it can be said that through

ploughing back of business profits, organizations will be able to fulfil their financial

requirements.

Personal savings: Owners can invest their personal savings in the business to

accomplish their finance need. The benefit of that source is that it will be available at

cheaper rates and helps to reduce debt funds to a great extent.

Squeezing cash: Another important source of finance is cash squeezing operations.

Business organization can make policies to receive their debts earlier and negotiate payment

to creditors. By doing this, organizations will be able to have greater availability of funds in

the business. This in turn, helps to mitigate the financial need of the business.

1 | P a g e

Finance is the life blood of every business and service organisation. Successful

business operations depend upon the availability of adequate funds. These sources are

classified into two broad categories that are internal and external sources. Internal sources are

available inside the corporations while external sources are available outside the organization.

Present project report will help us in identifying the type of various sources through which

funds can be generated. Moreover, the report will help us in determining different elements of

business cost, gross profit and selling prices as well. In addition to it, every organization

needs to maintain their inventory and cash availability in order to ensure smooth functioning

of their operations. Furthermore, the report will focus in analysing the business financial

performance through the company’s financial statements.

TASK 1

AC 1.1 Funding sources available to business and service industries

The given scenario depicts that a sole trader business organization desire to purchase

some new machinery costing 50000£. Therefore, he needs to collect the funds from possible

sources which include minimum cost to him. The sources are described below:

Internal finance sources: Every organization has certain amount of funds available

in the organization which is termed as internal finance sources, explained as below:

Ploughing back of profits: One of the most important and regular type of finance is

retained earnings. Businesses earn profits from their operating functions and they do not

distribute all of the profits among the shareholders. Therefore, the undistributed profits of the

business are known as retained earnings (Bernstein, 2015). Thus, it can be said that through

ploughing back of business profits, organizations will be able to fulfil their financial

requirements.

Personal savings: Owners can invest their personal savings in the business to

accomplish their finance need. The benefit of that source is that it will be available at

cheaper rates and helps to reduce debt funds to a great extent.

Squeezing cash: Another important source of finance is cash squeezing operations.

Business organization can make policies to receive their debts earlier and negotiate payment

to creditors. By doing this, organizations will be able to have greater availability of funds in

the business. This in turn, helps to mitigate the financial need of the business.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sale of assets: Assets which are not used for productive purpose can be resale at the

market place. This in turn generates greater availability of funds for the organization and

fulfils their financial need.

External finance sources: This type of finance sources are available outside the

organization, explained here as under:

Issuing shares: There are two types of shares that are; ordinary shares and preference

shares. Ordinary shares represent the ownership on business. However, preference shares

have two kind of preference over the equity share for repayment of capital and dividend

(Fraser, Bhaumik and Wright, 2015). Business organizations can issue both the type of shares

in the market to receive appropriate funds.

Bank loans: Bank loans represent the debt capital to business. Business organizations

can take bank loans through providing collateral security. Further, before providing loans to

the businesses, bank analyse the business solvency position to receive interest income with

the fixed amount and on right time (Van Auken, 2015). Business organization can get loans

from banks and other financial institution at implied interest rates.

Debentures: It is a debt acknowledgement through which debenture holders have

right to get fixed interest incomes at a fixed interval of time (External finance debt and

foreign direct investment, n.d.). Through issuing debentures in the market, both the

organizations will be able to satisfy their long term funds requirement.

Grants and subsidy: In every country, government provide grants and subsidies with

the intention of providing help to the organizations. The objective of the government grants

and subsidies are to make economic development and growth through making industrial

growth.

Overdraft facility: It is a great solution to fulfil short term financial needs of the

business. In every country, bank provides this facility to withdraw higher the amount from

the available account balance (Kregal, 2004). The facility is provided at a higher the interest

rates comparatively than interest rates on bank loans. Furthermore, bank provides the

overdraft facility up to a certain limit.

AC 1.2 Contribution made by various methods of generating income for the large chain

Restaurant

Increasing the revenues leads to enhance the contribution to the business. There are

number of methods available for large chain restaurant businesses to get higher income,

which are described as below:

2 | P a g e

market place. This in turn generates greater availability of funds for the organization and

fulfils their financial need.

External finance sources: This type of finance sources are available outside the

organization, explained here as under:

Issuing shares: There are two types of shares that are; ordinary shares and preference

shares. Ordinary shares represent the ownership on business. However, preference shares

have two kind of preference over the equity share for repayment of capital and dividend

(Fraser, Bhaumik and Wright, 2015). Business organizations can issue both the type of shares

in the market to receive appropriate funds.

Bank loans: Bank loans represent the debt capital to business. Business organizations

can take bank loans through providing collateral security. Further, before providing loans to

the businesses, bank analyse the business solvency position to receive interest income with

the fixed amount and on right time (Van Auken, 2015). Business organization can get loans

from banks and other financial institution at implied interest rates.

Debentures: It is a debt acknowledgement through which debenture holders have

right to get fixed interest incomes at a fixed interval of time (External finance debt and

foreign direct investment, n.d.). Through issuing debentures in the market, both the

organizations will be able to satisfy their long term funds requirement.

Grants and subsidy: In every country, government provide grants and subsidies with

the intention of providing help to the organizations. The objective of the government grants

and subsidies are to make economic development and growth through making industrial

growth.

Overdraft facility: It is a great solution to fulfil short term financial needs of the

business. In every country, bank provides this facility to withdraw higher the amount from

the available account balance (Kregal, 2004). The facility is provided at a higher the interest

rates comparatively than interest rates on bank loans. Furthermore, bank provides the

overdraft facility up to a certain limit.

AC 1.2 Contribution made by various methods of generating income for the large chain

Restaurant

Increasing the revenues leads to enhance the contribution to the business. There are

number of methods available for large chain restaurant businesses to get higher income,

which are described as below:

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Increasing total sales: Restaurant organization serves variety of foods to the

customers for their satisfaction. Therefore, increasing the business revenues will greatly

contributes to increase their business income. It can be done by increasing the number of

customers and customer loyalty. Through providing qualified customer services at affordable

prices, restaurant can enhance their customers to a great extent (Jiang and Galm, 2014). This

in turn enables them to generate higher incomes and contribution as well.

Opening new Branches: Restaurant chain can start their new branches in different

markets to grab larger market share. This in turn, helps to enhance their business income,

contribution and profits.

Franchise: Franchise is the right method of using business brand name of other

company for a defined time period. Large restaurant chains have well known position in the

market. Therefore, they can generate increased income by providing their business franchise

to others.

Effective marketing: Worst business marketing will not help to enhance the restaurant

sales. Therefore, by making plans for effective marketing such as social media outreaching

through facebook and twitter helps to enhance total business sales (Kwok and et. al., 2015).

Further, it can be done by designing creative menus. This in turn, restaurant incomes and

profits will be increase.

Increase the prices: Prices are the charges of customer services. Large chain

restaurant can increase the service prices which help to get high level of income. It is the

most effective way when the restaurant is well known for the services and its taste of food.

Infrastructure: Through building innovative infrastructure, restaurants will be able to

attract large number of customers (Amit and Zott, 2012). Moreover, by providing various

facilities such as Wi-Fi service, companies can generate larger incomes from operations.

TASK 2

AC 2.1 Elements of cost, gross profit percentage and selling prices

Elements of cost: As stated scenario, Marks and Spencer is Europe's largest retailer

company that has global brand and recognition in the market. The elements of cost can be

major classified into two categories that are as follows:

Direct cost: The expenditures that are directly related to the volume of production are

known as direct cost. It includes material, labour and other direct overheads. Every

organization incurred these expenses for manufacturing purpose. Material is the raw products

while labour are the persons who convert the raw material into finished goods. Moreover,

3 | P a g e

customers for their satisfaction. Therefore, increasing the business revenues will greatly

contributes to increase their business income. It can be done by increasing the number of

customers and customer loyalty. Through providing qualified customer services at affordable

prices, restaurant can enhance their customers to a great extent (Jiang and Galm, 2014). This

in turn enables them to generate higher incomes and contribution as well.

Opening new Branches: Restaurant chain can start their new branches in different

markets to grab larger market share. This in turn, helps to enhance their business income,

contribution and profits.

Franchise: Franchise is the right method of using business brand name of other

company for a defined time period. Large restaurant chains have well known position in the

market. Therefore, they can generate increased income by providing their business franchise

to others.

Effective marketing: Worst business marketing will not help to enhance the restaurant

sales. Therefore, by making plans for effective marketing such as social media outreaching

through facebook and twitter helps to enhance total business sales (Kwok and et. al., 2015).

Further, it can be done by designing creative menus. This in turn, restaurant incomes and

profits will be increase.

Increase the prices: Prices are the charges of customer services. Large chain

restaurant can increase the service prices which help to get high level of income. It is the

most effective way when the restaurant is well known for the services and its taste of food.

Infrastructure: Through building innovative infrastructure, restaurants will be able to

attract large number of customers (Amit and Zott, 2012). Moreover, by providing various

facilities such as Wi-Fi service, companies can generate larger incomes from operations.

TASK 2

AC 2.1 Elements of cost, gross profit percentage and selling prices

Elements of cost: As stated scenario, Marks and Spencer is Europe's largest retailer

company that has global brand and recognition in the market. The elements of cost can be

major classified into two categories that are as follows:

Direct cost: The expenditures that are directly related to the volume of production are

known as direct cost. It includes material, labour and other direct overheads. Every

organization incurred these expenses for manufacturing purpose. Material is the raw products

while labour are the persons who convert the raw material into finished goods. Moreover,

3 | P a g e

overhead includes all the direct overheads such as production expenses (Holguín-Veras,

2013). According to the scenario, the direct costs are carrier bags, food wastes and staffing

costs.

Indirect cost: Indirect business expenditures are not related to the production activities

hence are termed as indirect cost. It includes overheads such as stationery; telephone bills,

electricity bill, non productive expenses, security charges, rent and rates and assets

depreciation (Lewis, 2013). The scenario includes stationery, telephone expenses, security

and electricity under the indirect cost.

Elements of gross profit percentage: On dividing the total gross profit to the total

business sales, gross profit margin can be found out. However, the gross profit is the excess

of total business sales over the total of direct cost. Therefore, it can be said that it includes the

elements of gross profit, sales and direct business cost. Higher the sales will leads to higher

profits and gross profit margin as well. On contrary, increasing the production cost at fixed

sales leads to decrease the amount of gross profit and gross profit percentage also.

Elements of selling prices: Unit cost and mark up percentage are the two elements that

decide the selling prices. Higher cost and mark up percentage deals with the increase in

selling prices and vice versa (Bebbington and Thomson, 2013).

AC 2.2 Controlling business cash and inventory

There are number of ways that are available to control business inventory that are

listed as below:

Inventory controlling:

Just in time: According to this method, inventory must be ordered at the time of its

need. The aim of the method is to reduce overtrading consequences (Schwarz, 2008). The

method says that overtrading will enhance the unnecessary cost of the business. Therefore,

order must be placed at the time when the requirement of inventory arises. The condition of

the method is that businesses must be confident that inventory will be delivered by the

supplier when they demanded.

Economic order quantity: It is the method of controlling inventory by reducing both

the holding and ordering cost. The method says that having too much inventory will

contributes to the increase in cost. However, in case where inventories are managed at lower

level, the business will not be able to satisfy the customer’s demand (Zinn and Charnes,

2005). Therefore, according to this method, ordering units must be determined by dividing

4 | P a g e

2013). According to the scenario, the direct costs are carrier bags, food wastes and staffing

costs.

Indirect cost: Indirect business expenditures are not related to the production activities

hence are termed as indirect cost. It includes overheads such as stationery; telephone bills,

electricity bill, non productive expenses, security charges, rent and rates and assets

depreciation (Lewis, 2013). The scenario includes stationery, telephone expenses, security

and electricity under the indirect cost.

Elements of gross profit percentage: On dividing the total gross profit to the total

business sales, gross profit margin can be found out. However, the gross profit is the excess

of total business sales over the total of direct cost. Therefore, it can be said that it includes the

elements of gross profit, sales and direct business cost. Higher the sales will leads to higher

profits and gross profit margin as well. On contrary, increasing the production cost at fixed

sales leads to decrease the amount of gross profit and gross profit percentage also.

Elements of selling prices: Unit cost and mark up percentage are the two elements that

decide the selling prices. Higher cost and mark up percentage deals with the increase in

selling prices and vice versa (Bebbington and Thomson, 2013).

AC 2.2 Controlling business cash and inventory

There are number of ways that are available to control business inventory that are

listed as below:

Inventory controlling:

Just in time: According to this method, inventory must be ordered at the time of its

need. The aim of the method is to reduce overtrading consequences (Schwarz, 2008). The

method says that overtrading will enhance the unnecessary cost of the business. Therefore,

order must be placed at the time when the requirement of inventory arises. The condition of

the method is that businesses must be confident that inventory will be delivered by the

supplier when they demanded.

Economic order quantity: It is the method of controlling inventory by reducing both

the holding and ordering cost. The method says that having too much inventory will

contributes to the increase in cost. However, in case where inventories are managed at lower

level, the business will not be able to satisfy the customer’s demand (Zinn and Charnes,

2005). Therefore, according to this method, ordering units must be determined by dividing

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the product of twice of annual production and ordering cost per order to carrying cost per

unit.

LIFO and FIFO: According to LIFO, last inventory receipts must be delivered

initially. Therefore, ending inventory represent the initial inventory receipts. However, FIFO

method indicates that first inventory receipts must be delivered initially and so on. Therefore,

ending inventory balance represents the closing inventory receipts.

Methods of controlling business cash:

Preparing cash budget is the most effective way of controlling cash in the business. It

helps to identify cash incomes and allocate it in different operating functions in an effective

way. Moreover, maintaining effective internal control also helps to reduce the unnecessary

cash expenses. Cash can be safeguarded by checking all the transactions from the authorised

evidences. It also helps to detect fraud that has been taken place in the organization.

Segregation of duties also can be done for managing the business cash. Moreover, cash can

be controlled by making policies in regards to authorisation of the cash receipts and payments

by the management (Whitecotton, Libby and Phillips, 2013). Further, proper documentation

also helps to identify the reality of cash transaction that is reported in the financial statements.

TASK 3

AC 3.3 Process and purpose of budgetary control

Purpose: Budgtary control is the process to forecasting future probable incomes and

expenditures from the business operations. It mainly aims at identifying variances and takes

corrective actions in order to eliminate the deviations and meet the targets effectively.

Moreover, it aims at controlling business expenses and generating higher the level of incomes

from the operating functions (Heinle, Ross and Saouma, 2013.). By making budget, cost can

be controlled to a great extent. Furthermore, the process helps to monitor business

performance and provides a financial framework that helps to take effective managerial

decisions.

Budgetary process: The process involves four steps that are explained here as follows:

Estimate the incomes and expenses: At Initial stage, managers have to ascertain the

revenues and expenditures that can be incur in the future period (DRURY, 2013). Managers

estimate incomes from sales and other operative functions. However, business expenses

include salary and wages, purchase, rent, and other kind of operating as well as capital

expenditures.

5 | P a g e

unit.

LIFO and FIFO: According to LIFO, last inventory receipts must be delivered

initially. Therefore, ending inventory represent the initial inventory receipts. However, FIFO

method indicates that first inventory receipts must be delivered initially and so on. Therefore,

ending inventory balance represents the closing inventory receipts.

Methods of controlling business cash:

Preparing cash budget is the most effective way of controlling cash in the business. It

helps to identify cash incomes and allocate it in different operating functions in an effective

way. Moreover, maintaining effective internal control also helps to reduce the unnecessary

cash expenses. Cash can be safeguarded by checking all the transactions from the authorised

evidences. It also helps to detect fraud that has been taken place in the organization.

Segregation of duties also can be done for managing the business cash. Moreover, cash can

be controlled by making policies in regards to authorisation of the cash receipts and payments

by the management (Whitecotton, Libby and Phillips, 2013). Further, proper documentation

also helps to identify the reality of cash transaction that is reported in the financial statements.

TASK 3

AC 3.3 Process and purpose of budgetary control

Purpose: Budgtary control is the process to forecasting future probable incomes and

expenditures from the business operations. It mainly aims at identifying variances and takes

corrective actions in order to eliminate the deviations and meet the targets effectively.

Moreover, it aims at controlling business expenses and generating higher the level of incomes

from the operating functions (Heinle, Ross and Saouma, 2013.). By making budget, cost can

be controlled to a great extent. Furthermore, the process helps to monitor business

performance and provides a financial framework that helps to take effective managerial

decisions.

Budgetary process: The process involves four steps that are explained here as follows:

Estimate the incomes and expenses: At Initial stage, managers have to ascertain the

revenues and expenditures that can be incur in the future period (DRURY, 2013). Managers

estimate incomes from sales and other operative functions. However, business expenses

include salary and wages, purchase, rent, and other kind of operating as well as capital

expenditures.

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Identifying actual business performance: After deciding the budgeted incomes and

expenditures, actual business performance must be analyse. Mangers have to determine the

actual incomes and expenses that had been incurred.

Identifying variances: Variance can be ascertained through comparing budgeted and

actual results (York, 2012). There are two kinds of variances that are favourable and adverse.

Higher the actual incomes and lower the actual expenses indicate favourable balance and vice

versa.

Corrective actions: At this stage, managers have to take necessary step and make

decisions that help to mitigate negative variances. This in turn, they can meet the set or

decided business targets.

AC 3.4 Variance analysis and appropriate future management decisions

The scenario indicates budgeted and accrual data for 25000 units. Therefore variances

can be calculated here as under:

Particular Budgeted Actual Variance (budgeted -actual)

Sales units 100000 75000 25000

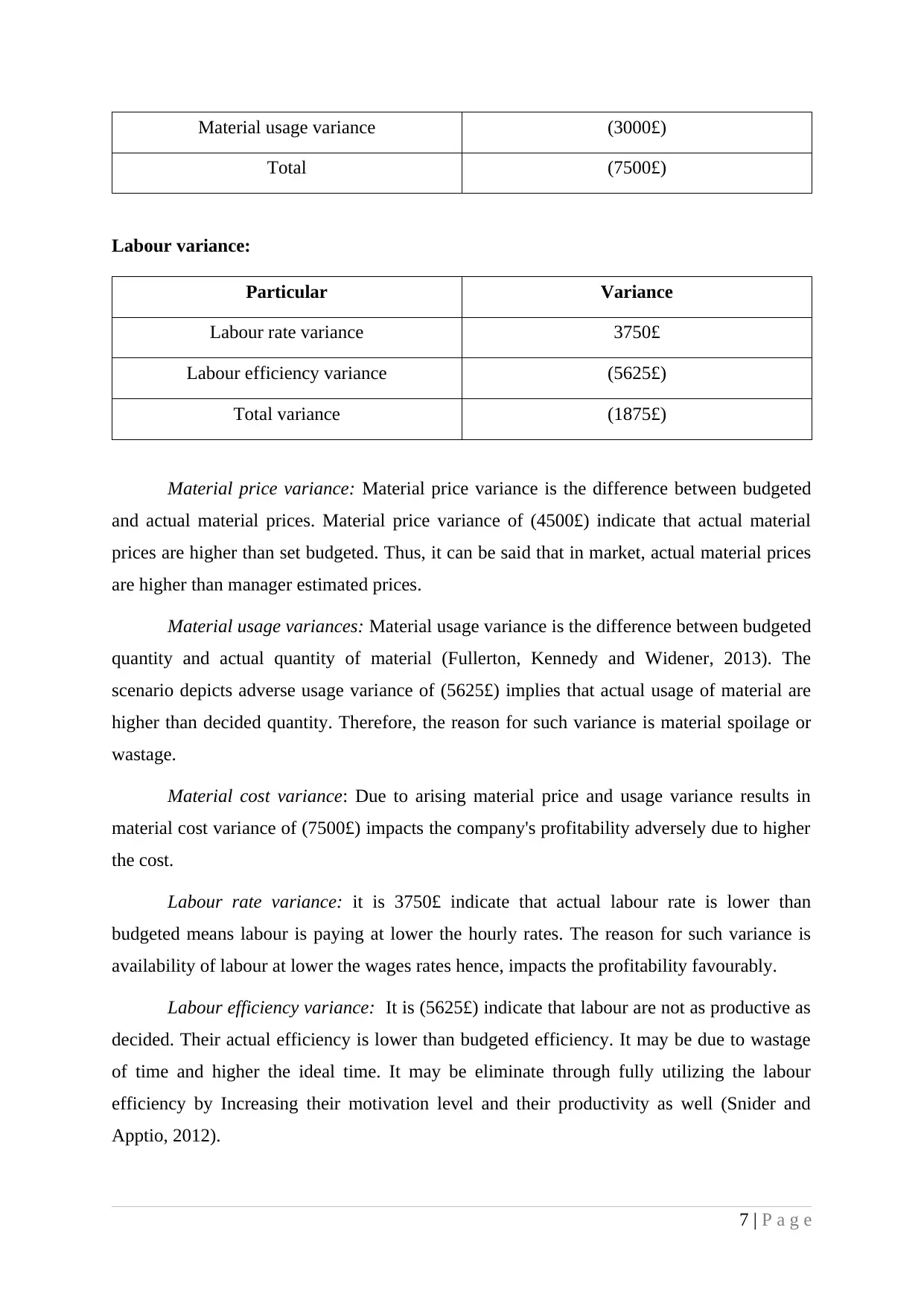

Material 15000£ 22500£ (7500£)

Labour 22500£ 24375£ (1875£)

Sales unit variance: Manager decided budgeted sales for 100000 units however;

actual sales have been made for only 75000 units respectively. Therefore, total business sales

and profitability will be reduced.

Moreover, the scenario depicts that material variance is the result of material price

variance and material usage variance. According to the scenario material price variance and

usage variance are (4500£) and (3000£) respectively. However, total labour variances are the

result of labour rate variance and labour efficiency variance. The scenario represents labour

rate variance arises for amounted to 3750£ while labour efficiency variance arises for

(5625£).

Material Variance:

Particular Variance

Material price variances (4500£)

6 | P a g e

expenditures, actual business performance must be analyse. Mangers have to determine the

actual incomes and expenses that had been incurred.

Identifying variances: Variance can be ascertained through comparing budgeted and

actual results (York, 2012). There are two kinds of variances that are favourable and adverse.

Higher the actual incomes and lower the actual expenses indicate favourable balance and vice

versa.

Corrective actions: At this stage, managers have to take necessary step and make

decisions that help to mitigate negative variances. This in turn, they can meet the set or

decided business targets.

AC 3.4 Variance analysis and appropriate future management decisions

The scenario indicates budgeted and accrual data for 25000 units. Therefore variances

can be calculated here as under:

Particular Budgeted Actual Variance (budgeted -actual)

Sales units 100000 75000 25000

Material 15000£ 22500£ (7500£)

Labour 22500£ 24375£ (1875£)

Sales unit variance: Manager decided budgeted sales for 100000 units however;

actual sales have been made for only 75000 units respectively. Therefore, total business sales

and profitability will be reduced.

Moreover, the scenario depicts that material variance is the result of material price

variance and material usage variance. According to the scenario material price variance and

usage variance are (4500£) and (3000£) respectively. However, total labour variances are the

result of labour rate variance and labour efficiency variance. The scenario represents labour

rate variance arises for amounted to 3750£ while labour efficiency variance arises for

(5625£).

Material Variance:

Particular Variance

Material price variances (4500£)

6 | P a g e

Material usage variance (3000£)

Total (7500£)

Labour variance:

Particular Variance

Labour rate variance 3750£

Labour efficiency variance (5625£)

Total variance (1875£)

Material price variance: Material price variance is the difference between budgeted

and actual material prices. Material price variance of (4500£) indicate that actual material

prices are higher than set budgeted. Thus, it can be said that in market, actual material prices

are higher than manager estimated prices.

Material usage variances: Material usage variance is the difference between budgeted

quantity and actual quantity of material (Fullerton, Kennedy and Widener, 2013). The

scenario depicts adverse usage variance of (5625£) implies that actual usage of material are

higher than decided quantity. Therefore, the reason for such variance is material spoilage or

wastage.

Material cost variance: Due to arising material price and usage variance results in

material cost variance of (7500£) impacts the company's profitability adversely due to higher

the cost.

Labour rate variance: it is 3750£ indicate that actual labour rate is lower than

budgeted means labour is paying at lower the hourly rates. The reason for such variance is

availability of labour at lower the wages rates hence, impacts the profitability favourably.

Labour efficiency variance: It is (5625£) indicate that labour are not as productive as

decided. Their actual efficiency is lower than budgeted efficiency. It may be due to wastage

of time and higher the ideal time. It may be eliminate through fully utilizing the labour

efficiency by Increasing their motivation level and their productivity as well (Snider and

Apptio, 2012).

7 | P a g e

Total (7500£)

Labour variance:

Particular Variance

Labour rate variance 3750£

Labour efficiency variance (5625£)

Total variance (1875£)

Material price variance: Material price variance is the difference between budgeted

and actual material prices. Material price variance of (4500£) indicate that actual material

prices are higher than set budgeted. Thus, it can be said that in market, actual material prices

are higher than manager estimated prices.

Material usage variances: Material usage variance is the difference between budgeted

quantity and actual quantity of material (Fullerton, Kennedy and Widener, 2013). The

scenario depicts adverse usage variance of (5625£) implies that actual usage of material are

higher than decided quantity. Therefore, the reason for such variance is material spoilage or

wastage.

Material cost variance: Due to arising material price and usage variance results in

material cost variance of (7500£) impacts the company's profitability adversely due to higher

the cost.

Labour rate variance: it is 3750£ indicate that actual labour rate is lower than

budgeted means labour is paying at lower the hourly rates. The reason for such variance is

availability of labour at lower the wages rates hence, impacts the profitability favourably.

Labour efficiency variance: It is (5625£) indicate that labour are not as productive as

decided. Their actual efficiency is lower than budgeted efficiency. It may be due to wastage

of time and higher the ideal time. It may be eliminate through fully utilizing the labour

efficiency by Increasing their motivation level and their productivity as well (Snider and

Apptio, 2012).

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Labour cost variance: Labour cost variance arises due to arising the labour rate and

labour usage variance. The adverse balance of 1875£ impacts the business profits in a

negative direction.

TASK 4

AC 3.1 Source and structure of trial balance

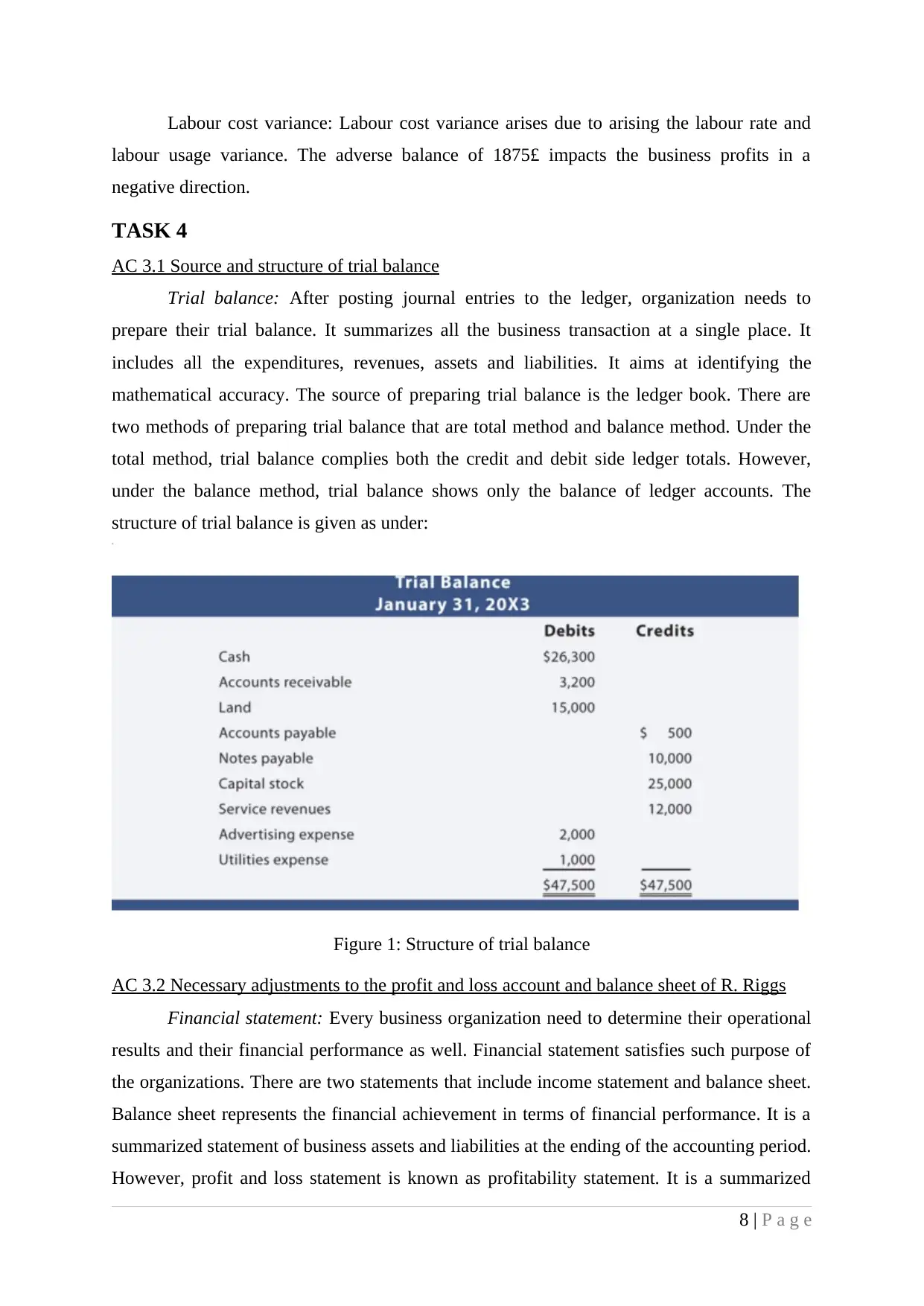

Trial balance: After posting journal entries to the ledger, organization needs to

prepare their trial balance. It summarizes all the business transaction at a single place. It

includes all the expenditures, revenues, assets and liabilities. It aims at identifying the

mathematical accuracy. The source of preparing trial balance is the ledger book. There are

two methods of preparing trial balance that are total method and balance method. Under the

total method, trial balance complies both the credit and debit side ledger totals. However,

under the balance method, trial balance shows only the balance of ledger accounts. The

structure of trial balance is given as under:

Figure 1: Structure of trial balance

AC 3.2 Necessary adjustments to the profit and loss account and balance sheet of R. Riggs

Financial statement: Every business organization need to determine their operational

results and their financial performance as well. Financial statement satisfies such purpose of

the organizations. There are two statements that include income statement and balance sheet.

Balance sheet represents the financial achievement in terms of financial performance. It is a

summarized statement of business assets and liabilities at the ending of the accounting period.

However, profit and loss statement is known as profitability statement. It is a summarized

8 | P a g e

labour usage variance. The adverse balance of 1875£ impacts the business profits in a

negative direction.

TASK 4

AC 3.1 Source and structure of trial balance

Trial balance: After posting journal entries to the ledger, organization needs to

prepare their trial balance. It summarizes all the business transaction at a single place. It

includes all the expenditures, revenues, assets and liabilities. It aims at identifying the

mathematical accuracy. The source of preparing trial balance is the ledger book. There are

two methods of preparing trial balance that are total method and balance method. Under the

total method, trial balance complies both the credit and debit side ledger totals. However,

under the balance method, trial balance shows only the balance of ledger accounts. The

structure of trial balance is given as under:

Figure 1: Structure of trial balance

AC 3.2 Necessary adjustments to the profit and loss account and balance sheet of R. Riggs

Financial statement: Every business organization need to determine their operational

results and their financial performance as well. Financial statement satisfies such purpose of

the organizations. There are two statements that include income statement and balance sheet.

Balance sheet represents the financial achievement in terms of financial performance. It is a

summarized statement of business assets and liabilities at the ending of the accounting period.

However, profit and loss statement is known as profitability statement. It is a summarized

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

account of business payments and receipts for a fixed period. The excess of incomes over the

expenditures are known as business profits and vice versa.

Date Particular L.F. Debit Credit

March, 3

2012

Furniture a/c Dr.

To Bank a/c

(Additional furniture worth 525£

has been purchased)

525

525

December, 30

2012

Bank a/c Dr.

To Interest receive

( Business receive interest on

their bank deposits)

50

50

June, 4

2012

Accrued expenses a/c Dr.

To Bank a/c

200

200

Total 775 775

Table 1: Profitability statement of R. Riggs

Total sales 157165

Cost of goods sold 94520

Gross profit 62645

Discount received 160

Interest received 50

Total incomes 62855

Wages and salaries 31740

Rent 3170

Discount allowed 820

Van running cost 687

Bad debts 730

Doubtful debt provisions 91

Depreciation 1630

Accrued expenses 200

Total operating expenses 39068

Net profit 23787

9 | P a g e

expenditures are known as business profits and vice versa.

Date Particular L.F. Debit Credit

March, 3

2012

Furniture a/c Dr.

To Bank a/c

(Additional furniture worth 525£

has been purchased)

525

525

December, 30

2012

Bank a/c Dr.

To Interest receive

( Business receive interest on

their bank deposits)

50

50

June, 4

2012

Accrued expenses a/c Dr.

To Bank a/c

200

200

Total 775 775

Table 1: Profitability statement of R. Riggs

Total sales 157165

Cost of goods sold 94520

Gross profit 62645

Discount received 160

Interest received 50

Total incomes 62855

Wages and salaries 31740

Rent 3170

Discount allowed 820

Van running cost 687

Bad debts 730

Doubtful debt provisions 91

Depreciation 1630

Accrued expenses 200

Total operating expenses 39068

Net profit 23787

9 | P a g e

Table 2: Balance sheet of R. Riggs

Fixed cost

Office furniture and Van (6650+525) 7175

Less: depreciation 1630

Net fixed assets 5545

Current assets

Stock 2400

Debtors 12316

Less: Provision for doubtful debts 496

Net debtors 11820

Prepaid expenses 230

Cash at bank and hand (4424-525+50-200) 4274

Total current assets 18724

Total assets 24269

Current liabilities

Creditors 5770

Accruals 412

Total current liability 6182

Finance by capital 11400

Net profit 23787

less drawings 17100

Total finance made by capital 18087

Total liabilities 24269

AC 4.1 calculation of ratios for R. Riggs

Ratio Formula Calculation Answer

Gross profit ratio (Gross

profit)/(Revenue)*100

(62645£)/(157165£)*100 39.86%

Net profit ratio (Net profit)/(revenue)*100 (23787£)/(157165£)*100 15.13%

Current ratio (Current assets)/(Current

liability)

(18724£)/(6182£) 3.03

Acid test ratio (Current (18724£-2400£)/(6182£) 2.64

10 | P a g e

Fixed cost

Office furniture and Van (6650+525) 7175

Less: depreciation 1630

Net fixed assets 5545

Current assets

Stock 2400

Debtors 12316

Less: Provision for doubtful debts 496

Net debtors 11820

Prepaid expenses 230

Cash at bank and hand (4424-525+50-200) 4274

Total current assets 18724

Total assets 24269

Current liabilities

Creditors 5770

Accruals 412

Total current liability 6182

Finance by capital 11400

Net profit 23787

less drawings 17100

Total finance made by capital 18087

Total liabilities 24269

AC 4.1 calculation of ratios for R. Riggs

Ratio Formula Calculation Answer

Gross profit ratio (Gross

profit)/(Revenue)*100

(62645£)/(157165£)*100 39.86%

Net profit ratio (Net profit)/(revenue)*100 (23787£)/(157165£)*100 15.13%

Current ratio (Current assets)/(Current

liability)

(18724£)/(6182£) 3.03

Acid test ratio (Current (18724£-2400£)/(6182£) 2.64

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.