Financial Analysis in the Hospitality Industry: Saba Hotel Report

VerifiedAdded on 2020/06/06

|16

|4692

|28

Report

AI Summary

This report provides a comprehensive analysis of finance within the hospitality industry, utilizing Saba Hotel London as a case study. It delves into various aspects of financial management, including the identification of funding sources such as equity and debt financing, and the generation of income through sales, commissions, and other avenues. The report examines cost elements like direct materials and labor, along with pricing strategies and methods for controlling stocks and cash. It includes an analysis of Saba Hotel's trial balance, evaluation of financial statements, and the process of budgetary controls, including variance analysis. Furthermore, the report covers ratio analysis, future management strategies, cost categorization, contribution margin calculations, and short-term decision-making based on profit and loss potentials and business risks, providing a holistic view of financial operations in the hospitality sector.

FINANCE IN

HOSPITALITY INDUSTRY

HOSPITALITY INDUSTRY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of funding available for business and services industry..........................................1

1.2 Generation of income for businesses and services industry..................................................2

TASK 2............................................................................................................................................3

2.1 Elements of cost, gross profit percentage and selling prices for goods and services............3

2.2 Methods of controlling stocks and cash ..............................................................................4

TASK 3............................................................................................................................................4

3.1 Source and structure of the trial balance of Saba hotel London...........................................4

3.2 Evaluation of financial statements........................................................................................5

3.3 Process and purpose of budgetary controls...........................................................................7

3.4 Variance analysis by comparing budgeted and actual figures..............................................8

TASK 4 ...........................................................................................................................................8

4.1: Calculation and analysis of ratios........................................................................................8

4.2 Appropriate future management strategies ..........................................................................9

TASK 5..........................................................................................................................................10

5.1: Categorisation of costs.......................................................................................................10

5.2: Calculation of contribution per product and analysis of cost/ profit / volume relationship:

...................................................................................................................................................10

5.3 short term decision based upon profit and loss potentials and risk in business operations 11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of funding available for business and services industry..........................................1

1.2 Generation of income for businesses and services industry..................................................2

TASK 2............................................................................................................................................3

2.1 Elements of cost, gross profit percentage and selling prices for goods and services............3

2.2 Methods of controlling stocks and cash ..............................................................................4

TASK 3............................................................................................................................................4

3.1 Source and structure of the trial balance of Saba hotel London...........................................4

3.2 Evaluation of financial statements........................................................................................5

3.3 Process and purpose of budgetary controls...........................................................................7

3.4 Variance analysis by comparing budgeted and actual figures..............................................8

TASK 4 ...........................................................................................................................................8

4.1: Calculation and analysis of ratios........................................................................................8

4.2 Appropriate future management strategies ..........................................................................9

TASK 5..........................................................................................................................................10

5.1: Categorisation of costs.......................................................................................................10

5.2: Calculation of contribution per product and analysis of cost/ profit / volume relationship:

...................................................................................................................................................10

5.3 short term decision based upon profit and loss potentials and risk in business operations 11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Finance is the only element which helps to execute business operations and management

in effective and professional manner. Proper management of financial resources is the only key

factor to attain organisations aim and objective in desired timeline. Finance is also becoming the

essential factor in organisational context to explore the hospitality sector. This report defines the

scope of finance in hospitality industry. Sources of funding available for business, contribution

ranges and income generations explained in this context with briefly. Methods of controlling

stock and the prices of products with cost and gross profit analysis illustrated in organisational

context. Budgetary control and the trial balance analysis done in effective manner.( Harris, 2010)

Cost concept as fixed cost, variable cost, semi variable cost and variable cost aspects are

also defined in this report. Calculation of contribution per unit, short term management decision

and strategic planning also defined in this context. Saba Hotel is the give organisation to analyse

the subject of finance in hospitality.

TASK 1

1.1 Sources of funding available for business and services industry

Every business or services industry requires finance in order to initiate and perform

business operations efficiently and effectively. There are various sources from where the

companies can consider when they are looking to finance for starting up businesses. These are

discussed as under:

Equity financing: Financing through equity means sharing part of the company's

ownership for this purpose of investing funds in the business. The equity investment in

companies allows the investor a stake of share in earnings of the company. The equity of

company can be issued in two ways, common equity and preferred equity. The preferred

stockholders of the company have a preference over the common stockholders, the preference

shareholders of the company receive a pre-determined rate of dividend, which is given to them

before the common shareholders.( Legrand, Chen, and Sloan 2013)

Personal savings: The first source from where the owner looks for financing the business

is his own personal funds that he has saved. Personal sources from where the business person can

include are shares in profits, retirement funds, real estate equity loans and insurance policies.

Venture capital: This is the type of source of capital which is arises from the companies

or individuals who invests in young and privately held start ups. These ventures provide funds

1

Finance is the only element which helps to execute business operations and management

in effective and professional manner. Proper management of financial resources is the only key

factor to attain organisations aim and objective in desired timeline. Finance is also becoming the

essential factor in organisational context to explore the hospitality sector. This report defines the

scope of finance in hospitality industry. Sources of funding available for business, contribution

ranges and income generations explained in this context with briefly. Methods of controlling

stock and the prices of products with cost and gross profit analysis illustrated in organisational

context. Budgetary control and the trial balance analysis done in effective manner.( Harris, 2010)

Cost concept as fixed cost, variable cost, semi variable cost and variable cost aspects are

also defined in this report. Calculation of contribution per unit, short term management decision

and strategic planning also defined in this context. Saba Hotel is the give organisation to analyse

the subject of finance in hospitality.

TASK 1

1.1 Sources of funding available for business and services industry

Every business or services industry requires finance in order to initiate and perform

business operations efficiently and effectively. There are various sources from where the

companies can consider when they are looking to finance for starting up businesses. These are

discussed as under:

Equity financing: Financing through equity means sharing part of the company's

ownership for this purpose of investing funds in the business. The equity investment in

companies allows the investor a stake of share in earnings of the company. The equity of

company can be issued in two ways, common equity and preferred equity. The preferred

stockholders of the company have a preference over the common stockholders, the preference

shareholders of the company receive a pre-determined rate of dividend, which is given to them

before the common shareholders.( Legrand, Chen, and Sloan 2013)

Personal savings: The first source from where the owner looks for financing the business

is his own personal funds that he has saved. Personal sources from where the business person can

include are shares in profits, retirement funds, real estate equity loans and insurance policies.

Venture capital: This is the type of source of capital which is arises from the companies

or individuals who invests in young and privately held start ups. These ventures provide funds

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for a large stake of ownership in the profits of the company. These ventures capital firms

generally do not provide financing to the company in the initial phase, they invest in those

companies who already have equity funding and have a proven track record and are profitable.

Debt financing: Financing the funds by debt includes borrowing from the creditors with the

promise of repayment at a pre-specified date , the principle amount plus the interest. The debt

financing is cheaper and more suitable when the companies have fixed source of income to pay

regular interest payments. Debt financing can be obtained through bank loans, relatives, financial

institutions and bonds.( Jang, and Park, 2011)

11 Debentures: The companies issues debentures to raise the capital in the company. These

are debt instruments on which the company is required to pay a fixed interest and these

papers are issued to general public just like the equity but the debenture holders are the

creditors of the company and not owners.

11 Bank loan: This is the most common kind of debt financing that is used by many

companies , but the only drawback of this kind of financing is that they require the

collateral or solid business plan on which the banks can trust and issue the loan.

11 Credit purchases: This is very essential type of credit that every company should take in

order improve the working capital position of the company. In this system the raw

material is purchased by the company on a credit periods of particular period and the cash

is paid after the completion of that period which helps in the retention of cash in the

company.

1.2 Generation of income for businesses and services industry

The hospitality businesses like Saba Hotel London generate income from various

operations in their hotel, these are discussed below:

Sales: The sales of the Saba hotel London includes services provided by them such as

providing rooms to guest, food and beverages sales, and other supportive services that are

provided by the business in order to generate income from these.( Zhang, Joglekar, and Verma,

2012 )

Commission income: The commissions are received from the third parties which

includes suppliers that provide goods to the organisation.

Sponsorship income: This income is received by the hotels for promoting and displaying

the names of other organisation in their hotel premises or parties conducted by the hotel.

2

generally do not provide financing to the company in the initial phase, they invest in those

companies who already have equity funding and have a proven track record and are profitable.

Debt financing: Financing the funds by debt includes borrowing from the creditors with the

promise of repayment at a pre-specified date , the principle amount plus the interest. The debt

financing is cheaper and more suitable when the companies have fixed source of income to pay

regular interest payments. Debt financing can be obtained through bank loans, relatives, financial

institutions and bonds.( Jang, and Park, 2011)

11 Debentures: The companies issues debentures to raise the capital in the company. These

are debt instruments on which the company is required to pay a fixed interest and these

papers are issued to general public just like the equity but the debenture holders are the

creditors of the company and not owners.

11 Bank loan: This is the most common kind of debt financing that is used by many

companies , but the only drawback of this kind of financing is that they require the

collateral or solid business plan on which the banks can trust and issue the loan.

11 Credit purchases: This is very essential type of credit that every company should take in

order improve the working capital position of the company. In this system the raw

material is purchased by the company on a credit periods of particular period and the cash

is paid after the completion of that period which helps in the retention of cash in the

company.

1.2 Generation of income for businesses and services industry

The hospitality businesses like Saba Hotel London generate income from various

operations in their hotel, these are discussed below:

Sales: The sales of the Saba hotel London includes services provided by them such as

providing rooms to guest, food and beverages sales, and other supportive services that are

provided by the business in order to generate income from these.( Zhang, Joglekar, and Verma,

2012 )

Commission income: The commissions are received from the third parties which

includes suppliers that provide goods to the organisation.

Sponsorship income: This income is received by the hotels for promoting and displaying

the names of other organisation in their hotel premises or parties conducted by the hotel.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Grants: Grants are received from the government organisations other government

authorities to hotels for conducting various programs.

Sub- letting: This is the income that is generated when the hotels provide space to the

various parties for organising exhibitions, fancy items shops, jewellery shops in the premises .(

Lopes, 2016)

TASK 2

2.1 Elements of cost, gross profit percentage and selling prices for goods and services

Cost Element: In the hospitality industries such as Saba hotel London there are various

cost elements that are taken into consideration , these are as below:

Direct material: This is the cost component that is related to the prices of final products

that are purchased by the hotels in order to provide further products and services.

Examples of these products are Glassware, Cutleries, linen, silverware.

Consumables: Consumables are the main components of cost that is incurred in these

industries like Saba hotel London. The consumables are required in the food and

beverage department of the hotel and these are further processed to provide final

products.

Labour: This is the cost related to the manpower that is employed in the hotels for

undertaking various operations in order to provide final goods and services to guests.

Example of this is salary paid to waiters, chefs and front office staff etc.

Selling price and Gross profit margin:

Pricing in tourism: Selling prices are decided in the tourism industry according to the

seasons. During the peak seasons pricing are prepared by adding a higher markup in the

operating cost as selling price and in off season the pricing are reduced by lowering that mark up

and offering discounts.( Millar, Mao, and Moreo, 2010)

Absorption pricing: In this pricing variable costs are calculated first and then the fixed

costs are absorbed in the per unit cost. And then at the end the mark up is added in the total cost

to determine the selling price in order to increase profitability.

Contribution pricing method: In this pricing strategy only the variable overheads are

considered in determining the selling price of the products. The variable cost is deducted from

selling price in order to come at gross profit.

3

authorities to hotels for conducting various programs.

Sub- letting: This is the income that is generated when the hotels provide space to the

various parties for organising exhibitions, fancy items shops, jewellery shops in the premises .(

Lopes, 2016)

TASK 2

2.1 Elements of cost, gross profit percentage and selling prices for goods and services

Cost Element: In the hospitality industries such as Saba hotel London there are various

cost elements that are taken into consideration , these are as below:

Direct material: This is the cost component that is related to the prices of final products

that are purchased by the hotels in order to provide further products and services.

Examples of these products are Glassware, Cutleries, linen, silverware.

Consumables: Consumables are the main components of cost that is incurred in these

industries like Saba hotel London. The consumables are required in the food and

beverage department of the hotel and these are further processed to provide final

products.

Labour: This is the cost related to the manpower that is employed in the hotels for

undertaking various operations in order to provide final goods and services to guests.

Example of this is salary paid to waiters, chefs and front office staff etc.

Selling price and Gross profit margin:

Pricing in tourism: Selling prices are decided in the tourism industry according to the

seasons. During the peak seasons pricing are prepared by adding a higher markup in the

operating cost as selling price and in off season the pricing are reduced by lowering that mark up

and offering discounts.( Millar, Mao, and Moreo, 2010)

Absorption pricing: In this pricing variable costs are calculated first and then the fixed

costs are absorbed in the per unit cost. And then at the end the mark up is added in the total cost

to determine the selling price in order to increase profitability.

Contribution pricing method: In this pricing strategy only the variable overheads are

considered in determining the selling price of the products. The variable cost is deducted from

selling price in order to come at gross profit.

3

2.2 Methods of controlling stocks and cash

Stock control: If the company are able to control stocks smoothly then it will lead to

efficient operations in the hotels. There are various methods that are recommended in the

hospitality industry which are discussed below:

Calculating economic order quantity and re- order quantity.

They should ensure that unnecessary goods are not purchased.

Formulate an effective system of inventory management.(Liu, and Pennington-Gray,

2015 )

The hospitality industries generally purchases products that are perishable in nature and

thus they should adopt FIFO system of inventory management.

Reporting the inventory in the financial accounts of the hotel.

Cash control:

Maintaining a sufficient cash balance is important for carrying smooth operations in the

industry. Saba hotel London is using following cash control systems:

Implementing dual control process over the cash

It is necessary to authorise two person in the handling and verification of cash to avoid

embezzlements and manipulations.

Identifications of reasons for the differences in cash books figures and bank statements

and taking proper actions if uncertainty is found.

TASK 3

3.1 Source and structure of the trial balance of Saba hotel London

The sources that are considered in the trial balance of the company include general

ledger, sales ledger and purchase ledger of the company. The trial balance of the company

includes various accounts such as personal account , real account and nominal accounts. The

structure of trial balance is explained as under:

Current assets: Cash / Bank/ marketable securities/ debtors

Fixed assets & contra assets: Machinery/ Building/ accumulated depreciation.

Current Liability: Bills payables.

Long term liability: Debentures/ bonds / bank loans (long-term)

Owner's capital: Equity share capital/ retained earnings

4

Stock control: If the company are able to control stocks smoothly then it will lead to

efficient operations in the hotels. There are various methods that are recommended in the

hospitality industry which are discussed below:

Calculating economic order quantity and re- order quantity.

They should ensure that unnecessary goods are not purchased.

Formulate an effective system of inventory management.(Liu, and Pennington-Gray,

2015 )

The hospitality industries generally purchases products that are perishable in nature and

thus they should adopt FIFO system of inventory management.

Reporting the inventory in the financial accounts of the hotel.

Cash control:

Maintaining a sufficient cash balance is important for carrying smooth operations in the

industry. Saba hotel London is using following cash control systems:

Implementing dual control process over the cash

It is necessary to authorise two person in the handling and verification of cash to avoid

embezzlements and manipulations.

Identifications of reasons for the differences in cash books figures and bank statements

and taking proper actions if uncertainty is found.

TASK 3

3.1 Source and structure of the trial balance of Saba hotel London

The sources that are considered in the trial balance of the company include general

ledger, sales ledger and purchase ledger of the company. The trial balance of the company

includes various accounts such as personal account , real account and nominal accounts. The

structure of trial balance is explained as under:

Current assets: Cash / Bank/ marketable securities/ debtors

Fixed assets & contra assets: Machinery/ Building/ accumulated depreciation.

Current Liability: Bills payables.

Long term liability: Debentures/ bonds / bank loans (long-term)

Owner's capital: Equity share capital/ retained earnings

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

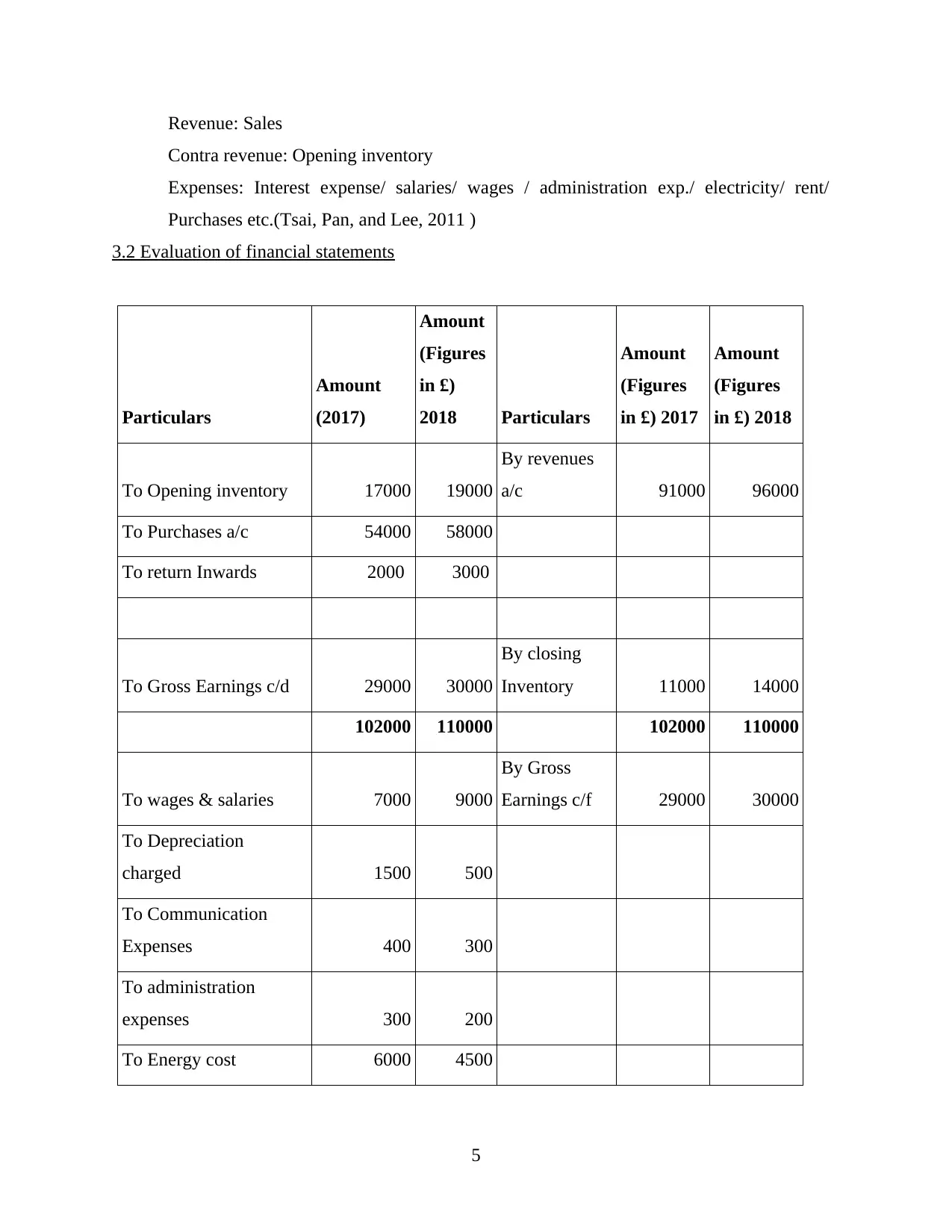

Revenue: Sales

Contra revenue: Opening inventory

Expenses: Interest expense/ salaries/ wages / administration exp./ electricity/ rent/

Purchases etc.(Tsai, Pan, and Lee, 2011 )

3.2 Evaluation of financial statements

Particulars

Amount

(2017)

Amount

(Figures

in £)

2018 Particulars

Amount

(Figures

in £) 2017

Amount

(Figures

in £) 2018

To Opening inventory 17000 19000

By revenues

a/c 91000 96000

To Purchases a/c 54000 58000

To return Inwards 2000 3000

To Gross Earnings c/d 29000 30000

By closing

Inventory 11000 14000

102000 110000 102000 110000

To wages & salaries 7000 9000

By Gross

Earnings c/f 29000 30000

To Depreciation

charged 1500 500

To Communication

Expenses 400 300

To administration

expenses 300 200

To Energy cost 6000 4500

5

Contra revenue: Opening inventory

Expenses: Interest expense/ salaries/ wages / administration exp./ electricity/ rent/

Purchases etc.(Tsai, Pan, and Lee, 2011 )

3.2 Evaluation of financial statements

Particulars

Amount

(2017)

Amount

(Figures

in £)

2018 Particulars

Amount

(Figures

in £) 2017

Amount

(Figures

in £) 2018

To Opening inventory 17000 19000

By revenues

a/c 91000 96000

To Purchases a/c 54000 58000

To return Inwards 2000 3000

To Gross Earnings c/d 29000 30000

By closing

Inventory 11000 14000

102000 110000 102000 110000

To wages & salaries 7000 9000

By Gross

Earnings c/f 29000 30000

To Depreciation

charged 1500 500

To Communication

Expenses 400 300

To administration

expenses 300 200

To Energy cost 6000 4500

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

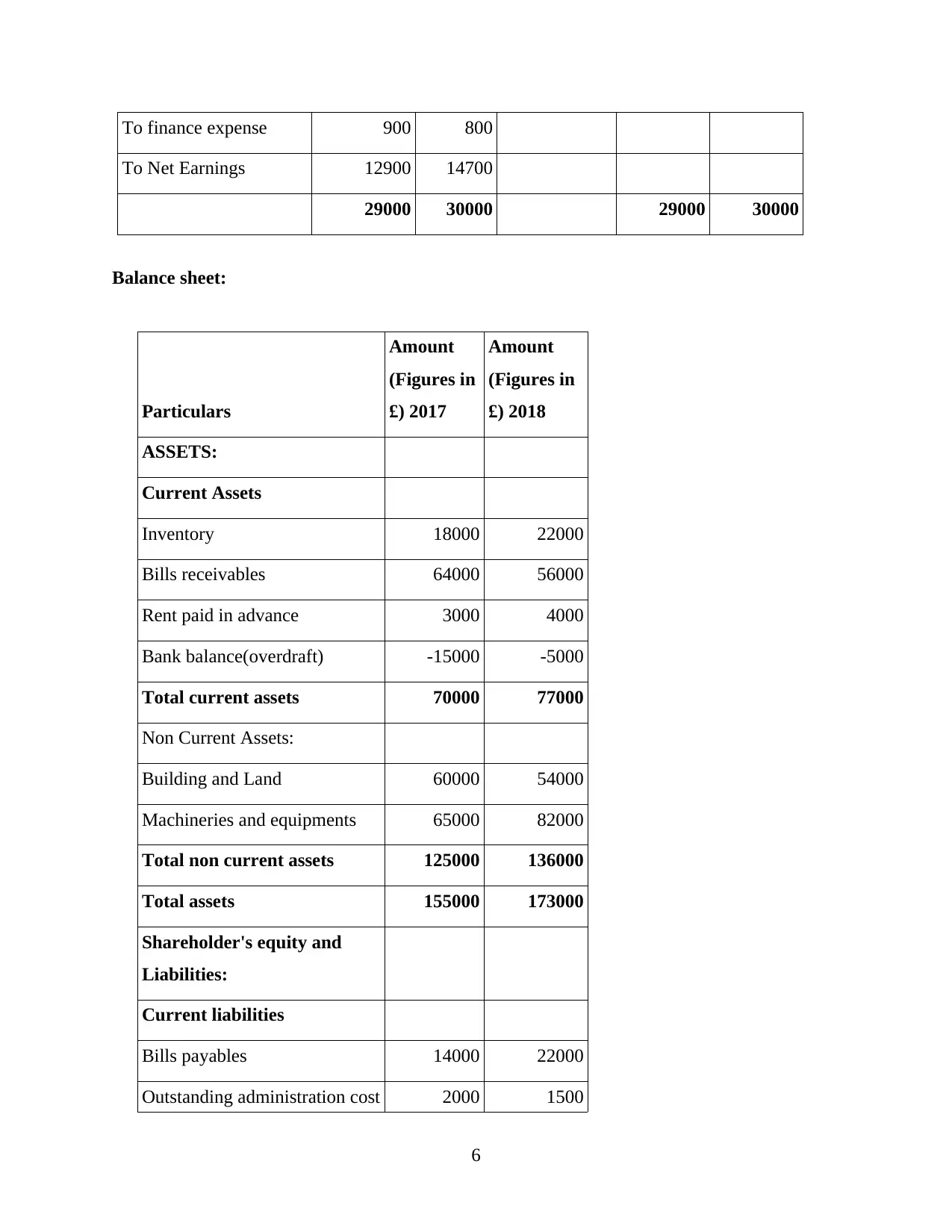

To finance expense 900 800

To Net Earnings 12900 14700

29000 30000 29000 30000

Balance sheet:

Particulars

Amount

(Figures in

£) 2017

Amount

(Figures in

£) 2018

ASSETS:

Current Assets

Inventory 18000 22000

Bills receivables 64000 56000

Rent paid in advance 3000 4000

Bank balance(overdraft) -15000 -5000

Total current assets 70000 77000

Non Current Assets:

Building and Land 60000 54000

Machineries and equipments 65000 82000

Total non current assets 125000 136000

Total assets 155000 173000

Shareholder's equity and

Liabilities:

Current liabilities

Bills payables 14000 22000

Outstanding administration cost 2000 1500

6

To Net Earnings 12900 14700

29000 30000 29000 30000

Balance sheet:

Particulars

Amount

(Figures in

£) 2017

Amount

(Figures in

£) 2018

ASSETS:

Current Assets

Inventory 18000 22000

Bills receivables 64000 56000

Rent paid in advance 3000 4000

Bank balance(overdraft) -15000 -5000

Total current assets 70000 77000

Non Current Assets:

Building and Land 60000 54000

Machineries and equipments 65000 82000

Total non current assets 125000 136000

Total assets 155000 173000

Shareholder's equity and

Liabilities:

Current liabilities

Bills payables 14000 22000

Outstanding administration cost 2000 1500

6

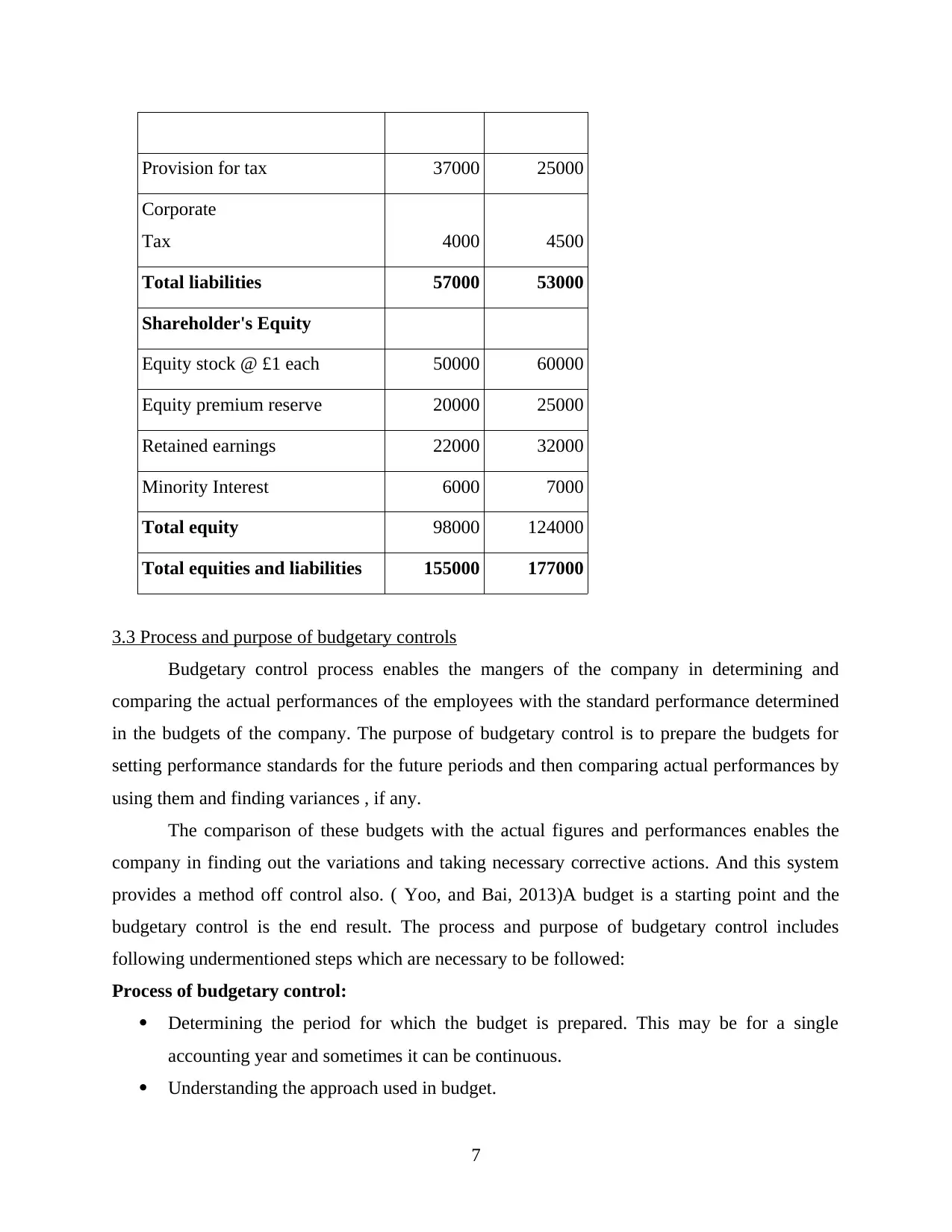

Provision for tax 37000 25000

Corporate

Tax 4000 4500

Total liabilities 57000 53000

Shareholder's Equity

Equity stock @ £1 each 50000 60000

Equity premium reserve 20000 25000

Retained earnings 22000 32000

Minority Interest 6000 7000

Total equity 98000 124000

Total equities and liabilities 155000 177000

3.3 Process and purpose of budgetary controls

Budgetary control process enables the mangers of the company in determining and

comparing the actual performances of the employees with the standard performance determined

in the budgets of the company. The purpose of budgetary control is to prepare the budgets for

setting performance standards for the future periods and then comparing actual performances by

using them and finding variances , if any.

The comparison of these budgets with the actual figures and performances enables the

company in finding out the variations and taking necessary corrective actions. And this system

provides a method off control also. ( Yoo, and Bai, 2013)A budget is a starting point and the

budgetary control is the end result. The process and purpose of budgetary control includes

following undermentioned steps which are necessary to be followed:

Process of budgetary control:

Determining the period for which the budget is prepared. This may be for a single

accounting year and sometimes it can be continuous.

Understanding the approach used in budget.

7

Corporate

Tax 4000 4500

Total liabilities 57000 53000

Shareholder's Equity

Equity stock @ £1 each 50000 60000

Equity premium reserve 20000 25000

Retained earnings 22000 32000

Minority Interest 6000 7000

Total equity 98000 124000

Total equities and liabilities 155000 177000

3.3 Process and purpose of budgetary controls

Budgetary control process enables the mangers of the company in determining and

comparing the actual performances of the employees with the standard performance determined

in the budgets of the company. The purpose of budgetary control is to prepare the budgets for

setting performance standards for the future periods and then comparing actual performances by

using them and finding variances , if any.

The comparison of these budgets with the actual figures and performances enables the

company in finding out the variations and taking necessary corrective actions. And this system

provides a method off control also. ( Yoo, and Bai, 2013)A budget is a starting point and the

budgetary control is the end result. The process and purpose of budgetary control includes

following undermentioned steps which are necessary to be followed:

Process of budgetary control:

Determining the period for which the budget is prepared. This may be for a single

accounting year and sometimes it can be continuous.

Understanding the approach used in budget.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Choosing a suitable method for using a budget. Such as zero based budgeting.

Proper implementation of budgets. This should be done after preparing and approving the

budget.

Measurement of performance of actual performances during budgetary period.

Comparing actual performance with the standard performance and finding variances, if

any.

Taking proper corrective actions, such that the actual performance come closer to

standard performance.

Purpose of budgetary control:

It assists in achieving organisational objectives as determined earlier.

Delegation of work responsibilities to the employees and leaders.

Optimum utilisation of resources.

Assists in taking corrective actions.

Can be used as future policy and as performance measurement tool.

3.4 Variance analysis by comparing budgeted and actual figures

Computation of Raw material variances:

Total variance of raw material = Standard cost – Actual cost

= (20000* 10 $) - 1,94,600

= $ 5,400 (F)

Raw Material price variance = Quantity used (Standard price- Actual price)

= (22,400 * 10$) - 1,94,600

= 29,400 (F)

Raw material usage variance = Standard price(Standard usage – actual usage)

= $10 ((10 * 2000) – 22,400)

= 24000 (A)

Analysis of variances

This has been observed that total raw material variance has come out to be 5400

favourable from the budgeted figures , which implies that actual material cost is less than the

standard cost and this means that it is under control. Further, the raw material price variance is

also 29400 favourable from the budgeted figures, which also shows that the actual price is less

8

Proper implementation of budgets. This should be done after preparing and approving the

budget.

Measurement of performance of actual performances during budgetary period.

Comparing actual performance with the standard performance and finding variances, if

any.

Taking proper corrective actions, such that the actual performance come closer to

standard performance.

Purpose of budgetary control:

It assists in achieving organisational objectives as determined earlier.

Delegation of work responsibilities to the employees and leaders.

Optimum utilisation of resources.

Assists in taking corrective actions.

Can be used as future policy and as performance measurement tool.

3.4 Variance analysis by comparing budgeted and actual figures

Computation of Raw material variances:

Total variance of raw material = Standard cost – Actual cost

= (20000* 10 $) - 1,94,600

= $ 5,400 (F)

Raw Material price variance = Quantity used (Standard price- Actual price)

= (22,400 * 10$) - 1,94,600

= 29,400 (F)

Raw material usage variance = Standard price(Standard usage – actual usage)

= $10 ((10 * 2000) – 22,400)

= 24000 (A)

Analysis of variances

This has been observed that total raw material variance has come out to be 5400

favourable from the budgeted figures , which implies that actual material cost is less than the

standard cost and this means that it is under control. Further, the raw material price variance is

also 29400 favourable from the budgeted figures, which also shows that the actual price is less

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

than standard. Although the raw material variance is 24000 adverse from the budgeted figures.

And this indicates that RM usage are not under control.

TASK 4

4.1: Calculation and analysis of ratios

Liquidity ratios: These ratios tells the company's ability to repay its short term

obligations. The major ratios that are calculated under this head are current ratio and liquid ratio.

The current ratio of the Saba hotel London has improved since last year which was 1.22 in year

2017 and 1.45 in 2018. the liquid ratio of the company has also improves in comparison to

previous year which was 0.91 in the year 2017 and 1.03 in the year 2018.( Sisson, and Adams,

2013 )

Efficiency ratios: This ratio calculates and analyse how efficiently the company is

analysing its resources , the ratios which determines the efficiency of the company are inventory

turnover ratio, accounts receivable ratio and accounts payable ratio. In the above example the

accounts receivable turnover ratio has increased in the year 2018 as compared to 2017 from 1.42

to 1.71 times which is good indication. And the accounts payable ratio has declined in the year

2018 which also indication of good efficiency , it is recorded as 3.85 in 2017 and 2.63 in 2018.

Profitability ratios: These ratios indicates the profitability of the company during the

financial year. The ratios which are calculated to determine the profitability of the company is

gross profit ratio and net profit ratio. The company's profitability have decreased in the current

year by seeing the decrease in the gross profit ratio from 31.86%(2017) to 31.25%(2018). but the

net profit of the company have substantially improves as compared to previous year the N.P.

Ratio for the years are 14.17%(2017) and 15.31%(2018)

Financial ratios: These ratios include earning per share of the company has declined a

little bit in the current year which was 0.25 in the year 2017 and 0.24 in the year 2018.(

Richardson, and Thomas, 2012 )

4.2 Appropriate future management strategies

The strategies which should be adapted by the management of the company in order to

eliminate the discrepancies identified are as under:

9

And this indicates that RM usage are not under control.

TASK 4

4.1: Calculation and analysis of ratios

Liquidity ratios: These ratios tells the company's ability to repay its short term

obligations. The major ratios that are calculated under this head are current ratio and liquid ratio.

The current ratio of the Saba hotel London has improved since last year which was 1.22 in year

2017 and 1.45 in 2018. the liquid ratio of the company has also improves in comparison to

previous year which was 0.91 in the year 2017 and 1.03 in the year 2018.( Sisson, and Adams,

2013 )

Efficiency ratios: This ratio calculates and analyse how efficiently the company is

analysing its resources , the ratios which determines the efficiency of the company are inventory

turnover ratio, accounts receivable ratio and accounts payable ratio. In the above example the

accounts receivable turnover ratio has increased in the year 2018 as compared to 2017 from 1.42

to 1.71 times which is good indication. And the accounts payable ratio has declined in the year

2018 which also indication of good efficiency , it is recorded as 3.85 in 2017 and 2.63 in 2018.

Profitability ratios: These ratios indicates the profitability of the company during the

financial year. The ratios which are calculated to determine the profitability of the company is

gross profit ratio and net profit ratio. The company's profitability have decreased in the current

year by seeing the decrease in the gross profit ratio from 31.86%(2017) to 31.25%(2018). but the

net profit of the company have substantially improves as compared to previous year the N.P.

Ratio for the years are 14.17%(2017) and 15.31%(2018)

Financial ratios: These ratios include earning per share of the company has declined a

little bit in the current year which was 0.25 in the year 2017 and 0.24 in the year 2018.(

Richardson, and Thomas, 2012 )

4.2 Appropriate future management strategies

The strategies which should be adapted by the management of the company in order to

eliminate the discrepancies identified are as under:

9

The company should reduce the selling prices of the products or services and increase the

volume of sales in order to increase the overall earnings of the company.

Unnecessary utilisation of the funds on the inventory should be reduced. The LIFO

inventory management system should be implemented in order to minimise the handling

cost of the inventory.

The company should undertake the important steps in order to decrease the regular

expenditure.

The company must focus on obtaining longer credit periods from the suppliers and ask

lower credit period from the customers to improve cash conversion cycle of the company.

Formulating a systematic cash flow management in the company.

Implementing innovative procedures to attract new customers in the company to increase

the revenues while providing discounts and promotions.

The company should focus on utilising the fixed assets of the company in an effective

and efficient manner so that a good earnings can be generated from it.

TASK 5

5.1: Categorisation of costs

The cost that occurs in the organisation are categorised into three broad categories

namely fixed cost, variable cost and semi variable cost. These are discussed as under:

Fixed cost: These are those costs of the company which remains unchanged during the

different accounting years. The fixed cost of productions also does not increase if the company

increases its production on smaller scale. The fixed cost of productions include Rent expenses,

depreciation expenses etc. For Example the fixed cost of production is 250000$( Joshua, and

Mohammed, 2013 )

Variable cost : This is the cost of company which changes from time to time and it also

changes when the company increases or decreases the production. When the company increases

the production the variable expenditures such as direct labour , direct material, etc. also increases

and whenever the production deceases these costs also decreases. The example of variable cost is

– the price of a unit of food is 15$ per unit.

Semi variable cost: The semi variable cost is that cost which includes some part of the

variable component and some part of fixed component for a given expenditure. The semi

variable cost remains fixed to some extent and becomes variable till some aspect. The example

10

volume of sales in order to increase the overall earnings of the company.

Unnecessary utilisation of the funds on the inventory should be reduced. The LIFO

inventory management system should be implemented in order to minimise the handling

cost of the inventory.

The company should undertake the important steps in order to decrease the regular

expenditure.

The company must focus on obtaining longer credit periods from the suppliers and ask

lower credit period from the customers to improve cash conversion cycle of the company.

Formulating a systematic cash flow management in the company.

Implementing innovative procedures to attract new customers in the company to increase

the revenues while providing discounts and promotions.

The company should focus on utilising the fixed assets of the company in an effective

and efficient manner so that a good earnings can be generated from it.

TASK 5

5.1: Categorisation of costs

The cost that occurs in the organisation are categorised into three broad categories

namely fixed cost, variable cost and semi variable cost. These are discussed as under:

Fixed cost: These are those costs of the company which remains unchanged during the

different accounting years. The fixed cost of productions also does not increase if the company

increases its production on smaller scale. The fixed cost of productions include Rent expenses,

depreciation expenses etc. For Example the fixed cost of production is 250000$( Joshua, and

Mohammed, 2013 )

Variable cost : This is the cost of company which changes from time to time and it also

changes when the company increases or decreases the production. When the company increases

the production the variable expenditures such as direct labour , direct material, etc. also increases

and whenever the production deceases these costs also decreases. The example of variable cost is

– the price of a unit of food is 15$ per unit.

Semi variable cost: The semi variable cost is that cost which includes some part of the

variable component and some part of fixed component for a given expenditure. The semi

variable cost remains fixed to some extent and becomes variable till some aspect. The example

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.