Financial Analysis of Hospitality Business: Budget and Variance Report

VerifiedAdded on 2023/06/06

|18

|3501

|154

Report

AI Summary

This report presents a comprehensive financial analysis of a hospitality business, focusing on budget analysis, performance evaluation, and variance reporting. The analysis includes detailed examination of revenue, cost of goods sold, expenses, and profit margins over a two-year period, along with a variance report comparing budgeted and actual figures. It identifies key financial management issues, such as ineffective discount recording, inadequate cash management, and poor debtor management. The report also explores accounting principles like matching principles and probity, and discusses the impact of trade agreements on the hospitality sector. Recommendations are provided to improve financial management practices, including the implementation of an ERP system, improved reporting structures, and employee training to ensure compliance with regulations.

Running head: HOSPITALITY

Hospitality

Name of the Student:

Name of the University:

Author’s Note:

Hospitality

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

HOSPITALITY

Table of Contents

Assessment 1...................................................................................................................................2

Part A...............................................................................................................................................2

Analysis of the Budget.................................................................................................................5

Part B...............................................................................................................................................8

Assessment 2.................................................................................................................................12

Variance Report.........................................................................................................................12

Debtor Analysis.........................................................................................................................12

Issues which Can be Identified..................................................................................................13

Analysis of Variances in Budgets..............................................................................................13

Performance...............................................................................................................................14

Recommendation...........................................................................................................................15

Financial Management Processes in Place....................................................................................15

Reference.......................................................................................................................................17

HOSPITALITY

Table of Contents

Assessment 1...................................................................................................................................2

Part A...............................................................................................................................................2

Analysis of the Budget.................................................................................................................5

Part B...............................................................................................................................................8

Assessment 2.................................................................................................................................12

Variance Report.........................................................................................................................12

Debtor Analysis.........................................................................................................................12

Issues which Can be Identified..................................................................................................13

Analysis of Variances in Budgets..............................................................................................13

Performance...............................................................................................................................14

Recommendation...........................................................................................................................15

Financial Management Processes in Place....................................................................................15

Reference.......................................................................................................................................17

2

HOSPITALITY

Assessment 1

Part A

HOSPITALITY

Assessment 1

Part A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

HOSPITALITY

HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

HOSPITALITY

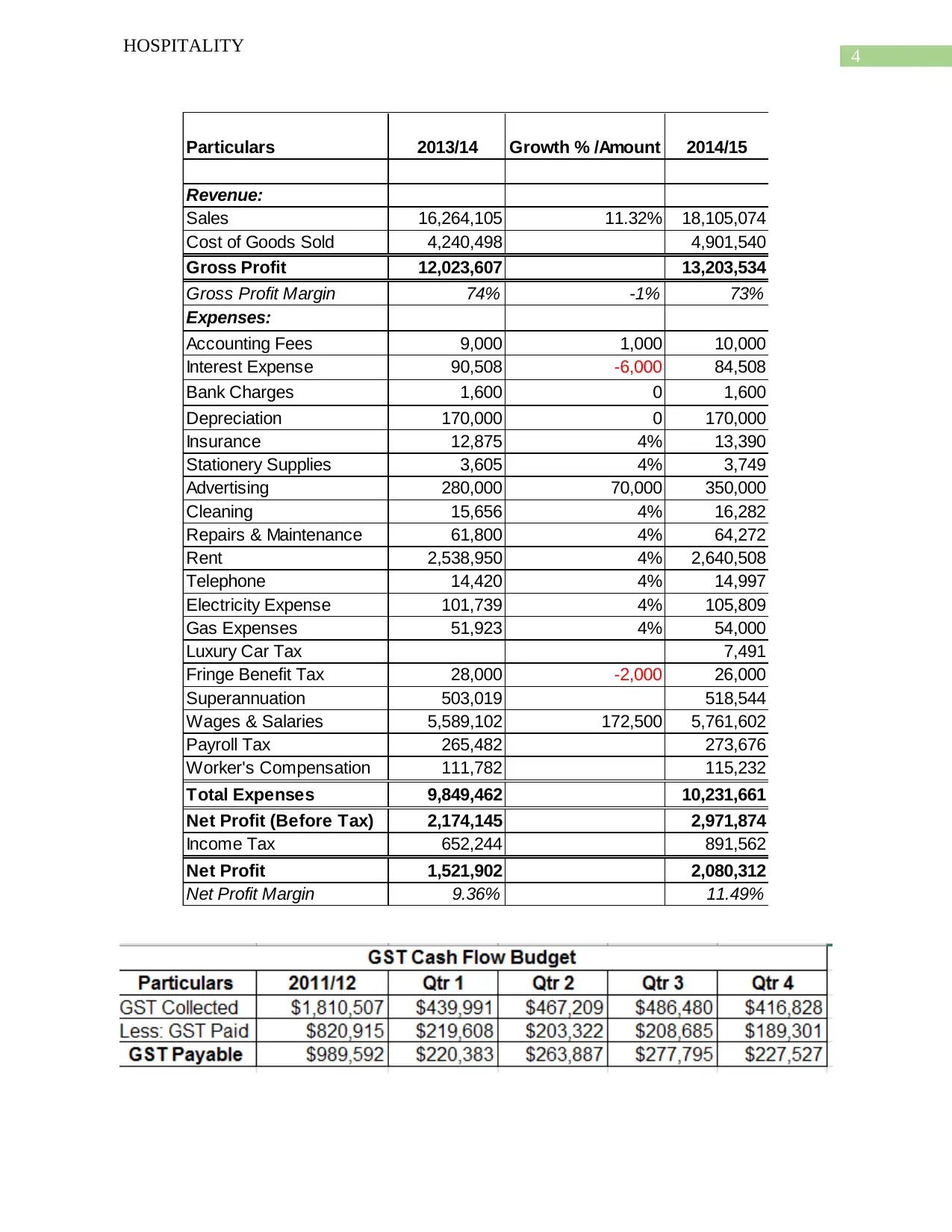

Particulars 2013/14 Growth % /Amount 2014/15

Revenue:

Sales 16,264,105 11.32% 18,105,074

Cost of Goods Sold 4,240,498 4,901,540

Gross Profit 12,023,607 13,203,534

Gross Profit Margin 74% -1% 73%

Expenses:

Accounting Fees 9,000 1,000 10,000

Interest Expense 90,508 -6,000 84,508

Bank Charges 1,600 0 1,600

Depreciation 170,000 0 170,000

Insurance 12,875 4% 13,390

Stationery Supplies 3,605 4% 3,749

Advertising 280,000 70,000 350,000

Cleaning 15,656 4% 16,282

Repairs & Maintenance 61,800 4% 64,272

Rent 2,538,950 4% 2,640,508

Telephone 14,420 4% 14,997

Electricity Expense 101,739 4% 105,809

Gas Expenses 51,923 4% 54,000

Luxury Car Tax 7,491

Fringe Benefit Tax 28,000 -2,000 26,000

Superannuation 503,019 518,544

Wages & Salaries 5,589,102 172,500 5,761,602

Payroll Tax 265,482 273,676

Worker's Compensation 111,782 115,232

Total Expenses 9,849,462 10,231,661

Net Profit (Before Tax) 2,174,145 2,971,874

Income Tax 652,244 891,562

Net Profit 1,521,902 2,080,312

Net Profit Margin 9.36% 11.49%

HOSPITALITY

Particulars 2013/14 Growth % /Amount 2014/15

Revenue:

Sales 16,264,105 11.32% 18,105,074

Cost of Goods Sold 4,240,498 4,901,540

Gross Profit 12,023,607 13,203,534

Gross Profit Margin 74% -1% 73%

Expenses:

Accounting Fees 9,000 1,000 10,000

Interest Expense 90,508 -6,000 84,508

Bank Charges 1,600 0 1,600

Depreciation 170,000 0 170,000

Insurance 12,875 4% 13,390

Stationery Supplies 3,605 4% 3,749

Advertising 280,000 70,000 350,000

Cleaning 15,656 4% 16,282

Repairs & Maintenance 61,800 4% 64,272

Rent 2,538,950 4% 2,640,508

Telephone 14,420 4% 14,997

Electricity Expense 101,739 4% 105,809

Gas Expenses 51,923 4% 54,000

Luxury Car Tax 7,491

Fringe Benefit Tax 28,000 -2,000 26,000

Superannuation 503,019 518,544

Wages & Salaries 5,589,102 172,500 5,761,602

Payroll Tax 265,482 273,676

Worker's Compensation 111,782 115,232

Total Expenses 9,849,462 10,231,661

Net Profit (Before Tax) 2,174,145 2,971,874

Income Tax 652,244 891,562

Net Profit 1,521,902 2,080,312

Net Profit Margin 9.36% 11.49%

5

HOSPITALITY

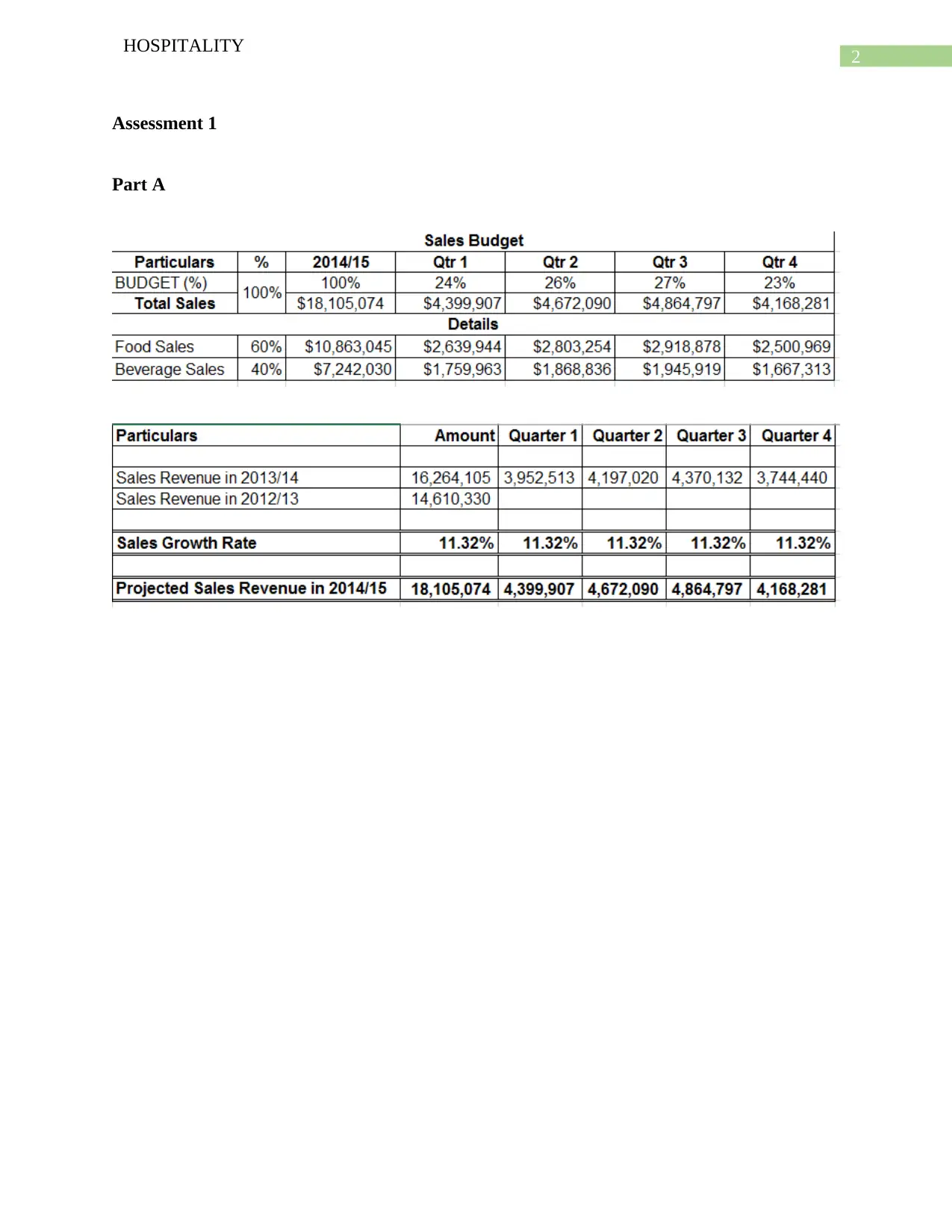

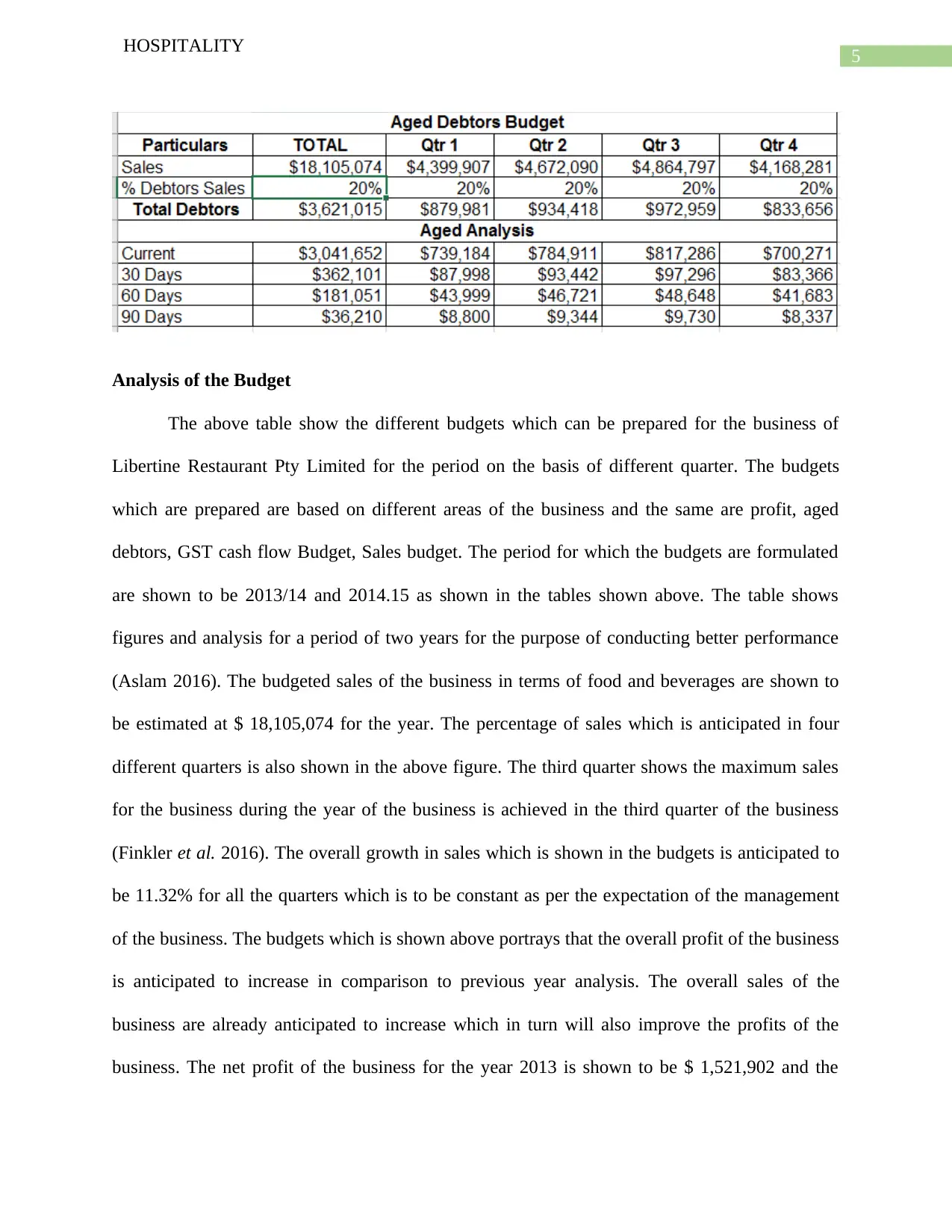

Analysis of the Budget

The above table show the different budgets which can be prepared for the business of

Libertine Restaurant Pty Limited for the period on the basis of different quarter. The budgets

which are prepared are based on different areas of the business and the same are profit, aged

debtors, GST cash flow Budget, Sales budget. The period for which the budgets are formulated

are shown to be 2013/14 and 2014.15 as shown in the tables shown above. The table shows

figures and analysis for a period of two years for the purpose of conducting better performance

(Aslam 2016). The budgeted sales of the business in terms of food and beverages are shown to

be estimated at $ 18,105,074 for the year. The percentage of sales which is anticipated in four

different quarters is also shown in the above figure. The third quarter shows the maximum sales

for the business during the year of the business is achieved in the third quarter of the business

(Finkler et al. 2016). The overall growth in sales which is shown in the budgets is anticipated to

be 11.32% for all the quarters which is to be constant as per the expectation of the management

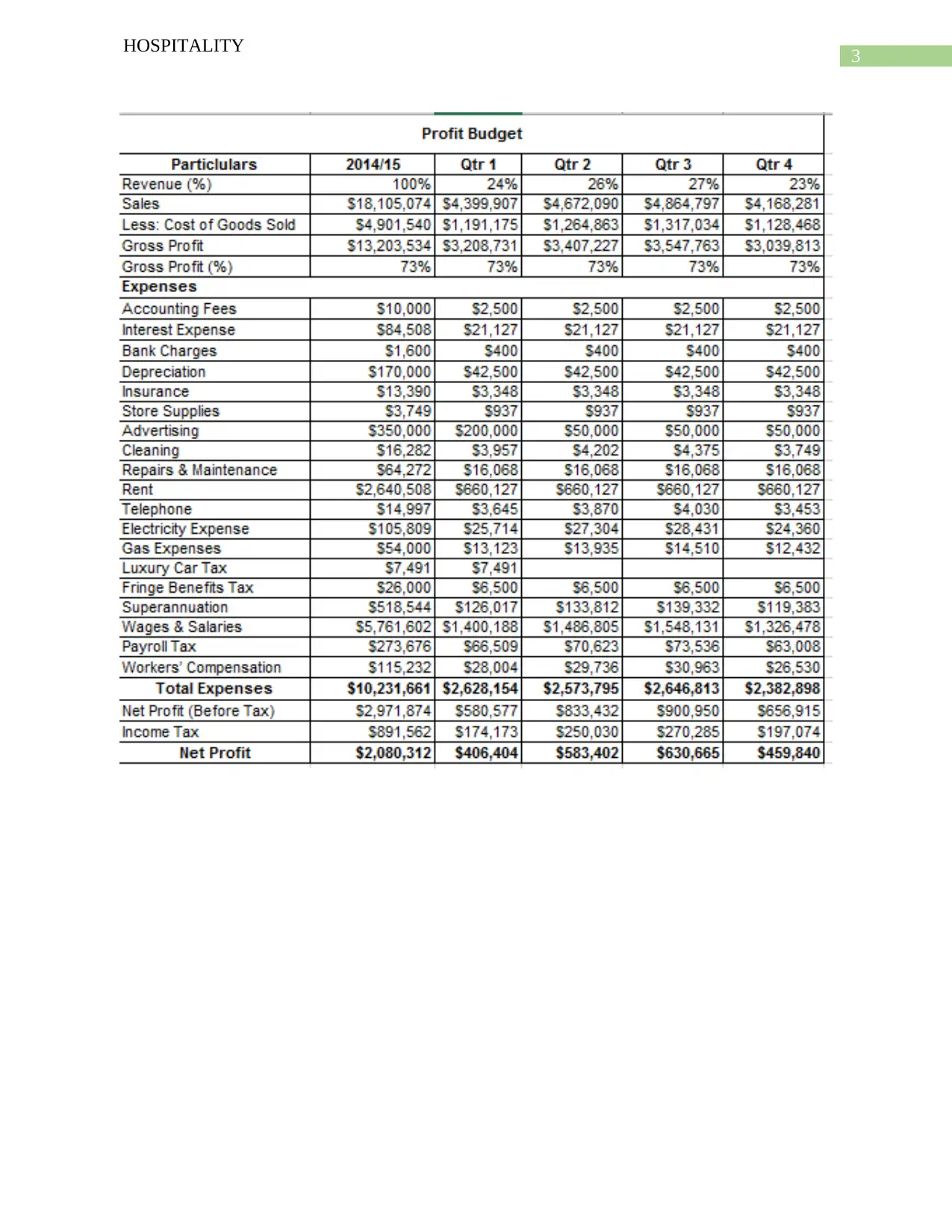

of the business. The budgets which is shown above portrays that the overall profit of the business

is anticipated to increase in comparison to previous year analysis. The overall sales of the

business are already anticipated to increase which in turn will also improve the profits of the

business. The net profit of the business for the year 2013 is shown to be $ 1,521,902 and the

HOSPITALITY

Analysis of the Budget

The above table show the different budgets which can be prepared for the business of

Libertine Restaurant Pty Limited for the period on the basis of different quarter. The budgets

which are prepared are based on different areas of the business and the same are profit, aged

debtors, GST cash flow Budget, Sales budget. The period for which the budgets are formulated

are shown to be 2013/14 and 2014.15 as shown in the tables shown above. The table shows

figures and analysis for a period of two years for the purpose of conducting better performance

(Aslam 2016). The budgeted sales of the business in terms of food and beverages are shown to

be estimated at $ 18,105,074 for the year. The percentage of sales which is anticipated in four

different quarters is also shown in the above figure. The third quarter shows the maximum sales

for the business during the year of the business is achieved in the third quarter of the business

(Finkler et al. 2016). The overall growth in sales which is shown in the budgets is anticipated to

be 11.32% for all the quarters which is to be constant as per the expectation of the management

of the business. The budgets which is shown above portrays that the overall profit of the business

is anticipated to increase in comparison to previous year analysis. The overall sales of the

business are already anticipated to increase which in turn will also improve the profits of the

business. The net profit of the business for the year 2013 is shown to be $ 1,521,902 and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

HOSPITALITY

same is estimated to increase in 2014 as shown in the budget at $ 2,090,312. The net profit

margin of the business shows tremendous improvement if the expectation of the management is

accurate. The management has estimated the expenses of the business which are common to the

business to rise in 2014.

The financial management of the business for the year 2014 shows that the business has

does not have an effective policy. The discounts which are offered to the customers are not

effectively recorded in the books of account of the business. and therefore, the same affect the

recording of the business. The menu of the restaurant is not showing appropriate view of the

discount and prices which are shown for the products which are offered by the business

(Jindrichovska 2013). The cash management of the business is ineffective as the cash balances

are reconciled on a regular basis with the printed cash register prints. The service invoices which

are related to some of the equipment are not linked with the purchase order the business. The

debtor management policy of the business is also inappropriate in nature as the balances of

debtors are not reconciled on a regular basis and sometimes these balances are not reconciled at

all. The following deficiencies in the financial management practices of the business needs to be

improved in order to ensure that the business structure of the business is appropriate (Allen,

Hemming and Potter 2013).

The assumptions which are considered for the purpose of formulating the budget and

included the changes in expectations of the management. The basic assumptions which are

considered is in relation to sales that all the units which are produced by the business are sold.

The quarter sales percentage breakup and also the growths in sales of the business are also taken

on assumption basis. The budgets which are prepared by the management shows expenses and

growth in expenses of the business relating to different quarters shown in the budget.

HOSPITALITY

same is estimated to increase in 2014 as shown in the budget at $ 2,090,312. The net profit

margin of the business shows tremendous improvement if the expectation of the management is

accurate. The management has estimated the expenses of the business which are common to the

business to rise in 2014.

The financial management of the business for the year 2014 shows that the business has

does not have an effective policy. The discounts which are offered to the customers are not

effectively recorded in the books of account of the business. and therefore, the same affect the

recording of the business. The menu of the restaurant is not showing appropriate view of the

discount and prices which are shown for the products which are offered by the business

(Jindrichovska 2013). The cash management of the business is ineffective as the cash balances

are reconciled on a regular basis with the printed cash register prints. The service invoices which

are related to some of the equipment are not linked with the purchase order the business. The

debtor management policy of the business is also inappropriate in nature as the balances of

debtors are not reconciled on a regular basis and sometimes these balances are not reconciled at

all. The following deficiencies in the financial management practices of the business needs to be

improved in order to ensure that the business structure of the business is appropriate (Allen,

Hemming and Potter 2013).

The assumptions which are considered for the purpose of formulating the budget and

included the changes in expectations of the management. The basic assumptions which are

considered is in relation to sales that all the units which are produced by the business are sold.

The quarter sales percentage breakup and also the growths in sales of the business are also taken

on assumption basis. The budgets which are prepared by the management shows expenses and

growth in expenses of the business relating to different quarters shown in the budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

HOSPITALITY

The monitoring and implementation of the budgets are the responsibility of the

management of the business. The management sets the standards which is to be followed by the

employees and the management can also check whether the same is being effectively followed or

not as per the plans of the management.

HOSPITALITY

The monitoring and implementation of the budgets are the responsibility of the

management of the business. The management sets the standards which is to be followed by the

employees and the management can also check whether the same is being effectively followed or

not as per the plans of the management.

8

HOSPITALITY

Part B

As the business is engaged in restaurant business, the management of the company needs

to follow the tax regulations which are applicable on the business in Australia. The company is

liable to pay income taxes which is on the revenues which is generated by the business during

the year. In addition to this, the management also needs to incur GST expenses which are

incurred during the year. In addition to this, the management also needs to incur expenses which

are related to licensing fees and other legal costs of the business.

The management of Libertine Restaurant Pty Ltd needs to comply with the regulations of

Corporation Act 2001. The management needs to follow the provisions of section 111AA and

also the division 2 and division 3 of the act. This is to be followed effectively by the

management in order to ensure that the business complies with the rules and regulations of the

business.

The overall business conditions and the market of the restaurant business is on the growth

and therefore naturally the sales of Libertine Restaurant Pty Ltd is growing and the management

of the company anticipates further growth in the sales of the business. In order to effectively

manage and record the revenue and expenses of the business, the management needs to introduce

a new recording software which can help the business to effective record its sales. As per the

plan of the management, the company can implement ERP system or develop a software which

is suitably tailored for the business of the restaurant. The management can also develop its own

software which will a costly process for the business. However, the management of the company

is of the opinion that ERP system would be able to effectively meet the requirements of the

business by keeping appropriate records of the revenue and expenses of the business. Another

HOSPITALITY

Part B

As the business is engaged in restaurant business, the management of the company needs

to follow the tax regulations which are applicable on the business in Australia. The company is

liable to pay income taxes which is on the revenues which is generated by the business during

the year. In addition to this, the management also needs to incur GST expenses which are

incurred during the year. In addition to this, the management also needs to incur expenses which

are related to licensing fees and other legal costs of the business.

The management of Libertine Restaurant Pty Ltd needs to comply with the regulations of

Corporation Act 2001. The management needs to follow the provisions of section 111AA and

also the division 2 and division 3 of the act. This is to be followed effectively by the

management in order to ensure that the business complies with the rules and regulations of the

business.

The overall business conditions and the market of the restaurant business is on the growth

and therefore naturally the sales of Libertine Restaurant Pty Ltd is growing and the management

of the company anticipates further growth in the sales of the business. In order to effectively

manage and record the revenue and expenses of the business, the management needs to introduce

a new recording software which can help the business to effective record its sales. As per the

plan of the management, the company can implement ERP system or develop a software which

is suitably tailored for the business of the restaurant. The management can also develop its own

software which will a costly process for the business. However, the management of the company

is of the opinion that ERP system would be able to effectively meet the requirements of the

business by keeping appropriate records of the revenue and expenses of the business. Another

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

HOSPITALITY

example of the usefulness of ERP system is that the same can minimum time for process the data

and thereby can effectively help the business in scrutiny of the revenue and sales of the business.

Therefore, the management of the company is considering ERP system for the purpose of

recording the transactions of the business.

Matching Principles in accounting terms refers to the concept which states that the

expenses of the business should be equivalent to the revenues which is earned by the business. In

other words, every expense which the business incurs should be matched with the revenue which

the business earns. The budgets which is to be prepared by the management of the company

should be made considering what expenses the business needs to incur for generating a revenue.

The budget which is prepared by the business considers the anticipated income and expenses of

the business during the period. The principle of account groups states that the budgets should be

prepared considering various items which are shown in the business. These forms an integral part

of the budgets of the business. The budgets should be prepared as per a deadline for achieving a

particular target for the business. The budgets which is prepared by the management are based on

quarters and achievement milestones are set by the management for the purpose of ensuring that

the plans of the business are being implemented.

The principle of probity refers to the application of honesty, decency and principles of

moral values while preparing budgets for the company. The principle basically states that the

budgets should be prepared by following accurate forecasting techniques and approach of the

management should be fair and honest.

The most viable financial quarter for the business of Libertine Restaurant Pty Ltd as per

the anticipation of the management is the third quarter in which the sales of the business is

HOSPITALITY

example of the usefulness of ERP system is that the same can minimum time for process the data

and thereby can effectively help the business in scrutiny of the revenue and sales of the business.

Therefore, the management of the company is considering ERP system for the purpose of

recording the transactions of the business.

Matching Principles in accounting terms refers to the concept which states that the

expenses of the business should be equivalent to the revenues which is earned by the business. In

other words, every expense which the business incurs should be matched with the revenue which

the business earns. The budgets which is to be prepared by the management of the company

should be made considering what expenses the business needs to incur for generating a revenue.

The budget which is prepared by the business considers the anticipated income and expenses of

the business during the period. The principle of account groups states that the budgets should be

prepared considering various items which are shown in the business. These forms an integral part

of the budgets of the business. The budgets should be prepared as per a deadline for achieving a

particular target for the business. The budgets which is prepared by the management are based on

quarters and achievement milestones are set by the management for the purpose of ensuring that

the plans of the business are being implemented.

The principle of probity refers to the application of honesty, decency and principles of

moral values while preparing budgets for the company. The principle basically states that the

budgets should be prepared by following accurate forecasting techniques and approach of the

management should be fair and honest.

The most viable financial quarter for the business of Libertine Restaurant Pty Ltd as per

the anticipation of the management is the third quarter in which the sales of the business is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

HOSPITALITY

anticipated to be maximum in comparison to sales which is achieved by the business in other

quarters. This suggest that the season for the restaurant business is the third quarter where the

demand for the products are maximum as per the expectation of the business.

The management should appropriately segregate the costs of the business on the basis of

direct and indirect costs of the business for the purpose of better presentation of the information

which is shown in the budgets above. The management can also include more costs which the

business incurs but the same are not considered for the purpose of the budget.

The risk management of the business can be done appropriately by establishing a new

control structure in the business. The management can improve the reporting structure of the

company by incorporating a new accounting software which can effectively record all expenses

and losses of the business. In addition to this, the management also needs to properly train the

employees of the business so that they are follow all rules and regulations which are already

established in the business.

The following trade agreements affect the business of hospitality in the following ways

which are discussed below:

1. Bilateral Trade Agreements: These refers to the trade agreements which is established

between the business and another party. This sort of agreement can be set up by the business

with suppliers of resources and other complementary business which can support the

restaurant business.

2. International Commercial Terms: These are pre-defined trade terms which are published

by International Council of Commerce. These can be used by businesses in various foreign

HOSPITALITY

anticipated to be maximum in comparison to sales which is achieved by the business in other

quarters. This suggest that the season for the restaurant business is the third quarter where the

demand for the products are maximum as per the expectation of the business.

The management should appropriately segregate the costs of the business on the basis of

direct and indirect costs of the business for the purpose of better presentation of the information

which is shown in the budgets above. The management can also include more costs which the

business incurs but the same are not considered for the purpose of the budget.

The risk management of the business can be done appropriately by establishing a new

control structure in the business. The management can improve the reporting structure of the

company by incorporating a new accounting software which can effectively record all expenses

and losses of the business. In addition to this, the management also needs to properly train the

employees of the business so that they are follow all rules and regulations which are already

established in the business.

The following trade agreements affect the business of hospitality in the following ways

which are discussed below:

1. Bilateral Trade Agreements: These refers to the trade agreements which is established

between the business and another party. This sort of agreement can be set up by the business

with suppliers of resources and other complementary business which can support the

restaurant business.

2. International Commercial Terms: These are pre-defined trade terms which are published

by International Council of Commerce. These can be used by businesses in various foreign

11

HOSPITALITY

trade transactions. If the restaurant businesses engages in such a trade than the revenue of the

business will receive a boast and the sales o the business might increase.

3. Trade Practice Act: This is a legislation which is in force in Australia which deals with the

trade practices of the business. The legislation promotes fair trade practices and prohibits

anti-competitive practices of a business. The business will be affected by the same and must

adhere to such principles.

4. Warsaw Convention: The Warsaw convention deals with the unification of air carriage

rules which reduces the liability of the air carriage of person or goods. This act is not

applicable to the business of Libertine Restaurant Pty Ltd.

5. World Trade Organization Determination: As per the rules of the WTO which mainly

focuses on achieving fair trade and smooth operation in trade of the business for the year.

The rules will not be applicable to the business as the same is not going to engage in so much

global trade initially.

HOSPITALITY

trade transactions. If the restaurant businesses engages in such a trade than the revenue of the

business will receive a boast and the sales o the business might increase.

3. Trade Practice Act: This is a legislation which is in force in Australia which deals with the

trade practices of the business. The legislation promotes fair trade practices and prohibits

anti-competitive practices of a business. The business will be affected by the same and must

adhere to such principles.

4. Warsaw Convention: The Warsaw convention deals with the unification of air carriage

rules which reduces the liability of the air carriage of person or goods. This act is not

applicable to the business of Libertine Restaurant Pty Ltd.

5. World Trade Organization Determination: As per the rules of the WTO which mainly

focuses on achieving fair trade and smooth operation in trade of the business for the year.

The rules will not be applicable to the business as the same is not going to engage in so much

global trade initially.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.